vat resources - eu- · pdf filevat resources . 2/54 ... person who states the vat in an...

TRANSCRIPT

Republic of Serbia

Chapter 33 – Financial and Budgetary Provisions

VAT RESOURCES

2/54

CONTENT (1/5)

The legal framework of the Republic of Serbia;

The legal framework of the European Union;

VAT system in the Republic of Serbia;

Subject of Taxation;

The following shall not be understood to mean the sale of

goods an services;

Taxpayer;

Tax Debtor;

Tax Base;

3/54

CONTENT (2/5)

Onset of Tax Liability;

Tax Rate;

Tax Exemption;

Input Tax;

Proportional Tax Deduction;

Special Taxation Procedure;

Registration of Taxpayer;

Duties of Taxpayers;

Taxation Period;

Tax Declaration filing, VAT Assessment and Payment;

Tax Liability;

4/54

CONTENT (3/5) Tax Refund and Rebate;

Level of achieved harmonization and further steps;

Number of VAT Taxpayer;

Register of VAT Payers;

Submission of Tax Return in E- form;

General Administrative capacity of the Tax

administration;

General Administrative capacity of the Tax administration –

Legal base;

Tax Administration Organizational Chart;

5/54

CONTENT (4/5)

Tax Administration Organizational Chart - Headquarter;

Tax Administration Administrative Capacities;

Audit Sector Organizational Chart;

Administrative Capacities of Tax Control;

Collection Sector Organizational Chart;

Administrative Capacities of Tax Collection;

Tax Control Types and Organization;

Control Procedure;

Plans of Audit Sector;

Plans – Building Administrative Capacity;

6/54

CONTENT (5/5)

Tax Debt Collection;

Regular Collection of Tax Debt;

Enforced Collection;

VAT Revenues;

Plans of Collection Sector.

7/54

THE LEGAL FRAMEWORK

OF THE REPUBLIC OF SERBIA

Value added tax law („Official Gazette RS“, No. 84/2004, 86/2004,

61/2005, 61/2007, 93/2012, 108/2013, 68/2014 – other law, 142/2014)

Law on tax procedure and tax administration (”Official Gazette

of RS”, No. 80/02, 84/02 - corrigendum, 23/03 - corrigendum, 70/03, 55/04, 61/05,

85/05 – other Law 62/06 - other Law, 61/07, 20/09 - other law, 53/10, 101/11, 2/12

– corrigendum, 93/12, 47/13, 108/13, 68/14, 105/14)

8/54

THE LEGAL FRAMEWORK

OF THE EUROPEAN UNION

COUNCIL DECISION of 7 June 2007 on the system of the European

Communities’ own resources (2007/436/EC, Euratom)

COUNCIL REGULATION (EC, Euratom) No 1150/2000 of 22 May

2000 implementing Decision 94/728/EC, Euratom on the system of the

Communities' own resources (as last amended by Council regulation No

105/2009 of 26 January 2009)

COUNCIL REGULATION (EEC, Euratom) No 1553/89 of 29 May 1989

on the definitive uniform arrangements for the collection of own

resources accruing from value added tax

COUNCIL DIRECTIVE 2006/112/EC of 28 November 2006 on the

common system of value added tax

9/54

VAT SYSTEM

IN THE REPUBLIC OF SERBIA

Value Added Tax (VAT) has been introduced in Serbia since 1

January 2005;

It was introduced the EU VAT model which is characterized by:

Consumable type;

TAX credit method;

Destination principle;

The tax base is broadly defined - includes a large part of the

transactions.

10/54

SUBJECT OF TAXATION

Delivery of goods;

Provision of services.

carried out by a taxpayer in the Republic for a charge, in the

conduct of its business;

Import of goods into the Republic (entry of goods into the

customs territory of the Republic).

11/54

VAT is not payable to:

Transfer of property wholly or partly, with or without charge,

if the transferee is a taxpayer and if it carries on conducting the

same business;

Replacement of goods within the warranty period;

Giving away free of charge business samples in the usual

quantity for such purposes to buyers;

Giving advertising material and other gifts of small value, if

given periodically to different persons presents of small value.

