week 10: accounting process mis2101: management information systems based on material developed by...

TRANSCRIPT

Week 10:

Accounting process

MIS2101: Management Information Systems

Based on material developed by C.J. Marselis

2

Introduction

Accounting tightly integrated with other functional areas PurchasingMarketing and SalesSupply Chain Management

Accounting activities are necessary for decision making

3

Types of Accounting

Financial Accounting Documents all transactions that impact the firm Uses this transaction data to make external reports for

various agencies (FASB, SEC, IRS) Managerial Accounting

Determine profitability of a company’s activities Managerial information is used for planning and to

control a company’s day-to-day activities Tax Accounting

Specialized field that uses Financial Accounting information

4

Financial Accounting Statements

Income Statement

Shows sales, cost of sales and overall profit for a period of time

(quarter, year)

Balance Sheet

Shows account balances Picture of the overall financial

health of a company

5

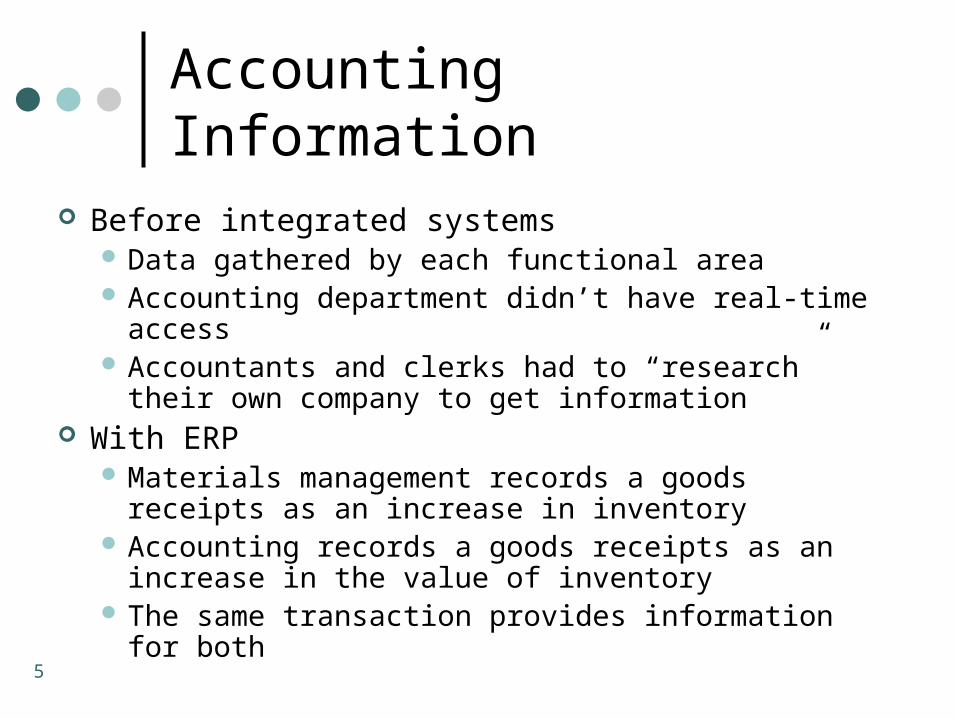

Accounting Information

Before integrated systems Data gathered by each functional area Accounting department didn’t have real-time access Accountants and clerks had to “research” their own

