volkswagen – on the road of successvolkswagen – on the road of success goldman sachs investor...

TRANSCRIPT

Volkswagen –

On the Road of SuccessGoldman Sachs Investor VisitWolfsburg, September 22, 2010

22

Volkswagen –

On the Road of Success

Part 1:

Hans Dieter Pötsch, Member of the Board of Management

Part 2: Frank Fiedler, CFO Volkswagen Financial Services AG

Part 3: Dr. Christof

Spathelf, Senior Vice President of Volkswagen Group Manufacturing Overseas

3

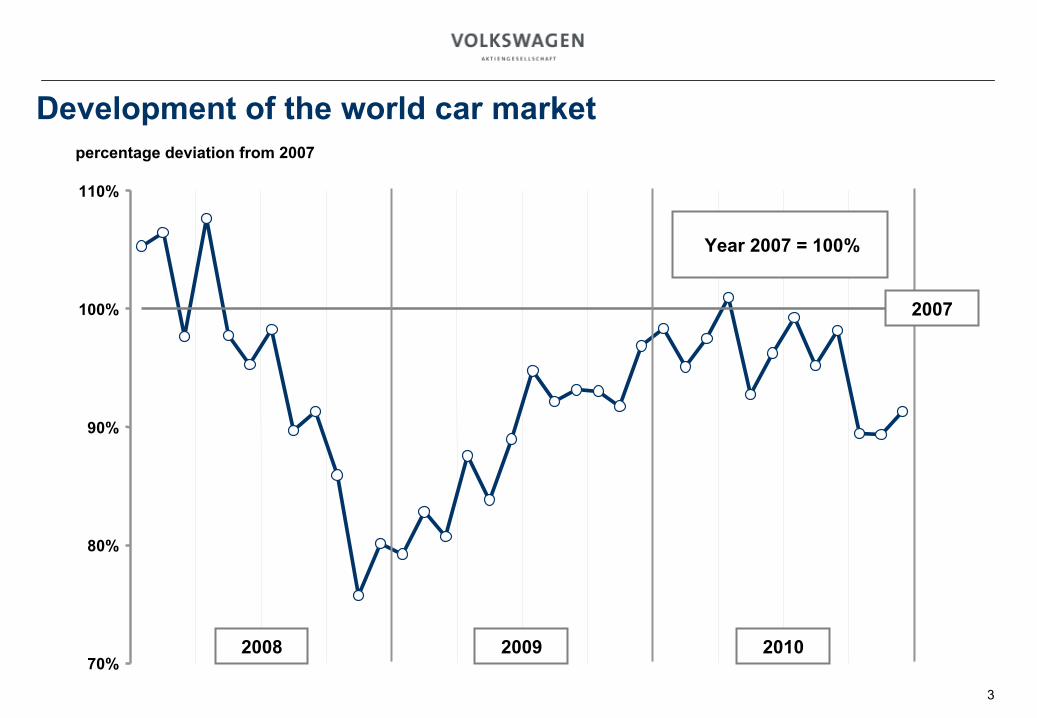

Development

of the world

car

market

70%

80%

90%

100%

110%

percentage

deviation

from

2007

2008

Year

2007 = 100%

2009 2010

2007

41 incl. Scania (Jan-Jun), incl. Trucks and Busses (until

Feb 2009)

World car markets and VW Group deliveries

to customers January to August

2010 vs. 2009

Source: Volkswagen

1

World car

market: +12.4% VW Group: +13.5%

14.4%8.1%

-2.5%

1.0% 4.5%0.3%

4.8%10.2% 9.2%

36.6%41.4%

30.9%

North America Western Europe Central & Eastern Europe

South America Asia

PacificRest of World

Car marketCars + LCV

VW Group Car market VW Group Car market VW Group

Car market VW GroupCar market VW GroupCar market VW Group

55

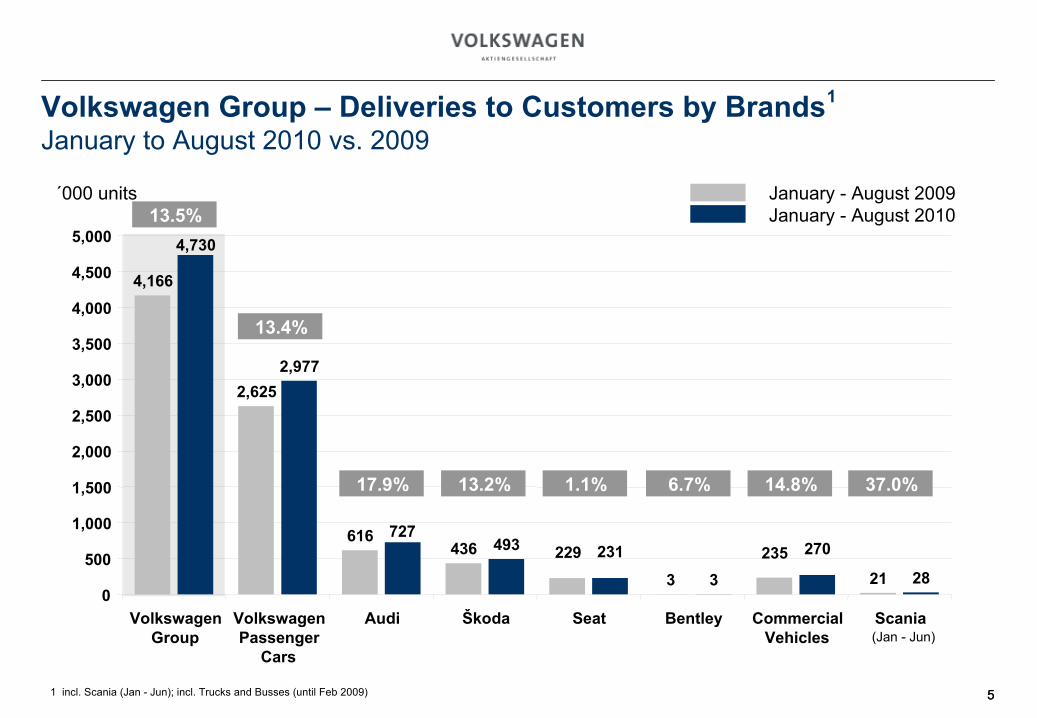

Volkswagen Group –

Deliveries to Customers by Brands January to August 2010 vs. 2009

1

´000 units January

-

August 2009January

-

August 2010

1 incl. Scania (Jan -

Jun); incl. Trucks and Busses (until

Feb 2009)

213 28

436 229 235

4,166

2,625

616

3

231493 270

4,730

2,977

727

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

VolkswagenGroup

VolkswagenPassenger

Cars

Audi Škoda Seat Bentley CommercialVehicles

Scania

13.5%

13.4%

17.9% 13.2% 1.1% 6.7% 14.8% 37.0%

(Jan -

Jun)

66

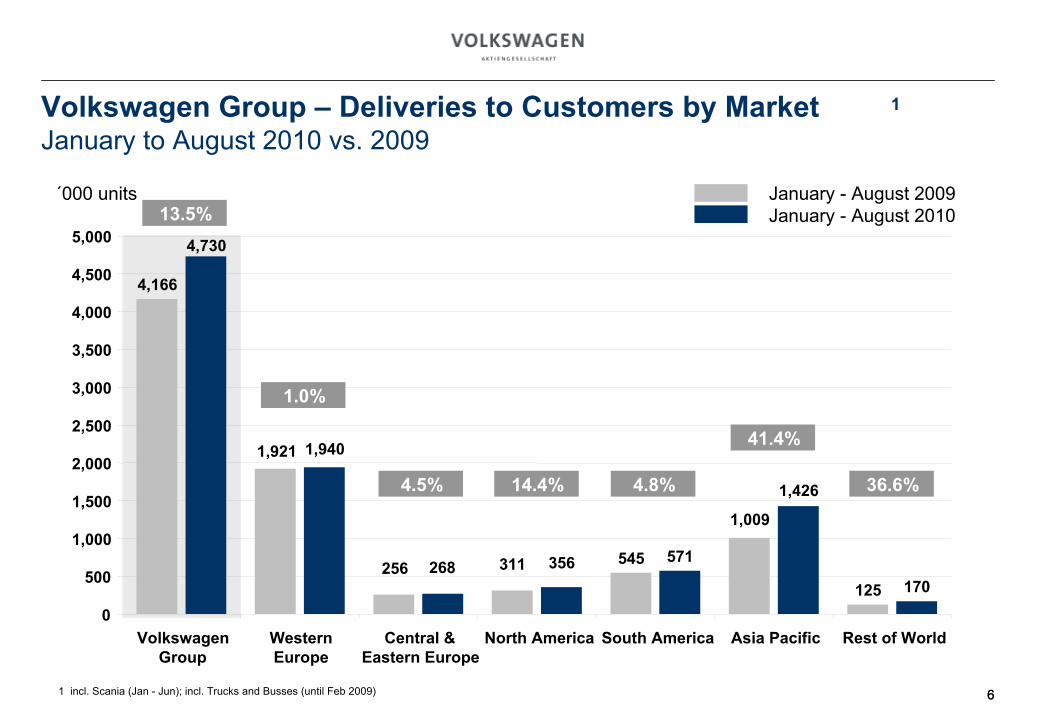

Volkswagen Group –

Deliveries to Customers by Market January to August 2010 vs. 2009

1

´000 units January

-

August 2009January

-

August 2010

1 incl. Scania (Jan -

Jun); incl. Trucks and Busses (until

Feb 2009)

125 170

1,921

545256 311

1,009

4,166

1,426

1,940

571268 356

4,730

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

VolkswagenGroup

WesternEurope

Central &Eastern Europe

North America South America Asia

Pacific Rest of World

13.5%

1.0%

4.5% 14.4% 4.8%

41.4%

36.6%

77

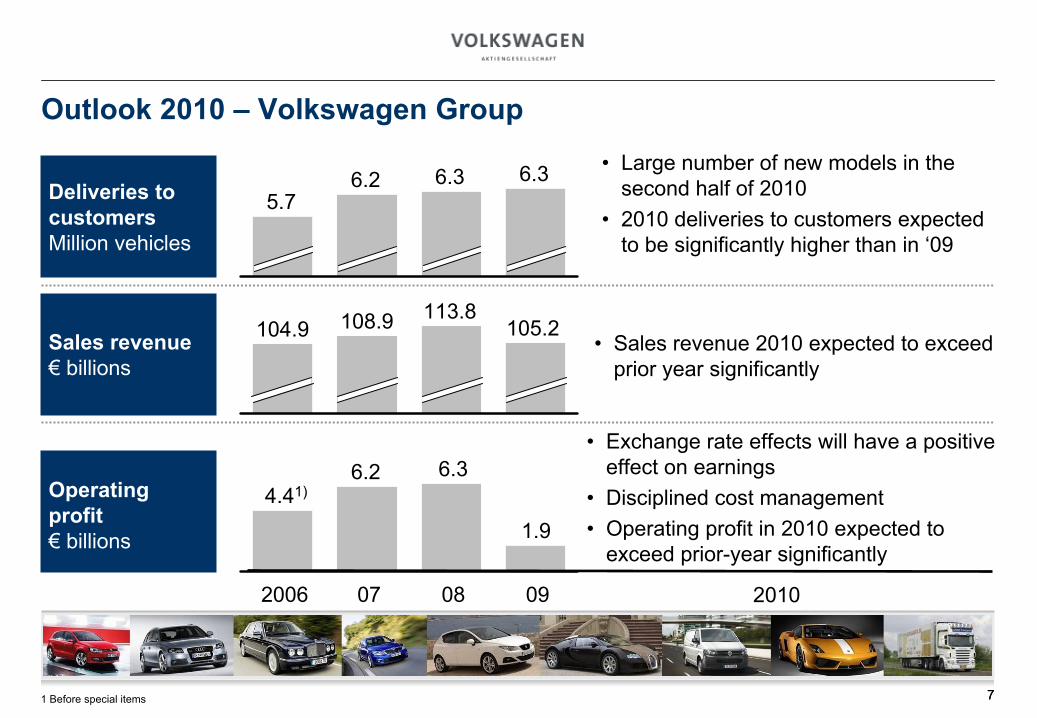

2010

1.9

09

6.3

08

6.2

07

4.41)

2006

Sales revenue€

billions

Operating profit€

billions

105.2113.8108.9104.9

6.36.36.25.7Deliveries to

customersMillion vehicles

•

Large number of new models in the second half of 2010

•

2010 deliveries to customers expected to be significantly higher than in ‘09

•

Sales revenue 2010 expected to exceed prior year significantly

•

Exchange rate effects will have a positive effect on earnings

•

Disciplined cost management•

Operating profit in 2010 expected to exceed prior-year significantly

1 Before special items

Outlook 2010 –

Volkswagen Group

88

Volkswagen Group Strategy 2018: Substantial Growth and Sustainable Profitability

Top employer

Volkswagen

Group profit

before tax

margin > 8%Volumes

> 10 million units p.a.2

Leading

in customer

satisfaction

and quality

1 Growth market focus

•

Increased market penetration•

Emerging markets expansion•

Balanced global footprint 2 Modular toolkit strategy

•

Reduction in investment, development and unit costs

•

Scale and efficiency effects•

Increased production flexibility•

Reduced time to market

3 Capital discipline

•

> 16% RoI

target in automotive business

•

20% RoE1 goal in Financial Services

•

Around 6% automotive capex in PPE/sales4 Operating profit measures

•

Strong cost control•

Process/product optimization•

Regional scale effects

5 Synergy potential

•

Leveraging best practices across the Group

•

Purchasing, production, and distribution benefits

6 Potential upside

•

Product portfolio extension•

North American expansion and market recovery

•

Commercial vehicle strategy and market recovery

•

Financial Services: strengthen the automotive value chain

1 Pretax 2 Including ChinaSource: Volkswagen Group Note: All stated Volkswagen Group figures represent financial targets for 2018

999

Volkswagen Offers Diversified Economic Exposure through Attractive Mix of Emerging and Mature Markets

EmergingMarkets

47%

MatureMarkets

53% 27%

60%

Mature Markets

EmergingMarkets

Volkswagen Group 2018(based on units)Market growth 2009 -

18Volkswagen Group 2009(based on units)

Source: Global Insight, Volkswagen GroupNote: Market = Cars and LCVs; Mature markets: Western Europe, US, Canada, Japan, Australia and New Zealand; all other countries defined as emerging markets

EmergingMarkets

52%

MatureMarkets

48%

1010

We Are Well Positioned to Reach Our Strategic Goal of Achieving Sustainable Profitable Growth

Medium-term Group targets Medium-term China targets

Group no. of units sold

Automotive EBIT margin

Financial Services pre-tax RoE

Credit rating

Financial Services cost-income ratio

Automotive capex/sales

China no. of units sold

Automotive EBIT margin

China RoI

Investments

Note: Porsche AG not reflected1 Normalized RoE

based on 8% equity ratio2 Represents total investment of Joint Ventures, new investments announced in April 2010

8.0 million (incl. Scania)

