view/download the chartercapital advisory teamsa winning report

TRANSCRIPT

A BOARD REPORT ON THE KEY ISSUES FACING YJCIMA GBC2015

Team members:Tshegofatso Makhene (Team leader)Justice TshabalalaTshenolo RamawelaRaymond Miiro

CharterQuest Financial Training Institutea division of:

CharterCapital Advisory

CharterCapital Advisory: YJ Board Report

Table of Contents

PAGE

1. INTRODUCTION 2

2. TERMS OF REFERENCE 2

3. IDENTIFICATION AND PRIORITISATION OF ISSUES 2

4. EVALUATION OF THE MAIN ISSUES FACING YJ 4

5. ETHICAL CONSIDERATIONS 13

6. RECOMMENDATIONS 16

7. APPENDICES 20

1 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

1. Introduction The global E&P industry is particularly risky and capital intensive but with good return

prospects. It relies on a finite resource: fossil fuel, thus placing it as the focal point of

global consensus on sustainable development. A minor Health, Safety and Environmental

(HSE) incident can quickly translate into a disaster of catastrophic proportions costing

billions of USD for shareholders. For instance in 2010 the BP Deepwater horizon incident

cost them an estimated $42.2 billion and wiped off 55% of their market capitalisation.

Furthermore, the industry remains an attractive target for militant/terrorist groups seeking

to make demands on governments or the international community. Industry consensus

is that HSE, technical and financial capacities are the Critical Success Factors (CSFs).

Unless YJ's strategy continues to deliver a relatively superior track record in these CSFs

and broadens its current CSR stance to embrace sustainability development, it will see

its long-term prospects erode rapidly.

2. Terms of Reference This report identifies, prioritises and evaluates the issues facing YJ and offers appropriate

recommendations. It also includes a briefing paper as requested by Ullan Shah.

3. Identification and Prioritisation of Issues The issues below have been prioritised based on the impact each has combined with

the urgency. A full SWOT analysis is presented in Appendix 1.

License application results

Winning 3 of 4 licenses has had a significant impact on YJ’s market capitalisation, which

has increased by 31%. The licenses are to be accepted in 2 weeks and if YJ cannot, they

could experience a reversal of this 31% gain. This issue is therefore prioritised first.

2 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Outsourcer - DrilllT Awareness and superior track record in environmental issues is a critical success factor

for obtaining licenses in this industry. A vital safety check was compromised that may

have had serious consequences, the underlying cause being ongoing militant attacks. YJ

must deal with this issue to prevent any further escalation before considering long term

plans as below.

YJ’s long–term future Sustainability is a business challenge in this industry. YJ has at least seven years’ worth

of reserves and needs to evaluate its strategic position and address its going concern.

The impact of this is high but cannot be addressed unless current operations are secure.

This issue is therefore dealt with third.

Farm out offer The Farm Out proposal is dealt with last because even though it’s an opportunity for YJ

to raise funds for the more urgent test drilling, it’s not in line with the current strategy of

bringing fields into production.

Other issues Other issues are considered less significant and are not dealt with further whereas ethical

issues have been addressed in section 5.

Recommendations to issues are all in section 6.

3 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

4. Evaluation of the main issues facing YJ License application results

YJ needs to have the funds to test drill and for production. This is a critical success

factor in obtaining any licenses. In 2005, Gazprom was able to secure financing of

$12bn to fund expansion. Shareholders are currently happy due to the 31%

increase in market capitalisation ($35/share from $26.80/share). It is of utmost

importance that this increase be maintained and not let a reversal happen.

Johnson, Scholes and Whittington’s SAF model is used to appraise this opportunity.

Suitability

The 3 licenses will make the company grow two-fold if all three come into

production. This achievement is within the strategy of YJ which is not only to

explore new fields but to bring them into production as well.

Acceptability

Bringing the 3 oil fields into production will not only increase returns in the form of

dividends but will also improve the image of the company.

YJ’s strength is to produce in shallow waters - which the oil fields are. This

minimises the risk on production and makes it acceptable to key stakeholders

(Appendix 2). However, accepting all the licenses then raises shareholders

expectation in terms of the return (and dividends to be paid consistently).

