vanguard’s approach to constructing diversified funds

TRANSCRIPT

Vanguard’s approach to constructing Diversified Funds

Executive summary. Vanguard Diversified Funds are designed to address a particular challenge facing many investors: constructing a professionally managed diversified portfolio for longer time horizons.

When it comes to portfolio construction, many investors lack the time or interest and can become overwhelmed by the choice of investment options, asset classes, and other portfolio implementation hurdles such as rebalancing regularly. Investors also face behavioural risks in adhering to their investment plan over time due to the temptation of performance chasing or overreacting to market events. Vanguard’s Diversified Funds provide portfolio solutions designed to help long-term investors achieve their goals and overcome these challenges. They are constructed on a number of investment best practices – the principles of asset allocation, diversification and transparency, and the maintaining of a balance among risk, return, and cost.

This paper provides an overview of Vanguard’s framework for designing its Diversified Funds in Australia. We explain the rationale for the asset allocation of the funds and discuss the importance of some key implementation considerations, such as the use of indexed versus active strategies and the importance of rebalancing.

Authors

Roger Aliaga-Díaz, PhD

Paul W. Chin, F Fin

Vijay A. Murik, PhD

Vanguard research August 2013

Connect with Vanguard™The indexing specialist > vanguard.com.au > 1300 655 102

2

Defining investment goals and objectives

A sound investment plan for individuals begins with an outline of objectives, as well as any significant constraints. Most investment objectives are straightforward: saving for retirement, preserving assets, funding a pension plan or funding a large expense such as buying a house or paying for university education. Constraints facing investors are their tolerance for risk and the time horizon of the investment.1 As investment solutions, the Diversified Funds should offer portfolio options that are flexible enough to accommodate different constraints, allowing for a reasonable range of risk tolerances and time horizons.

While differences in investment horizons, degrees of risk aversion and age are all key considerations for the design of the Diversified Funds, ultimately the key objective of these single-fund solutions is to maximise the chances of investment success by aiming for return outcomes over the long term that are commensurate with the level of risk assumed.

Some investors with shorter-term financial goals or extremely low risk tolerances may find cash or other low-volatility vehicles to be a suitable investment for their entire portfolio. But the reality is that a large majority of Australian investors may need to accept some market risk in order to adequately save towards their investment goals.

Vanguard Diversified Funds have been engineered for investors with a desire to outperform inflation during their investing years. Investment portfolios with a high allocation to cash-like investments carry significant risks in terms of their ability to meet many investors’ financial goals. While cash offers capital stability and liquidity with marginal returns in the short term, fixed income provides an income stream, potential for capital growth in the medium to long term, and diversification to growth assets due to its imperfect correlation to equities.

Over the long term, fixed income generally yields a higher return than cash. Figure 1 notes the existence of a material risk premium for local equities and local fixed income over cash, accompanied with higher volatility. The higher expected level of returns on fixed income securities over cash reflects compensation to investors for taking on interest rate, credit, inflation and liquidity risk.

1 Different situations of individual investors may also call for additional constraints related to liquidity needs, legal issues and even desire to avoid certain types of investments entirely.

Figure 1 Historical risk premium over cash.

5.3%

0.9%

12.3%

6.2%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0%

Aus Equities Aus Bonds

Exc

ess

retu

rn v

olat

ility

(sta

ndar

d de

viat

ion)

Ris

k pr

emiu

m (r

elat

ive

to c

ash)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0%

Aus Equities Aus Bonds

Exc

ess

retu

rn v

olat

ility

(sta

ndar

d de

viat

ion)

Ris

k pr

emiu

m (r

elat

ive

to c

ash)

4.7%

1.1%

11.9%

5.7%

Excess return (relative to cash) Risk relative to cash (standard deviation) - RHS

Australian markets 1963-2013 Australian markets 2003-2013

Excess return (relative to cash) Risk relative to cash (standard deviation) - RHS

Note: Aus Equities references the All Ordinaries Accumulation Index, Aus Bonds references 10-year Aus government bonds and cash references bank bills. As of 8 August 2013, 10yr Aus Govt Bonds Yield = 3.67% and 90-day bank bills yield = 2.60% (for a premium of 1.07%).

Source: Vanguard’s Investment Strategy Group, based on data from Credit Suisse from June 1963 to June 2013.

3

A common misconception in portfolio construction is that a high allocation to cash is recommended in an environment of rising interest rates (i.e. shortening the duration of the bond portfolio). However, this recommendation misses the fact that interest rate risk is a symmetric risk around the expected path of interest rates. That is, if most bond investors and market participants expect interest rates to increase, then that common view about rates will already be priced by the bond market and factored into the level and shape of the yield-maturity curve of government bonds. Thus, if interest rates do increase as expected, then bond portfolios of different durations (long-term bonds, short-term bonds and cash) should break even (i.e. perform equally) (see Steinfort, 2013).

Only if interest rates were to increase more than anticipated would short bonds and cash outperform a long-duration portfolio. However, equally likely, interest rates could increase at a lower rate than anticipated, in which case the long-duration portfolio would outperform. Given the general expectation of rising rates, the probability of a positive or a negative surprise relative to that expectation is nothing more than a coin toss. Thus, from a strategic asset allocation (SAA) perspective, there are no expected benefits of shortening duration even if interest rates are expected to go up.

Broad asset-class allocation

The portfolio construction process of the Diversified Funds follows a top-down hierarchy that starts by defining the allocations at the level of broad asset classes (equities, fixed income and cash) and then continues with the weightings of the various specific assets (such as domestic versus international equities or bonds) and market sectors (such as value stocks, small caps, government bonds or credit).

In portfolios with broadly diversified holdings, the broad mixture of asset classes will determine the majority of the returns and their variability over time. Vanguard research covering the US, Canada and the UK equity markets shows that it is the broad asset allocation decision that drives the vast majority of portfolio return and movement, rather than market-timing or stock-selection pursuits. This conclusion is consistent with analysis on Australian data, as depicted in Figure 2.

Thus, from a SAA perspective, the broad allocations to cash, income (fixed income) and growth (equities) are the main determinants of the risk-return profiles of the Diversified Funds’ portfolios.

