vicentiu covrig 1 options and futures options and futures (chapter 18 and 19 hirschey and nofsinger)

Post on 21-Dec-2015

216 views

TRANSCRIPT

Vicentiu Covrig

11

Options and FuturesOptions and Futures(Chapter 18 and 19 Hirschey and Nofsinger)(Chapter 18 and 19 Hirschey and Nofsinger)

Vicentiu Covrig

22

Potential Benefits of DerivativesPotential Benefits of Derivatives

Derivative instruments: Value is determined by, or derived from, the value of another instrument vehicle, called the underlying asset or security

Risk shifting- Especially shifting the risk of asset price changes or interest rate changes to

another party willing to bear that risk Price formation

- Speculation opportunities when some investors may feel assets are mis-priced Investment cost reduction

- To hedge portfolio risks more efficiently and less costly than would otherwise be possible

Vicentiu Covrig

33

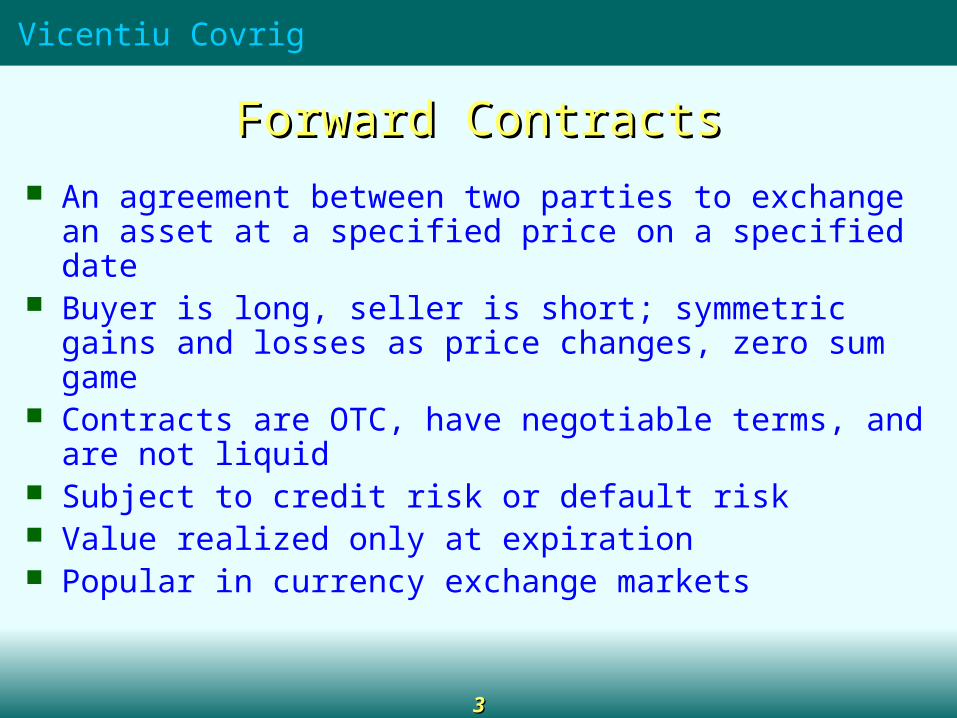

Forward ContractsForward Contracts An agreement between two parties to exchange an asset at a

specified price on a specified date Buyer is long, seller is short; symmetric gains and losses as price

changes, zero sum game Contracts are OTC, have negotiable terms, and are not liquid Subject to credit risk or default risk Value realized only at expiration Popular in currency exchange markets

Vicentiu Covrig

44

Futures ContractsFutures Contracts Like forward contracts…

- Buyer is long and is obligated to buy- Seller is short and is obligated to sell

Unlike forward contracts…- Traded on an exchange- Standardized – size, maturity- More liquidity - can “reverse” a position and offset the future

obligation, other party is the exchange- Less credit risk - initial margin required - Additional margin needs are determined through a daily

“marking to market” based on price changes

Vicentiu Covrig

55

Futures ContractsFutures Contracts

Futures Quotations- One contract is for a fixed amount of the underlying

asset5,000 bushels of corn (of a certain grade)$250 x Index for S&P 500 Index Futures (of a

certain maturity)- Prices are given in terms of the underlying asset

Cents per bushel (grains)Value of the index

- Value of one contract is price x contract amount

Vicentiu Covrig

66

Futures ContractsFutures Contracts

Example: Suppose you bought (go long) the most recent (June) S&P 500 contract at the settle price of 1180.80.

