w4 g2 simplification and saving

TRANSCRIPT

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 1/23

SIMPLIFICATION AND SAVING

Lee Wei Hao

Loh Yi Wen, Yvonne

Mohana Priya

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 2/23

Introduction

• Household financial decisions are complicated.

▫ Individuals put off confronting these decisions

▫ Discourages employees from timely enrollment inemployer-sponsored savings plan even when they

prefer to participate.

• Can lead to substantial reductions in LR wealthaccumulation

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 3/23

QUICK ENROLLMENT [QE](By Choi, Laibson, Madrian (CLM))

Asset Allocation(Pre-selected)

Contribution Rate(Pre-selected)

ACCEPT REMAINSTATUSQUO

OR

Increased savings planenrollment at 2 firms by

10-20 percentage points

Introduction

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 4/23

Providing repeated opportunities touse QE increases the participation

rate

Just as effective at raisingenrollment when its pre-selectedcontribution rate = 4% of salary

(CLM – 2-3% of salary)

Complementary intervention – Easy Escalation

Allows already-participatingemployees to increase contribution

rate to 6% of salary

Assess the effect up to 54 monthsafter its implementation

(CLM – 11 months)

Introduction

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 5/23

Quick Enrollment Implementations – Company A

40,000 employeesImmediately eligible for the savings plan

Could make before and after tax contributions up to 100% of pay

50% matching contribution for the 1st 4% or 6%

Prior to July 2003

Standard opt-in

Choose:(1) before and

after taxcontribution

rate(2) allocation of funds

July 2003 -Dec 2003

QE – For new employees

Contribution rates:Before-tax = 2% After-tax = 0%

Allocation: Evenly split between money market fund and a

balanced fund

Feb 2004

Adopted QE asa permanent

feature

March 2006

QE–

For new employees

Contribution rates:Before-tax = 4%;

After-tax = 0%

Allocation: 100% inan age-

appropriate targetdate retirement

fund

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 6/23

Quick Enrollment Implementations – Company A

2nd

ImplementationMid-June 2004 to mid-October 2004Seasoned employees not enrolled in savings plan

Conjunction with the

adoption of Web-based

benefitsmanagement

system

Non-enrolled

employees canenroll in thesavings plans

using new interface

Allocation:

split evenly betweenmoney market

fund and balanced fund

Pre-taxcontributionnot pre-selected

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 7/23

Impact of Quick Enrollment – Company A

Impact of 2nd QE implementation on savings plan participation

Sample: employees who were continuously employed at Company A and

eligible to participate in its savings plan from Jan 1, 2002 to Dec 31, 2005.

Participation rate increase at 0.3percentage points per month

Participation rate increase at 2.1percentage points per month

Increasing at 0.02 percentagepoints per month

No sign of subsequent reversal

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 8/23

Impact of Quick Enrollment – Company A

Impact of 1st QE implementation on savings plan participation

Feb to June2002/2003

Feb to June2004/2005

March toJune 2006

Control groupNew hires without QE;

exposed to the 2nd QE

Attended orientationContribution rate =

2% Allocation: Split evenly

between money market fund and a

balanced fund

Attended orientation

Contribution rate =4%

Allocation: Target dateretirement fund

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 9/23

Impact of Quick Enrollment – Company A

3 percentagepoints higher

21% - 46% / 25 percentagepoints increase

26 percentagepoints increase

Impact of 1st QE implementation on savings plan participation

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 10/23

Impact of Quick Enrollment – Company A

Impact of QE on initial contribution rates

Cluster atdefault rates

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 11/23

Impact of Quick Enrollment – Company A

Impact of QE on initial contribution rates

Increased the fraction of employees at each total contribution ratebetween 1% and 6%, but caused little increase at higher contributionrates

f Q k ll

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 12/23

Impact of Quick Enrollment – Company A

Impact of QE on asset allocation

Feb to June2002/2003

Feb to June2004/2005

March toJune 2006

0.4% split theircontribution flows

evenly

54% split theircontribution evenly

78% contribute to atarget date retirement

fund

2nd ImplementationMid-June 2004 to mid-October 2004

79% split theircontribution evenly

I f Q i k E ll C A

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 13/23

Impact of Quick Enrollment – Company A

Contribution rate pre-select persistence under QE

• Saving plan participation is very persistent for all cohorts

• Persistence at initial contribution rates is also high

• Early participators who enrolled at the QE contribution rate exhibitless persistence than those before QE.5

▫ Will forgo matching contributions (matching rate = 6%)

I f Q i k E ll C A

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 14/23

Impact of Quick Enrollment – Company A

Asset allocation pre-select persistent under QE

Remarkablysimilar

Stickier

• 2006 QE is considerably stickier because target date retirementfunds are marketed as customized solutions to the asset allocationproblemmore attractive

• 2004 QE exhibit more asset allocation persistence

▫

Attracted a particularly inertial population

I t f Q i k E ll t C A

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 15/23

Impact of Quick Enrollment – Company A

Effect of QE on average contribution rates

Q i k E ll t d E E l ti C B

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 16/23

Quick Enrollment and Easy Escalation - Company B

20,000 employeesImmediately eligible for the savings plan

Could make before and after tax contributions up to 25% of pay 55% to 125% matching contribution for the 1st 6%

Investment options increase from 9 to 12The match was invested in the employer stock