Figure 3 shows the full range of cash, income and growth splits increasing with the level of volatility of the portfolios. Any combination of cash, growth and income assets shown in Figure 3 represents a portfolio that is most likely to yield maximum diversification benefits and the best possible returns for the level of risk assumed. More risky portfolios are expected to yield higher return as a compensation for bearing the extra risk.2

The selection of specific portfolio options should feature enough variety to cover a wide array of risk tolerances and investment horizons that different investors may have. For example, a more conservative portfolio (such as Diversified Fund 1 in the chart) would allocate around 70% of the portfolio towards fixed income assets while a more aggressive asset allocation (such as Diversified Fund 3) would feature around

2 Vanguard Diversified Funds do not rely exclusively on this sort of quantitative calculation to derive their asset allocation.There are significant (and well-known) limitations to the use of simplistic mean-variance optimisation and efficient-frontiers methods to derive portfolios, including parameter instability, structural breaks in the data and regime changes, just to name a few. The danger of relying blindly on these tools is that they may give a false sense of precision, when in reality their portfolio recommendations depend entirely on arbitrary assumptions about the key inputs into the optimisation exercise.

Figure 2 Role of asset allocation policy in return variation of balanced funds.

Source: The global case for strategic asset allocation (Wallick et al., 2012)

Asset allocationSecurity selection and market timing

90%

10%

4

70% weight toward growth assets. A balanced portfolio would probably fall in the middle of the previous two (such as Diversified Fund 2) with a 50%/50% allocation.

Specific asset allocation

Once the broad strategic asset-class allocation of the Diversified Funds portfolios has been determined, the focus turns to building diversified asset exposures within the broad asset categories. This is a critical step in order to reduce risks associated with a particular company, sector, or market segment.

In practice, diversification takes place as different market segments or individual securities behave differently from each other at any given time. Vanguard believes that the best way to incorporate these diversification benefits in the Diversified Funds portfolios is via a market-cap weighted exposure to all the segments of the market (Donaldson et al, 2013).3

The allocation between Australian markets and non-Australian securities (both for bonds and

equities) adds another important dimension to the diversification benefits in the Diversified Funds. A global asset allocation can reduce risks associated with domestic market sector concentration, issuer concentration and low market liquidity, to name a few (Steinfort and Chin, 2013).

Asset composition within the growth split

The asset allocation within the growth split of Vanguard Diversified Funds follows the principle of market-cap-weighted exposure to the entire Australian equity market.

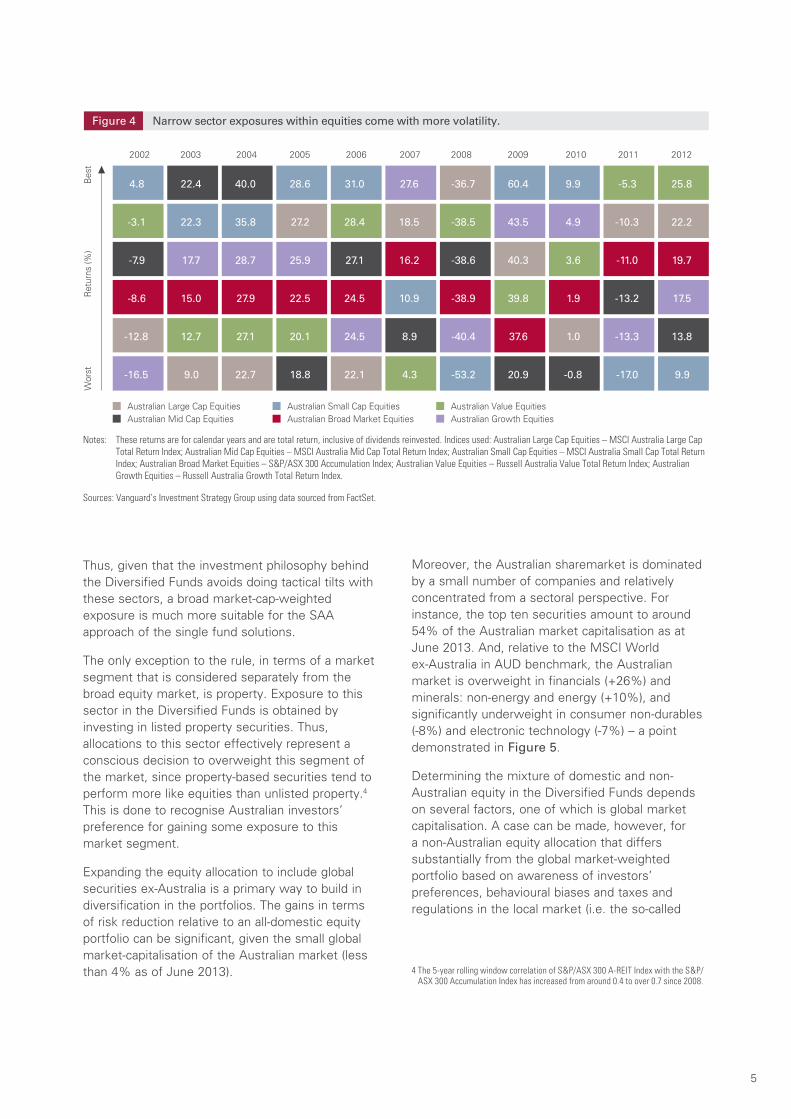

Figure 4 shows that the relative performance of any given sector of the Australian equity market changes year to year, sometimes significantly. In contrast, the broad market index dissects these options, and offers a consistent average outcome over all periods.

The growth and income splits are the main determinant of portfolios’ risk-return profile. Figure 3

0

10

20

30

40

50

60

70

80

90

100%

0.4 0.6 1.0 1.4 1.8 2.2 2.7 3.1 3.5 4.0 4.5 5.1 5.7 6.4 7.0 7.7 8.4 9.1 9.8 10.5

Por

tfol

io w

eigh

ts

Annualised Standard Deviation

'

DiversifiedFund 1

'

DiversifiedFund 2

'

DiversifiedFund 3

'

DiversifiedFund 4

'

Note:

Source: Vanguard’s Investment Strategy Group.