What was the original contract value?Value = $250 x 1180.80 = $295,200 What is your profit if you close your position (sell a

contract) for 1250.00?Value = $250 x 1250.00 = $312,500Profit = $312,500 - $295,200 = $17,300

Vicentiu Covrig

77

OptionsOptions Option to buy is a call option

Call options gives the holder the right, but not the obligation, to buy a given quantity of some asset at some time in the future, at prices agreed upon today.

Option to sell is a put optionPut options gives the holder the right, but not the obligation, to sell a given quantity of some asset at some time in the future, at prices agreed upon today

Option premium – price paid for the option Exercise price or strike price – the price at which the asset can be bought or sold

under the contract Open interest: number of outstanding options Expiration date

- European: can be exercised only at expiration

- American: exercised any time before expiration

Vicentiu Covrig

88

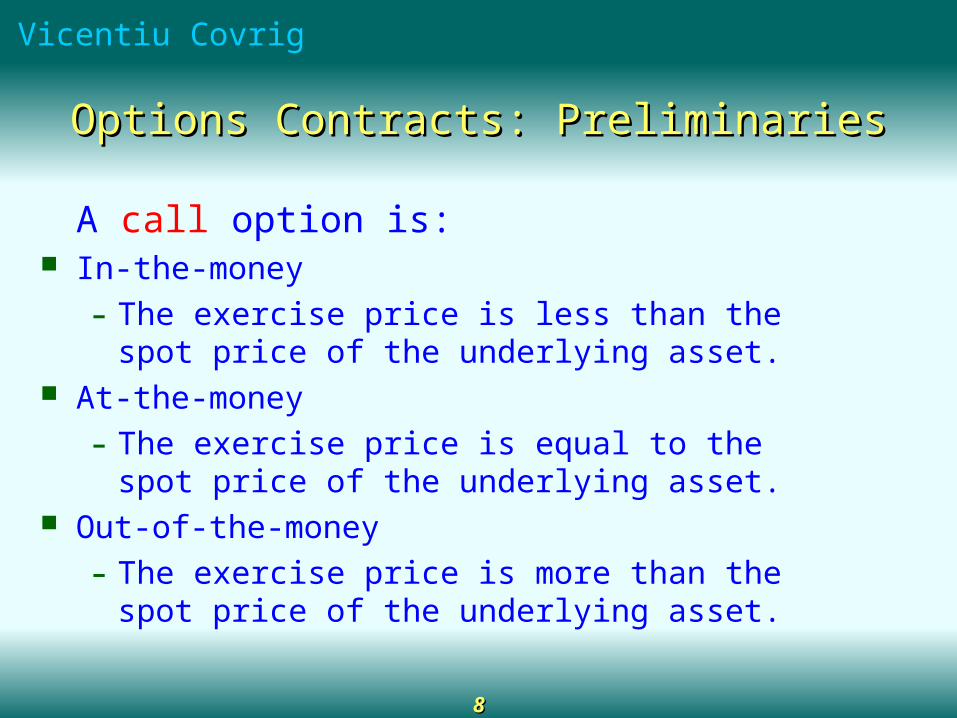

Options Contracts: PreliminariesOptions Contracts: Preliminaries

A call option is: In-the-money

- The exercise price is less than the spot price of the underlying asset.

At-the-money

- The exercise price is equal to the spot price of the underlying asset.

Out-of-the-money

- The exercise price is more than the spot price of the underlying asset.

Vicentiu Covrig

99

Options Contracts: PreliminariesOptions Contracts: Preliminaries

A put option is: In-the-money

- The exercise price is greater than the spot price of the underlying asset.

At-the-money

- The exercise price is equal to the spot price of the underlying asset.

Out-of-the-money

- The exercise price is less than the spot price of the underlying asset.

Vicentiu Covrig

1010

OptionsOptions

Example: Suppose you own a call option with an exercise (strike) price of $30.

If the stock price is $40 (in-the-money):- Your option has an intrinsic value of $10 - You have the right to buy at $30, and you can exercise and then sell

for $40. If the stock price is $20 (out-of-the-money):

- Your option has no intrinsic value- You would not exercise your right to buy something for $30 that you

can buy for $20!

