vat worksheet guidevat.gov.lc/nc-cms/content/upload/filing the vat return worksheet.pdf · vat...

TRANSCRIPT

1

VAT Worksheet Guide

FLOW CHART

SAMPLE OUTPUT TAX WORKSHEET

SAMPLE INPUT TAX WORKSHEET

VAT ACCOUNT

VAT RETURN

WORKING PAPERS

The information provided herein can be used as a guide to show the flow of information from source documents to the monthly VAT Return.

2

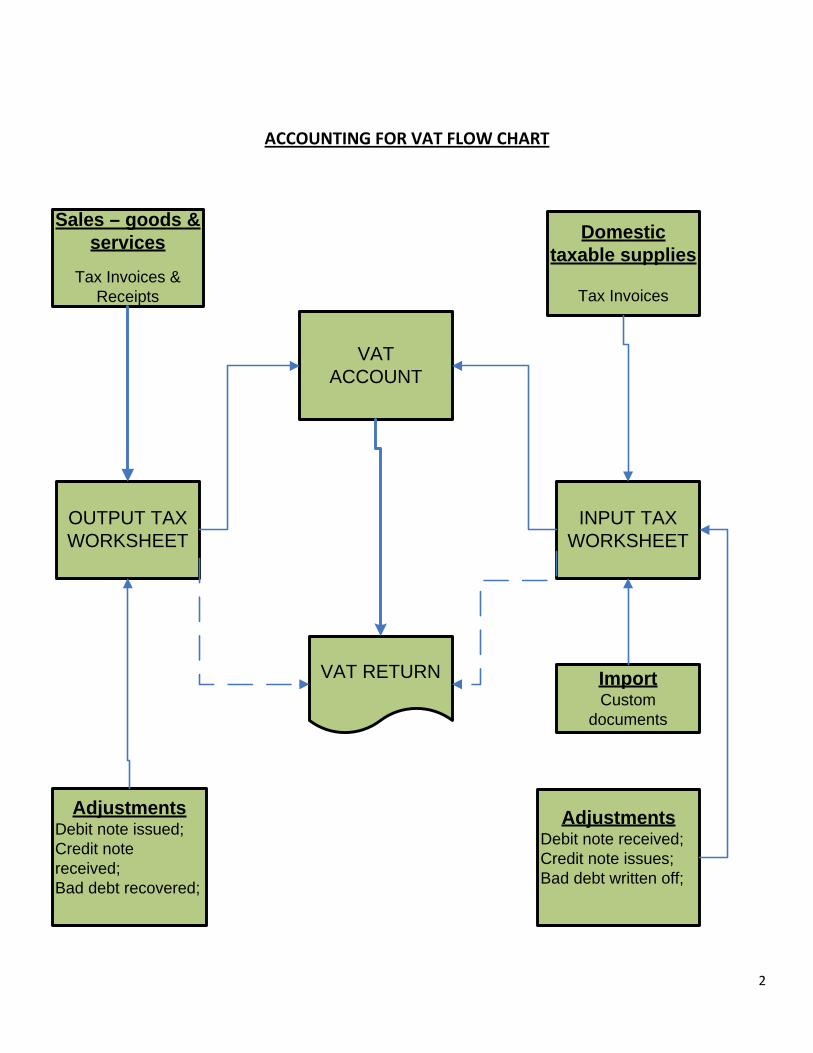

AdjustmentsDebit note issued;Credit note received;Bad debt recovered;

Sales – goods & services

Tax Invoices & Receipts

OUTPUT TAXWORKSHEET

VATACCOUNT

VAT RETURN

Domestic taxable supplies

Tax Invoices

INPUT TAXWORKSHEET

ImportCustom

documents

AdjustmentsDebit note received;Credit note issues;Bad debt written off;

ACCOUNTING FOR VAT FLOW CHART

3

OUTPUT TAX SOURCE DOCUMENTS

Output tax is generated from the local sale of taxable goods and services provided to other businesses and the final consumer. Source documents that identify output tax are VAT Invoices and VAT Sales receipts issued.

Output Tax can also be derived from VAT Credit Notes received, VAT Debit Notes issued and Bad Debt recovered that was previously written off and the business was allowed an input tax deduction for such Bad Debt.

All output tax is recorded in the output tax worksheet, which is subsequently transferred to the VAT Account and later used to calculate the output tax reportable on the VAT Return Form for a Tax Period.

There are other transactions that also give rise to output tax. These include where goods or services taken for personal or employee use; donated to related persons or to an approved charitable organization.

INPUT TAX SOURCE DOCUMENTS

Input tax is generated from the purchase of local taxable goods (including allowable fixed assets) and services and on importation. Source documents that identify input tax are VAT Invoices and the Customs Declaration Form.

Input tax can also be derived from VAT Credit Notes issued, VAT Debit Notes received and Bad Debt written off, where the Comptroller is satisfied that all efforts to collect proved unsuccessful.

All allowable input tax is recorded in the input tax worksheet, which is subsequently transferred to the VAT Account and the VAT Return Form for that Tax Period.

4

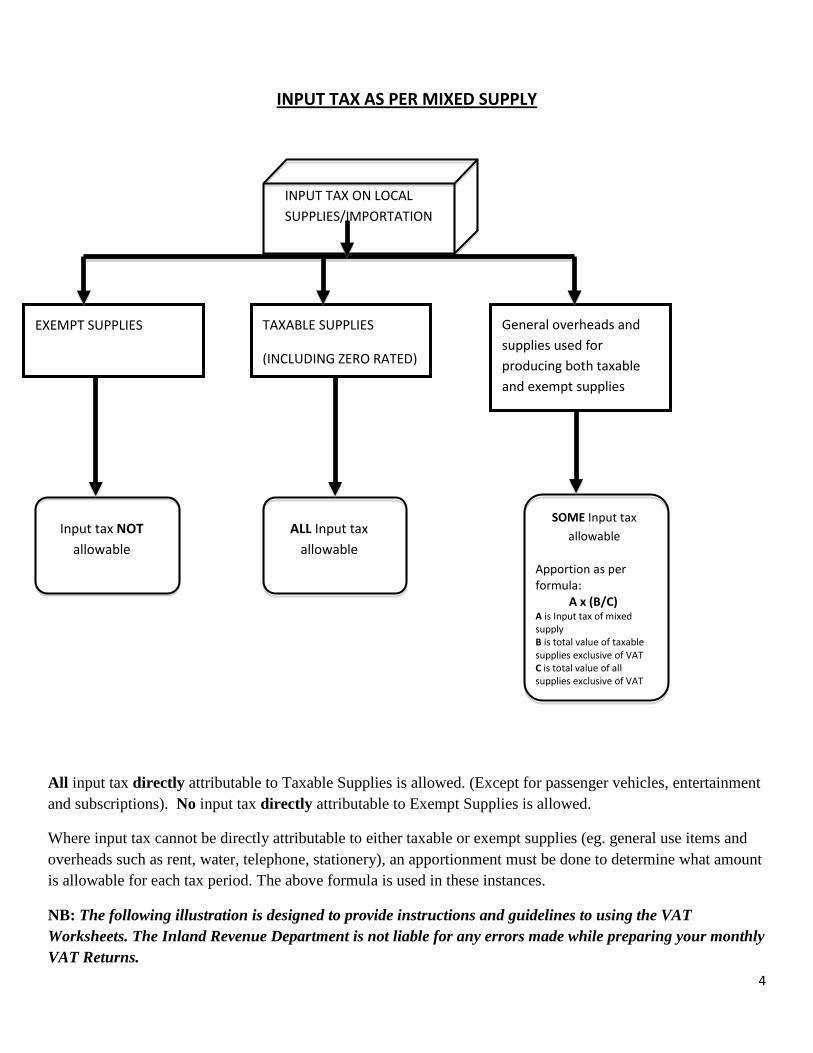

INPUT TAX AS PER MIXED SUPPLY

All input tax directly attributable to Taxable Supplies is allowed. (Except for passenger vehicles, entertainment and subscriptions). No input tax directly attributable to Exempt Supplies is allowed.