THE FOLLOWING SHALL NOT BE

UNDERSTOOD TO MEAN THE SALE

OF GOODS AND SERVICES

12/54

TAXPAYER

A taxpayer shall mean a person that is selling goods and services or

importing goods independently in the scope of its business as lasting

activity of a producer, merchant or provider of services that is

pursued for the purpose of generating income

A business activity is a continuous operation of the manufacturer, dealer or

service provider for the purpose of earning income, including the activities

of exploitation of natural resources, agriculture, forestry and self-

employment.

The Republic of Serbia, authorities and legal entities

13/54

TAX DEBTOR

Taxpayer

Tax Representative

Recipient of goods and services, if the foreign person does not

appoint a tax representative, and in other cases stipulated by

the Law

Person who states the VAT in an invoice or other document

serving as the invoice, and who is not subject to VAT or did

not perform the supply of goods and services

A person who imports goods

14/54

TAX BASE

The tax base in the case of sale of goods and services shall be the

price (in money, things or services) received or to be received by

the taxpayer for the goods delivered or services rendered.

15/54

ONSET OF TAX LIABILITY

Tax liability shall run from the date of completion of

the earliest of the following operations:

Sale of goods and services;

Collection of payment;

Onset of the duty to pay customs debt.

16/54

TAX RATE

The general VAT rate 20%;

The special VAT rate 10% (applies mainly to the

existential products - food, medicines, means of

agricultural production, utilities, services in the field

of culture, passenger transport, etc.).

17/54

TAX EXEMPTIONS

With the Right to Deduct Input Tax (Article 24 of VAT

law)

Without Right to Deduction of Input Tax (Article 25 of

VAT law)

Tax Exemptions in the Importing of Goods (Article 26 of

VAT law)

18/54

INPUT TAX

The input tax shall be the amount of VAT assessed in

the input stage of the sale of goods and services,

which the taxpayer may deduct from the VAT owed;

Requirements for Deduction of Input Tax;

Previous tax is deducted from the VAT owed to the

same tax period, under the conditions and in the

manner established by the Law on VAT.

19/54

PROPORTIONAL TAX DEDUCTION

The percentage of proportional tax deduction for the tax period

shall be established by relating the sale of goods and services

to the right to deduction of input tax in which VAT is not

included and the total sales of goods and services in which

VAT is not included, effected from 1 January of the current

year to expiration of the tax period for which the tax

declaration is filed.

The proportionate tax deduction shall be worked out by

applying the percentage of the proportionate tax deduction to

the amount of input tax in the previous taxation period

20/54

SPECIAL TAXATION PROCEDURE

Small taxpayers - taxpayers with an annual turnover of

less than 8 million (around 65.000 EUR);

Farmers;

Tourist Agency;

Second-hand Goods, Works of Art, Collector Pieces and

Antiques.

21/54

REGISTRATION OF TAXPAYER

A taxpayer whose sales totaled more than 8.000.000 dinars

(about 65.000 EUR) in the previous 12 months shall file with

the competent tax office an application for registration before

expiration of the first deadline for filing the interim tax

declaration.

The right to opt for the obligation to pay VAT has a small

taxpayer, whose total turnover in the preceding 12 months is

not more than 8.000.000 dinars, including farmers.

22/54

DUTIES OF TAXPAYERS

It shall be the duty of a taxpayer to do as follows:

Present the registration form;

Issue bills for the goods and services sold;

Keep records in accordance with this Law;

Assess and pay the VAT and file tax declarations.

23/54

TAXATION PERIOD

The taxation period, for which VAT is assessed, the tax

declaration is filed and VAT is paid is

• calendar month in the case of a taxpayer whose sales totaled

more than 50.000.000 dinars in the previous 12 months

• calendar quarter in the case of a taxpayer whose sales totaled

less than 50.000.000 dinars in the previous 12 months

24/54

TAX DECLARATION FILING, VAT

ASSESSMENT AND PAYMENT

The tax return is submitted in electronic form:

within 15 days after the end of the tax period - calendar

month,

20 days after the end of the tax period - calendar quarter.