GrowthIncomeCash

Colour areas represent optimal portfolio weights across cash/income/growth for a given level of risk. The portfolios were calculated as follows: 1) Benchmark returns for each of the sub-asset classes are weighted to form cash/income/growth asset returns. Sub-asset class weights are consistent with Vanguard Diversified Fund weights (see the appendix for details); 2) Risk/return metrics are calculated for cash/income/growth. Risk is based on historical covariance matrix (1993-2012). Returns are based 10-year expected returns (Cash=45%, Income=5.5% and Growth=9.1%); and 3) Portfolio returns are optimised using mean variance optimisation across cash/income/growth assets for a given level of risk.

3 A market cap-weighted index reflects the consensus estimation of each company’s value at any given moment. In any efficient market, new information affects the price of one or more securities and is reflected instantaneously in an index via the change in market capitalisation. Because current prices (and, hence, company values) are set based on current and expected events, market cap-weighted indices represent the expected, theoretically mean-variance-efficient, portfolio of securities in a given asset class (Philips, 2012).

5

Thus, given that the investment philosophy behind the Diversified Funds avoids doing tactical tilts with these sectors, a broad market-cap-weighted exposure is much more suitable for the SAA approach of the single fund solutions.

The only exception to the rule, in terms of a market segment that is considered separately from the broad equity market, is property. Exposure to this sector in the Diversified Funds is obtained by investing in listed property securities. Thus, allocations to this sector effectively represent a conscious decision to overweight this segment of the market, since property-based securities tend to perform more like equities than unlisted property.4 This is done to recognise Australian investors’ preference for gaining some exposure to this market segment.

Expanding the equity allocation to include global securities ex-Australia is a primary way to build in diversification in the portfolios. The gains in terms of risk reduction relative to an all-domestic equity portfolio can be significant, given the small global market-capitalisation of the Australian market (less than 4% as of June 2013).

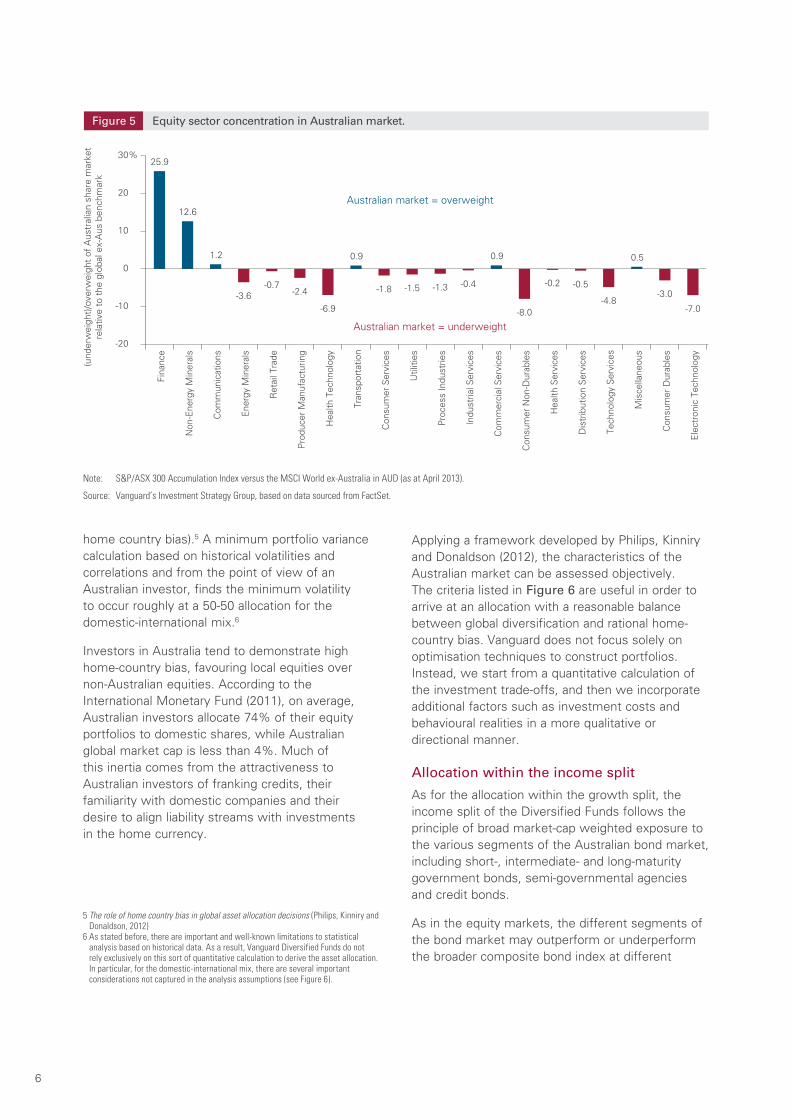

Moreover, the Australian sharemarket is dominated by a small number of companies and relatively concentrated from a sectoral perspective. For instance, the top ten securities amount to around 54% of the Australian market capitalisation as at June 2013. And, relative to the MSCI World ex-Australia in AUD benchmark, the Australian market is overweight in financials (+26%) and minerals: non-energy and energy (+10%), and significantly underweight in consumer non-durables (-8%) and electronic technology (-7%) – a point demonstrated in Figure 5.

Determining the mixture of domestic and non-Australian equity in the Diversified Funds depends on several factors, one of which is global market capitalisation. A case can be made, however, for a non-Australian equity allocation that differs substantially from the global market-weighted portfolio based on awareness of investors’ preferences, behavioural biases and taxes and regulations in the local market (i.e. the so-called

Narrow sector exposures within equities come with more volatility.Figure 4

Notes: These returns are for calendar years and are total return, inclusive of dividends reinvested. Indices used: Australian Large Cap Equities – MSCI Australia Large Cap Total Return Index; Australian Mid Cap Equities – MSCI Australia Mid Cap Total Return Index; Australian Small Cap Equities – MSCI Australia Small Cap Total Return Index; Australian Broad Market Equities – S&P/ASX 300 Accumulation Index; Australian Value Equities – Russell Australia Value Total Return Index; Australian Growth Equities – Russell Australia Growth Total Return Index.