Where input tax cannot be directly attributable to either taxable or exempt supplies (eg. general use items and overheads such as rent, water, telephone, stationery), an apportionment must be done to determine what amount is allowable for each tax period. The above formula is used in these instances.

NB: The following illustration is designed to provide instructions and guidelines to using the VAT Worksheets. The Inland Revenue Department is not liable for any errors made while preparing your monthly VAT Returns.

EXEMPT SUPPLIES General overheads and supplies used for producing both taxable and exempt supplies

TAXABLE SUPPLIES

(INCLUDING ZERO RATED)

Input tax NOT allowable

ALL Input tax allowable

SOME Input tax allowable

INPUT TAX ON LOCAL SUPPLIES/IMPORTATION

Apportion as per formula:

A x (B/C) A is Input tax of mixed supply B is total value of taxable supplies exclusive of VAT C is total value of all supplies exclusive of VAT

5

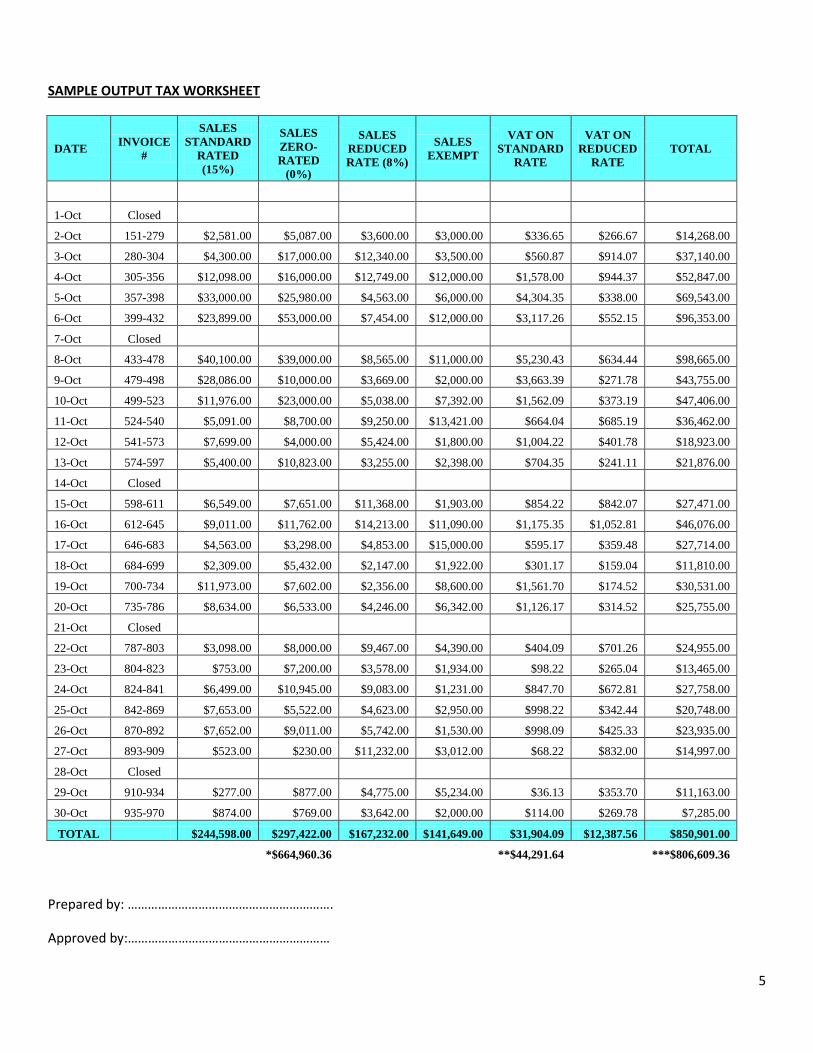

SAMPLE OUTPUT TAX WORKSHEET

DATE INVOICE #

SALES STANDARD

RATED (15%)

SALES ZERO-RATED

(0%)

SALES REDUCED RATE (8%)

SALES EXEMPT

VAT ON STANDARD

RATE

VAT ON REDUCED

RATE TOTAL

1-Oct Closed

2-Oct 151-279 $2,581.00 $5,087.00 $3,600.00 $3,000.00 $336.65 $266.67 $14,268.00

3-Oct 280-304 $4,300.00 $17,000.00 $12,340.00 $3,500.00 $560.87 $914.07 $37,140.00

4-Oct 305-356 $12,098.00 $16,000.00 $12,749.00 $12,000.00 $1,578.00 $944.37 $52,847.00

5-Oct 357-398 $33,000.00 $25,980.00 $4,563.00 $6,000.00 $4,304.35 $338.00 $69,543.00

6-Oct 399-432 $23,899.00 $53,000.00 $7,454.00 $12,000.00 $3,117.26 $552.15 $96,353.00

7-Oct Closed

8-Oct 433-478 $40,100.00 $39,000.00 $8,565.00 $11,000.00 $5,230.43 $634.44 $98,665.00

9-Oct 479-498 $28,086.00 $10,000.00 $3,669.00 $2,000.00 $3,663.39 $271.78 $43,755.00

10-Oct 499-523 $11,976.00 $23,000.00 $5,038.00 $7,392.00 $1,562.09 $373.19 $47,406.00

11-Oct 524-540 $5,091.00 $8,700.00 $9,250.00 $13,421.00 $664.04 $685.19 $36,462.00

12-Oct 541-573 $7,699.00 $4,000.00 $5,424.00 $1,800.00 $1,004.22 $401.78 $18,923.00

13-Oct 574-597 $5,400.00 $10,823.00 $3,255.00 $2,398.00 $704.35 $241.11 $21,876.00

14-Oct Closed

15-Oct 598-611 $6,549.00 $7,651.00 $11,368.00 $1,903.00 $854.22 $842.07 $27,471.00

16-Oct 612-645 $9,011.00 $11,762.00 $14,213.00 $11,090.00 $1,175.35 $1,052.81 $46,076.00

17-Oct 646-683 $4,563.00 $3,298.00 $4,853.00 $15,000.00 $595.17 $359.48 $27,714.00

18-Oct 684-699 $2,309.00 $5,432.00 $2,147.00 $1,922.00 $301.17 $159.04 $11,810.00

19-Oct 700-734 $11,973.00 $7,602.00 $2,356.00 $8,600.00 $1,561.70 $174.52 $30,531.00

20-Oct 735-786 $8,634.00 $6,533.00 $4,246.00 $6,342.00 $1,126.17 $314.52 $25,755.00

21-Oct Closed

22-Oct 787-803 $3,098.00 $8,000.00 $9,467.00 $4,390.00 $404.09 $701.26 $24,955.00

23-Oct 804-823 $753.00 $7,200.00 $3,578.00 $1,934.00 $98.22 $265.04 $13,465.00

24-Oct 824-841 $6,499.00 $10,945.00 $9,083.00 $1,231.00 $847.70 $672.81 $27,758.00

25-Oct 842-869 $7,653.00 $5,522.00 $4,623.00 $2,950.00 $998.22 $342.44 $20,748.00

26-Oct 870-892 $7,652.00 $9,011.00 $5,742.00 $1,530.00 $998.09 $425.33 $23,935.00

27-Oct 893-909 $523.00 $230.00 $11,232.00 $3,012.00 $68.22 $832.00 $14,997.00

28-Oct Closed

29-Oct 910-934 $277.00 $877.00 $4,775.00 $5,234.00 $36.13 $353.70 $11,163.00

30-Oct 935-970 $874.00 $769.00 $3,642.00 $2,000.00 $114.00 $269.78 $7,285.00

TOTAL $244,598.00 $297,422.00 $167,232.00 $141,649.00 $31,904.09 $12,387.56 $850,901.00

*$664,960.36

**$44,291.64

***$806,609.36

Prepared by: …………………………………………………….

