wgc stratstruck_case study

TRANSCRIPT

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 1/17

`

World Gold Council Stratstruck

Case Document

It was the shimmering glow of the decorations outside the Jewellery shops that brought Rajeev’sattention back to the meeting scheduled for the day after tomorrow. Passing through the marketscrowded with families on a shopping spree at the occasion of Dhanteras- the first day of the five daylong festival of Diwali, Rajeev was continuously trying to focus on the task at hand. As a principalFinance Secretary to the Government of India, he had to present the strategic policy document tothe Cabinet to tackle the challenges faced by one of the most important segments of IndianEconomy – the Gold Industry.

Introduction

An IAS from the batch of 1972, Mr. Rajeev belonged to a family running jewellery business in Indoreand was always interested in the Gold & Jewellery sector. He had undertaken the currentresponsibility after performing a multitude of roles in Ministry of Commerce, Ministry of Finance,RBI, and a brief stint as Ambassador & Permanent Representative of India to the WTO . Over thisvaried experience he had overseen various government policy initiatives and observed variousindustry segments in their growth phase during the late 90’s.

It was an interesting coincidence that he was assigned the responsibility of developing the

government policy document for this sector in January 2013. He had met different industryrepresentatives in the past three months including World Gold Council, FICCI, CII, major organizedretailers and representatives of unorganized businesses in the past 3 months to understand theissues and challenges faced by the industry.

The Gold Industry

In India, gems and jewellery had always inspired passion unlike any other object of desire. Thedomestic gems and jewellery industry had a market size of INR 251,000 Cr in 2013, with a potentialto grow to INR 500,000–530,000 Cr by 2018. The gems and jewellery industry had been crucial tothe Indian economy given its role in large-scale employment generation, foreign exchange earningsthrough exports, and value addition. The industry was a source of direct employment to roughly 2.5

million people and was expected to generate employment of 0.7–1.5 million over 2014-2020. Incomparison to the 2.1 million jobs provided by IT services, it was one of the most important sectorsof Indian economy. The industry was to drive a value addition of more than INR 99,000 Cr, a figurecomparable to several large industries such as apparel manufacturing.