Sources: Vanguard’s Investment Strategy Group using data sourced from FactSet.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Ret

urns

(%)

Wor

stB

est

Australian Broad Market EquitiesAustralian Value EquitiesAustralian Growth EquitiesAustralian Mid Cap Equities

Australian Small Cap EquitiesAustralian Large Cap Equities

4.8 22.4 40.0 28.6 31.0 27.6 -36.7 60.4 9.9 -5.3 25.8

-3.1 22.3 35.8 27.2 28.4 18.5 -38.5 43.5 4.9 -10.3 22.2

-7.9 17.7 28.7 25.9 27.1 16.2 -38.6 40.3 3.6 -11.0 19.7

-8.6 15.0 27.9 22.5 24.5 10.9 -38.9 39.8 1.9 -13.2 17.5

-12.8 12.7 27.1 20.1 24.5 8.9 -40.4 37.6 1.0 -13.3 13.8

-16.5 9.0 22.7 18.8 22.1 4.3 -53.2 20.9 -0.8 -17.0 9.9

4 The 5-year rolling window correlation of S&P/ASX 300 A-REIT Index with the S&P/ASX 300 Accumulation Index has increased from around 0.4 to over 0.7 since 2008.

6

home country bias).5 A minimum portfolio variance calculation based on historical volatilities and correlations and from the point of view of an Australian investor, finds the minimum volatility to occur roughly at a 50-50 allocation for the domestic-international mix.6

Investors in Australia tend to demonstrate high home-country bias, favouring local equities over non-Australian equities. According to the International Monetary Fund (2011), on average, Australian investors allocate 74% of their equity portfolios to domestic shares, while Australian global market cap is less than 4%. Much of this inertia comes from the attractiveness to Australian investors of franking credits, their familiarity with domestic companies and their desire to align liability streams with investments in the home currency.

Applying a framework developed by Philips, Kinniry and Donaldson (2012), the characteristics of the Australian market can be assessed objectively. The criteria listed in Figure 6 are useful in order to arrive at an allocation with a reasonable balance between global diversification and rational home-country bias. Vanguard does not focus solely on optimisation techniques to construct portfolios. Instead, we start from a quantitative calculation of the investment trade-offs, and then we incorporate additional factors such as investment costs and behavioural realities in a more qualitative or directional manner.

Allocation within the income split

As for the allocation within the growth split, the income split of the Diversified Funds follows the principle of broad market-cap weighted exposure to the various segments of the Australian bond market, including short-, intermediate- and long-maturity government bonds, semi-governmental agencies and credit bonds.

As in the equity markets, the different segments of the bond market may outperform or underperform the broader composite bond index at different

Figure 5 Equity sector concentration in Australian market.

25.9

12.6

1.2

-3.6-0.7

-2.4

-6.9

0.9

-1.8 -1.5 -1.3 -0.4

0.9

-8.0

-0.2 -0.5

-4.8

0.5

-3.0

-7.0

-20

-10

0

10

20

30%

(und

erw

eigh

t)/o

verw

eigh

t of

Aus

tral

ian

shar

e m

arke

tre

lativ

e to

the

glo

bal e

x-A

us b

ench

mar

k

Australian market = overweight

Australian market = underweight

Fina

nce

Non

-Ene

rgy

Min

eral

s

Com

mun

icat

ions

Ener

gy M

iner

als

Ret

ail T

rade

Prod

ucer

Man

ufac

turin

g

Hea

lth T

echn

olog

y

Tran

spor

tatio

n

Con

sum

er S

ervi

ces

Util

ities

Proc

ess

Indu

strie

s

Indu

stria

l Ser

vice

s

Com

mer

cial

Ser

vice

s

Con

sum

er N

on-D

urab

les

Hea

lth S

ervi

ces

Dis

trib

utio

n Se

rvic

es

Tech

nolo

gy S

ervi

ces

Mis

cella

neou

s

Con

sum

er D

urab

les

Elec

tron

ic T

echn

olog

y

Note: S&P/ASX 300 Accumulation Index versus the MSCI World ex-Australia in AUD (as at April 2013).

Source: Vanguard’s Investment Strategy Group, based on data sourced from FactSet.

5 The role of home country bias in global asset allocation decisions (Philips, Kinniry and Donaldson, 2012)

6 As stated before, there are important and well-known limitations to statistical analysis based on historical data. As a result, Vanguard Diversified Funds do not rely exclusively on this sort of quantitative calculation to derive the asset allocation. In particular, for the domestic-international mix, there are several important considerations not captured in the analysis assumptions (see Figure 6).

7

points in time. Thus, a SAA portfolio that does not intend to dynamically adjust allocations as a function of changing market conditions would be more robust from a diversification perspective by allocating to all sectors of the market proportional to market-cap weights. Figure 7 depicts the dynamic nature year-to-year of sub-asset classes within Australian fixed income.

As discussed with equity sub-asset allocation, an allocation to non-Australian fixed income within the income split provides significant diversification opportunities for the Diversified Funds. Global bonds represent the world’s largest investable asset class currently, comprising about two-thirds of the combined global capitalisation of the equity and bond markets. Thus, with the global share of the

Figure 6 Factors affecting the decision to invest in global assets.

Validate home-bias decision Reduce home bias Assessments

Risk and return impact of adding foreign securities

Limited benefits Significant benefits Historical minimum-variance analysis suggests that the introduction of a diversified international equities portfolio to an Australian equities portfolio can improve the risk-adjusted returns: assessment = material benefits.

Domestic-sector concentration

Unconcentrated Concentrated Figure 5 illustrates the concentrated nature: assessment = concentrated.

Domestic-issuer concentration

Unconcentrated Concentrated The top 10 holdings in the Australian market represent in excess of 50%: assessment = concentrated.

Domestic transaction costs

Low High On a global scale (e.g. comparing the US, the UK and Canada), the Australian market is substantially high (as measured by the comparable bid-ask spreads): assessment = high.

Domestic liquidity High Low On a global scale, liquidity in the Australian market is reasonable: assessment = medium.

Domestic asset taxes Advantages Disadvantages Dividend imputation system supports the holding of Australian equities, especially if an investor is in a low- or zero-tax environment: assessment = advantages.

Source: Vanguard Investment Strategy Group, adapted from Philips (2012).

Figure 7 Individual bond market segments display more volatility than the broad market.

Notes: Calendar year total returns for stated benchmarks. Indices used: Broad – UBS Composite Bond Index; Govt – UBS Government Index; Semi-Govt – UBS Semi Govt Index; Supra/Sov – UBS Supra/Sov Index; Credit – UBS Credit Index; Bank Bills – 0+YR – Index Total Return Level

Source: Vanguard Investment Strategy Group, based on data sourced from FactSet.

