weathering the storm - samsungoriginus.samsung.com/us/business/semiconductor/news/downloads/... ·...

TRANSCRIPT

Weathering the Storm: Fortifying Memory Storage Through the Global Recession

Jim ElliottVice President, Marketing

Samsung Semiconductor, Inc.

Confidential

Presentation AgendaPresentation Agenda

Macro-Economic Perspective

Memory Market Overview

Storage Growth Drivers

SSD: 2009 is the Break-Out Year

Parting Thoughts

Confidential

Presentation AgendaPresentation Agenda

Macro-Economic Perspective

Memory Market Overview

Storage Growth Drivers

SSD: 2009 is the Break-Out Year

Parting Thoughts

Confidential

Some Economic PerspectiveSome Economic Perspective

Confidential

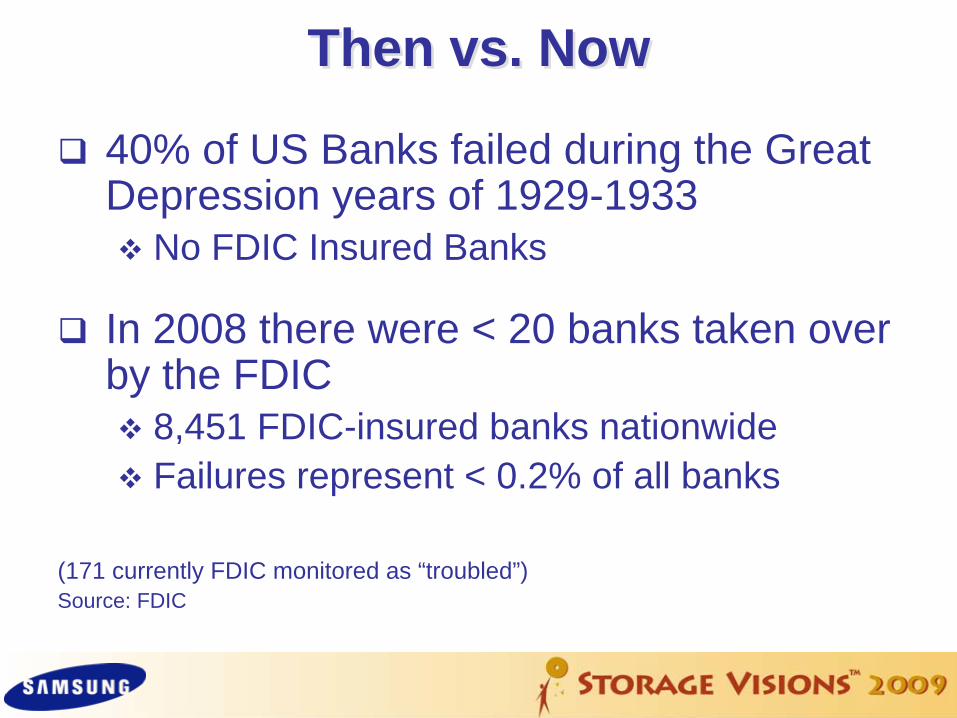

Then vs. NowThen vs. Now

40% of US Banks failed during the Great Depression years of 1929-1933

No FDIC Insured Banks

In 2008 there were < 20 banks taken over by the FDIC

8,451 FDIC-insured banks nationwideFailures represent < 0.2% of all banks

(171 currently FDIC monitored as “troubled”)Source: FDIC

Confidential

Economic Analysis – Upside FactorsGovernments Providing Financial-rescue Plans

US, UE and Chinese Governments Spending $Trillions

Oil Prices Back to Earth$145.7 (July) down to < $45 (December)

Refinancing Boom to Drive Discretionary Spending

$146

$45

Oil PriceOil Price

Confidential

Economic Analysis – Downside FactorsEconomic Analysis – Downside FactorsUncertain Macro Outlook

Financial Crisis in the U.S. is Spreading

Business and Consumer Spending WeakeningCorporations Freezing Some Non-essential Expenditures (CES?)Disposable Income DecreasingConsumer Confidence Levels at All-time Lows

