wavefront technology solutions inc. 4 of 46 wavefront technology solutions inc. consolidated...

TRANSCRIPT

Consolidated Financial Statements of

WAVEFRONT TECHNOLOGY SOLUTIONS INC. August 31, 2012 and 2011

TABLE OF CONTENTS CONSOLIDATED FINANCIAL STATEMENTS

Consolidated statements of financial position 1Consolidated statements of net loss and comprehensive loss 2Consolidated statements of changes in shareholders' equity 3Consolidated statements of cash flows 4

NOTES TO THE CONSOLIDATED FINANICAL STATEMENTSNote 1 Nature of operations and corporate information 5Note 2 Basis of presentation and adoption of IFRS 5Note 3 Significant accounting policies 6Note 4 Recent accounting pronouncements 15Note 5 Critical accounting estimates and judgements 18Note 6 Cash and short term deposits 19Note 7 Property, plant and equipment 20Note 8 Intangible assets 21Note 9 Goodwill 22Note 10 Jointly controlled assets 23Note 11 Decommissioning liabilities 23Note 12 Share capital 24Note 13 Revenue 27Note 14 Expense by nature 28Note 15 Income taxes 29Note 16 Loss per share 31Note 17 Capital management 32Note 18 Financial instruments 33Note 19 Net change in non-cash working capital items 37Note 20 Commitments, contingencies and guarantees 38Note 21 Related party transactions 38Note 22 Economic dependence and segmented information 39Note 23 Transition to IFRS 39Note 24 Seasonality of operations 46Note 25 Subsequent events 46

PricewaterhouseCoopers LLP TD Tower, 10088 102 Avenue NW, Suite 1501, Edmonton, Alberta, Canada T5J 3N5 T: +1 780 441 6700, F: +1 780 441 6776

“PwC” refers to PricewaterhouseCoopers LLP, an Ontario limited liability partnership.

December 20, 2012

Independent Auditor’s Report

To the Shareholders of

Wavefront Technology Solutions Inc.

We have audited the accompanying consolidated financial statements of Wavefront Technology Solutions Inc. and its subsidiaries, which comprise the consolidated statements of financial position as at August 31, 2012, August 31, 2011 and September 1, 2010 and the consolidated statements of net loss and comprehensive loss, changes in shareholders’ equity and cash flows for the years ended August 31, 2012 and August 31, 2011 and the related notes, which comprise a summary of significant accounting policies and other explanatory information. Management’s responsibility for the consolidated financial statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Wavefront Technology Solutions Inc. and its subsidiaries as at August 31, 2012, August 31, 2011 and September 1, 2010 and their financial performance and their cash flows for the years ended August 31, 2012 and August 31, 2011 in accordance with International Financial Reporting Standards.

(Signed) “PricewaterhouseCoopers LLP”

Chartered Accountants

Edmonton, Alberta, Canada

Page 1 of 46

WAVEFRONT TECHNOLOGY SOLUTIONS INC.Consolidated Statements of Financial PositionAs at August 31, 2012, August 31 2011, and September 1, 2010(Canadian dollars)

August 31, August 31, September 1,Note 2012 2011 2010

(Note 23) (Note 23)ASSETS

CURRENT ASSETSCash and cash equivalents 6 15,169,284$ 24,510,593$ 29,442,956$

Trade and other receivables 1,667,743 1,045,043 865,092 Inventories 613,162 373,925 99,969 Prepaid expenses 223,478 142,298 83,701

17,673,667 26,071,859 30,491,718

NON-CURRENT ASSETSDeposits 95,331 118,880 103,573 Property, plant and equipment 7 6,172,180 5,357,777 4,919,959 Intangible assets 8 4,291,470 483,774 451,314 Goodwill 9 1,222,217 1,222,217 1,222,217

29,454,865$ 33,254,507$ 37,188,781$

LIABILITIES AND SHAREHOLDERS' EQUITY

CURRENT LIABILITIESTrade accounts payable and accrued liabilities 1,646,483 1,044,298 1,173,495

NON-CURRENT LIABILITIESDecommissioning liability 11 37,057 378,541 374,785

1,683,540 1,422,839 1,548,280

SHAREHOLDERS' EQUITYShare capital 12b 66,438,909 66,320,249 66,288,967 Contributed surplus 12e 8,582,757 8,112,618 7,477,519 Accumulated and other comprehensive loss (411) - - Deficit (47,249,930) (42,601,199) (38,125,985)

27,771,325 31,831,668 35,640,501 29,454,865$ 33,254,507$ 37,188,781$

APPROVED BY THE BOARD

"Steve Percy" (signed) Director

"Jeff Saponja" (signed) Director

Page 2 of 46

WAVEFRONT TECHNOLOGY SOLUTIONS INC.Consolidated Statements of Net Loss and Comprehensive LossAs at August 31, 2012 and August 31, 2011(Canadian dollars)

August 31, August 31,Note 2012 2011

(Note 23)

Revenue 5,632,001$ 3,991,624$

Cost of sales 1,254,295 1,320,441 General and administrative 5,193,128 3,963,425 Sales and marketing 2,025,176 1,986,284 Amortization, depreciation, and depletion 1,367,488 944,066 Research and development 593,735 413,738

10,433,822 8,627,954

OPERATING LOSS (4,801,821) (4,636,330)

Financing costs 14 (39,521) (118,814) Financing income 192,611 279,930

Net finance income 153,090 161,116

NET LOSS (4,648,731) (4,475,214)

OTHER COMPREHENSIVE LOSSTranslation loss on foreign operations (411) -

NET LOSS AND COMPREHENSIVE LOSS (4,649,142)$ (4,475,214)$

LOSS PER COMMON SHAREBasic and diluted 16 (0.06)$ (0.05)$

Page 3 of 46

WAVEFRONT TECHNOLOGY SOLUTIONS INC.Consolidated Statements of Changes in Shareholders' EquityAs at August 31, 2012 and August 31, 2011(Canadian dollars)

Share ContributedNote Capital Surplus Deficit Total

Balance at September 1, 2010 23 66,288,967$ 7,477,519$ - $ (38,125,985)$ 35,640,501$ Net loss and comprehensive loss - - - (4,475,214) (4,475,214) Stock options exercised 31,282 (13,682) - - 17,600 Recognition of shared-based payments - 648,781 - - 648,781

Balance at August 31, 2011 23 66,320,249 8,112,618 - (42,601,199) 31,831,668 Net loss and comprehensive loss - - (411) (4,648,731) (4,649,142) Stock options exercised 118,660 (53,861) - - 64,799 Recognition of shared-based payments - 524,000 - - 524,000

Balance at August 31, 2012 66,438,909 8,582,757 (411) (47,249,930) 27,771,325

Accumulated other

comprehensive

Page 4 of 46

WAVEFRONT TECHNOLOGY SOLUTIONS INC.Consolidated Statements of Cash FlowsAs at August 31, 2012 and August 31, 2011(Canadian dollars)

August 31, August 31,Note 2012 2011

OPERATING ACTIVITIESNet loss (4,649,142)$ (4,475,214)$ Items not affecting cash

Share-based payments 12d 524,000 648,781 Amortization, depreciation, depletion and accretion expenses 1,373,378 948,282 Loss (gain) on disposal of property, plant and equipment (97,593) 173,485 Write-down (gain) of property, plant and equipment (72,304) -Translation loss on foreign operations (411) -

(2,922,072) (2,704,666) Net change in non-cash working capital items 19 (317,383) (657,008)

Cash used in operating activities (3,239,455) (3,361,674)

INVESTING ACTIVITIESPurchase of property, plant and equipment (1,841,701) (1,523,975) Proceeds on disposal of property, plant and equipment 7 (155,146) 21,041 Acquisition of intangible assets 8 (4,083,281) - Additions to intangible assets (86,525) (85,355)

Cash used in investing activities (6,166,653) (1,588,289)

FINANCING ACTIVITIESProceeds from options exercised 64,799 17,600

Cash provided by financing activities 64,799 17,600

NET DECREASE IN CASH AND CASHEQUIVALENTS (9,341,309) (4,932,363)

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 24,510,593 29,442,956

CASH AND CASH EQUIVALENTS, END OF YEAR 15,169,284$ 24,510,593$

Supplementary InformationInterest paid (2,015) (2,775)

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 5 of 46

1. NATURE OF OPERATIONS AND CORPORATE INFORMATION Wavefront Technology Solutions Inc. (the “Corporation”) is incorporated under the Canada Business Corporations Act. The address of the registered head office of the Corporation is 5621 – 70 Street, Edmonton, Alberta. The Corporation’s principal business activities involve the licensing and utilization of the Corporation’s patented process for the enhancement and improvement of oil recovery and oil well stimulation (“PowerwaveTM”), and the optimization of groundwater remediation (“PrimawaveTM”) approaches. In the oil sector the Corporation’s strategy is to leverage its intellectual property through licenses of the technology to service providers, and to provide site licenses to oil producers. In the environmental sector the Corporation’s strategy is to provide site licenses to those involved in groundwater clean-up.