Vicentiu Covrig

1111

OptionsOptions

Example: Suppose you own a put option with an exercise (strike) price of $30.

If the stock price is $20 (in-the-money):- Your option has an intrinsic value of $10 - You have the right to sell at $30, so you can buy the stock at

$20 and then exercise and sell for $30 If the stock price is $40 (out-of-the-money):

- Your option has no intrinsic value- You would not exercise your right to sell something for $30

that you can sell for $40!

Vicentiu Covrig

1212

OptionsOptions

Stock Option Quotations- One contract is for 100 shares of stock- Quotations give:

Underlying stock and its current priceStrike priceMonth of expirationPremiums per share for puts and callsVolume of contracts

Premiums are often small- A small investment can be “leveraged” into high profits

(or losses)

Vicentiu Covrig

1313

OptionsOptionsExample: Suppose that you buy a January $60 call option on Hansen at a

price (premium) of $9.Cost of your contract = $9 x 100 = $900If the current stock price is $63.20, the intrinsic value is $3.20 per share. What is your dollar profit (loss) if, at expiration, Hansen is selling for

$50?

Out-of-the-money, so Profit = ($900) What is your percentage profit with options?

Return = (0-9)/9 = -100% What if you had invested in the stock?

Return = (50-63.20)/63.20 = (20.89%)

Vicentiu Covrig

1414

OptionsOptionsWhat is your dollar profit (loss) if, at expiration, Hansen is selling for $85?

Profit = 100(85-60) – 900 = $1,600 Is your percentage profit with options?

Return = (85-60-9)/9 = 77.78% What if you had invested in the stock?

Return = (85-63.20)/63.20 = 34.49%

Vicentiu Covrig

1515

OptionsOptions Payoff diagrams

- Show payoffs at expiration for different stock prices (V) for a particular option contract with a strike price of X

- For calls:if the V<X, the payoff is zeroIf V>X, the payoff is V-XPayoff = Max [0, V-X]

- For puts:if the V>X, the payoff is zeroIf V<X, the payoff is X-VPayoff = Max [0, X-V]

Vicentiu Covrig

1616

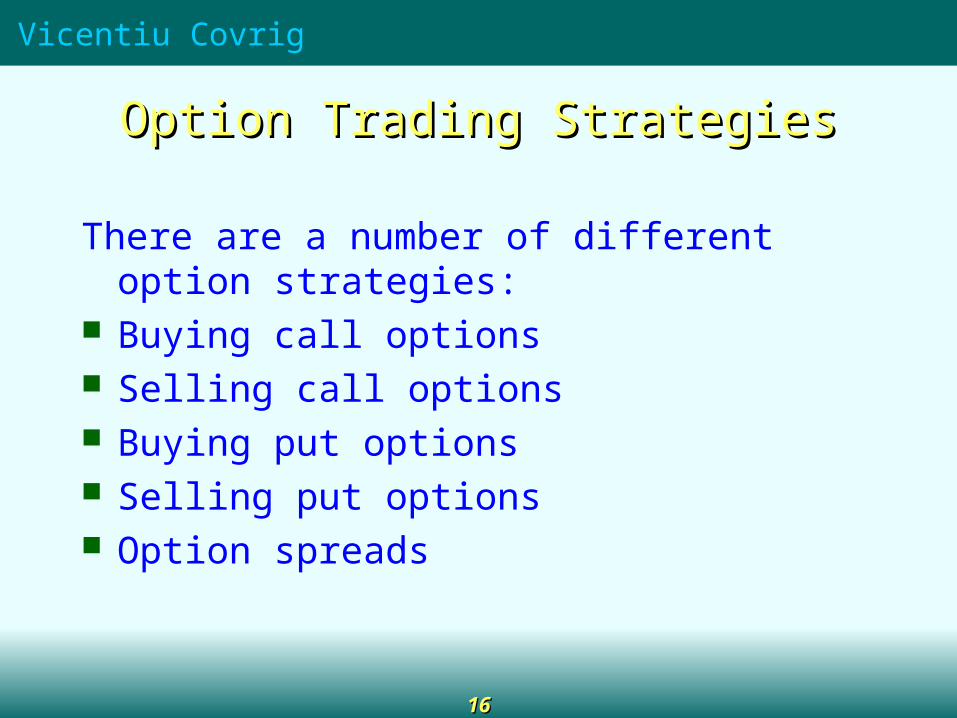

Option Trading StrategiesOption Trading Strategies

There are a number of different option strategies: Buying call options Selling call options Buying put options Selling put options Option spreads