5%+

c.6%

15%1

c.55%

Maintain A

2.0 million+

6%+

20%+

€

6.0 billion2

1111

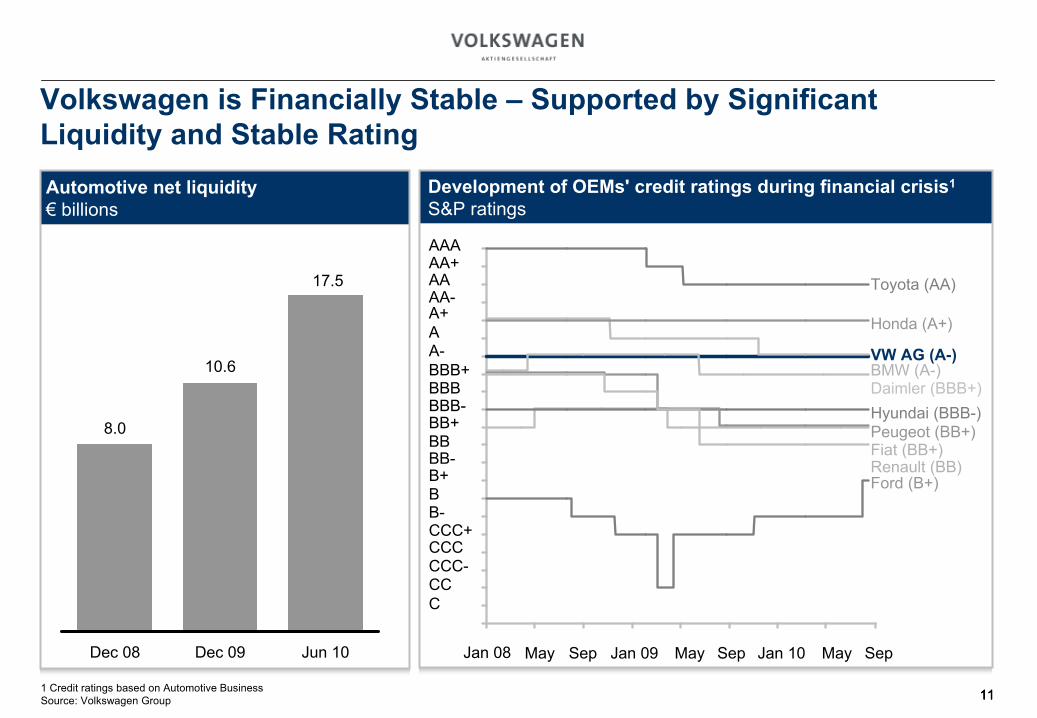

Volkswagen is Financially Stable –

Supported by Significant Liquidity and Stable RatingAutomotive net liquidity€

billions

Jun 10

17.5

Dec 09

10.6

Dec 08

8.0

1 Credit ratings based on Automotive BusinessSource: Volkswagen Group 11

Development of OEMs' credit ratings during financial crisis1

S&P ratings

Jan Mai Sep Jan Mai Sep Jan Mai Sep

AAA

Toyota (AA)

Honda (A+)

VW AG (A-)BMW (A-)Daimler (BBB+)Hyundai (BBB-)Peugeot (BB+)Fiat (BB+)Renault (BB)Ford (B+)

AA+AAAA-A+AA-BBB+BBBBBB-BB+BBBB-B+BB-CCC+CCCCCC-CCC

May Sep Jan 09 May Sep Jan 10 May SepJan 08

1212

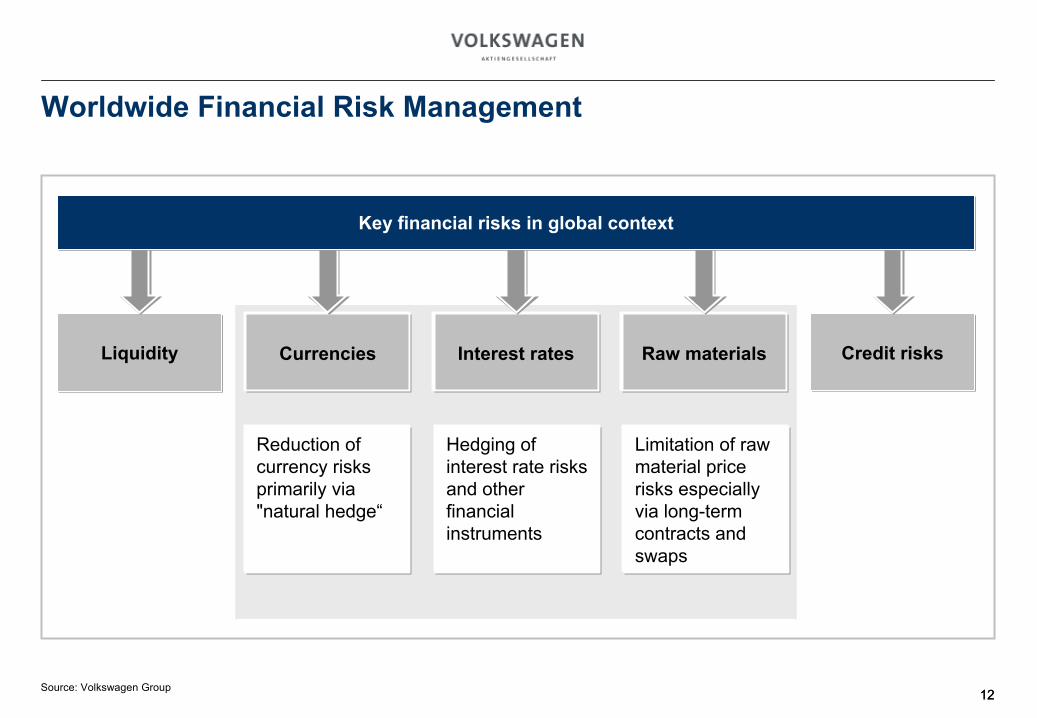

Worldwide Financial Risk Management

Credit risksRaw materialsInterest ratesCurrenciesLiquidity

Hedging of interest rate risks and other financial instruments

Limitation of raw material price risks especially via long-term contracts and swaps

Reduction of currency risks primarily via "natural hedge“

Key financial risks in global context

Source: Volkswagen Group

1313

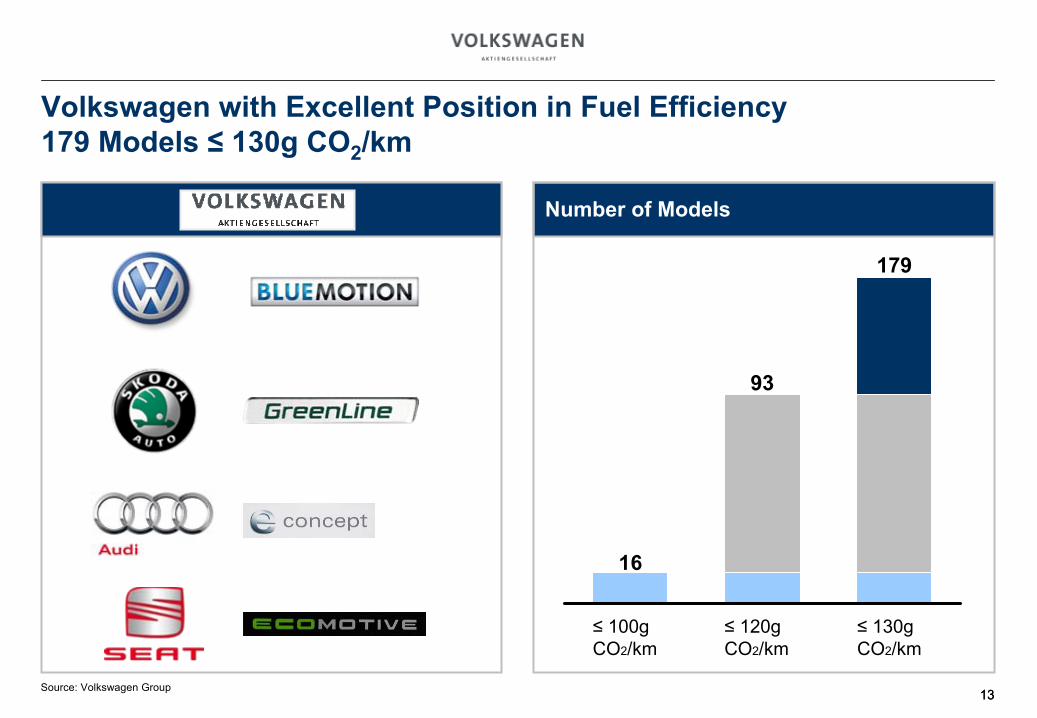

Volkswagen with Excellent Position in Fuel Efficiency 179 Models ≤

130g CO2

/km

16

≤

130g CO2/km

179

≤

120g CO2/km

93

≤

100g CO2/km

Number of Models

Source: Volkswagen Group

1414

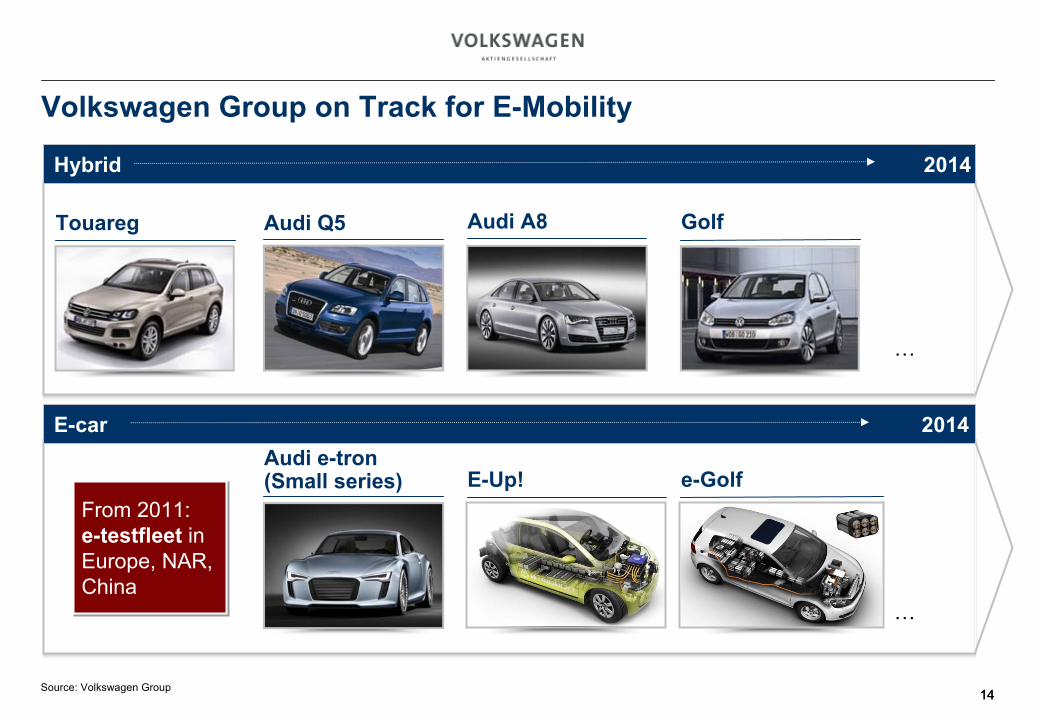

Volkswagen Group on Track for E-Mobility

Hybrid 2014

Touareg Audi Q5 Audi A8

Audi e-tron (Small series) e-GolfE-Up!

Golf

…

…

From 2011: e-testfleet

in Europe, NAR, China

E-car 2014

Source: Volkswagen Group

1515

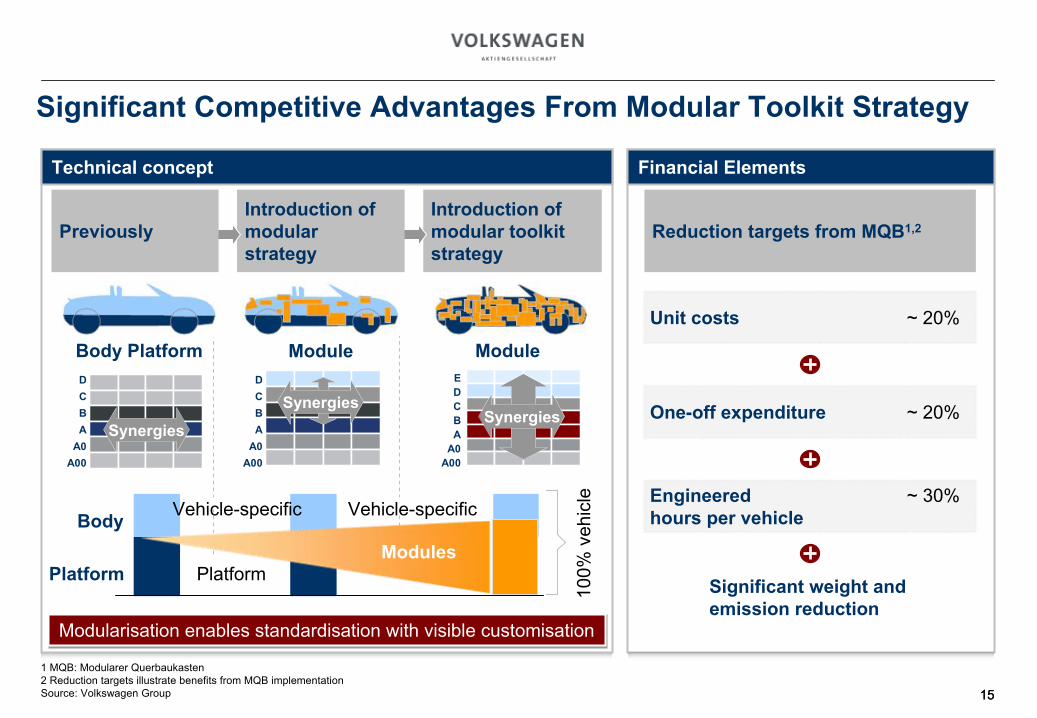

Significant Competitive Advantages From Modular Toolkit Strategy

1 MQB: Modularer

Querbaukasten2 Reduction targets illustrate benefits from MQB implementationSource: Volkswagen Group

Synergies

D

C

B

A

A0

A00

Introduction ofmodular toolkit strategy

Introduction ofmodular strategy

Previously

100%

veh

icle

Vehicle-specificVehicle-specific

Platform

Body

PlatformModules

ModuleModuleBody PlatformD

C

B

A

A0

A00

SynergiesE

D

C

B

A

A0

A00

Synergies

Technical concept

Modularisation

enables standardisation

with visible customisation

Reduction targets from MQB1,2

Financial Elements

Unit costs ~ 20%

One-off expenditure ~ 20%

Engineered

hours per vehicle

~ 30%

Significant weight and emission reduction

16

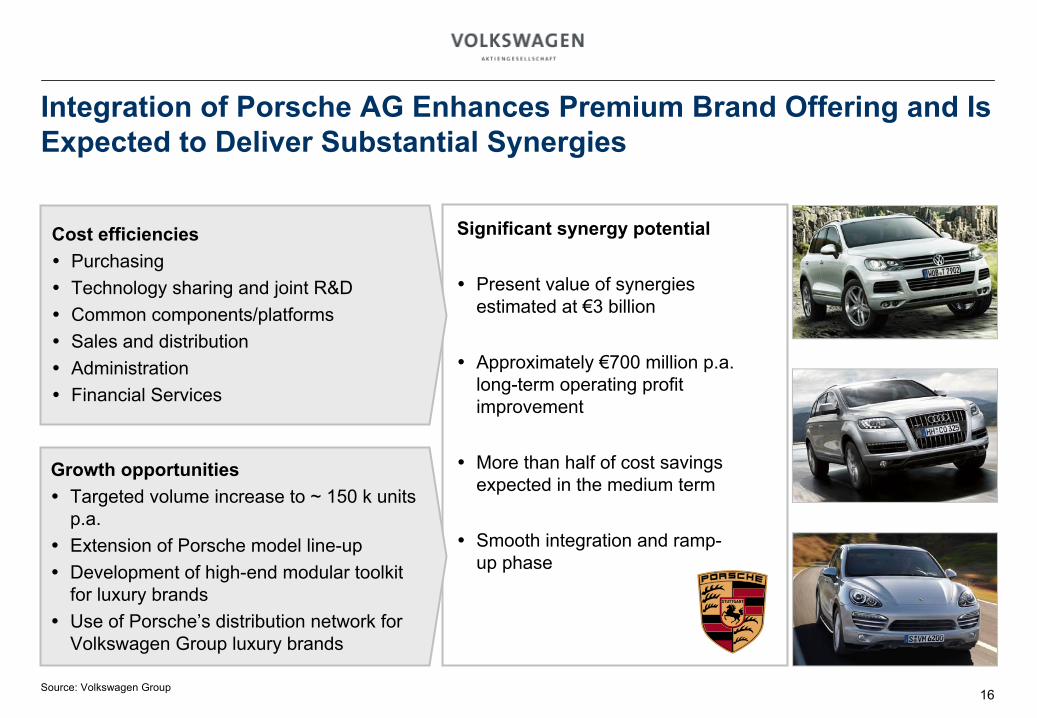

Integration of Porsche AG Enhances Premium Brand Offering and Is Expected to Deliver Substantial Synergies

