viewpoints - top and emerging risks - ey - united...

TRANSCRIPT

ViewPoints

27 July 2015

There are things we could envision happening that could call into question

the very existence of the organization, and they are not quantifiable, nor can

the bank put a timescale on them … They make normal business risks seem

inconsequential. – Bank director

Bank boards continue to face increasing accountability for ensuring banks are

effectively overseeing risks. Yet, despite improvements in risk identification,

reporting, and interaction between banks and their supervisors, participants in the

Bank Governance Leadership Network (BGLN) question whether they are truly

engaging in the right ways on the key risks that could bring down an individual bank

or have a broader systemic impact.

Over several months, culminating with meetings on 9th June in New York and

17th June in London, BGLN participants shared perspectives on the top and

emerging risks facing large banks and the financial system and how boards and

supervisors can improve oversight. The exchange of perspectives yielded new

insights and produced actionable next steps for individual and collective responses.

This ViewPoints synthesizes the perspectives and ideas raised in the meetings, as well

as in nearly 30 conversations beforehand with directors, executives, supervisors, and

banking professionals.1

This document is divided into five sections.

The first describes the challenges and opportunities in how boards can improve

oversight of top and emerging risks. The remaining four focus on top risks

prioritized for discussion by participants.

Improving identification and discussion of key risks (pages 3-4).

Boards and risk committees spend a lot of time reviewing risk reports and

discussing how their institutions are managing key risks. Yet, participants see

opportunities to shift the focus of their efforts to be sure they are spending

more time openly and informally discussing with management the key risks

that are emerging and could impact the viability of their institutions.

Emerging sources of systemic risk (pages 5-8). Much effort has been

expended globally to decrease systemic risk in banking through new

regulatory requirements. But these actions may be creating new risks by

limiting the role banks can play in providing market liquidity, and in pushing

systemic risk into the world of shadow banking, to which banks still have

significant exposure, but which remains opaque and largely unregulated.

In addition, participants question whether central clearing parties might be

systemically important themselves.

The risk from misconduct could be an existential one (pages 9-10).

Banks and regulators have been focused on addressing conduct issues, notably

by launching culture reform initiatives and improving accountability and

controls. But, participants see persistent risk of legal and financial damage, but

also reputational and political risk that could threaten banks’ ability to operate

in some markets.

Increasing strategic risk and potential for disruption (pages 11-13).

Banks are all identifying ways to build more agile, profitable institutions in the

face of mounting pressure to improve returns with increasing competitive

pressure from multiple directions, including financial technology companies,

that threatens margins in core businesses. As the threat grows more quickly

than many expected, the urgency to respond is increasing.

The unique and growing cyber threat (pages 14-16). Participants

expressed growing frustration with the challenges of managing cyberrisk. As

awareness and knowledge about the threat has improved, the nature of the

risk continues to evolve, and while the damage from attacks to date has been

relatively limited, participants see the potential for long-term threats to

emerge in different and more damaging ways. Discussions included necessary

actions individual firms can take, and the continued need for improved

collaboration among banks, regulators, and governments to protect the

system.

Since the beginning of the BGLN, conversations on risk identification have been

closely aligned with broader themes around risk governance and culture. While

participants said they have made significant improvements to their risk identification

and escalation processes, they still feel that senior management and boards can

improve the dialogue on the real risks their institutions face.

Why is identifying and discussing top and emerging risks so challenging?

Participants described the following obstacles to improving board engagement on

key risks:

The time and resources for discussing emerging risks are limited.

Time and resources are largely focused on reviewing near-term, core

banking risks, compliance, and regulatory reporting activities. A director

noted, “There are very few human or technical resources available to look at

extremely unlikely events.” Part of the challenge is that managers and

boards often allocate time to current, near-term risks that are easy to capture

at the expense of more distant and less manageable ones.

There is a tendency to avoid the really hard questions. A chief risk

officer (CRO) said two things are very difficult for executives and directors:

“One, asking the genuinely confounding and difficult questions about our

strategy, and two, considering what we should really be stress testing. It is

human nature to say, ‘That will never happen here,’ or to forget how

painful it was the last time, or to blame someone else. That is why banks go

through cycles.” A director elaborated, “There is a danger that we have all

been educated in not being the outlier and to do the same as everyone. It is

a herd risk where we accept something is the status quo.”

The truly systemic risks are difficult to identify and mitigate in

advance. One participant argued, “It is a struggle to figure out the process

for identifying these top risks and the systemic risk beyond your books. The

overall contagion effect is really hard to put your arms around.” Another

director concurred, stating, “It is one of the great challenges to know what

is correlated.”

Practical solutions to improving oversight of top and emerging risks

An executive asserted, “We know what good looks like: focusing on a smaller

number of topics and facilitating a discussion with good, challenging questions

without obvious answers.” For most, the key to success is allowing the board to

“provide insight and foresight.” A director stated, “We need a forum for that.”

Specific recommendations included the following:

Streamline reporting and make risk information usable. Directors

said that “voluminous” risk reports are part of the problem. A CRO said,

“Directors often tell me they don’t need the whole list of horrors. They say,

‘Just tell me, what do I need to know? What are the two to three things

that really impact our bank?’” Another said, “What we do in board

“There are very

few human or

technical resources

available to look at

extremely unlikely

events.”

—Director

“We know what

good looks like:

focusing on a

smaller number of

topics and

facilitating a

discussion with

good, challenging

questions without

obvious answers.”

—Executive

meetings is too formal, with a thousand pages in every meeting. We are

trying to get it down and highlight the actual issues.”

Move from formal tick-the-box sessions to real discussions. Most

participants agreed that they continue to spend too much time in formal

settings, running through a checklist of risk-related issues. One director

noted, “We need more opportunities for informal discussion where we can

speak candidly without worrying that we will send a whole team scrambling

for a deep dive.”

Focus on a limited number of issues on which board members can

provide value. Directors and executives continue to work toward a

balance between being thorough and what most believe is the more

effective approach to risk oversight: focusing on a limited number of issues

that represent the greatest potential threats and those most amenable to

board members’ judgment. One CRO said, “The key is ignoring the press

and understanding your own top risks. The top risks that sell newspapers

may be different than the risks that could kill your bank.”