9.3 4.9 7.1 6.0 6.0 6.7 17.4 6.1 7.1 12.6 9.8

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

8.8 3.7 7.0 5.8 3.9 3.8 16.2 3.5 6.3 11.7 9.7

7.8 3.0 7.0 5.8 3.1 3.6 15.3 2.3 6.0 11.4 8.1

4.8 2.8 6.9 5.7 2.9 3.5 14.9 1.7 6.0 9.2 7.7

-12.8 12.7 5.6 5.7 2.9 3.2 10.7 1.6 5.8 9.2 6.7

-16.5 9.0 22.7 18.8 2.7 3.2 7.6 0.0 4.7 5.0 4.0

Ret

urns

(%)

Wor

stB

est

Supra/Sov Credit Bank BillsGovt Semi-GovtBroad

8

Australian bond market being around 2% as of 2013 – even a smaller share than the equity market – adding non-Australian bonds should reduce the overall volatility of the portfolios.7

Global treasuries (as represented by the Barclays Global Treasury Index hedged to AUD) cover more than 1,200 investment grade issues; global credit (Barclays Global Aggregate Government-Related and Corporate Index hedged to AUD) covers a wider pool at around 12,000 securities. In both cases the diversification benefits emanate from the underlying exposures which are significantly different from the UBS Composite Bond Index in terms of size of issues, number of issuers, origin of issuers and market conditions. A good example of this is the imperfect correlation of overseas interest rates and inflation with those of Australia.

As with equities, significant departures from global market-cap weightings may be defensible on the grounds of considerations such as behavioural biases, currency hedging costs and risks, or exchange-rate volatility if currency exposures are left unhedged.

Currency exposure and hedging considerations

By investing in global assets – be they equities or bonds – exposure to overseas currencies is created. Vanguard views currency exposures in a portfolio as a source of uncompensated risk to investors, i.e. high volatility with no expected risk premium to be earned in the long term.8 This means that the only consideration behind the decision on whether or not to hedge the currency exposures in the Diversified Funds is the potential reduction of the portfolio risk.

In theory, when addressed from a volatility reduction perspective, the currency exposure decision is done at the portfolio level. The theoretical prescription for optimal currency exposure is for it to be left unhedged when there is a high positive correlation between the Australian dollar and global returns. As shown in Figure 8, over the last 20 years the Australian dollar has tended to

7 Philips (2012) presents data from the IMF’s Coordinated Portfolio Investment Survey for Australia, showing home-country bias in fixed income is even more extreme than in equities. The average Australian investor holds 87% of their bond portfolio in domestic bonds.

8 Similar to the discussion on interest rates, market consensus expectations about either rising or falling currencies should be priced by the markets and factored into security prices. As a result, currency movements that are anticipated by the markets should not impact performance of international assets relative to domestic allocations.

Portfolio volatility, risk impact, and equity-currency correlations over five-year increments.Figure 8

Unhedged portfolio standard deviationHedged portfolio standard deviation

% risk impact

Notes: Annualised standard deviations of equity index returns and the associated risk impact of hedging (represented by the left axis), as well as equity-currency correlations (represented by the right axis), were calculated using the MSCI World Price Index (local), the MSCI World Price Index in AUD, the MSCI World Hedged Index in AUD and the Bank for International Settlements effective exchange rate index (narrow) for Australia with month-end data from June 1993 to June 2013.

Source: Vanguard Investment Strategy Group calculations, based on data from FactSet and MSCI.

Correlation (BIS effective exchange rate, local MSCI World Price Index) RHS

12.3 14.2 10.7 11.711.2 17.5 9.7 17.8-8.6 23.0 -9.7 52.1

0.0

0.3

0.1

0.6

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-30

-20

-10

0

10

20

30

40

50

60

70%

1993–1998 1998–2003 2003–2008 2008–2013

Equ

ity-c

urre

ncy

corr

elat

ions

Port

folio

vol

atili

ty a

nd a

ssoc

iate

d ris

k im

pact

(%)

9

fall against a basket of currencies whenever global equity markets also declined. However, the currency hedging decision is not independent of the underlying asset allocation. Even with a positive currency correlation, the degree of currency hedging should increase in portfolios with a larger allocation to fixed income assets.9

In practice, Vanguard Diversified Funds portfolios arrive at a reasonably efficient currency exposure by constructing the asset allocation with unhedged global equities and with hedged global fixed interest assets.

For fixed income assets, the extra volatility of the currency exposure overwhelms the low volatility character of this asset class even if there are modest diversification benefits from a positive currency correlation. Thus, the standard recommendation is for global fixed income portfolios to be hedged. This is not the case for global equities for which the currency exposure signifies a modest increase in volatility (relative to the usual high volatility of equities) that can be more than compensated by the stronger diversification benefits from a positively correlated currency. Figure 9 shows the currency exposure increasing as we move from income to growth portfolios.

Although historically the correlation between the Australian dollar and global equity markets has been positive on average since the 1990s, we do not expect large risk reduction benefits from the currency exposure. As shown in Figure 8, currency-equity market correlations tend to be statistically unstable and time-varying in nature.

Key implementation aspects for the Diversified Funds

The rebalancing process is essentialVarious asset classes produce different returns over time. If left alone, the allocation weights of the assets in the Diversified Funds can change and cause the asset allocations to drift from their neutral position. This drift may subject investors to more (or less) risk than they originally intended. To ensure the portfolio aligns with its target risk and return characteristics, it must be periodically rebalanced to its intended asset allocation.

Professionally managed single-fund solutions such as the Diversified Funds can help investors adhere to a targeted asset allocation without having to continuously monitor and manually rebalance their portfolios. Although the idea of rebalancing is simple, there are many factors to be considered for its actual implementation.