Approved by:……………………………………………………

6

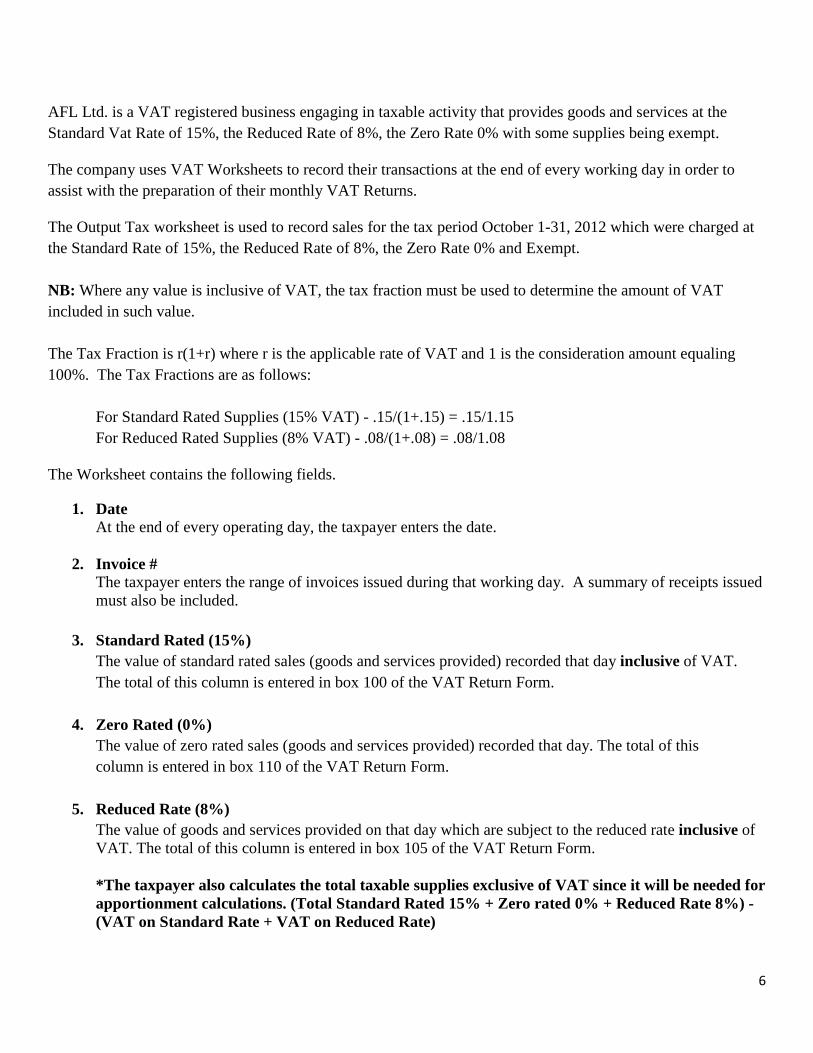

AFL Ltd. is a VAT registered business engaging in taxable activity that provides goods and services at the Standard Vat Rate of 15%, the Reduced Rate of 8%, the Zero Rate 0% with some supplies being exempt. The company uses VAT Worksheets to record their transactions at the end of every working day in order to assist with the preparation of their monthly VAT Returns. The Output Tax worksheet is used to record sales for the tax period October 1-31, 2012 which were charged at the Standard Rate of 15%, the Reduced Rate of 8%, the Zero Rate 0% and Exempt. NB: Where any value is inclusive of VAT, the tax fraction must be used to determine the amount of VAT included in such value. The Tax Fraction is r(1+r) where r is the applicable rate of VAT and 1 is the consideration amount equaling 100%. The Tax Fractions are as follows:

For Standard Rated Supplies (15% VAT) - .15/(1+.15) = .15/1.15 For Reduced Rated Supplies (8% VAT) - .08/(1+.08) = .08/1.08

The Worksheet contains the following fields.

1. Date At the end of every operating day, the taxpayer enters the date.

2. Invoice # The taxpayer enters the range of invoices issued during that working day. A summary of receipts issued must also be included.

3. Standard Rated (15%) The value of standard rated sales (goods and services provided) recorded that day inclusive of VAT. The total of this column is entered in box 100 of the VAT Return Form.

4. Zero Rated (0%) The value of zero rated sales (goods and services provided) recorded that day. The total of this column is entered in box 110 of the VAT Return Form.

5. Reduced Rate (8%) The value of goods and services provided on that day which are subject to the reduced rate inclusive of VAT. The total of this column is entered in box 105 of the VAT Return Form.

*The taxpayer also calculates the total taxable supplies exclusive of VAT since it will be needed for apportionment calculations. (Total Standard Rated 15% + Zero rated 0% + Reduced Rate 8%) - (VAT on Standard Rate + VAT on Reduced Rate)

7

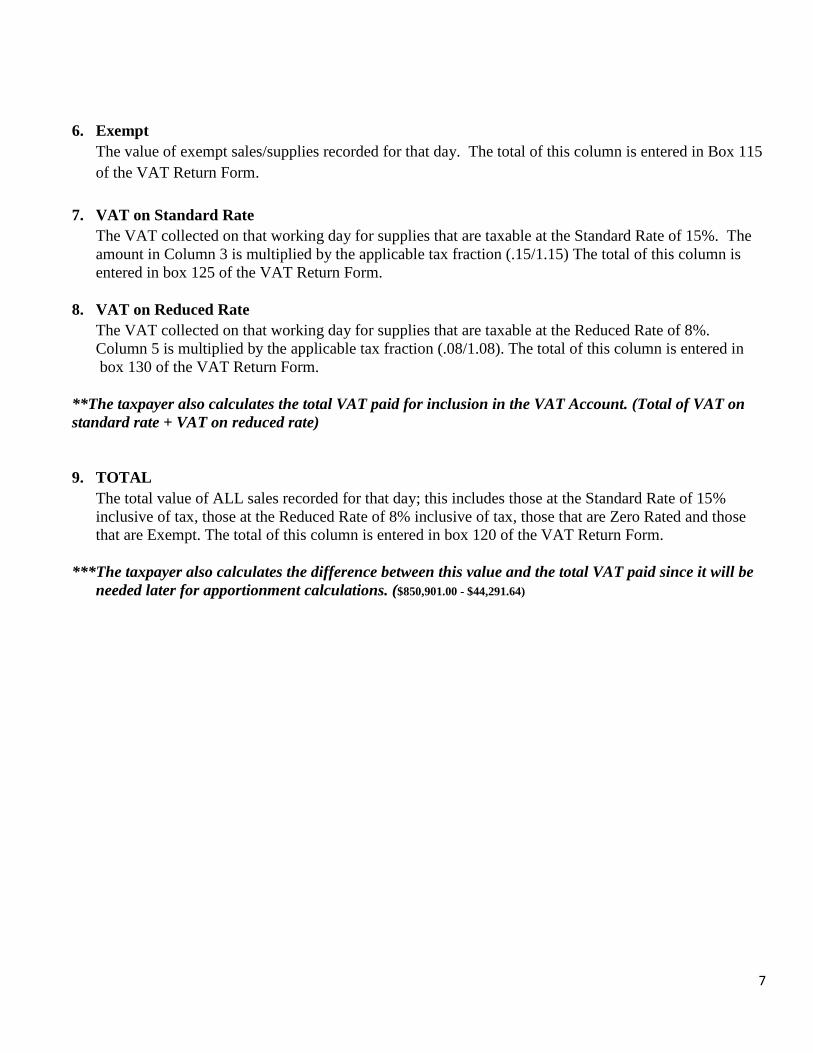

6. Exempt The value of exempt sales/supplies recorded for that day. The total of this column is entered in Box 115 of the VAT Return Form.

