€¦ · web viewfreeing up orbitz from agreements with worldspan that restrict supplier link usage...

TRANSCRIPT

I’m actually penning (beginning to type) on this as I sit in the Minneapolis St. Paul airport in the middle of the afternoon of the 30th – running well behind on my normal end-of-the-month summary. I have spent the early part of the day attending the regional ACTE Forum conference here … and participating on the GDS deregulation Panel. Since I’ve pretty well off-loaded my current thinking about the impact of GDS deregulation over the past two OTWCs … I’ll not bore you with more; although I do have some thoughts on one of Jack O’Neill’s comments during his luncheon presentation today. But first … to the issue of the moment … the Orbitz acquisition by Cendant!

Eastman's "Off-the-Wall Comment(s)"© ...

As with last month’s lead regarding the Northwest gambit … let’s start with the disclaimers first. I have friends, clients and associates on all sides of this transaction; many of whom get OTWC. Accordingly, what follows is a personal opinion that reflects the trends as I see them -- and an effort to explain why those trends are or will evolve,

The snippet above was one of more than 20 that I captured from various sources, including a Word document/copy identified as the “approved final” of the news release distributed to the press by Orbitz. Virtually all of the media stories paraphrased the Orbitz (or I’m sure, equivalent Cendant) release – that …

The deal was worth $1.25 billion in cash, or $27.50 per Orbitz share. That Cendant also owns Galileo, CheapTickets, Travelport, various other

travel technology brands; Avis and Budget car rental firms; several hotel brands including Ramada, Howard Johnson and Days Inn (depending on the story and its emphasis)

The Orbitz management team is a great addition to the Cendant team The deal had been approved by both Boards subject to regulatory

approvals That Jeff Katz, President of Orbitz is not related to Samuel Katz, CEO and

Division Chairman of Cendant

The Financial Times of London expanded its financial analysis to reflect on the potential impact of the purchase on both e-Bookers, Opodo, and Amadeus … two online travel or

_____________________________________document.doc Page: 1

All rights reserved by The Eastman Group Incwww.eastmangroup.com

Eastman’s Off the Wall Comments©

From FT.Com© (Financial Times), September 29, 2004Cendant confirms Orbitz.com deal. Cendant Corporation, the travel and property services company which owns Avis and Budget, said on Wednesday it would acquire Orbitz.com, the online travel company, in a deal worth about $1.25bn.

GDS competitors to Orbitz and/or Cendant in Europe that are purported to be “in play” with various investors.

Jay Campbell, who authors “The Beat” [[email protected]] provided probably the most insightful and poignant (as in pleasantly stimulating) piece on the proposed merger – in that he went beyond the basic reprinting of the financial impact to make six points. They are, in his words …

Such a transaction carries a wide range of implications, not the least of which is delivering to Cendant a more solid consumer web presence than it had achieved through CheapTickets and Trip.com.

If the deal goes down, the industry's most diversified vendor will make decisions that reshape travel distribution. For one thing, it looks like Atlanta-based Worldspan may lose yet another chunk of online agency business. Orbitz is under contract to book in the Worldspan global distribution system a quarterly minimum of 16 million segments, which most likely will be moved to Cendant's Galileo’

Cendant also will decide the fate of Orbitz' Supplier Link direct connection program. Having an alternative to global distribution system connectivity would put Cendant in a driver's seat to help break the ongoing GDS-to-travel agency incentive cycle.

Freeing up Orbitz from agreements with Worldspan that restrict Supplier Link usage could pave the way for its implementation through Orbitz For Business, if not also Cendant's Galileo GDS and Travelport. More than 40 percent of Orbitz' air bookings are made through Supplier Link even with the commitment to Worldspan. That could explode if Cendant made an attractive offer to its agency subscribers that also allowed airlines to pay something less than what Galileo gets now.

This is not to say that Cendant would definitely keep Supplier Link. The direct connect programs at GetThere and E-Travel hit the back burner after Sabre and Amadeus, respectively, bought them in 2000 and 2001. If Cendant dropped Supplier Link and pushed all those transactions through Galileo, that could mean more than $200 million in added annual revenue.

Most likely, though, Cendant would not trash an instant answer to the airlines' recently elevated GDS wrath--not to mention the so-called GDS alternatives that are on the horizon.

