wharton fintech - p2p lending discussion

DESCRIPTION

Wharton FinTech Club hosted a seminar on P2P (peer-to-peer) lending in October '14. Take a look at our key insights and analyses on this fast-growing industry!TRANSCRIPT

Wharton FinTech

P2P Lending DiscussionClub Meeting

October 21, 2014

KNOWLEDGE FOR ACTION

Agenda

• News and announcements

• P2P Lending

• Lending Club

KNOWLEDGE FOR ACTION

What is P2P Lending?

Loan money to individuals (“peers”) through a simple online platform

•Online platforms that connect institutional and retail investors to borrowers, cutting out traditional FIs

•Use proprietary credit scoring and checking tools to establish APRs and offer term loans to borrowers

•Borrowers typically use money to refinance credit card debt or pay off other obligations

• Lenders can diversify their portfolio through P2P investments

• Loans are unsecured and risk is borne solely by investors

•Over $6.0B P2P loans issued to date

LENDING

KNOWLEDGE FOR ACTION

P2P Lending: Key Players

Overview and market share

Founding and total loans

issued

Borrower profile

Minimum FICO

Loan terms

APR range

Most common use of loan

• Largest P2P lending platform

• Market leader– own about 70% share of market

• Second largest P2P lending player

• About 30% share of market

• Emerging competitor• Likely <1% market share

• Opened to investors in 2007

• $5.0B in loans to date

• First entrant into P2P lending; founded in 2006

• $2.0B in loans to date

• Founded in 2012• Likely about 5,000 loans

funded to date

• Has historically attracted higher-quality borrowers, with approval rates at ~10%

• Initially catered to more sub-prime borrowers; suffered a 22% total charge-off rate in 2010

• Targeted towards younger borrowers with less established credit histories

• 660 • 640 (imposed after high post-recession charge offs)

• 640, but do accept insufficient credit information

• 3 and 5 year terms • 3 and 5 year terms • 3 year term

• 6.78 – 29.99% • 6.73 – 35.36% • 6 – 24.60%

• Credit card debt consolidation / refinancing

• Credit card debt consolidation / refinancing

• Credit card debt consolidation / refinancing

KNOWLEDGE FOR ACTION

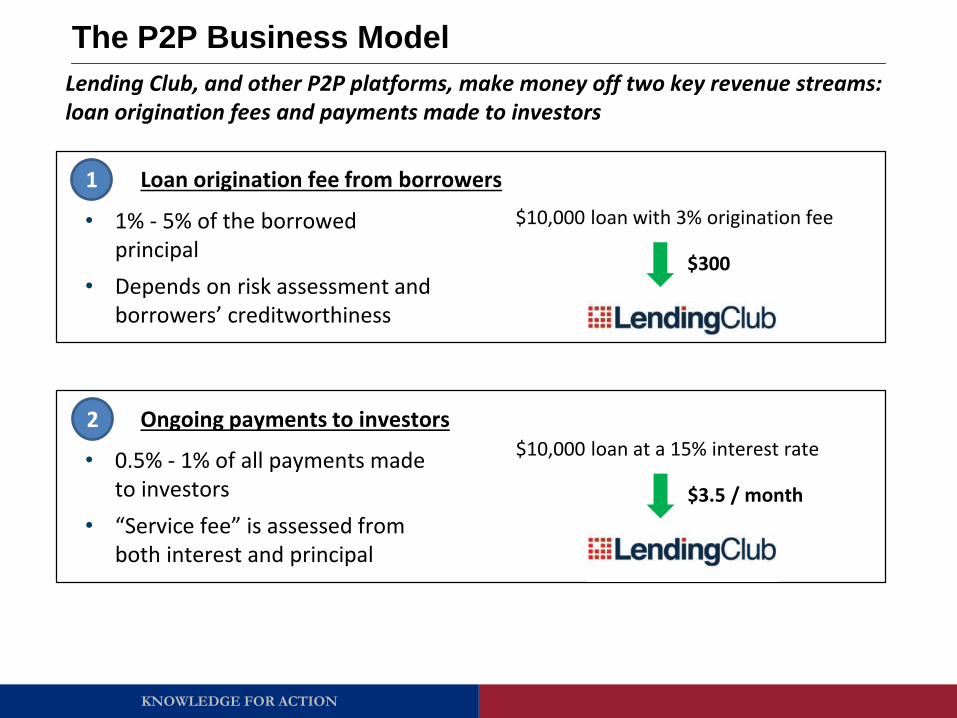

The P2P Business Model

Lending Club, and other P2P platforms, make money off two key revenue streams: loan origination fees and payments made to investors

1

2

Loan origination fee from borrowers

Ongoing payments to investors

• 1% - 5% of the borrowed principal

• Depends on risk assessment and borrowers’ creditworthiness

$10,000 loan with 3% origination fee

$300

• 0.5% - 1% of all payments made to investors

• “Service fee” is assessed from both interest and principal

$10,000 loan at a 15% interest rate

$3.5 / month

KNOWLEDGE FOR ACTION

Agenda

• News and announcements

• P2P Lending

• Lending Club

KNOWLEDGE FOR ACTION

Lending Club: Overview

Lending Club is the market leader in P2P lending, showing rapid growth in loan issuance over the past five years

KNOWLEDGE FOR ACTION

Lending Club: Default Rates

Default rates have recently averaged around 3%, but also vary widely depending on the loan rating