7. VAT on Standard Rate The VAT collected on that working day for supplies that are taxable at the Standard Rate of 15%. The amount in Column 3 is multiplied by the applicable tax fraction (.15/1.15) The total of this column is entered in box 125 of the VAT Return Form.

8. VAT on Reduced Rate The VAT collected on that working day for supplies that are taxable at the Reduced Rate of 8%. Column 5 is multiplied by the applicable tax fraction (.08/1.08). The total of this column is entered in box 130 of the VAT Return Form.

**The taxpayer also calculates the total VAT paid for inclusion in the VAT Account. (Total of VAT on standard rate + VAT on reduced rate)

9. TOTAL The total value of ALL sales recorded for that day; this includes those at the Standard Rate of 15% inclusive of tax, those at the Reduced Rate of 8% inclusive of tax, those that are Zero Rated and those that are Exempt. The total of this column is entered in box 120 of the VAT Return Form.

***The taxpayer also calculates the difference between this value and the total VAT paid since it will be needed later for apportionment calculations. ($850,901.00 - $44,291.64)

8

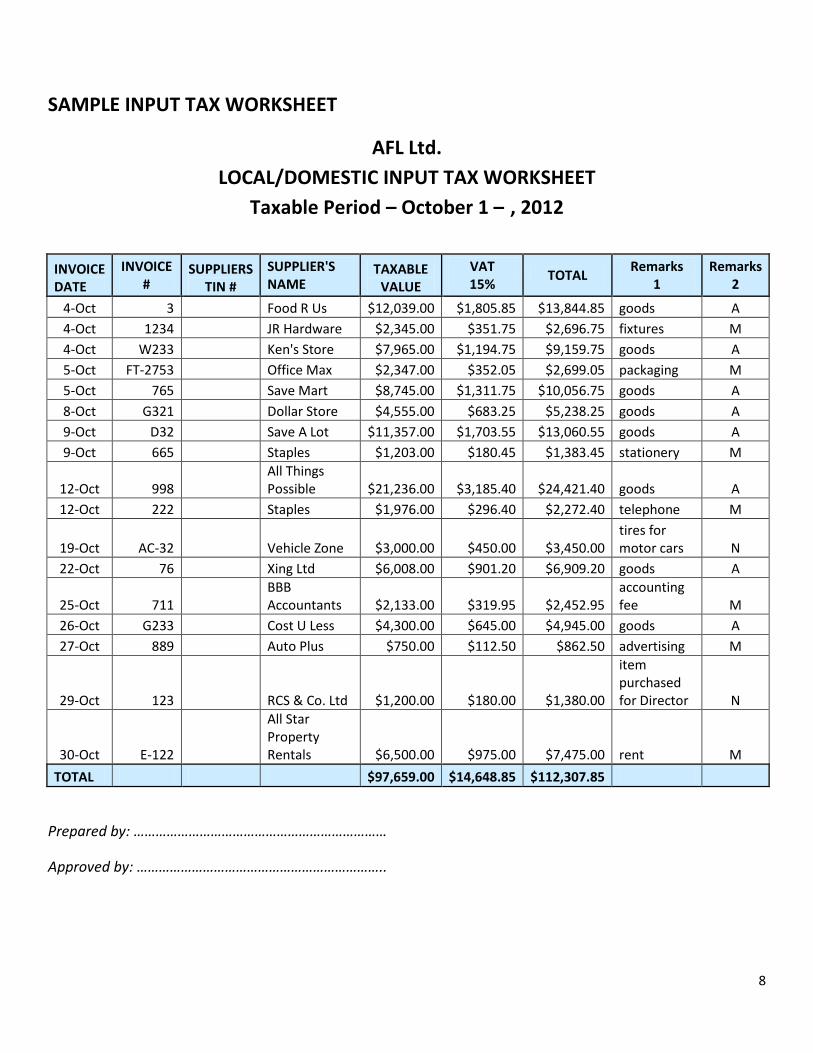

SAMPLE INPUT TAX WORKSHEET

AFL Ltd. LOCAL/DOMESTIC INPUT TAX WORKSHEET

Taxable Period – October 1 – , 2012

INVOICE DATE

INVOICE #

SUPPLIERS TIN #

SUPPLIER'S NAME

TAXABLE VALUE

VAT 15%

TOTAL Remarks

1 Remarks

2

4-Oct 3 Food R Us $12,039.00 $1,805.85 $13,844.85 goods A 4-Oct 1234 JR Hardware $2,345.00 $351.75 $2,696.75 fixtures M 4-Oct W233 Ken's Store $7,965.00 $1,194.75 $9,159.75 goods A 5-Oct FT-2753 Office Max $2,347.00 $352.05 $2,699.05 packaging M 5-Oct 765 Save Mart $8,745.00 $1,311.75 $10,056.75 goods A 8-Oct G321 Dollar Store $4,555.00 $683.25 $5,238.25 goods A 9-Oct D32 Save A Lot $11,357.00 $1,703.55 $13,060.55 goods A 9-Oct 665 Staples $1,203.00 $180.45 $1,383.45 stationery M

12-Oct 998 All Things Possible $21,236.00 $3,185.40 $24,421.40 goods A

12-Oct 222 Staples $1,976.00 $296.40 $2,272.40 telephone M

19-Oct AC-32 Vehicle Zone $3,000.00 $450.00 $3,450.00 tires for motor cars N

22-Oct 76 Xing Ltd $6,008.00 $901.20 $6,909.20 goods A

25-Oct 711 BBB Accountants $2,133.00 $319.95 $2,452.95

accounting fee M

26-Oct G233 Cost U Less $4,300.00 $645.00 $4,945.00 goods A 27-Oct 889 Auto Plus $750.00 $112.50 $862.50 advertising M

29-Oct 123 RCS & Co. Ltd $1,200.00 $180.00 $1,380.00

item purchased for Director N

30-Oct E-122

All Star Property Rentals $6,500.00 $975.00 $7,475.00 rent M

TOTAL $97,659.00 $14,648.85 $112,307.85

Prepared by: ……………………………………………………………

Approved by: …………………………………………………………..