VAT is paid within the time limits for filing a tax return.

25/54

TAX LIABILITY

The obligation under the VAT is equal to the difference

between the total amount of tax liability and the amount of

input tax:

If the difference is positive, the taxpayer pays VAT;

If the difference is negative, the taxpayer is entitled to a

refund or a tax credit.

26/54

TAX REFUND AND REBATE

VAT REFUND

45 DAYS (general case);

15 days for taxpayers who mainly export goods.

VAT REBATE

to Foreign taxpayers (under condition of reciprocity),

Humanitarian Organisations;

Diplomatic and consular missions and international

organizations;

Foreign citizens.

27/54

LEVEL OF ACHIEVED

HARMONIZATION AND FURTHER

STEPS

Legislation governing the VAT taxation of consumption in

the Republic of Serbia, are partially harmonized with the EU

acquis governing this area.

Further harmonization of legislation will be conducted in the

forthcoming period.

28/54

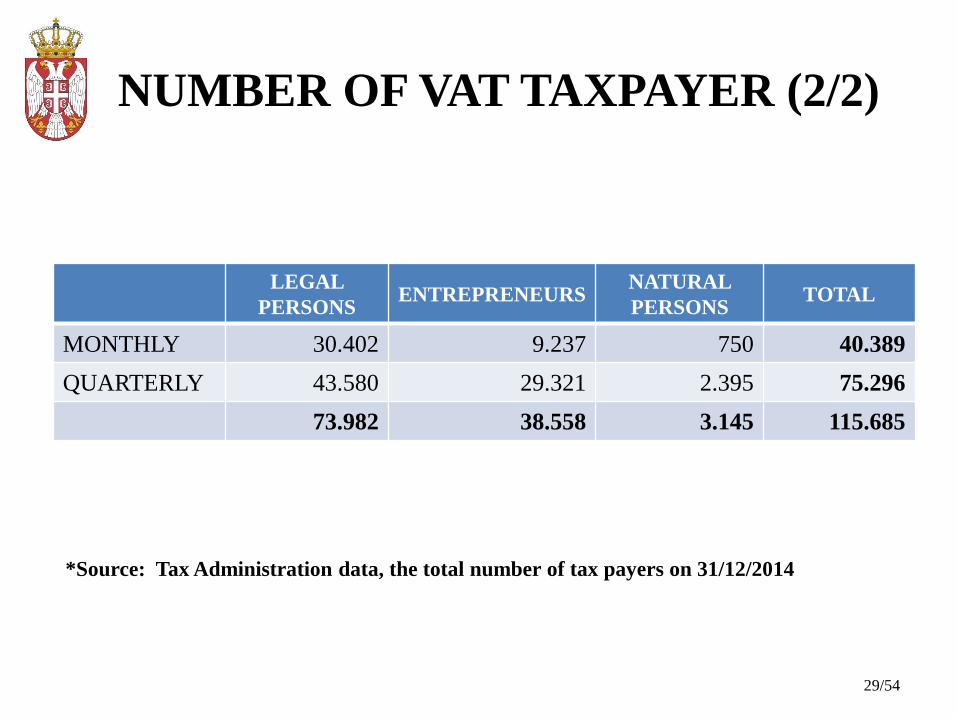

NUMBER OF VAT TAXPAYER (1/2)

Source: Tax Administration data (31/12/2014)

29/54

NUMBER OF VAT TAXPAYER (2/2)