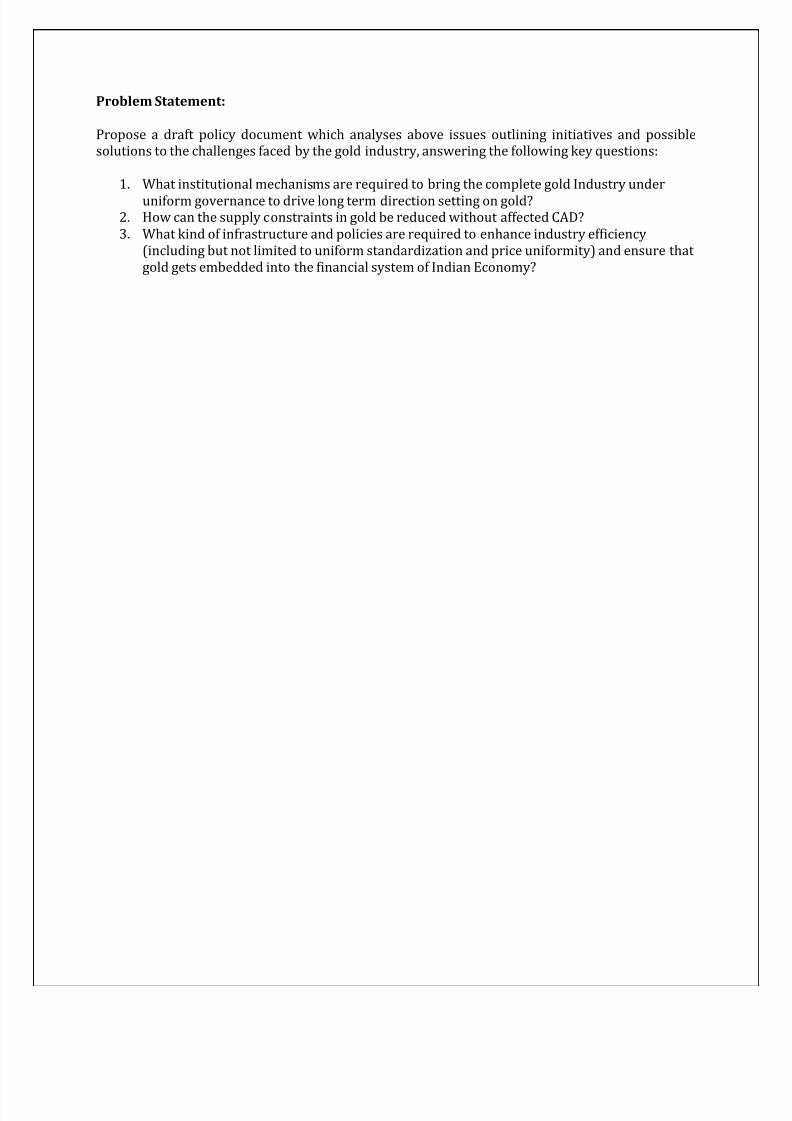

The domestic gold industry was considered the focal point with a market size of $46 Billion in 2012and a growth rate of 75%(in Value terms) for the past 5 years. Gold, the precious shiny metal wasused in the preparation of jewellery and ornaments and as a mode of investment through bullions,bars & coins. The estimated gold stock in India was more than 20,000 tonnes valued at more than

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 2/17

$1 Trillion. This was approximately 60% of India’s total GDP and 200% of India’s Infrastructureinvestment in the 11th Five Year Plan.

However gold had been in focus due to almost complete dependence on imports for supply and anexpanding current account deficit (CAD). As a result of increasing pressures to bring CAD down,regulatory action had been taken to limit gold imports. The CAD for India had increased to 4.8

percent of GDP in 2012–2013 from a positive current account balance of 1.2 percent of GDP in2002–2003. It was worth noting that while imports had grown by a CAGR of 25 percent in thisperiod, exports, however, had not kept pace, with a CAGR of 20 percent between 2002 –2003 and2012–2013.

Gold had the second-highest share in imports, increasing from 6 percent in 2002–2003 to 11percent in 2012–2013. The increase in gold imports had largely been driven by the spectaculargrowth in gold prices, with prices moving from INR 5332 per 10 gm in 2002–2003 to INR 30,164per 10 gm in 2012–2013 (CAGR of 19 percent), leading to a CAGR of 32 percent in value terms. Incomparison, import of gold in volume had only increased by a CAGR of 5 percent.

The other two large segments were crude oil, other petroleum products, machinery and otherequipment. These were considered more essential to the economy than gold and as a result, theregulations to curtail imports have focused on gold. Consequently, there have been changes inregulations that aim to curb gold imports. Because gold was the most important raw material, anyuncertainty in its supply had a crippling impact on the entire industry.

The gold industry in India was facing challenges at multiple fronts. These challenges were supplyconstraints, limited recycling, import restrictions, smuggling, lack of standardization acrossindustry and alienation from the financial market and capital system. With multiple regulationswithout any single co-coordinating body and lack of clear policy framework to incentivize inclusionof gold into the financial mainstream, the industry was calling for a major policy directive.

Gold: The Value Chain

Gold had enjoyed a special significance in Indian culture. Backed by intricate workmanship anddesigns developed over the ages, it had been an integral part of Indian lifestyle and culture forcenturies. Today, India was the largest consumer of gold jewellery in the world with 29 percentshare of the total global demand for gold as jewellery.

The value chain for gold includes mining, refining, trading, manufacturing, retailing of gold as wellas trading of gold-based financial products. The gold value chain had a distinct characteristic: itcatered to both consumption-led demand and investment-led demand. As a result, there were twovalue chains with distinct drivers and needs; however, there was extensive intermingling of theplayers across the two value chains. The industry value chain was comprised of sourcing (mining

and imports), refining, trading, manufacturing, and retailing (see Figure 1). While some of theplayers catered primarily to consumption demand or investment demand separately, there were ahost of players catering to both consumption and investment demand.