Nevertheless, now would be a good time to start paying dividends to re-assure

shareholders of their investment.

4 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Feasibility

YJ needs to meet all expected costs ($63m) to test drill. 2015 cash forecast reveals

$69.84m (Appendix 4) after taking into account the suggested $10m dividend. This

can be used to cover the entire $63m. However, this cash balance is best left for

operations to finance working capital (Appendix 5.2). It is only the surplus cash

($56.44m) that can be used to partly finance the test drilling costs. This in effect,

would show strong cash control which would assist in obtaining debt finance for

production after the threshold as stipulated by the Bank of England has been

crossed. However, other costs such as security increase and managerial

improvement costs are to be taken into account as well.

Option 1: Debt

$31m can be raised from debt (Appendix 5.3) in accordance with the central bank’s

requirements.

Benefits

Cheaper form of finance in relation to equity; less risky for it is secured against

assets and interest is well known before any payments. Moreover, the interest is

tax-deductible and since YJ’s tax losses have now been used up, it will reduce the

total tax liability. Debt also reduces YJ’s Weighted Average Cost of Capital,

WACC1 as stated by the Modigliani & Miller theory with tax.

Drawbacks At a given level, WACC would increase due to the expectation of shareholders

being exposed to risk thus expecting a higher return (as stated by the traditional

view). YJ’s current debt results in gearing of 69.4% (Appendix 5.6) making it risky

which could possibly deter potential investors. If the $31m is raised, it would result

1 WACC, the rate (percentage) a company is expected to pay on average to all its security holders to finance its assets

5 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

in a gearing of 73.4% (140+31/[140+31+61.7]). The remaining amount of $32m

($63m-$31m) can be raised through cash (Appendix 5.5)

Option 2: Rights issue

A rights issue would raise $74,4m (Appendix 5.4) covering the test drilling.

However, it’s the most expensive form of finance (pecking order theory).

Drawbacks: The calculations on the rights issue are views of the market but could easily not be

the views of YJ’s shareholders.

Benefits Apart from the shares issued during the IPO, no other shares have been issued

thereafter. New share issues would be in high demand. The increase in market

capitalisation influences this demand as well. A rights issue would also reduce the

current gearing which would be far more favourable. However, YJ also needs to

raise finance for production and given the benefits, a rights issue would be more

in line given that reserves would have been found and proven. An alternative would

be to take YJ from AIM to main board listing to raise even more finance.

Addressing the managerial capacity

Training and Development

Develop managers from within. Supervisors can be sent for training and

development and a succession plan put in place to replace any manager who may

leave in the future. However, there are 7 months before test drilling commences

and training a sufficient number of people may be a challenge.

Headhunting

Headhunt the required management staff. Given the focused approach of

headhunting, the packages are usually offered at above competitive rates in order

6 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

to attract desired individuals away from their current occupation. This will be a

challenge given the current financial constraints.

Outsourcing

A last resort would be to outsource the requisite managerial capacity. However,

exploring this option alludes to YJ outsourcing one of its core competencies;

managers who are of major importance to YJ’s operations.

7 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Outsourcer - DrilllT

Impact of the considerable unrest

Attacks by militant groups in the Niger River Delta cut Nigeria’s oil production by

more than 28% from 2006 to 2009. YJ has to manage political risk in order to

prevent it from experiencing a similar incident as Chevron in 2003 at AAA. It could

escalate and result in militants taking over AAA automatically impacting YJ’s

revenue (AAA contributed 40% of 2014 revenue), causing a significant fall in the

share price and impacting the acquisition of further finance.

Impact of the control failures

A vital safety check concerning the flow of oil was compromised and even though

nothing major happened, a minor accident could be catastrophic. Gas leakage

could cause an explosion and the loss of assets. Severe injuries and death would

negatively impact SHE, one of YJ’s critical success factors pertaining to obtaining

future licences. This all could bring YJ’s entire operation to a close.

The following options seek to address this threat. (All ethical issues have been

dealt with in Section 5)

Addressing security concerns

A security risk management strategy for the entire AAA operation using the “Four

Ts” of the risk management process is to be immediately implemented:

Transfer

The risk of asset-loss can be transferred to an insurance company. However,

ongoing militant attacks could make it difficult for YJ to receive insurance cover.