Prior to Jay’s message above, Chris Elliott (who writes a number of industry and Internet media columns including “Ombudsman” for National Geographic Traveler and others … see [http://www.elliott.org] ) posed some questions to me which I pass along … paraphrased … with my responses.

<<Samuel Katz suggests that the acquisition provides "… considerable benefits to both customers and our shareholders." Does the acquisition benefit consumers? >>

Actually, I suspect that it should benefit consumers in the very near future for two reasons. First ... Orbitz (and Travelocity, for that matter) has had some difficulty competing with Expedia in capturing cost-effective hotel pricing with margins that would sustain aggressive hotel marketing. Cendant is a hotel-owner/franchiser -- and with Cendant backing, will likely evolve Orbitz into a very early truly dynamic-packaging e-

_____________________________________document.doc Page: 2

All rights reserved by The Eastman Group Incwww.eastmangroup.com

travel solution. Orbitz has direct gateways to key airlines that even Expedia can't match -- so the ability to interactively package direct purchase solutions becomes a real advantage to technology literate buyers. Second ... through this acquisition, it would appear to me that Cendant is clearly intending to compete head-to-head with IAC … pitting its “franchise model” against IAC’s “digital brands distribution” model. That will drive rapid innovation throughout the distribution segments of the travel industry and, concurrently, prices to consumers will become increasingly competitive as the two drive for dominance in digital distribution of commodity travel products and the necessary “dynamic repackaging” necessary to enhance supplier/vendor margins.

<< Are there any drawback to the acquisition in your perspective? >>

I’m still pondering … but nothing that is glaring...There are some concerns … issues like how the airlines will respond to direct booking by Cendant and/or will Cendant try to shut down the direct bookings and funnel them through Galileo for the segment revenue (very doubtful in my view; but also a consideration of Jay Campbell above). But I don’t see any major drawback at the moment. As I see it, over the next two years this merger will leverage the Internet and other tools of the information hyperarchy up a level – or more likely, three levels! The transactional manual packaging of travel will become digitized. Dynamic digital packaging will tear aggressively at the heard of the core business model of the corporate travel service providers (the Travel Management Companies or TMCs) and traditional GDSs. Both TMCs and GDSs will be forced to re-engineer their own business processes … either piggybacking on the current ITMCs (Internet TMCs) or building new more competitive tools. It won’t be just the small agencies that will feel the squeeze!

Another “up-level” that will likely evolve from this acquisition will be an expansion of direct-booking solutions at air, hotel, car, and a number of other travel-related vendors. Such direct booking will force dynamic packaging technologies further down (or up … depending on your view) the distribution food-chain – into the hands of TMCs, ITMCs, and/or travel agencies, tour and cruise operators with volumes big enough to get solid ROIs (return-on-investment) through shortening the distribution channel process. And yet a final “up-level” result of this acquisition will be more and more direct settlement; settlement that by-passes ARC and even credit card companies.

Accordingly, in my view, the greatest impact will be on the traditional GDS distribution model and those dependent on that structure! I expect one or more of the remaining GDSs will swoop in and “gobble up” that new Switchworks G2 offering – in an effort to stay in the game. And Sabre will have to leverage their product offerings up four or five levels to stay in the game. It would appear to me that if this deal is actually culminated, it will be the beginning-of-the-final-end-game for the traditional GDS distribution structure.

<< If Cendant owns Avis, Budget, Ramada and other travel companies, will buyers be comfortable trusting Orbitz? >>

A legitimate question! But for the competitive reasons noted in the answer to your first question, I expect that over time, anything that travelers find on Orbitz will be fairly and competitively priced. The problem with “selective pricing” is that the Internet is

_____________________________________document.doc Page: 3

All rights reserved by The Eastman Group Incwww.eastmangroup.com

ubiquitous and getting even more-so – thus, distorted prices are very easily identified and discarded except by the very naïve or technologically incompetent. Further, technology is improving to the point that such distortions are increasingly identified by automated auditing or monitoring tools.

In my view, neither Cendant nor Orbitz can allow those distortions to happen in the public domain. That is not to say that they won’t be the conduit of negotiated vendor-direct solutions; but neither can afford to long allow a pricing disparity in the ubiquitous hyperarchy of information without damaging their respective brands. That is, among other reason, why I believe that digital dynamic packaging MUST evolve – to protect public brand pricing!

