what businesses ought to know about healthcare reform

TRANSCRIPT

HEALTH CARE REFORM ESSENTIALSImportant details for businesses navigating the Affordable Care Act (ACA)

Z1301763/13

Preparing to Implement Health Care Reform

As the health care reform implementation continues, it is imperative that businesses understand how they will be affected and are prepared to make strategic health care decisions.

This presentation will cover the initial implementation to offer some back ground:• 3 essential questions every business must ask in 2013• 5 health care reform dates• 7 important facts about health care exchanges

2

3 Essential Questions Every Business Must Ask in 2013

Q#1: Should I offer employer-provided coverage?

• Employer-sponsored benefits may offer cost-effective way to boost employee compensation.

• Only employers with more than 50 FTEs may be subject to penalties if they do not provide affordable and minimum value employer-sponsored health insurance.

• Employers’ contributions to health benefits plans are tax deductible—the $2000 - $3000 penalty is not.

4

THE MAJORITY OF EMPLOYEES (88%) SAY THEY WILL CONTINUE TO OFFER HEALTH BENEFITS TO ACTIVE

EMPLOYEES IN 2014.1

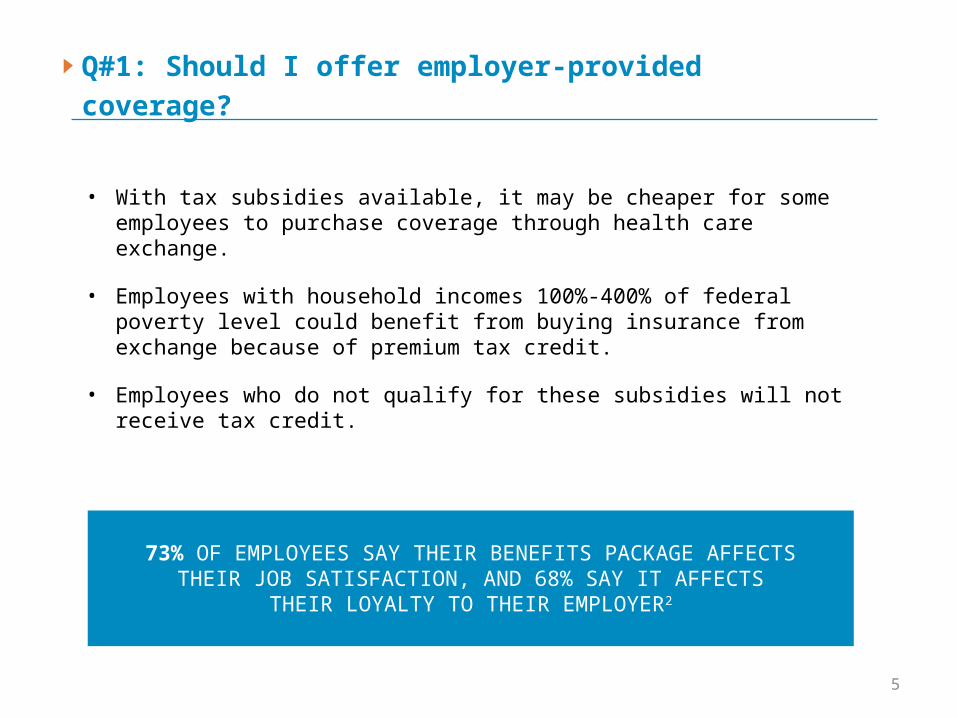

Q#1: Should I offer employer-provided coverage?

• With tax subsidies available, it may be cheaper for some employees to purchase coverage through health care exchange.

• Employees with household incomes 100%-400% of federal poverty level could benefit from buying insurance from exchange because of premium tax credit.

• Employees who do not qualify for these subsidies will not receive tax credit.

5

73% OF EMPLOYEES SAY THEIR BENEFITS PACKAGE AFFECTS THEIR JOB SATISFACTION, AND 68% SAY IT AFFECTS THEIR

LOYALTY TO THEIR EMPLOYER2

Q#2: How much can my business afford to spend?

