tcaccfin4.files.wordpress.com · web viewquestion 1 bank date details debit credit balance 20 jul...

TRANSCRIPT

EXAM REVISION QUESTIONS UNIT 4 SOLUTIONSQUESTION 1BankDATE DETAILS DEBIT CREDIT BALANCE20 JUL

APPLICATIONS – ORDINARY

500,000 500,000DR

24 JUL

PREMLINARY EXPENSES 10,000 490,000DR

Application - ordinaryDATE DETAILS DEBIT CREDIT BALANCE20 JUL

BANK 500,000 500,000CR

24 JUL

ORDINARY SHARE CAP 500,000 0

Ordinary Share CapitalDATE DETAILS DEBIT CREDIT BALANCE24 JUL

APPLICATION – ORDINARY

500,000 500,000CR

Preliminary expensesDATE DETAILS DEBIT CREDIT BALANCE24 JUL

CASH AT BANK 10,000 10,000DR

QUESTION 2DATE DETAILS DEBIT CREDIT31 July Cash at Bank

Applications – ordinaryApplications for ordinary share issue

2,000,0002,000.,000

3 August

Applications – ordinary Ordinary share capitalAllotment of 2,000,000 ordinary shares at $1 each

2,000,0002,000,000

BALANCE SHEETEQUITYShare Capital 2,000,000

QUESTION 3DATE DETAILS DEBIT CREDIT31 Cash at Bank 400,000

Aug Applications – ordinaryApplications for ordinary share issue

400,000

9 Sept Applications – ordinary Ordinary share capitalAllotment of 400,000 ordinary shares at $1 each

400,000400,000

30 Sept

Share issue costs Cash at BankPayment of share issue costs

2,0002,000

Ordinary share capital Share issue costsTransfer of share issue costs.

2,0002,000

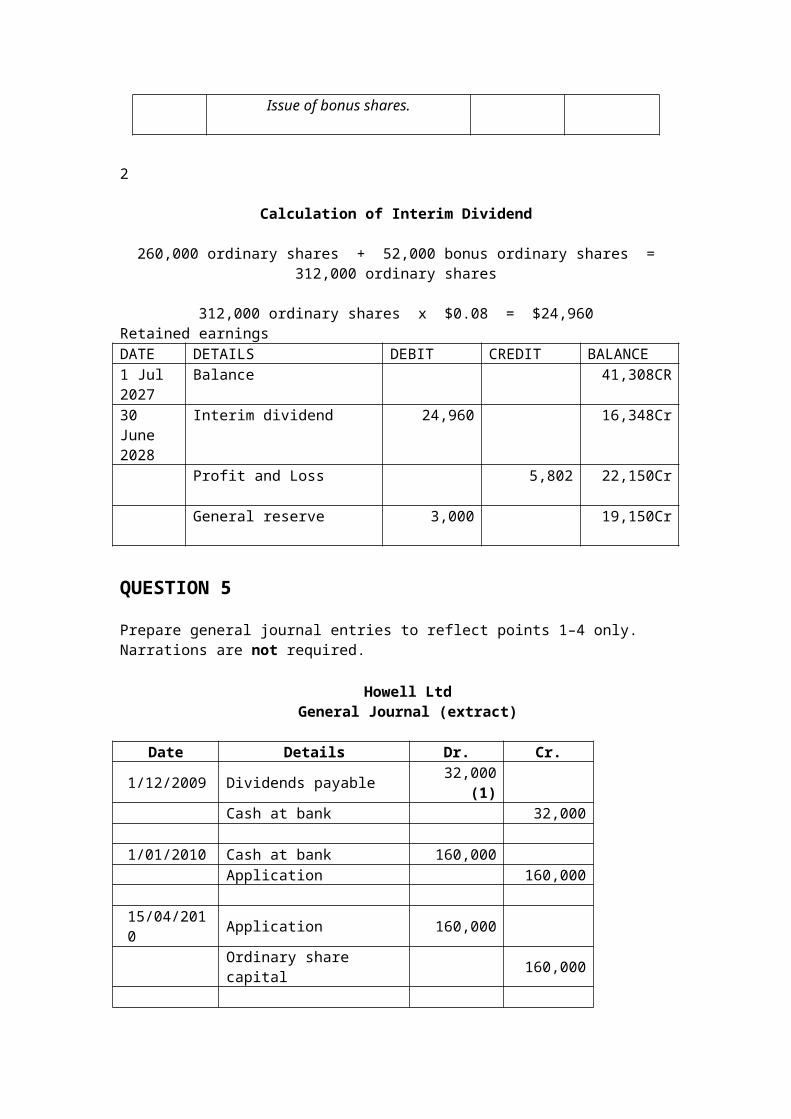

QUESTION 4Calculation of Bonus Share Issue

260,000 ordinary shares

5

= 52,000 bonus ordinary shares

52,000 bonus ordinary shares x $2.00 per share = $104,000 additional share capital

General JournalDate Details Debit Credit

2024Aug 19 Cash at Bank

Application

Cash received from share issue.

520,000520,000

Aug 31 Application 520,000

Share Capital

Issue of 260,000 $2.00 ordinary shares.

520,000

Aug 31 Share Issue Costs Cash at Bank

Payment of share issue costs.

3,100 3,100

Share Capital Share Issue Costs

Transfer of share issue costs.

3,100 3,100

Calculation of Bonus Share Issue

(260,000 ordinary shares / 5) x $2.00 per share = $104,000

General JournalDate Details Debit Credit

2026Nov 1 General Reserve

Share Capital

Issue of bonus shares.

104,000104,000

2

Calculation of Interim Dividend

260,000 ordinary shares + 52,000 bonus ordinary shares = 312,000 ordinary shares

312,000 ordinary shares x $0.08 = $24,960Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2027

Balance 41,308CR

30 June2028

Interim dividend 24,960 16,348Cr

Profit and Loss 5,802 22,150Cr

General reserve 3,000 19,150Cr

QUESTION 5Prepare general journal entries to reflect points 1–4 only. Narrations are not required.