Gold Sourcing: Mining & ImportsDue to India’s limited gold reserves, the yearly production of gold was around two tons in theperiod 2011–2012, which amounted to just 0.2 percent of the total gold imported. It was importantto encourage exploration and mining activities of gold in India. FDI up to 100% in mining sector

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 3/17

with respect to gold is eligible for automatic approval. The concessions and mining leases for goldwere granted by State governments after prior approval from central government.

Most of the gold was imported only through a handful of bodies, including bullion banks andGovernment trading agencies, and was largely organized and consolidated among fewer players.Also, the imported gold was usually sold in bulk to manufacturers and dealers. Gold was imported

primarily in unwrought or semi-manufactured form (INR 292,000 Cr in 2012–2013). However,some gold was imported as jewellery (jewellery import was INR 27,000 Cr in 2012 –2013). Theseimports however, were, lately subjected to government duties and taxes. Custom duty on Goldimports was increased to 10% from 2% in 2012. The custom duty on gold jewellery was increasedto 15% in September 2013.

Resale Regulatory RestrictionsAlong with other restrictions, the gold imports were subjected to a unique regulation clubbing itwith exports. The Reserve bank of India had put further curbs on gold import in July 2013mandating the banks and nominated agencies to retain 20 percent (or one fifth) of every lot of goldimports in the customs bonded warehouses. They were allowed to import further gold only oncethey released the 75 percent of that stored gold for the purpose of exports. This put all the domestictraders like Tanishq, TBZ etc. in a fix as they did not have any export business. This could result inexporters demanding unjustified premiums for export replenishments and increase pressure on thedomestic supplies.

RefiningRefineries in India operate mainly on imported gold bars and scrap gold collected from thedomestic market. Refineries thus played a crucial role in the recycling of gold in the country. Themarket for refining was small, however. Currently, it was estimated that refineries were operatingat 25 percent of total installed capacity due to a shortage of used jewellery. The market consisted ofa few larger units and other smaller units, mostly in the private sector and a few Governmentrefineries. In addition, none of the private refineries were LBMA (London Bullion Market

Association)-certified for gold, hence gold bars produced by them could not be used for exchangetraded funds (ETFs) or bought back by banks and as a result these refineries were not part of thefinancial system.

Bullion TradersGold was sold from banks and other Gold importers to the wholesale bullion dealers (~ 200 innumber). Some of the big dealers cater to the jewelers and second level dealers. The complete valuechain is described in (See Figure 2 and 3).

Manufacturing

The last few years had seen the emergence of larger organized manufacturers of jewellery having

modern, well organized manufacturing units. With higher focus on design, quality, standardizationas well as efficiency (minimal gold loss); they primarily catered to consumption demand forjewellery. These players operated primarily from the major jewellery manufacturing hubs in thecountry. The rest of the jewellery manufacturing industry was fragmented, with a large share of theoutput produced by small manufacturers. The manufacturing industry imparts the value addition ofmore than INR 99,000 Cr. The taxation has been mainly governed via Customs and Excisedepartment and state departments for CST and VAT.

Retailers

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 4/17

The past decade had witnessed the emergence of organized players, with Government liberalizinggold imports into the country. The industry was, however, still fragmented, with local andindependent stores constituting roughly 80 percent of the overall market, in comparison to a muchhigher proportion of share from organized players. Despite that, there has been a sharp increase inthe share of organized retail, which was almost negligible 15 years ago. Over the period between

2008 and 2013, the share of regional chains has increased significantly from 7 percent to 17percent, while the share of national chains has grown from 3 percent to 5 percent. Around 65% oftotal gold demand in 2012 was jewellery demand with almost flat demand in tonnage, butappreciation in value has been driven by rising gold prices.

While the share of organized players in Gems and Jewellery industry had been increasing, there wasa risk of a slowdown in this trend due to regulatory restrictions on gold imports and pricedifferential between official and unofficial supply of gold in the market. Lack of optimal checks bygovernment to restrict unaccounted gold trade had also encouraged sale of smuggled gold intomarket at lower prices putting pressure on organized retailers.