• Discuss your options with your benefits consultant or broker to help weigh costs.

• Use cost estimates to determine cost per employee.

• Estimate potential penalties for not providing employee health coverage.

• Small business tax credits can help defray costs associated with health care coverage through public exchange.

6

IN 2013, HEALTH CARE COSTS ARE EXPECTED TO INCREASE PER EMPLOYEE BY 5.3% (0.6% LOWER THAN IN 2012)1

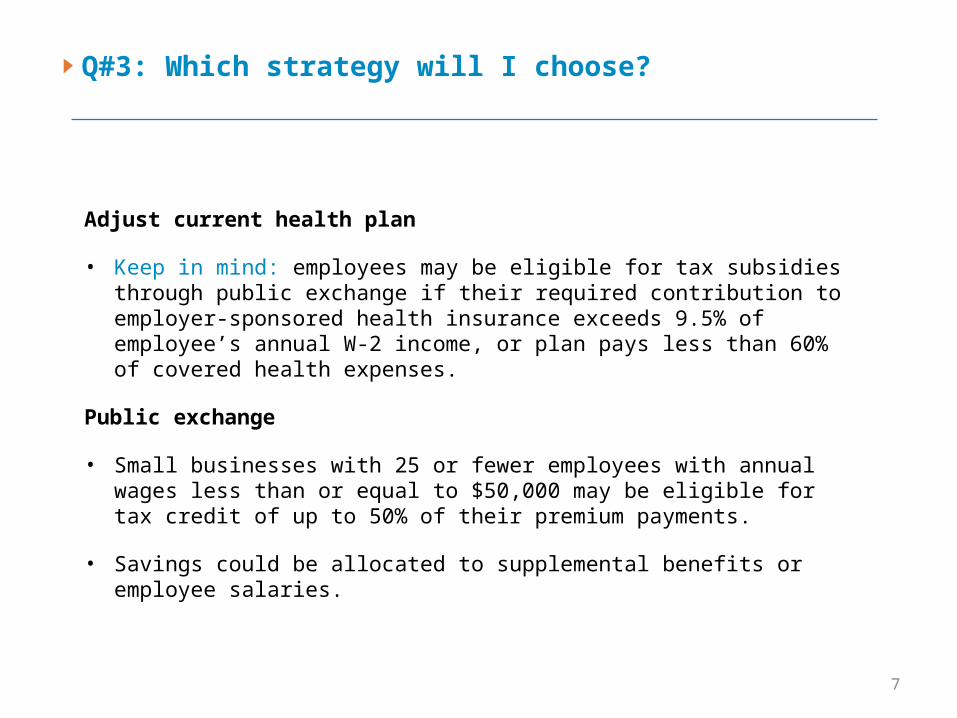

Q#3: Which strategy will I choose?

Adjust current health plan

• Keep in mind: employees may be eligible for tax subsidies through public exchange if their required contribution to employer-sponsored health insurance exceeds 9.5% of employee’s annual W-2 income, or plan pays less than 60% of covered health expenses.

Public exchange

• Small businesses with 25 or fewer employees with annual wages less than or equal to $50,000 may be eligible for tax credit of up to 50% of their premium payments.

• Savings could be allocated to supplemental benefits or employee salaries.

7

Q#3: Which strategy will I choose?