Should insurance companies accept greater risk, it may result in higher premiums.

8 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Tolerate

Continuously monitor the situation but should militants attack, emergency safety

procedures should be implemented. YJ would accept all consequences arising

from such an incident.

Treat

YJ could re-deploy security from each of the other fields to assist with the

safeguarding of assets and transporting of all employees to and from AAA. This

would fortify the security already at AAA without increasing the costs significantly.

The government would be enlisted to assist, since they have a vested interest in

the oil and gas fields.

Terminate

This would see YJ shut down AAA and exit the country. Termination of the field

will however, strain the financial capacity that YJ already lacks.

9 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

YJ’s Long – Term Future

Fossil fuels are finite which affects the longevity of companies in this industry.

Sustainability remains a business challenge and whilst YJ may discover more

reserves in the new fields, the issue will remain.

Three key criteria are identified in the option to exit, and the 9Ms model applied in

the option to broaden energy sources. A briefing paper was prepared (Appendix

6) to assist in making this decision. Both options would be evolutionary in terms of

Hopely and Balogun’s Type of Change Model, and would constitute a change in

YJ's strategic direction.

10 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Farm out Offer

Issue

An opportunity has been offered to farm-out GGG by Liquid Gold (LG). The option

payment will partly help YJ financially in financing the test drilling. YJ has never

had a farm out before making it lack the experience to handle one.

This will be evaluated using ‘modified’ Enterprise Risk Management framework.

Strategic YJ has successfully brought its current three fields into production without having

to farm-out. This is a key strength (Appendix 1). Accepting the farm out will result

in a different view by the market; what was once a strength is no more.

Financial & Risk

As calculated in Appendix 4.4, YJ’s 2015 cash flow would improve by $2m. This is

a very negligible difference unlike if the $10m was to be available at once after

signing the agreement. Penalties of $1m if drilling is not completed within the

deadline are attached. YJ would be making such payments monthly till an

unforeseeable time which is highly risky for a company that already lacks cash.

The offer is also short by $8m to meet GGG cost ($18m- $10m=$8m). If the field

does prove to hold more oil than is predicted, then it will surely be valued higher

leading to more bids by different companies. Accepting the farm out would give

rise to the risk of loss of future profits. On the other hand, GGG could prove to not

have oil resulting in the total cost ($18m) of the test drilling being written off. The

$10million farm out offer in this case would then help in reducing this loss down to

$8million. However, such losses should be anticipated for they are a business risk

for companies in such an industry.

11 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Operational

The farm out can improve the managerial problem faced by YJ. As GGG would not

come into production, the current constraint would be relaxed, giving YJ leeway to

focus on the other two fields.

Compliance

The government would need to approve the farm out which can lead to different

terms altogether such as those of a share agreement of profits to be given to the

government. Not much can be said about LG for little is known about it.

Review of deal terms and suggestions to amend:

• The $10m should be made in cash as a whole amount for YJ to consider

and for it to contribute to the costs of test drilling.

• LG having place on the board should be reviewed. Debriefing of all

information relating to GGG would be a better option through a status report

with meetings to clear any misunderstandings. LG being given a place on

the board is a risky step as it could lead to information leak and LG out-

playing YJ.

• The $1m fine imposed if time given to test drill does run out before the task

is completed is a high amount to pay which enables LG recover its given

amount and more within a period of 12months. The penalty should be

restructured in a more reasonable manner say: pay = work unfinished as a

% of the $10m that was given or a lower fixed amount.

12 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

5. Ethical considerations 5.1 Fraud Committed by DrilllT Underlying ethical issue

The Forgery puts into question DrilllT’s Integrity. DrilllT has a duty to act with due

care and transparency in carrying out its work. However, DrilllT acted unethically

in forging Mr. Brown’s signature and concealing it. Instead a replacement engineer

was found and YJ was given an apology but no formal disciplinary plan was

communicated. DrilllT put profit ahead of employees’ HSE by protecting those

involved in the forgery.

