welcome. cost share & rate changes benefit changes life insurance flexible spending...

TRANSCRIPT

Open Enrollment for 2015

October 20 through November 7

Welcome

Cost Share & Rate Changes Benefit Changes Life Insurance Flexible Spending Accounts Open Enrollment Process Qualifying Events Questions & Answers Raffle

Agenda

3

Cost Sharing and Rate Changes

4

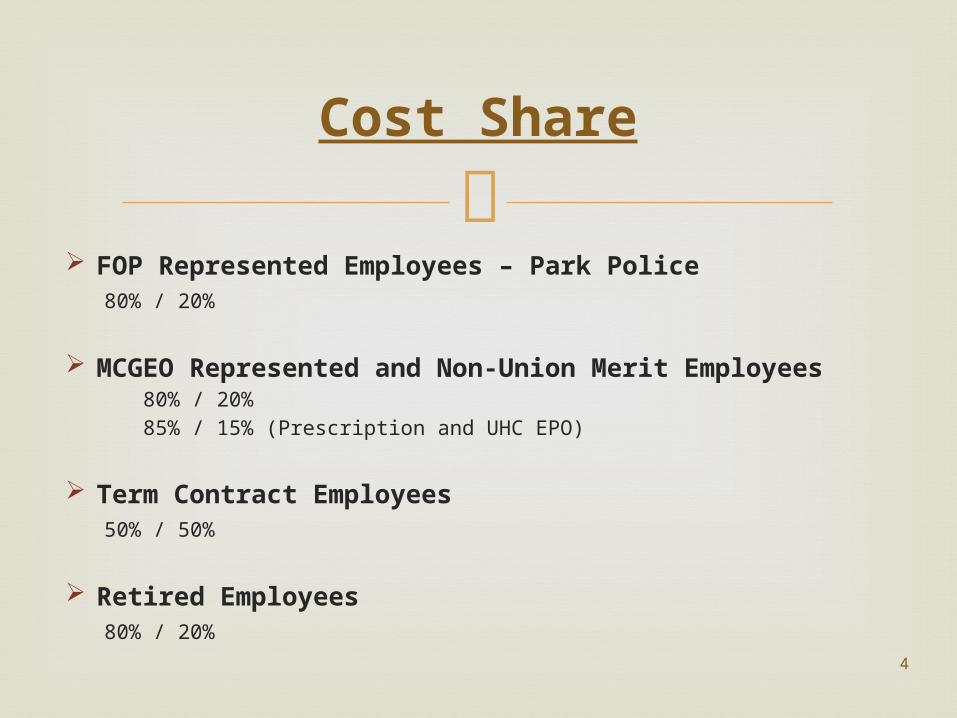

Cost Share

FOP Represented Employees – Park Police80% / 20%

MCGEO Represented and Non-Union Merit Employees

80% / 20% 85% / 15% (Prescription and UHC EPO)

Term Contract Employees50% / 50%

Retired Employees80% / 20%

5

Rate Changes

Self-Insured Plans

CIGNA Open Access Plus EPO – 0%

UHC EPO – 0%

UHC POS – 5.6% increase ($2.77 bi-weekly for single)

Prescription Plan – 14.8% increase ($1.53 bi-weekly for single)

UHC Medicare Complement – 25.7% increase ($10 monthly for single)

6

Rate Changes

Fully Insured Plans

Vision Service Plan – 19.8% increase ($0.06 /$0.30/$0.54 bi-weekly)

United Concordia Dental – 0%

CIGNA Long Term Disability (LTD) FOP Plan – from $1.84 to $2.13 per $100 of benefit Non-FOP Plan and Supplemental LTD – 0%

Minnesota Life and Accidental Death & Dismemberment – 0%

Legal Resources – 0%

7

Benefit Changes

8

Benefit Plan Changes

Dental and Vision Coverage for Young Adults Effective January 1, 2015, M-NCPPC will extend

dental and vision coverage for young adults up to age 26 without proof of full-time student status to coincide with medical coverage

Employees may add previously terminated and new dependents by completing an enrollment form and submitting a copy of the birth certificate.