LEGAL

PERSONS ENTREPRENEURS

NATURAL

PERSONS TOTAL

MONTHLY 30.402 9.237 750 40.389

QUARTERLY 43.580 29.321 2.395 75.296

73.982 38.558 3.145 115.685

*Source: Tax Administration data, the total number of tax payers on 31/12/2014

30/54

REGISTER OF VAT PAYERS

31/54

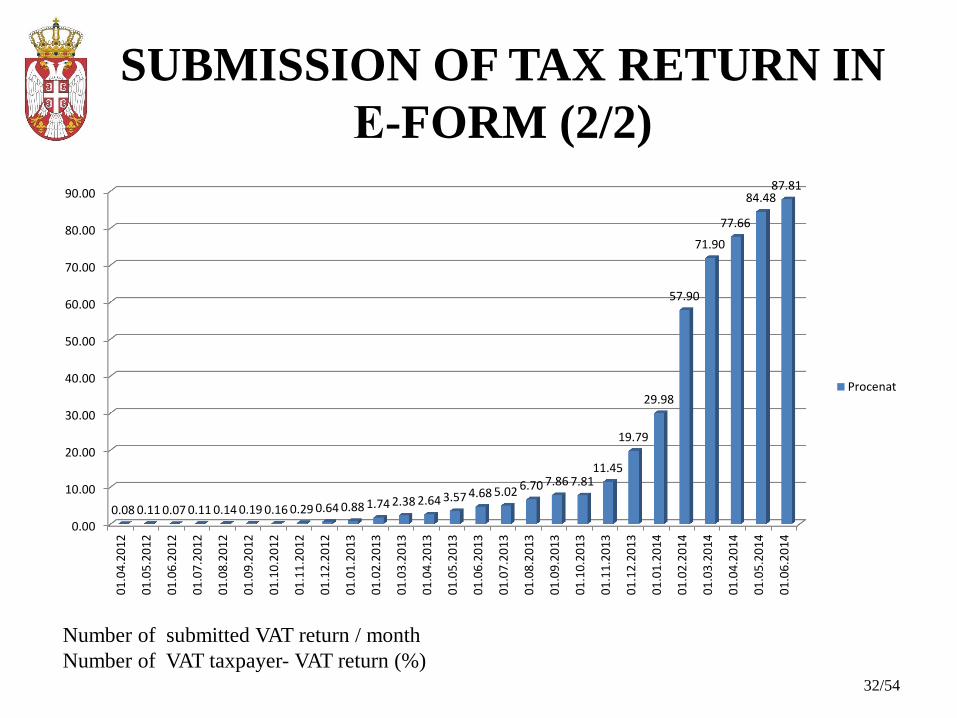

SUBMISSION OF TAX RETURN

IN Е-FORM (1/2)

Since 2008. taxpayers of Centre for large taxpayers

(CLTP) submitt tax returns electronically;

Since 01.07.2014. Vat tax returns (PPPDV) have only

been submitted electronically

32/54

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

01

.04

.20

12

01

.05

.20

12

01

.06

.20

12

01

.07

.20

12

01

.08

.20

12

01

.09

.20

12

01

.10

.20

12

01

.11

.20

12

01

.12

.20

12

01

.01

.20

13

01

.02

.20

13

01

.03

.20

13

01

.04

.20

13

01

.05

.20

13

01

.06

.20

13

01

.07

.20

13

01

.08

.20

13

01

.09

.20

13

01

.10

.20

13

01

.11

.20

13

01

.12

.20

13

01

.01

.20

14

01

.02

.20

14

01

.03

.20

14

01

.04

.20

14

01

.05

.20

14

01

.06

.20

14

0.08 0.11 0.07 0.11 0.14 0.19 0.16 0.29 0.64 0.88 1.74 2.38 2.64 3.57 4.68 5.02 6.70 7.86 7.81 11.45

19.79

29.98

57.90

71.90

77.66

84.48 87.81

Procenat

Number of submitted VAT return / month

Number of VAT taxpayer- VAT return (%)

SUBMISSION OF TAX RETURN IN

Е-FORM (2/2)

33/54

GENERAL ADMINISTRATIVE

CAPACITY OF TAX ADMINISTRATION

LEGAL BASE

The Law on Tax Procedure and Tax Administration („Official

Gazette Of RS”, no. 80/02, 84/02 - corrigendum, 23/03 - corrigendum, 70/03, 55/04,