Lee Wang wants to conceal the irregularities. This shows a lack of honesty and

objectivity. His suggestion if carried out, would have serious repercussions on the

company should the government discover safety measures were compromised

and YJ concealed this. Lee Wang upheld his duty of care by suggesting that

“everything be done to ensure things are now safe” and he should be credited for

this. His contradicting actions show an attempt at avoiding consequences and thus

puts his level of ethical maturity at the pre-conventional level of Kohlberg’s stages

of moral development.

Advice

DrilllT’s management should compile a written report fully disclosing the incident to

the government officials within the week and signed off by Jason Oldman. Lee

Wang should be removed from the process completely. Should the government

impose any penalties, DrilllT should be held liable depending on the terms of

DrilllT’s contract with YJ.

YJ should instruct DrilllT to take disciplinary action (e.g. Dismissal) against the

perpetrators involved in the fraud. This is to restore YJ’s confidence in DrilllT.

Should DrilllT not take these measures, Jason Oldman is to initiate contract

termination procedures.

13 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Lee Wang should be reprimanded for proposing this unethical act. A mentor should

be assigned to help him progress to post-conventional level of ethical maturity as

he lacks practical understanding and application of ethical principles.

5.2 Ullan Shah Statement during Greenbies Protest

Underlying ethical issue

Ullan Shah’s statement and outburst during the Greenbies protest shows that he

does not care about the development of sustainable energy sources and does not

consider the wellbeing of future generations. He lacks due care and professional

behaviour. His ignorance shows inappropriate leadership which points to lack of

Professional Competence. On the other hand, his actions of being angry that he

couldn’t park his BMW 650i on its usual parking spot highlights that he is egoistic

and has self-interest only.

Advice

Given the relatively new integration of sustainability into the corporate space, Ullan

Shah may not fully understand and recognise the resulting responsibilities. He

must first offer a full apology for his actions/outburst. It is then advised that an

assessment be done on his competence in this area by external sustainability

experts. Should the assessment reveal he has been adequately trained, Jeremy

Lion is to initiate a disciplinary process resulting in a written warning stating that

Ullan needs to lead by example and be cognisant of his duty to future generations.

Should the assessment reveal that he has not received adequate training, the

experts are to draw up a comprehensive sustainability plan which he should

internalise.

14 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

5.3 Facilitation payments

Underlying ethical issue

It is rumoured that the HHH license was awarded to another E&P company that

‘bribed’ government officials. The underlying ethical issue is the unfair competitive

advantage gained by the bidders.

Advice

The YJ board and all employees throughout YJ should understand the unethical

conduct of bribery. Jason Oldman should draft an anti-corruption policy that is

strongly against bribery in all its forms.

YJ should seek legal advice and report any suspicion of corruption to relevant

regulatory bodies in order for investigations to be conducted.

15 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

6. Recommendations 6.1 License application results

Recommendation

Finance the test drilling with $32m cash and $31m debt.

To address the managerial capacity, Training and Development should be undertaken

in combination with head hunting.

Justification

This is in line with the pecking order theory but also then lets YJ use the rights issue to

finance production. $29m cash ($5m overdraft facility included) can then be used for

working capital requirements as well as fund the other issues.

Training and Development will be a cost effective way of addressing the managerial

issue in light of current financial constraints and as the employees already know the job

and industry, will save time and offer more motivation. Capacity not addressed by

promotion, head hunting will suffice.

Actions

• Jason Oldman should draft the acceptance letters of all licenses to the

governments.

• Once Orit Mynde returns to work, he should immediately begin the process of

issuing new bonds or negotiate directly with the bank to raise finance from debt.

• Orit Mynde should take steps to ensure a strong cash control regime is

maintained so that the projected cash flows are realised.

• Orit Mynde should also begin the process of taking YJ from AIM to full mainboard

listing in time for production.

• The HR manager should be instructed to put in motion a managerial internal

succession plan that will facilitate Training and Development. Further, a

16 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

headhunting strategy to address the shortfall is to be implemented within the next

3 months. Funds are also to be set aside for this process by Orit Mynde.

6.2 Outsourcer - DrilllT Recommendation Re-deploy more security personnel to AAA from the Asian fields and continuously monitor

the militant threat, assessing its escalation. If this is not adequate, the security company

should provide more personnel and the government petitioned to improve security

controls.