9

Benefit Plan Changes

Vision Coverage We are switching from Vision Service

Plan’s Signature plan to their Choice plan, providing a greater benefit for covered services, but reducing the discount for non-covered items. Allow lenses every 12 months instead of

24 months for the Moderate Option Allow eye exams every 12 months

instead of 24 months for the Low Option

10

Benefit Plan Changes

Vision Coverage Increase the frame allowance from $130 to

$200 for the High Option and from $130 to $150 for the Moderate and Low Options

Increase the contact lenses allowance from $130 to $150 for the High Option and keep at $130 for the Moderate and Low Options

Lower the discount on non-covered lens options from 35-40% to 20-25%. The member’s maximum out-of-pocket expense for these lens options will increase; e.g. $37 to $41 for anti-reflective coating and $23 to $31 for polycarbonates.

11

Benefit Plan Changes

Sick Leave Bank

Current members of the bank will not have to contribute hours to participate for 2015

New members will have to contribute required hours

12

Benefit Plan Changes

UHC SELECT EPO The schedule of when mammograms are covered was

changed back in 2012 to mirror the schedule under the UHC Choice POS plan but it was never communicated

Mammograms were previously covered every year The new frequency limits follow the current Maryland

Mandate for mammograms Ages 35-39, one baseline Ages 40-49, one every 2 years Ages 50+ - annually

13

Specialty Drugs Step Therapy

Specialty drugs are medications that are used to treat specific low-incidence chronic and/or genetic conditions.

Similar to the generic step therapy implemented this year. We are implementing this for the following three specialty drug classes Auto-Immune, Multiple Sclerosis and Infertility

Members must try a lower cost drug for 30 days before they are approved for the higher cost drug.

14

Specialty Drugs Step Therapy

The step therapy will apply only to new users of a medication.

When a prescription for one of the targeted specialty drugs is presented to the pharmacy, the pharmacy will check for previous use of an appropriate lower cost alternative.

15

Prior Authorization for Compound Drugs

Compounding is the combining, mixing, or altering of ingredients to create a customized medication that is not otherwise commercially available.

We are implementing a Prior Authorization for compounded medications with an ingredient cost exceeding $300

The PA criteria require that any individual ingredient component being requested must be FDA approved in the same finished dosage form of the compound. For example, if an ingredient is not approved for topical

use, it will not be approved for topical use within a compound.

16

Prior Authorization for Compound Drugs

When a member presents a prescription that requires PA to the pharmacy, the pharmacist will advise the member that their physician will need to call Caremark.

If the prescribed therapy meets nationally approved clinical guidelines then the prescription will be approved.

Our current drug program already has the PA process in place for other drugs such as medications for acne, antifungals, anabolic steroids, testosterone and erectile dysfunction.

Compounded drugs prescribed to treat any non-covered condition will be rejected.

17

Pharmacy Advisor Program

The Pharmacy Advisor Counseling program helps improve members’ health through one-on-one pharmacists counseling (face to face and by phone), tailored messaging, and coordination with health care providers at the most critical point in therapy.

This program reinforces adherence from the first time a prescription is filled and throughout recommended usage, and closes gaps in care for the 10 most prevalent and costly chronic conditions: Diabetes Hypertension Dyslipidemia (High Cholesterol) Coronary Artery Disease Congestive Heart Failure Asthma Coronary Obstructive Pulmonary Disease (COPD) Depression Osteoporosis Breast Cancer

18

Pharmacy Advisor Program

In addition to improving adherence and closing gaps in care, the program identifies potential drug interactions and other safety concerns such as managing potential non-critical side effects. When a member presents a prescription to be filled,

based on his or her prescription history, the pharmacist will consult with the member if he or she determines that other prescription regimens are missing, if the member is not refilling prescriptions in a timely manner, or if there potential side effects.

The pharmacist may contact the member’s physician for additional information or refer the member to his or her health plan’s disease management program.

19

SilverScript Medicare Part D

The prescription plan for Medicare eligible retirees and employees on long term disability (LTD) who are eligible for Medicare will be converted to a Medicare Part D prescription plan.

The administrator of the prescription drug program for retirees, LTD employees and their dependents who are on Medicare will change from CVS/Caremark to SilverScript® Insurance Company, a CVS/Caremark company.

SilverScript® is a Medicare Part D group prescription plan. This new plan is a combination of two separate plans called an Employer Group Waiver Plan (EGWP) + Wrap Plan.