Rising Demand for Gold

Jewellery Demand

A unique feature of Indian demand for gold jewellery was its steady growth leading to appreciationin terms of value by 4.2 times in nominal terms, despite higher import duties. The jewellerydemand accounted for around 64 percent of the total market demand. This demand was led by theneed for gold and non-gold jewellery that caters to specific wear occasions. However it wasdifferent from any other luxury products in terms of appreciation in value over time. Moreoverunlike other luxury products, gold purchase, even as a jewellery was always backed with a stronginvestment perspective.

Investment Demand

Investment demand was mainly in form of bars and coins accounting for about 36 percent of thetotal market demand. The high investment demand in India was driven by lack of alternateinvestment or savings options, perceived capacity to hedge against inflation, ability to invest in goldin small denominations, ease of investing unaccounted money in gold and the limited presence ofalternate investment or savings options for a large section of the society. (See Figure 5 & 6)

Gold-Based Financial Industry

The investment demand for gold was also fulfilled through financial products. There were differenttypes of products available in the market. Retail investors may take positions in gold throughfinancial instruments such as gold ETF, e-gold, and gold-based mutual funds.

Gold ETFs

These were exchange-traded funds backed by gold. Gold ETFs were provided by about 14 financialinstitutions in India and were traded on the NSE and BSE. They provide returns that closely matchthat of gold, though there was a need for actual backing with physical gold up to 90 to 95 percent ofthe value of the gold ETF. It was also possible to back these (up to 20 percent) with the gold deposit

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 5/17

schemes of banks. However, retail investors need not take physical possession of gold during thetransaction. The instrument works on a platform similar to equity trading, with investors needingequity demat accounts to have positions.

There was a comparatively larger market for gold ETFs globally, with combined holdings of 2,691tons at the end of 2012. However, the market for gold ETFs in India was smaller, with gold holdings

of around 40 tons (around INR 10,660 Cr of total assets under management). Of this, the top fourfunds (Goldman Sachs, Reliance Mutual Fund, SBI Mutual Fund, and Kotak Mutual Fund) havearound 75 percent share. Launched in 2007, gold ETFs were relatively new, with significant rise involumes only in the past two years. However, recent pressures on CAD had led to instances ofmarket regulator SEBI turning down applications for new gold ETFs.

Gold funds

These were usually fund of funds schemes backed by gold ETFs. They operate along similar lines tomutual funds, and do not require a demat account. Being fund of funds, they incur recurringexpenses of the underlying scheme (gold ETFs). Gold funds also offer Systematic Investment Plans(SIPS) that allow customers to invest in small value.

Overall, the market for financial products was comparatively new in India, with low off-take andlimited product options. Recent pressure on CAD also had led to initiatives impacting the industry.

Banks/NBFCs dealing in Physical Gold

Banks earlier sold gold coins and bars to the customers at premium. However, selling of gold coinswas suspended due to import restrictions from banks on gold coins (imports were the only sourceof certified gold coins in absence of LMBA accredited refinery in India). Banks were not permittedto buy back the gold coins or give loans against gold coins or bars. This tightened the reverseliquidity of gold into the market as the gold coins bought by customers were not being bought backby banks. Also while loans could be given up to value of 50 grams of gold jewellery and specially

minted coins by some financial institutions, it was also restricted by RBI recently constraining thesupply of gold back into market. Also as a result of overregulation, the customers were beingpushed back to old system where the jeweler also acted as a financial institutions without anymonitoring and control mechanism.

Gold Trading

Trading of physical gold was done by dealers and gold jewellery manufacturers and retailers.Physical gold was usually purchased in bulk from importing agencies and then resold to smallerjewelers across the country. This trading caters to both consumption and investment demand in themarket.

Commodity-based trading of gold was done through exchanges such as the Multi CommodityExchange of India (MCX), National Commodity & Derivatives Exchange Ltd. (NCDEX), NationalMulti-Commodity Exchange of India Ltd. (NMCE), and National Spot Exchange Limited (NSEL).Several organizations engage in trading activities, including bullion dealers and jewellerymanufacturers. Most of these transactions were done by industry players and not by retailinvestors. For example, jewellery retailers would hedge position in MCX while buying jewellerydirectly from vendors.

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 6/17

Gold based futures market was still in very nascent stage. The futures transactions were limited dueto liquidity issues in gold and the price visibility was not more than 1 month. At the same timeOptions were not allowed in gold for trading.