CCI: 61.4(Sep `08) → 38.0(Oct `08)*)* Source: 1) The Conference Board (Oct 2008)

`08~`09 W/W GDP Growth RateGrowth Rate

* Source: IMF,OECD (Nov 2008)

- 0.9%- 0.7%

- 0.5%

IMFOECD 1.4%

1.6%

- 0.5%1.1%

- 0.1%0.5%('08) ('09)

1.3%

- 0.2%0.7%

Confidential

Slowing Growth in 20092009: Stagnant Mobile Phone and PC Markets

Possibility of Negative Growth (First Since 2001)

* Source :SEC Marketing, Theodoor Gilison Bank (1)

Avg CAGR (’03~’07)

15%

'09

PC 13%

Mobile Phone 23% -1%

13%DTV 13%

7%

'08

0~4%

14%(?)

Confidential

Presentation AgendaPresentation Agenda

Macro-Economic Perspective

Memory Market Overview

Storage Growth Drivers

SSD: 2009 is the Break-Out Year

Parting Thoughts

Confidential

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

`07.Q1 Q2 Q3 Q4 `08.Q1 `08.Q2 `08.Q3

Memory Makers Financial CrisisManufacturers “In the Red” Since Q2’07

Aggregate of $12.8B lost in 6 QuartersUnsustainable Trend on Supply SideProfound Impact to Future CAPEX and Supply…

* Source : Company Reports, SEC Marketing, UBS (Oct 2008)

-1.1B -0.8B -2.5B -3.1B -3.0B-2.2B-0.1B

$-12.8B

Confidential

CAPEX vs. Memory RevenueCAPEX vs. Memory Revenue

($B)

2733

47 49

58 58

47 50

68

1318

23

30

22

38%28%25%21%

0

10

20

30

40

50

60

70

2002 2003 2004 2005 2006 2007 2008 20090%

10%

20%

30%

40%

50%

60%RevenueCapExCapEx / Rev

13

47%

26%

39%

53%

* Source: WSTS, Company Reports, SEC Marketing

2007: CAPEX Peaked at $30B, or 53% of Revenue2009: CAPEX Reduction to <$13B 26% of Revenue2009: Lowest Ratio Since 2003, Staging Recovery…

Rev / CAPEX

Confidential

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 2008 2009 2010 2011

DSC / Card

UFD

MP3 / PMP

CellularSSD

NAND Transcending CE Arena…NAND Transcending CE Arena…

DSC /Card Era

Mobile Era

PC EraNAND GB

Distribution

Application Diversification:

- Less CE Centric

- Creates More Stability

Confidential

Presentation AgendaPresentation Agenda

Macro-Economic Perspective

Memory Market Overview

Storage Growth Drivers

SSD: 2009 is the Break-Out Year

Parting Thoughts

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

“Innovation”First Time Buyers

“Good Enough”Beholden to

Replacement Cycle

“Mainstream”Proliferation Phase

Confidential

Smart Phones Key to Cellular GrowthSmart Phones Key to Cellular Growth

`01 `02 `03 `04 `05 `06 `07 `08 `09

MemoryContent

7MB7MB 14MB14MB 21MB21MB 45MB45MB95MB95MB

180MB180MB

304MB304MB

588MB588MBYoY G/R

5%

22%32%

22% 22%16%

7%7%0%0%

674512

418400

1,159997

820

1,237 1,200

* Source : DQ (Sep 2008) , Samsung

Smartphone

Non- Smartphone

(M Phones)

2009: Flat-to-Reduced Category Sales in AggregateGrowth Slowing in Mature-3G Markets and Emerging Markets

Smart Phones will Carry the Torch: >150M in 2009North America is Fastest Growing Region: 68% in Q3/08

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

“Innovation”Lure First Time Buyers

“Good Enough”Beholden to

Replacement Cycle

“Mainstream”Proliferation Phase

Confidential* Source : iSuppli (Oct 2008)

`01 `02 `03 `04 `05 `06 `07 `08 `09

135% 150%116%

250%

38%

11%11% 6%6% 6%6%

PMP

MP3

YoY G/R M Units

3 7 1737

129

178197 209

221

MP3 Category: PMP to Drive GrowthMP3 Category: PMP to Drive GrowthGrowth Slowing Since 2005 Peak

MP3 Stand-Alone Growth Rate is NegativeCompetition with Convergent Devices (Phone, etc.)