20

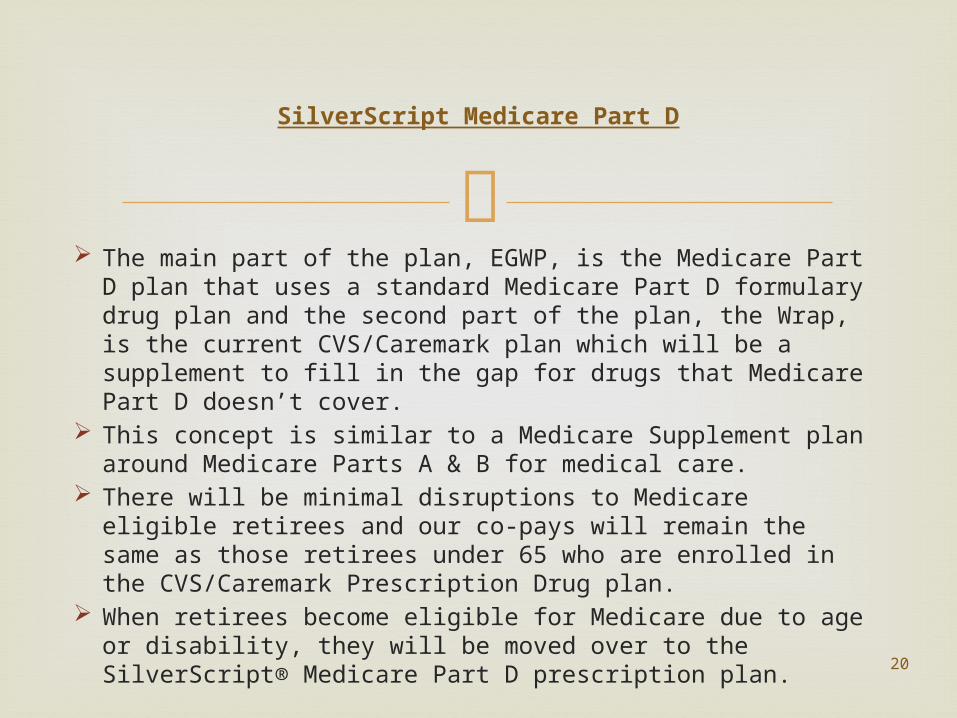

SilverScript Medicare Part D

The main part of the plan, EGWP, is the Medicare Part D plan that uses a standard Medicare Part D formulary drug plan and the second part of the plan, the Wrap, is the current CVS/Caremark plan which will be a supplement to fill in the gap for drugs that Medicare Part D doesn’t cover.

This concept is similar to a Medicare Supplement plan around Medicare Parts A & B for medical care.

There will be minimal disruptions to Medicare eligible retirees and our co-pays will remain the same as those retirees under 65 who are enrolled in the CVS/Caremark Prescription Drug plan.

When retirees become eligible for Medicare due to age or disability, they will be moved over to the SilverScript® Medicare Part D prescription plan.

21

Paper Reduction Initiative

22

Paper Reduction

Everyone should have received a letter from Patti Barney announcing open enrollment and changes

All open enrollment documents and forms are available on our website at www.mncppc.org or on our intranet, inSite, by clicking the link for 2015 Open Enrollment.

Those that don’t have access to the internet may

request a hard copy of the enrollment packet or a specific form from local benefits coordinators or the Health & Benefits Office.

Open Enrollment Guide Employee Benefits Handbook Schedule of Open Enrollment meetings Excerpt of Benefit Changes and Highlights Contribution Rate Sheets Supplemental Information for Retirees Summary of Benefits Coverage (SBC) for each health plan Application for Benefits Enrollment Form Flexible Spending Form – Must complete each year Sick Leave Bank Form – Use only if enrolling for the first time Legal Resources Form - Use only if enrolling for the first time

Documents Online

your HEALTH · your MEDICAL · your DENTAL

your INSURANCE · your FLEXIBLE SPENDING

your BENEFITS · your CHOICES

YOUR 2015

OPEN ENROLLMENT

October 20 through November 7

Open Enrollment Link

25

Life Insurance

26

Supplemental Life Insurance

Currently, the maximum is 3 times salary capped at $300,000

Employees can now elect supplemental life insurance up to five times their base salary up to a maximum of $750,000.