Could not be fully diversified until 55Quick Enrollment implemented in 2003

Jan 2003

Mail to employees who were not

enrolled in savingsplan

If participate,Contribution rates: before-tax = 3%

Allocation: money market fund

Jan 2004

Sent to non-enrolled employees

Contribution rates: before-tax = 3%

Allocation: money marketfund

Feb 2005

Sent to non-enrolled employees

Contribution rates: before-tax = 3%

Allocation: lifestyle fund

Sent Easy Escalation forms to already-enrolled employees (<6%)Increase contribution rate to 6%

I t f Q i k E ll t d E E l ti C B

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 17/23

• Compare with cohorts before QE: 1 Mar 2000, 1 Feb 2001, 1 Feb 2002

• Standard enrollment (2000-2002) cohorts experienced slow andsteady enrollment increases over time

• QE cohort – participation increases till 41% at 26 months

▫ Each mailing on average converted 10% of previously non-enrolled

recipients into savings plan participants.

Impact of Quick Enrollment and Easy Escalation – Company B

Impact of QE on enrollment

I t f Q i k E ll t d E E l ti C B

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 18/23

Impact of Quick Enrollment and Easy Escalation – Company B

Impact of Easy Escalation on movements to the match threshold

• Only a small fraction of contributors changed their contribution rates▫ Except Feb 2004 and Feb/Mar 2005Process of the forms

• The effect of each mailing is 14.7%

Impact of Q ick Enrollment and Eas Escalation Compan B

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 19/23

•

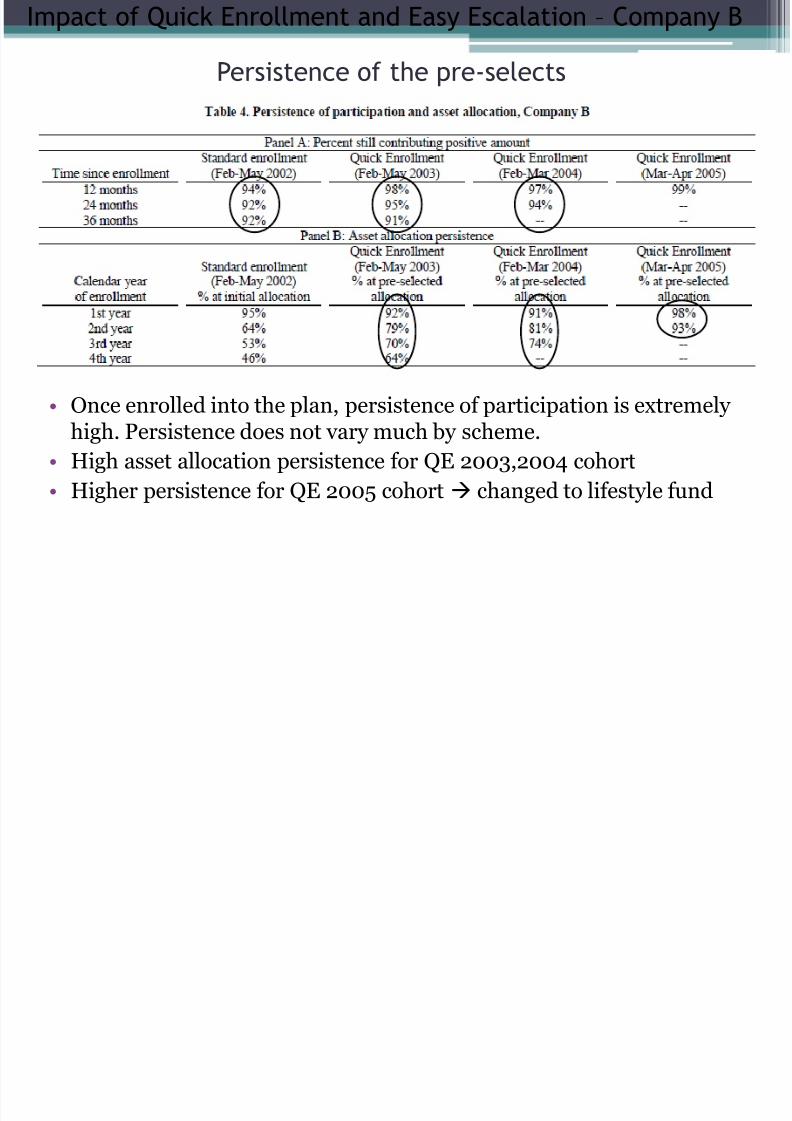

Once enrolled into the plan, persistence of participation is extremely high. Persistence does not vary much by scheme.

• High asset allocation persistence for QE 2003,2004 cohort

• Higher persistence for QE 2005 cohort changed to lifestyle fund

Impact of Quick Enrollment and Easy Escalation – Company B

Persistence of the pre-selects

Impact of Quick Enrollment and Easy Escalation Company B

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 20/23

Impact of Quick Enrollment and Easy Escalation – Company B

Impact of QE and Easy Escalation on the average

contribution rate

• Increase in average contribution rate over time

C l i

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 21/23

• QE is a low-cost intervention that reduces the

complexity to make savings decisions.

• It increased savings plan enrollment.

• Participation rates do not subsequently reverse.

• Remains in default for years.

• Easy escalation can also increase contributionrates among those already participated.

Conclusion

C l i

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 22/23

Conclusion

8/2/2019 W4 G2 Simplification and Saving

http://slidepdf.com/reader/full/w4-g2-simplification-and-saving 23/23

THE END