PMP Now Driving the Category: Massive GB Requirements for Video

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

SmartPhone

“Innovation”Lure First Time Buyers

“Good Enough”Beholden to

Replacement Cycle

Phone

“Mainstream”Proliferation Phase

Confidential* Source : Samsung (3Q ’08 )

55

10

96

15

16

7

23

38

8

47

54

10

66

75

12

87

45%

107%

40%36%

51%

In-DashPND

`04 `05 `06 `07 `08 `09

12

10

8

77

55 8 16

3856

75

(M units)

YoY G/R

Car Navigation: Auto Industry Woes?Car Navigation: Auto Industry Woes?2009: Category Slowing to 36% for ~90M Units

In-Dash Represents Only 15% or 12M UnitsNAND TAM Doubling Each Year: >250M EQ’s

8GB to Represent 15% in 2009 for 3D Maps

In-Dash

Portable

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

SmartPhone

“Innovation”Lure First Time Buyers

“Good Enough”Beholden to

Replacement Cycle

Phone MP3

PMP

“Mainstream”Proliferation Phase

Confidential[Source : iSuppli 2008.10

Memory Card / USB Drive Regional Market Size

[Source : iSuppli, SEC]

Card / USB Market SnapshotCard / USB Market SnapshotUnit Growth Strong, but ASPs Compress Revenue

Digital Camera Attach Rate: 2.7 Cards perCell Phone Attach Rate: 0.3 per. Growth Potential

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 20120%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

2GB

4GB

8GB

1GB2GB

4GB

8GB

1GB

Card Avg GB: 2X per Year USB Avg GB: 2X per Year

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

SmartPhone

NAV

PMP“Innovation”Lure First Time Buyers

“Good Enough”Beholden to

Replacement Cycle

Phone MP3

“Mainstream”Proliferation Phase

Confidential

2009 is the “BREAKOUT” Year for SSD!

2009!