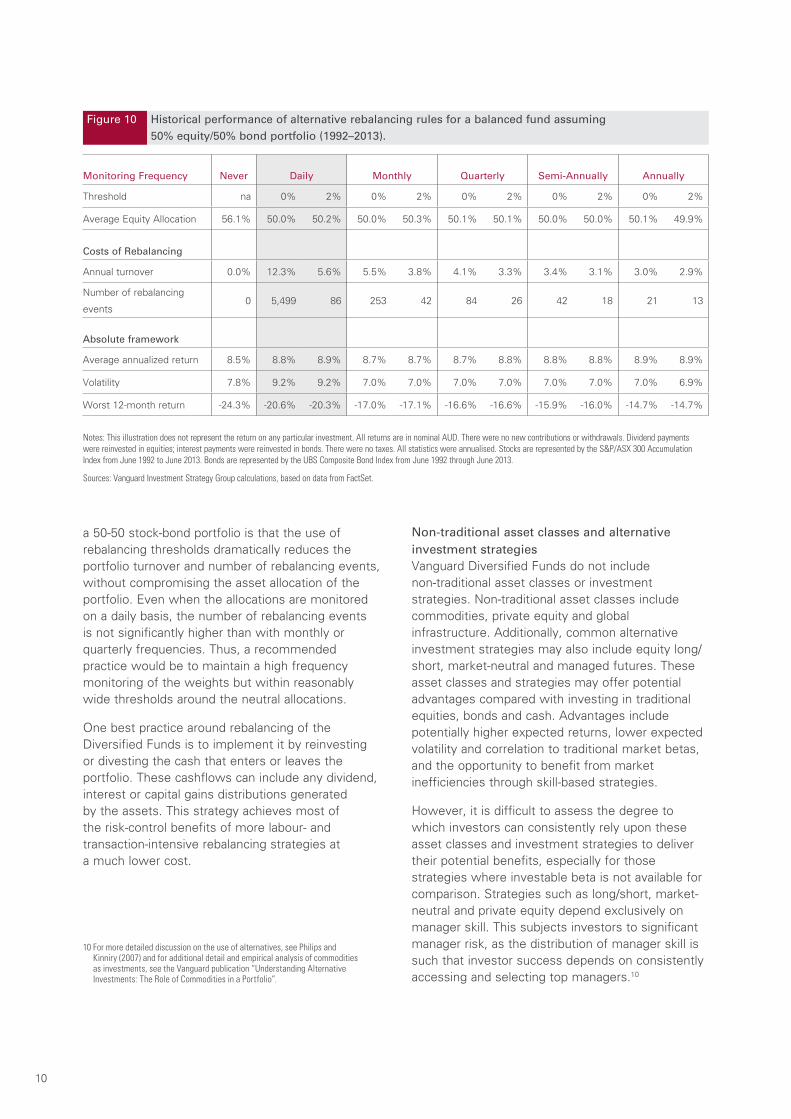

While one benefit of periodic rebalancing is to track closely the intended allocation of the Diversified Funds, the cost of rebalancing must also be considered. Rebalancing can involve costs related to securities turnover, transaction fees or capital gain taxes. Figure 10 shows the costs of rebalancing for different combinations of monitoring frequencies and rebalancing thresholds. The key message from this hypothetical exercise based on

9 From the standard portfolio volatility (vol) formula, the vol contribution of the currency exposure w can be represented as: σ2* = σ2 + w2σ$2 - 2wρσ$σ, where σ* is the overall global portfolio vol in domestic currency, σ is the vol in local currency, σ$ the vol of the currency itself (i.e. AUD appreciation rate) and ρ the currency correlation to the global portfolio. The optimal w results from solving the problem min σ2*, with the solution being w ≥ ρσ/σ$. If ρ≤0 , then w=0 (i.e. a fully hedged portfolio); if ρ>0 , then w=ρσ/σ$ (i.e. partially hedged). In the latter case, a fixed income portfolio would feature a lower ratio σ/σ$ compared to an equity portfolio, so the optimal currency exposure should be lower.

Sample diversified portfolio

Growth/Income split 30/70 50/50 70/30 90/10

Domestic/International mix* 50/50 50/50 50/50 50/50

Potential currency exposure 50% 50% 50% 50%

Weight of hedged global bonds 35% 25% 15% 5%

Implied% hedged for portfolio 70% 50% 30% 10%

*Assumes same domestic-international mix for growth and income splits

Source: Vanguard Investment Strategy Group

Figure 9 Implied currency hedge in sample asset allocations combining hedged global bonds and unhedged global equities.

10

a 50-50 stock-bond portfolio is that the use of rebalancing thresholds dramatically reduces the portfolio turnover and number of rebalancing events, without compromising the asset allocation of the portfolio. Even when the allocations are monitored on a daily basis, the number of rebalancing events is not significantly higher than with monthly or quarterly frequencies. Thus, a recommended practice would be to maintain a high frequency monitoring of the weights but within reasonably wide thresholds around the neutral allocations.

One best practice around rebalancing of the Diversified Funds is to implement it by reinvesting or divesting the cash that enters or leaves the portfolio. These cashflows can include any dividend, interest or capital gains distributions generated by the assets. This strategy achieves most of the risk-control benefits of more labour- and transaction-intensive rebalancing strategies at a much lower cost.

Non-traditional asset classes and alternative investment strategiesVanguard Diversified Funds do not include non-traditional asset classes or investment strategies. Non-traditional asset classes include commodities, private equity and global infrastructure. Additionally, common alternative investment strategies may also include equity long/short, market-neutral and managed futures. These asset classes and strategies may offer potential advantages compared with investing in traditional equities, bonds and cash. Advantages include potentially higher expected returns, lower expected volatility and correlation to traditional market betas, and the opportunity to benefit from market inefficiencies through skill-based strategies.