Cost efficiencies

Purchasing

Technology sharing and joint R&D

Common components/platforms

Sales and distribution

Administration

Financial Services

Growth opportunities Targeted volume increase to ~ 150 k units

p.a. Extension of Porsche model line-up Development of high-end modular toolkit

for luxury brands Use of Porsche’s distribution network for

Volkswagen Group luxury brands

Significant synergy potential

Present value of synergies estimated at €3 billion

Approximately €700 million p.a. long-term operating profit improvement

More than half of cost savings expected in the medium term

Smooth integration and ramp-up phase

Source: Volkswagen Group

1717

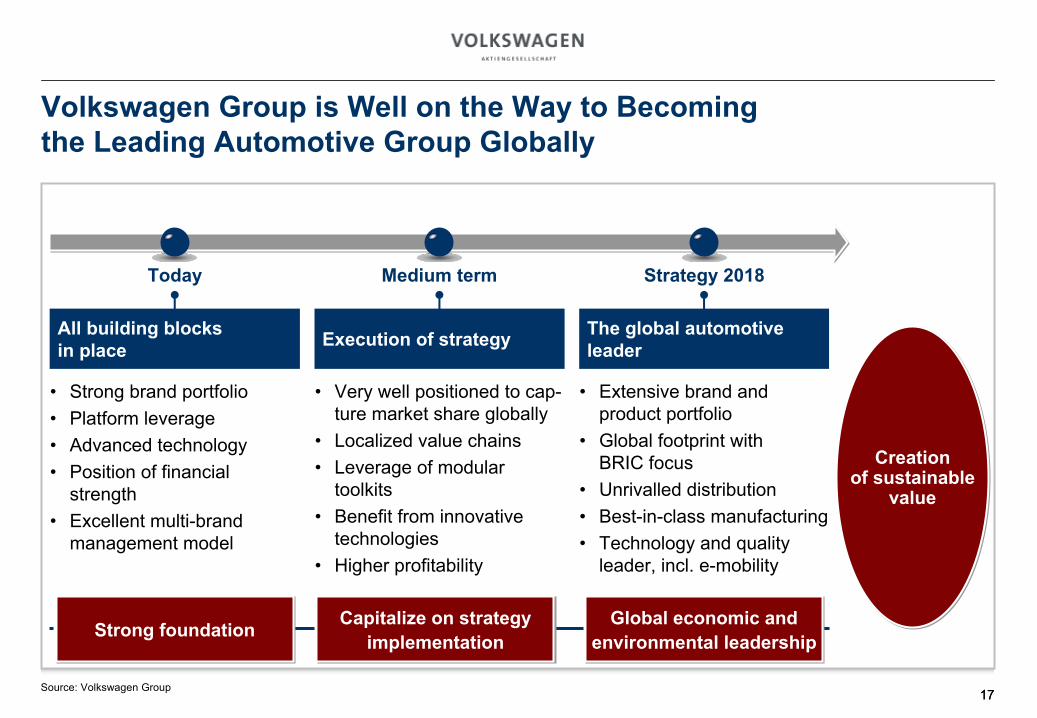

Volkswagen Group is Well on the Way to Becoming the Leading Automotive Group Globally

Creation of sustainable

value

Strong foundation Capitalize on strategy implementation

Global economic and environmental leadership

All building blocks in place Execution of strategy The global automotive

leader

Today Medium term Strategy 2018

•

Strong brand portfolio•

Platform leverage•

Advanced technology•

Position of financial strength

•

Excellent multi-brand management model

•

Very well positioned to cap-

ture

market share globally•

Localized value chains•

Leverage of modular toolkits

•

Benefit from innovative technologies

•

Higher profitability

•

Extensive brand and product

portfolio•

Global footprint with BRIC

focus•

Unrivalled distribution•

Best-in-class manufacturing•

Technology and quality leader, incl. e-mobility

Source: Volkswagen Group

1818

Volkswagen –

On the Road of Success

Part 1: Hans Dieter Pötsch, Member of the Board of Management

Part 2: Frank Fiedler, CFO Volkswagen Financial Services AG

Part 3: Dr. Christof

Spathelf, Senior Vice President of Volkswagen Group Manufacturing Overseas

19

Creating value

–

Our

Business Model

Volkswagen Financial Services:

Company Overview

Financial Basis

Preparing for the Future –

Our Strategy 2018

20

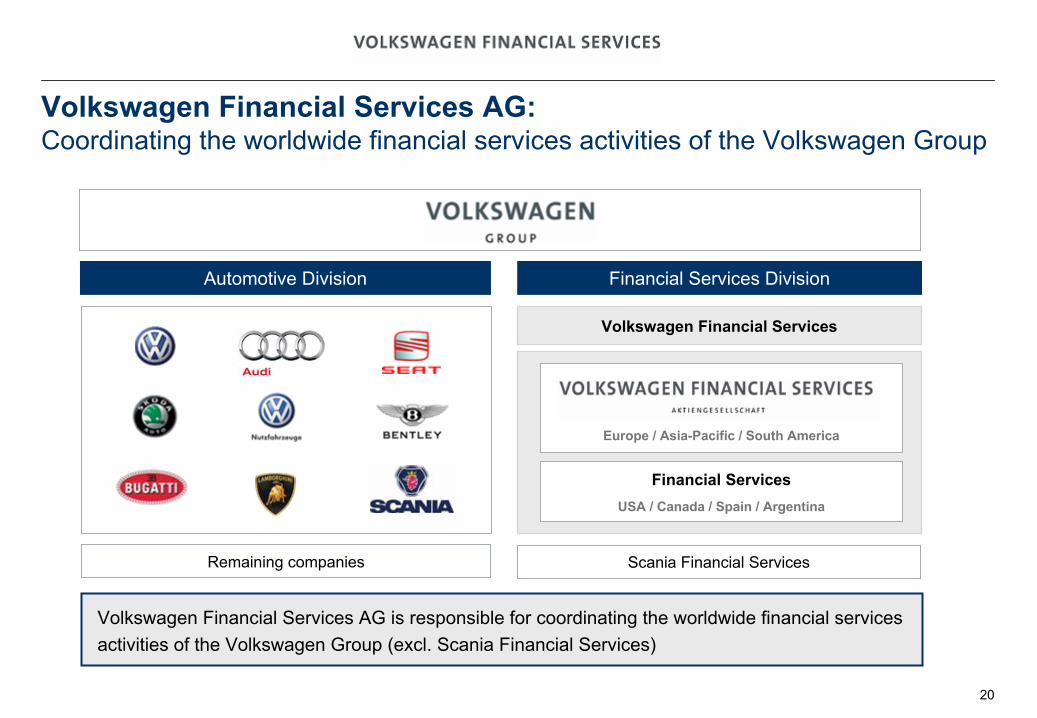

Scania Financial Services

Volkswagen Financial Services

Europe / Asia-Pacific / South America

Financial ServicesUSA / Canada / Spain / Argentina

Financial Services DivisionAutomotive Division

Remaining companies

Volkswagen Financial Services AG: Coordinating the worldwide financial services activities of the Volkswagen Group

Volkswagen Financial Services AG is responsible for coordinating

the worldwide financial services activities of the Volkswagen Group (excl. Scania Financial Services)

21

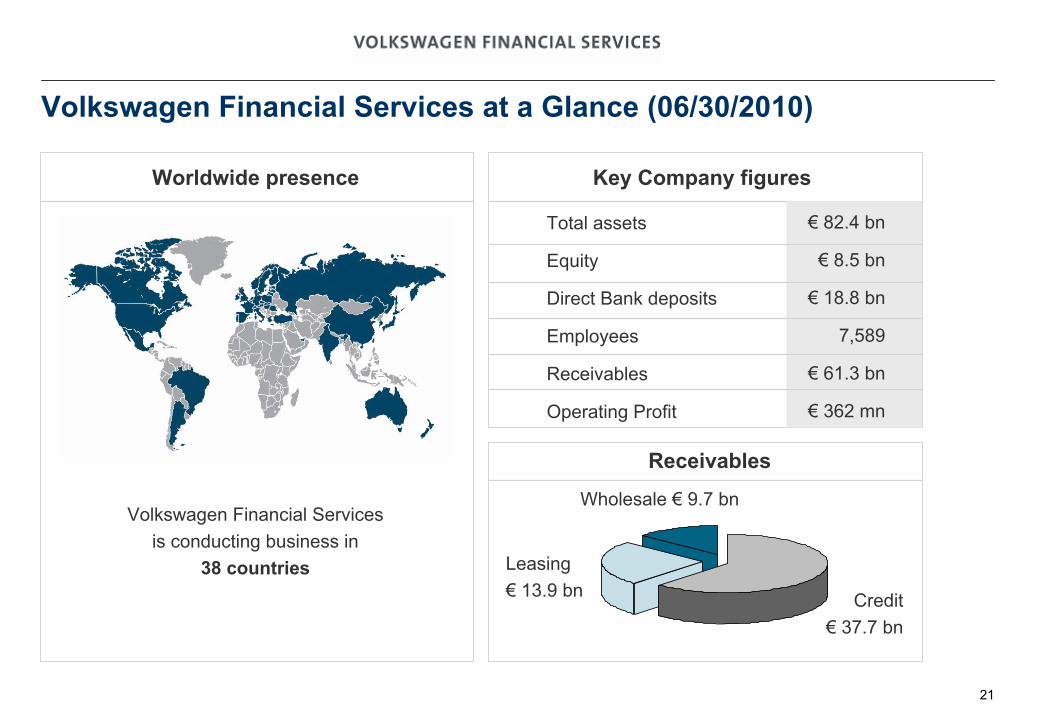

Total assets

Equity

Direct Bank deposits

Employees

Receivables

Operating

Profit

€

82.4 bn

€ 8.5 bn

€ 18.8 bn

7,589

€ 61.3 bn

€ 362 mn

Key Company figures

Volkswagen Financial Services at a Glance (06/30/2010)

Volkswagen Financial Services

is conducting business in 38 countries

Worldwide

presence

Receivables

Credit€

37.7 bn

Leasing€

13.9 bn

Wholesale €

9.7 bn

22

Creating value

–

Our

Business Model

Volkswagen Financial Services:

Company Overview

Financial Basis

Preparing for the Future –

Our Strategy 2018

23

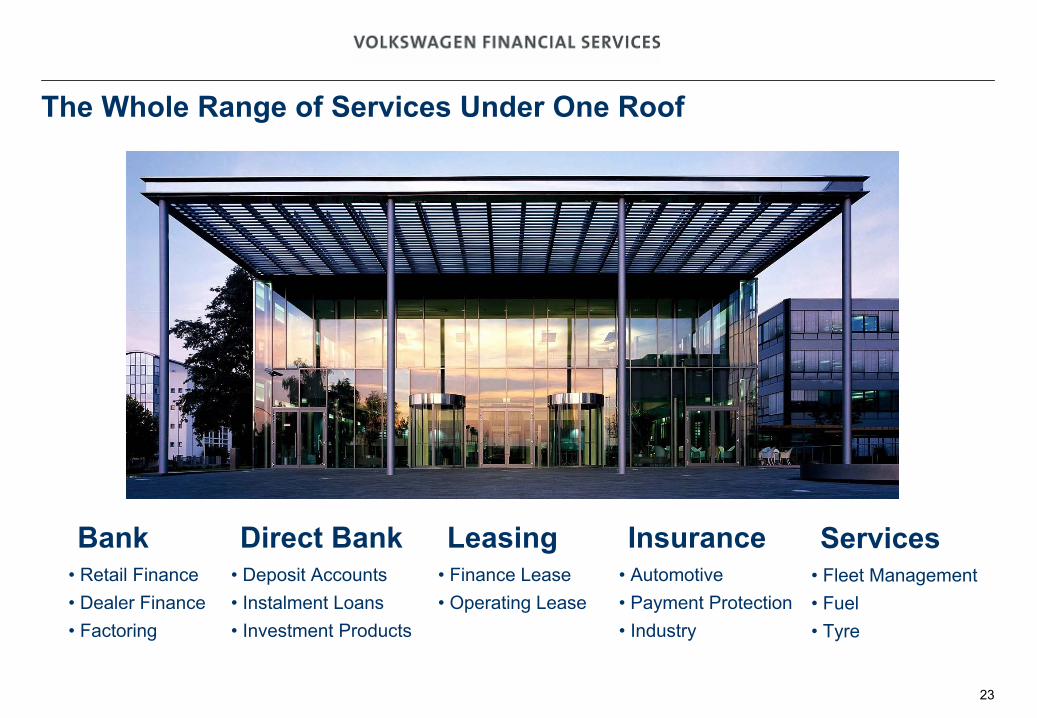

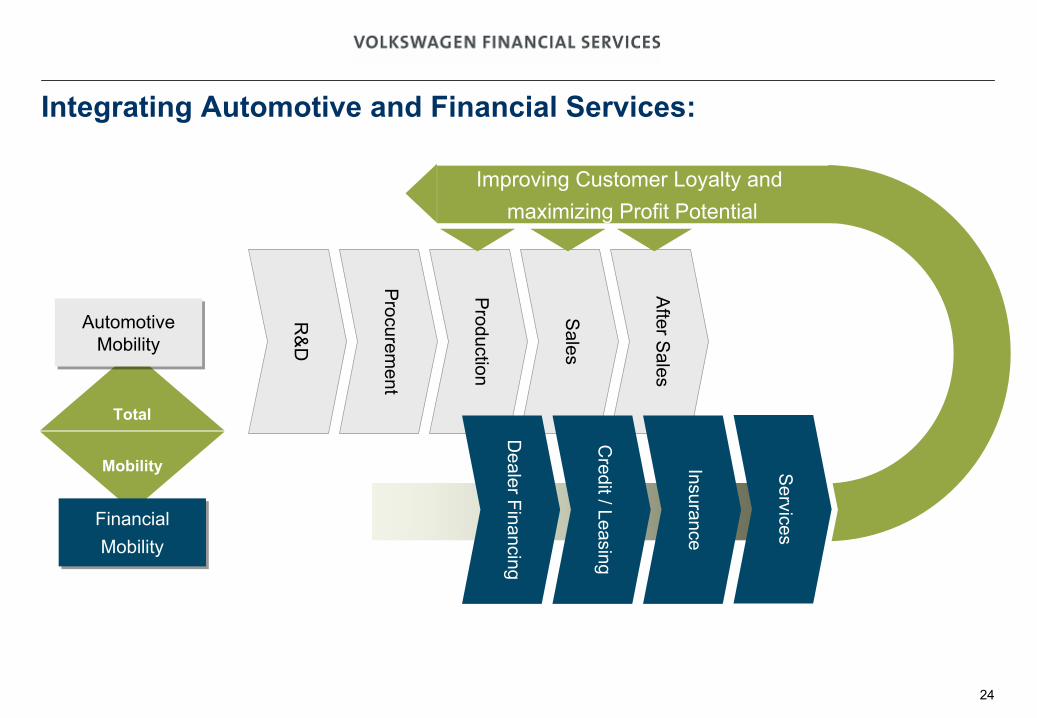

The Whole Range of Services Under One Roof

Bank• Retail Finance• Dealer Finance• Factoring

Direct Bank• Deposit Accounts• Instalment Loans• Investment Products

Leasing• Finance Lease• Operating Lease

Insurance• Automotive • Payment Protection • Industry

Services• Fleet Management• Fuel • Tyre

24

R&

D

Procurem

ent

Production

Sales

After S

ales

Credit

/ Leasing

Dealer Financing

Insurance

Total

Mobility

AutomotiveMobility

AutomotiveMobility

FinancialMobility

FinancialMobility

Integrating

Automotive and Financial Services:

Improving Customer Loyalty and maximizing Profit Potential

Services

25

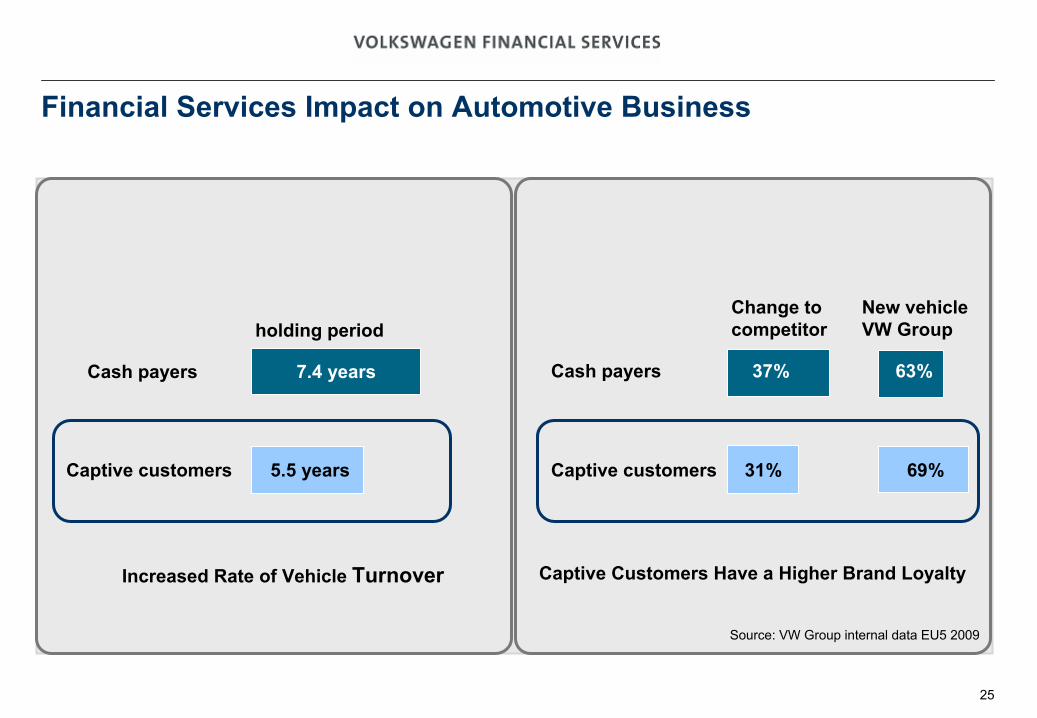

Financial Services Impact on Automotive Business

Cash payers

Captive customers

Increased Rate of Vehicle Turnover

5.5 years

7.4 years

Source: VW Group internal data EU5 2009

holding periodChange to competitor

New vehicle

VW Group

Cash payers

Captive customers 31%

37%

69%

63%

Captive Customers

Have

a Higher

Brand Loyalty

26

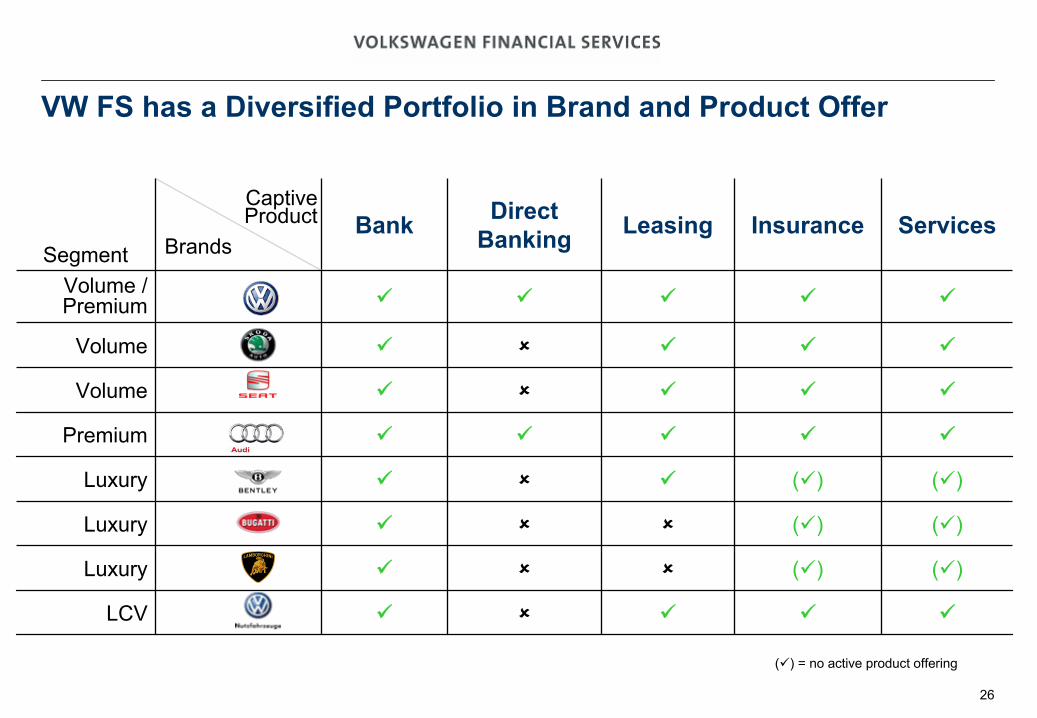

VW FS has a Diversified Portfolio in Brand and Product Offer

Segment

Captive

Product

BrandsBank Direct

Banking Leasing Insurance Services

Volume

/ Premium

Volume

Volume

Premium

Luxury () ()

Luxury () ()

Luxury () ()

LCV

() = no active product offering

27

Creating value

–

Our

Business Model

Volkswagen Financial Services:

Company Overview

Financial Basis

Preparing for the Future –

Our Strategy 2018

28

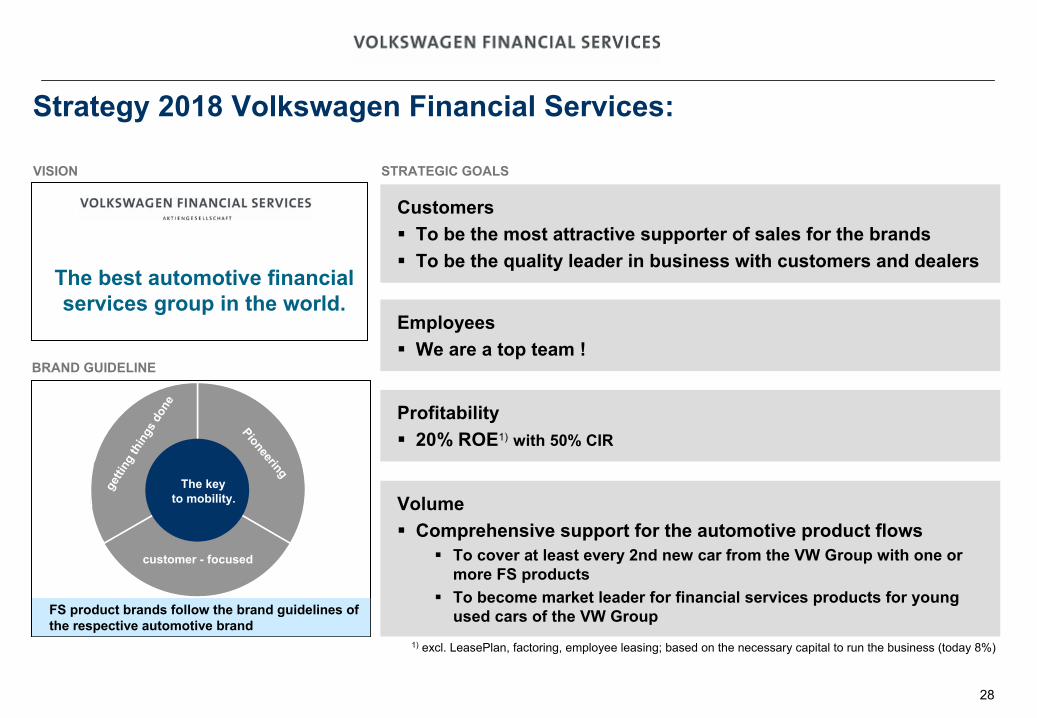

The best automotive financial services group in the world.

VISION

BRAND GUIDELINE

STRATEGIC GOALS

1)

excl. LeasePlan, factoring, employee leasing; based on the necessary capital to run the business (today 8%)

Strategy 2018 Volkswagen Financial Services:

FS product brands follow the brand guidelines of the respective automotive brand

getti

ng th

ings

don

e

Pioneering

customer -

focused

The keyto mobility.

Customers

To be the most attractive supporter of sales for the brands

To be the quality leader in business with customers and dealers

Volume

Comprehensive support for the automotive product flows

To cover at least every 2nd new car from the VW Group with one or more FS products

To become market leader for financial services products for young used cars of the VW Group

Profitability

20% ROE1)

with 50% CIR

Employees

We are a top team !

29

Core

Elements of Our

Sales and Growth Strategy: Germany

FlottenmanagementFleet

management

Neue MobilitätNew mobility

Einzel-/Firmenkunden

Versicherung, Wartung und Verschleiß

Gebrauchtwagen-

management

Individual

/ corporate

customers

Insurance / service

/ wear

& tearUsed

car

management

Area

of growth

Area

of growth

Develop

position

futher

Hold position

Hold position

e.g. Germany

Strategy 2018

VolumeProfitabilityCustomers Employees

Global Trends

30

Used car management

Used

car

management

Roll-Out

of Our

Sales and Growth Strategy: Example

UK

New mobility

Insurance / service / wear & tear

Insurance / service

/ wear

& tear

Fleet

management

Fleet

management

Area

of growth

Area

of growth

UK

Develop

position

futher

Individual / corporate customers

Individual

/ corporate

customers

Hold position

Strategy 2018

VolumeProfitabilityCustomers Employees

Global Trends

31

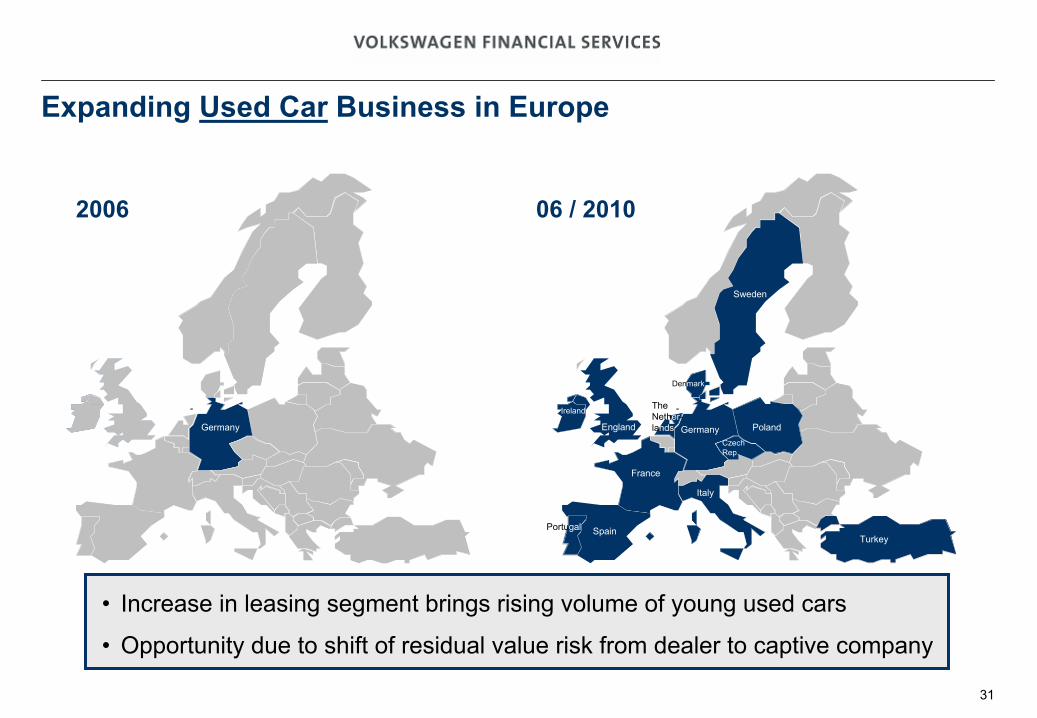

Expanding Used Car

Business in Europe

06 / 2010

-

2006

Sweden

-

England

Ireland

France

Spain

Italy

GermanyCzechRep.