61/05, 85/05 – other law, 62/06 – other law, 61/07, 20/09, 72/09 – other law, 53/10,

101/11, 2/12 - corrigendum, 93/12, 47/13, 108/13 and 68/14, 105/14)

Rulebook on the internal organization and job classification in

the Ministry of Finance – Tax Administration (08 No: 112-01-1/221-1-

2013 as of 08.04.2013., with amendments and supplements 08 No: 112-01-3/105-1-

2013 as of 28.10.2013., 08 No: 112-01-1/79-1-2014 as of 05.03.2014. and 08 No:

112-01-1/452-1-2014 as of 26.09.2014.)

34/54

TAX ADMINISTRATION

ORGANIZATIONAL CHART

Director

Headquarter (regional departments)

Branch А

Sub-branches

Branch B

Sub-branches

Branch C

Sub-branches

CLTP

Deputy Director

35/54

Director General

Audit Sector

Collection Sector

Tax Police Sector

Sector for Exchange

and Foreign

Exchange Affairs and Games of Chance

Tax-legal Affairs and Coordination Sector

Transformation

Sector

Human resources

Sector

Education, Communication and Internatio

nal Cooperatio

n Sector

Material Resources

Sector ICT Sector

Deputy Director

Director General Office

Group for strategy, planning and risk management

Department for Internal Control and Administrative Surveillance

group for internal audit

TAX ADMINISTRATION

ORGANIZATIONAL CHART HEADQUARTER

36/54

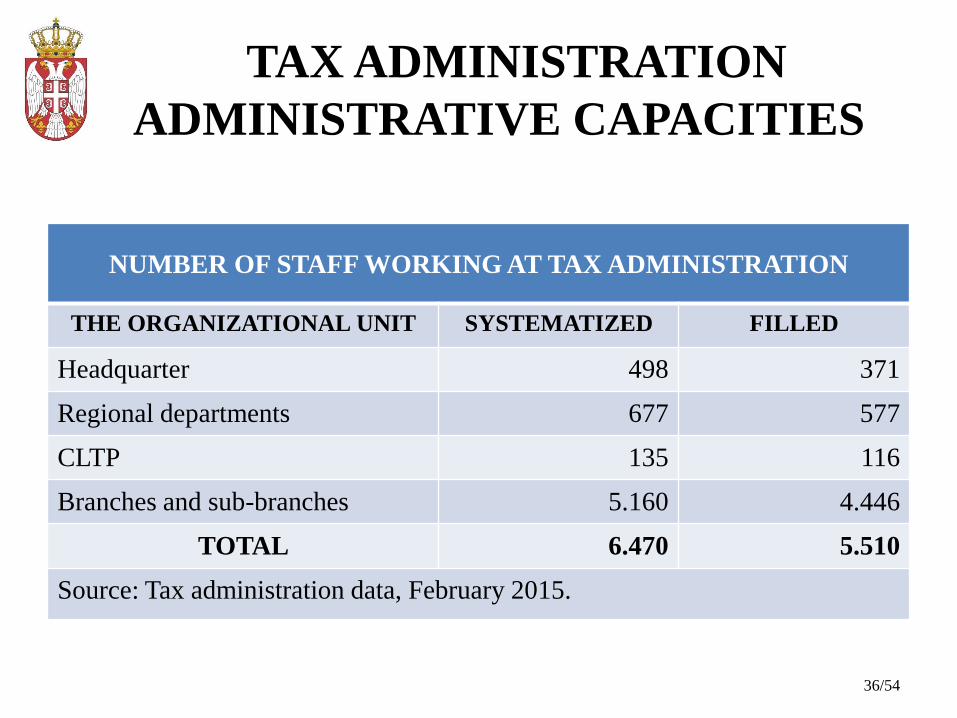

TAX ADMINISTRATION

ADMINISTRATIVE CAPACITIES

NUMBER OF STAFF WORKING AT TAX ADMINISTRATION

THE ORGANIZATIONAL UNIT SYSTEMATIZED FILLED

Headquarter 498 371

Regional departments 677 577

CLTP 135 116

Branches and sub-branches 5.160 4.446

TOTAL 6.470 5.510

Source: Tax administration data, February 2015.