However, it is difficult to assess the degree to which investors can consistently rely upon these asset classes and investment strategies to deliver their potential benefits, especially for those strategies where investable beta is not available for comparison. Strategies such as long/short, market-neutral and private equity depend exclusively on manager skill. This subjects investors to significant manager risk, as the distribution of manager skill is such that investor success depends on consistently accessing and selecting top managers.10

Monitoring Frequency Never Daily Monthly Quarterly Semi-Annually Annually

Threshold na 0% 2% 0% 2% 0% 2% 0% 2% 0% 2%

Average Equity Allocation 56.1% 50.0% 50.2% 50.0% 50.3% 50.1% 50.1% 50.0% 50.0% 50.1% 49.9%

Costs of Rebalancing

Annual turnover 0.0% 12.3% 5.6% 5.5% 3.8% 4.1% 3.3% 3.4% 3.1% 3.0% 2.9%

Number of rebalancing

events0 5,499 86 253 42 84 26 42 18 21 13

Absolute framework

Average annualized return 8.5% 8.8% 8.9% 8.7% 8.7% 8.7% 8.8% 8.8% 8.8% 8.9% 8.9%

Volatility 7.8% 9.2% 9.2% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0% 6.9%

Worst 12-month return -24.3% -20.6% -20.3% -17.0% -17.1% -16.6% -16.6% -15.9% -16.0% -14.7% -14.7%

Notes: This illustration does not represent the return on any particular investment. All returns are in nominal AUD. There were no new contributions or withdrawals. Dividend payments were reinvested in equities; interest payments were reinvested in bonds. There were no taxes. All statistics were annualised. Stocks are represented by the S&P/ASX 300 Accumulation Index from June 1992 to June 2013. Bonds are represented by the UBS Composite Bond Index from June 1992 through June 2013.

Sources: Vanguard Investment Strategy Group calculations, based on data from FactSet.

Figure 10 Historical performance of alternative rebalancing rules for a balanced fund assuming 50% equity/50% bond portfolio (1992–2013).

10 For more detailed discussion on the use of alternatives, see Philips and Kinniry (2007) and for additional detail and empirical analysis of commodities as investments, see the Vanguard publication “Understanding Alternative Investments: The Role of Commodities in a Portfolio”.

11

Vanguard does not include commodities, and specifically commodities futures, in the Diversified Funds at the moment. While recognising the historical diversifying benefit of commodities futures, Vanguard cautions against making such an allocation solely based on historical commodity returns. The long-term economic justification for expecting significant, positive returns from a static, long-only commodities futures exposure is subject to ongoing debate. Figure 11 presents a full summary of relevant Vanguard research assessing the viability of alternative asset classes and investment strategies.

The case for index fund investing in the Diversified FundsThe case for index fund investing and the active-passive investment debate are major areas of research in Vanguard (see Phillips, 2013, Steinfort and McIntosh, 2012 and references cited therein). All the main results and findings from this research carry through directly to the Vanguard Diversified Funds.

In any market, a dollar invested is bound by the zero-sum game: for every dollar buying a security, there must be a dollar sold. That is, for every belief that a security will outperform, there is a counter view that it will underperform. At every moment, an index, or a fund that tightly tracks that index, reflects all of these beliefs, trades and positions. But, after accounting for the constant drag of higher transaction, management and other costs,

Reservation Vanguard research

Alternatives (including: Hedge funds, private equity/venture capital and infrastructure)

Selecting the alpha generating manager(s) from the universe of hedge fund managers is difficult.

Costs matter: the average hedge fund manager costs over +1.50%, compared with the average Australian equity manager costing +0.90% p.a.

Funds of hedge funds are expensive, and have a double layer of fees.

Infrastructure is already represented in global equity benchmarks: a discrete allocation will essentially be doubling up on this exposure.

Hammer, Sarah and Anatoly Shtekhman, 2012. A mixed bag: Performance of hedge fund categories before and after the financial crisis.

Philips, Christopher B., 2008. Understanding alternative investments: A primer on hedge fund evaluation.

Philips, Christopher B, David J. Walker and Francis Kinniry, 2012. Dynamic correlations: the implications for portfolio construction.

Wallick, Daniel W. 2008. The life cycle of an investment idea: How to consider alternative investments.

Commodities Commodities have a limited performance history (which is free of backfill bias).

The long-term economic justification for expecting significant, positive returns from a static, long-only commodities futures exposure is subject to ongoing debate.

Stockton, Kimberly 2007. Understanding alternative investments: The role of commodities in a portfolio.

Inflation linked bonds Linkers in Australia have a low liquidity and market depth (which is small, but growing).

Murik, Vijay A. and Paul W. Chin, 2013. A primer on inflation-linked bonds.

High Yield Bonds High yield bonds reflect characteristics of both equity and fixed interest markets; illiquidity and lack of transparency are concerns and have not historically improved the risk and return characteristics of a portfolio.

Philips, Christopher B. 2012. Worth the risk? The appeal and challenges of high yield bonds.

EM bonds Dedicated exposure to speculative grade EM bonds represents a material increase in sovereign risk exposure with no reliable diversification benefits at times of financial distress in developed markets.

Philips, Christopher, Joanne Yoon, Michael DiJoseph, Ravi G. Tolani, Scott J, Donaldson and Todd Schlanger, 2013. Emerging market bonds – beyond the headlines.

Source: Vanguard Investment Strategy Group.

Figure 11 Relevant research on asset classes and investment strategies not included in the Diversified Funds.

12

a majority of actively managed portfolios fall to the losing side of the index’s performance.

Figure 12 shows this point using actual active fund performance data for active equity and bond funds available to Australian investors. Further, Vanguard research shows that those funds that successfully outperform the benchmark over a given period often find it extremely difficult to maintain that outperformance in subsequent periods.

Index funds provide lower-risk, efficient, transparent, diversified and low-cost investment vehicles with the potential to increase unitholder wealth through exposures in a broad range of asset and sub-asset classes.

• Lower risk: Whether measured by the number of security holdings, return volatility, downside risk or likelihood of outperforming, passive management generally carries lower risk than active management.

• Efficient: Portfolio turnover is limited to additions and deletions from an index, mergers and acquisitions and other corporate actions. Rebalancing is continuous and costless since security weights reflect the market weight.

• Transparent: Because an index fund generally holds all or most of the securities in a given index benchmark at the same weights as that of the

Figure 12 Distribution of active equity and bond fund returns in Australia

Active returnActive return

Active returnActive return

0

50

100

150

200

250

Closedfunds

<-6% -6% to-4%

-4% to-2%

-2% to0%

0% to2%

2% to4%

4% to6%

>6%

Australian equity funds10 years ending 30 June 2013

Underperformed: 56%(including closed funds 72%)

Num

ber

of f

unds

Num

ber

of f

unds

Num

ber

of f

unds

Num

ber

of f

unds

Closedfunds

<-6% -6% to-4%

-4% to-2%

-2% to0%

0% to2%

2% to4%

4% to6%

>6%

Aus & Intl Equity funds available for Aus investors10 years ending 30 June 2013

Underperformed: 58%(including closed funds 76%)

050

100150200250300350400450500

Note: Period covered is 10 years ending 30 June 2013. Closed funds are assumed to be closed due to underperformance. Includes all Global and Australian equity and fixed income funds available for investment to an Australian investor. For original analysis and details see Phillips, 2013 and Steinfort and McIntosh, 2012.