Justification This ensures that the entire AAA operation is safe and allays the fears of employees,

improving retention. Government has a vested interest, thus petitioning them for

protection would be justified. The Asian fields under no militant threat would still have

adequate security.

Action

• Lee Wang should arrange to re-deploy security from the other Asian fields to AAA

within the month. The security personnel should be armed and on high alert. Orit

Mynde in consultation with Lee Wang should estimate how much from the $24m

(excluding $5m overdraft facility) to set aside to cater for any extra costs.

• Jason Oldman should immediately draft a petition letter to the government

requesting assistance with security.

17 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

6.3 YJ’s long term future Recommendation Begin implementing the steps necessary to diversify energy sources. A number of large

energy companies such as Exxon Mobile and Chevron have taken similar steps with great

results.

Justification Exiting the whole industry would unsettle investors and cause share price to drop

significantly. By diversifying, YJ would retain the technical capability it has already built

and even raise finance from more ethical investors.

Action

• The Board should set up a high level Sustainability Committee to oversee the

transformation within the next month.

• The committee should commission a detailed study for each resource area in the

briefing paper, by appointing external consultants. They should report back within

3 months with detailed actions/project plans.

• The above action plans should be compiled into Sustainability/Change

Management Plan document and secure board approval.

• The committee should then appoint a change agent and begin implementing the

plan. Special care should be taken to communicate the rollout widely, to help

reposition the company’s image in relation to the Greenbies Party protest.

• The HR Manager should develop and implement a plan to ensure all employees

are educated on sustainability and are aware of the coming changes (Kotter and

Schlesinger).

18 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

6.4 Farm out Offer

Recommendation

YJ should not accept the farm out offer.

Justification

The impact the farm out has on the cash flow is minor. If it’s accepted, YJ’s strength of

bringing oil fields into production is no more. Waiting could lead to better offers being

made if the fields do hold oil.

Actions:

• Jason Oldman should draft a decline of the offer and send to LG but with

indications that a future option can be reviewed.

19 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

7. Appendices

Appendix 1: SWOT Analysis SWOT

1. Strengths

• No accidents

• Technical capability

• Relationship with DrillT

• Ability to find oil reserves, test drill and bring fields to production

2. Weaknesses

• Lack of financial and managerial capacity to test drill

• Lack of financial and managerial capacity to go into production

3. Opportunities

• Three licenses obtained and eight survey and explorations

• Farm out offer from LG

• Alternative energy sources

• Increasing rate at which licenses can be obtained for test drilling

4. Threats

• Bank regulator may not allow YJ to loan money

• Protest action, bad publicity for industry – could affect sustainability of business once alternatives are present in market, and could cause governments to enforce legislature more or change legislature unfavourably for industry.

• Militant action currently affecting staff retention – may escalate

• Government check subsequent to DrillT incident may lead to action from

government

Items in bold are the key issues

20 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Appendix 2: Mendelow Analysis Stakeholders

1. Mendelow’s Power Interest Matrix

INTEREST

Low High

POW

ER

Low

Minimal Action

2.5 DrillT Employees

3.2 Community

3.4 News Agencies

4. Future generations

Keep Informed

1.2 YJ Supervisors

3.1 Greenbies

3.3 LG

Hig

h

Keep Satisfied

2.3 African Government

2.4 Lenders of finance

2.6 DrillT

3.5 Bank Regulator

3.6 License Issuing

Governments

Keep Players Involved in Everything

1.1 YJ Board of Directors

2.1 Shareholders

21 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Appendix 3: PEST Analysis Political

• YJ being awarded three licenses means it was awarded by three governments from

three different countries and it needs to understand different environments of these

different countries.

• Militant attacks in the African country were AAA field is located exposes YJ to

political risk.

• Government spot checks mean that there are different safety policies in place for

different countries that YJ has licenses in.

• If Governments from some countries are willing to accept bribes from license bidders

hinders YJ’s possibility of attaining new licenses.

Economical

• Shareholders/investors that invested in E&P companies are requesting to buy

shares on a 15% discount.

• Share price rose to a record high of $35 due to attaining three new licenses.