Confidential

SSD Advantage Re-CapSSD Advantage Re-Cap

Higher Performance

More Reliability

Less Power Consumption

Less Heat / Less Cooling

Reduced Hardware Footprint

Easier Recycling

Confidential

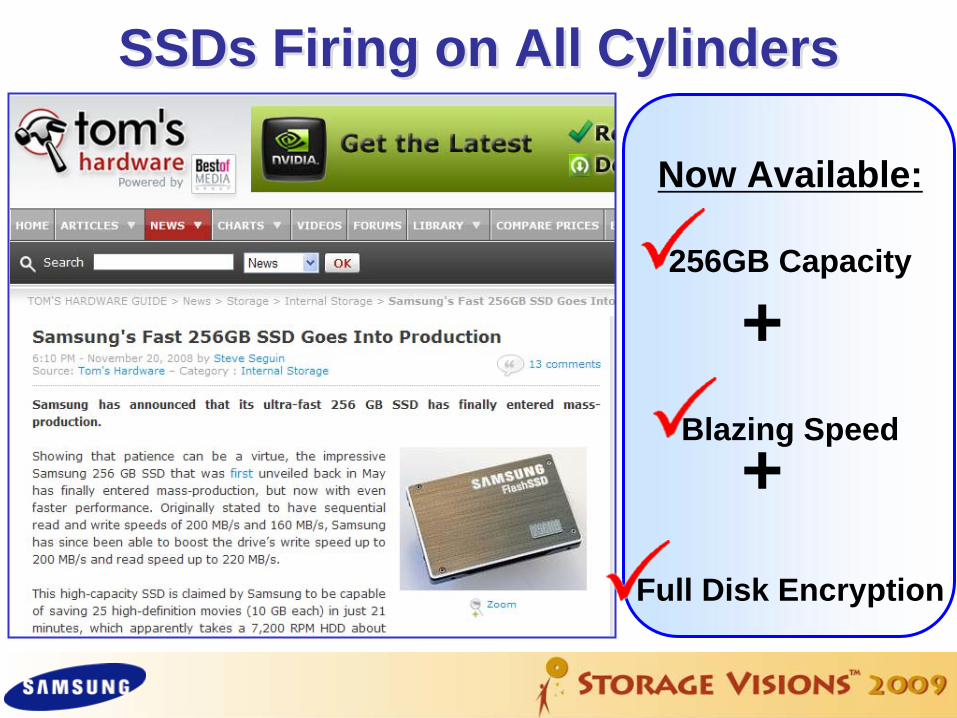

SSDs Firing on All CylindersSSDs Firing on All Cylinders

Now Available:

256GB Capacity

Blazing Speed

Full Disk Encryption

+

+

Confidential

New SSDs Pushing the LimitsNew SSDs Pushing the Limits

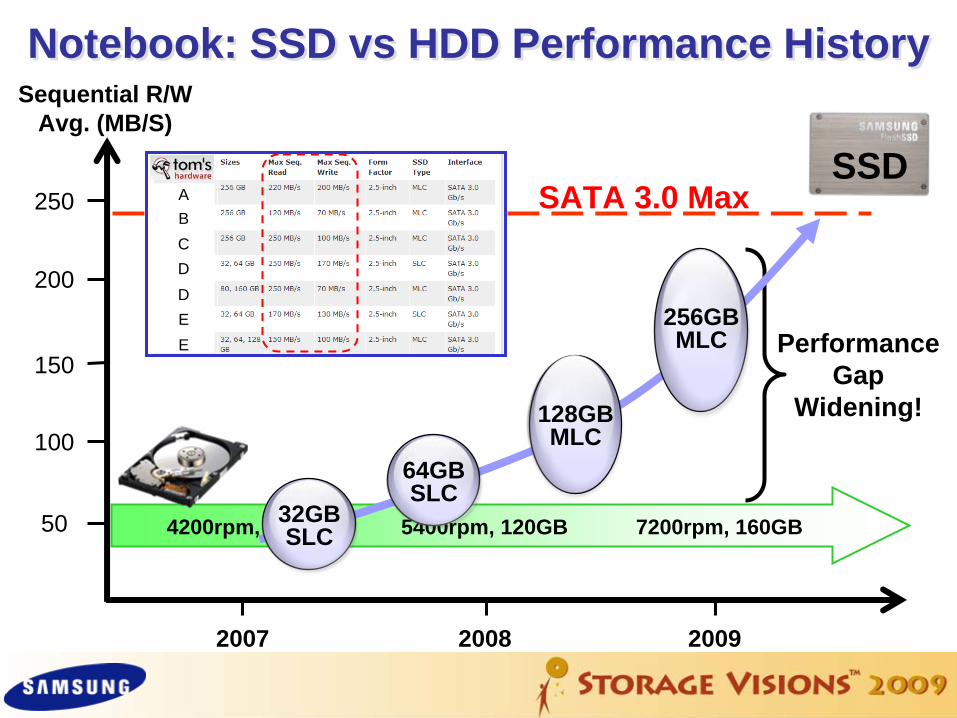

Today’s SSDs Are Nearly Saturating the SATA 3.0 Interface

A

B

C

D

D

E

E

Confidential

Notebook: SSD vs HDD Performance HistoryNotebook: SSD vs HDD Performance History

2007 20092008

50

100

4200rpm, 80GB 5400rpm, 120GB 7200rpm, 160GB

Sequential R/W Avg. (MB/S)

150

200

250

Performance Gap

Widening!