Germany Poland

Turkey

Denmark

TheNether-lands

Portugal

•

Increase in leasing segment brings rising volume of young used cars

•

Opportunity due to shift of residual value risk from dealer to captive company

32

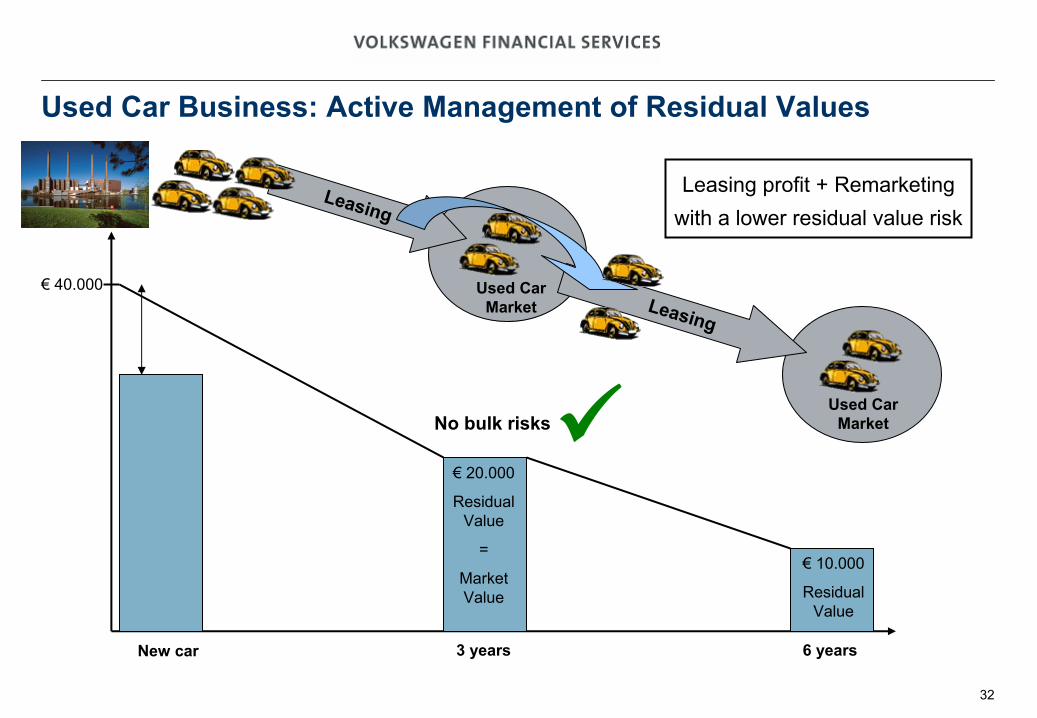

Used

Car Market

Used

Car Business: Active

Management of Residual Values

€

40.000

€

20.000

Residual Value

=

Market

Value

Leasing

€

10.000

Residual Value

New car 3 years 6 years

No bulk

risks

Leasing profit

+ Remarketing

with

a lower

residual value

risk

Leasing

Used

Car Market

33

Key Strategic

Growth Markets: Opportunities

and Challenges

Russia

India

ChinaUSA

Brasil

34

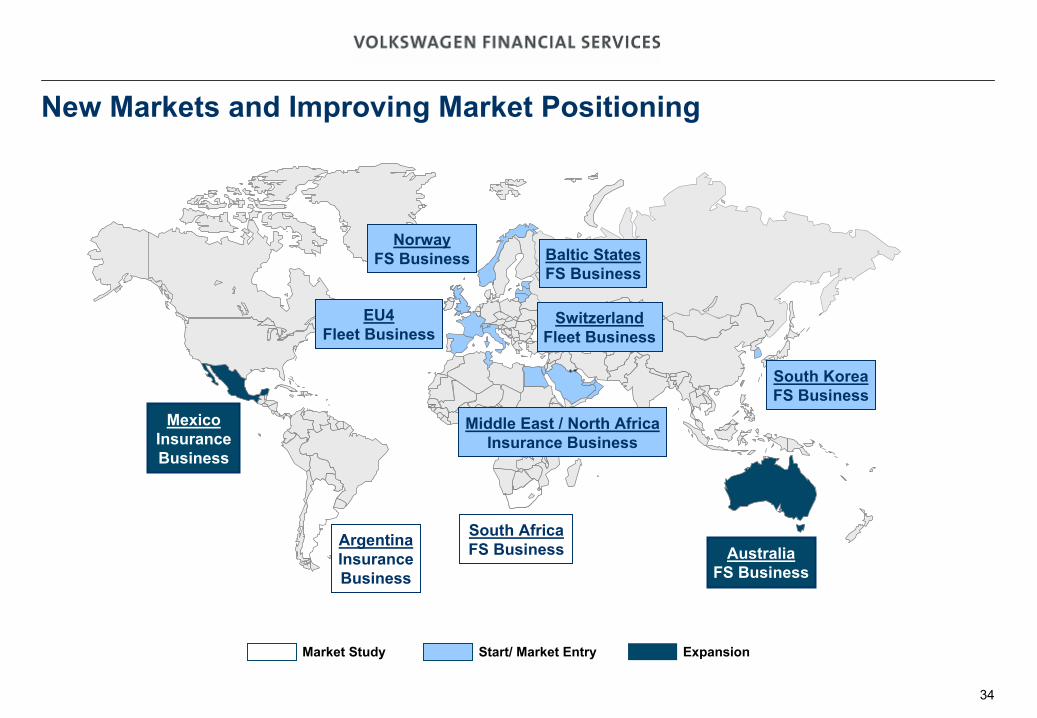

New Markets and Improving

Market Positioning

South Africa

FS Business

Middle East / North Africa

Insurance Business

Argentina

Insurance Business

MexicoInsurance Business

South KoreaFS Business

Australia FS Business

NorwayFS Business

EU4Fleet Business

Baltic States

FS Business

Switzerland Fleet Business

Market Study Start/ Market Entry Expansion

35

Creating value

–

Our

Business Model

Volkswagen Financial Services:

Company Overview

Financial Basis

Preparing for the Future –

Our Strategy 2018

36

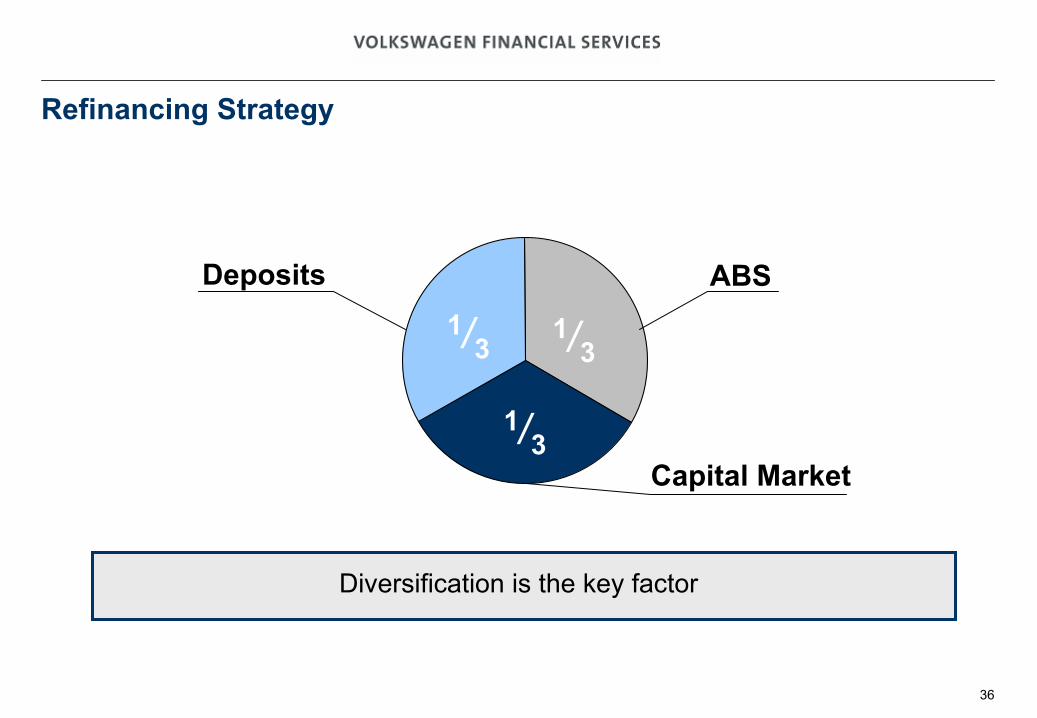

Refinancing Strategy

Diversification is the key factor

ABS

Capital Market

Deposits1/3

1/3

1/3

37

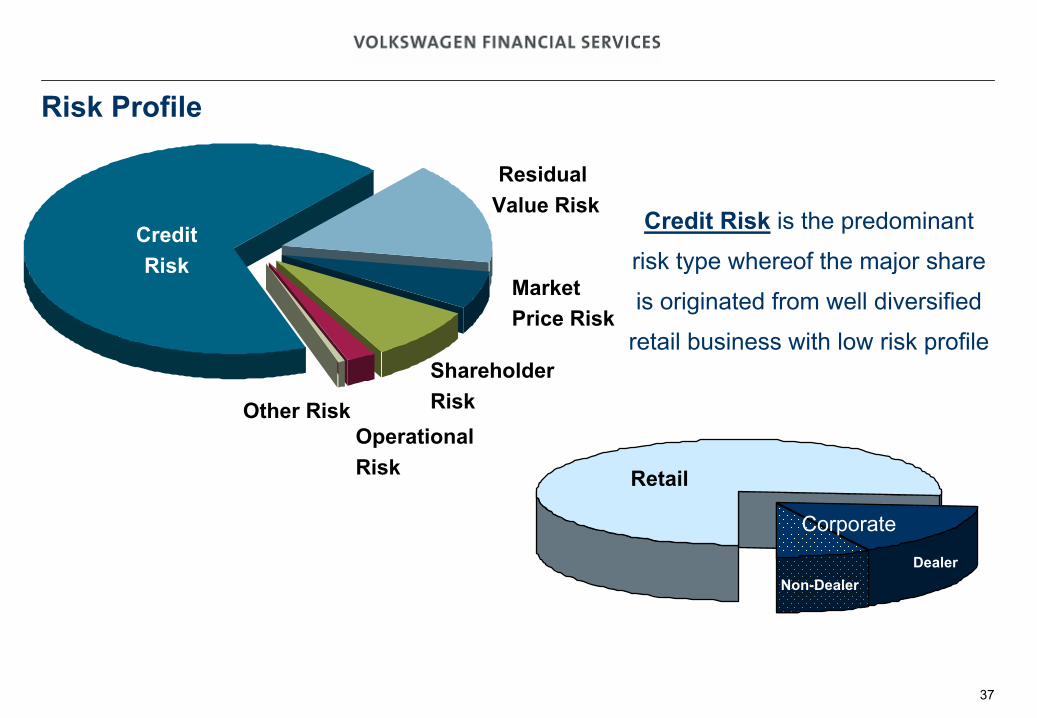

Risk Profile

Credit Risk

Residual Value Risk

Market Price Risk

Shareholder RiskOther

Risk

Credit Risk

is the predominant

risk type

whereof

the major

share

is originated

from

well diversified retail

business

with

low

risk profile

Retail

Operational Risk

Corporate

Non-DealerDealer

38

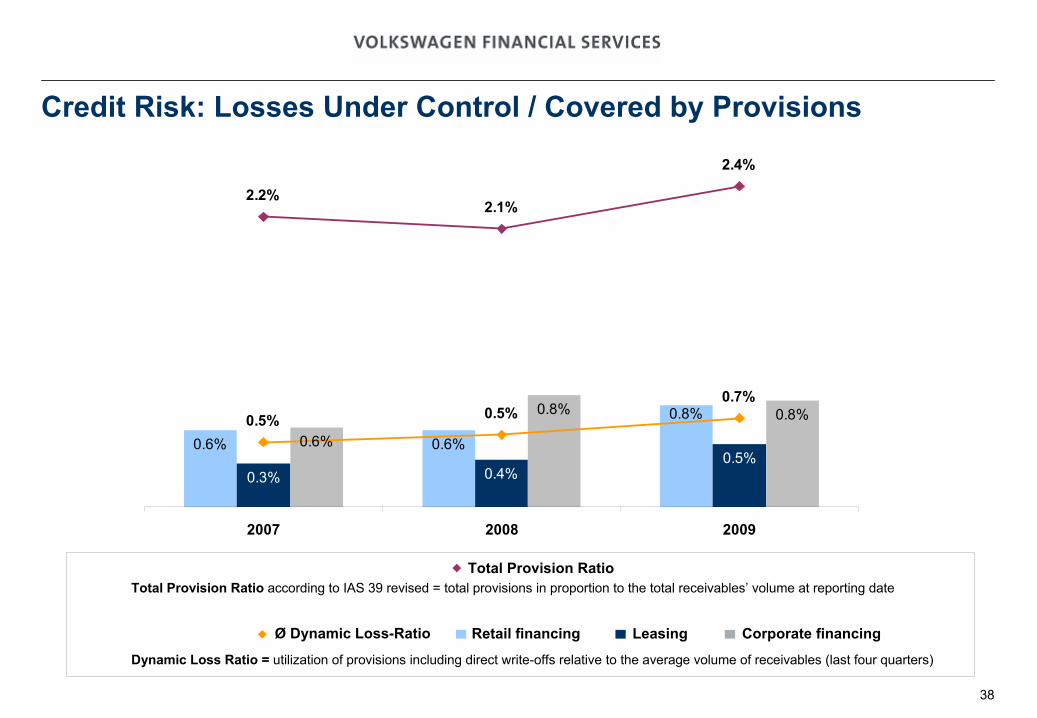

0.6% 0.6%

0.3% 0.4%0.5%

0.6%

0.8% 0.8%0.8%

2.2%2.1%

2.4%

0.5% 0.5%0.7%

2007 2008 2009

Credit Risk: Losses Under Control / Covered by Provisions

Retail financing Leasing Corporate financingØ

Dynamic Loss-Ratio

Total Provision Ratio

Dynamic Loss Ratio = utilization of provisions including direct write-offs relative to the average volume of receivables (last four quarters)

Total Provision Ratio

according to IAS 39 revised = total provisions in proportion to

the total receivables’ volume at reporting date

39

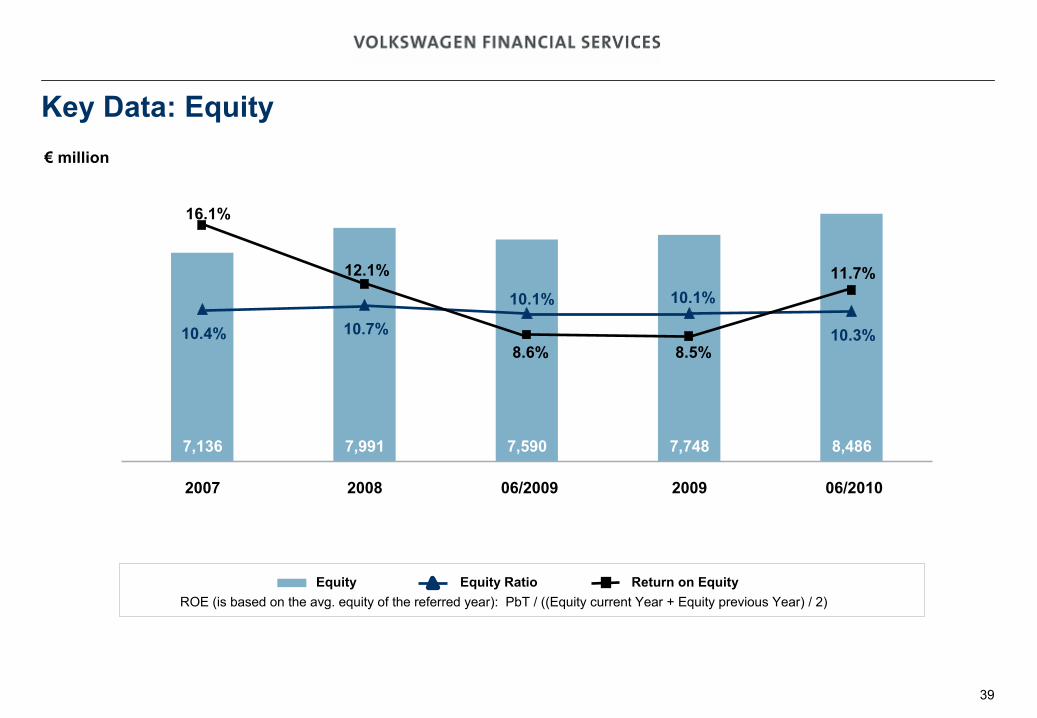

8,4867,7487,5907,9917,136

10.4% 10.7% 10.3%8.5%

16.1%

11.7%

8.6%

12.1%10.1%10.1%

2007 2008 06/2009 2009 06/2010

Equity Equity

Ratio Return on EquityROE (is

based

on the avg. equity

of the referred

year): PbT

/ ((Equity

current

Year

+ Equity

previous

Year) / 2)