2. BASIS OF PRESENTATION AND ADOPTION OF IFRS The Corporation prepares its financial statements in accordance with Canadian generally accepted accounting principles as defined in the Handbook of the Canadian Institute of Chartered Accountants (CICA Handbook). In 2010, the CICA Handbook was revised to incorporate International Financial Reporting Standards as issued by the International Accounting Standards Board (IFRS) and to require publicly accountable enterprises to apply these standards effective for years beginning on or after January 1, 2011. Accordingly, these are the Corporation’s first annual consolidated financial statements prepared in accordance with IFRS. In these financial statements, “Canadian GAAP” refers to Canadian GAAP before the adoption of IFRS. These consolidated financial statements have been prepared in accordance with IFRS, including the interpretations adopted by the International Accounting Standards Board (“IASB”) and the International Financial Reporting Interpretations Committee of the IASB (“IFRIC”). These consolidated financial statements were authorized by the Board of Directors on December 17, 2012. Subject to certain transition elections and exceptions disclosed in Note 23, the Corporation has consistently applied the accounting policies used in the preparation of its opening IFRS statement of financial position at September 1, 2010 (the “transition date”) throughout all periods presented as if these policies had always been in effect. Note 23 discloses the impact of the transition to IFRS on the Corporation’s reported financial position, financial performance and cash flows, including the nature and effect of significant changes in accounting policies from those used in the Corporation’s consolidated financial statements for the year ended August 31, 2011 prepared under Canadian GAAP.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 6 of 46

3. SIGNIFICANT ACCOUNTING POLICES These accounting policies have been applied consistently by the Corporation and entities controlled by the Corporation. Basis of measurement These consolidated financial statements have been prepared on the historical cost basis. Subsidiaries These consolidated financial statements incorporate the financial statements of the Corporation and entities controlled by the Corporation (its wholly owned subsidiaries). Control is achieved when the Corporation has the power to, directly or indirectly, govern the financial and operating policies of an entity so as to obtain benefits from its activities. In assessing control, potential voting rights that are presently exercisable or convertible are taken into account. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. Inter-company transactions, balances, income and expenses and unrealized gains and losses have been eliminated on consolidation. Jointly controlled assets A joint venture is a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control. Joint control is the sharing of control under contractual agreement, such that significant operating and financing decisions require the unanimous consent of the parties sharing control. A portion of the Corporation’s oilfield activities include a jointly controlled operation whereby a contractual arrangement has been entered into without establishing a separate entity. Each venturer uses its own assets, incurs its own expenses and liabilities and funds its own participation in the operation. These consolidated financial statements include the Corporation’s share of assets and liabilities and a proportionate share of the relevant revenues and related costs, classified according to their nature. Foreign currency translation Functional and presentation currency These consolidated financial statements are presented in Canadian dollars, the Corporation’s functional currency, as that is the currency of the primary economic environment in which the Corporation operates. Translation of foreign entities The functional currency of the Corporation’s foreign subsidiary is the U.S. dollar which is the currency of the primary economic environment in which it operates. Assets and liabilities of the

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 7 of 46

U.S. subsidiary are translated into Canadian dollars at the closing rate at the date of the statement of financial position. Revenues and expenses are translated at the average rate for the period. Gains or losses on translation of foreign operations are recognized in other comprehensive income as cumulative translation adjustments. Translation of transactions and balances Foreign currency transactions are translated into Canadian dollars by applying exchange rates in effect at the transaction date. At each reporting period end, assets and liabilities denominated in foreign currencies are converted to Canadian dollars at rates of exchange prevailing on that date. Gains and losses on exchange differences are recognized in the statement of net loss. Cash and cash equivalents Cash and cash equivalents are comprised of cash on deposit, net of cheques issued in excess of cash on deposit; and, balances held in short-term, highly liquid, Guaranteed Investment Certificates and Term Deposits with original maturities of 90 days or less and annualized interest rates of 1.05%.

Inventories Inventories, which consist of installation components, repair parts and goods held for sale, are valued at the lower of cost, determined on a first-in, first-out basis, and net realizable value. Cost includes expenditures incurred in acquiring the inventories and bringing them to their existing location and condition. Net realizable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and selling and distribution expenses. Where necessary, the carrying amounts of inventories are adjusted for obsolete, slow-moving and defective inventories. Property, plant and equipment Property, plant and equipment are recorded at cost less accumulated depreciation and accumulated impairment losses. The initial cost of an asset comprises its purchase price or construction costs, any costs directly attributable to bringing the asset into operation, the initial decommissioning provision, and for qualified assets, borrowing costs. The purchase price or construction cost is the aggregate amount paid and the fair value of any consideration given to acquire the asset. The cost of self-constructed assets includes the costs of materials and direct labour. The cost of replacing a part of an item of property, plant and equipment is recognized in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Corporation, and its cost can be measured reliably. The carrying amount of the replaced part is derecognized and included in profit or loss. The costs of the day-to-day servicing of property, plant and equipment are recognized in profit or loss as incurred. Depreciation is recognized so as to write off the cost of assets less their residual values over their estimated useful lives, when the assets are available for use. The estimated useful lives and related depreciation methods are:

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 8 of 46

Oilfield property, plant and equipment Units of production

Leasehold improvements Straight line over the term of the lease

Tools and equipment 20% to 30% declining balance

Computer equipment 30% declining balance

Automotive equipment 30% declining balance

Office equipment 20% declining balance Where components of an item of property, plant and equipment, meeting the recognition criteria of an asset, have different useful lives, they are accounted for as separate items of property, plant and equipment. The gain or loss on disposal or retirement of an item of property, plant and equipment is determined as the difference between the net sale proceeds and the carrying amount of the asset and is recognized in profit or loss in the period the asset is derecognized. Development and production costs (oilfield property, plant and equipment) Development and production expenditures Items of property and equipment, which include petroleum and natural gas development and production assets, are measured at cost (including directly attributable general and administrative costs) less accumulated depletion and depreciation and accumulated impairment losses. Costs include lease acquisition, drilling and completion, production facilities, decommissioning costs, and geological and geophysical costs directly attributable to development and production activities, net of any government programs. When significant parts of an item of property and equipment, including oil and gas properties, have different useful lives, they are accounted for as separate items (major components). Costs related to unsuccessful development wells or damaged wells are expensed immediately as losses on disposal. Subsequent costs Costs incurred subsequent to development and production that are significant are recognized as oil and gas assets only when they increase the future economic benefits embodied in the specific assets to which they relate. All other expenditures are recognized in income as incurred. Such capitalized oil and gas interests generally represent costs incurred in developing proved and probable reserves and bringing in or enhancing production from such reserves, and are accumulated on a field or area basis. The carrying amount of any replaced or sold component is derecognized. The costs of day-to-day servicing of property and equipment are recognized in income as incurred. Depletion and depreciation The net carrying value of oil and gas properties is depleted using the units of production method by reference to the ratio of production in the period to the related proved and probable reserves, taking