Howell Ltd General Journal (extract)

Date Details Dr. Cr.1/12/2009 Dividends payable 32,000

(1)Cash at bank 32,000

1/01/2010 Cash at bank 160,000Application 160,000

15/04/2010 Application 160,000Ordinary share capital 160,000

30/04/2010 Retained earnings 140,000General reserve 140,000

1/06/2010 General reserve 240,000 (2)

Ordinary share capital 240,000

All correct dates given

Workings:

Dividends payable = 400,000 x $0.08 = $32,000Bonus share issue:

480,000 ¿ 4 = 120,000120,000 x $2 = $240,000

(b) Prepare a Statement of comprehensive income

Howell LtdStatement of comprehensive income

for the year ended 30 June 2010

Revenue 575,000Cost of Sales (250,000)Gross Profit 325,000Other Income 25,000Expenses (excluding finance costs) (49,000)Finance costs (1,000)Profit before income tax 300,000Income tax expense 90,000

Profit for the period 210,000Other comprehensive incomeGain on asset revaluation 50,000Other comprehensive income for the period net of income tax

50,000

Total comprehensive income for the period 260,000

QUESTION 61 Calculation of Other Expenses

Wages ($162,000 + $9,361) 171,361Telephone 33,000Insurance ($25,000 – $5,400) 19,600Rent 147,000Depreciation of Office Equipment 3,000Total Other Expenses 373,961

Marketing Consultants LimitedStatement of Comprehensive Income

for the year ended 30 June 2028Fees ($609,010 – $15,900) 593,110Other IncomeInterest ($3,500 + $291) 3,791

596,901Less Other Expenses (373,961)Less Finance Expenses (interest on loan) (7,800)Profit before Income Tax 215,140Less Income Tax Expense (64,542)Profit for the period 150,598Total comprehensive income for the period 150,598

2 Bonus Share Issue

103,950 ordinary shares / 9 = 11,550 new shares

11,550 ordinary shares x $1.30 = $15,015

Total Share Capital = $101,000 + $15,015 = $116,015

Calculation of General Reserve

Balance on 1 July 2024 26,000Less Bonus share issue 15,015Balance on 30 June 2025 10,985

Calculation of Asset Revaluation Reserve

Balance on 1 July 2024 0Add revaluation of land 18,000Balance on 30 June 2025 18,000

Calculation of Totals Reserve

General Reserve 10,985Asset Revaluation Reserve 18,000Balance on 30 June 2025 28,985

Calculation of Retained Earnings

Balance on 1 July 2024 39,400Add Profit 150,598Less Dividend 67,000Balance on 30 June 2025 122,998

Marketing Consultants LimitedBalance Sheet

as at 30 June 2028EquityShare Capital 116,015Reserves 28,985Retained Earnings 122,998Total Equity 267,998

QUESTION 7

Note On April 30 – can use 2 entries :(1) Declaration of dividend:Debit – Retained earnings, Credit – Interim Dividend payable

Then: (2) Payment of dividendDebit – Interim dividend payable, Credit – Bank

Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2003

Balance 625,000Cr

30 Apr 2003

Interim dividend 57,500 567,500Cr

30 June 2004

Profit and Loss 140,000 707,500Cr

General reserve 85,000 622,500Cr

QUESTION 8

(B)

Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2002

Balance 41,000Cr

30 June 2003

Final preference dividends paid

2,000 39,000Cr

Interim ordinary dividend paid

36,000 3,000Cr

Profit and Loss 40,000 43,000Cr

General reserve 15,000 28,000Cr

QUESTION 9

Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2008

Balance 10,000Dr

30 June 2000

Final Preference Dividend

6,400 16,400Dr

Final Ordinary Dividend 32,200 48,600DRInterim Preference Dividend

4,480 53,080Dr

Interim Ordinary Dividend

25,760 78,840Dr

General Reserve 10,000 88,840DrProfit and Loss 260,000 171,160CR

General JournalDate Details Debit CreditJune 30 09 Profit and Loss

Retained EarningsTransfer of profit to retained earnings

260,000260,000

Retained Earnings Final Preference Dividend Final Ordinary Dividend

68,8406,400

32,200

Interim Preference Dividend Interim Ordinary DividendTransfer of dividends to retained earnings

4,48025,760

Retained earnings General ReserveTransfer to general reserve

10,00010,000

Balance Sheet (extract) as at June 30, 2009

Property, Plant and Equipment 140,000

EquityShare Capital 414,200Reserves 77,800Retained earnings 171,160

663,160

Show the note attached to the balance sheet for the final dividends at June 30, 2009

The directors have recommended a 3% final dividend for preference shareholders and a 9 cents per share final dividend for ordinary shareholders

QUESTION 10

General JournalDate Details Debit CreditOct 31 Bank

ApplicationApplication received for

48,000 shares

168,000168,000

Nov 2 Application Preference Share CapitalTo record the allotment of 48,000 shares at $3.50 each

168,000168,000

Nov 2 Preference Share capital Share issue costsTransfer of share issue costs

2,0002,000

Share issue costsBankPayment of share issue

costs

2,0002,000

Preference share capitalShare issue costsShare issue costs

transferred

2,0002,000

Application - preferenceDATE DETAILS DEBIT CREDIT BALANCE31 OCT

BANK 168,000 168,000Cr

SHARE CAPITAL 2,000 0

Share CapitalDATE DETAILS DEBIT CREDIT BALANCE

APPLICATION – PREFERENCE

168,000 168,000CR

SHARE ISSUE COSTS 2,000 166,000CR

Share issue costsDATE DETAILS DEBIT CREDIT BALANCE

CASH AT BANK 2,000 2,000DRSHARE CAPITAL 2,000 0

General JournalDate Details Debit CreditJune 30 07 Profit and Loss

Retained EarningsTransfer of profit to retained earnings

72,80072,800

Retained earnings General ReserveTransfer to general reserve

10,00010,000

Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2006

Balance 21,500Cr

30 June 2007

General Reserve 10,000 11,500Dr

Profit and Loss 72,800 84,300CR

Balance sheet (extract)

Share capital 562,000

General reserve 30,000

Retained earnings 84,300

676,300

Notes attached to the Balance Sheet for final proposed dividends at 30 June 2007.