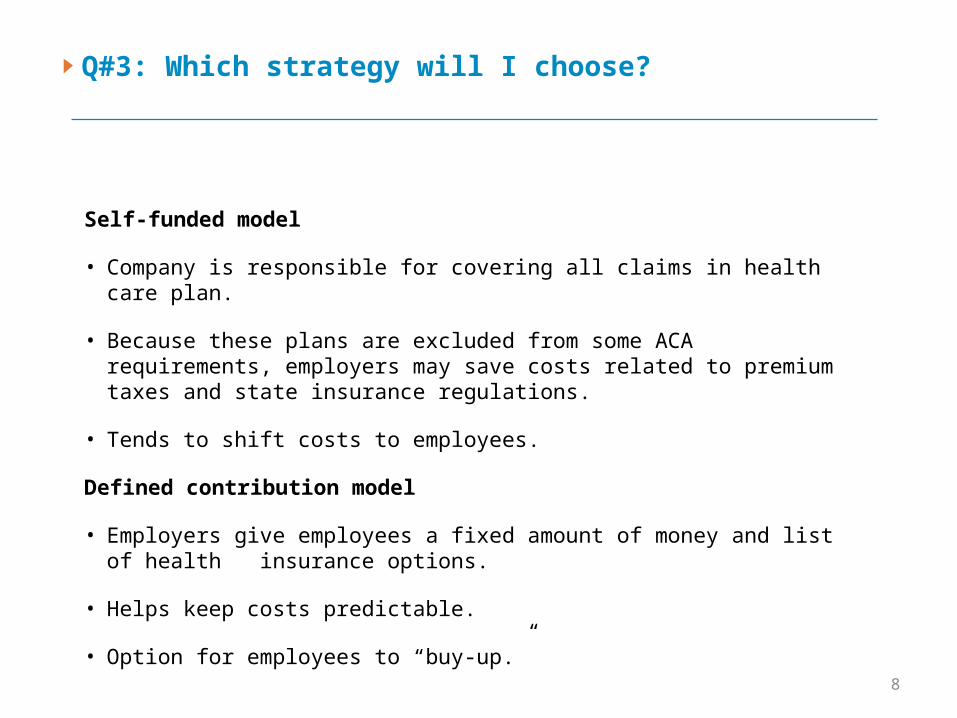

Self-funded model

• Company is responsible for covering all claims in health care plan.

• Because these plans are excluded from some ACA requirements, employers may save costs related to premium taxes and state insurance regulations.

• Tends to shift costs to employees.

Defined contribution model

• Employers give employees a fixed amount of money and list of health insurance options.

• Helps keep costs predictable.

• Option for employees to “buy-up.”

8

Q#3: Which strategy will I choose?