Ensure boards have access to expertise and exposure to internal and

external perspectives. Boards have sought to broaden their expertise

through who they recruit, but they cannot bring on an expert for each

technical, operational, and strategic risk the institution faces. There are

other options. For example, one director’s board now brings in outside

experts as full members of special board committees. Others hold board

meetings in places near emerging trends – for example, one bank held their

recent board meeting in Silicon Valley. Others suggested boards should

reach out to more employees deeper in their organization to get more

insight into the organization’s day-to-day workings.

Participate in more informal engagement with supervisors.

Directors and executives said there is still only limited informal discussion

between bank boards and supervisors on emerging risks. One director was

more critical of the content of the meetings than of their frequency: “The

regulators are starting to engage quite regularly with the board, but are

asking more about how things are going rather than giving us information.”

Participants agreed that more constructive dialogue requires additional trust.

“The top risks that

sell newspapers

may be different

than the risks that

could kill your

bank.”

—CRO

Individually, the banks are safer. Collectively, the system might not be.

– Participant

Since the financial crisis, governments, supervisors, and individual banks have been

deploying significant resources to monitor systemic risks to the financial system. The

financial crisis revealed that neither regulators nor institutions had a clear picture of

risks building up in the financial system. In response, central banks have been given

a more prominent role in macroprudential supervision and are using their new

power to ensure individual firms are less susceptible to systemic risks. BGLN

participants are concerned, however, about the movement of risk outside the

regulated banking sector as a result. In addition, they see the potential for a liquidity

crisis because of the restrictions on banks and the changing roles of market

participants, as well as the potential creation of new systemically important financial

institutions (SIFIs) in the form of central clearinghouses. The BGLN discussion on

these topics resulted in concrete recommendations for actions to prepare for and

address these risks.

Several investment firm leaders, including the Blackstone Group’s Stephen

Schwarzman and Larry Fink from BlackRock, have cautioned that a lack of liquidity

could cause or exacerbate a financial crisis.2 Participants expressed concern that

when the Federal Reserve ends its quantitative easing program and raises interest

rates, a sell-off of assets might be triggered, prompting a chain reaction with

unexpected correlations and impacts. One director remarked, “I’m concerned about

second-order unforeseen risks of the unwinding of low interest rates. We will see

things that we don’t expect in different asset classes.” A supervisor observed,

“I don’t think it would take a great deal to break down liquidity, because it can’t

continue functioning as it should in a crisis, and the probability of a crisis is now

higher.”

Rising rates may prompt a sell-off with few buyers

A director expressed concerns about retail customer behavior as interest rates rise:

“On the bond side, for example in the ETF [exchange-traded fund] market, do retail

customers understand yield maturity? When they see returns go negative for the first

time, will they just sell? If so, where does the liquidity come from? Not the SIFIs.”

And retail investors are not the only ones that might sell. One participant worried,

“When asset prices change, shadow bankers and investors, in theory, are

professional, and these changes in prices will be passed on and stay contained, but I

don’t think this will happen. The herd instinct will be magnified by the algorithms

used by many players. It will amplify the speed and momentum, and they will feed

off of each other.”

New regulations tie SIFIs’ hands

Participants felt that new leverage and proprietary trading prohibitions have curtailed

big banks’ ability to act as shock absorbers by buying distressed assets. Many banks

have removed themselves from key equity and debt markets, significantly reducing

“We will see things

that we don’t

expect in different

asset classes.”

—Director

liquidity in the trading markets, especially for debt,3 and non-bank players are

stepping in to fill the void. A CRO summarized the problem: “The industry has

been firmly trained that size matters. Capital requirements, the leverage ratio, etc.,

have been driving every bank to shrink their balance sheets. Every firm is trying to

keep inventory to the bare minimum. If you go back before the crisis, banks had

large balance sheets with an ability to absorb corrections … Volatility now is quite

significant.” One participant went even further, claiming, “We created a procyclical

system without buffers on the other side to buy assets. If ETFs, insurers, all say,

‘Now is a good time to sell,’ large institutions will be sitting there with their hands

tied.”

Correlations may not be well understood

A director said banks need to be looking beyond what they believe to be their direct

and secondary exposures to consider how exposed they could be to potentially

correlated risks. Participants expressed concerns about two related issues:

Models understate the correlations. Several participants raised concerns

about model risk more broadly. In the event of a liquidity crisis, those

concerns could be realized. A director said, “I am a mathematical modeler by

training and I don’t believe them.” Another warned, “Volatility will be

higher and the correlations will be higher than the models think.” A related

concern is that the value of collateral is overstated and the counterparties may

be less robust than expected. As a result, a participant said, “I worry about the

liquidity of so-called liquid assets. I am skeptical about the value of collateral

on the trading books in investment banks.”

Accounting could exacerbate contagion. Fair-value accounting has the

potential to exacerbate contagion. Participants fear that the vulnerabilities of

pension funds, insurers, and others to liquidity issues could be “magnified into

the banks by mark-to-market accounting.” A director predicted,

“[Vulnerability] will move quickly into bank balance sheets, then into

capital.”

Though some commentators suggest the risk from liquidity issues is overstated,

BGLN participants cautioned against understating a risk that could cause a crisis.

An executive asserted, “I think this is more urgent than regulators think. We are

sitting in a big asset price bubble. At some point, it will unwind. It is going to

happen.”

Participants urged greater collective preparation

Participants had several recommendations for concrete steps the industry and

regulators can take to prepare for the worst:

Stakeholders should support constructive dialogue. Regulators

acknowledged the merit of banks’ liquidity concerns, but said the refrain from

banks often sounds like they are making the case for reversing new regulatory

limitations. Industry participants recognized that they need to frame it

differently. One director argued, “We need a positive, more constructive

“We created a

procyclical system

without buffers on

the other side to

buy assets.”

—Participant

dialogue with the regulators. We need to identify positive ways to introduce

liquidity as opposed to unpicking regulations.”

Supervisors ought to lead banks in scenario analysis. In London,

participants suggested that regulators adjust stress testing to include different

scenarios. All participants favored candid discussion of how different

constituencies can prepare and how they should react in the event of a crisis.