The directors have recommended that preference shareholders receive their annual preference dividend and that ordinary shareholders receive a dividend of 6 cents per share

QUESTION 11Workings: Bonus Share issue 480,000/5 = 96,000

Leighton LimitedStatement of changes in equityfor the year ended 30 June 2010

Share capital

Retained earnings

Revaluation surplus

General reserve

Total equity

Balance at 1/7/2009 576,000 65,600 64,000 48,000 753,600

Changes in equity for the year

Issue of share capital 57,600 (57,600) 0

Share issue costs

Dividends (14,000) (14,000)

Total comprehensive income for the year

61,600 40,000 101,600

Transfer to General Reserve

(10,000) 10,000 0

Balance at 30/6/2010 633,600 103,200 104,000 400 841,200

Leighton LimitedBalance Sheet

as at 30 June 2010

Current AssetsCash and cash equivalents 70,400Trade Receivables 25,500Inventories 34,600Other 5,600Total Current Assets 136,100Non-Current AssetsInvestments 41,000Property, Plant and Equipment 866,900Total Non-Current Assets 907,900Total Assets 1,044,000Current LiabilitiesTrade and other payables 66,800Other 2,000Current Tax Liability 22,000Total Current Liabilities 90,800Non-Current LiabilitiesBorrowings 112,000Total Non-Current Liabilities 112,000Total Liabilities 202,800Net Assets 841,200

EquityShare capital 633,600Other reserves 104,400Retained earnings 103,200Total Equity 841,200

Note 3: Property, plant and equipmentLand 633,900Buildings 186,000Accumulated depreciation (48,000)

138,000Plant and equipment 134,000Accumulated depreciation (39,000)

95,000Total property, plant and equipment 866,900

Calculation of final dividend:633,600 x 10c = 63,360

QUESTION 12

General Journal

Date Details Folio Number

Debit Credit

2008Jun 30

Profit and Loss Retained Earnings

Transfer of profit after tax.

89,50089,500

Retained Earnings Interim Ordinary Dividend

Transfer of interim dividends.

20,00020,000

General Reserve Retained Earnings

Transfer from general reserve.

25,00025,000

ASK LtdStatement of changes in equityfor the year ended 30 June 2009

Share capital

Retained earnings

Revaluation surplus

General reserve

Total equity

Balance at 1/7/2009 300,000 (1,500) 40,000 80,000 418,500

Changes in equity for the year

Issue of share capital

Share issue costs

Dividends (20,000) (20,000)

Total comprehensive income for the year

89,500 89,500

Transfer from General Reserve

25,000 (25,000) 0

Balance at 30/6/2010 300,000 93,000 40,000 55,000 488,000

ASK LimitedBalance Sheet

as at 30 June 2009

Current Assets

Cash and cash equivalents 46,200Trade Receivables 62,800Inventories 17,000Total Current Assets 126,000Non-Current AssetsProperty, Plant and Equipment 474,500Total Non-Current Assets 474,500Total Assets 600,500Current Liabilities

Trade and other payables 20,500Current Tax Liability 42,000Total Current Liabilities 62,500Non-Current Liabilities

Borrowings 50,000Total Non-Current Liabilities 50,000Total Liabilities 112,500Net Assets 488,000EquityShare capital 300,000Other reserves 95,000Retained earnings 93,000Total Equity 488,000

Extract of the notes to the balance sheetas at 30 June 2009

Note 2: Final DividendsThe directors have recommended a 5c per share final dividend to ordinary shareholders

Note 3: Property, plant and equipmentLand 260,000Buildings 230,000Accumulated depreciation 62,000

168,000Plant and equipment 65,000Accumulated depreciation 18,500

46,500Total property, plant and equipment 474,500Note 4: EquityShare Capital600,000 ordinary shares of .50 each fully paid less share issue costs

300,000

Other reservesAsset revaluation 40,000General 55,000

QUESTION 13ADate Details Debit CreditJune 30 09

BankApplicationApplication monies

received

1,000,0001,000,000

Application Preference Share CapitalShares allotted

1,000,0001,000,000

Retained earningsInterim dividend payable

Interim dividend approved

100,000100,000

Interim dividend payableBank

Interim dividend paid

100,000100,000

Retained earningsFinal ordinary dividend

payableFinal preference dividend

payableFinal dividend approved

121,00097,00024,000

Final ordinary dividend payableFinal preference dividend payableBank

Final dividend paid

97,000

24,000121,000

BStatement of comprehensive income

for the year ended 30 June 2009Revenue 5,119,000Cost of Sales (2,800,000)Gross Profit 2,319,000Other Income 91,000Expenses (excluding finance costs) (1,746,000)Finance costsProfit before income tax 664,000Income tax expense (199,200)Profit for the period 464,800Other comprehensive incomeGain on asset revaluation

Other comprehensive income for the period net of income taxTotal comprehensive income for the period 464,800

Balance Sheet (extract)as at 30 June 2009

Current Liabilities

Trade and other payables 486,000Debentures 100,000Bank Loan 50,000Current Tax Liability 199,200Total Current Liabilities 817,200Non-Current Liabilities

Borrowings 270,000Total Non-Current Liabilities 270,000Total Liabilities 1,087,200

Note 3: Property, plant and equipmentLand 1,100,000Buildings 750,000Accumulated depreciation 33,000

717,000Plant and machinery 570,000Accumulated depreciation 172,000

398,000Fixtures and fittingsLess Accumulated depreciation

98,00039,00059,000

Total property, plant and equipment 2,274,000

Statement of changes in equity (extract)for the year ended 30 June 2009

Retained earnings

Balance at 1/7/2009 660,000Changes in equity for the yearIssue of share capitalShare issue costsDividends (221,000)Total comprehensive income for the year