• Banks are finding it risky to loan E&P companies funds.

Social

• Risk is posed by public protests by environmental groups that E&P companies

should consider developing sustainable resources.

• Drill T employees fearing to come to work due to the fear of being attacked by

militants affects YJ’s business.

• The challenge that YJ has been facing for a while now of the threat of terrorist

attacks.

22 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Technological

• Lack of capabilities to develop sustainable sources of energy

• YJ lacking drilling capabilities by outsourcing companies to drill for them poses as a

weakness.

• At the moment YJ strategy is not based on exploring ways of becoming a renewable

energy company which poses a threat because may need to do so in the future.

23 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

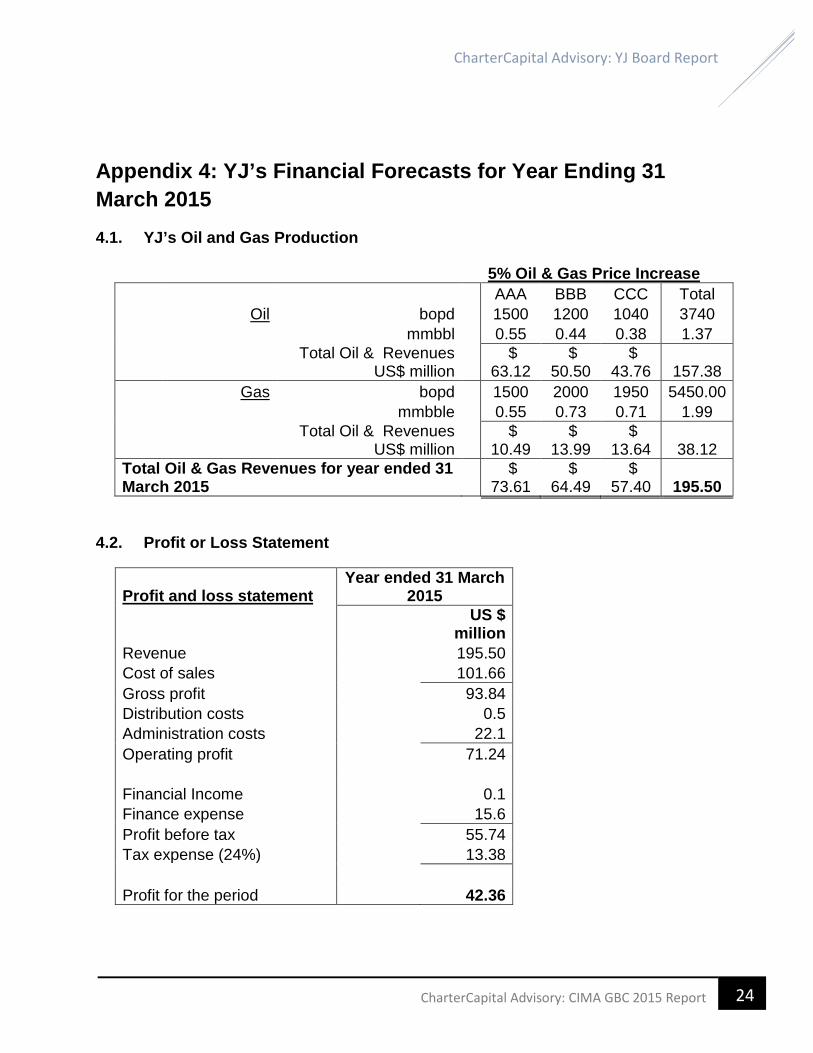

Appendix 4: YJ’s Financial Forecasts for Year Ending 31 March 2015 4.1. YJ’s Oil and Gas Production

5% Oil & Gas Price Increase AAA BBB CCC Total Oil bopd 1500 1200 1040 3740 mmbbl 0.55 0.44 0.38 1.37