However, I do expect that over time, Orbitz will tend to reflect the “franchise” pricing that Cendant is making available through its Galileo travel agency distribution channels. Franchising and franchise pricing appears to be a core strategic initiative of Cendant management. It would be illogical to think that Orbitz and users of the Orbitz environment would not be similarly incentivized. I also expect that Orbitz will become a very aggressive Galileo travel agency distribution center – possibly replacing or eliminating the traditional Galileo distribution channel (at least technologically) in three to five years. How the “brand name game” will play out is a matter of speculation – but as the story on the merger that appeared in Information Week implied … one of the reasons (paraphrased) for the Orbitz acquisition by Cendant is to aggressively replace the archaic and dieing legacy technology platforms of the traditional Galileo platform. << Do you expect any antitrust or anticompetitive issues to arise? >> I would be very, very surprised if antitrust or anticompetitive issues surfaced to the point that they got any serious attention from the DOJ! Remember, under de-regulation, DOJ now handles airline product distribution antitrust issues (not DOT as in the past). DOT’s “oversight” would be limited solely to the airline issues … which implies only issues pertaining to direct-connect links. The GDSs are no longer owned by airlines in this country, and thus, the DOJ becomes the government oversight agency. DOJ would only consider issues that would be “normal” in all aspects of commerce … not peculiar to the travel industry. It is hard to see the Cendant/Orbitz (or IAC/Expedia or Sabre/Travelocity) as any kind of an antitrust or anticompetitive “threat” in the new wide-open world in Internet e-commerce. There is just too much evolving in the digital e-travel world for anybody to sustain such a claim. I suspect that some – particularly vocal – “mom and pop” agencies (and their trade groups) will rise up in arms; but it’s because these agents are now even more threatened by the new digital knowledge era – not because of any antitrust or anticompetitive control that might be exercised by this new affiliation. The new buyer-driven consumer distribution tools are rapidly replacing the traditional distribution channels because they are more cost effective and competitive; and thus, in demand by buyers. But these solutions also erode the margins of small agencies still dependant on manual (human-based) transaction processing. And those margins will continue to erode as long as agencies try to insert people into the transaction processing function! But new technology replacing old human processes is not a legitimate antitrust or anticompetitive issue; albeit an emotional one for many.

_____________________________________document.doc Page: 4

All rights reserved by The Eastman Group Incwww.eastmangroup.com

In summary, the acquisition of Orbitz by Cendant is probably a win-win situation for just about everybody except the small agency. The investors in Orbitz (including the airline owners) are getting a premium for their shares. The investors in Cendant gain a new dimension that strengthens the company’s strategic and tactical initiatives (although I heard their stock slipped initially). Vendors, due to the evolving competitive hegemony of digital transaction processing in the service of consumer needs, should find their distribution costs lowered. Consumers should benefit from the ever increasing competitive environment through either lower prices and/or better dynamic packaging of their travel needs (keeping in perspective that many people shop convenience or efficiency in lieu of just low price).

Eastman's "Off-the-Wall Comment(s)"© ...

Now Jack is very bright (you don’t get to head a major agency without being a bright guy) … and a valued reader of OTWCs! Still, in his perception of the future role of GDSs in travel distribution, I have some concerns. Those concerns are three-fold:

1 … acquisitions and the rule-of-three2 … the hub-centric network model versus nodal networks3 … content providers versus context retrieval systems.

OTWC readers will have noted my past used of management guru Peter Drucker’s observation that (paraphrased), "When major players in an industry buy smaller, growing companies, the industry itself is growing. When major players in an industry merge ... the industry is topping out and profit margins are incrementally improved only through consolidating overhead”.

If one looks at the TMCs (Travel Management Companies … the mega corporate travel agencies), the major players are “merging” as the TMCs seek incremental improvement through consolidated overhead. The TMCs are, of course, the virtual extensions of the GDSs. This would suggest that the TMCs … and thus, the GDSs … have reached a point of “topping out.”