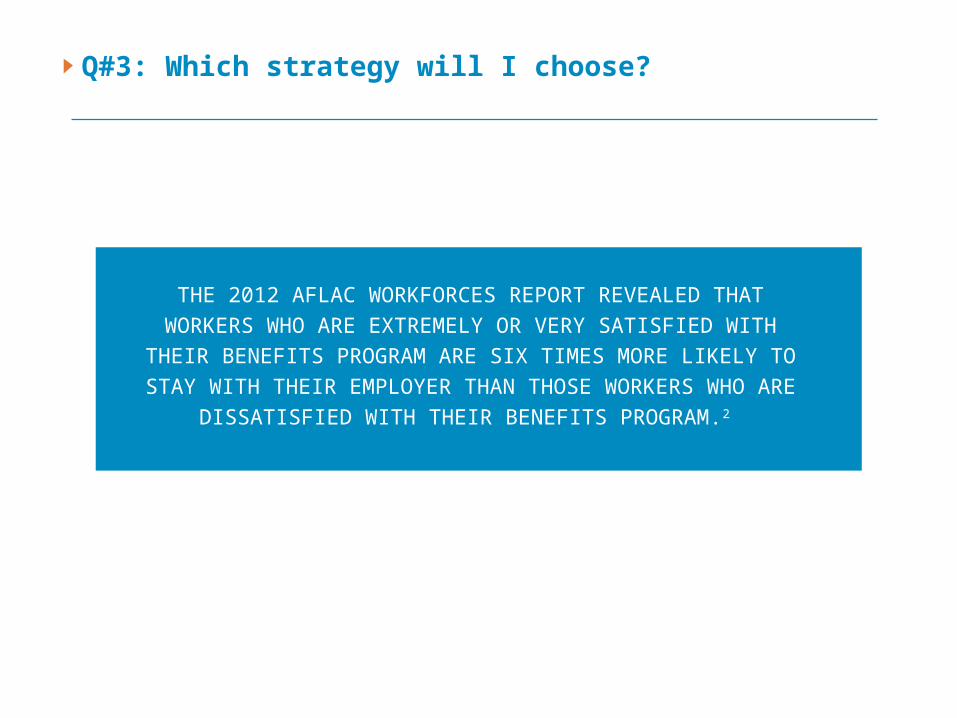

THE 2012 AFLAC WORKFORCES REPORT REVEALED THAT WORKERS WHO ARE EXTREMELY OR VERY SATISFIED WITH THEIR BENEFITS PROGRAM ARE SIX TIMES MORE LIKELY TO STAY WITH THEIR EMPLOYER THAN THOSE WORKERS WHO

ARE DISSATISFIED WITH THEIR BENEFITS PROGRAM.2

7 Important Facts About Health Care Exchanges

#1: An exchange is a web portal to buy and sell products

There will be two types of exchanges throughout the US that will impact employee benefits:

1. Public exchanges facilitated by state and/or federal government.

2. Private exchanges facilitated by private industry stakeholders.

11

#2: Public exchanges will be open for small businesses and individuals to enroll Oct. 1, 2013

Coverage will go into effect Jan. 1, 2014. These exchanges will be open for:

1. Individuals without access to affordable* employer-provided health insurance coverage.

2. Small businesses with fewer than 100 full-time employees.

* Employer-provided coverage in which employee’s required contribution does not exceed 9.5% of their annual W-2 income.3

12

Exchange eligibility by business size

13

#3: Private exchanges generally provide cost-controlling options for businesses of all sizes

• Provide more flexibility than public exchanges because they are not associated with federal guidelines.

• Offer health coverage options to multiple workforce segments and sizes.

• Can sell all products and services including voluntary insurance.

• Help employers move toward defined contribution model that can control costs, while still offering robust benefits.

14

#4: Tax subsidies are only available through public exchange

15

INDIVIDUAL CREDITS

Individuals with household incomes between 100% and 400% of the federal poverty level are eligible for tax subsidies if they are not eligible for affordable employer-provided coverage.

SMALL BUSINESS CREDITS

Small businesses may be eligible for tax credit of up to 50% of their premium payments if they have 25 or fewer FTEs whose annual avg. wages are no more than $50,000.