2012 default rates, by loan type

KNOWLEDGE FOR ACTION

Lending Club: Portfolio Landing Page

KNOWLEDGE FOR ACTION

Lending Club: Investing

KNOWLEDGE FOR ACTION

Lending Club: Borrower Profile

KNOWLEDGE FOR ACTION

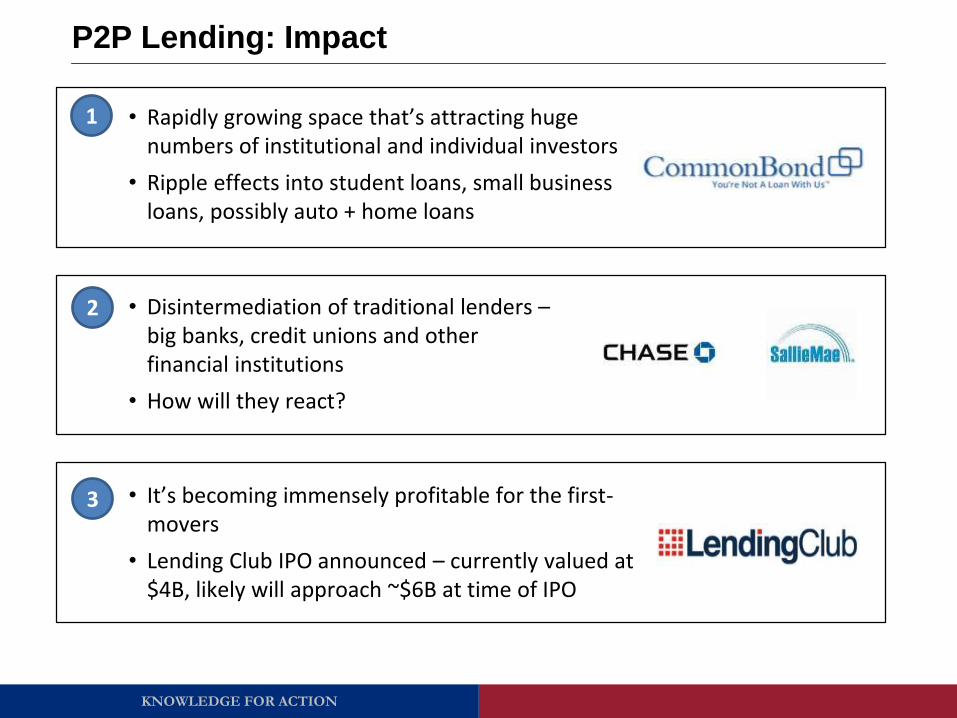

P2P Lending: Impact

1

2

3

• Rapidly growing space that’s attracting huge numbers of institutional and individual investors

• Ripple effects into student loans, small business loans, possibly auto + home loans

• Disintermediation of traditional lenders –big banks, credit unions and other financial institutions

• How will they react?

• It’s becoming immensely profitable for the first-movers

• Lending Club IPO announced – currently valued at $4B, likely will approach ~$6B at time of IPO

KNOWLEDGE FOR ACTION

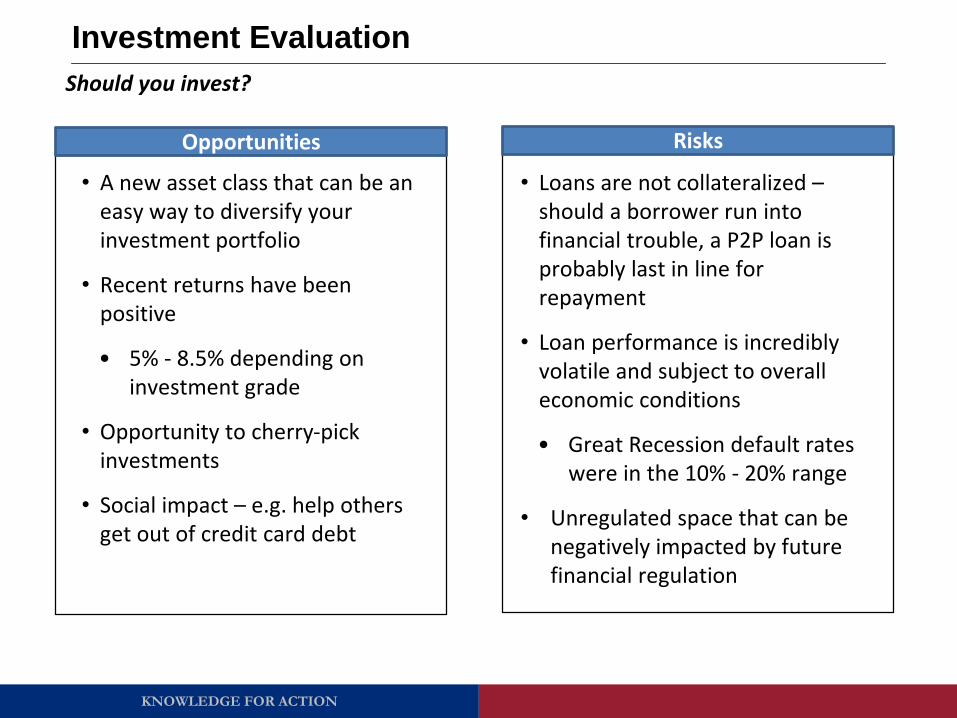

Investment Evaluation

Should you invest?

• Loans are not collateralized –should a borrower run into financial trouble, a P2P loan is probably last in line for repayment

• Loan performance is incredibly volatile and subject to overall economic conditions

• Great Recession default rates were in the 10% - 20% range

• Unregulated space that can be negatively impacted by future financial regulation

• A new asset class that can be an easy way to diversify your investment portfolio

• Recent returns have been positive

• 5% - 8.5% depending on investment grade

• Opportunity to cherry-pick investments

• Social impact – e.g. help others get out of credit card debt

Opportunities Risks

KNOWLEDGE FOR ACTION

Questions

@whartonfintech

Wharton FinTech

Wharton FinTech

whartonfintech.org