9

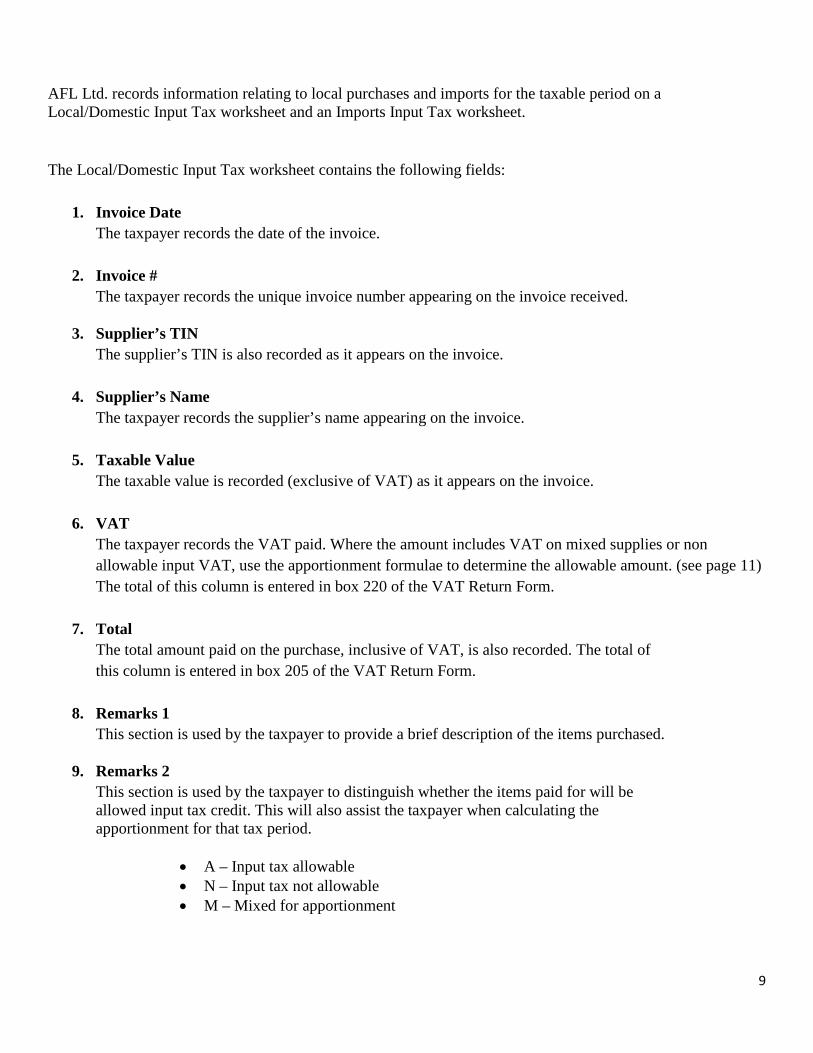

AFL Ltd. records information relating to local purchases and imports for the taxable period on a Local/Domestic Input Tax worksheet and an Imports Input Tax worksheet. The Local/Domestic Input Tax worksheet contains the following fields:

1. Invoice Date The taxpayer records the date of the invoice.

2. Invoice # The taxpayer records the unique invoice number appearing on the invoice received.

3. Supplier’s TIN The supplier’s TIN is also recorded as it appears on the invoice.

4. Supplier’s Name The taxpayer records the supplier’s name appearing on the invoice.

5. Taxable Value The taxable value is recorded (exclusive of VAT) as it appears on the invoice.

6. VAT The taxpayer records the VAT paid. Where the amount includes VAT on mixed supplies or non allowable input VAT, use the apportionment formulae to determine the allowable amount. (see page 11) The total of this column is entered in box 220 of the VAT Return Form.

7. Total The total amount paid on the purchase, inclusive of VAT, is also recorded. The total of this column is entered in box 205 of the VAT Return Form.

8. Remarks 1 This section is used by the taxpayer to provide a brief description of the items purchased.

9. Remarks 2

This section is used by the taxpayer to distinguish whether the items paid for will be allowed input tax credit. This will also assist the taxpayer when calculating the apportionment for that tax period.

• A – Input tax allowable • N – Input tax not allowable • M – Mixed for apportionment

10

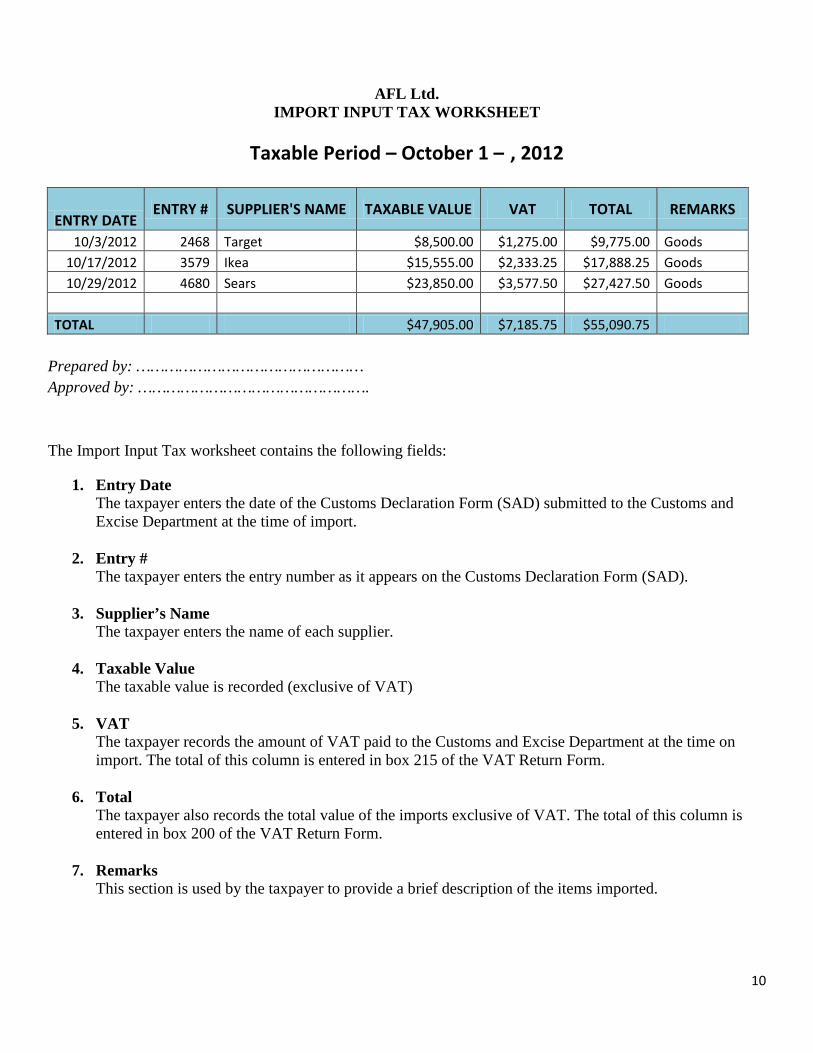

AFL Ltd. IMPORT INPUT TAX WORKSHEET

Taxable Period – October 1 – , 2012

ENTRY DATE ENTRY # SUPPLIER'S NAME TAXABLE VALUE VAT TOTAL REMARKS

10/3/2012 2468 Target $8,500.00 $1,275.00 $9,775.00 Goods 10/17/2012 3579 Ikea $15,555.00 $2,333.25 $17,888.25 Goods 10/29/2012 4680 Sears $23,850.00 $3,577.50 $27,427.50 Goods

TOTAL $47,905.00 $7,185.75 $55,090.75

Prepared by: ………………………………………… Approved by: …………………………………………. The Import Input Tax worksheet contains the following fields:

1. Entry Date The taxpayer enters the date of the Customs Declaration Form (SAD) submitted to the Customs and Excise Department at the time of import.

2. Entry # The taxpayer enters the entry number as it appears on the Customs Declaration Form (SAD).

3. Supplier’s Name The taxpayer enters the name of each supplier.

4. Taxable Value The taxable value is recorded (exclusive of VAT)

5. VAT The taxpayer records the amount of VAT paid to the Customs and Excise Department at the time on import. The total of this column is entered in box 215 of the VAT Return Form.