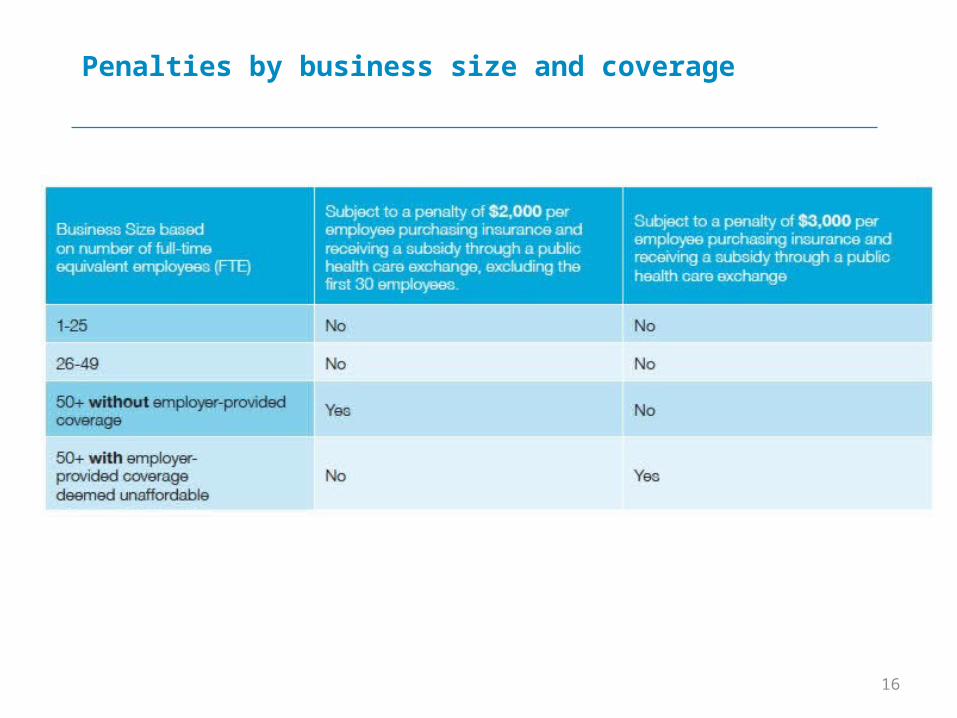

PENALTIES

Employers with at least 50 FTEs must offer min. essential health care coverage to full-time employees or face a penalty.

Penalties by business size and coverage

16

#5: “Silver” coverage will be public exchange benchmark

State exchanges will offer four levels of coverage that vary depending on the proportion of medical expenses the insurance plan is expected to cover.

17

Bronze: plan pays 60% of medical expenses

Silver: plan pays 70% of medical expenses

Gold: plan pays 80% of medical expenses

Premium: plan pays 90% of medical expenses

#6: Exchanges affirm importance of employee education

• Individuals will need to better understand their options and health risks.

• Employees will be responsible for deciding how they spend their health care dollars.

• As some employers move toward defined contribution plans, employees will be in control of how they use and add to their employer’s contribution.

18

43% OF EMPLOYEES SAY THEY DO NOT TRULY UNDERSTAND THEIR EMPLOYER’S CONTRIBUTION TO THEIR

INSURANCE BENEFITS.2

#7: Voluntary products work with major medical coverage to provide essential safety net

• As health care costs continue to rise, supplemental policies help provide a layer of financial protection to employees—without adding to your overall costs.

• Unlike major medical insurance, these policies pay cash benefits directly to policyholder.

• These policies are a way to offer broader benefits package to your workforce.

19

EMPLOYEES WHO ARE OFFERED VOLUNTARY BENEFITS BY THEIR EMPLOYER ARE 15% MORE LIKELY TO SAY THEIR

CURRENT BENEFITS PACKAGE MEETS THEIR FAMILY’S NEEDS EXTREMELY OR VERY WELL.2

5 Health Care Reform Dates Every Business Needs to Know

JANUARY 1, 2013

• Health Flexible Spending Arrangement Contribution Limit: FSA participants will have salary reduction limit of $2,500.

• W-2 Reporting Requirement: All employers that issued at least 250 Form W-2s in 2011 will need to report value of health care coverage that employees participated in 2012.

• Medicare Retiree Drug Subsidy Tax Deduction Eliminated.

21

MARCH 1, 2013

Notice About State Health Insurance Exchanges

Employers subject to Fair Labor Standards Act are required to notify employees of state health insurance exchanges and potential eligibility for premium credits.

22

JANUARY 1, 2014

Play or Pay

Employers with at least 50 full-time employees must offer minimum essential health coverage to their full-time employees (FTEs) or face a penalty.

23

$2,000 Per EmployeeIf employer does not offer minimum essential coverage to all FTEs, and at least one employee obtains premium subsidy through exchange (excluding first 30 employees.)

$3,000 Per EmployeeFor businesses offering coverage considered unaffordable or not meeting minimum value standards. Fine is for each FTE purchasing coverage through an exchange and receiving tax credits, up to $2,000 times number of FTEs, excluding first 30 FTEs.

JANUARY 1, 2014 (cont’d)

• Required Contribution to Temporary Reinsurance Program: Per capita amount is paid for each enrollee by insurer or third-party administrators on behalf of self-funded plans.

• Small Business Tax Credits: Will expand to 50% of the small business’ premium costs for two consecutive years. Available to businesses that offer health insurance through an exchange, with average wages $25,000 to $50,000, fewer than 25 FTEs.

24

JANUARY 1, 2014 (cont’d)

Second Wave of Health Insurance Reforms:• Pre-existing condition exclusions no longer permitted.

• No annual dollar limits on benefits.