37/54

AUDIT SECTOR

ORGANIZATIONAL CHART

AUDIT SECTOR

Department for planning and methodology for direct taxes

Division for planning and methodology for indirect taxes

Department

for operative tasks

Division for performance measurement, quality assurance

and technical support

Department

for Registers

Department for risk analysis, exemptions and VAT refund

38/54

ADMINISTRATIVE CAPACITIES

OF TAX CONTROL

NUMBER OF STAFF WORKING ON TAX CONTROL ACTIVITIES

ORGANIZATIONAL UNIT SYSTEMATIZED FILLED

Headquarter 62 42

Regional departments 46 37

Centre for Large Taxpayers 62 54

Branches and sub-branches 2.433 2.103

Total 2.603 2.236

Around 40% of the total number of Tax Administration staff

is working on tax control activities.

VAT control perform 480 tax inspectors

Source: Data obtained from Tax Administration, February 2015

39/54

COLLECTION SECTOR

ORGANIZATIONAL CHART

COLLECTION

SECTOR

Collection

Department

Tax accounting Department

40/54

ADMINISTRATIVE CAPACITIES

OF TAX COLLECTION

NUMBER OF STAFF WORKING ON PAYMENT COLLECTION AND

TAX ACCOUNTING

ORGANIZATIONAL UNIT SYSTEMATIZED FILLED

Headquarter 24 22

Regional departments 42 39

Centre for Large Taxpayers 26 24

Branches and sub-branches 1.938 1.669

TOTAL 2.030 1.754

Around 30% of the total number of Tax Administration staff is working on payment

collection and tax accounting activities.

Data source: Tax Administration, February, 2015

41/54

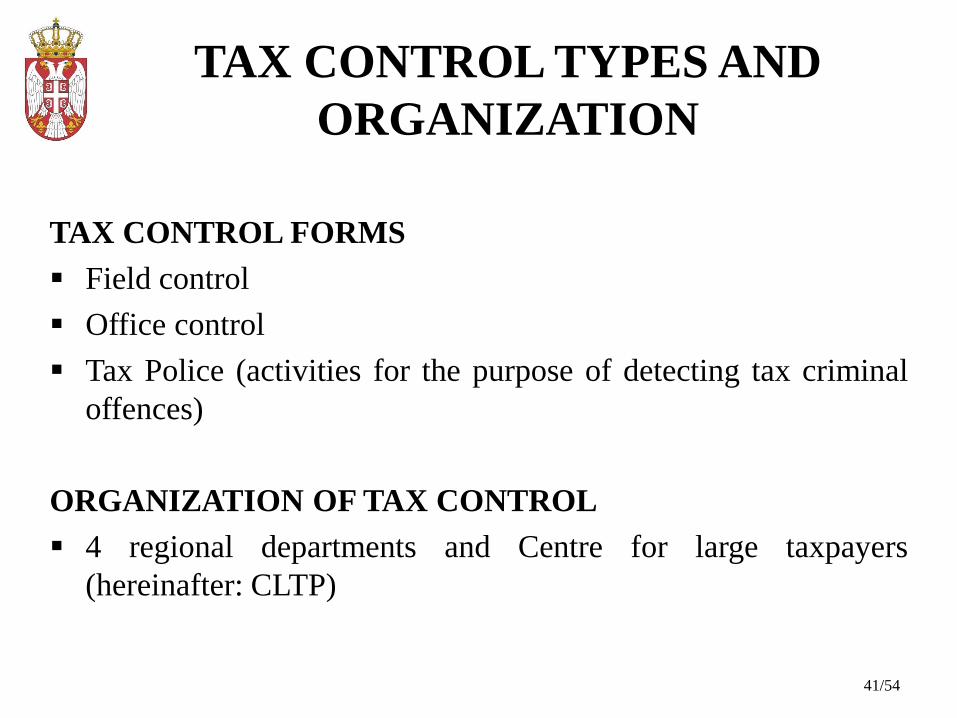

TAX CONTROL TYPES AND

ORGANIZATION

TAX CONTROL FORMS

Field control

Office control

Tax Police (activities for the purpose of detecting tax criminal

offences)