Participants suggested collaborative scenario planning involving banks and

regulators could help participants think through how a liquidity event could

play out for their firms and the system.

Market participants should identify “circuit breakers” in the network

that can stem the spread of problems. Participants suggested that

regulators introduce circuit breakers in extreme market conditions. They

recommended that market participants and regulators work together to

identify these circuit breakers, what the transmission mechanisms are and how

they work.

Central banks may be forced to step in regardless

If a new crisis arises, will central banks intervene to inject liquidity? One regulator

was of the opinion that “central banks won’t be lenders of last resort, but lenders of

first resort” because they will have to act to provide market liquidity. Part of the

challenge is political pressure opposing government intervention and legal constraints

on what the Fed or other central banks are permitted to do. One regulator stated,

“I don’t see any other mechanism other than the Fed growing their balance sheet

[further]. The problem is Dodd-Frank restrained what the Fed can do. We would

need an act of Congress.”

It is impossible that in a large bank, someone won’t be doing the wrong

thing. The fear we have at this point is that we are subject to the pile-on

effect and populism will feed those with political interests to take more drastic

actions. – Bank director

Recently, the BGLN has discussed conduct supervision and the need to address

culture in the face of growing costs for conduct-related fines and provisions.4 In the

wake of the string of banking scandals, media and regulatory attention on cultural

challenges, and increasingly aggressive commentary by senior regulators, some

participants expressed a sense of fatigue at the prospect of addressing culture and

conduct yet again.

But today’s levels of conduct risk – with attendant fines, litigation, and reputation

damage – threaten firms’ very existence and have even been highlighted as a

potential source of systemic risk. At the very least, misconduct could jeopardize

banks’ ability to operate in certain markets or businesses, with potential systemic

consequences. A June report from the European Systemic Risk Board stated,

“Misconduct at banks … may damage confidence in the financial system …

Financial and other penalties applied in misconduct cases … may themselves entail

systemic risks that … can create uncertainty about the business model, solvency and

profitability of banks.” The report continued, “The consequences of misconduct

could be a withdrawal from financial markets and activities by a bank, either forced

or on a voluntary basis, such that the functioning of a particular market is impaired,

leading to a direct loss of financial services for the end user.”5

Long-term solutions for a short-term risk

One CRO remarked, “I would argue there is not a single firm in financial services

that can say with confidence that they know the amount of conduct risk they are

running or what their tolerance is for it.” Despite all the attention given to conduct

and culture, much is out of the organization’s control. Another director said, “With

thousands of people in your organization, there will always be someone doing

something that they shouldn’t.” Policymakers, regulators, and bank leaders have

embraced the idea that culture change is the way to improve conduct. BGLN

discussions earlier in 2015 focused on how banks can take a holistic approach to

addressing culture, a process that will take years.6 A regulator suggested that banks

will need to demonstrate that meaningful steps are being taken.

In the near term, improving oversight and accountability may only highlight isolated

bad conduct, making progress difficult to measure and continuing to feed the

narrative that banks and bankers are bad and need to be punished or, in the extreme,

that large, universal banks inherently produce bad behavior and need to be broken

up.

Continued legal uncertainty

The costs of past misconduct have accumulated, and the totals are massive: the total

litigation costs for the biggest global banks since 2010 have broken the $300 billion

barrier.7 A new Bank of England assessment concluded that the amount British

banks paid in fines in 2015 was equivalent to the amount raised from private

“I would argue

there is not a single

firm in financial

services that can

say with confidence

that they know the

amount of conduct

risk they are

running.”

—CRO

investors to bolster capital ratios during that same period.8 What’s more, there may

yet be future litigation costs, even from issues thought to be settled. One participant

noted specifically that the UK Supreme Court decision in Plevin v Paragon

regarding payment protection insurance “could open up more claims even among

those deemed to be sold fairly in the previous process. The court ruled that high

commission charges in and of themselves can render a product as mis-sold.”

A director asserted, “Some of these are very complex cases where there is no law or

regulation we have contravened, but that is not limiting regulators and legal

authorities from applying new standards to past practices. It could involve massive

costs for reviews, lawsuits, and immeasurable make-good payments.”

Anti-bank populism and political backlash

Despite some signals that the enthusiasm for fining banks large sums may be waning

in some key jurisdictions,9 participants remain concerned about rising populist anti-

bank sentiment. Referring to a recent multibillion dollar US Justice Department

settlement on exchange-rate rigging, US Senator Elizabeth Warren wrote in an

email, “This is not accountability for Wall Street. It’s business as usual, and it stinks

… The big banks have been caught red-handed conspiring to manipulate financial

markets … but not a single trader is being held individually accountable, and

regulators are stumbling over themselves to exempt the banks from the legally

required consequences of their criminal behavior.”10 This kind of rhetoric has led

participants to contemplate the following possibilities:

Increasing individual liability. A regulator observed, “No individuals

really paid the price for 2008 because the legal standard has to show they

committed fraud, not just negligence or incompetence,” but another asserted,

“We have the tools to go after individuals, and I think we should.”

Increasing institutional liability. While supportive of increasing individual

accountability for bad actors, participants are concerned that institutions could

be indicted, with potentially grave consequences. One participant argued that

some US state attorneys general are moving in that direction and said the

possibility that deferred prosecution agreements will become indictments in

the future is “a real risk that is being ignored.” While there was some debate

about the extent of the threat, several participants agreed with one who

asserted, “It could kill a SIFI if it escalates too much.”

Political pressure to restructure large banks. A participant asked,

“Is regulatory risk [or] political risk going to tip?” A regulator suggested,

“We need to celebrate successes, so people are aware, but also acknowledge

the bad behavior, demonstrate what is being done to address it, and make sure

your people know what they shouldn’t do. You are still playing catch-up,

and I don’t know if you have time before someone says, ‘Let’s see if we can

break up a big bank.’”

“We have the tools

to go after

individuals, and

I think we should.”

—Regulator

“It could kill a SIFI

if it escalates too

much.”