company to get information With ERP

Materials management records a goods receipts as an increase in inventory

Accounting records a goods receipts as an increase in the value of inventory

The same transaction provides information for both

6

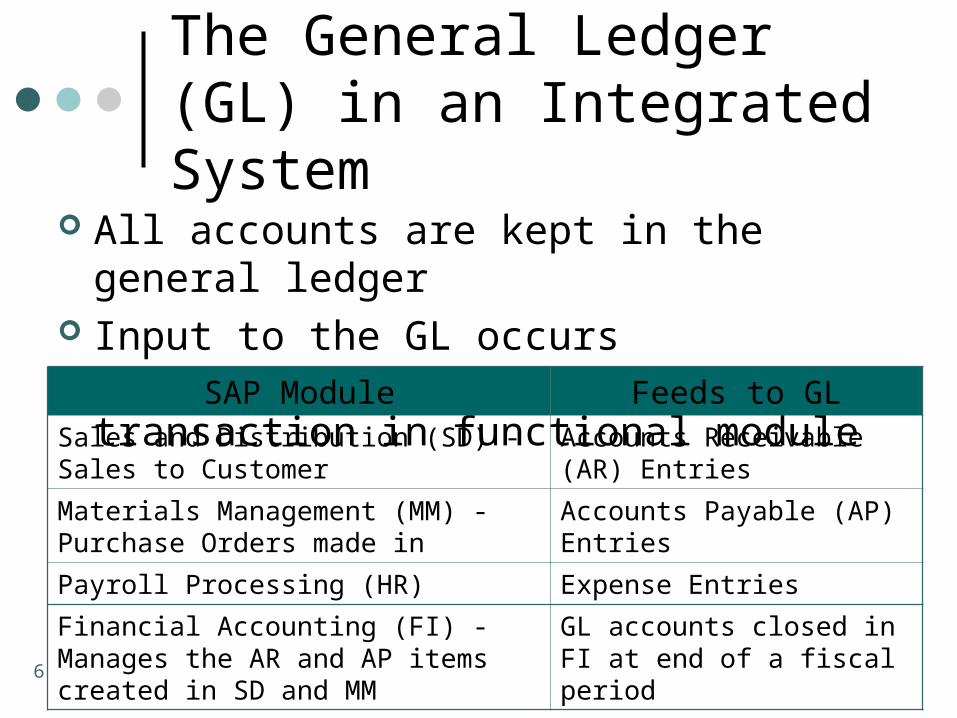

The General Ledger (GL) in an Integrated System

All accounts are kept in the general ledger Input to the GL occurs simultaneously with

business transaction in functional moduleSAP Module Feeds to GL

Sales and Distribution (SD) - Sales to Customer

Accounts Receivable (AR) Entries

Materials Management (MM) - Purchase Orders made in

Accounts Payable (AP) Entries

Payroll Processing (HR) Expense Entries

Financial Accounting (FI) - Manages the AR and AP items created in SD and MM

GL accounts closed in FI at end of a fiscal period

7

Accounting Data and Profitability Analysis

Inaccurate or incomplete data leads to flawed analysis

3 main causes of data problemsInconsistent record keeping

• Much of work done manually including analyses• Manual entry leads to errors

Inaccurate inventory costing Problems consolidating data from subsidiaries

8

Inaccurate Inventory Costing Systems

Inventory is expensiveCost of raw materials used in the itemLabor used specifically to produce the product

(direct labor)Overhead (all other costs)

• Factory utilities• General factory labor (custodial services, security)• Manager’s salaries• Storage• Insurance