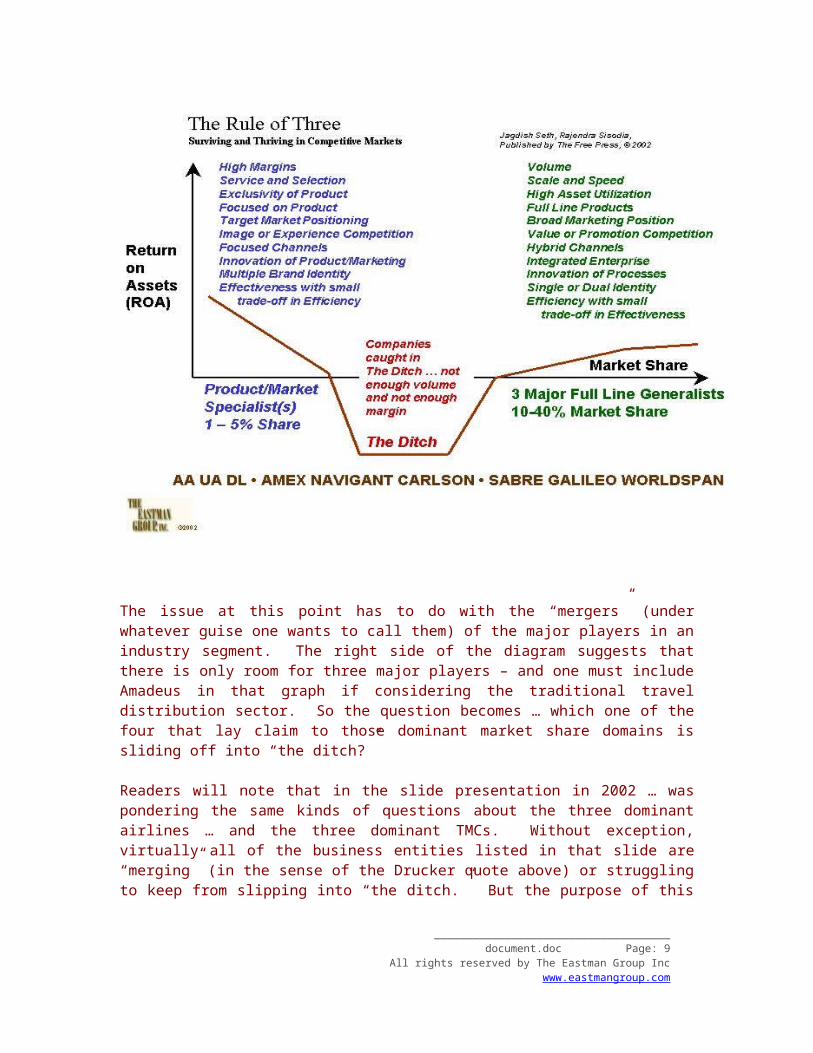

Jack suggested the possibility that the GDSs would soon fall into the “Rule of Three”, which has also been discussed in prior OTWCs. The premise of the “Rule-of-Three” is depicted in one of my slide presentation diagrams and presented below – the premise having originated from the book of the same name by Jagdish Seth and Rajendra Sisodia. While my two year old slide interpretation depicts Sabre, Galileo, and Worldspan as the “three” GDSs … the presentation at the time focused on U.S. GDSs;

_____________________________________document.doc Page: 5

All rights reserved by The Eastman Group Incwww.eastmangroup.com

From Jack O’Neill, COO North America, Carlson Wagonlit TravelKeynote Luncheon Comments to ACTE Executive ForumMinneapolis, MN, September 30, 2004In discussing the future of GDSs (paraphrased from notes), Jack said, “While GDSs will change their pricing models, they will survive as centers for travel product distribution in the future. As airline and other travel products continue to fractionalize, distribution will consolidate around the GDSs.”

and did not include Amadeus. Depending on how one might interpret today’s real-world – Galileo is no longer a GDS survivor; no longer a member of the GDS “Rule-of-Three” … having been replaced by Amadeus. Review the chart and pick up on this thread thereafter.

The issue at this point has to do with the “mergers” (under whatever guise one wants to call them) of the major players in an industry segment. The right side of the diagram suggests that there is only room for three major players – and one must include Amadeus in that graph if considering the traditional travel distribution sector. So the question becomes … which one of the four that lay claim to those dominant market share domains is sliding off into “the ditch?”