—Participant

“Banking is one of the least agile industries. We have expensive, old IT

systems, expensive structures, and it needs to change, almost totally, in five

years.” – Director

Over the last seven years, banks have made significant strategic changes. In addition

to the regulatory and market changes driving strategic moves, a rapidly evolving

competitive landscape is increasingly adding to concerns about the sustainability of

bank business models. Last year, Francisco Gonzalez, chairman and CEO of BBVA,

predicted that the next 20 years will see the world go from 20,000 “analogue” banks

to no more than several dozen “digital” institutions.11 Others warn that banks are in

danger of “just becoming the plumbing” if they don’t work out their role in the

evolving financial ecosystem.12

Despite past discussions on the potential for disruption, the urgency with which

participants view the potential risk has heightened. A participant suggested that

banks have been too focused on the short term to properly consider long-term

business model risks. A director noted, “The risk meeting agenda is focused on

current risks borne by the bank. Things like strategic risks are not being discussed

because they won’t blow up in your face, but they may cause your business to go

away.”

As a range of new competitors threaten margins or disintermediation from

customers, banks are determining the appropriate response. Recent BGLN

discussions have focused on the increasing threat of digitally savvy competitors.13

“Every second start-up in Silicon Valley is in financial services,” noted one

participant. Other new competitors include non-bank hedge funds, large private

equity firms, and asset managers. Large banks’ responses are hamstrung by large

organizations, cultures developed over many years, processes and systems not

designed for the changing market, and limits imposed by regulators and supervisors.

Taken cumulatively, these new sources of competition could present real threats to

margins in banks’ core businesses. Participants described two primary concerns:

Disruption is about much more than payments. One director

commented, “This issue crosses all lines, including relationships to

customers, profitability, regulation, and the soundness of these businesses.

A whole bunch of people are out there who think about eating the lunch of

the established banks.” One director stated, “All kinds of people are saying

digitization poses an enormous threat in the payment space, but it could be

way beyond that.” In one scenario, large, cumbersome banks with high

operating costs struggle to compete with innovative, lower-cost, more

customer-friendly enterprises. In another, banks are disintermediated from

their customers by new intermediaries and customer-facing companies. In a

third, digital competition threatens high-margin businesses and currently

profitable business practices, such as cross-selling.

The threat is emerging faster than many expected. For years, BGLN

participants acknowledged these distant realities, but now the threat feels

“This issue crosses

all lines, including

relationships to

customers,

profitability,

regulation, and the

soundness of these

businesses.”

—Director

closer. “The threat from emerging competitors is materializing quicker than

many of us thought. We used to be quite dismissive,” admitted one

director. “This is not a problem that is 10 years out; it is coming now,” said

another.

Banks are not agile enough to respond quickly. Several directors

lamented the inertia and inflexibility in their systems: “We struggle to cope

with new regulations and old IT systems … and are therefore mainly

reactive to new entrants,” said one. Participants agreed agility concerns

extend beyond traditional anxieties about legacy systems. “It is not just IT

systems,” said one, “We spend a billion and a half on IT, we have a staff

brought up in a particular way, a culture groomed by management, and

established systems, which are all in the way. We are hopelessly inadequate

when competitors come in and take share.”

One participant predicted, “There will be big failures. Large amounts of revenue in

banking are payment related and will be disintermediated. Research shows that

30%–35% of earnings are at stake on the fee-based side.” Another said, “The excess

in profit is easy for Silicon Valley to extract. The fee-based model is disappearing.”

A director warned, “In a relatively short period of time, we could be looking back

and saying, ‘How did that happen?’”

All banks are under pressure to improve returns. A participant observed that at

many banks, “the cost base is not shrinking as fast as the balance sheet.” If banks are

to adapt, they need to understand their business models, where and how they are

generating returns, and what they can do to improve the efficiency of their capital

allocations and operations. One regulator criticized bank leadership: “Looking at

transfer pricing, structural reform, [and] recovery and resolution planning revealed

that when you pick something out, bank leaders don’t know how profitable it is or

how it is capitalized.” Another observed, “Most institutions lack real knowledge of

the costs or profitability of individual products.”

In spite of these concerns, participants emphasized it is not all doom and gloom.

In London, one director argued, “There is a huge plus in the names of these

institutions. It is hard to build that trust. There is quite a lot of inertia on our side.”

Another pointed out, “All of these potential entrants would die to have the

information we do.” One director said, “We should use the scale benefits that banks

have. We don’t need to be as agile. We just need to be more paranoid and act

more quickly.”

Participants highlighted the following strategies to confront digital disruption heads

on:

Disrupt better than the competition. One director said, “Our

competitors target the most profitable parts of the value chain. They go for

the inefficiencies in the economics, but we know these things better than

they do. We should choose what we want to play with and have strategic

flexibility.” Others suggested watching market shifts to see where the

greatest threats are emerging, then responding accordingly: “Look at an area

“In a relatively

short period of

time, we could be

looking back and

saying, ‘How did

that happen?’”

—Director

“Most institutions

lack real knowledge

of the costs or

profitability of

individual

products.”

—Regulator

like payments. We can see Apple is targeting it and competing with limited

risk, while extracting a rent. In peer-to-peer, competitors are attacking the

intermediary subsidy that banks take. We can see where the big moves are

and where they are coming from.” With this insider view, bank staff should

think like the innovators. A BGLN participant commented, “Boards should

be encouraging management to test, innovate, partner, and explore.

We need our people working with customers on these things to understand

what they want.”

Refocus core business strategies. Banks may need to drastically alter

practices that have become commonplace. “Banks have to get out of

businesses that are suboptimal,” said one participant. “You used to be able to

subsidize the non-profitable portions of your business, but not anymore.”

One director suggested an even more fundamental change is necessary:

“Rather than being good at a lot of things, we need to be great at a few. It is

about focus versus complexity. Focus gets you a huge benefit, and some

businesses still benefit from scale, but it is about scale in a product segment or

geography.”

“Rather than being

good at a lot of

things, we need to

be great at a few.”

—Director

Any problem we have with hackers is nothing compared to the system being

hacked. Banks should have a handle on day-to-day cyberrisks,

but the bigger ones require the government taking a role. – Director

Since 2012, the BGLN devoted a series of discussions to cybersecurity.14 It is clearly

a risk that has emerged, and most institutions have accepted the notion that attacks

are unavoidable. Even governments are unable to defend against breaches, as events

such as the hacking of the White House computer system in April and the US Office

of Personnel Management in June have shown. “Cyber is not a risk, it is a

certainty,” stated one executive. A director characterized current knowledge of the

threat as “the tip of the iceberg,” and said the threat is revealed as “bigger and bigger

the more we dig.”