464,800

Transfer from General ReserveBalance at 30/6/2010 903,800

QUESTION 14 Kevin 07 Holdings LtdStatement of changes in equityfor the year ended 30 June 2008

Share capital

Retained earnings

Revaluation surplus

General reserve

Total equity

Balance at 1/7/2009 - 84,000 - 300,000 384,000

Changes in equity for the year

Issue of share capital 5,000,000

5,000,000

Share issue costs

Dividends (160,000)

(160,000)

Total comprehensive income for the year

626,000 600,000 1,226,000

Transfer to General Reserve

(100,000)

100,000 0

Balance at 30/6/2010 5,000,000

450,000 600,000 400,000 6,450,000

Retained earnings at 30 Sept 08:Retained earningsDATE DETAILS DEBIT CREDIT BALANCE1 Jul 2007

Balance 84,000Cr

30 June 2008

Profit and Loss 626,000 710,000Cr

General reserve 100,000 610,000Cr

Dividends 160,000 450,000Cr

EquityShare capital 6,200,000Other reserves 600,000Retained earnings 450,000Total Equity 7,250,000

Note 4: EquityShare Capital8,800,000 ordinary shares of .50 each fully paid 4,400,000800,000 ordinary shares of $1 each fully paid200,000 8% cumulative preference shares of $5 each fully paid

800,0001,000,0006,200,000

Other reservesAsset revaluation 200,000General 400,000

600,000

QUESTION 15BanlDATE DETAILS DEBIT CREDIT BALANCE1 MAY

APPLICATION 30,000 30,000DR

Application - ordinaryDATE DETAILS DEBIT CREDIT BALANCE1 MAY

BANK 30,000 30,000CR

SHARE CAPITAL 2,000 0

Share Capital - OrdinaryDATE DETAILS DEBIT CREDIT BALANCE

APPLICATION – ORDINARY

30,000 30,000CR

General JournalDate Details Debit CreditJune 30 08

Profit and Loss Retained earningsProfit after tax transferred

9,9009,900

General reserveRetained earnings

Transfer from reserve

1,0001,000

Retained earningsInterim ordinary dividend

payableFinal preference dividend

payable

Interim dividends

7,6002,0005,600

approvedEquityShare capital 140,000Other reserves 8,000Retained earnings 7,800Total Equity 155,800

QUESTION 16Calculation of Profit after Tax

Old insurance policy expires on 30 September 2020.

New insurance policy begins on 1 October 2020 costing $3,720.

Closing balance of prepaid insurance on 30 June 2020 is 3 months x $3,720 = $930

Prepaid Insurance – Opening balance 900 + Bank 3,720– ?? expense 3,690 = closing balance 930

$900 (3 months) + (9/12 x $3,720) = $3,690 insurance expense

Bottles of mineral water sold for year ended 30 June 2020 = 69,100 - 2,100 = 67,000

Energy Mineral Water Wholesalers LimitedCalculation of Profit after Tax

for the year ended 30 June 2020Sales (67,000 units x $3.00) 201,000Less Cost of Sales (67,000 units x $1.80) 120,600Gross Profit 80,400Less Other ExpensesWages ($51,000 + $1,900) 52,900Insurance 3,690Interest 2,500Depreciation of plant and equipment($11,000 accum dep - $5,000 accum dep)

6,000 65,090

Profit before tax 15,310Less Income tax expense 4,593

Profit after tax $10,717

Calculation of Cash at Bank

Inventory Opening balance 2,500 + ??Bank – Cost of sales = 120,600 = Closing balance 4,800 - therefore bank amount 122,900

Calculation of number of Ordinary Shares Issued

[($101,400 share capital + $1,600 share issue costs) x 2] = 206,000 ordinary shares

Calculation of Cash at Bank on 30 June 2020Cash at bank on 1 July 2019 $19,614Add sales of mineral water (69,100 units x $3.00) 207,300

226,914LessPurchase of mineral water 122,900Wages 51,000Insurance 3,720Interest 2,500Interim dividend (206,000 ordinary shares x $0.05) 10,300Repayment of debentures 9,600Cash at bank on 30 June 2020 26,894

Calculation of Retained Earnings on 30 June 2020 Opening balance 27,314 + Profit 10,717 + General Reserve

transfer 2,000 – Interim dividend 10,300 = closing balance 29,731

Property, Plant and EquipmentLand 105,000Plant and equipment 40,700Accumulated depreciation (11,000)

29,700Total property, plant and equipment at net book value

$134,700

Energy Mineral Water Distributors LimitedBalance Sheet

as at 30 June 2020Current Assets

Cash at Bank 26,894Prepaid Insurance (3 /12 x $3,720) 930Inventory 4,800Total Current Assets 32,624Non-Current AssetsProperty, Plant and Equipment 134,700Total Non-Current Assets 134,700Total Assets 167,324Current LiabilitiesAccrued Wages 1,900Income Tax Payable 4,593Unearned Revenue (2,100 units x $3.00) 6,300Total Current Liabilities 12,793Non-Current LiabilitiesDebentures 22,400Total Non-Current Liabilities 22,400Total Liabilities 35,193Net Assets 132,131EquityShare Capital 101,400Reserves 1,000Retained Earnings 29,731Total Equity 132,131

QUESTION 17Retained earningsDATE DETAILS DEBIT CREDIT BALANCE30 June 2003

Net Loss 25,200 25,000DR

30 June 2004

Net Profit 661,500 636,500Cr

Ordinary final dividend 300,000 336,500CrPreference final dividend

260,000 76,500Cr

General reserve 50,000 26,500Cr30 June 2005

Net Profit 606,900 633,400Cr

Interim Ordinary dividend

200,000 433,400Cr

Preference final dividend

130,000 303,400Cr

General reserve 280,000 23,400Cr

General JournalDate Details Debit CreditJune 30 09

BankApplication – ordinaryApplication – preferenceApplication monies

received

5,500,0005,000,000

500,000

Application – ordinaryApplication – preference Ordinary Share Capital Preference Share CapitalShares allotted