Vicentiu Covrig

1717

Buying Call OptionsBuying Call Options Position taken in the expectation that the price will increase (long

position) Profit for purchasing a Call Option:Per Share Profit =Max [0, V-X] – Call Premium The following diagram shows different total dollar profits for

buying a call option with a strike price of $70 and a premium of $6.13

Vicentiu Covrig

1818

Buying Call OptionsBuying Call Options

40 50 60 70 80 90 100

1,000

500

0

1,500

2,000

2,500

3,000

(500)

(1,000)

Exercise Price = $70

Option Price = $6.13

Profit from Strategy

Stock Price at Expiration

Vicentiu Covrig

1919

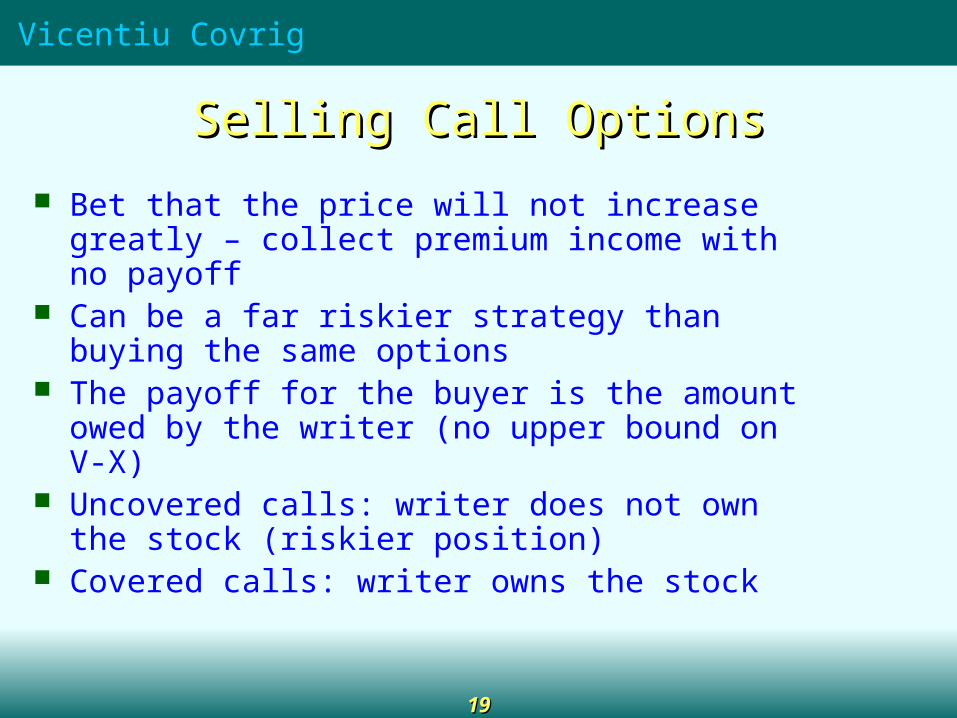

Selling Call OptionsSelling Call Options

Bet that the price will not increase greatly – collect premium income with no payoff

Can be a far riskier strategy than buying the same options The payoff for the buyer is the amount owed by the writer

(no upper bound on V-X) Uncovered calls: writer does not own the stock (riskier

position) Covered calls: writer owns the stock

Vicentiu Covrig

2020

Selling Call OptionsSelling Call Options

40 50 60 70 80 90 100

(1,000)

(1,500)

(2,000)

(500)

0

500

1,000

(2,500)

(3,000)