Potential of Gold in the Indian Economy

It was widely believed that gold had a potential role to play in the Indian economy. Gold had earlierbeen used as collateral in the unorganized sector and was strongly entering into the financialsystem through formalized lending against gold holdings. Gold was to reach its position as anormalized and taxed store of wealth and a standardized trading commodity at retail level. Thiswould reap benefits for all stake holders including the exchequer, regulators, consumers industryand intermediaries alike.

The long term milestones for the industry were reduction of gold imports without constraining thesupply side, increased usage of gold standards to effect “commoditization” of gold in retail marketand institutionalization of a robust and centralized regulatory framework to increase thedeployment of gold as capital in the economy.

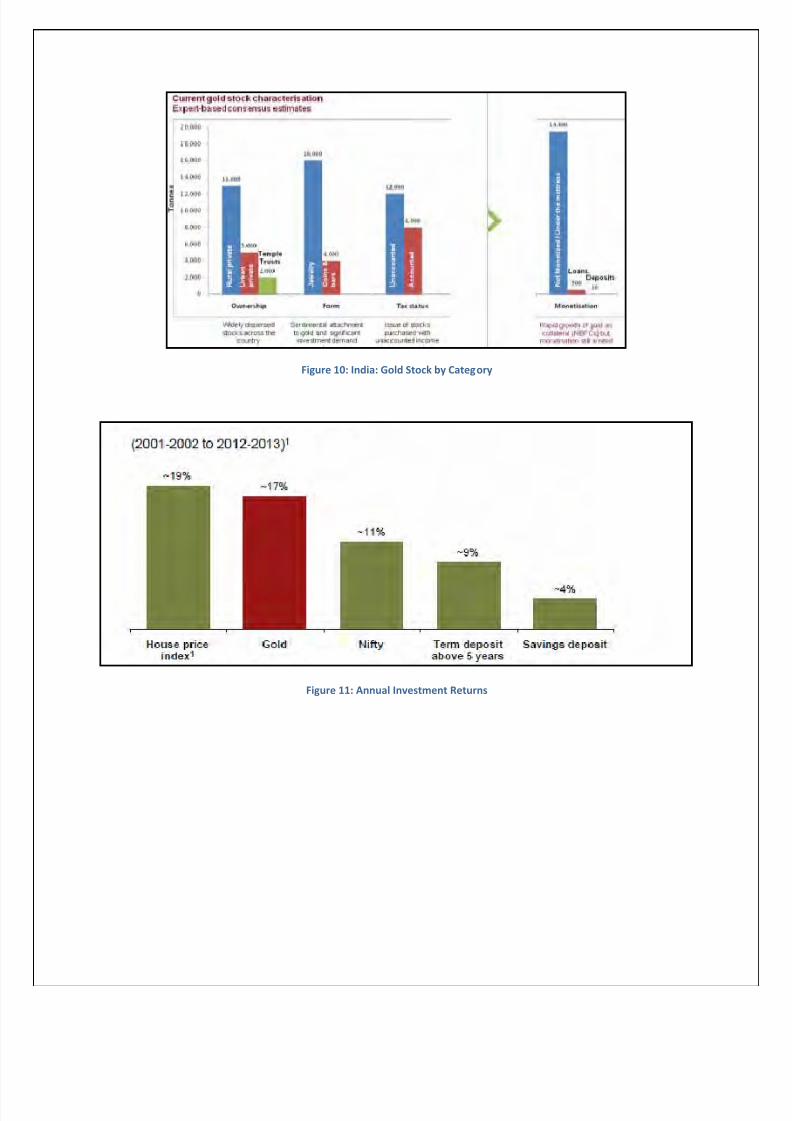

Increasing monetization of gold was also imperative to free up the locked wealth in the Indianeconomy. From 2005 to 2012 the percentage of gold demand as investment instrument hadincreased from 19% to 36% (See Figure 12) thus presenting a stronger case for monetization ofgold. However, a strong policy framework to monitor, regulate and encourage this exercise was stillnot in place.