5,000,000500,000

5,000,000500,000

Share Capital20,000,000 ordinary shares @ 50c each fully paid 10,000,000750,000 13% cumulative preference shares @ $2 each fully paid

1,500,000

11,500,000

Statement of changes in equityfor the year ended 30 June 2005

General reserve

Balance at 1/7/2004 50,000Changes in equity for the yearIssue of share capital (250,000

)Share issue costsDividendsTotal comprehensive income for the yearTransfer to General Reserve

280,000

Balance at 30/6/2005 80,000

QUESTION 18

General JournalJune 30 04

Profit and Loss Retained earningsProfit after tax transferred

246,800246,800

General reserveRetained earnings

Transfer from reserve

20,00020,000

Retained earningsInterim ordinary dividend

payableFinal dividend payable

Interim dividends approved

77,50037,50040,000

EquityShare Capital 825,000Reserves 180,000Retained Earnings 114,300Total Equity 1,119,300

Retained earningsDATE DETAILS DEBIT CREDIT BALANCE30 June 2003

Balance 35,000Dr

Profit 246,800 211,800CrDividends 77,500 134,300CrGeneral reserve 20,000 114,300Cr

Share capital calculation:500,000 ordinary shares at 50c250,000 ordinary shares at 90 c150,000 ordinary shares at $1100,000 ordinary shares at $2

QUESTION 19

Statement of changes in equityfor the year ended 30 June 2006

Share capital

Retained earnings

Revaluation surplus

General reserve

Total equity

Balance at 1/7/2005 6,200,000

72,000 - 130,000 6,402,000

Changes in equity for the year

Issue of share capital 1,600,000

1,600,000

Share issue costs

Dividends (100,000)

(100,000)

Total comprehensive income for the year

480,000 400,000 880,000

Transfer to General Reserve

(70,000) 70,000 0

Balance at 30/6/2006 7,800,000

382,000 400,000 200,000 8,782,000

Current LiabilitiesTrade and other payables 140,000Income Tax Payable 210,000Total Current Liabilities 350,000Non-Current LiabilitiesBorrowings 500,000Total Non-Current Liabilities 500,000

Total Liabilities 850,000EquityShare Capital 7,800,000Reserves 600,000Retained Earnings 382,000Total Equity 8,782,000

QUESTION 20

QUESTION 21

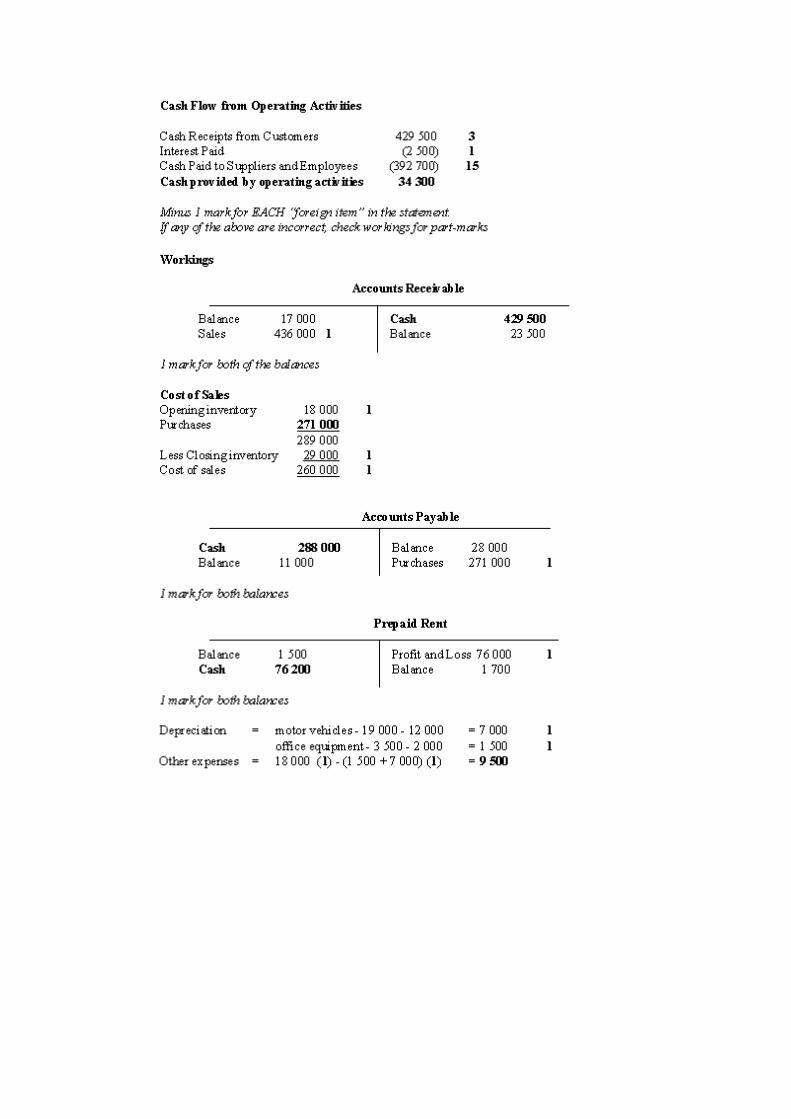

Lizard LtdStatement of cash flows

for the year ended 30 June 2010

$ $ MarksCash flows from operating activitiesReceipts from customers 2,849,000 3

Payments to suppliers and employees(1,878,300

) 11Income tax paid (136,000) 1Interest paid (18,750) 1Net cash from operating activities 815,950

Cash flows from investing activitiesInterest received 2,400 1Dividends received 24,000 1Sale of investments 100,000 1Proceeds from disposal 20,000 2Payments for property, plant and equipment (560,000) 3

(413,600)

Cash flows from financing activitiesIssue of debentures 120,000 1Additional share capital 100,000 1Dividends paid (671,350) 4

(451,350)

Net cash decrease for period (49,000) 1Cash and cash equivalents at start 110,000 2Cash and cash equivalents at end $61,000 2

Total 35

Marking:

Award the marks shown in the final column for numerical accuracy. Amounts which require calculation are worth more than one mark.