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 9 of 46

into account estimated future development costs necessary to bring those reserves into production. Future development costs are estimated taking into account the level of development required to produce reserves. These estimates are reviewed by independent reserve engineers at least annually. Major development projects are not depleted until production commences. Goodwill Goodwill represents the excess of the purchase price of a business acquisition over the estimated fair value of the net assets acquired, including tangible and identifiable intangible assets, at the date of acquisition. Goodwill is not amortized but is tested for impairment annually or more frequently if events or changes in circumstances indicate a potential impairment. Gains and losses on the disposal of an entity include the carrying amount of goodwill relating to the entity sold. Intangible assets Acquired intangible assets Intangible assets acquired individually or as part of a group of other assets are recorded at cost less accumulated amortization and accumulated impairment losses. Amortization is provided over the estimated useful life of the assets. The estimated useful life and amortization method are reviewed annually, with the effect of any changes in estimate being accounted for on a prospective basis. Amortization has been calculated using the following annual rates and methods:

Fully paid-up license Straight-line basis over 15 years

Patents Straight-line basis over 10 to 14 years Software 100% declining balance Internally generated intangible assets - Research and development As at August 31, 2012 and 2011 and September 1, 2010, no development costs have been capitalized. Expenditures on research activities, undertaken with the prospect of gaining new scientific or technical knowledge and understanding, are recognized in profit or loss as an expense as incurred. Impairment of non-financial assets Non-financial assets with indefinite useful lives Intangible assets with indefinite useful lives are tested annually for impairment at the cash generating unit (“CGU”) level. A CGU is the smallest identifiable group of assets that generates cash inflows largely independent of the cash inflows from other assets or groups of assets.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 10 of 46

Non-financial assets with finite useful lives The Corporation assesses the carrying amounts non-financial assets including property, plant and equipment and intangible assets with finite useful lives when events or changes in circumstances indicate that the carrying amount may not be recoverable. Internal factors, such as budgets and forecasts, as well as external factors, such as expected future prices, costs and other market factors are monitored to determine if indications of impairment exist. For the purpose of impairment testing, assets are grouped together into CGU’s. The assets of the corporate head office are allocated on a reasonable and consistent basis to CGUs or groups of CGUs. The carrying amounts of assets of the corporate head office that have not been allocated to a CGU are compared to their recoverable amounts to determine if there is any impairment loss. An impairment loss is the amount equal to the excess of the carrying amount over the recoverable amount. The recoverable amount is the higher of value in use (being the net present value of expected pre-tax future cash flows of the relevant asset) and the fair value less costs to sell the asset. The best evidence of fair value is the quoted price in an active market or a binding sale agreement for the same or similar asset. Where neither exists, the fair value is based on the best information available to estimate the amount the Corporation could obtain from the sale of the asset in an arm’s length transaction. This is often accomplished by using discounted cash flow techniques. In assessing value in use, the estimated future cash flows to be derived from the CGU are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For oil and gas assets, this is the present value of future cash flows expected to be derived from production of proved and probable reserves. Fair value less cost to sell is assessed utilizing market valuation based on an arm’s length transaction between active participants. For CGUs with goodwill associated with them, an impairment loss is allocated first to any goodwill and then pro rata to other assets within the group. If, after the Corporation has previously recognized an impairment loss, circumstances indicate that the fair value of the impaired asset is greater than the carrying amount, the Corporation reverses the impairment loss by the amount the revised fair value exceeds the carrying amount, to a maximum of the previous impairment loss. In no case shall the revised carrying amount exceed the original carrying amount, after depreciation or amortization, that would have been determined if no impairment loss had been recognized. Impairment of goodwill is not reversed. Revenue recognition Revenue from the sale of goods and services is recognized when the Corporation has transferred to the buyer the significant risks and rewards of ownership of the goods, the Corporation retains neither the continuing managerial involvement nor effective control over the goods sold, the amount of revenue can be measured reliably, it is probable that the economic benefits associated with the transaction will flow to the Corporation, and the costs incurred or to be incurred with

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 11 of 46

respect of the transaction can be measured reliably. Revenue is reduced for estimated warranty claims, customer returns, rebates and other similar allowances. Service revenue and royalties Licensing royalties and technology fees are recognized over the term of the contract. Revenue from oilfield services is recognized when the underlying services are provided. Revenue from the sale of rental equipment is recognized when the equipment is delivered and accepted by third party customers. Production fee and operator revenue Revenue associated with the production and sale of crude oil owned by the Corporation is recognized in the period title passes to the external party. Share-based payments The Corporation has an equity-settled share-based payment plan for certain employees and others providing similar services as described in Note 12(d). The fair value of a stock option is calculated at the date of grant and is expensed over the vesting period of those stock options with a corresponding entry to Shareholders’ equity. The Corporation uses the Black-Scholes model to calculate the fair value of stock options issued, which requires certain assumptions be made at the time the stock options are awarded, including the expected life of the stock option, the expected number of granted stock options that will vest and the expected future volatility of the stock. The fair value of stock options is only re-measured if there is a modification to the terms of the stock options, such as a change in exercise price or legal life. Details regarding the determination of the fair value of equity-settled share-based transactions are included in Note 12. Any consideration paid by stock option or warrant holders for the purchase of stock, together with any amount previously recognized in contributed surplus are credited to issued share capital. If plan entitlements are repurchased from the holder, the consideration paid is charged to deficit. The Corporation has no cash-settled instruments. Employee benefits The costs of all short-term employee benefits are measured on an undiscounted basis and are expensed during the period in which the employee renders the related service. A liability is recognized for the amount expected to be paid under short-term cash bonus or profit-sharing plans if the Corporation has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee and the obligation can be estimated reliably. Provisions Provisions are recognized when the Corporation has a present obligation (legal or constructive) as a result of a past event, it is probable that the Corporation will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation. Where the Corporation

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 12 of 46

expects some or all of a provision to be reimbursed, for example, under an insurance contract, the reimbursement is recognized as a separate asset, but only when the reimbursement is virtually certain. A contingent liability is disclosed where the existence of an obligation will only be confirmed by future events or where the amount of the obligation cannot be measured with reasonable reliability. Contingent assets are not recognized, but are disclosed where an inflow of economic benefits is probable. Onerous contracts Present obligations arising under onerous contracts are recognized and measured as provisions. An onerous contract is considered to exist where the Corporation has a contract under which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received. The Corporation is not party to any onerous contracts at August 31, 2012, 2011 and September 1, 2010. Decommissioning liabilities The Corporation provides for future decommissioning liabilities related to its oil and gas activities based on current legislation, constructive obligations and industry operating practices. Decommissioning liabilities are recognized as a liability in the period in which they are incurred. When the liability is initially recognized, an amount equivalent to the liability is capitalized as a cost of the related oil and gas asset. The liability recognized is the estimated future cost of decommissioning, discounted to its net present value using a pre-tax rate that reflects the current market assessment of the time value of money which is determined based on government bond interest rates and inflation rates. The provision for decommissioning liability is reviewed and adjusted each period to reflect developments which could include changes in closure dates, legislation, and the discount rate or estimated future costs. Changes in the estimated amount or timing of the decommissioning costs are recorded prospectively by recording an adjustment to the decommissioning liability and a corresponding adjustment to the related asset. The unwinding of the present value on the decommissioning liability is recognized as a financing cost. Income taxes The Corporation recognizes deferred income tax assets to the extent that it is probable that taxable profit will be available to allow the benefit of that deferred income tax asset to be utilized. Assessing the recoverability of deferred income tax assets requires the Corporation to make significant estimates related to expectations of future taxable income. Estimates of future taxable income are based on forecasted cash flows from operations and the application of existing tax laws. To the extent that future cash flows and taxable income differ significantly from estimates, the ability of the Corporation to realize the deferred income tax assets recorded at the reporting date could limit the ability of the Corporation to obtain tax deductions in future periods.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 13 of 46