SSD

128GB MLC

256GB MLC

64GB SLC

32GB SLC

ABCDDEE

SATA 3.0 Max

Confidential

Notebook PC: SSD vs HDD PriceNotebook PC: SSD vs HDD Price

2007 2009

$100

2008

$200

$300

$400

$500

$600

$700

$800

$900

$1000

4200rpm, 80GB 5400rpm, 120GB 7200rpm, 160GB

Capacity Avg. Price32 GB MLC $9564 GB MLC $180128 GB MLC $320

~30X

~10X$

32GB SLC

64GB SLC

128GB MLC

$SSD

<5X

Confidential

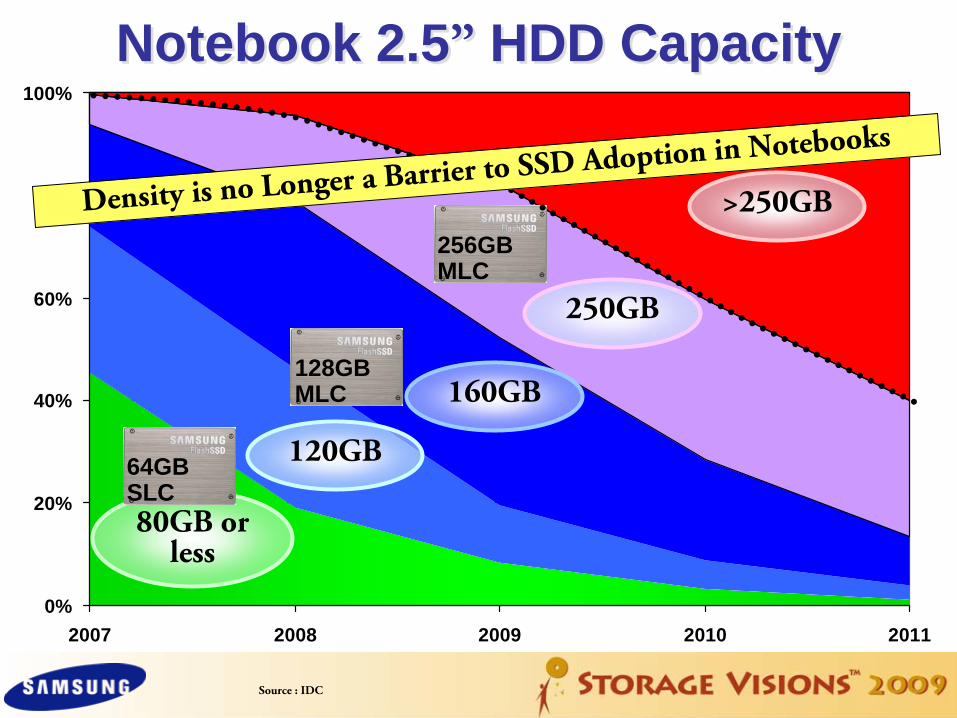

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Source : IDC

80GB or less

120GB

160GB

250GB

>250GB

Notebook 2.5”

HDD CapacityNotebook 2.5”