6. Total The taxpayer also records the total value of the imports exclusive of VAT. The total of this column is entered in box 200 of the VAT Return Form.

7. Remarks This section is used by the taxpayer to provide a brief description of the items imported.

11

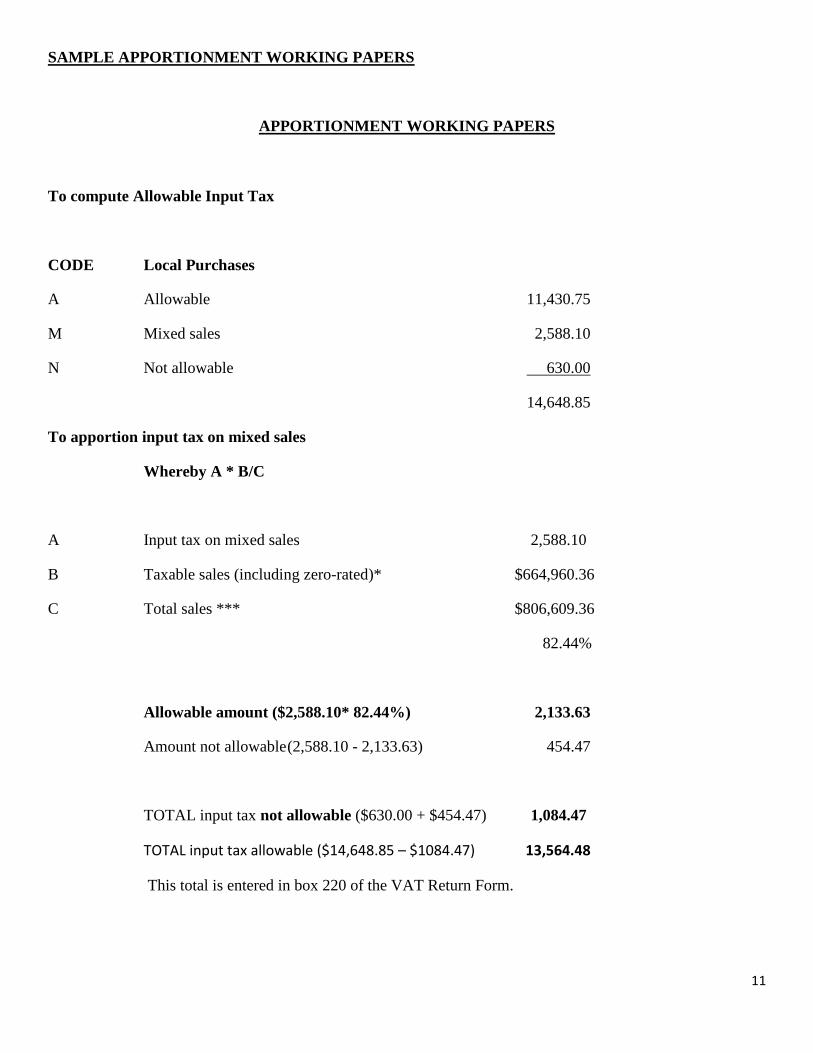

SAMPLE APPORTIONMENT WORKING PAPERS

APPORTIONMENT WORKING PAPERS

To compute Allowable Input Tax

CODE Local Purchases

A Allowable 11,430.75

M Mixed sales 2,588.10

N Not allowable 630.00

14,648.85

To apportion input tax on mixed sales

Whereby A * B/C

A Input tax on mixed sales 2,588.10

B Taxable sales (including zero-rated)* $664,960.36

C Total sales *** $806,609.36

82.44%

Allowable amount ($2,588.10* 82.44%) 2,133.63

Amount not allowable (2,588.10 - 2,133.63) 454.47

TOTAL input tax not allowable ($630.00 + $454.47) 1,084.47

TOTAL input tax allowable ($14,648.85 – $1084.47) 13,564.48

This total is entered in box 220 of the VAT Return Form.

12

Apportionment is necessary for those goods and services received where input tax in not directly attributable to neither taxable nor exempt supplies. Information pertaining to Local purchases was derived from the Local Purchases Input Tax Worksheet. The taxpayer used the Remark 2 column in this worksheet to separate those items where input tax was fully allowable ‘A’ ($11,430.75), not allowable ‘N’ ($630.00) and those attributable to the mixed/partial activity ‘M’ ($ 2,588.10). Apportionment must be done to determine what portion of that input tax attributable to the mixed activity is allowable for this tax period. The following formula is used: A * B/C Where A = Input tax attributable to mixed activity B = total taxable sales C = total sales A is derived from the Local Purchases Input Tax Worksheet. B includes all TAXABLE sales exclusive of VAT. This includes Standard Rated supplies of 15%, sales subject to the Reduced Rate of 8% and Zero Rated sales. This amount can be obtained from the Output Tax Worksheet where total VAT collected is deducted from total VAT inclusive taxable sales. C includes all sales exclusive of VAT made by the taxpayer in the tax period. This includes Standard Rated sales of 15%, sales subject to the Reduced Rate of 8%, Zero Rated sales and Exempt sales. This amount can be obtained from the Output Tax Worksheet where total VAT collected is deducted from total sales. In this illustration, B/C = 87.93% which means 87.93% of $2,588.10 will be allowed as input tax credit for this period.

Where B/C ≥ 90%, all of the input tax attributable to the mixed activity will be allowed.

13

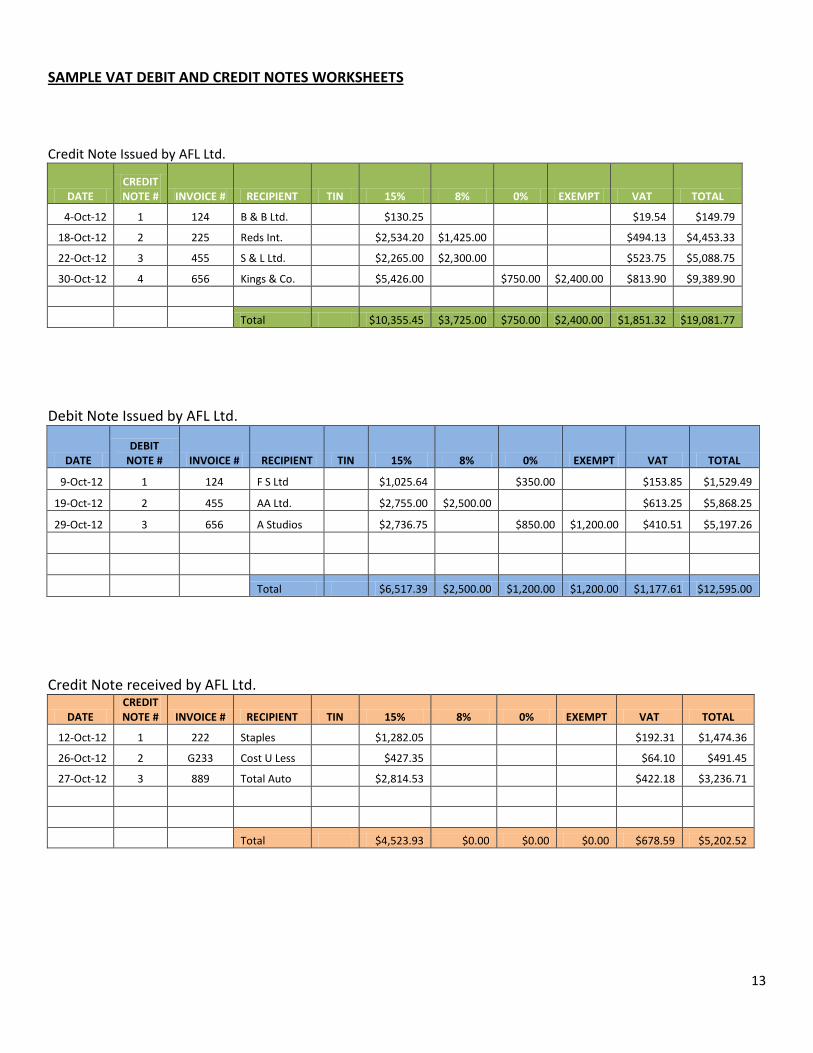

SAMPLE VAT DEBIT AND CREDIT NOTES WORKSHEETS Credit Note Issued by AFL Ltd.