Leases The Corporation determines whether a lease exists at the inception of an arrangement. A lease exists when one party is effectively granted control of a specific asset over the term of the arrangement. Leases are classified as finance leases whenever terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments under operating leases are recognized in profit or loss on a straight-line basis over the term of the lease. Lease incentives received or granted are recognized in profit or loss as an integral part of the total lease expense or revenue. Financial instruments Management determines the classification of financial assets and financial liabilities at initial recognition and, except in very limited circumstances, the classification is not changed subsequent to initial recognition. The classification depends on the purpose for which the financial instruments were acquired, their characteristics and/or management’s intent. Transaction costs with respect to instruments not classified as held-for-trading are recognized as an adjustment to the cost of the underlying instruments and amortized using the effective interest method. The Corporation’s financial instruments are classified in the following categories: Financial assets An instrument is classified as fair value through profit or loss (“FVTPL”) if it is held-for-trading or is designated as such upon initial recognition. A financial asset is classified as held-for-trading if acquired principally for the purpose of selling in the short-term or if so designated by management. Financial instruments included in this category are initially recognized at fair value and transactions costs are taken directly to earnings along with gains and losses arising from changes in fair value. As at August 31, 2012, August 31, 2011 and September 1, 2010 the Corporation had no financial assets recorded at FVTPL. Financial assets designated as loans and receivables are measured at amortized cost. Cash and cash equivalents and trade and other receivables are classified as loans and receivables and are initially recognized at fair value including direct and incremental transaction costs and are subsequently measured at amortized cost, using the effective interest method, reduced for any impairment losses. A provision for impairment of trade accounts receivable is established when there is objective evidence that an amount will not be collectible or, in the case of long-term receivables, if there is evidence that the amount will not be collectible in accordance with payment terms.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 14 of 46

Financial liabilities Trade accounts payable and accrued liabilities are initially recognized at fair value including direct and incremental transaction costs and are subsequently measured at amortized cost using the effective interest method. Financial liabilities designated as other liabilities are measured at amortized cost. Derivative instruments Derivative instruments, including embedded derivatives, are recorded at fair value unless exempted from derivative treatment as a normal purchase and sale. All changes in their fair value are recorded in income. As at August 31, 2012, August 31, 2011 and September 1, 2010 the Corporation had no derivative instruments. Derecognition of financial assets and liabilities A financial asset is derecognized when its contractual rights to the cash flows that compose the financial asset expire or substantially all the risks and rewards of the asset are transferred. A financial liability is derecognized when the obligation under the liability is discharged, cancelled or expired. Gains and losses on derecognition are recognized within financing income and financing costs respectively. Financial instrument measurement hierarchy All financial instruments are required to be measured at fair value on initial recognition. For those financial assets or liabilities measured at fair value at each reporting date, financial instruments and liquidity risk disclosures require a three-level hierarchy that reflects the significance of the inputs used in making the fair value measurements. These levels are defined below: Level 1: determined by reference to quoted prices in active markets for identical assets and

liabilities;

Level 2: valuations using inputs other than the quoted prices for which all significant inputs are based on observable market data, either directly or indirectly; and

Level 3: valuations using inputs that are not based on observable market data. The Corporation had no financial assets recorded at fair value at August 31, 2012, August 31, 2011 and September 1, 2010.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 15 of 46

Impairment of financial assets At each reporting date the Corporation assesses whether there is any objective evidence that a financial asset or group of financial assets is impaired. A financial asset or group of financial assets is impaired if there is objective evidence that the estimated future cash flows of the financial asset of the group or financial assets have been negatively impacted. Evidence of impairment may include indicators that debtors are experiencing financial difficulty, default or delinquency in interest or principal payments, or other observable data which indicates that there is measureable decrease in the estimated future cash flows. If an impairment loss has occurred, the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected credit losses that have not yet been incurred). The carrying amount of the asset is reduced through the use of an allowance account, and the loss is recognized in financing costs. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognized, the previously recognized impairment loss is increased or reduced by adjusting the allowance account. Equity instruments An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Corporation are recorded at proceeds received, net of direct issue costs.

4. RECENT ACCOUNTING PRONOUNCEMENTS The Corporation has reviewed new and revised accounting pronouncements that have been issued but are not yet effective and determined that the following may have an impact on the Corporation:

a) IFRS 9 - Financial instruments IFRS 9, Financial Instruments (“IFRS 9”), was issued by the IASB in November 2009 and will replace IAS 39, Financial Instruments: Recognition and Measurement (“IAS 39”). IFRS 9 replaces the multiple rules in IAS 39 with a single approach to determine whether a financial asset is measured at amortized cost or fair value and a new mixed measurement model for debt instruments having only two categories: amortized cost and fair value. The approach in IFRS 9 is based on how an entity manages its financial instruments in the context of its business model and the contractual cash flow characteristics of the financial assets. This standard also requires a single impairment method to be used, replacing the multiple impairment methods in IAS 39. IFRS 9 is effective for annual periods beginning on or after January 1, 2015. The Corporation is currently evaluating the impact of this standard on its consolidated financial statements.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 16 of 46

b) IFRS 10 - Consolidated financial statements

IFRS 10, Consolidated Financial Statements (“IFRS 10”), was issued by the IASB in May 2011 and will replace SIC 12, Consolidation - Special Purpose Entities, and parts of IAS 27, Consolidated and Separate Financial Statements. Under the existing IFRS, consolidation is required when an entity has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. IFRS 10 establishes principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities. This standard (i) requires an entity that controls one or more other entities to present consolidated financial statements; (ii) defines the principle of control and establishes control as the basis for consolidation; (iii) sets out how to apply the principle of control to identify whether an investor controls an investee and therefore must consolidate the investee; and (iv) sets out the accounting requirements for the preparation of consolidated financial statements. IFRS 10 is effective for annual periods beginning on or after January 1, 2013. The Corporation is currently evaluating the impact of this standard on its consolidated financial statements.

c) IFRS 11 - Joint arrangements IFRS 11, Joint Arrangements (“IFRS 11”), was issued by the IASB in May 2011 and will supersede IAS 31, Interest in Joint Ventures, and SIC 13, Jointly Controlled Entities – Non-monetary Contributions by Venturers, by removing the option to account for joint ventures using proportionate consolidation and requiring equity accounting. Venturers will transition the accounting for joint ventures from the proportionate consolidation method to the equity method by aggregating the carrying values of the proportionately consolidated assets and liabilities into a single line item on their financial statements. In addition, IFRS 11 will require joint arrangements to be classified as either joint operations or joint ventures. The structure of the joint arrangement will no longer be the most significant factor when classifying the joint arrangement as either a joint operation or a joint venture. IFRS 11 is effective for annual periods beginning on or after January 1, 2013. The Corporation is currently evaluating the impact of this standard on its consolidated financial statements.

d) IFRS 12 - Disclosure of interests in other entities IFRS 12, Disclosure of Interests in Other Entities (“IFRS 12”), was issued by the IASB in May 2011. IFRS 12 requires enhanced disclosure of information about involvement with consolidated and unconsolidated entities, including structured entities commonly referred to as special purpose vehicles or variable interest entities. IFRS 12 is effective for annual periods beginning on or after January 1, 2013. The Corporation is currently evaluating the impact of this standard on its consolidated financial statements.

e) IFRS 13 - Fair value measurement IFRS 13, Fair Value Measurement (“IFRS 13”), was issued by the IASB in May 2011. This standard clarifies the definition of fair value, required disclosures for fair value measurement, and sets out a single framework for measuring fair value. IFRS 13 provides guidance on fair value in a single standard, replacing the existing guidance on measuring and disclosing fair value which is dispersed among several standards. IFRS 13 is effective for annual periods beginning on or after

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 17 of 46

January 1, 2013. The Corporation is currently evaluating the impact of this standard on its consolidated financial statements.

f) IAS 1 - Presentation of financial statements An amendment to IAS 1, Presentation of Financial Statements (“IAS 1”), was issued by the IASB in June 2011. The amendment requires separate presentation for items of other comprehensive income that would be reclassified to profit or loss in the future if certain conditions are met, from those that would never be reclassified to profit or loss. The effective date is July 1, 2012 and earlier adoption is permitted. The Corporation is currently evaluating the impact of this amendment on its consolidated financial statements.

g) IAS 19 - Employee benefits

An amendment to IAS 19, Employee Benefits (“IAS 19”), was issued by the IASB in June 2011. The amendment requires all actuarial gains and losses to be immediately recognized in other comprehensive income rather than profit and loss and requires expected returns on plan assets recognized in profit or loss to be calculated based on the rate used to discount the defined benefit obligation. The amended standard is effective for annual periods beginning on or after January 1, 2013 and earlier adoption is permitted. The Corporation is currently evaluating the impact of the amendment on its consolidated financial statements.