HDD Capacity

64GB SLC

128GB MLC

256GB MLC

Density is no Longer a Barrier to SSD Adoption in Notebooks

Confidential

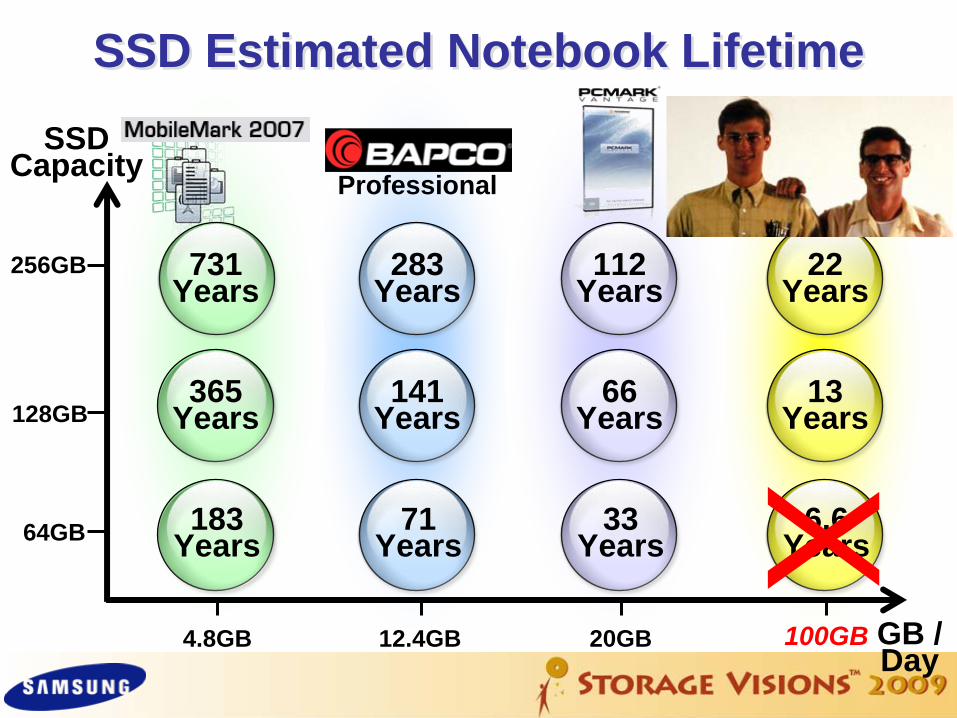

SSD Estimated Notebook LifetimeSSD Estimated Notebook Lifetime

4.8GB 20GB GB / Day

SSD Capacity

64GB

128GB

256GB

12.4GB

Professional

71 Years

141 Years

283 Years

33 Years

66 Years

112 Years

183 Years

365 Years

731 Years

Confidential

SSD Estimated Notebook LifetimeSSD Estimated Notebook Lifetime

4.8GB 20GB GB / Day

SSD Capacity

64GB

128GB

256GB

12.4GB

Professional

71 Years

141 Years

283 Years

33 Years

66 Years

112 Years

183 Years

365 Years

731 Years

100GB

6.6 Years

13 Years

22 Years

Confidential

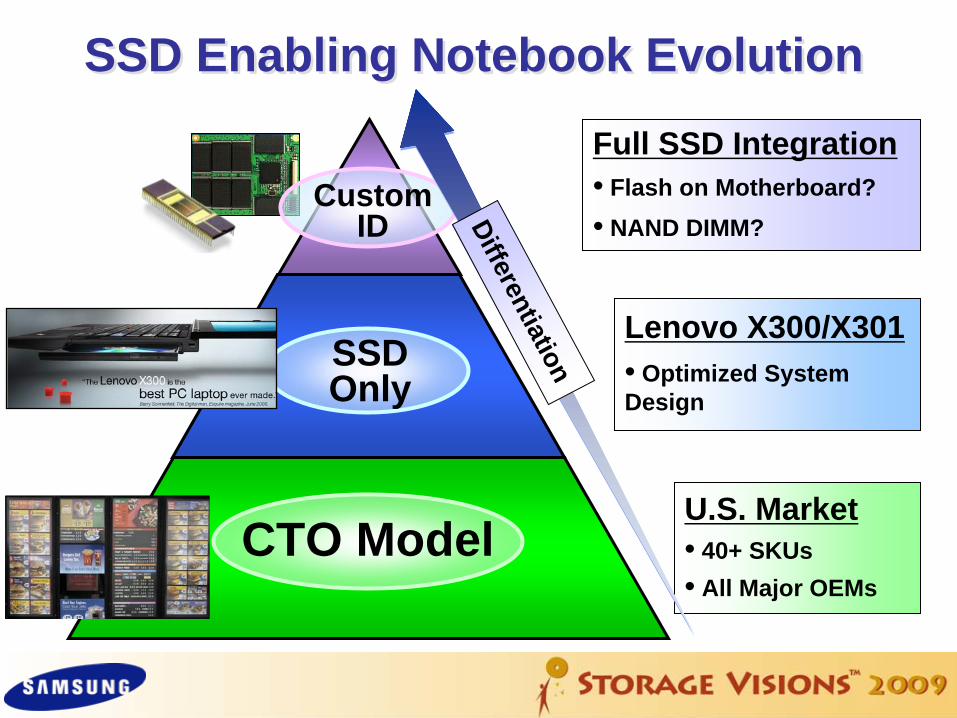

U.S. Market• 40+ SKUs• All Major OEMs

Lenovo X300/X301• Optimized System Design

Full SSD Integration• Flash on Motherboard?• NAND DIMM?Differentiation

SSD Enabling Notebook EvolutionSSD Enabling Notebook Evolution

CTO Model

Custom ID

SSD Only

Confidential

2009: A Conservative 5M SSD Units Forecasted2012: SSD Notebook Attach Rate of 35%