While banks have been aware of the threat for several years, a director noted,

“The things people were worried about four years ago are not the same things they

are worried about today.” As more activity moves to digital platforms, the risk only

increases. Furthermore, highly publicized breaches like the theft and subsequent

publication of information have shown the reputational damage that even “minor”

attacks can cause.

Despite numerous public breaches, there has not been “a billion dollar loss or any

period of time with the whole system being brought down.” Should we take

comfort in that? A participant suggested that attackers may be patient and that the

breaches to date could primarily represent reconnaissance for future attacks or uses of

data with potentially more harmful results. A regulator said, “There have been very

serious breaches. How long [the hackers] have been in there is unknown; the data

lost is unknown.” Trying to imagine the thought processes of an attacker, one

participant said, “If I was thinking about the long game, I would build a customer

information file and use analytics to predict behavior or steal money. The long-term

reconnaissance is the same as [many data aggregators] seeking to collect data to

monetize the customer.”

Increasing supervisory focus

Supervisors are increasingly focusing on ensuring all banks are appropriately

prepared. In the United Kingdom, the Prudential Regulation Authority and

Financial Conduct Authority have for the first time sent letters to banks with specific

questions about their preparedness for cyberattacks. Others are enhancing their

capabilities: one regulator took their best internal cyber expert and moved him into

supervision. Another participant suggested that regulators establish standards to

ensure weak links don’t threaten the system: “Anybody with a license to operate

should have these standards. If you want access to critical infrastructure, then you

need to have these standards.” Regulators, for their part, questioned whether they

can keep up with the changes in the nature of the threats, but acknowledged their

role in pressing for improvements and holding banks accountable.

“How long [the

hackers] have been

in there is

unknown; the data

lost is unknown.”

—Regulator

Challenges for risk management and oversight

In past BGLN discussions, risk executives and directors admitted they were

struggling with oversight of cyberrisk, with which few had direct experience. In the

most recent discussions in London and New York, participants were asked if boards

are any better prepared today. One director asked, “What would a well-prepared

board even look like?” Some participants questioned the ultimate goal. One said,

“You need an objective on cyber. I haven’t heard anyone articulate the objective.”

Therefore, participants discussed important steps for improving governance of

cyberrisk:

Defining a cyberrisk appetite or tolerance. One director commented,

“It is a big challenge to develop a risk appetite for cyber. What are the

metrics to do this? Most of the information is historical. How do you

prioritize and articulate your risk appetite?” As firms develop and improve

systems and move to increasingly digital platforms, participants emphasized

that a balance must be struck between customer ease of use and security. This

reality makes defining a cyberrisk appetite or tolerance all the more important.

One participant said, “You need a risk appetite for the level of protection, and

[you need to] determine the level of investment required to achieve the level

of protection that you are comfortable with.” The objective must be to

understand where the trade-offs are being made and how they are being

managed.

Getting the basics right. A participant asserted that in some respects,

“financial services is as good as it gets” regarding cybersecurity. But others

argued that banks are not even covering the basics. One regulator

commented on recently completed reviews of firm-level efforts, observing,

“It showed that banks do not know their IT assets and capabilities. It is at the

elementary level where they are finding deficiencies. For example, on things

like [software] patch management, they are well behind. These are

foundational issues that don’t need IT experts to grapple with. It is the

opposite of comforting. Basic infrastructure that should be in place is

absolutely missing.”

Prioritizing investment. Having increased their spending on cybersecurity,

many organizations struggle with deciding if those increases are sufficient and

where and how the money can be most effectively invested. One participant

said, “You are investing enough until there is a breach, and then it is not

enough.” One bank board reportedly doubled its spending following a major

hack. Benchmarking is also difficult, as one participant suggested, “You

shouldn’t care what your competitors are spending, the question is how do

you spend the right amount in the right ways for my organization?”

Deciding where to spend money requires an understanding of what

information is most valuable and potentially vulnerable. “Protecting the

crown jewels,” is an objective, and one director argued, “The crown jewel is

the information that shows how all of your data is organized, the map.”

Defining success. Some suggested that directors simply need to ensure that

management is doing everything possible, recognizing that breaches will

“[You need to]

determine the level

of investment

required to achieve

the level of

protection that you

are comfortable

with.”

—Participant

“The crown jewel is

the information

that shows how all

of your data is

organized, the

map.”

—Director

occur. One director said, “What worries me is the people with more

resources who may decide to make me a target. They have a lot more

resources than I can possibly aggregate. All I can do is try to make it harder

[for them].” A director stated, “I have no tolerance for not doing everything

possible to protect ourselves, with the caveat that we can offer an acceptable

customer and employee proposition.”

While firms acknowledge more needs to be done on at the level of the individual

institution, participants agreed that better cooperation among banks and an improved

two-way flow of information between banks and regulators is vital. Participants

highlighted the following possibilities for collaboration:

Pooling of resources. Participants cited institutions such as the Financial

Services Information Sharing and Analysis Center (FS-ISAC) as the standard

for collaboration, though some directors and executives complained that

information sharing is still not happening quickly enough. The reality is that

regulators’ and security services’ limited resources may be limiting their ability

to keep up and share information with the private sector in real time, and

there are a limited number of experts and heated competition for them.

Some participants suggested banks and the public sector could pool resources

to fund cybersecurity efforts where interests are aligned. One director argued,

“Because of the focus on financial services for things like anti–money

laundering, it means we are now on the front lines of the war on terror in

cyber. Cyberrisk is morphing with geopolitical risk.” One participant

commented, “The knowledge exists between Silicon Valley and professional

services to win this, but we don’t yet feel like we are in a war.”

Entering the security-privacy debate. One participant said the significant

cultural divide between Silicon Valley and the East Coast in the United States

hinders potential cooperation on cybersecurity. Essentially, there is

philosophical split, highlighted by the current encryption debate, with Silicon

Valley championing privacy and governmental agencies saying that defense

needs should supersede privacy needs.15 There was a general agreement that

the financial sector needs to use its resources to engage

with public opinion and restore balance to the debate.