Source: Vanguard Investment Strategy Group, based on Morningstar Direct data. Morningstar data © 2013 Morningstar, Inc. All Rights Reserved. The information contained above: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Closedfunds

<-6% -6% to-4%

-4% to-2%

-2% to0%

0% to2%

2% to4%

4% to6%

>6%

Australian fixed income funds10 years ending 30 June 2013

Underperformed: 58%(including closed funds 77%)

0

10

20

30

40

50

60

70

80

90

0

20

40

60

80

100

120

Closedfunds

<-6% -6% to-4%

-4% to-2%

-2% to0%

0% to2%

2% to4%

4% to6%

>6%

Aus & Intl Fixed income funds available for Aus investors 10 years ending 30 June 2013

Underperformed: 64%(including closed funds 80%)

13

index benchmark, investors can always determine which securities constitute their portfolio and how they performed.

• Diversified: Index funds tracking broad benchmarks hold all or most of the securities that comprise that benchmark. Investors benefit from the mitigation of security and sector concentration risk.

• Lower cost: Index funds typically have low management fees and low operating costs.

Conclusion

Vanguard Diversified Funds are professionally-managed single-fund solutions whose asset allocation design is focused on Vanguard’s global expertise in capital markets and portfolio construction research as well as Vanguard’s extensive practical experience with investors.

Too many investors focus on the markets, the economy, individual manager performance, or the performance of a given security or strategy instead of focusing their efforts on the core fundamentals of balanced asset allocation and a long-term investment perspective.

We believe a top-down approach, starting with a suitable asset allocation mix allowing for different investment goals and constraints, a straightforward design, all coupled with an index-focused approach that keeps investment costs low offers the best chance of investment success.

References

Brinson, Gary P., L. Randolph Hood, and Gilbert L. Beebower, 1986. Determinants of Portfolio Performance. Financial Analysts Journal 42(4): 39–44.

Brinson, Gary P., Brian D. Singer, and Gilbert L. Beebower, 1991. Determinants of Portfolio Performance II: An Update. Financial Analysts Journal 47(3): 40–48.

Davis, Joseph H., Roger Aliaga-Díaz, 2013. Vanguard’s economic and investment outlook. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Donaldson, Scott J., Maria Bruno, David J. Walker, Todd Schlanger and Francis M. Kinniry, Jr., 2013. Vanguard’s framework for constructing diversified portfolios. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Donaldson, Scott J., Francis M. Kinniry, Jr., John Ameriks, Roger Aliaga-Díaz, Brad Redding and Andrew J. Patterson, 2012. Vanguard’s approach to target-date funds. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Hammer, Sarah and Anatoly Shtekhman, 2012. A mixed bag: Performance of hedge fund categories before and after the financial crisis. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Jaconetti, Colleen M., Francis M. Kinniry Jr., and Yan Zilbering, 2010. Best practices for portfolio rebalancing. Valley Forge, PA.: Vanguard Investment Strategy Group, The Vanguard Group.

Lee, Randy J., Christopher B. Philips, David J. Walker and Francis M. Kinniry, Jr., 2013. Vanguard’s approach to target-allocation funds. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

McIntosh, Roger, Rosemary Steinfort and Eugene Lim, 2011. Understand the Vanguard® Diversified Funds. Southbank, Victoria: Vanguard Investment Strategy Group, The Vanguard Group.

Murik, Vijay A. and Paul W. Chin, 2013. A primer on inflation-linked bonds. Southbank, Victoria: Vanguard Investment Strategy Group, The Vanguard Group.

14

Peterson LaBarge, Karin., 2010. Currency management: Considerations for the equity hedging decision. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B., 2012. Considerations for International Equity. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B., 2012. The case for indexing. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B., 2008. Understanding alternative investments: A primer on hedge fund evaluation. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B. 2012. Worth the risk? The appeal and challenges of high yield bonds. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B., Francis M. Kinniry Jr. and Scott Donaldson, 2012. The role of home bias in global asset allocation. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher B., David J. Walker and Francis M. Kinniry, Jr., 2012. Dynamic correlations: The implications for portfolio construction. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Philips, Christopher, Joanne Yoon, Michael DiJoseph, Ravi G. Tolani, Scott J, Donaldson and Todd Schlanger, 2013. Emerging market bonds – Beyond the headlines. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Steinfort, Rosemary, and Paul W. Chin, 2013. The role of global equities – for Australian investors. Southbank, Victoria: Vanguard Investment Strategy Group, The Vanguard Group.

Steinfort, Rosemary, and Roger McIntosh, 2012. The case for indexing in Australia. Southbank, Victoria: Vanguard Investment Strategy Group, The Vanguard Group.

Tokat, Yesim, 2005. The asset allocation debate: provocative questions, enduring realities. Valley Forge, Pa. Investment Strategy Group, The Vanguard Group.

Wallick, Daniel W. 2008. The life cycle of an investment idea: How to consider alternative investments. Valley Forge, Pa. Investment Strategy Group, The Vanguard Group.

Wallick, Daniel W., Julieann Shanahan, Christos Tasopoulos and Joanne Yoon, 2012. The global case for strategic asset allocation. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

Vanguard’s Principles for Investing Success, 2013. Valley Forge, Pa.: Vanguard Investment Strategy Group, The Vanguard Group.

15

16

This paper includes general information and is intended to assist you. Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) is the product issuer. We have not taken your circumstances into account when preparing the information so it may not be applicable to your circumstances. You should consider your circumstances and our Product Disclosure Statements (“PDSs”) before making any investment decision. You can access our PDSs at vanguard.com.au or by calling 1300 655 101. Past performance is not an indication of future performance. This publication was prepared in good faith and we accept no liability for any errors or omissions.

© 2013 Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263). All rights reserved.

Morningstar data. © Morningstar 2013. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past financial performance is no guarantee of future results.

Connect with Vanguard®

The indexing specialist > vanguard.com.au > 1300 655 102

CONDIV 082013