Total Oil & Revenues

US$ million $

63.12 $

50.50 $

43.76 157.38 Gas bopd 1500 2000 1950 5450.00 mmbble 0.55 0.73 0.71 1.99

Total Oil & Revenues

US$ million $

10.49 $

13.99 $

13.64 38.12 Total Oil & Gas Revenues for year ended 31 March 2015

$ 73.61

$ 64.49

$ 57.40 195.50

4.2. Profit or Loss Statement

Profit and loss statement Year ended 31 March

2015

US $

million Revenue 195.50 Cost of sales 101.66 Gross profit 93.84 Distribution costs 0.5 Administration costs 22.1 Operating profit 71.24 Financial Income 0.1 Finance expense 15.6 Profit before tax 55.74 Tax expense (24%) 13.38 Profit for the period 42.36

24 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

4.3. Statement of Cash Flows

Year ended 31

March 2015

Cash from operating activities US$

million US$

million Profit before taxation 55.74 Adjustments:

Depreciation 28 Financial Cost 15.5 43.5 Decrease in Inventory 10 Increase in Receivables -2 Increase in Deferred tax Increase in Trade payables 5

13 Financial cost (net paid) -15.5 Tax paid -0.5

-16 Cash generated from operating activities: 96.24 Cash flow from investing activities:

Maintenance of non-current assets -30 -30 Cash flow from financial activities :

Dividend paid -10 -10 Net increase in cash and cash equivalents 56.24 Cash and cash equivalent at 31 March 2014 13.6 Cash and cash equivalent at 31 March 2015 69.84

25 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

4.4. Cash Flow With Farm Out Offer and Test Drilling

Cash generated from operating activities: 96.24 farm out 2 non-current assets -30 tests drills -63 Cash flow from financial activities : dividend paid -10 Cash and cash equivalent at 31 March 2014 13.6 Net decrease in cash and cash equivalent 8.84

4.5. Cash Flow Without Farm Out Offer and Test Drilling

Cash generated from operating activities: 96.24 non-current assets -30 tests drills -63 Cash flow from financial activities : dividend paid -10 Cash and cash equivalent at 31 March 2014 13.6 Net decrease in cash and cash equivalent 6.84

26 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Appendix 5: Financial Requirements, Options and Indicators 5.1. Test Drilling Costs

US$m EEE 20 FFF 25 GGG 18 Total test drilling cost 63

5.2. Working Capital – Cash Available

US$m Cash and Cash equivalent at 31 March 2015 69.84 Receivables (6,5 + 2) 8.5 Inventory (25 - 10) 15 less Payables (31,9 + 5) (36.9) Cash available 56.44

5.3. Debt Assessment

US$m Existing loan (140) Operating profit 57.00 Total lending 3 x Operating Profits 171.00 Total that can be obtained from the bank 31.00

5.4. Rights Issue Assessment

Rights Issue discount 15% Market price of shares US$ 35 Discounted offer per share 29.75 Number of shares to be offered (million) 2.5 Total that can be obtained from rights issue US$m 74.38

27 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

5.5. Hybrid Assessment

US$m Total drilling cost 63.00 Finance from debt (31.00) Finance to be obtained from cash available US$m 32.00

5.6. Gearing

Gearing = Debt 140 69.41% Current Gearing Equity + Debt 201.7 Gearing = Debt 171 73.49% Gearing with loan Equity + Debt + Bank Loan 232.7 Gearing = Debt 140 50.71% Gearing with rights issue

Equity + Debt + Rights Issue

276.08

28 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Appendix 6: Briefing Paper on YJ’s Long Term Future Briefing Paper

From: CharterCapital Advisory

To: Ullan Shah, CEO of YJ Oil and Gas

Date: 1 August 2014

Purpose

This briefing paper discusses the main matters to be considered in deciding on the long

term future of YJ in terms of a choice between A) exiting the E&P market or B) diversifying

its energy sources.

A) Exit the E&P Market

1. This would mean a bigger change for YJ than the choice to stay within the energy

market and diversify YJ's energy sources.

2. The viability of this option is looked at under 3 key criteria:

• The market into which it enters, if this is another sector dependent on a finite

resource such as gold or iron, YJ's long-term sustainability would remain in

question.

• The amount that YJ would have to change its strategic capability/core

competences, to fit with the new business model

• The attractiveness of the opportunities it can identify in such market (position

based strategy) as well as the entry barriers.

3. No decision has been made into which market YJ will exit into, or whether it would

go into liquidation so no further assessment is provided.