9

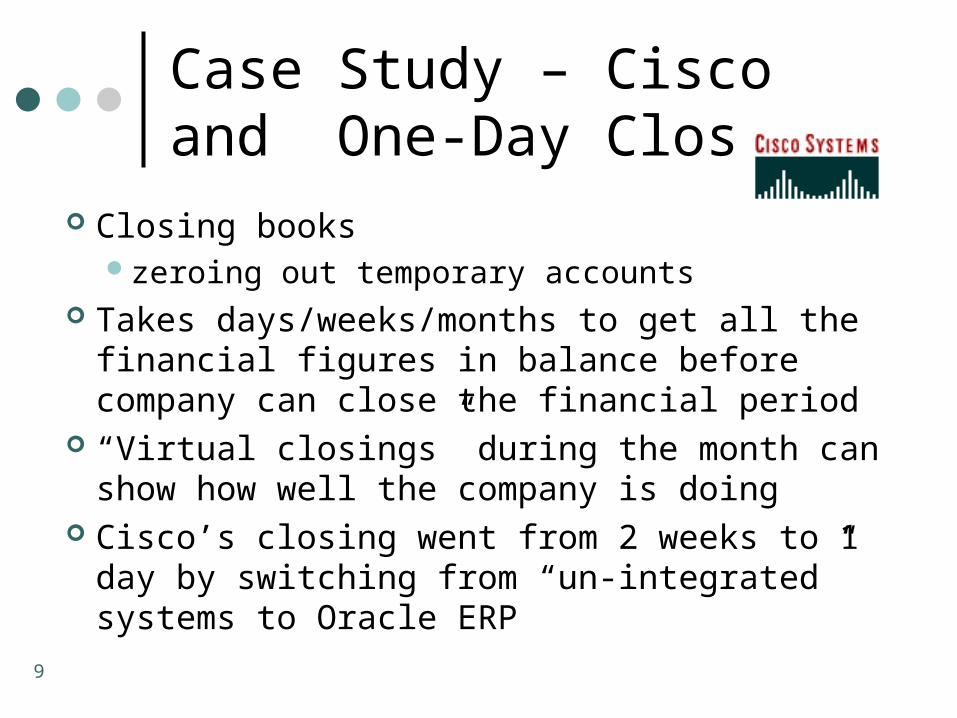

Case Study – Cisco and One-Day Close

Closing bookszeroing out temporary accounts

Takes days/weeks/months to get all the financial figures in balance before company can close the financial period

“Virtual closings” during the month can show how well the company is doing

Cisco’s closing went from 2 weeks to 1 day by switching from “un-integrated” systems to Oracle ERP

10

Even More Complicated for Companies with Subsidiaries

Must prepare Financial statements for each subsidiary Consolidated statement for entire company

Different currencies and transactions Must consider changes in exchange rates Sales from one subsidiary to another within a

company do not result in a profit or loss, because no money has entered or left the consolidated company

11

Case Study: Microsoft

Microsoft consolidates financial information from 130 subsidiaries

Pre-SAP: each subsidiary had separate accounting Each used different systems, with different field sizes,

types of characters, account structures Transmitted the files to another system where

manipulation of the data was required Consolidation took over a week

With SAP: Microsoft can look directly at financial activity at any subsidiary around the world

12

Enron Collapse

Energy company revolutionizing the oil and gas business On Oct. 16, 2001, Enron’s creative financial arrangements

began to unravel On Dec. 2, 2001, Enron made the largest bankruptcy filing

in history Key cause: Enron’s partnerships shifted billions of debt off

Enron’s books so Enron could borrow money more cheaply Arthur Andersen:

Respected accounting firm with firm with 28,000 employees - issued annual reports attesting to the validity of Enron’s financial statements

Arthur Andersen indicted for, among other things, destruction of Enron documents

13

Results of Enron Collapse

Enron’s 20,000 creditors will receive approximately 20% of the $63 billion they are owed

Shareholders will receive nothing Many employees invested large sums of money in

Enron stock via 401K savings plans Arthur Andersen dismantled 31 individuals either have been tried or will be

tried on criminal charges The Sarbanes-Oxley Act was passed

14

Sarbanes-Oxley Act of 2002

Requires public company’s annual report contain management’s internal control report

Must include documentation of controls An integrated information system provides

tools to implement internal controlsBut controls cannot necessarily prevent effort