€

million

Key Data: Equity

40

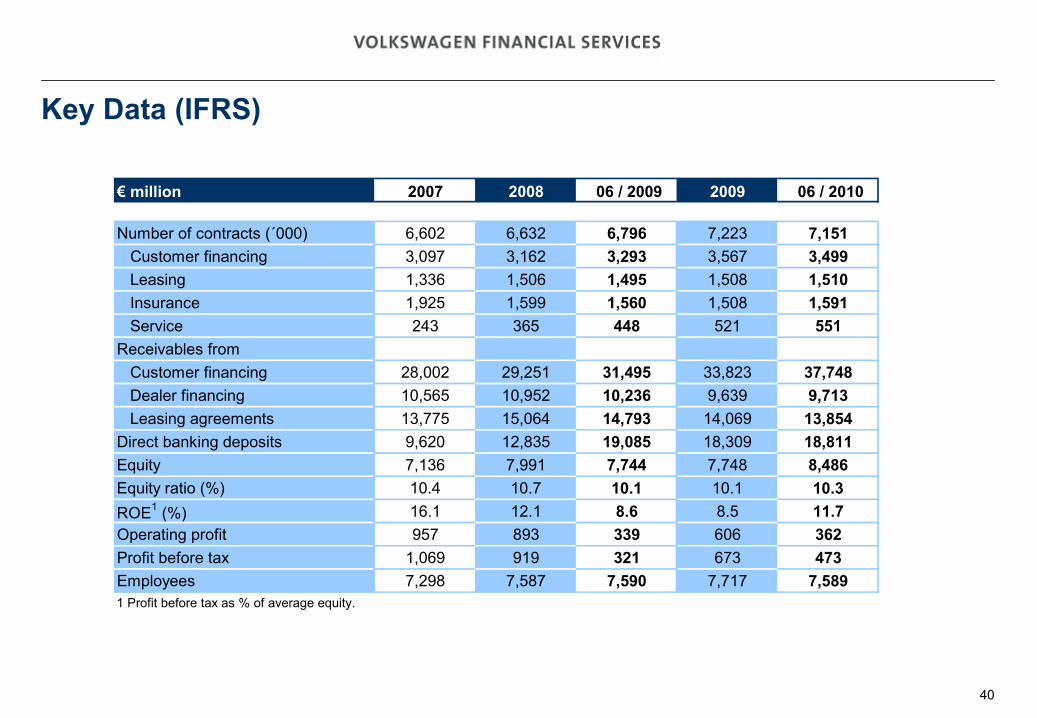

Key Data (IFRS)

€ million 2007 2008 06 / 2009 2009 06 / 2010

Number of contracts (´000) 6,602 6,632 6,796 7,223 7,151Customer financing 3,097 3,162 3,293 3,567 3,499Leasing 1,336 1,506 1,495 1,508 1,510Insurance 1,925 1,599 1,560 1,508 1,591Service 243 365 448 521 551

Receivables from Customer financing 28,002 29,251 31,495 33,823 37,748Dealer financing 10,565 10,952 10,236 9,639 9,713Leasing agreements 13,775 15,064 14,793 14,069 13,854

Direct banking deposits 9,620 12,835 19,085 18,309 18,811Equity 7,136 7,991 7,744 7,748 8,486Equity ratio (%) 10.4 10.7 10.1 10.1 10.3ROE1 (%) 16.1 12.1 8.6 8.5 11.7Operating profit 957 893 339 606 362Profit before tax 1,069 919 321 673 473Employees 7,298 7,587 7,590 7,717 7,5891 Profit before tax as % of average equity.

41

Strategic

Focus

Offer of innovative products for brand and local market requirements

Exploitation of further growth potential in mature European markets based upon our innovative products and customised services through all steps of

our value chain

Growth in emerging markets in Eastern Europe, Russia, Asia and Latin America together with Volkswagen Group brands

Ongoing diversification in worldwide refinancing

Further reduce risk exposure through customer segment-

and regional diversification

42

Risk Costs will improve,

Outlook 2010

Growth potential continues to exist,

Margin pressure likely to return,

Refinancing situation normalized at competitive costs,

Focus on Strategy 2018 implementation.

4343

Volkswagen –

On the Road of Success

Part 1: Hans Dieter Pötsch, Member of the Board of Management

Part 2: Frank Fiedler, CFO Volkswagen Financial Services AG

Part 3: Dr. Christof

Spathelf, Senior Vice President of Volkswagen Group Manufacturing Overseas

4444

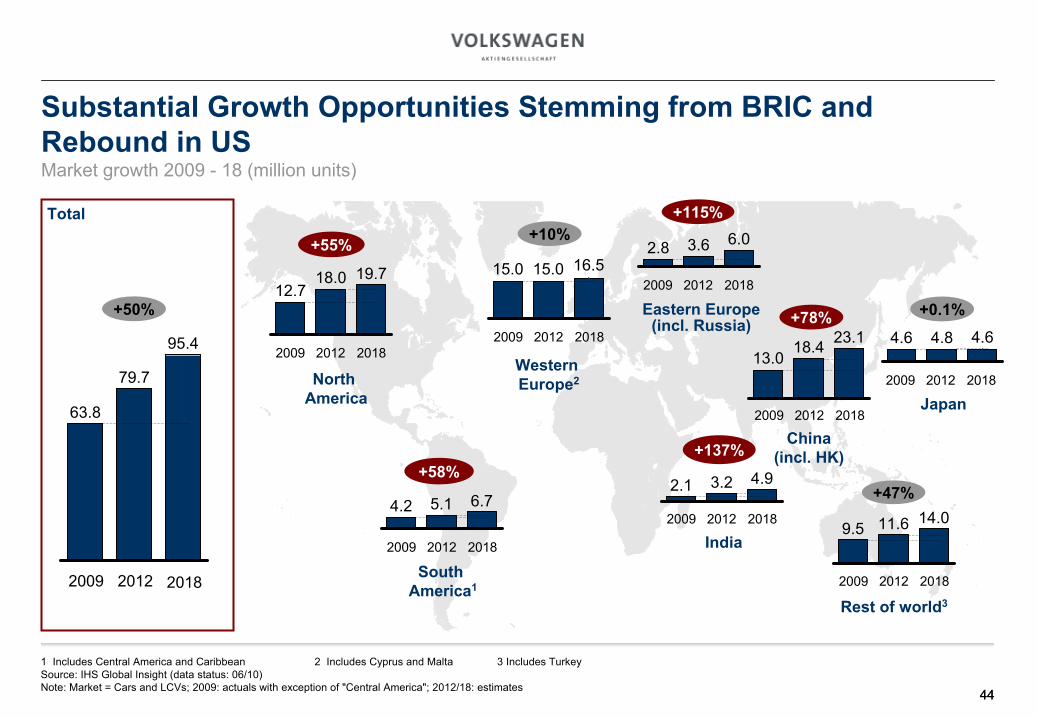

Substantial Growth

Opportunities Stemming from BRIC and Rebound in US

Market growth 2009 -

18 (million units)

1 Includes Central America and Caribbean

2 Includes Cyprus and Malta

3 Includes Turkey Source: IHS Global Insight (data status: 06/10)Note: Market = Cars and LCVs; 2009: actuals

with exception of "Central America"; 2012/18: estimates

Total

2009 2012 2018

19.712.7

18.016.515.015.0

+55% +10%

6.74.2 5.1

+58%

14.09.5 11.6

+47%

4.64.6 4.8

+0.1%23.1

13.018.4

+78%

6.03.62.8

+115%

North America

Western Europe2

Eastern Europe (incl. Russia)

China

(incl. HK)

4.92.1 3.2

+137%

South America1

Rest of world3

2009 2012 2018

95.4

63.8

79.7

+50%

Japan

India

2009 2012 2018

2009 2012 2018

2009 2012 2018

2009 2012 2018

2009 2012 2018

2009 2012 2018

2009 2012 2018

4545

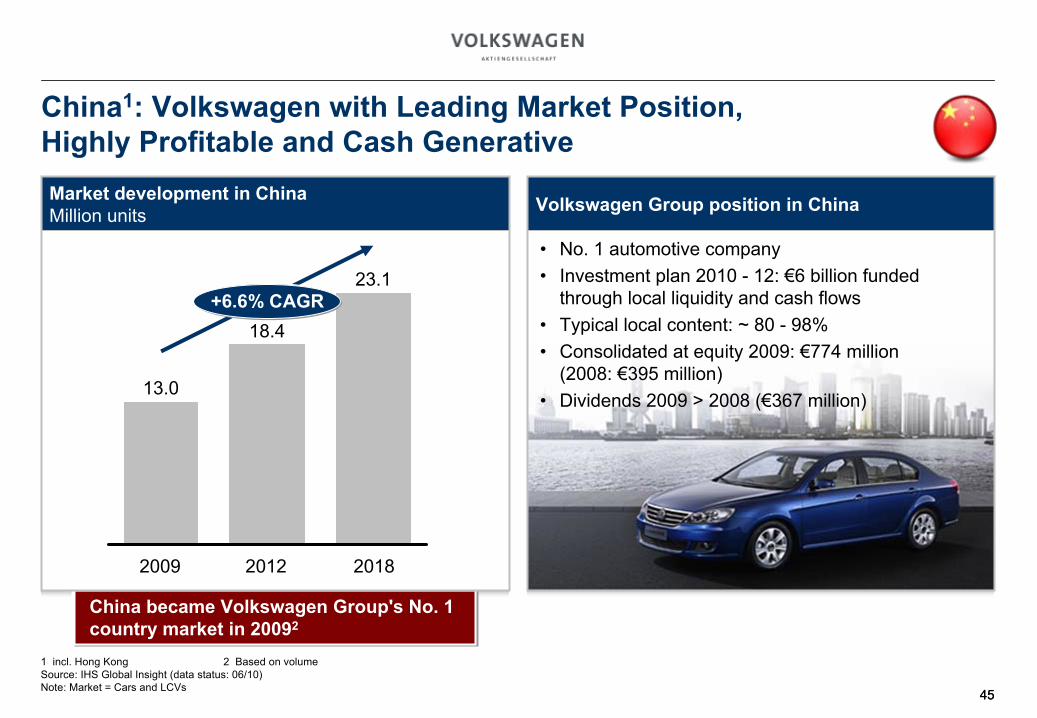

China1: Volkswagen with Leading Market Position, Highly Profitable and Cash Generative

Volkswagen Group position in China

•

No. 1 automotive company•

Investment plan 2010 -

12: €6 billion funded through local liquidity and cash flows

•

Typical local content: ~ 80 -

98%•

Consolidated at equity 2009: €774 million (2008: €395 million)

•

Dividends 2009 > 2008 (€367 million)

China became Volkswagen Group's No. 1 country market in 20092

Market development in China

Million units

+6.6% CAGR

2018

23.1

2012

18.4

2009

13.0

1 incl. Hong Kong

2 Based on volumeSource: IHS Global Insight (data status: 06/10)Note: Market = Cars and LCVs

4646

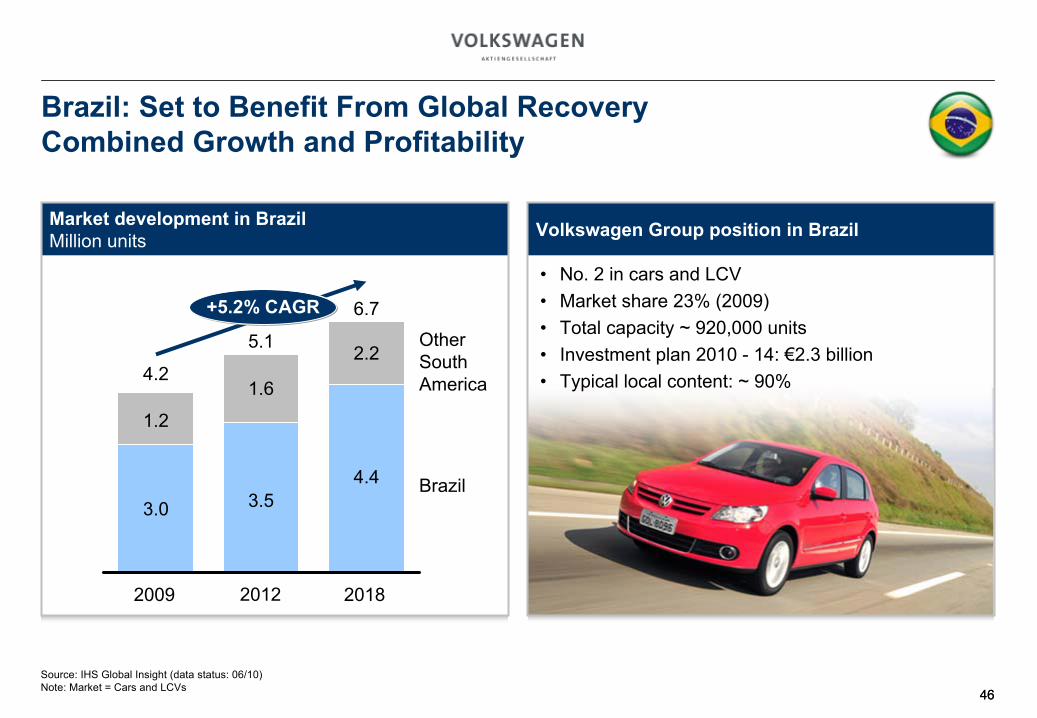

… k units p.a.

Brazil

Other

South

America

2018

6.7

4.4

2.2

2012

5.1

3.5

1.6

2009

4.2

3.0

1.2

Volkswagen Group position in Brazil

•

No. 2 in cars and LCV•

Market share 23% (2009)•

Total capacity ~ 920,000 units•

Investment plan 2010 -

14: €2.3 billion•

Typical local content: ~ 90%

Market development in Brazil

Million units

Brazil: Set to Benefit From Global Recovery Combined Growth and Profitability

Source: IHS Global Insight (data status: 06/10)Note: Market = Cars and LCVs

+5.2% CAGR

4747

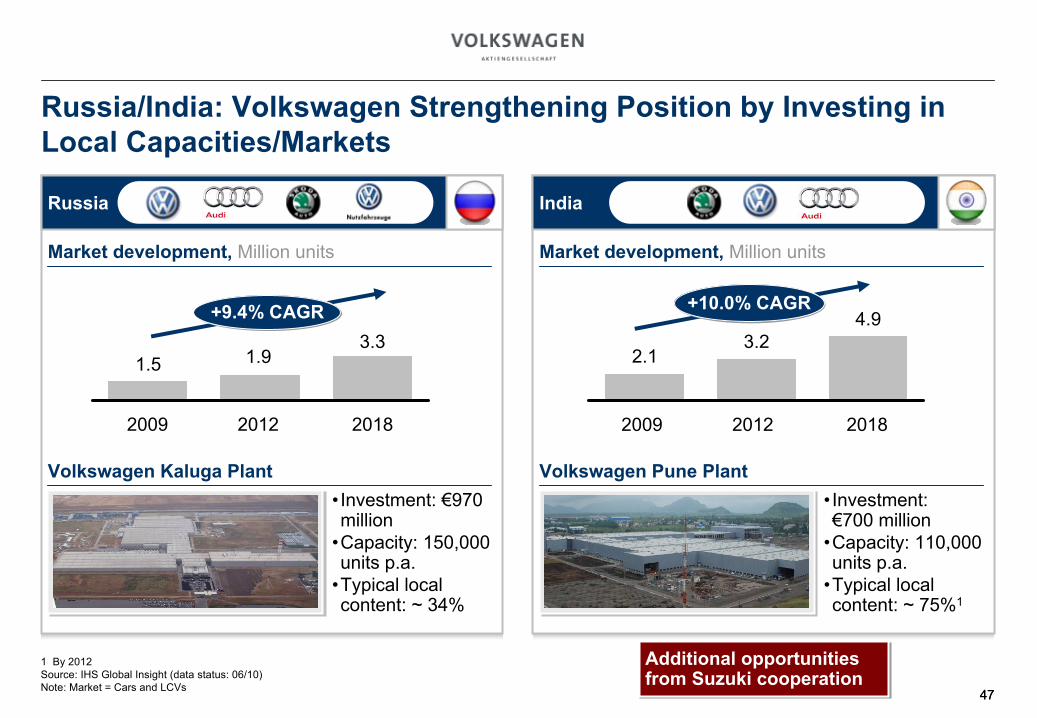

Russia/India: Volkswagen Strengthening Position by Investing in Local Capacities/Markets

3.3

2012

1.9

2009

1.5

2018

3.22.1

4.9

1 By 2012Source: IHS Global Insight (data status: 06/10)Note: Market = Cars and LCVs

Russia

Market development,

Million units

Volkswagen Kaluga Plant•

Investment: €970 million

•

Capacity: 150,000 units p.a.