The exact marks breakdown can be viewed in the items on the next page. If numerical calculations are correct but the item is misclassified, then deduct 1 mark, up to a maximum of 2 marks.

Item 1 (3 marks)

Calculating cash receipts MarksOpening balance 119,000Add credit sales 2,850,000 1Less accounts received ???Closing balance 2,969,000

Therefore cash received from customers is $2,849,000

1

Opening and closing balance 1Total 3

Item 2 (11 marks)

Payments to suppliers and employees

Marks

Calculating PurchasesClosing inventory 173,000Add cost of sales 1,340,000 1Less opening inventory 188,000Purchases 1,325,000 1

Opening and closing inventory 1Total 3

Calculate Cash Payments MarksOpening accounts payable balance 82,000Add purchases 1,325,000 1Less closing accounts payable balance

104,000

1,303,000 1Opening and closing balance 1

Total 3

Schedule of Payments to Suppliers and Employees

Marks

Payments to suppliers 1,303,000 1Other expenses 670,300 1Less depreciation 95,000* 3

1,878,300Total

5

* (65,000 – 12,000) + (187,000 – 145,000) = 53,000 + 42,000 = 95,000

Item 3 (2 marks)

Proceeds from Disposal MarksBook value 12,000 1Add gain on sale 8,000 1Proceeds from disposal 20,000

Total 2

Item 4 (3 marks)

Plant and equipment MarksOpening balance 795,000Less sale of equipment 65,000 1Acquisition of new plant and equipment

???

Closing balance 1,290,000

Therefore new equipment acquired = $560,000 1

Opening and closing balance 1Total 3

Item 5 (4 marks)

Retained earnings MarksOpening balance 169,000Add profit 663,350 1Less general reserve 50,000 1Less dividends ???Closing balance 111,000

Dividends paid must therefore be $671,350 1

Opening and closing balance 1Total 4

Item 6 (2 marks)

Cash and cash equivalents at start

Marks

Cash 45,000 1Add short-term deposits 65,000 1

110,000Total 2

Item 7 (2 marks)

Cash and cash equivalents at end

Marks

Cash 21,000 1Add short-term deposits 40,000 1

61,000Total 2

QUESTION 22

Financial reports are an essential component of all business activity as they provide a wide variety of information for both internal and external users. Over recent years corporate failures have called into question the reliability of financial information.

(a) Explain the roles of the FRC, AASB, ASX, ASIC, IASB (full titles should be included

in your answer) and external auditors. (18 marks)

Financial Reporting Council

Description MarksAny three of the following, to a max of 3 marks 3The main role of the FRC is to oversee the activities of the AASB 1Its main functions are to:

monitor the process for adopting International Accounting Standards

1

act as an advisory body to the AASB 1 give the Federal Treasurer reports and advice on the process of

standard setting1

Total 3

Australian Accounting Standards Board

Description MarksAny three of the following, to a max of 3 marks 3The main role of the AASB is to develop and amend accounting standards.

1

Another of its functions is to make accounting standards for the purpose of the Corporations Act.

1

It is also required to participate in and contribute to the development of a single set of Accounting Standards for world-wide use.

1

Total 3

Australian Stock Exchange

Description MarksAny three of the following, to a max of 3 marks 3Its main role of the ASX is to ensure that publicly listed companies comply with the Listing Rules.

1

The ASX aims to ensure that all companies listed on the Stock Exchange act in a manner which is at all times in the best interests of

1

shareholders and the general public.Listing Rules specify the form, content and frequency of published financial statements for public companies.

1

Total 3

Australian Securities and Investments Commission

Description MarksAny three of the following, to a max of 3 marks 3The overall role of the ASIC is to administer corporate legislation. 1The ASIC is responsible for enforcing the accounting standards set by the AASB.

1

It also interprets accounting standards where this is necessary and issues these interpretations through the medium of Accounting Practice Notes.

1

1Total 3

International Accounting Standards Board

Description MarksAny three of the following, to a max of 3 marks 3The IASB is responsible for the development of international accounting standards.

1

IASB is responsible for International Financial Reporting Standards. 1These standards are to be used by all countries so that financial information is comparable across borders

1

The IASB is also responsible for improving financial reporting by developing new standards in areas that have not been regulated previously.

1

Total 3

External auditors

Description MarksAny three of the following, to a max of 3 marks 3The role of external auditors is to provide an Independent review of the financial statements of reporting entities.

1

Auditors are required to ensure that: financial statements present a true and fair view (1 mark) of the

activities of an entity1

they comply with the Corporations Act and AASB Accounting Standards

1

Total 3

(b) Describe the effectiveness of these organisations in ensuring the reliability of financial

statements. (12 marks)

Description MarksDescription of effectiveness – any six of the following, to a max of 12 marks

12

Financial statements are the responsibility of the directors. 1–2Regulators are often restricted in their role due to resource constraints.

1–2

Audit function has been enhanced by the following measures in order to improve the quality of external audits:

Auditing standards have force of law equivalent to AASB standards

Auditors are required to sign an independence declaration which forms part of the financial report asserting their firm’s independence from the entity

1–2

Reliability as defined in the conceptual framework is an abstract concept. This makes it difficult to apply, leaving preparers scope to interpret the accounting requirements.

1–2

Despite an increase in financial reporting regulation, like all rules, if the rewards are great enough, there will always be those willing to break them.

1–2

Prosecution of directors is difficult to prove and costly to pursue. 1–2ASX, unlike some of the other regulatory authorities, has the capacity to suspend of de-list companies if they don’t comply. It can be more difficult for other regulatory authorities to enforce compliance.