2008 2009 2010 2011 2012

0.5%3%

8%

18%

35%

82M

37M

15M4.8M0.6M 0.3M 6M

13M28M

Note PC Shipment

Desktop Shipment

SSD (Note PC)SSD (Note PC)

SSD (Desktop)SSD (Desktop)

77GB106GB

119GB

143GB

153GB

: NB Attach Rate: Average GB

* Source : iSuppli (Jun 2008) , Goldman Sachs (Oct 2008), SEC Marketing

152

142 143 145 147134

159 184208

230

NB + DT SSD Growth ProjectionsNB + DT SSD Growth Projections

Confidential

Enterprise Space: Ripe for InnovationEnterprise Space: Ripe for Innovation

* Source : 2008 McKinsey Study, Fortune, Sept 15, 2008

•Average data center consumes energy equivalent of 25,000 households

• 90% of large data centers need more power/cooling in the next 30 months

• America consumes more power running data centers than TVs

Did You Know…?

Confidential

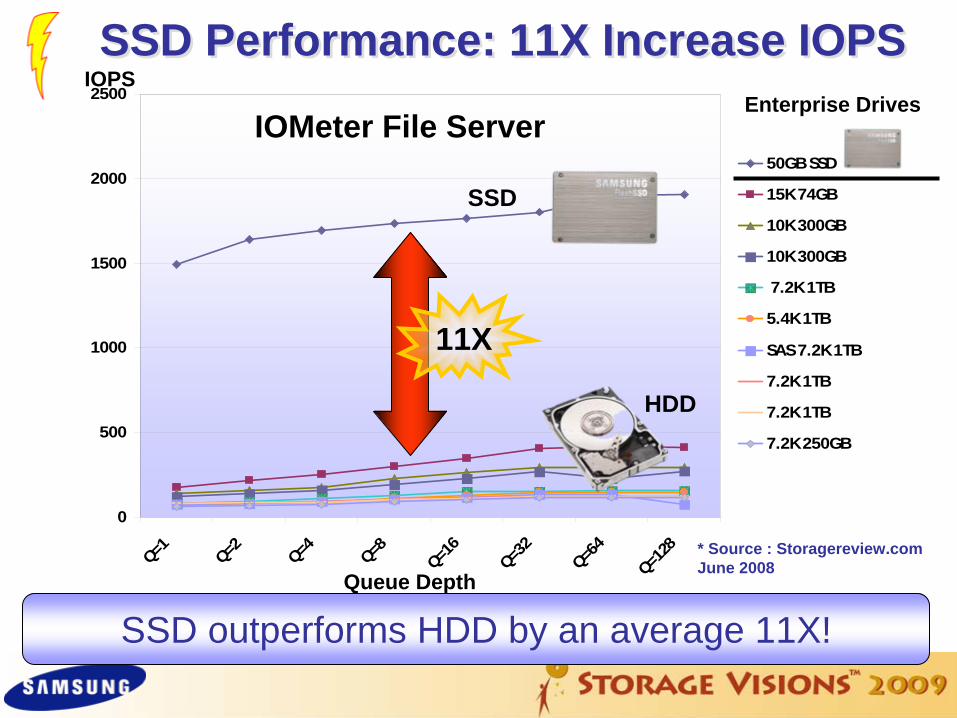

SSD Performance: 11X Increase IOPSSSD Performance: 11X Increase IOPS

SSD outperforms HDD by an average 11X!