to circumvent standard processes But companies with ERP systems will have

an easier time complying with Sarbanes-Oxley

15

Archiving And Fraud Detection

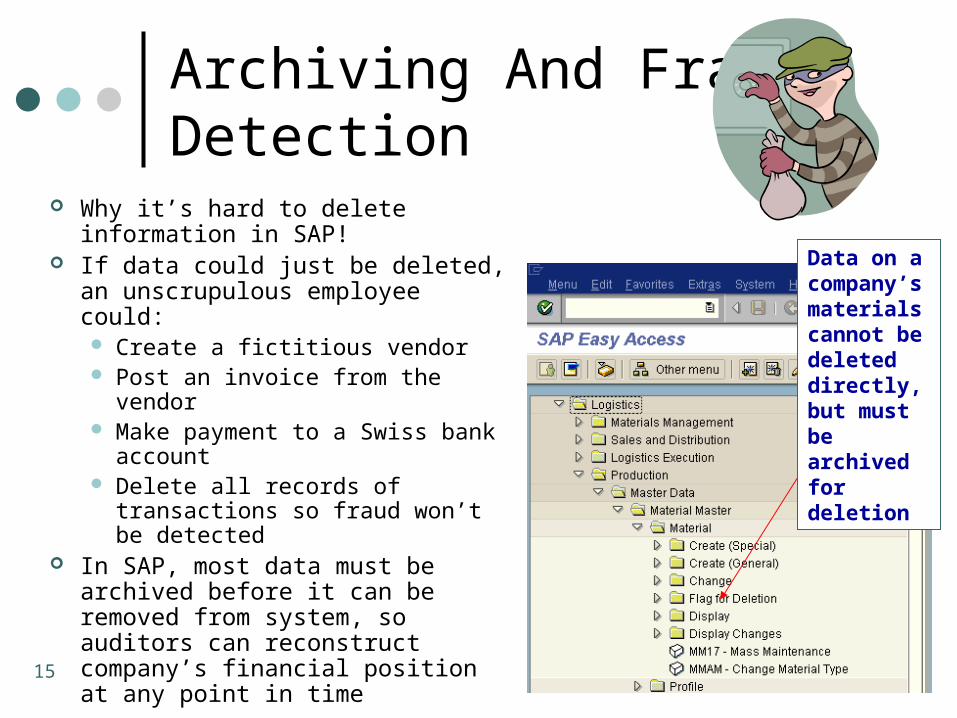

Why it’s hard to delete information in SAP!

If data could just be deleted, an unscrupulous employee could: Create a fictitious vendor Post an invoice from the vendor Make payment to a Swiss bank

account Delete all records of

transactions so fraud won’t be detected

In SAP, most data must be archived before it can be removed from system, so auditors can reconstruct company’s financial position at any point in time

Data on a company’s materials cannot be deleted directly, but must be archived for deletion

16

Integrated System (like an ERP) and Fraud Detection

Changes to data are tracked

SAP R/3 maintains detailed records on all changes made to material master data

17

Integrated System (like an ERP) and Fraud Detection

User authorization More than one employee often

required to perform critical business processes

Employees can only perform transactions required for their job

SAP’s “Profile Generator” used to create user authorizations based on the functions (transactions) user should be allowed to perform