1–2

Entities need flexible reporting requirements in order to be able to reflect their performance. US approach to financial reporting of rules based standards has not seen an end to the problem of creative accounting.

1–2

Total 12

QUESTION 23(a) Outline four incentives for businesses to act in an environmentally

responsible manner.(8 marks)

Description MarksIncentives – any four of the following, to a max of 8 marks 8Possible answers could include:Climate change and sustainability is a mainstream concern and the community expect government and business to take action to reduce their environmental impact.

1–2

Sustainable practice is required to maintain ‘licence to operate’. 1–2Failure to act may result in consumer boycott of products/services. 1–2Increasing environmental legislation requiring improved environmental performance

1–2

Coercive influence of suppliers and customers requiring organisations to reduce environmental impact

1–2

Total 8Note: Accept other appropriate answers.

(b) Describe the potential benefits to a business of engaging in environmentally responsible practices. (12 marks)

Description MarksBenefits – any four of the following, to a max of 12 marks 12Possible answers could include:Savings in outflows from reduced: 1–2

energy costs 1–2 water usage 1–2 materials 1–2

Increased sales due to ‘green’ image leading to: potentially perceived as lower risk 1–2 lower insurance premiums 1–2 lower lending rates 1–2

Higher staff morale leading to: higher productivity 1–2 higher retention 1–2 attraction of quality staff 1–2

Avoid costs associated with poor environmental performance due to: customer boycotts 1–2 fines for breaching environmental regulations 1–2 litigation 1–2

Total 12

(c) Describe the potential costs to a business of engaging in environmentally responsible practices. (4 marks)

Description MarksCosts – any four of the following, to a max of 4 marks 4Possible answers could include:Cost to purchase and implement environmental technologies 1–2

Cost of environmental consultants to identify areas for improvement 1–2Higher cost associated with green products/supplies 1–2Higher cost of being economically responsible will be passed on to consumers which may adversely affect competitiveness.

1–2

Total 4Note: Accept other appropriate answers.

(c) Describe briefly corporate social responsibility. Using two examples (other than environmental), explain how these demonstrate corporate social responsibility. (6 marks)

Description MarksCSR – any two of the following, to a max of 2 marks 2Possible answers could include:Responsible business practices and processes (1 mark) which contribute to the enhancement of society

1

‘Giving back to society/community’ 1Total 2

Note: Accept other appropriate answers.and

Description MarksExamples of CSR (other than environmental) – any two of the following, to a max of 4 marks

4

Possible answers could include:Philanthropic support which aids society by, for example, enhancing artistic endeavours, assisting the underprivileged and disadvantaged, developing community goodwill through community based events, support educational institutions.

1–2

To act in an ethical and responsible manner – for example not exploiting workers in third world nations, having a strong commitment to employee safety, respect for indigenous culture

1–2

To enhance local communities by providing employment opportunities and investing back into the local community

1–2

Total 4Note: Accept other appropriate answers.QUESTION 24Debt to equity

Description MarksDefinition: Measure of organisations debt level orMeasure of financial risk

1

Trend: Increasing trend indicating higher level of borrowings and at a level beyond other industries from 2008

1

Reason: Organisation borrowing more money to fund capital expenditure

1

Total 3

Quick assetDescription Marks

Definition: Ability of an organisation to repay short term debt using only most liquid assets

1

Trend: Increasing which suggests improved liquidity but well above industry average which suggests inefficient use of resources

1

Reason: Increase in cash on hand (not making best use of available cash) or receivables (poor credit collection procedures)

1

Total 3

Price/earningsDescription Marks

Definition: Amount investors are willing to pay, for every $1 of profit, to own ordinary shares in a company

1

Trend: Declining trend and well below industry average in 2008 and 2009 indicating company has fallen out of favour with investors

1

Reason: Firm specific issues such as legal action, market anxiety over debt levels, concerns about managerial competency, increase in competition. Any one answer will suffice

1

Total 3

ProfitDescription Marks

Definition: The amount earned in operating profit for every dollar of sales

1

Trend: Increasing trend however still well below industry average indicating the firm continues to lack control over expenditure, i.e. inefficient

1

Reason: Positive trend occurring due to; Increase in selling price due to increased demand Cost of sales, relative to selling price, declines due to

increased competition among suppliers Greater control over operating expense

1

QUESTION 25

QUESTION 26(a)WORKINGS

General ledger of Kurraloo LimitedAccounts receivable

Opening balance *112 000 Bank [1] 2 412 000

Sales [1] 2 450 000

Closing balance *150 000

2 562 000 2 562 000*[1] for both opening and closing balancesi.e. 3 marks for calculation of $2 412 000 cash received from accounts receivable carried forward to Cash Flow Statement

Accounts payableBank [1] 1 368

000Opening balance *67 000

Closing balance *83 000 Purchases [1] 1 384 000

1 451 000 1 451 000* [1] for both opening and closing balancesi.e. 3 marks for calculation of $1 368 000 cash paid to accounts payable carried forward to Schedule of payments to suppliers and employees

Plant and equipmentOpening balance *620 000 Sale of plant and

equipment[1] 50 000

Bank [1] 505 000

Closing balance *1 075 000

1 125 000 1 125 000* [1] for both opening and closing balancesi.e. 3 marks for calculation of $505 000 cash paid for new plant and equipment carried forward to Cash Flow Statement

Accumulated depreciation of plant and equipmentSale of plant and equipment

^[2] 42 000

Opening balance *135 000

Closing balance *162 000 Depreciation of plant and equipment

[1] 69 000

204 000 204 000*[1] for both opening and closing balances^[2] for correct sale of plant and equipment figure (50 000 [1] – 8 000 [1] = 42 000)i.e. 3 marks for calculation of $69 000 depreciation of plant and equipment carried forward to Schedule of payments to suppliers and employees

Sale of plant and equipmentPlant and equipment [1]

50 000 Accumulated depreciation of plant and equipment

[1] 42 000

Bank [1] 5 000Loss on sale of plant and equipment

[1] 3 000

50 000 50 000

i.e. 4 marks for calculation of $3 000 loss on sale of plant and equipment carried forward to Schedule of payments to suppliers and employees