• Small group fully insured plans required to offer essential health benefits.

• Limits on out-of-pocket expenses.

• Insurers subject to modified community ratings and guaranteed-issue requirements.

• Waiting periods in excess of 90 days prohibited.

25

JANUARY 1, 2015

IRS Reporting Requirements for Employers• Basic employee data, dates and types of coverage.

• Apply to coverage offered on or after January 1, 2014.

• First report not due until 2015.

26

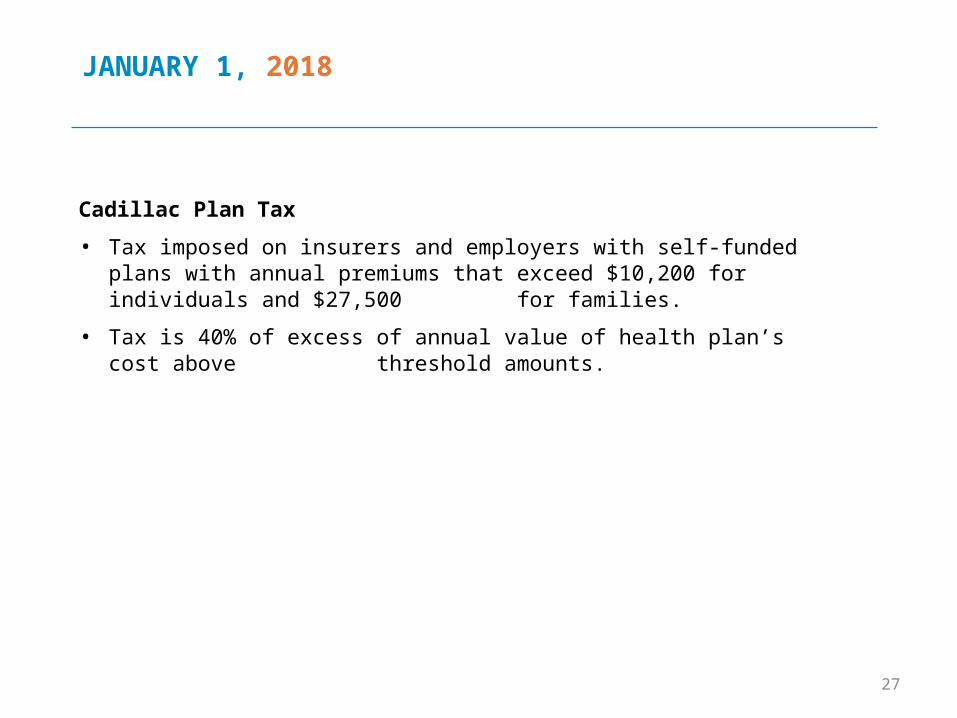

JANUARY 1, 2018

Cadillac Plan Tax• Tax imposed on insurers and employers with self-funded plans with

annual premiums that exceed $10,200 for individuals and $27,500 for families.

• Tax is 40% of excess of annual value of health plan’s cost above threshold amounts.

27

Conclusion

Health care costs continue to rise, and the Affordable Care Act has begun to fuel changes that are difficult for businesses to ignore.

It is more important than ever for businesses and individuals to have a clear understanding of their health benefits, to make smart benefits

choices, and to wisely manage their health care dollars.

28

Thank you

29Z130176 3/13

Source Information

1Towers Watson, 2012 Health Care Trends Survey, accessed on November 8, 2012, from towerswatson.com/assets/pdf/8139/TW-HealthCare-Trends-Survey-NA-2012.pdf

22012 Aflac WorkForces Report, a study conducted by Research Now on behalf of Aflac, January 24–February 23,2012

3HealthCare.gov. http://www.healthcare.gov/using-insurance/understanding/costs

This presentation is for informational purposes only and is not intended to be a solicitation for Aflac Insurance policies or plans. Aflac's family of insurers includes American Family Life Assurance Company of Columbus, American Family Life Assurance Company of New York, Continental American Insurance Company, and Continental American Life Insurance Company.