Unofficial gold market

A significant source and result of market and regulation inefficiencies was unofficial gold trade.With annual volumes as high as 100 tonnes per year, gold had been the first choice for smugglersdue to very high value to volume ratio, non-traceability after the supply into market and significantprofits per transaction. The price difference in the international and domestic market was huge(about 250$/oz., 1 oz. = 31 grams approx.), and was mainly because of import restrictions and highcustom duties. With size of total gold industry around USD 45 billion, it had the potential to giverise to one of the biggest illegal industries in India. Recent restrictions posed by government onimport of gold had only given a boost in gold smuggling which was estimated to cross 150 tonnes in2013. This not only had economic repercussions in terms of loss of revenue to the government andincreased inflow of unaccounted money into the system, but also posed serious social threat as itwas acting as source of organized criminal activities and terrorist financing. This issue requiredimmediate attention and serious steps to reduce regulatory inefficiencies to curb illegal trades andsmuggling in gold were needed.

Challenges to the Industry

Gold catered to two very distinct demands—consumption and investment —with very differentneeds and challenges. Some of these challenges could impact the industry’s performance if leftaddressed. While certain structural challenges kept the industry from reaching its full potential,

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 7/17

there were recent regulatory challenges that could further diminish the growth prospects for theindustry.

High import dependence

Out of total demand, only ~5% of gold was supplied from Indian mines. Gold was the second-

largest import item after crude, with an import bill of INR 307,000 Cr (including gold as part ofjewellery) in 2012–2013(See figure 8). Of this, around INR 152,000 Cr of imported gold was forjewellery manufacturing catering to the domestic market and around INR 92,000 Cr was for barsand coins; the remaining gold exported primarily as jewellery. The high CAD (4.8 percent of GDP) inIndia had led to concerns over the import bill of gold that catered to the domestic gems andjewellery industry and bars and coins manufacturing. Consequently, a series of regulatorymeasures had been taken to reduce gold imports. While the regulations aimed to reduce the currentaccount deficit, they also had put pressure on the growth of the gems and jewellery industry.

Limited recycling

The supply of gold from old gold scrap was only around 13 percent of total domestic consumer

demand for gold in 2012, which was less than 1 percent of the above-ground stock of gold in India.This was due to the unique positioning of gold in the minds of the Indian consumer, whereby thesale of family gold was seen as a social taboo and to be considered only in the case of acute financialcrisis. There was also a lack of incentive to sell household gold, since there was a loss in value onthe sale of gold jewellery and the buyback price provided by jewellery retailers for old gold waslower (up to 10 percent) than the gold selling price to account for impurities in the used gold. (See

Figure 7)

Given the import dependence and limited recycling, there have been initiatives to encourage higherrecycling such as the Gold Deposit Schemes of State Bank of India, which targeted both retailcustomers and trusts to loan out their gold holding. However, these schemes had limited successdue to insufficient coverage and communication, unattractive scheme structure, and consumer

inhibitions.

It was imperative to increase gold recycling and bring the idle gold stock into the market andembed gold int o the financial fabric of the country’s economy.

Absence of industry wide standards for gold refining and imports

India was the only large consumer of gold without any refinery accredited by internationalstandards. There was no common standard for Gold bullion (999.9 Kilobar, the most prevalentproduct accounting for ~70% of trades) (See Figure 15). The absence of any LMBA accreditedrefinery led to unavailability of authentic 99.9% pure gold. At the same time it also affected the

yield and quality of the recycled gold because of the impurities present in the initial stage itself.

Another big challenge was the absence of a uniform standardizing and certification authority inIndia at the retail level. Currently only about 10,000 Hallmark certified suppliers were present inthe industry. Presence of Hallmark had been limited due to logistical issues like lack of Hallmarkingcentres and low customer awareness regarding gold standards in India. More importantly Hallmarkcertified gold also rendered itself to uniformity in prices which was an important step towardsintegration of different bullion markets across India.