ORGANIZATION OF TAX CONTROL

4 regional departments and Centre for large taxpayers

(hereinafter: CLTP)

42/54

CONTROL PROCEDURE (1/2)

Performs the tax inspector on the basis of control order

By control order are determinized term and subject matter

of control.

VAT control is carrying out:

– within the regular control of taxpayer business;

– control fulfilled requests for VAT refund.

43/54

CONTROL PROCEDURE (2/2)

According to a determined fakts, tax inspector makes the

minutes on control and serves it to taxpayer.

Taxpayer shall submit objections in 5 days in office control,

i.e. 8 days in field control.

Appeal may be filed in 15 days from the day of receiving the

decision.

Possibility to initiate an administrative dispute proceeding.

If irregularities in control procedure

Minute Decision

44/54

PLANS OF AUDIT SECTOR

Training of tax inspectors in various fields;

Intensified control of medium and large legal entities;

Gradual increase of selection centralization of cases for control – at the

Headquarter of Tax Administration 80% of working hours of available

inspectors will be planned;

Activities in the sense of taxpayers assessment based on their size, type of

business operation and form of organization as well as defining new criteria;

Actions related to updating the list of criteria required for selecting taxpayers

for control of VAT refund and tax credit, the request for VAT return of which

will be the subject of controls. The updated criteria are integrated in the

application software the entire production of which is expected by the end of

February 2015.

Increasing activity regarding the suppression grey economy

45/54

PLANS - BUILDING

ADMINISTRATIVE CAPACITY

PLANED PROJECTS

Building administrative capacity

VAT Information Exchange Systems (Vies)

Vat System On E-services

Vat Refund System

Е-forms

М1ss -Mini One-stop Shop System

THESE PROJECTS WILL BE IMPLEMENTED

THROUGH IPA PROGRAM

46/54

TAX DEBT COLLECTION

Tax Administration enforces the following:

Regular collection and

Enforced collection of tax debt.

47/54

REGULAR COLLECTION

OF TAX DEBT(1/3)

Regular tax collection of VAT is performed by paying the due

tax on the prescribed accounts of public revenues, within the

time limits prescribed by the Law.

For monthly VAT payers deadline for payment is 15 days after

the end of the previous month, and for quarterly VAT payers

deadline for payment is 20 days after the end of the previous

quarter.

48/54

In case the taxpayer fails to pay the due VAT in entirety or

partially, Tax Administration shall issue a Tax Payment

Notice.

The taxpayer shall be ordered by the notice to immediately

pay the tax referred to in the notice and not later than 5 days

from receiving the notice.

REGULAR COLLECTION

OF TAX DEBT (2/3)

49/54

The notice includes an advice intended for the taxpayer

stating that Tax Administration will start enforced collection

of tax debt, in case the tax debt referred to in the notice is not

paid within the time limit referred to in the notice, or in case

the request for tax debt reprogram is not filed within the same

time limit.

The notice includes an advice intended for the taxpayer

stating that he must resolve all disputable issues with Tax

Administration within 5 days.

REGULAR COLLECTION

OF TAX DEBT (3/3)

50/54

ENFORCED COLLECTION

Enforced collection of VAT debt is started by Tax

Administration by passing the ruling on determining the

enforced collection procedure, in terms of the unpaid tax debt

referred to in the warning;

Enforced collection of tax debt is conducted in terms of the

following objects of enforced collection: pecuniary assets

(blocked accounts); real estate; movables; pecuniary and non-

pecuniary claims; wages; cash and securities.

Tax Administration may conduct enforced collection

concurrently in terms of several objects of enforced collection.