29 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

B) Diversify YJ's sources of energy to include renewable sources

1. This will be transformative but arguably less so than the exit option.

2. The core competencies required to produce energy from renewable sources are as

varied as the different forms of renewable energy however a preliminary

resource/feasibility audit guided by the modified 9 M’s model is provided as a

starting point:

• Materials: Some renewable energy sources e.g. wind and solar depend on the

availability of certain climate/weather patterns and geographical distribution

and location. It is reported that the production of some renewable sources of

energy requires much larger areas of land to produce the same energy

compared to fossil fuels. YJ needs to consider the resulting cost and scale

implications.

• Methods: The manner in which extracted energy is stored and transported

will be a key strategic point, as current fossil fuel extraction is outsourced.

• Manpower: The technical skill set will have to change from the current survey

and geologist capability YJ has relied upon, depending on the type of energy

resource chosen.

• Management: The lacking managerial capacity will not only have to be

expanded to address the requisite changes, but have the expertise and drive

necessary to carry out such a transformative though evolutionary change.

• Machines: The existing equipment & infrastructure’s suitability to the future

function requirements will have to be assessed and training be provided for the

operation of new machinery.

• Management Information: The role of science and technology in the

production methods and means of collecting data and producing and

30 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

distributing reports to guide decision making may alter significantly. The

systems to track and report on YJ's performance in accordance with the best

integrated reporting practices including setting up KPI's such as % of energy

from renewable sources would be key information instruments required.

• Make-up: YJ may have to change from a single product-geographical

(divisional strategy) to a multiproduct or matrix product-geographical structure

centered on the different extraction, conversion, storage and transport

processes. It may have to operate vastly different value chains within the same

entity. It would need to reconsider its product portfolio (BCG). Oil and gas as a

whole are likely to be classified as cash cows whereas wind energy could

become the star and nuclear possibly the dog. The new CSFs need to be

considered and should be part of the factors informing the new structure.

• Markets: YJ needs to spend resources to broaden its understanding of the

energy market including renewable energy sources, the key role players,

competitors, buyers, suppliers and how prices are set (Porters 5 forces and

Porters Generic Strategies). It currently sells to one type of buyer that is oil

refining companies, but going forward it may have to understand different types

of buyers, such as industrial buyers for construction companies associated with

solar energy products and agriculture companies for wind energy. YJ would

need to consider how it would capitalise on the new brand/reputation for going

green &sustainable. The Greenbies party protest would now offer a good

chance for YJ to break ahead of its rivals by creating what Michael Porter called

sustainable competitive advantage. It would also have to reconsider its overall

strategic missions, vision and objectives.

• Money: Some forms of renewable energy are more capital intensive than fossil

fuel. YJ needs to improve its ability to broaden and attract more long-term

investors who care about sustainability. The operating costs vs. selling prices

also need to be considered along with their impacts on YJ’s balance sheet.

31 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

• Time: YJ needs to consider how much time they have before the existing fossil

fuel reserves become obsolete and align this to plans that need to be

implemented in order to continue operations. YJ’s current oil fields in production

have 7 years worth of oil reserves. This is a relatively small time-frame in the

oil and gas industry and considering the scale of the transformation required.

Alternatives Venturing into other activities, such as midstream would allow YJ to explore other revenue

streams in even less capital intensive investments. A similar strategy was employed by

Statoil from 2008 which saw their business grow by positioning themselves to deal with

the uncertainty of a severe economic downturn. They attacked new realities with a strong

balance sheet, a robust project portfolio and excellent people. YJ would therefore have a

reduction of systematic risk through holding different portfolios as it becomes sustainable.

32 CharterCapital Advisory: CIMA GBC 2015 Report

CharterCapital Advisory: YJ Board Report

Appendix 8: Bibliography 1. Chartered Institute of Management Accounts. Fundamentals of Ethics, Corporate

Governance and Business Law, 2014. Berkshire, Kaplan Publishers.

2. Chartered Institute of Management Accounts. T4-Part B – Case Study, March 2014.

3. Chartered Institute of Management Accounts. T4-Part B – Case Study, May 2014.

33 CharterCapital Advisory: CIMA GBC 2015 Report