h) IAS 27 - Separate financial statements IAS 27, Separate Financial Statements (“IAS 27”), was re-issued by the IASB in May 2011 to only prescribe the accounting and disclosure requirements for investments in subsidiaries, joint ventures and associates when an entity prepares separate financial statements. The consolidation guidance will now be included in IFRS 10. The amendments to IAS 27 are effective for annual periods beginning on or after January 1, 2013. The Corporation is currently evaluating the impact of the amendments on its consolidated financial statements

i) IAS 28 - Investments in associates and joint ventures IAS 28, Investments in Associates and Joint Ventures (“IAS 28”), was re-issued by the IASB in May 2011. IAS 28 continues to prescribe the accounting for investments in associates but is now the only source of guidance describing the application of the equity method. The amended IAS 28 will be applied by all entities that have an ownership interest with joint control of, or significant influence over, an investee. The amendments to IAS 28 are effective for annual periods beginning on or after January 1, 2013. The Corporation is currently evaluating the impact of the amendments on its consolidated financial statements.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 18 of 46

5. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

The preparation of financial statements in conformity with IFRS requires management to make judgements, estimates and assumptions that may affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements about carrying values of assets and liabilities that are not readily apparent from other sources. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to these consolidated financial statements are as follows:

Note 11: Decommissioning liabilities Note 12: Stock based compensation plans

Impairment of non-financial assets The Corporation assess the carrying amount of non-financial assets, including property, plant and equipment, and intangible assets subject to depreciation and amortization at each reporting date to determine whether there are any indicators that the carrying amounts of the assets may be impaired. Goodwill is tested for impairment annually. For the purpose of determining fair value, management assess the recoverable amount of the asset using net present value of the expected future cash flows. Projections of future cash flows are based on factors relevant to the asset could include estimated recoverable production, commodity or contracted prices, foreign exchange rates, productions levels, cash costs of production, capital and reclamation costs. Projections inherently require assumptions and judgements to be made about each of the factors affecting future cash flows. Changes in any of these assumptions or judgements could result in a significant difference between the carrying amount and fair value of these assets. Where necessary, management engages qualified third-party professionals to assist in the determination of fair values. Proved reserves Estimate of recoverable quantities of proved reserves include judgemental assumptions regarding commodity prices, exchange rates, discount rates and production and transportation costs for future cash flows. It also requires interpretation of complex geological and geophysical models in order to make an assessment of the size, shape, depth and quality of reservoirs, and their anticipated recoveries. The economic, geological and technical factors used to estimate reserves may change from period to period. Changes in reported reserves can impact asset carrying values, the provision for decommissioning liabilities and the recognition of deferred tax assets, due to changes in expected future cash flows. Reserve estimates are prepared in accordance with Canadian Oil and Gas Evaluation Handbook and are reviewed by third party reservoir engineers.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 19 of 46

The amounts recorded for depletion and depreciation of oilfield property, plant and equipment, the provision for decommissioning liabilities, and the valuation of property and equipment are based on estimates of proved reserves, production rates, future commodity prices, future costs and the remaining lives and period of future benefit of the related assets. Valuation of equity compensation benefits Management classifies its share-based payment scheme as an equity-settled scheme based on the assessment of its role and that of the employees and brokerage firm in the transaction. In applying its judgement, management consulted with external expert advisors in the accounting and share-based payment advisory industry. The critical assumptions as used in the valuation model are detailed in Note 12.

6. CASH AND SHORT-TERM DEPOSITS The Corporation’s policy is to invest cash in excess of operating requirements in highly secured, liquid investments. Cash and cash equivalents consist of the following:

August 31, August 31, September 1,2012 2011 2010

Cash in bank and on hand 623,356$ 954,802$ 932,805$ Unrestricted investments 14,285,000 23,227,787 28,510,151 Restricted investements 260,928 328,004 -

15,169,284$ 24,510,593$ 29,442,956$

Restricted investments consist of a short-term term deposit held as security against a Letter of Credit issued by TD Canada Trust as security for an operating lease.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 20 of 46

7. PROPERTY, PLANT AND EQUIPMENT

Oilfield Computer,property, Tools automotive

Year ended plant and and and office LeaseholdAugust 31, 2012 equipment Equipment equipment improvements Total

Cost Balance at August 31, 2011 1,131,173$ 5,846,398$ 808,133$ 562,021$ 8,347,725$ Additions 72,304 1,777,835 44,279 11,923 1,906,341 Disposals (72,304) (56,573) - - (128,877)

Balance at August 31, 2012 1,131,173 7,567,660 852,412 573,944 10,125,189

Accumulated depreciation and impairment Balance at August 31, 2011 (305,265) (2,087,536) (573,832) (23,315) (2,989,948) Additions (63,622) (844,858) (44,158) (58,219) (1,010,857) Disposals - 47,796 - - 47,796

Balance at August 31, 2012 (368,887) (2,884,598) (617,990) (81,534) (3,953,009)

Net book value Balance at August 31, 2012 762,286$ 4,683,062$ 234,422$ 492,410$ 6,172,180$

Oilfield Computer,

property, Tools automotiveYear ended plant and and and office LeaseholdAugust 31, 2011 equipment Equipment equipment improvements Total

Cost Balance at September 1, 2010 1,131,173$ 5,343,871$ 810,133$ - $ 7,285,177$ Additions - 847,863 126,862 562,021 1,536,746 Disposals - (345,336) (128,862) - (474,198)

Balance at August 31, 2011 1,131,173 5,846,398 808,133 562,021 8,347,725

Accumulated depreciation and impairment Balance at September 1, 2010 (238,002) (1,497,353) (629,863) - (2,365,218) Additions (67,263) (731,419) (69,919) (23,315) (891,916) Disposals - 141,236 125,950 - 267,186

Balance at August 31, 2011 (305,265) (2,087,536) (573,832) (23,315) (2,989,948)

Net book value Balance at August 31, 2011 825,908$ 3,758,862$ 234,301$ 538,706$ 5,357,777$

Amortization expense for the year ended August 31, 2012 was $1,010,857 (August 31, 2011 - $891,916.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 21 of 46

Property, plant and equipment includes tools and equipment under construction of $711,638 (August 31, 2011 - $372,657), which is not being depreciated.

Effective July 31, 2012, the Corporation sold 100% of its interests in the Rogers County mineral rights and related oilfield assets (the “Assets”) to a privately-held, arms length buyer (the “Purchaser”) in exchange for cash consideration of $9,863 (US $10,000). Concurrent with the disposition, the Corporation paid the Purchaser $162,740 (US $165,000) for the assumption of and for indemnifying the Corporation of all plugging, abandonment, and environmental remediation efforts related to the Assets. As the Assets were previously written-off, the Corporation recorded a gain on the disposal of the Assets and a gain related to the disposition of the decommissioning liabilities (Note 11). The transaction was recorded as a monetary transaction to an arm’s length party.

8. INTANGIBLE ASSETS Year ended Fully-paidAugust 31, 2012 Patents up license Total

Cost Balance at August 31, 2011 609,092$ 106,990$ 716,082$ Net acquisitions 4,169,806 - 4,169,806 Balance at August 31, 2012 4,778,898.00 106,990.00 4,885,888.00

Accumulated amortization and impairment Balance at August 31, 2011 (199,604) (32,704) (232,308) Amortization (351,257) (10,853) (362,110) Balance at August 31, 2012 (550,861) (43,557) (594,418)

Net book value Balance at August 31, 2012 4,228,037$ 63,433$ 4,291,470$

Year ended Fully-paidAugust 31, 2011 Patents up license Total

Cost Balance at September 1, 2010 523,736$ 106,990$ 630,726$ Additions 85,356 - 85,356

Balance at August 31, 2011 609,092 106,990 716,082

Accumulated amortization and impairment Balance at September 1, 2010 (151,636) (27,776) (179,412) Amortization (47,968) (4,928) (52,896)

Balance at August 31, 2011 (199,604) (32,704) (232,308)

Net book value Balance at August 31, 2011 409,488$ 74,286$ 483,774$

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 22 of 46

Amortization expense for the year ended August 31, 2012 was $362,110 (August 31, 2011 - $52,896. Effective December 23, 2011, the Corporation acquired four patents and a trade name from Vortech Inc., a privately-held Texas company that provided specialized tools for the clean-up of oil well bore damage, stimulation of production and injection and drilling operations. Consideration was $4,083,281 (US $4 million) cash. The fair values ascribed to the acquired intangible assets were as follows:

Fair ValueIndefinite-life intangible asset

Trade name 18,627$

Finite-life intangible assetsPulsating jet tool patent 2,703,891 Self adjusting nozzle patent 1,158,810 Pulsating bit sub patent 155,573 Internal slip connector patent 46,380

4,083,281$

9. GOODWILL Review of impairment The Corporation has attributed $1,222,217 of goodwill to a CGU made up of the equipment and technology operations. The estimated recoverable amount has been determined based on a cash flow model as described below. Key assumptions in the valuation model include cash flows, growth opportunities, and the discount rate. Reasonably possible changes in key assumptions would not cause the recoverable amount of goodwill to fall below the carrying value. The details of how these assumptions were updated are described below. Cash flows Cash flows are projected over a five year period and are based on production and growth plans, internal forecasts, and risk assessments that take into account the unique operations. Revenue and expenses were projected over a five year period based on the Corporation’s long range plan. Revenue and expenses beyond this period were extrapolated using a growth rate of 5% based on average historical growth. Growth opportunities Cash flows from growth opportunities are probability-weighted and related to initiatives management expects to progress on in the medium to long term.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 23 of 46

Discount rate A blended discount rate of 15% was used to discount cash flows in the valuation model, which resulted in an excess of fair value over carrying amount of approximately $520,270 as at August 31, 2012. The valuation is sensitive to changes in the discount rate. A 0.5% increase in the discount rate would lead to a decrease in the excess of the estimated recoverable amount over the carrying amount by approximately $110,750. A corresponding decrease in the discount rate would increase the excess of the estimated recoverable amount over the carrying amount by approximately $123,194. The sensitivity was calculated as of the impairment testing date. The discount rate is based on current market information at the date of valuation.

10. JOINTLY CONTROLLED ASSETS The Corporation conducts its oilfield activities under the terms of production sharing contracts which it considers jointly-controlled operations. The Corporation has included its share of the following:

August 31, August 31, September 1,2012 2011 2010

Current assets - $ 2,900$ 20,267$ Non-current assets 746,813 810,433 843,495 Current liabilities (6,437) - -

740,376$ 813,333$ 863,762$

August 31, August 31, 2012 2011

Revenue 135,068$ 137,175$ Expenses (133,556) (100,692)

1,512$ 36,483$

At August 31, 2012, there were no capital commitments for the Corporation’s jointly controlled assets.

11. DECOMMISSIONING LIABILITY

The Corporation has a decommissioning liability associated with its Rodney South oilfield property, plant and equipment (Note 7) primarily related to the plugging of wells and abandonment costs. The following table summarizes the changes in the decommissioning liability:

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 24 of 46

August 31, August 31, 2012 2011

Balance, beginning of year 378,541$ 374,785$ Accretion expense 4,129 4,503 Disposition of decommissioning obligation (256,821) - Write-up of decommissioning obligation (72,304) - Foreign currency (16,488) (747)

Balance, end of year 37,057$ 378,541$

Rodney South The total undiscounted amount of estimated cash flows required to settle the obligation related to Rodney South is $61,812 (August 31, 2011 - $61,812), which has been discounted using the risk free rate of 3.47%. The majority of these obligations are not expected to be settled for one to twenty-nine years in the future and will be funded from general corporate resources at the time of the retirement and removal.

12. SHARE CAPITAL The Corporation’s authorized and issued share capital is as follows: a) Authorized share capital Unlimited common shares without par value b) Issued common shares The changes in the Corporation’s outstanding common shares were as follows:

Stated StatedNumber capital Number capital

Balance, beginning of period 82,844,574 66,320,249$ 82,814,744 66,288,967$ Stock options exercised (1)(2) 111,666 118,660 29,830 31,282

Balance, end of period 82,956,240 66,438,909$ 82,844,574 66,320,249$

August 31, 2012 August 31, 2011

(1) The 111,666 incentive stock options exercised during the year ended August 31, 2012, at prices ranging from

$0.54 to $0.97 for gross proceeds of $64,800. Of the 111,666 incentive stock options exercised during the year ended August 31, 2012, 10,000 incentive stock options were exercised by a director of the Corporation at a price of $0.97 for gross proceeds of $9,700.

(2) The 29,830 incentive stock options exercised during the year ended August 31, 2011, at a price of $0.59 for gross proceeds of $17,600.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 25 of 46

c) Warrants A summary of the status of the Corporation’s share purchase warrants is presented below:

Exercise Exercise Number price Number price

Outstanding, beginning of period 5,219,085 2.75$ 5,219,085 2.75$ Expired(1) (5,219,085) 2.75 - -

Outstanding, end of period - -$ 5,219,085 2.75$

August 31, 2012 August 31, 2011

(1) The 5,219,085 share purchase warrants expired unexercised on April 27, 2012.

d) Stock-based compensation plan The Corporation maintains an Employee, Director, Officer and Consultant Stock Option Plan under which the Corporation may grant incentive stock options for up to 10,771,588 shares of the Corporation at an exercise price equal to or greater than the market price of the Corporation’s stock at the date of grant. All stock options awarded are exercisable for a period of five years and vest in equal tranches at three (3) month intervals over a period of eighteen (18) months. Movements in stock options during the year A summary of the status of the Corporation’s Stock Option Plan is presented below:

Number Number

Outstanding, beginning of period 2,581,500 $ 1.15 2,845,920 $ 1.74Granted 415,000 0.70 1,020,000 1.12Exercised (111,666) 0.58 (29,830) 0.59Forteited (434,834) 1.38 - - Expired (70,000) 0.70 (1,254,590) 2.49

Outstanding, end of period 2,380,000 $ 1.06 2,581,500 $ 1.15

August 31, 2012 August 31, 2011Weighted

averageexercise

price

Weightedaverageexercise

price

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 26 of 46

Fair value of stock options granted during the period The fair value for the compensation costs of stock options issued to both employees and non-employees were calculated using the Black-Scholes option pricing model resulting in an additional charge to general and administrative expense with a corresponding increase in contributed surplus, assuming the following weighted average assumptions: Inputs into the model

Weighted Average Weighted AverageAugust 31 August 31

2012 2011

Share price at date of grant $ 0.70 $ 1.12Exercise price $ 0.70 $ 1.12Risk-free rate (based on 5 year Government of Canada bond) 1.33% 2.23%Expected volatility 93.72% 104.49%Dividend rate 0% 0%Expected life 5 years 5 yearsWeighted average value of options granted during the period $ 0.50 $ 0.86

Stock options outstanding at the end of the period The table below represents the amount of stock options outstanding at August 31, 2012:

Options outstanding

Remaining contractual

life in yearsOptions

exercisable

Remaining contractual

life in years

$ 2.90 65,000 0.82 65,000 0.82 $ 2.902.05 200,000 0.51 200,000 0.51 2.051.65 185,000 0.48 185,000 0.48 1.651.45 105,000 2.86 105,000 2.86 1.451.13 200,000 3.73 166,667 3.73 1.130.97 545,000 3.04 545,000 3.04 0.970.94 75,000 3.53 62,500 3.53 0.940.73 175,000 4.30 85,333 4.30 0.000.72 245,000 2.01 245,000 2.01 0.720.66 105,000 4.08 52,500 4.08 0.660.59 30,000 1.85 30,000 1.85 0.590.54 450,000 1.35 450,000 1.35 0.54

2,380,000 2.33 2,192,000 2.15

Awards Outstanding Awards Exercisable

Exercise price Exercise price

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 27 of 46

During the year ended August 31, 2012, the Corporation incurred $524,000 (August 31, 2011 - $648,781) in compensation expense relating to outstanding stock options. The amounts computed according to the Black-Scholes pricing model may not be indicative of the actual values realized upon the exercise of the stock options by the holders. e) Contributed surplus

August 31, August 31,2012 2011

Balance, beginning of period 8,112,618$ 7,477,519$ Share-based payment 524,000 648,781 Stock options exercised (53,861) (13,682)