Readers will note that in the slide presentation in 2002 … was pondering the same kinds of questions about the three dominant airlines … and the three dominant TMCs. Without exception, virtually all of the business entities listed in that slide are “merging” (in the sense of the Drucker quote above) or struggling to keep from slipping into “the ditch.” But the purpose of this comment is to address the GDSs specifically … and the TMCs in their linked relationship with the GDSs.

_____________________________________document.doc Page: 6

All rights reserved by The Eastman Group Incwww.eastmangroup.com

There was an interesting piece that appeared in the September 22 Wall Street Journal which said, << Worldspan Technologies Inc. and Galileo International Inc. have approached core shareholders in Amadeus Global Travel Distribution SA about buying their stakes, challenging private-equity firms already pursuing the Spanish computerized-reservation company, people familiar with the situation said. >> Given that the WSJ subsequently partially retracted its assertion that Galileo had approached Amadeus shareholders1

(although it did not retract the possibility that Amadeus had been approached), it would appear that the traditional GDSs are slipping into “the ditch” implicit in the “Rule of Three” – and seeking “mergers” for incremental gains by combining overhead.

Compare that issue with the Cendant purchase of Orbitz noted in the first comment this month – or with IAC’s acquisition of Expedia and a host of other smaller Internet “players!” Using Drucker’s observation that “When major players in an industry buy smaller, growing companies, the industry itself is growing,” it would seem that the hyperarchy of information distribution model reflects a growing market segment – not one that is topping out! And a growing market or industry segment is less susceptible to the ills of the “Rule-of-Three” … since the dominant players absorb the strong niche-market players before they fall into “the ditch.”

The second aspect of concern deals with the relative technological strength of hub-centric dependent technologies competing in the digital hyperarchy of information with nodal networks. Hub-centric networks have capacity limitations. Historically, mainframe providers simply ramped up the CPU horsepower to deal with increased demands on central sites.

But as the GDSs and virtually every other major centralized processing environment have experienced – the marginal gain in the ability of a large centralized CPU network hub becomes cost prohibitive beyond certain points – limited not only by the inability of the CPU to process the information internally; but more often by the external in and out put sources to provide or accept the data at speeds and in structures that match the horsepower of the central system.

This particular problem is not peculiar to digital hub-centric systems – but is one of the major problems confronting today’s legacy airlines and the airports that serve them. It is the inability of the three major legacy carriers depicted in the graph above … to move airplanes, people, and services through the major airport hubs in the cost-efficient manner that such hubs suggest; that is causing all three of those carriers to be slipping into “the ditch.” It is the nodal network carriers like Southwest and JetBlue that are leading the way in transforming the air transport industry – just as companies like Cendant and IAC are transforming the distribution of travel with new digital nodal networks of product distribution.

Finally, there is the issue of whether the future lies with “content providers” … those digital hosting systems that collect, assimilate, and offer a multitude of products on behalf of the vendors/sellers and offer those products to those who come to the content

1 Corrections & Amplifications: Galileo International Inc., which is owned by real-estate and travel-services company Cendant Corp., didn't make an approach to Amadeus Global Travel Distribution SA's core shareholders about buying their stakes in the Spanish company. This article incorrectly said Galileo had approached Amadeus's core shareholders.

_____________________________________document.doc Page: 7

All rights reserved by The Eastman Group Incwww.eastmangroup.com

provider in search of product – or whether the future lies with digital “context acquiring” solutions that use pre-determined and ever-changing business rules and conditional logic to reach out to specific providers of specific services to dynamically package travel solutions?

There is an excellent piece in the September issue of e-Trends Magazine pertaining to the new generation of people entering the work place … what e-Trends calls the “Gamer Generation.” e-Trends dubs them the “Gamer Generation” because they have all been raised playing digital games … and e-Trends authors suggest (and document) that this dimension of their upbringing has given “Gamers” a different perspective on how to deal with work and life in general.

<< … the gamer generation is able to multi-task with much more ease than the rest of us can. They can perform many routine chores the rest of us would have to think about. Games teach them to prioritize their attention — and regulate their concentration on the most important thing at hand. This clearly has implications for their success in today’s fast-moving business world. >>

It is the issue of Gamers being able to regulate their concentration on the most important thing at hand that suggests the dynamic that will transform the travel business from the constraints of having to cross-search multiple content providers – to a business of delivering contextually relevant solutions to those who need to solve “the most important thing at hand” in the immediate context of the moment.