“Cyberrisk is

morphing with

geopolitical risk.”

—Director

The perspectives presented in this document are the sole responsibility of Tapestry Networks and do not necessarily reflect the views of any

individual bank, its directors or executives, regulators or supervisors, or EY. Please consult your counselors for specific advice. EY refers to

the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal

entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. This material is prepared

and copyrighted by Tapestry Networks with all rights reserved. It may be reproduced and redistributed, but only in its entirety, including all

copyright and trademark legends. Tapestry Networks and the associated logos are trademarks of Tapestry Networks, Inc., and EY and the

associated logos are trademarks of EYGM Ltd.

Over the last several months, Tapestry and EY hosted two BGLN meetings on top and emerging risks

in banking and had over 30 conversations with directors, executives, regulators, supervisors, and other

thought leaders. Insights from these discussions informed this ViewPoints and quotes from these

discussions appear throughout.

The following individuals participated in BGLN discussions on top and emerging risks:

Kathy Casey, Non-Executive Director,

Audit Committee Member, Financial

System Vulnerabilities Committee Member,

HSBC

Juan Colombás, Chief Risk Officer, Lloyds

Sir Sandy Crombie, Non-Executive

Director, Performance and Remuneration

Committee Chair, Audit Committee

Member, Nomination Committee

Member, RBS Capital Resolution Board

Oversight Committee Member, RBS

Alan Dickinson, Non-Executive Director,

Risk Committee Chair, Audit Committee

Member, Lloyds

Laura Dottori-Attanasio, Chief Risk

Officer, CIBC

Dina Dublon, Non-Executive Director,

Risk Committee Chair, Deutsche Bank

Byron Grote, Non-Executive Director,

Audit Committee Member, Brand, Values

and Conduct Committee Member,

Standard Chartered

Mike Hawker, Governance and

Compliance Committee Chair, Audit

Committee Member, Nominating

Committee Member, Risk Committee

Member, Macquarie

Bob Herz, Non-Executive Director, Audit

Committee Chair, Nominating and

Governance Committee Member, Morgan

Stanley

Mark Hughes, Chief Risk Officer, RBC

Phil Lofts, Chief Risk Officer, UBS

Mike Loughlin, Chief Risk Officer, Wells

Fargo

Alan MacGibbon, Non-Executive Director,

Audit Committee Member, TD Bank

Heidi Miller, Risk Committee Member,

Conduct and Values Committee Member,

HSBC

Sir Callum McCarthy, Non-Executive

Director, Strategy Committee Vice Chair,

Risk Management Committee,

Nomination Committee, ICBC

Tom O’Neill, Audit and Conduct Review

Committee Member, Corporate

Governance Committee Member,

Executive and Risk Committee Member,

Human Resources Committee Member,

Scotiabank

Nathalie Rachou, Non-Executive Director,

Risk Committee Chair, Audit, Internal

Control and Risk Committee Member,

Société Générale

David Roberts, Chair, Risk Committee

Chair, Audit Committee Member,

Nomination Committee Member, IT

Strategy and Resilience Committee

Member, Nationwide

David Sidwell, Non-Executive Director,

Risk Committee Chair, Governance and

Nominating Committee Member, UBS

Alan Smith, Global Head, Risk Strategy,

HSBC

David Stephen, Chief Risk Officer, RBS

Kate Stevenson, Non-Executive Director,

Audit Committee Member, Corporate

Governance Committee Member, CIBC

Katie Taylor, Chair, RBC

Richard Thornburgh, Risk Committee

Chair, Audit Committee Chair, Chairman’s

and Governance Committee Member,

Credit Suisse

Alexander Wolfgring, Internal Controls &

Risks Committee Chair, Remuneration

Committee Member, UniCredit

Tony Wyand, Internal Controls and Risks

Committee Member, Remuneration

Committee Member, UniCredit

Ron Cathcart, Senior Vice President,

Enterprise Risk, Financial Institution

Supervision, Federal Reserve Bank of New

York

Lyndon Nelson, Executive Director, UK

Deposit-Takers Supervision, Bank of

England

Marty Pfinsgraff, Senior Deputy

Comptroller for Large Bank Supervision,

Office of the Comptroller of the Currency

Todd Vermilyea, Senior Associate Director,

Division of Banking Supervision and

Regulation, Federal Reserve System

Steve Weber, Center for Long-Term

Cybersecurity, UC Berkeley

Ian Baggs, Global Banking & Capital

Markets, Deputy Leader, Financial Services

Steve Holt, Head of Cybersecurity for

Financial Services

Ted Price, Advisor, Risk Governance

Isabelle Santenac, EMEIA FSO Assurance

Managing Partner

Bill Schlich, Global Banking and Capital

Markets Leader, Financial Services

Dennis Andrade, Principal

Jonathan Day, Vice Chairman

Colin Erhardt, Associate

Type of risk Concern/potential impact

Market risks

Changing interest rates

Changing interest rates could cause serious disruption in financial markets. Participants expressed concerns around the end of quantitative easing in the United States and the looming interest rate hike. Specifically, they questioned whether the authorities have the ability to

control the rate of the adjustment and cited the risk of a possible liquidity event.

Commodity prices Significant fluctuations in commodity prices could cause second-and third-order impacts on sovereign bonds, derivative corporate lending, and stress on housing markets in places dependent on oil revenue.

Deteriorating lending standards

Deteriorating lending standards creates increased credit risk as the industry enters a new stage in the credit cycle. Some participants noted a

significant deterioration in lending standards across asset classes. Specific concerns centered on the mortgage and auto lending markets, along with punishing levels of US student debt.

European instability

Continued uncertainty over European instability poses major challenges for companies. Anxiety is increasing with the ongoing ambiguity over

Greece’s economic situation. Meanwhile, the triumph of the

Conservative Party in the recent UK election means a UK exit from the European Union (EU) will be put to a referendum, creating new insecurity about the EU’s future.

Geopolitical concerns

A range of geopolitical risks may create additional volatility in financial markets. Participants noted the increasing isolation of Russia and the

crisis in the Ukraine, the rise of the Islamic State and war in Syria and Yemen, and political instability in South America as examples of risks they are monitoring.

