western irrigation futures customer information sessions may 2010 bacchus marsh irrigation district

TRANSCRIPT

Western Irrigation Futures

Customer Information sessions May 2010

Bacchus Marsh Irrigation District

2

Today’s discussion…

1. Feedback from customer workshops and surveys

2. Key findings from WIF

– Bulk water options

– Infrastructure options investigated

– On-farm management practices

3. Future water supply

– Longer term

– Next season

4. Next steps

– Customer reference group

3

Recap…

WIF Atlas

Customer Consultation

Technical Workshops

Draft Options Paper

Detailed Technical Work

Bulk Water Environment Infrastructure On farm

Final Options Paper

Customer engagement and consultation

Government / Agency consultation

Today’s

discussion

4

1. Customer Feedback

5

What you told us you would like…

• Key issues

– Secure source of water

– Sufficient volume to support historic production levels

– Water at affordable price

– Make recycled water available, and

– Fix leaky channels

• Other concerns raised

– Farming viability

– Agricultural practices

– Future of the district

And, we gave a commitment to keep you informed

6

2. Key Findings:Bulk Water Supply Options

7

Bulk water options investigated

• River water supply• Trading options

– Connection to Goldfields super pipe• Supply to Pykes Creek reservoir• Supply direct to Bacchus Marsh• Reinstate Central Highlands Scheme

– North/South pipeline– Macalister Irrigation District

• Metro water– Accessing water from the Melbourne pool

• Government announced access to 3,000ML for BMID

• Recycled water – Supply from WTP – Caroline Springs– Other sources

• Groundwater – Increasing bore numbers (allocation)– Accessing deeper aquifer

8

River water supply – climate scenarios…

Lerderderg River Seasonal Inflows (at Sardine Creek)

9

Goldfields Superpipe

• 760 mm diameter pipe– Urban supply for Ballarat

– Water from Goulburn system via pipe to Bendigo

• Pipe route located near top of Werribee catchment

• 3 options– Pipe to upper Werribee

– Reinstate Central Highlands scheme

– Pipe to BMID

11

Trading options…• Purchase Goulburn Water• Pay transfer cost through via Bendigo and Goldfields Super pipe• Build connecting infrastructure

Option Capital Cost

Key issue $ per ML

Reinstate Central Highlands Scheme

$4.5 m High water loss $2,150

Supply to Upper Werribee $15.2 m High water loss $2,200

Supply direct to Bacchus Marsh $65 m High capital cost $3,000

12

Trading options…

• North South Pipeline

– Government committed to maximum 75,000 ML/year cap

– Commitment to Northern Irrigators that this would be maximum amount

– Option to access water from northern Victoria not available

• MID – Thomson Dam

– 11,000 ML Entitlement on key rivers in the MID (trading zone)

– 30% can be transferred across the system

– Water must be purchased and water transferred through district.

– Cost to transfer is $745 per ML for 2009/10.

– Limited flow rate and timing of delivery

13

Metro water supply…

• Available to access up to 3,000ML per year

• Delivery via Western Water’s urban water supply system

• Contract details

– Supply by Agreement (Entitlement) with City West Water to SRW

– Delivery agreement with Western Water

• Access and pricing arrangements reviewed every five years

• Price structure set by Essential Services Commission (ESC)

• Same structure for all water authorities

14

Other Options…• Recycled Water

– Caroline Springs

• Option no longer available commitments made elsewhere in investment and usage and has high operating cost

– Bacchus Marsh

• Fully contracted by Western Water and

• Fully committed in the future

– Western Treatment Plant

• Not economic – $50m pipe/pump investment plus

• Cost to expand Class A plant

• Groundwater– Merrimu – full allocated, hydro assessment no further water available

– Parwan – full allocated, hydro assessment no further water available

– Other – accessing groundwater elsewhere and pipeline to BMID is capital intensive and high risk

15

2. Key Findings:Infrastructure Options

16

Infrastructure options ….• Pipelining

– Piping from weir technically difficult due to flat grade

– Large pipes and low velocities

– Uncertainty if some existing pipes can take higher pressure

– Not costed

• Channel lining – Lining of Werribee Vale Road channel unfeasible due to silting