While this structure is already beginning to surface in travel packaging, the “Gamer Generation” will simply not even bother to consider content source providers – but will simply expect the business rules relevant to their need to be digitally in place and the needs to be resolved in the context of the moment. In order to enable this type of business-rules buyer-driven dynamic travel packaging – travel technology will have to migrate out of the content and supplier dominated hosting environments and into the corporate travel or bulk travel-buyer domain.

Taken together, these three aspects of dynamic travel packaging suggest that the GDSs and the content-provider solution that they represent will slide into the “Rule-of-Three ditch” … to be absorbed or transformed by Drucker-type “topping out” mergers. The new digital nodal network technology driven companies that are evolving into the forefront of travel distribution and growing through acquisition of smaller players in the industry … will structurally come to dominate travel distribution. Context-driven automated dynamic purchasing by volume buyers will replace content providers – which mean that the buying-decisions will move from supplier dominated distribution to buyer controlled acquisition. Implicit in that assumption is that the automated management of buying will move to corporate buyers and/or TMCs acting to acquire on behalf of their corporate buyers (i.e. not distributing products from suppliers).

In this assumption, I disagree with Jack.

As to which companies or business entities will provide these solutions – that remains to be seen. Whether it will be the GDSs, TMCs, ITMCs, e-travel distribution companies, or e-franchise outlets – only time will tell. What is important to recognize is that the model will NOT be the same as it is today; for the present model no longer reflects the optimum technology or economic solution for distribution of travel.

_____________________________________document.doc Page: 8

All rights reserved by The Eastman Group Incwww.eastmangroup.com

Eastman's "Off-the-Wall Comment(s)"© ...

The airline or vendor need to lower costs is, of course, the other dynamic that is at play in the role of travel distribution intermediaries – GDSs and/or TMCs. The airlines simply cannot afford the GDSs as a distribution intermediary with the GDSs charging segment and other fees tied to what have historically been manual agent transaction processing (to which Bethune alludes). The dilemma for the GDSs … or at least, for those whose costs will allow … is how to transform their revenue base from the airline segment fee model to a distributed revenue structure that reflects the value-add contribution of the GDS as it serves the different users of its systems. Solve that problem and the GDSs will survive a little longer … maybe long enough to evolve into the totally different roles noted above.

What is important about Bethune’s comment is that it reflects the other half of the dynamic currently working against the GDSs. Note, he did not say that travel agencies were a dying business – only the GDSs. Of course, he also didn’t comment on the viability of legacy carriers like his own Continental either “;-]. Still, whether one believes in the survival of the GDSs in their present form … or in some new embodiment – it is essential to regularly assess their status. The next six to 12 months should be very telling with respect to the future of each of the GDSs; and the structure of travel product distribution that will ultimately evolve.

_____________________________________document.doc Page: 9

All rights reserved by The Eastman Group Incwww.eastmangroup.com

From TravelAgent.Com©, September 13, 2004Bethune Calls GDSs a Dying Business. Speaking to reporters after a Sky Team announcement in New York Monday, Continental Chairman and CEO Gordon Bethune said airlines would like to drive more customers to the Web by offering discounts, rather than charge fees for booking by other methods, such as calling for reservations or using a GDS. "The GDS is a dying business," he said, adding that years ago travel agents were the only ones who could understand how to use them to make a booking. But with the Internet now, he questioned the need for customers and airlines to be forced to pay the fees incurred by using a GDS.

Eastman's "Off-the-Wall Comment(s)"© ...

These are some of the first efforts being put forth by Sabre as a direct result of the GDS deregulations … and Sabre’s need to step up if it is to remain viable in the distribution of travel product as noted above! Sabre clearly needs to find ways to leverage its retail connected network -- if it is to sustain the "value-add" to the airlines and other travel vendors. Airline segment revenue remains vital to Sabre because they do not have the hotel base to fall back on as do Cendant and IAC.

Respectfully, \\ Richard

_____________________________________document.doc Page: 10

All rights reserved by The Eastman Group Incwww.eastmangroup.com

From TravelWeekly.Com, September 24, 2004Sabre launches co-op marketing deal with preferred agencies. It's not often that a GDS company trots out its brand to consumers, but that is what Sabre is doing as it tests a co-op ad program with several preferred agencies in the New York market.