•

Typical local content: ~

34%

Additional opportunities from Suzuki cooperation

India

Market development,

Million units

Volkswagen Pune Plant• Investment:

€700 million

•Capacity: 110,000 units p.a.

•Typical local content: ~ 75%1

20122009 2018

+9.4% CAGR +10.0% CAGR

48

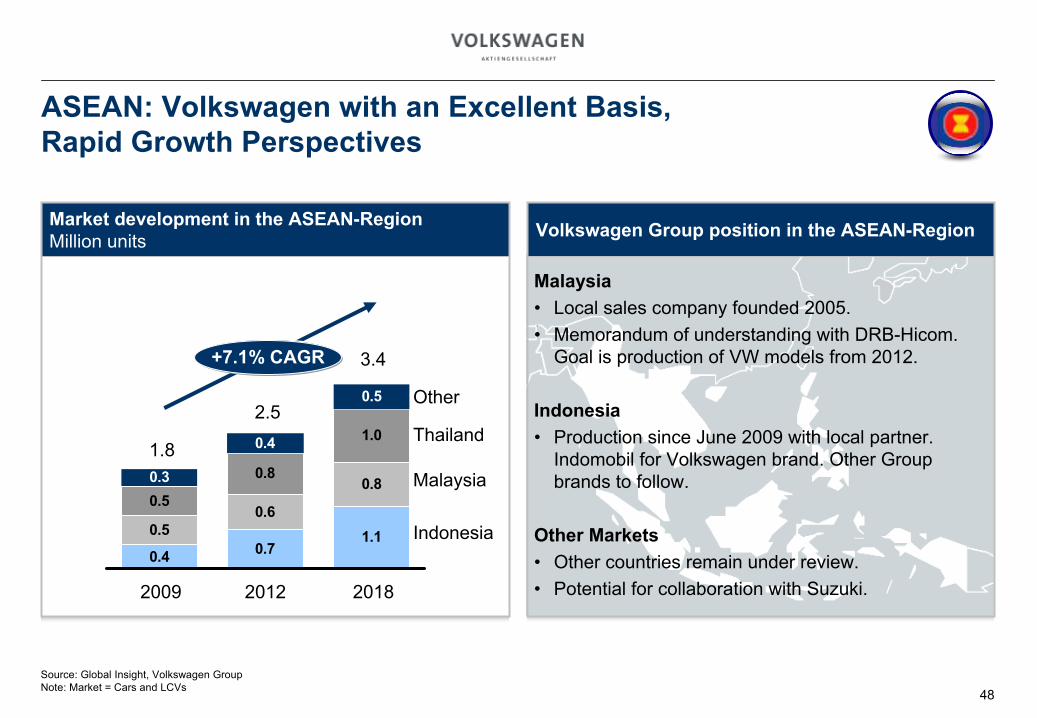

Volkswagen Group position in the ASEAN-Region

Malaysia•

Local sales company founded 2005.•

Memorandum of understanding with DRB-Hicom. Goal is production of VW models from 2012.

Indonesia•

Production since June 2009 with local partner. Indomobil

for Volkswagen brand. Other Group brands to follow.

Other Markets•

Other countries remain under review.•

Potential for collaboration with Suzuki.

Market development in the ASEAN-Region

Million units

1.10.70.4

0.50.6

0.8

1.0

0.8

0.5

0.5

0.4

0.3

+7.1% CAGR

2018

3.4

2012

2.5

2009

1.8

Source: Global Insight, Volkswagen GroupNote: Market = Cars and LCVs

ASEAN: Volkswagen with an Excellent Basis,Rapid Growth Perspectives

Indonesia

Malaysia

Thailand

Other

4949

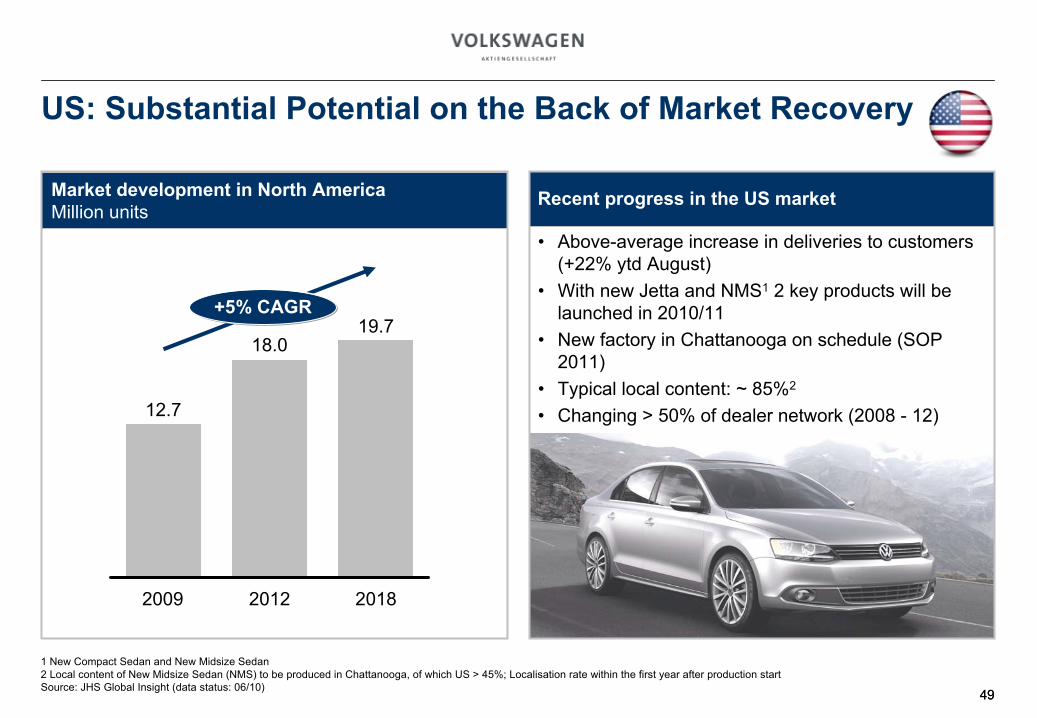

US: Substantial Potential on the Back of Market Recovery

Market development in North America

Million units

Recent progress in the US market

•

Above-average increase in deliveries to customers (+22% ytd August)

•

With new Jetta and NMS1

2 key products will be launched in 2010/11

•

New factory in Chattanooga on schedule (SOP 2011)

•

Typical local content: ~ 85%2

•

Changing > 50% of dealer network (2008 -

12)

2018

19.7

2012

18.0

2009

12.7

+5% CAGR

1 New Compact Sedan and New Midsize Sedan2 Local content of New Midsize Sedan (NMS) to be produced in Chattanooga, of which US > 45%; Localisation

rate within the first year after production startSource: JHS Global Insight (data status: 06/10)

5050

•

Localized purchasing throughout supply chain

Localized Value Chain Key Ingredient for Sustainable Profitability

•

Adaption

to local customer needs

•

Local R&D teams in regions

•

Local production facilities for key products

•

Strong dealer network

•

Adapted local marketing

•

Local offer of Financial Services

()1

()

New: Pune

New: Kaluga

Quick expansion

Quick expansion

Market

entry

()

Market entry

()

Market entry

()1

PurchasingResearch andDevelopment Production Distribution Financial

Services

1

Partial development capacities

2 Market entry plannedSource: Volkswagen Group

2

2

2

51

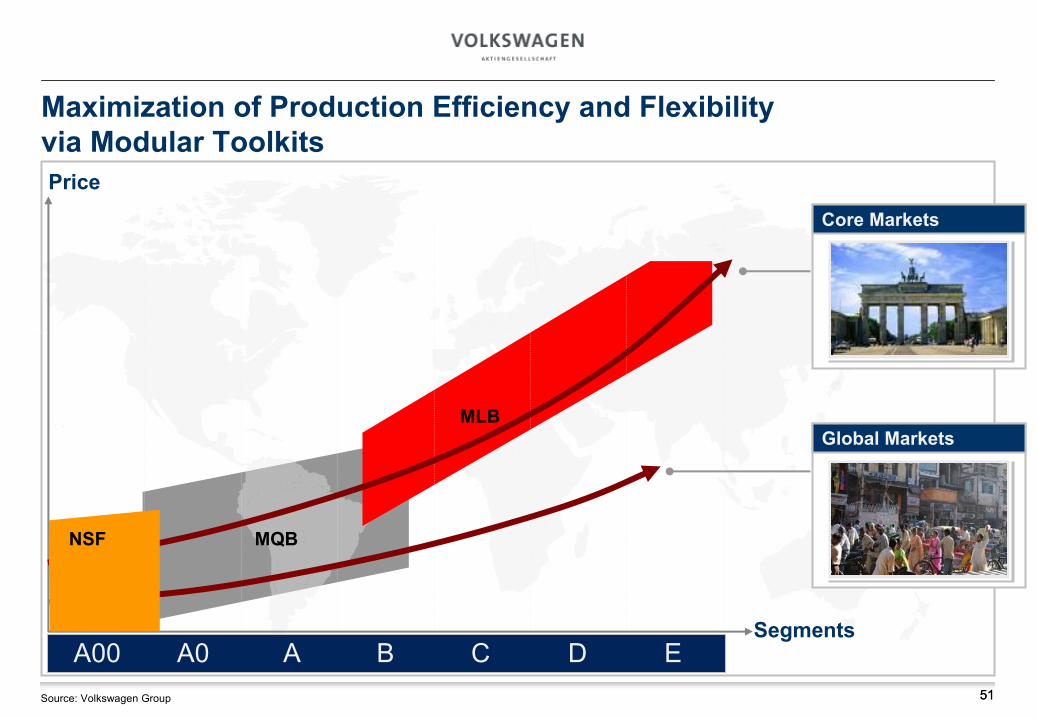

Maximization of Production Efficiency and Flexibility via Modular Toolkits

SegmentsA00 A0 A B C D E

Price

MLB

NSF MQB

Core Markets

Global Markets

Source: Volkswagen Group 51

5252

Local Sourcing of Key Components Examples for local parts

Europe

Polo steering system

Electronic hydraulic power system

India

Electric power system

Cost savings: 15 -

25%

Polo twist beam rear axle

Source: Volkswagen Group

5353

Continuous Productivity Improvements Volkswagen Way: Lower Ramp up Costs and Production Time

Touareg New Touareg

Lower ramp-up costs and production efficiency via•

Production friendly development•

Process standardization•

Improved logistics

Reduction by > 25%

Source: Volkswagen Group

5454

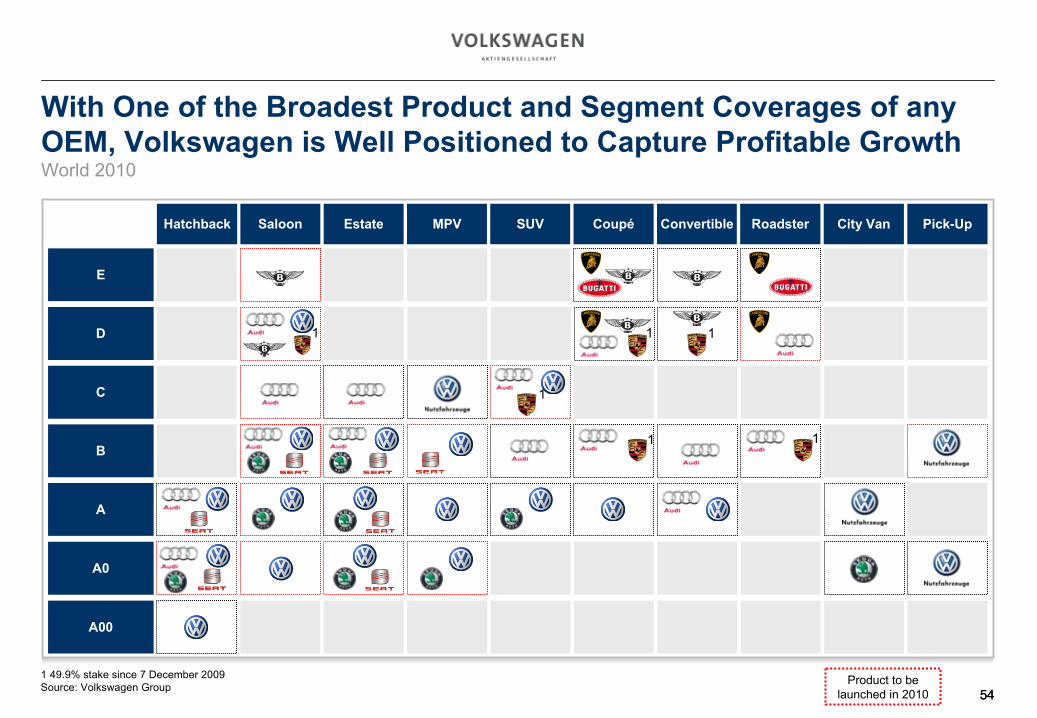

With One of the Broadest Product and Segment Coverages

of any OEM, Volkswagen is Well Positioned to Capture Profitable Growth World 2010

Product to be launched in 2010

E

D

C

B

A

A0

Hatchback Saloon Estate MPV Coupé Roadster City VanConvertibleSUV Pick-Up

A00

1 1

1

1 1

1

1

49.9% stake since 7 December 2009Source: Volkswagen Group

5555

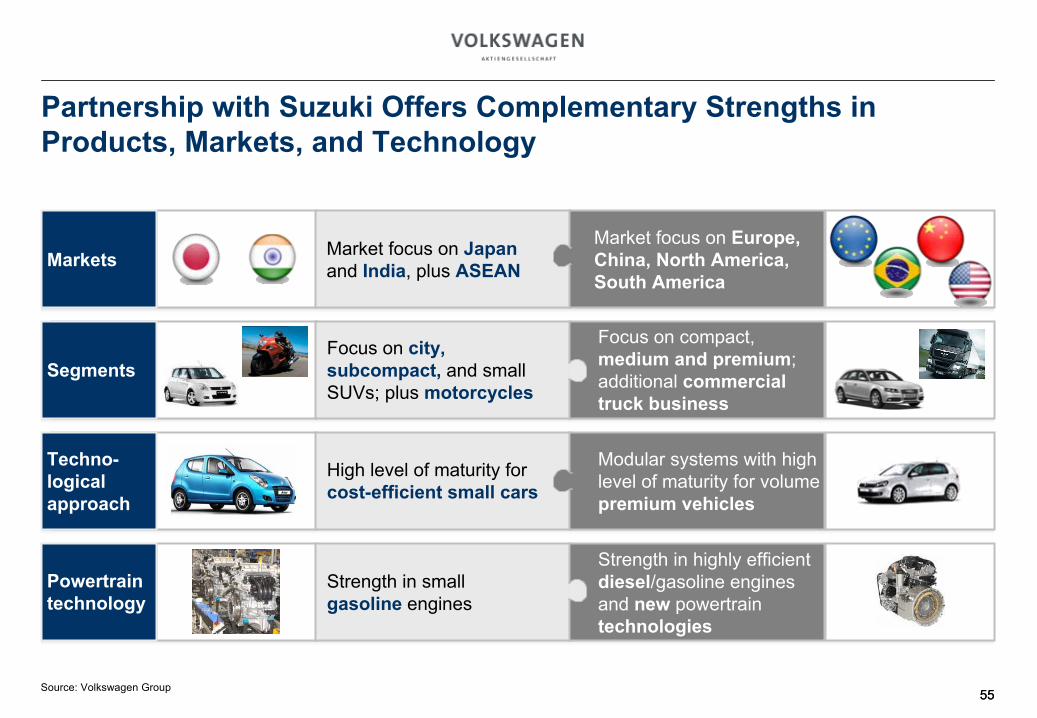

Partnership with Suzuki Offers Complementary Strengths in Products, Markets, and Technology