DATE CREDIT NOTE # INVOICE # RECIPIENT TIN 15% 8% 0% EXEMPT VAT TOTAL

4-Oct-12 1 124 B & B Ltd. $130.25 $19.54 $149.79

18-Oct-12 2 225 Reds Int. $2,534.20 $1,425.00 $494.13 $4,453.33

22-Oct-12 3 455 S & L Ltd. $2,265.00 $2,300.00 $523.75 $5,088.75

30-Oct-12 4 656 Kings & Co. $5,426.00 $750.00 $2,400.00 $813.90 $9,389.90

Total $10,355.45 $3,725.00 $750.00 $2,400.00 $1,851.32 $19,081.77

Debit Note Issued by AFL Ltd.

DATE DEBIT

NOTE # INVOICE # RECIPIENT TIN 15% 8% 0% EXEMPT VAT TOTAL

9-Oct-12 1 124 F S Ltd $1,025.64 $350.00 $153.85 $1,529.49

19-Oct-12 2 455 AA Ltd. $2,755.00 $2,500.00 $613.25 $5,868.25

29-Oct-12 3 656 A Studios $2,736.75 $850.00 $1,200.00 $410.51 $5,197.26

Total $6,517.39 $2,500.00 $1,200.00 $1,200.00 $1,177.61 $12,595.00

Credit Note received by AFL Ltd.

DATE CREDIT NOTE # INVOICE # RECIPIENT TIN 15% 8% 0% EXEMPT VAT TOTAL

12-Oct-12 1 222 Staples $1,282.05 $192.31 $1,474.36

26-Oct-12 2 G233 Cost U Less $427.35 $64.10 $491.45

27-Oct-12 3 889 Total Auto $2,814.53 $422.18 $3,236.71

Total $4,523.93 $0.00 $0.00 $0.00 $678.59 $5,202.52

14

AFL Ltd. records information relating to credit and debit notes issued and received for the taxable period on a Debit Notes Issued, Credit Notes Issued, Debit Notes Received and Credit Notes Received worksheets. The Debit and Credit Notes Issued/Received worksheets contain the following fields:

1. Date The taxpayer records the date of the Credit/Debit Note issued.

2. Credit/Debit Note #

The unique number of each Credit/Debit Note issued is recorded.

3. Invoice # The taxpayer records the invoice number of the original invoice to which the Credit/Debit Note relate.

4. Recipient/Supplier

The taxpayer records the name of the receipt/supplier of the Credit/Debit Note.

5. TIN The taxpayer records the recipient/supplier TIN if registered.

6. Standard

The value of the Standard Rated sales is recorded exclusive of VAT.

7. Reduced The value of the sales subject to the Reduced Rate exclusive of VAT.

8. Zero

The value of the Standard Rated sales is recorded.

9. Exempt The value of the Exempt sales is recorded.

10. VAT

The total VAT reported in the Credit/Debit Note is recorded.

11. TOTAL The taxable value is recorded (inclusive of VAT) as it appears on the Credit/Debit Note.

15

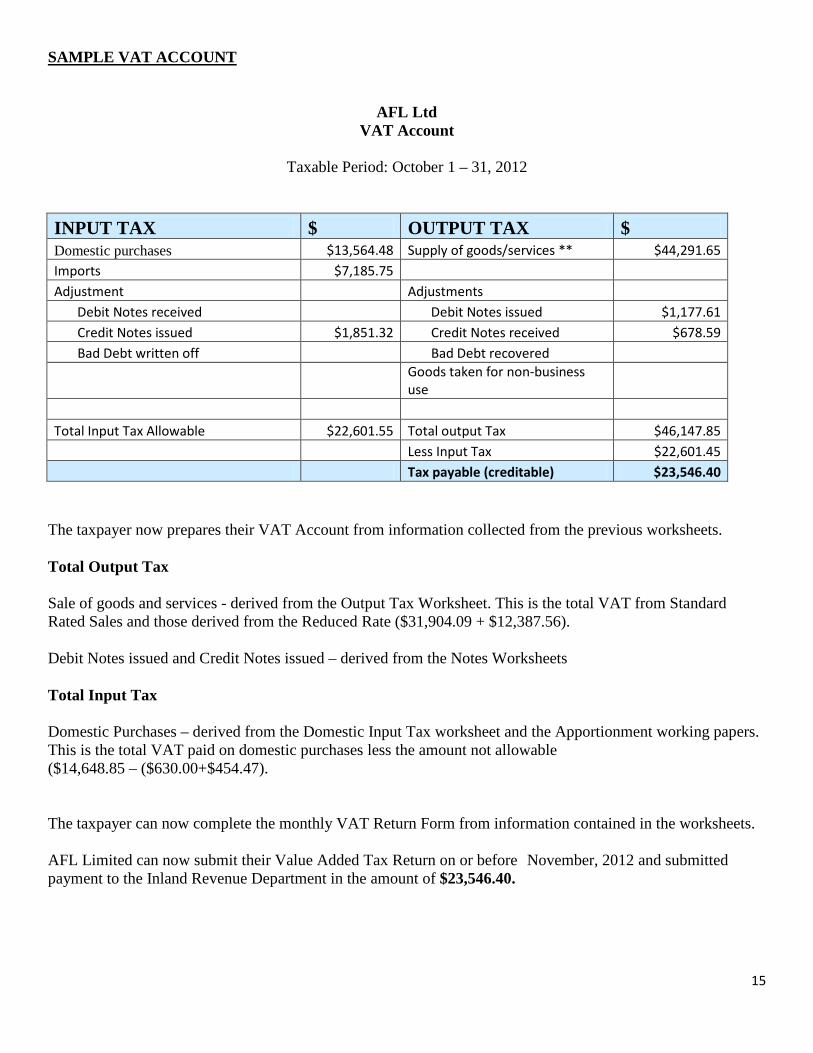

SAMPLE VAT ACCOUNT

AFL Ltd VAT Account

Taxable Period: October 1 – 31, 2012

INPUT TAX $ OUTPUT TAX $ Domestic purchases $13,564.48 Supply of goods/services ** $44,291.65 Imports $7,185.75 Adjustment Adjustments Debit Notes received Debit Notes issued $1,177.61 Credit Notes issued $1,851.32 Credit Notes received $678.59 Bad Debt written off Bad Debt recovered

Goods taken for non-business use

Total Input Tax Allowable $22,601.55 Total output Tax $46,147.85 Less Input Tax $22,601.45 Tax payable (creditable) $23,546.40