18

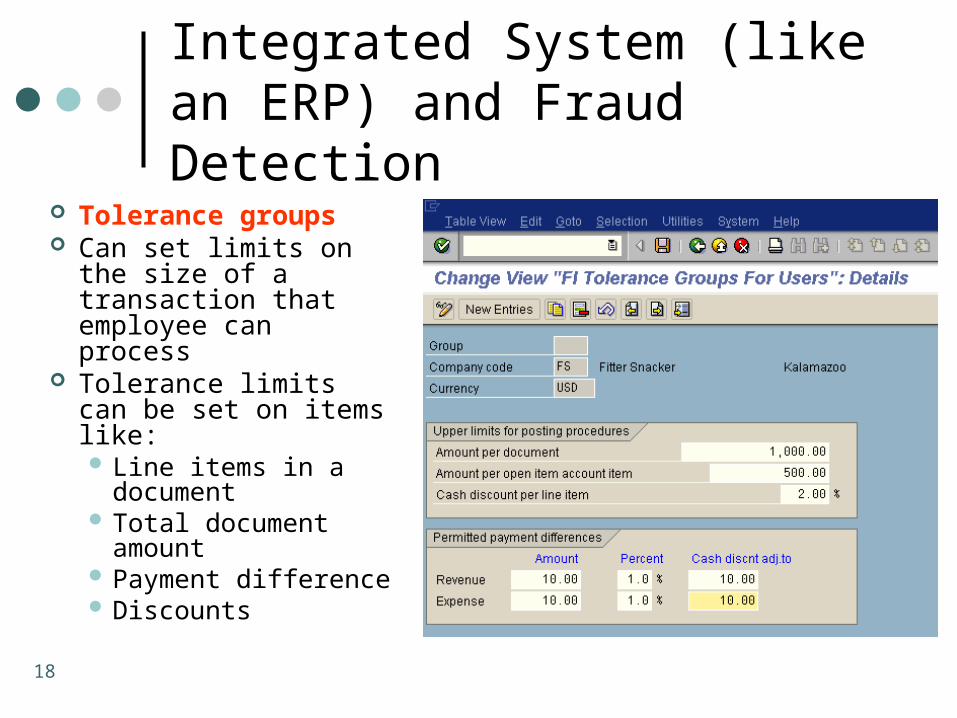

Integrated System (like an ERP) and Fraud Detection

Tolerance groups Can set limits on the

size of a transaction that employee can process

Tolerance limits can be set on items like: Line items in a

document Total document

amount Payment difference Discounts

19

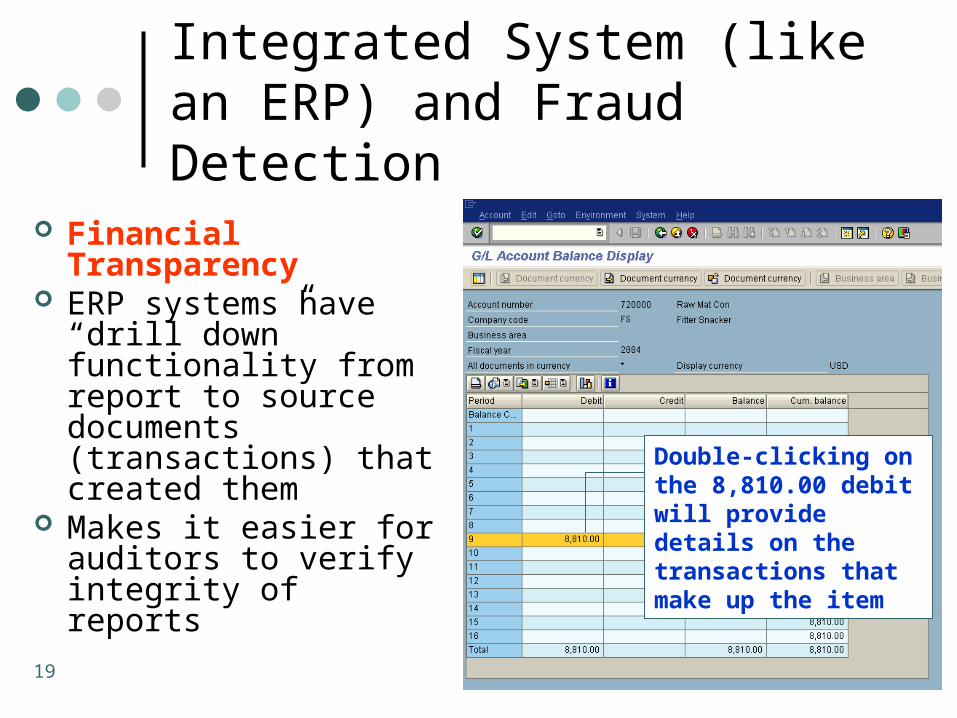

Integrated System (like an ERP) and Fraud Detection

Financial Transparency

ERP systems have “drill down” functionality from report to source documents (transactions) that created them

Makes it easier for auditors to verify integrity of reports

Double-clicking on the 8,810.00 debit will provide details on the transactions that make up the item

20

Line items linked…

Figure 5.12 Documents that make up G/L Account Balance for Raw Material Consumption

Selecting the 10.00 item and clicking on the details icon will provide more information on the item

21

…to the documents that created them

Figure 5.13 Details on $10.00 line item in G/L account for raw material consumption

22

Summary

Companies use accounting systems to record transactions and generate financial statements

Should have ability to summarize data to assist managers in their daily and strategic work

With “un-integrated” systems, accounting data might not be current

Integrated IS with common database to record accounting data facilitates inventory benefits

Compliance with Sarbanes-Oxley Act facilitated with integrated systems