Market focus on Japan

and India, plus ASEAN

Market focus on Europe, China, North America, South America

Focus on city, subcompact,

and small SUVs; plus motorcycles

Focus on compact, medium and premium; additional commercial

truck

business

High level of maturity for cost-efficient small cars

Modular systems with high level of maturity for volume premium vehicles

Strength in small gasoline

engines

Strength in highly efficient diesel/gasoline engines and new

powertrain technologies

Markets

Segments

Techno-logical approach

Powertrain technology

Source: Volkswagen Group

Volkswagen –

On the Road of SuccessGoldman Sachs Investor VisitWolfsburg, September 22, 2010

57

APPENDIX

58

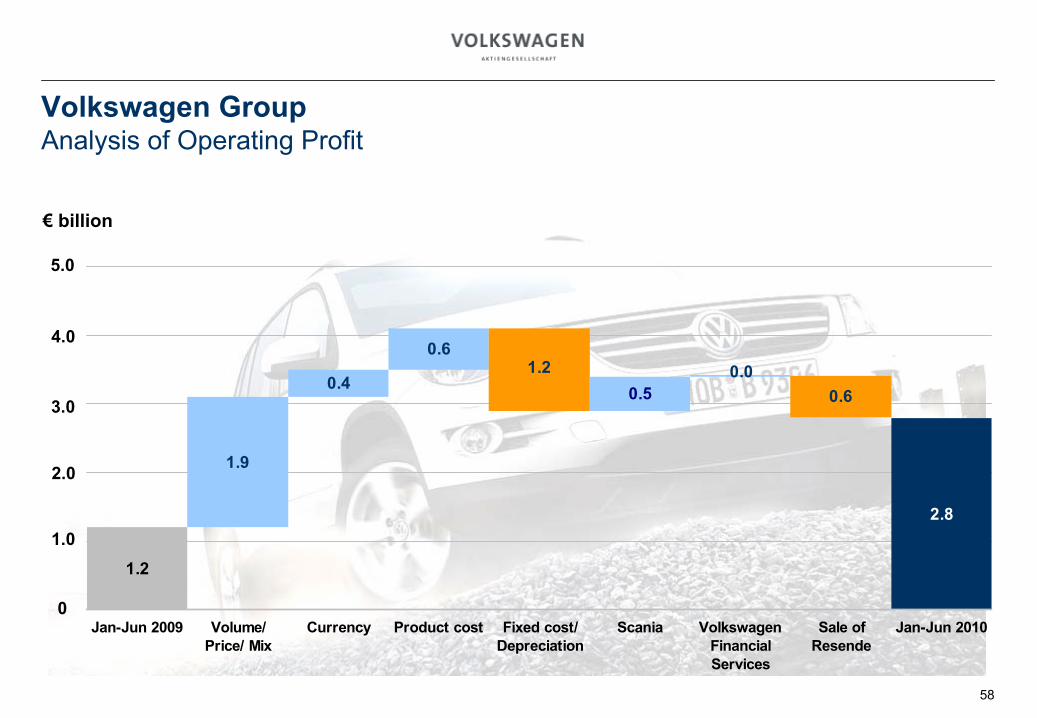

2.8

1.2

0.60.0

1.9

0.4

0.61.2

0.5

Jan-Jun 2009 Volume/Price/ Mix

Currency Product cost Fixed cost/Depreciation

Scania VolkswagenFinancialServices

Sale ofResende

Jan-Jun 2010

Volkswagen Group Analysis of Operating Profit

€

billion

2.0

1.0

0

3.0

5.0

4.0

59

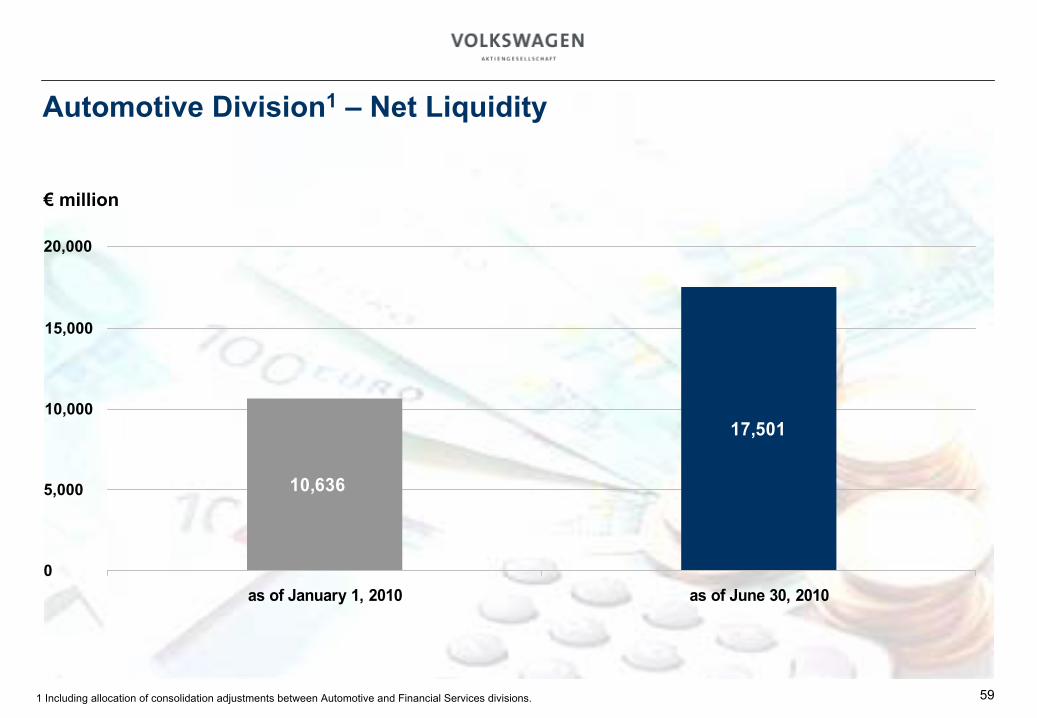

10,636

17,501

as of January 1, 2010 as of June 30, 2010

Automotive Division1

–

Net Liquidity

10,000

15,000

5,000

0

1 Including allocation of consolidation adjustments between Automotive and Financial Services divisions.

€

million

20,000

60

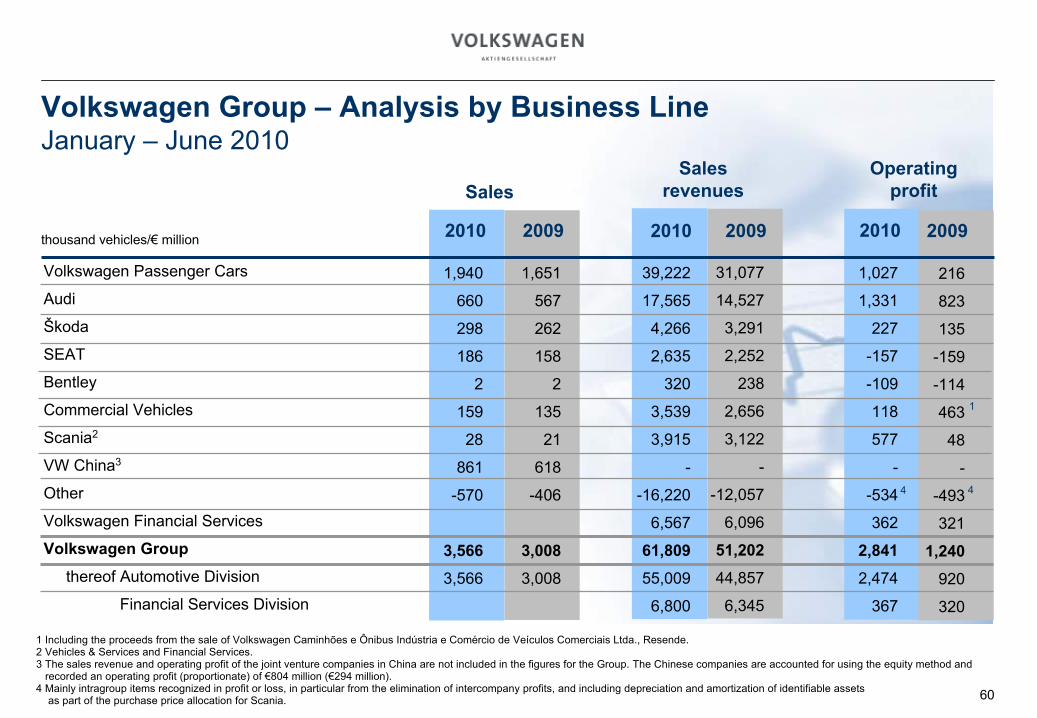

Volkswagen Group –

Analysis by

Business Line January

–

June

2010

Operating profit

Sales revenuesSales

thousand

vehicles/€

million

1,027

1,331

227

-157

-109

118

577

-

-534

362

2,841

2,474

367

2010

Volkswagen Passenger

Cars

Audi

Škoda

SEAT

Bentley

Commercial Vehicles

Scania2

VW China3

Other

Volkswagen Financial Services

Volkswagen Group

thereof Automotive Division

Financial Services Division

2009

216

823

135

-159

-114

463

48

-

-493

321

1,240

920

320

2009

31,077

14,527

3,291

2,252

238

2,656

3,122

-

-12,057

6,096

51,202

44,857

6,345

39,222

17,565

4,266

2,635

320

3,539

3,915

-

-16,220

6,567

61,809

55,009

6,800

2010

1,651

567

262

158

2

135

21

618

-406

3,008

3,008

20092010

1,940

660

298

186

2

159

28

861

-570

3,566

3,566

1

4 4

1 Including

the proceeds

from

the sale

of Volkswagen Caminhões

e Ônibus

Indústria

e Comércio

de Veículos

Comerciais

Ltda., Resende.2 Vehicles & Services and Financial Services.3 The sales revenue and operating profit of the joint venture companies in China are not included in the figures for the Group. The Chinese companies are accounted for using the equity method and

recorded an operating profit (proportionate) of €804 million (€294 million).4 Mainly intragroup

items recognized in profit or loss, in particular from the elimination of intercompany

profits, and including depreciation and amortization of identifiable assetsas part of the purchase price allocation for Scania.

61

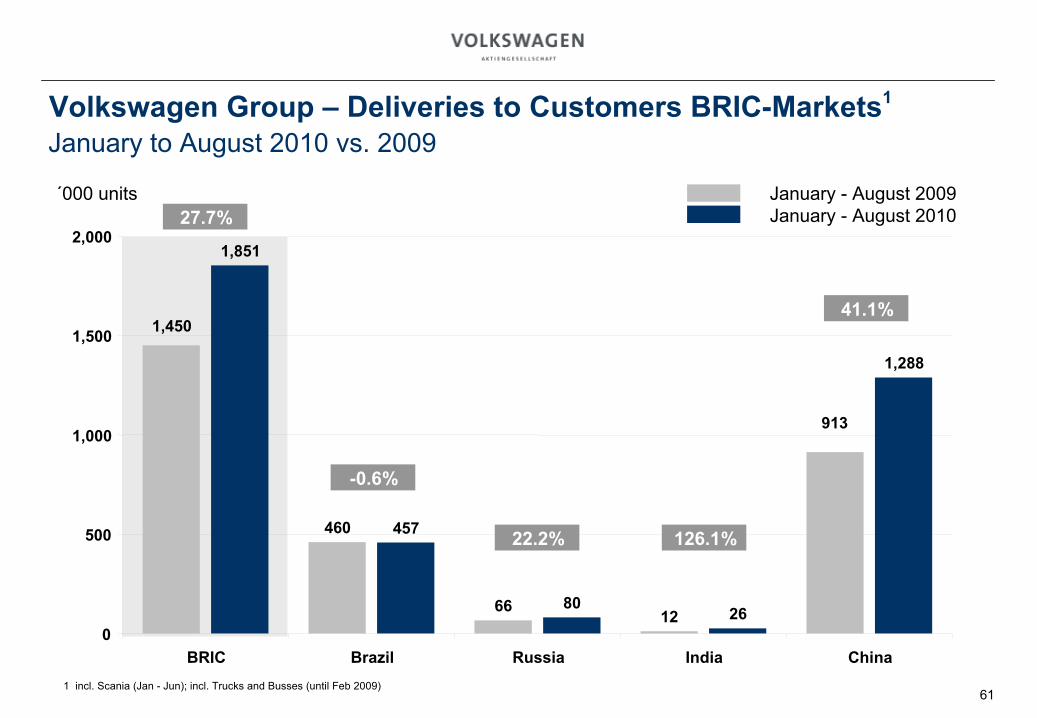

21.2%

Volkswagen Group –

Deliveries

to Customers

BRIC-Markets1

January

to August 2010 vs. 2009

´000 units January

-

August 2009January

-

August 2010

1 incl. Scania (Jan -

Jun); incl. Trucks and Busses (until

Feb 2009)

460

913

66 12

1,450

1,288

80 26

1,851

457

0

500

1,000

1,500

2,000

BRIC Brazil Russia India China

27.7%

-0.6%

22.2% 126.1%

41.1%

62

Volkswagen Polo Limousine

63

Volkswagen Sharan

64

Audi A7

6565

Audi A8

66

Škoda Fabia Combi GreenLine

6767

SEAT Ibiza ST

6868

Volkswagen Amarok

69

Scania R 620 Highline

70

This presentation contains forward-looking statements and information on the business development of the Volkswagen Group. These statements may be spoken or written and can be recognized by terms such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “will”

or words with similar meaning. These statements are based on assumptions relating to the development of the economies of individual countries, and in particular of the automotive industry, which we have made on the

basis of the information available to us and which we consider to be realistic at the time of going to press. The estimates given involve a degree of risk, and the actual developments may differ from those forecast.

Consequently, any unexpected fall in demand or economic stagnation in our key sales markets, such as in Western Europe (and especially Germany) or in the USA, Brazil or China, will have a corresponding impact on the development of our business. The same applies in the event of a significant shift in current exchange rates relative to the US dollar, sterling, yen, Brazilian real, Chinese rinminbi

and Czech koruna.

If any of these or other risks occur, or if the assumptions underlying any of these statements prove incorrect, the actual results may significantly differ from those expressed or implied by such statements.

We do not update forward-looking statements retrospectively. Such statements are valid on the date of publication and can be superceded.

Disclaimer