This will be a good time to enroll in life insurance if not already covered. Proof of good health is required before coverage is approved

A special enrollment will take place during the first quarter of 2015, but employees can enroll at anytime during the year

27

Dependent Life Insurance

Current coverage for spouses and children: $2000 for spouse and $1000 for each child at a flat rate of 43 cents per month

Increased coverage options starting 3/1/15. $10,000/$5000 at 2.45 per month $20,000/$10,000 at 4.90 per month $30,000/$15,000 at 7.35 per month

Proof of good health is required for spouses for option 3 only, none is required for children up to age 26

A special enrollment will take place during the first quarter of 2015

28

Flexible Spending

29

Flexible Spending Accounts

The purpose of flexible spending accounts is to reduce your taxable income by paying for certain health care and dependent care on a tax-free basis

Deductions are taken from your pay before taxes are applied, reducing your taxable income

Yearly limits for health care expenses is $2,500 and $5,000 for dependent care expenses

30

Flexible Spending Accounts

Must enroll every year

Dependent care is for dependents under age 13

Must use by March 15th following the end of the plan year and submit claims by March 31st

Unused amounts are forfeited

FSA decision tool is posted online

31

Open Enrollment & Qualifying Life Events

32

Open Enrollment Process

Open Enrollment starts 10/20/14 and ends 11/07/14 at 5:00P.M.

This is the time you can add, drop or change plans; and remove or add dependents

Paper Reduction Initiative In preparation for Employee Self Service Forms must still be submitted to the Health & Benefits

office Request copies from benefit coordinators or the Health

& Benefits Office if you don’t have access to a computer

33

Open Enrollment Process

If adding a dependent (child and/or spouse) please submit a copy of the birth certificate and/or the marriage certificate.

Complete a Legal Resources and/or Sick Leave Bank enrollment form if terminating coverage or enrolling for the first time. These benefits automatically rollover

You must re-enroll in the Flexible Spending Accounts (FSA) every open enrollment period (even if you are not making changes)

If applying for Domestic Partner Benefits (DPB), employees must the complete DPB Affidavit and enrollment application. Employees currently enrolled with a domestic partner must submit the Domestic Partner Certification form and enrollment application.

34

Open Enrollment Process

All forms must be submitted by 11/07/14, close of business, 5:00P.M.

Forms may be submitted in the following manner Interoffice mail Hand deliver Certified mail Overnight carrier Email to [email protected]

Don’t send to individual specialists Fax to 301-454-1687

Except for FSA, if you are not making any changes, YOU DO NOTHING!!!

35

Qualifying Life Events

Your marriage or divorce, annulment, or legal separation;

Your child’s marriage, divorce or annulment; A birth, adoption or change in a child's custody; A change in your or your spouse's or child’s

employment status, including part-time, full-time or retirement;

A change in your or your spouse's insurance (cost or coverage);

Commencement of or return from an unpaid leave of absence taken by you or your spouse;

Your dependent child no longer meets the eligibility requirements of a dependent;

36

Qualifying Life Events

The death of your spouse, domestic partner or child;

Your relocation out of your plan’s coverage area;

Your domestic partnership ends; Your spouse’s open enrollment period; A change in dependent eligibility due to a

plan design change; A change in the dependent care

arrangements; A change in eligibility for a Commission plan

(i.e. Medicare Complement Plan)

37

Qualifying Life Events

What should I do if I have one of these events – complete an application for benefit enrollment and submit to H&B within 45 days

If I fail to act during this period what is my recourse – failing to act means you wait until the next open enrollment period to make changes

Are there any special circumstance that allow me to enroll outside of the 45 days – NO!!!! Employees must act within the 45 day period or wait until the next open enrollment period.

38

Qualifying Life Events

We continue to learn of employees who fail to add newborns timely or drop a spouse after a divorce. It is imperative that you notify the Health & Benefits office within 45 following any qualifying event if you wish to add, drop or make changes to your current elections Failure to act in a timely manner will cause you unnecessary expenses for which you will be responsible. If you are unsure contact the H&B staff and we can answer any questions surrounding a qualifying event. Do not rely on co-workers’ or doctors office staff’s advice.

39

Questions ?

Answers