Balance, end of period 8,582,757$ 8,112,618$

13. REVENUE

August 31, August 31,2012 2011

Service revenue and royalties 5,414,760$ 3,774,089$ Production revenue 208,241 217,535

5,623,001$ 3,991,624$

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 28 of 46

14. EXPENSES BY NATURE

August 31, August 31, 2012 2011

Wages and benefits 3,098,639$ 2,659,402$ Professional and consulting fees 1,526,496 894,574 Depreciation, amortization and depletion 1,367,488 948,282 Sales and marketing 1,110,511 1,010,849 Materials and related costs 945,152 691,324 Office expenses 899,753 805,181 Share-based payments 524,000 648,781 Repairs and maintenance 473,660 376,368 Vehicle 283,019 212,806 Listing and public company fees 228,052 155,154 Other 146,991 51,748 Loss (gain) on disposition of assets (169,939) 173,485

10,433,822$ 8,627,954$

Compensation of key management personnel of the Corporation The Corporation’s key management personnel include its directors, chief executive officer and president, chief financial officer, vice presidents and senior management. The following outlines their compensation:

August 31, August 31,2012 2011

Wages, and other short-term employment benefits 1,179,641$ 1,208,217$ Share-based payments 486,628 574,623 Directors' fees 88,836 76,400

1,755,105$ 1,859,240$

Share-based payments are the fair value of stock options granted to key personnel as disclosed in Note 12.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 29 of 46

Financing Costs Financing costs include the following select information:

August 31, August 31,2012 2011

Financing costs include the followingInterest expense (4,549)$ (2,934)$ Accretion expense on decommissioning liability (4,129) (4,503) Foreign exchange (loss) gain (30,843) (111,377)

(39,521)$ (118,814)$

15. INCOME TAXES

2012 2011

Current income tax expense -$ -$ Deferred income tax expense - -

-$ -$

The tax recovery on the Company's loss before tax differs from the theoretical amount that would arise using the weighted average tax rate applicable to losses of the entity as follows:

2012 2011

Loss before income tax (4,649,142)$ (4,475,214)$

Expected income tax recovery at statutory income tax rate (1,203,054) (1,209,546)

Adjusted for the following:Differences between U.S. And Canadian tax rates on U.S. losses (221,640) (74,389) Stock-based compensation 135,224 174,387 Re-measurement of deferred tax - substantively enacted rates 406,936 (17,963) Expiry of non-capital losses - 268,483 Valuation allowances 831,048 286,492 Non-deductible and other items 51,486 536,510

Net future income tax asset - $ - $

The Corporation’s substantially enacted Canadian statutory tax rate is approximately 25.81% (2011 – 26.88%). The decrease in rate is due to a previously legislated decrease in the federal statutory corporate income tax rates from fiscal 2011 to fiscal 2012.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 30 of 46

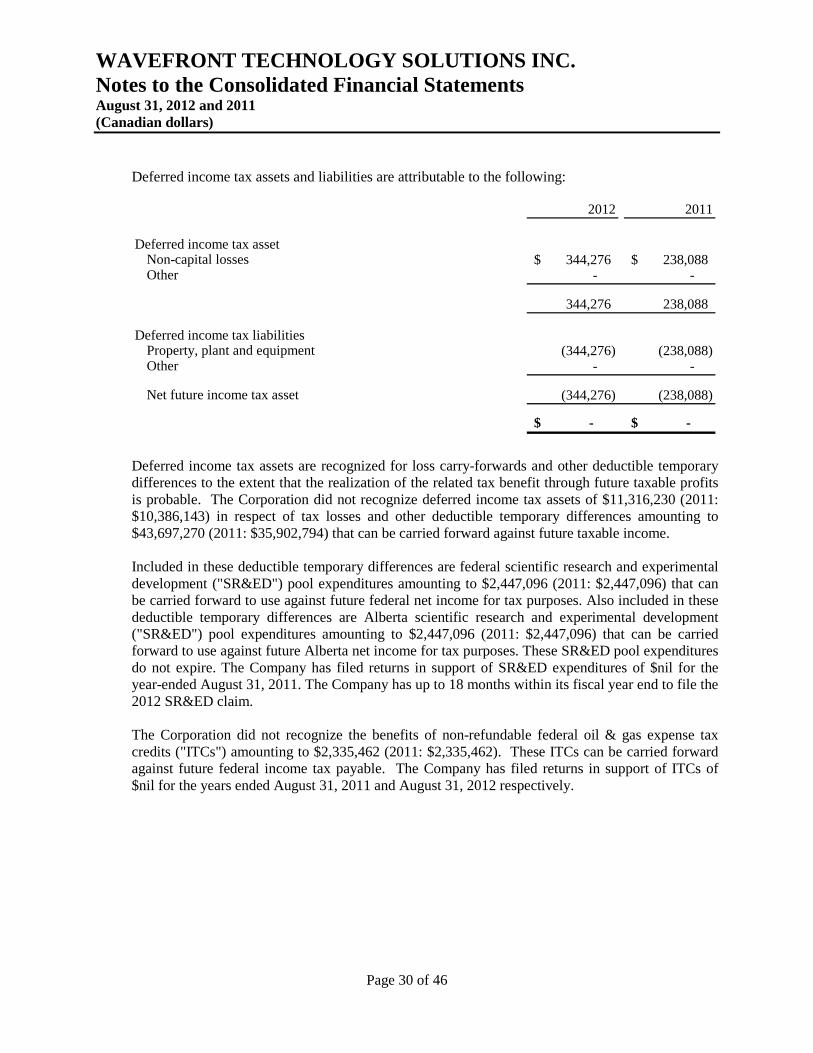

Deferred income tax assets and liabilities are attributable to the following:

2012 2011

Deferred income tax assetNon-capital losses 344,276$ 238,088$ Other - -

344,276 238,088

Deferred income tax liabilitiesProperty, plant and equipment (344,276) (238,088) Other - -

Net future income tax asset (344,276) (238,088)

- $ - $

Deferred income tax assets are recognized for loss carry-forwards and other deductible temporary differences to the extent that the realization of the related tax benefit through future taxable profits is probable. The Corporation did not recognize deferred income tax assets of $11,316,230 (2011: $10,386,143) in respect of tax losses and other deductible temporary differences amounting to $43,697,270 (2011: $35,902,794) that can be carried forward against future taxable income. Included in these deductible temporary differences are federal scientific research and experimental development ("SR&ED") pool expenditures amounting to $2,447,096 (2011: $2,447,096) that can be carried forward to use against future federal net income for tax purposes. Also included in these deductible temporary differences are Alberta scientific research and experimental development ("SR&ED") pool expenditures amounting to $2,447,096 (2011: $2,447,096) that can be carried forward to use against future Alberta net income for tax purposes. These SR&ED pool expenditures do not expire. The Company has filed returns in support of SR&ED expenditures of $nil for the year-ended August 31, 2011. The Company has up to 18 months within its fiscal year end to file the 2012 SR&ED claim. The Corporation did not recognize the benefits of non-refundable federal oil & gas expense tax credits ("ITCs") amounting to $2,335,462 (2011: $2,335,462). These ITCs can be carried forward against future federal income tax payable. The Company has filed returns in support of ITCs of $nil for the years ended August 31, 2011 and August 31, 2012 respectively.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 31 of 46

These non-capital losses expire as follows:

U.S. Canadian

2014 -$ 1,823,383$ 2015 - 1,112,562 2024 669 - 2025 180,377 - 2026 327,314 1,721,014 2027 1,381,982 1,055,478 2028 1,493,262 1,834,185 2029 1,485,648 2,586,521 2030 1,069,737 4,062,139 2031 532,902 2,717,796 2032 1,910,957 3,342,277

8,382,848$ 20,255,355$

16. LOSS PER SHARE The Corporation uses the treasury stock method to calculate diluted earnings per share. Under the treasury stock method, the numerator remains unchanged from the basic earnings per share calculation, as the assumed exercise of the Corporation’s share purchase warrants and stock options do not result in an adjustment to income. The weighted average number of common shares outstanding is 82,926,495 (August 31, 2011 - 82,837,923). Diluted loss per share is computed by giving effect to the potential dilution that would occur if the Corporation’s share purchase warrants or stock options were exercised. The treasury stock method assumes that the proceeds received from the exercise of the “in-the-money” share purchase warrants or stock options are used to repurchase common shares at the average market price for the year ended August 31, 2012. In determining diluted loss per share, the weighted average number of shares outstanding for the year ended August 31, 2012 excluded 484,594 (2011 - 1,297,349) for stock options eligible for exercise where the average market price of the common shares for the year exceeds the exercise price because the result was anti-dilutive in both periods.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 32 of 46

17. CAPITAL MANAGEMENT

The Corporation’s primary objectives when managing capital are as follows:

• To safeguard the Corporation’s ability to continue as a going concern; • To ensure that the Corporation’s business plans are developed so that research and

development and capital expenditure commitment costs do not exceed the Corporation’s financial resources;

• To maintain flexibility in order to preserve the Corporation’s ability to meet financial obligations with a long-term view of maximizing shareholder value; and

• To maintain sufficient cash and cash equivalents and short-term investments to fund its business plan.