0

500

1000

1500

2000

2500

Q=1 Q=2 Q=4 Q=8

Q=16

Q=32

Q=64

Q=128

50GB SSD

15K 74GB

10K 300GB

10K 300GB

7.2K 1TB

5.4K 1TB

SAS 7.2K 1TB

7.2K 1TB

7.2K 1TB

7.2K 250GB

IOPS

Queue Depth* Source : Storagereview.com June 2008

IOMeter File Server

11X

Enterprise Drives

HDD

SSD

Confidential

Announcing High Speed 100GB Enterprise SSDAnnouncing High Speed 100GB Enterprise SSD

Samsung Introducing High-speed, HighCapacity “Green” SSD for Enterprise Market

Las Vegas, NV – Jan. 6, 2009: Samsung Electronics Co., Ltd., the world leader in advanced semiconductor technology, announced today at the Storage Visions 2009 Conference here that it has developed a 100 gigabyte (GB) solid state drive for use in servers for applications such as video on demand, streaming media content delivery, internet data centers, virtualization and on-line transaction processing…

25,000 Read IOPS25,000 Read IOPS6,000 Write IOPS6,000 Write IOPS

Confidential

SSD Disruptive to Enterprise: $/IOPS, IOPS/W

15K HDD 3.5”

15K HDD 2.5” SSD 2.5”

Capacity 146GB 76GB 100GB

$ / IOPS $0.43 $0.82 $0.05

IOPS / W 43 70 13100

*HDD: Price and Data from storagereview.com; IOPS: average read speed

*SSD: IOPS - random read @ 512B, Data (Samsung)

8X 16X

304X 187X

“Short Stroking”

Green

Confidential

Power: IOPS/W Data is AstoundingPower: IOPS/W Data is Astounding

* Source : EMC

98% Power Improvement

kWh/yr Per 100K IOPS

Capacity Optimized

Performance Optimized

SSD

30X IOPS Jump

Confidential

Metric HDD SSDMechanics Motor, Moving Head No Moving Parts

Wear Quasi-Predictable with S.M.A.R.T. (~30%) 100% Predictable

Lifespan Unpredictable 100% Predictable

Reading Data Wears the drive Infinite Capability

Fragmentation Performance Attenuates; Defrag Time and Cost No Effect

Top Server OEM: Enterprise SSD offers 25% higher reliability

SSD Reliability and PredictabilitySSD Reliability and Predictability

Confidential

Video on Demand: SSD Ready for PrimetimeVideo on Demand: SSD Ready for PrimetimeCapacity Optimized

Performance Optimized

VOD: SSD Allows 70% Power Savings, 80% Space Savings

“Hot Data” “Cold Data”

High IOPS for New ReleasesMultiple Simultaneous Streams

High CapacityStoring Thousands of Archives

Confidential

* Source: IDC (May, 2008)

2008 2009 2010 2011 2012

32M

14M

33M36M

41M

45M

17M 22M30M

42M

* Assumes 1 SSD replaces 4 HDDs

Capacity Optimized

Performance Optimized

0.5% 55GB

2% 57GB

6% 83GB

12% 102GB

20% 121GB

SSD Penetration, CapacitySSD Penetration, Capacity

Enterprise HDD Unit Forecast

Enterprise HDD Unit Forecast

Enterprise SSD Attach Rate ForecastEnterprise SSD Attach Rate Forecast

Confidential

Technology Adoption is Non-LinearTechnology Adoption is Non-Linear“Bass Diffusion Model”

Time

Adoption Rate %

Early Adoption

Ramp - Up

Saturation

SmartPhone

“Innovation”Lure First Time Buyers

“Good Enough”Beholden to

Replacement CycleNAV

PMP

Phone MP3CardUSB

“Mainstream”Proliferation Phase

Confidential

Parting ThoughtsParting Thoughts

Confidential

Parting ThoughtsParting Thoughts2008:

“Visibility is Poor”

Confidential

Parting ThoughtsParting Thoughts

2009:Disruptive Technology Will Drive InnovationInnovation Will Enable EfficienciesEfficiency Will Create New MarketsNew Markets Will Save the EconomyLet’s Go Make it Happen!

2008:“Visibility is Poor”

Confidential

Thank You!Thank You!