Exercise Price = $70

Option Price = $6.13

Stock Price at Expiration

Profit from Uncovered Call Strategy

Vicentiu Covrig

2121

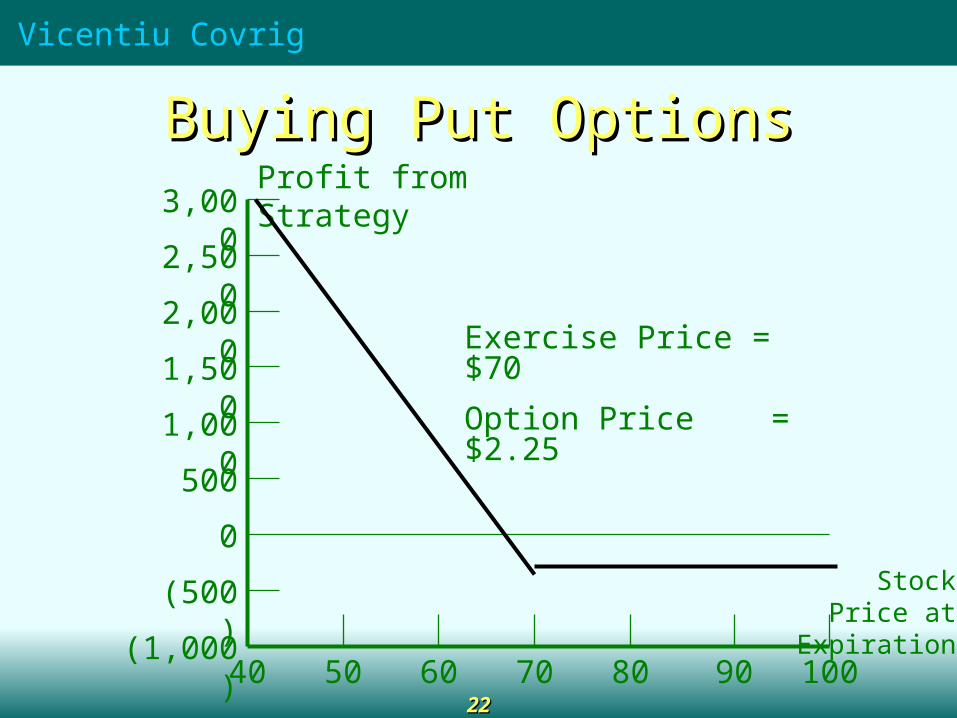

Buying Put OptionsBuying Put Options Position taken in the expectation that the price will

decrease (short position) Profit for purchasing a Put Option:Per Share Profit = Max [0, X-V] – Put Premium Protective put: Buying a put while owning the stock (if the

price declines, option gains offset portfolio losses)

Vicentiu Covrig

2222

Buying Put OptionsBuying Put Options

40 50 60 70 80 90 100

1,000

500

0

1,500

2,000

2,500

3,000

(500)

(1,000)

Exercise Price = $70

Option Price = $2.25

Profit from Strategy

Stock Price at Expiration

Vicentiu Covrig

2323

Selling Put OptionsSelling Put Options Bet that the price will not decline greatly – collect

premium income with no payoff The payoff for the buyer is the amount owed by the writer

(payoff loss limited to the strike price since the stock’s value cannot fall below zero)

Vicentiu Covrig

2424

Selling Put OptionsSelling Put Options

40 50 60 70 80 90 100

(1,000)

(1,500)

(2,000)

(500)

0

500

1,000

(2,500)

(3,000)

Exercise Price = $70

Option Price = $2.25

Stock Price at Expiration

Profit from Strategy

Vicentiu Covrig

2525

Combinations Combinations Spread: both buyer and writer of the same type of

option on the same underlying asset- Price spread: purchase or sale of options on the same

underlying asset but different exercise price

- Time spread: purchase or sale of options on the same underlying asset but different expiration dates

Bull call spread: purchase of a low strike price call and sale of a high strike price call.

Bull put spread: sale of high strike price put and purchase or a low strike price put

Vicentiu Covrig

2626

Payoff Long call

Short call

Bull call spread

PayoffLong put

Short put

Bull put spread

Payoff

Long call Short put

Straddle

Straddle : purchasing a call andWriting a put on the same asset,

exercise price, and expiration date

Vicentiu Covrig

2727

Option pricingOption pricing Factors contributing value of an option

- price of the underlying stock- time until expiration- volatility of underlying stock price- cash dividend- prevailing interest rate.

Intrinsic value: difference between an in-the-money option’s strike price and current market price

Time value: speculative value. Call price = Intrinsic value + time value

Vicentiu Covrig

2828

Black-Scholes Option Pricing ModelBlack-Scholes Option Pricing Model

Where C: current price of a call option S: current market price of the underlying stock X: exercise price r: risk free rate t: time until expiration N(d1) and N (d2) : cumulative density functions for d1 and d2

)()( 21 dNe

XdNSC

rt

funds invested of

cost yOpportunit

potential upside

of Value

price

Call

t

trXSd

2

1

5.0ln tdd 12