Schedule of payments to suppliers and employees Accounts payable [3] 1 364 000 Note: these 12

marks to be carried forward to the Cash Flow Statement

Other expenses [1] 580 700

LessDepreciation of plant and equipment [4] (69

000)Loss on sale of plant and equipment [4] (3

000)508 700

1 876 700

Sale of investments: $500 000 [1] – $400 000 [1] = $100 000

KURRALOO LIMITEDCash Flow Statement for the year ended 30 June 2008

Cash flows from operating activities $ $

Receipts from customers 2 412 000[3] + 1

Payments to suppliers and employees (1 876 700)[12] + 1

Income tax paid (128 000)[1]

Interest paid (13 500) [1] Net Cash from operating activities

393 800

Cash flows from investing activitiesProceeds from sale of investments 100 000

[2] + 1Proceeds of sale of plant and equipment 5 000

[1]Dividends received 18 000

[1] Interest received 1 200

[1]Purchase of plant and equipment (505 000) [3]

Net cash used in investing activities(380 800)

Do not penalise consequential errors [28 marks]

(b)

Cash includes cash on hand and in the bank, including at-call deposits with banks or other financial institutions [1] such as the cash holdings of Kurraloo Limited. [1] Cash equivalents includes short-term, highly liquid investments which are readily convertible into cash [1] such as the short-term deposits held by Kurraloo Limited. [1]

[4 marks]

QUESTION 27City Traders Limited

Allowance for Doubtful DebtsBad Debts 4 Opening Balance 7Closing Balance 9 Doubtful Debts 6

13 13

Accounts ReceivableOpening Balance 33 Discount Allowed 2Sales 165 Sales Returns 3

Bad Debts 4

Bank 142Closing Balance 47

198 198

InventoryOpening Balance 10 Cost of Sales 37Bank 38 Closing Balance 11

48 48

Prepaid RentOpening Balance 13 Rent Expense 65Bank 73 Closing Balance 21

86 86

WagesBank 29 Opening Balance 19Closing Balance 20 P + L 30

49 49

Motor VehiclesOpening Balance 60 Sale of Asset 22

Bank 34 Closing Balance 7294 94

Accumulated Depreciation of Motor VehiclesSale of Asset 13 Opening Balance 14Closing Balance 17 Depreciation Expense 16

30 30

Sale of AssetMotor Vehicles 22 Accumulated

Depreciation 13Gain on Sale of Asset

8 Bank 17

30 30

Retained EarningsGeneral Reserve 1 Opening Balance 4Dividend 2 Profit and Loss 5Closing Balance 6

9 9

other Cash Expenses

Other Expenses (income statement) 25Less Depreciation 16Cash Expenses 9

City Traders LimitedPayments to Suppliers and Employees

Inventory purchased 38Rent 73Wages 29Other expenses 9Total $149

City Traders LimitedStatement of Cash Flowsfor the year ended 30 June 2017

Cash flows from operating activities

Receipts from customers 142Payments to suppliers and employees (149)Interest received 2Interest paid (1)Income tax paid (2)Net cash from operating activities (8)Cash flows from investing activitiesProceeds of sale of motor vehicle 17Payment for motor vehicle (34)Net cash from investing activities (17)Cash flows from financing activitiesDebentures 5Additional share capital 49Dividend paid (2)Net cash from financing activities 52Net increase in cash held 27Cash and cash equivalents at start of period 19Cash and cash equivalents at end of period 46

QUESTION 28Current Ratio1

30 June 2025

$40 + $5 + $34 + $11 + $110 X

100

$92 + $8 + $30 1

$200X

100

$130 1

B154%

2b should be able to pay its short term debts

Quick Asset Ratio

30 June 2025

$40 + $5 + $34X

100

$92 + $8 + $30 1

$79X

100

$130 1A

61%

4A may, in an emergency, find it difficult to pay its short term debts

Debt to Equity Ratio5

30 June 2025

$170X

100

$220 1

A77%

6Given the industry average debt to equity ratio is 80%, then Perth Traders Limited has:a a reasonable level of debt

Times Interest Earned Ratio

730 June 2025

$90 + $15X

100

$15 1

A7 times

8 Which of the following statements is correct?a The number of times the profit before tax covers the interest

cost is above the often quoted appropriate safety margin of 3 or 4 to 1.

Profit Ratio9

30 June 2025

$63X

100

$342 1

C18.4%

10d both a and c

Rate of Return on Assets11 Average Assets = ($270 + $390) / 2 = $330

Year Ended 30 June 2025

$90 + $15X

100

$330 1

B

31.8%

12 True

Earnings per Ordinary Share

13

The total weighted average number of issued ordinary shares is calculated:

335 x 290 ordinary shares = 266 shares365 1

30 x 480 ordinary shares = 39 shares

365 1

Total weighted average number of issued ordinary shares

= 305 shares

Year Ended 30 June 2025$63 – $16

305

C

15 cents per share

14

a be satisfied with the performance of the company

Price Earnings Ratio15

Year Ended 30 June 2025$3.00$0.15

A20 times

16

a the future growth in the profit of the company is likely to be very good

but the shares may be fully priced with little short term growth prospects

Dividend Yield

17

Year Ended 30 June 2025

$0.31X

100

$3.00 1

B

10.3%

18

Given that the fixed term bank deposit interest rate is 8% per annum, is Perth Traders Limited shares a suitable investment for a person who wants a cash (that is, a dividend) return?a Yes

Debtors Collection Period

19Average Debtors ($14 + $34) / 2 = $24

Year Ended 30 June 2025

$24X

365

$342 1

C26 days

20

b improved credit control and collection procedures.

Inventory Turnover

21Average Inventory ($46 + 110) / 2 = $78

Year Ended 30 June 2025

$204

$78

A

2.6 times

22

a the products sold by the business are popular with consumers.