– Liners damaged with silt removal

• Balancing Storage (320 ML)– Cost $6.2m, plus

– 2 kilometre transfer pipe $1.5m

• Reconfiguration…– Suggested at first workshops

– Focus on upgrading parts of the supply system

– Improve operational flexibility and reduce delivery losses

17

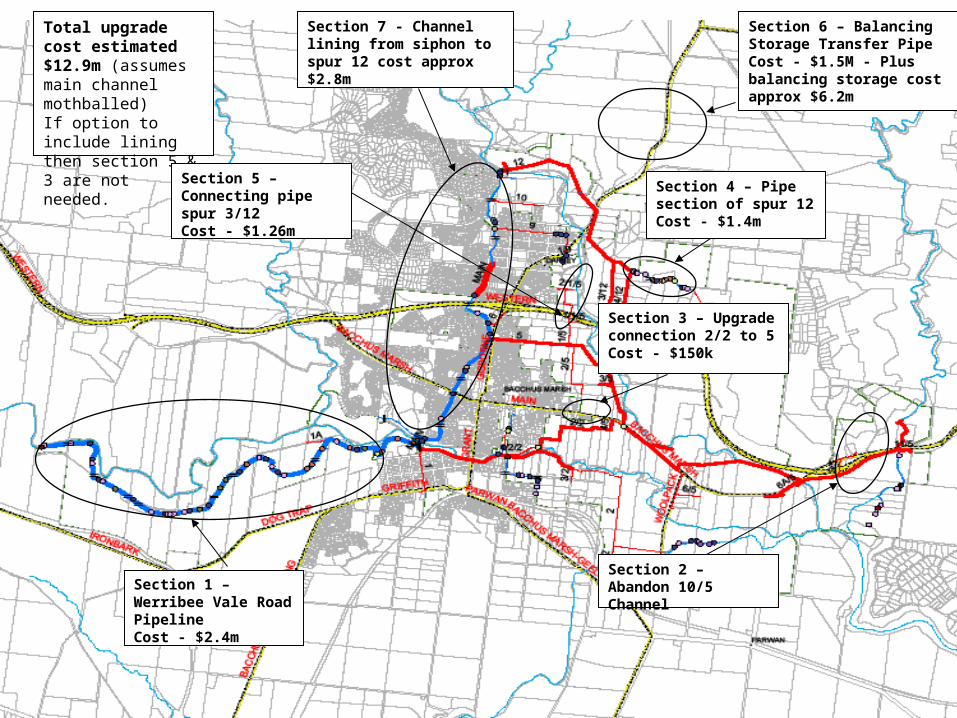

Infrastructure Options

Section 6 – Balancing Storage Transfer PipeCost - $1.5M - Plus balancing storage cost approx $6.2m

Section 1 – Werribee Vale Road PipelineCost - $2.4m

Section 7 - Channel lining from siphon to spur 12 cost approx $2.8m

Section 3 – Upgrade connection 2/2 to 5Cost - $150k

Section 4 – Pipe section of spur 12Cost - $1.4m

Section 2 – Abandon 10/5 Channel

Total upgrade cost estimated $12.9m (assumes main channel mothballed)If option to include lining then section 5 & 3 are not needed.

Section 5 – Connecting pipe spur 3/12Cost - $1.26m

18

Infrastructure options ….

• Reconfiguration option 1 – cost $12.9m– Interconnection of existing pipelines

– Pipelining supply to Werribee Vale Road customers

– Mothballing main channel

– Balancing storage and transfer pipe

– Pipe section of spur 12

– Expected efficiency 85% – 90%

• Reconfiguration option 2 – $14.3m

– Pipelining supply to Werribee Vale Road customers

– Balancing storage and transfer pipe

– Pipe section of spur 12

– Channel lining from siphon to spur 12 crossing

– Expected efficiency 85% – 90%

19

2. Key Findings:On-farm issues

20

On-farm issues addressed…

• Commercial considerations– Cost of production – Choice, mix and rotation of crop types– Scale of operation and constraints– Land values, planning regulations and impacts of development on farming

• Water resource availability– Security of water supply to grow crops – Scope to reduce water use by utilising other irrigation methods

• Agronomy and water quality– Identification and costing of best practice requirements for irrigation, soil salinity

and nutrient management

• Environmental implications– Understanding of potential impacts on environmental assets

• Social factors– Social, cultural, adoption of technology, management practices and business

decisions

21

3. Future Water Supply

22

Future supply options…

• Government announced access to 3,000ML of metro water

• Access limited to 10ML/d flow rate with possible reduction during peak demand days

• Addition of balancing storage would provide ability to increase up to 20 ML/d during summer on limited days

• Supply may include a mix of river water (when available), and metro water to maximise supply and flow rate and minimise losses

23

Water availability – 2011/12…

• Water outlook 1 July 2010– River water allocation likely to commence at 6%

• Based on zero inflows and no deliveries

– Emergency water supply not used by 30 June 2010 to be re-allocated

• Supplementary options– Access a volume of the metro water for next season

• Price is $1,357 per ML

– Potential trading Options

• Macalister trading

• Trading with Werribee (if water balance OK)

24

BMID water balance – 2009/10

*Remaining river water based on 14% allocation

Delivered Volumes (2009/10)Minimum Target ML

Actual 2009/10 ML

Actual Usage to 18 Apr

Remaining 2009/10

Target Volume (25% equivilent allocation) 1085Emergency water carried over from 2008/09 (Thomson and Merrimu unallocated)* 556 530 295 235River Water - 2009/10 180 616 302 3142009/10 Thomson Water (inc second connection) 350 425 190 235Total Estimated 1086 1571 787 784

–

25

BMID estimated water balance – 2010/11

Source ML CommentsCurrent Emergency supply 470 Current volume availableEstimated usage remainder 2009/10 100 Based on last year pus about 15%Estimated Starting allocation - 6% 264 Based on current usage and no further inflowsMinimum inflows (4%) 180 Based on historical minimum inflowsMinimum available volume 814 Similar to usage in 2009/10

26

Effective charges including usage from Metro system…

Average charges - 150ML Entitlement

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Status Quo Next season

0

10

20

30

40

50

60

70

80

90

100

ML

27

4. Next steps

28

Consultation process…

• Establish Customer Reference Groups – Separate groups for WID and BMID

• Seek nominations

– 1 WBMCCC for each group

– 6 customer representatives for each group

– Stakeholder representatives

• Appoint independent chair

• Terms of reference to include

– Bulk water supply options

– Pricing matters

– Infrastructure issues (e.g. channels and storages)

– Environmental matters

– Contract matters (metro water supply)