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 8/17

Overregulated consumption industry and under-developed investment industry

The industry faced regulatory challenge due to lack of differentiation between consumption andinvestment resulting in overregulated consumption and under-developed investment industry.Currently there were 8 different agencies under three different ministries overseeing the completeGold Value chain. For different players in the supply chain, multiple regulatory bodies existed which

governed the transactions. There was absence of a central body to facilitate all utility functionsrelated to gold like price discovery and act as centre for inter-dealer bullion trading. (See figure 10)

The financial industry for gold-based products also faced regulatory challenges. Approvals for newgold ETFs had been rejected by the SEBI in an effort to contain gold imports. Also, some regulationsprevented banks from sourcing gold from the domestic market. However, these multipleregulations had resulted in inefficiencies in the market and constrained business growth. A centralregulatory structure was required to provide holistic understanding of gold across facets, developspecialized expertise on gold transactions across consumption and investment market.

Further, a large section of the jewellery industry was playing the role of financial institution bycatering to investment needs and money lending, particularly in rural areas. And since it was notregulated like other financial institutions, it could be a risk to consumers who were not aware.There was a high demand for physical gold for investment purposes due to the attractiveness ofgold as an investment option, lower availability of alternate savings or financial options, and limitedfinancial products backed by gold. Initiatives to increase gold involvement in the financial systemcould bring in the consumers to a more secure investment and lending environment.

Initiatives in the Foreign Markets

Gold markets in Turkey, Dubai and China had developed from similar challenges in the previousyears. Shanghai Gold Exchange was started in China to act as a marketplace for gold transactions.Aggressive acquisition of overseas gold mines was effected to secure gold supplies. Dubai alsolaunched a separate gold exchange to tap into increasing gold demand in Middle East.

Turkey faced current account deficit issues similar to India. Turkey followed a set of coordinatedmeasures to tackle these challenges. Between 1985 and late 2000’s, Turkey established 3 worldclass LMBA certified refineries that produced gold bars and coins. Using Reserves optionmechanism, the Turkish Bank incentivized gold deposit products to collect “idle” gold. The Turk ishBank also allowed use of gold bullion to satisfy reserve requirements in 2010 and increased goldreserves limits to 25% in 2012 to increase monetization of Gold. Within 2 years, more than 300tonnes of gold was monetized through various such measures (See figure 15).

Way Forward

The gold industry which had a potential of being a kingpin of the Indian financial system andtreasury, was facing potential stagnation, with challenges at multiple fronts. It was thereforeimperative for various stakeholders, such as the government, RBI, and industry, to drive large-scaletransformation and ensure a sustainable and growing industry. A clear policy framework wasrequired to be designed to address key structural and regulatory challenges.

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 9/17

Problem Statement:

Propose a draft policy document which analyses above issues outlining initiatives and possiblesolutions to the challenges faced by the gold industry, answering the following key questions:

1.

What institutional mechanisms are required to bring the complete gold Industry under

uniform governance to drive long term direction setting on gold?2.

How can the supply constraints in gold be reduced without affected CAD?3. What kind of infrastructure and policies are required to enhance industry efficiency

(including but not limited to uniform standardization and price uniformity) and ensure thatgold gets embedded into the financial system of Indian Economy?

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 10/17

Exhibits

Fi

gure 1: Gold Value Chain in India

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 11/17

Figure 2: Value addition across value chains in Gems and Jewellery Industry(others include other precious metals like silver, platinum and gemstones)

Figure 3: Indian Gold Industry Structure

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 12/17

Figure 4: Gold price trend (2005 -2012)

Figure 5: Demand trend for Domestic Gems & Jewellery and Gold Bars & Coins market

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 13/17

Figure 6: Gold Demand: India’s share in Global Demand (by volumes of gold consumption)

Figure 7: Recycling of Gold - Ratio of gold supply from scrap to gold demand

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 14/17

Figure 8: India’s total Imports 2012-13

Figure 9: Agencies overseeing Gold industry regulations

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 15/17

Figure 10: India: Gold Stock by Category

Figure 11: Annual Investment Returns

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 16/17

Figure 12: Consumption v/s Investment share of Domestic Gold Demand

Figure 13: Percentage of Gold in total reserves held by Central Banks

8/11/2019 WGC Stratstruck_Case Study

http://slidepdf.com/reader/full/wgc-stratstruckcase-study 17/17

Figure 14: Gold Reforms in Turkey and its economic parameters

Figure 15: International Gold Standards and Accreditations, gold refineries in different countries