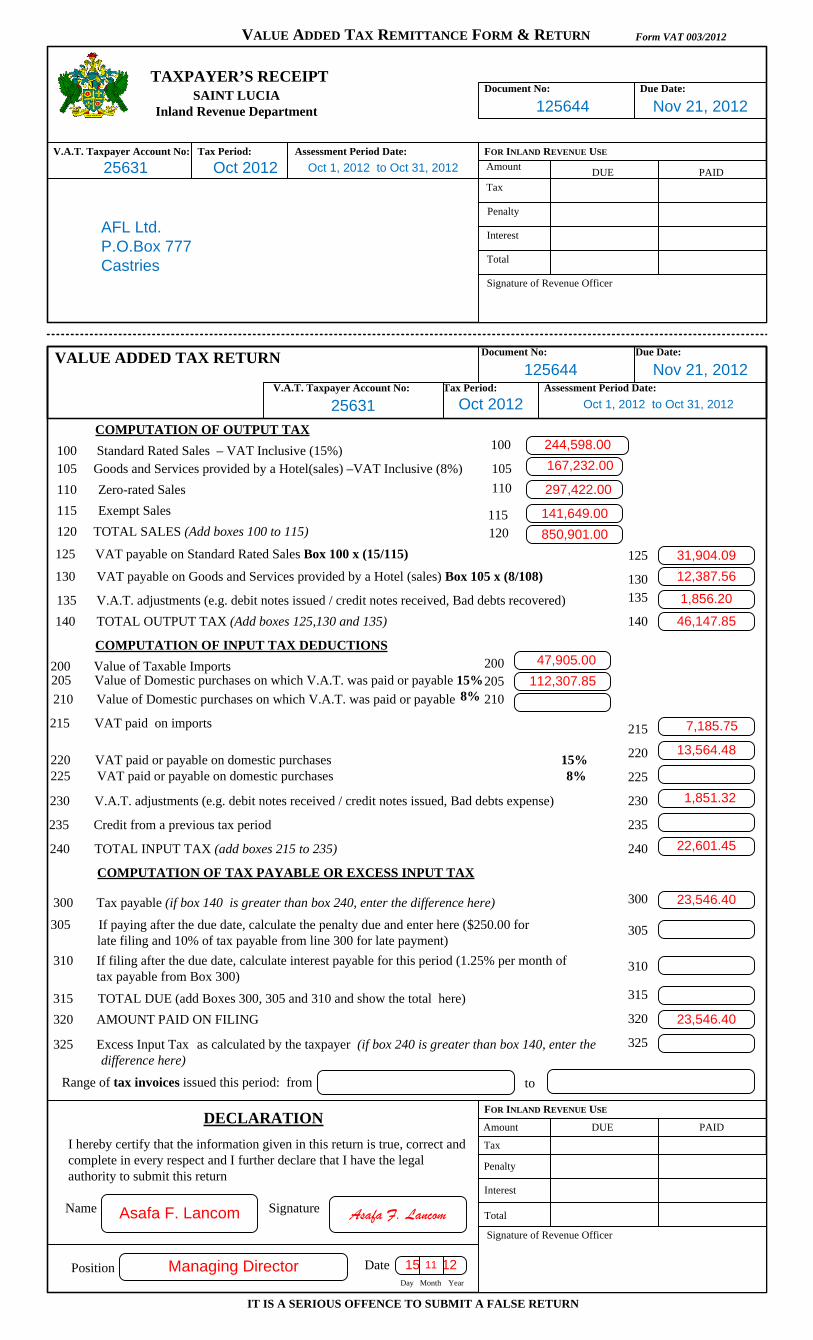

The taxpayer now prepares their VAT Account from information collected from the previous worksheets. Total Output Tax Sale of goods and services - derived from the Output Tax Worksheet. This is the total VAT from Standard Rated Sales and those derived from the Reduced Rate ($31,904.09 + $12,387.56). Debit Notes issued and Credit Notes issued – derived from the Notes Worksheets Total Input Tax Domestic Purchases – derived from the Domestic Input Tax worksheet and the Apportionment working papers. This is the total VAT paid on domestic purchases less the amount not allowable ($14,648.85 – ($630.00+$454.47). The taxpayer can now complete the monthly VAT Return Form from information contained in the worksheets. AFL Limited can now submit their Value Added Tax Return on or before November, 2012 and submitted payment to the Inland Revenue Department in the amount of $23,546.40.

TAXPAYER’S RECEIPTDue Date:Document No:

SAINT LUCIAInland Revenue Department

VALUE ADDED TAX REMITTANCE FORM & RETURN

V.A.T. Taxpayer Account No: Tax Period: Assessment Period Date: FOR INLAND REVENUE USE

Amount

Tax

Penalty

Interest

Total

DUE PAID

Signature of Revenue Officer

Document No: Due Date:

V.A.T. Taxpayer Account No: Tax Period: Assessment Period Date:

115 Exempt Sales

110 Zero-rated Sales

140 TOTAL OUTPUT TAX (Add boxes 125,130 and 135)

135 V.A.T. adjustments (e.g. debit notes issued / credit notes received, Bad debts recovered)

125 VAT payable on Standard Rated Sales Box 100 x (15/115)

105 Goods and Services provided by a Hotel(sales) –VAT Inclusive (8%)100 Standard Rated Sales – VAT Inclusive (15%)

COMPUTATION OF OUTPUT TAX

COMPUTATION OF INPUT TAX DEDUCTIONS

215 VAT paid on imports

230 V.A.T. adjustments (e.g. debit notes received / credit notes issued, Bad debts expense)

220 VAT paid or payable on domestic purchases 15% 225 VAT paid or payable on domestic purchases 8%

200 Value of Taxable Imports

240 TOTAL INPUT TAX (add boxes 215 to 235)

DECLARATION

Signature of Revenue Officer

FOR INLAND REVENUE USE

Amount DUE PAID

Tax

Penalty

Interest

Total

I hereby certify that the information given in this return is true, correct and complete in every respect and I further declare that I have the legal authority to submit this return

Name

Position

Signature

Date

100

220

215

205200

140

135

125

115

105

IT IS A SERIOUS OFFENCE TO SUBMIT A FALSE RETURN

130 VAT payable on Goods and Services provided by a Hotel (sales) Box 105 x (8/108) 130

244,598.00

297,422.00

31,904.09

12,387.56

1,856.20

46,147.85

112,307.85

47,905.00

1,851.32

13,564.48

7,185.75

Asafa F. Lancom Asafa F. Lancom

Managing Director 15 11 1211

Day Month Year

235 Credit from a previous tax period

300 23,546.40

315 TOTAL DUE (add Boxes 300, 305 and 310 and show the total here)

235

230

240

120 TOTAL SALES (Add boxes 100 to 115) 850,901.00

110

120

Form VAT 003/2012

VALUE ADDED TAX RETURN

205 Value of Domestic purchases on which V.A.T. was paid or payable 15%8%

310 If filing after the due date, calculate interest payable for this period (1.25% per month of tax payable from Box 300)

300 Tax payable (if box 140 is greater than box 240, enter the difference here)

COMPUTATION OF TAX PAYABLE OR EXCESS INPUT TAX

315

310

23,546.40

Range of tax invoices issued this period: from to

305 If paying after the due date, calculate the penalty due and enter here ($250.00 for late filing and 10% of tax payable from line 300 for late payment)

22,601.45

305

320 AMOUNT PAID ON FILING

325325 Excess Input Tax as calculated by the taxpayer (if box 240 is greater than box 140, enter the difference here)

320

225

210

167,232.00

141,649.00

210 Value of Domestic purchases on which V.A.T. was paid or payable

125644 Nov 21, 2012

25631 Oct 2012 Oct 1, 2012 to Oct 31, 2012

AFL Ltd.P.O.Box 777Castries

125644 Nov 21, 2012

25631 Oct 2012 Oct 1, 2012 to Oct 31, 2012