Slowdown in China A slowdown in China may generate significant headwinds for the global economy.

Operational risks

Herd risk

Risk management practices may be threatened by potential herd risk, which leads to the acceptance of the current status quo and the lack of

necessary action to avert certain risks. A handful of directors mentioned the danger of everyone being trained not to be the outlier leading all organizations and individuals to do the same as others.

Information systems

Lack of confidence in insights coming from information systems could hinder effective risk management. Some directors questioned how to know whether the correct information is coming forward, especially

with the biases within institutions.

IT legacy systems

Many firms’ existing technology systems are not well suited to respond to the realities and needs of the 21st century impacting their ability to compete. Modernizing and upgrading these systems will require massive investments of time and resources.

Type of risk Concern/potential impact

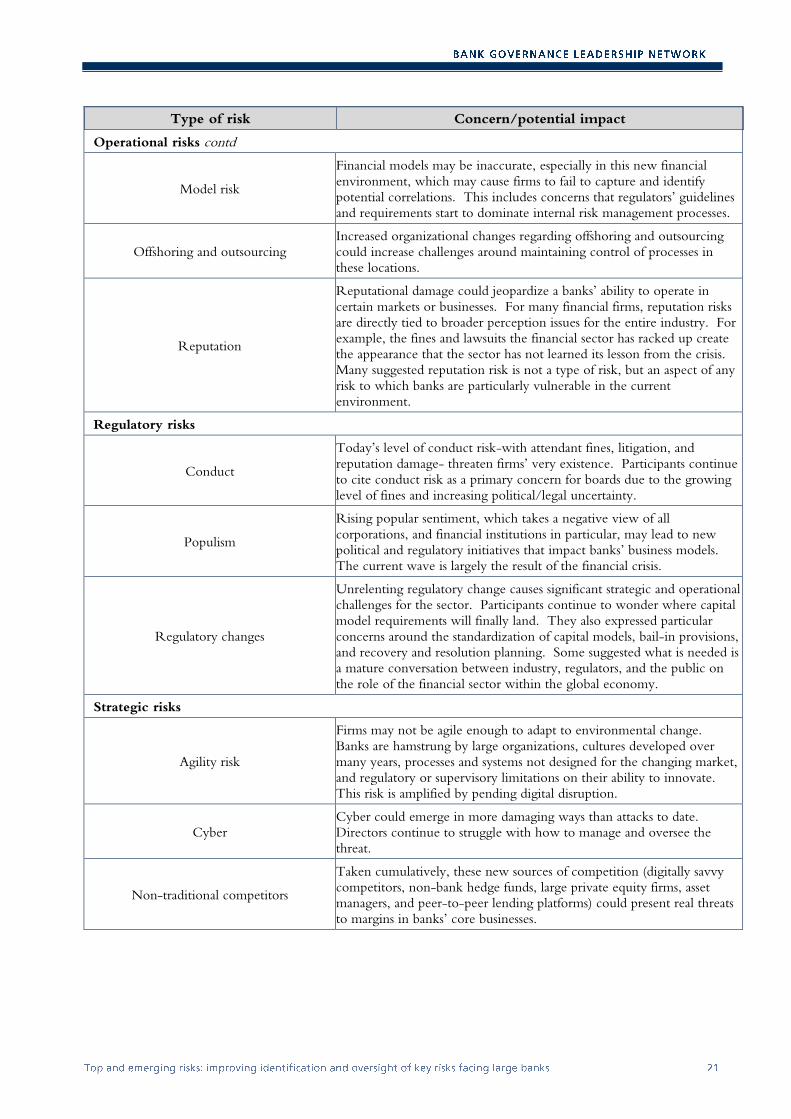

Operational risks contd

Model risk

Financial models may be inaccurate, especially in this new financial

environment, which may cause firms to fail to capture and identify potential correlations. This includes concerns that regulators’ guidelines and requirements start to dominate internal risk management processes.

Offshoring and outsourcing Increased organizational changes regarding offshoring and outsourcing could increase challenges around maintaining control of processes in these locations.

Reputation

Reputational damage could jeopardize a banks’ ability to operate in

certain markets or businesses. For many financial firms, reputation risks are directly tied to broader perception issues for the entire industry. For example, the fines and lawsuits the financial sector has racked up create the appearance that the sector has not learned its lesson from the crisis. Many suggested reputation risk is not a type of risk, but an aspect of any

risk to which banks are particularly vulnerable in the current environment.

Regulatory risks

Conduct

Today’s level of conduct risk-with attendant fines, litigation, and

reputation damage- threaten firms’ very existence. Participants continue to cite conduct risk as a primary concern for boards due to the growing

level of fines and increasing political/legal uncertainty.

Populism

Rising popular sentiment, which takes a negative view of all

corporations, and financial institutions in particular, may lead to new political and regulatory initiatives that impact banks’ business models. The current wave is largely the result of the financial crisis.

Regulatory changes

Unrelenting regulatory change causes significant strategic and operational challenges for the sector. Participants continue to wonder where capital

model requirements will finally land. They also expressed particular concerns around the standardization of capital models, bail-in provisions, and recovery and resolution planning. Some suggested what is needed is a mature conversation between industry, regulators, and the public on

the role of the financial sector within the global economy.

Strategic risks

Agility risk

Firms may not be agile enough to adapt to environmental change.

Banks are hamstrung by large organizations, cultures developed over many years, processes and systems not designed for the changing market,

and regulatory or supervisory limitations on their ability to innovate. This risk is amplified by pending digital disruption.

Cyber Cyber could emerge in more damaging ways than attacks to date. Directors continue to struggle with how to manage and oversee the

threat.

Non-traditional competitors

Taken cumulatively, these new sources of competition (digitally savvy competitors, non-bank hedge funds, large private equity firms, asset managers, and peer-to-peer lending platforms) could present real threats to margins in banks’ core businesses.