51/54

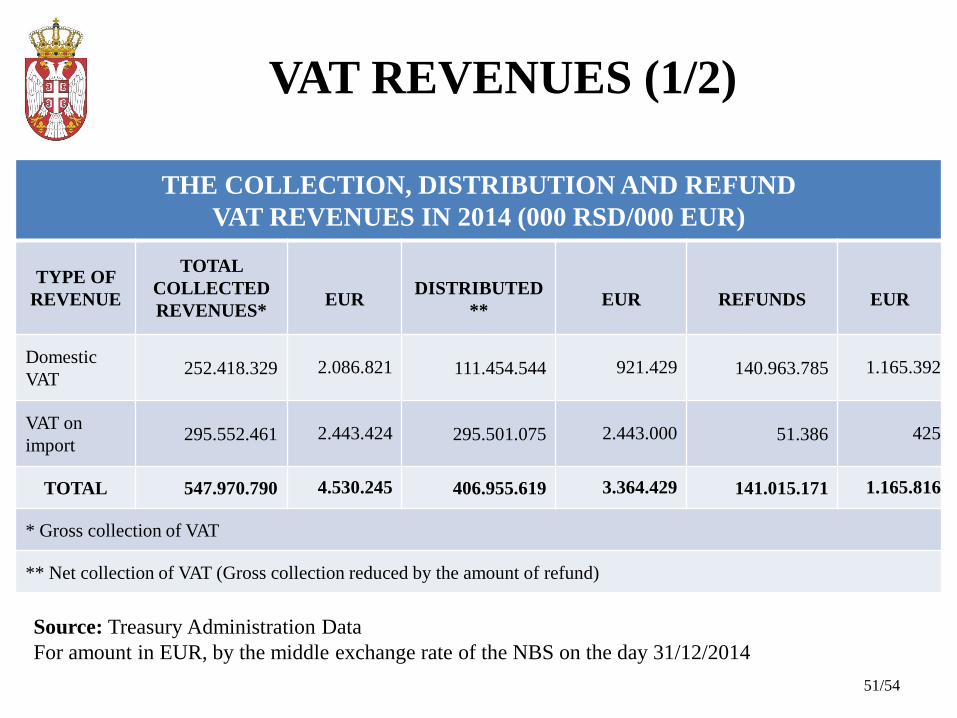

VAT REVENUES (1/2)

THE COLLECTION, DISTRIBUTION AND REFUND

VAT REVENUES IN 2014 (000 RSD/000 EUR)

TYPE OF

REVENUE

TOTAL

COLLECTED

REVENUES*

EUR

DISTRIBUTED

**

EUR

REFUNDS

EUR

Domestic

VAT 252.418.329 2.086.821 111.454.544 921.429 140.963.785 1.165.392

VAT on

import 295.552.461 2.443.424 295.501.075 2.443.000 51.386 425

TOTAL 547.970.790 4.530.245 406.955.619 3.364.429 141.015.171 1.165.816

* Gross collection of VAT

** Net collection of VAT (Gross collection reduced by the amount of refund)

Source: Treasury Administration Data

For amount in EUR, by the middle exchange rate of the NBS on the day 31/12/2014

52/54

VAT REVENUES (2/2)

ANALYSIS OF TOTAL REVENUE FROM VAT IN 2014

(000 RSD/000 EUR)

TOTAL COLLECTED

REVENUES FROM VAT

AMOUNT IN

RSD

AMOUNT IN

EUR

STRUCTURE

(%)

On the territory of the

Republic of Serbia

252.418.329 2.086.821

46,06

On import 295.552.461 2.443.424 53,94

TOTAL 547.970.790 4.530.245 100,00

Source: Treasury Administration Data

For amount in EUR, by the middle exchange rate of the NBS on the day 31/12/2014.

53/54

PLANS OF COLLECTION SECTOR

STREIGHTENING OF ADMINISTRATIVE

CAPACITY

MAINTAING THE TREND OF THE VAT

COLECTION

54/54

Thank you for your attention!

QUESTIONS?