The Corporation’s primary uses of capital are to finance commercialization of its PowerwaveTM and PrimawaveTM technologies, tool development and manufacturing, market development, working capital, capital expenditures and operating losses. The Corporation manages its capital structure and makes adjustments to it in the light of changes in economic conditions and the risk characteristics of its underlying assets. The Corporation maintains or adjusts its capital level to enable it to meet its objectives by:

• Realizing proceeds from the disposition of its investments; and • Raising capital through equity financings.

In the management of capital, the Corporation includes the components of shareholders’ equity comprised of share capital, contributed surplus and accumulated deficit to provide capital of $27,771,325 as at August 31, 2012 (2011 - $33,831,668). Since inception, the Corporation has financed its liquidity needs through public offerings and private placements of common shares and interest income. In order to maintain or adjust the capital structure, the Corporation may adjust the number of shares issued, enter into collaborative and/or licence agreements, enter into mergers and acquisitions, acquire debt or enter into some other form of financing facility. In order to maximize funds available for investment, the Corporation does not pay dividends. The Corporation expects its current capital resources will be sufficient to fund operations. The Corporation is not subject to any externally imposed capital requirements.

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 33 of 46

18. FINANCIAL INSTRUMENTS a) Categories of financial instruments The Corporation has classified its financial instruments as follows:

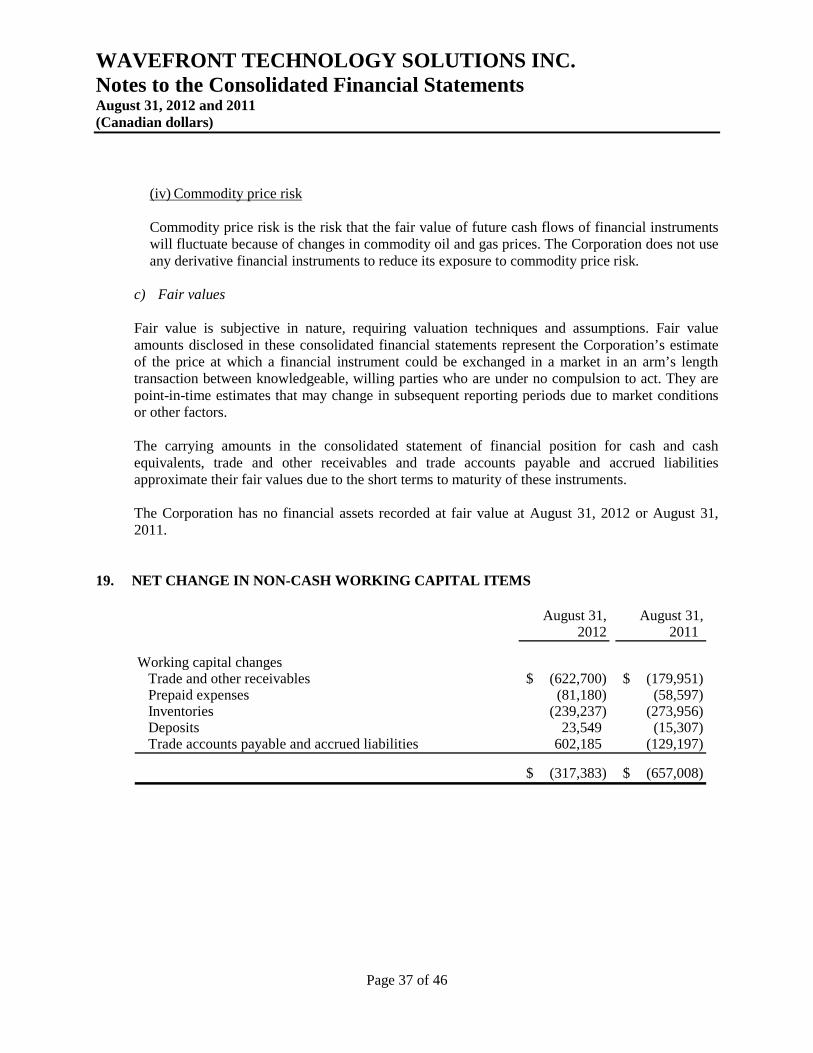

August 31, August 31, September 1,2012 2011 2010

Financial assets Cash and cash equivalents, measured at amortized cost (loans and receivables) 15,169,284$ 24,510,593$ 29,442,956$ Trade and other receivables, measured at amortized cost (loans and receivables) 1,667,743 1,045,043 865,092

Financial liabilities Trade accounts payable and accrued liabilities, measured at amortized cost (other financial liabilities) 1,646,483 1,044,298 1,173,495

b) Financial risk management The Corporation, through its financial assets and liabilities, has exposure to the following risks from its use of financial instruments: credit risk, foreign currency risk, liquidity risk and commodity price risk. An analysis of these risks as at August 31, 2012, is provided below.

(i) Foreign currency risk Foreign currency risk is the risk that the fair value of future cash flows of financial instruments will fluctuate because of changes in foreign currency exchange rates. The Corporation conducts a significant portion of its business activities in the United States, in U.S. dollars. Cash and cash equivalents, trade and other receivables, trade accounts payables and accrued liabilities that are denominated in foreign currencies will be affected by the changes in the exchange rates between the Canadian dollar and U.S. dollar. The Corporation currently does not enter into any derivative financial instruments to reduce its exposure to foreign currency risk. The tables that follow provide an indication of the Corporation’s exposure to changes in the value of the U.S. dollar relative to the Canadian dollar as at and for the year ended August 31, 2012. The analysis is based on financial assets and liabilities denominated in U.S. dollars at the statement of financial position date (“statement of financial position exposure”), and U.S. dollar denominated revenue and operating expenses during the year (“operating exposure”).

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 34 of 46

U.S. dollarsStatement of financial position exposureAs at August 31, 2012Cash and cash equivalents 321,232$ Trade and other receivables 454,492 Trade accounts payable and accrued liabilities (99,485)

Net statement of financial position exposure 676,239$

As at August 31, 2011Cash and cash equivalents 198,456$ Trade and other receivables 330,694 Trade accounts payable and accrued liabilities (142,258)

Net statement of financial position exposure 386,892$

U.S. dollarsOperating exposureYear ended August 31, 2012Sales 1,180,042$ Operating expenses (884,729)

Net operating exposure 295,313$

Year ended August 31, 2011Sales 748,835$ Operating expenses (751,633)

Net operating exposure (2,798)$

Based on the Corporation’s foreign currency exposure for fiscal 2012, as noted above, with other variables unchanged, a 5% change in the Canadian dollar would have impacted net loss as follows: Net statement of financial position exposure 33,812$ Net operating exposure 14,766

Change in net loss 48,578$

(ii) Credit risk Credit risk arises from the potential that a counterparty to a financial instrument fails to meet its contractual obligations. The Corporation manages credit risk associated with the cash and cash equivalents by investing primarily in cash equivalents issued by Schedule 1 Canadian banks and government investment instruments. While the Corporation does not hold asset-backed securities directly, these parties may be exposed in varying degrees to asset-backed

WAVEFRONT TECHNOLOGY SOLUTIONS INC. Notes to the Consolidated Financial Statements August 31, 2012 and 2011 (Canadian dollars)

Page 35 of 46