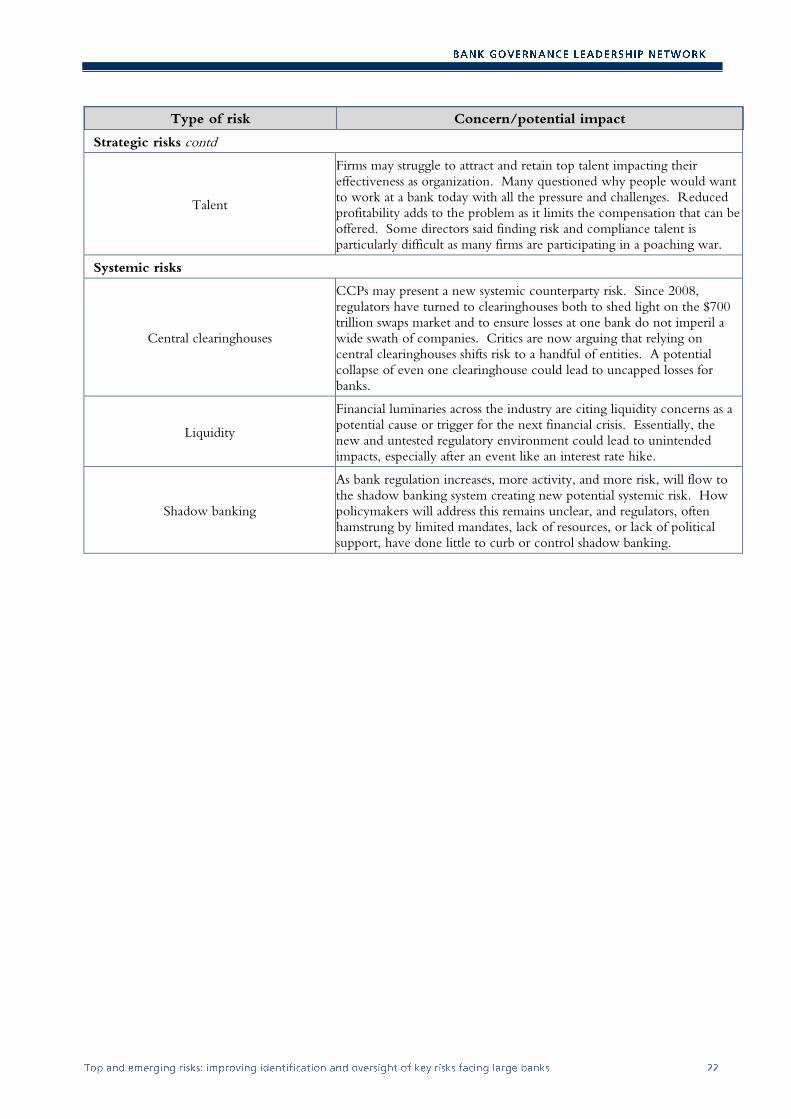

Type of risk Concern/potential impact

Strategic risks contd

Talent

Firms may struggle to attract and retain top talent impacting their

effectiveness as organization. Many questioned why people would want to work at a bank today with all the pressure and challenges. Reduced profitability adds to the problem as it limits the compensation that can be offered. Some directors said finding risk and compliance talent is particularly difficult as many firms are participating in a poaching war.

Systemic risks

Central clearinghouses

CCPs may present a new systemic counterparty risk. Since 2008,

regulators have turned to clearinghouses both to shed light on the $700 trillion swaps market and to ensure losses at one bank do not imperil a wide swath of companies. Critics are now arguing that relying on central clearinghouses shifts risk to a handful of entities. A potential collapse of even one clearinghouse could lead to uncapped losses for

banks.

Liquidity

Financial luminaries across the industry are citing liquidity concerns as a potential cause or trigger for the next financial crisis. Essentially, the new and untested regulatory environment could lead to unintended impacts, especially after an event like an interest rate hike.

Shadow banking

As bank regulation increases, more activity, and more risk, will flow to

the shadow banking system creating new potential systemic risk. How policymakers will address this remains unclear, and regulators, often hamstrung by limited mandates, lack of resources, or lack of political support, have done little to curb or control shadow banking.

1 ViewPoints reflects the network’s use of a modified version of the Chatham House Rule whereby comments are not attributed to individuals,

corporations, or institutions. Network participants’ comments appear in italics. 2 See Stephen A. Schwarzmann, “How the Next Financial Crisis Will Happen,” Wall Street Journal, June 9, 2015, and “Fed’s Tarullo,

BlackRock’s Fink Cite Bond Market Liquidity Concerns,” Today, June 5, 2015. 3 Stephen A. Schwarzmann, “How the Next Financial Crisis Will Happen.” 4 Bank Governance Leadership Network, Addressing Conduct and Cultural Issues in Banking, ViewPoints (Waltham, MA: Tapestry

Networks, 2015). 5 European Systemic Risk Board, Report on Misconduct Risk in the Banking Sector (Frankfurt am Main: European Systemic Risk Board,

2015), 3. 6 Bank Governance Leadership Network, Addressing Conduct and Cultural Issues in Banking. 7 Ben McLannahan, “Banks Post-Crisis Legal Costs Hit $300bn,” Financial Times, June 8, 2015. 8 Jill Treanor, “Banks’ £30bn in Compensation Claims and Fines 'Pose Risk to Stability,'” Guardian, July 1, 2015. 9 George Parker, Caroline Binham, and Laura Noonan,” George Osborne to Signal End to ‘Banker Bashing,’” Financial Times, June 5, 2015. 10 Steven Mufson and Jonelle Marte, “Five Big Banks Agree to Pay More Than $5 Billion to Settle Regulatory Charges,” Washington Post,

May 20, 2015. 11 Francisco Gonzalez, “Banks Need to Take on Amazon and Google or Die,” Financial Times, December 2, 2013. 12 Natalie Mortimer, “Lloyds Bank Digital Transformation Chief – ‘We Are in Danger of Just Becoming the Plumbing,’” Drum, June 17,

2015. 13 See Bank Governance Leadership Network, Leading the Digital Transformation of Banking, ViewPoints (Waltham, MA: Tapestry

Networks, 2014). 14 See Bank Governance Leadership Network, Addressing Cybersecurity as a Human Problem, ViewPoints (Waltham, MA: Tapestry

Networks, 2013). 15 J.D. Tuccille, “Hands Off Americans’ Private Information, Tech Industry Tells President,” Hit & Run (blog), June 10, 2015.