valuing early stage companies - wild apricot...valuing early stage companies or how to appear that...

TRANSCRIPT

Valuing Early Stage Companies

or how to appear that you can negotiate

with a sophisticated investor

Jan Klein THP, LLC [email protected]

January 16, 2014

Beauty or Value is in the eyes of the beholder

Financial Investors Friends and Family

Angels

Venture Capitalists

Strategic Synergistic players

Competitors

What constitutes value

Hard Assets

Ideas/Products

Individuals/Teams

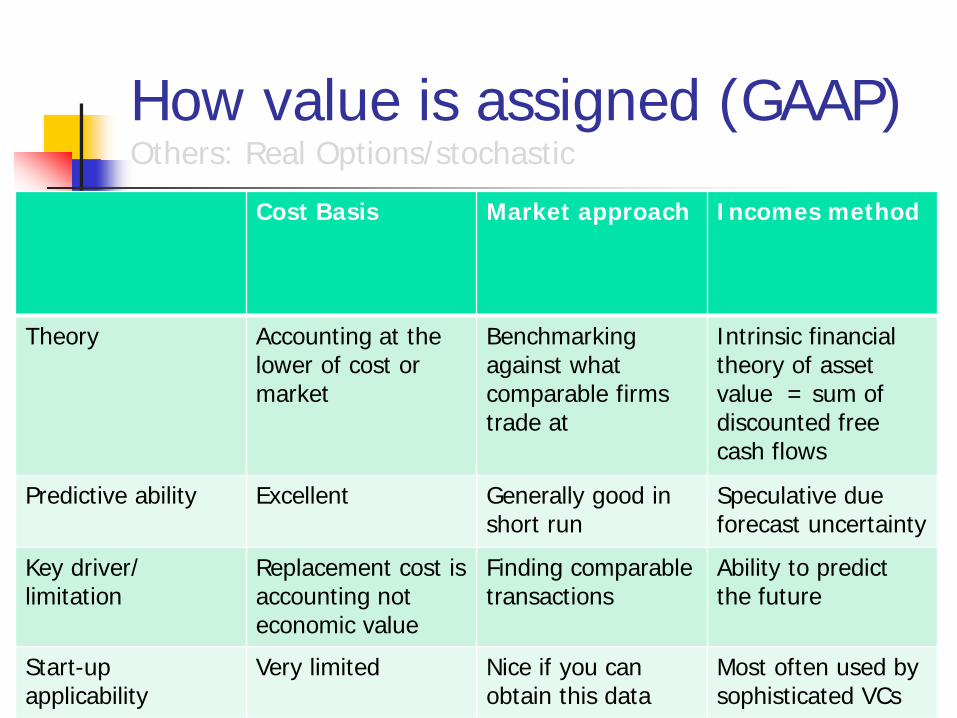

How value is assigned (GAAP) Others: Real Options/stochastic

Cost Basis Market approach Incomes method

Theory Accounting at the lower of cost or market

Benchmarking against what comparable firms trade at

Intrinsic financial theory of asset value = sum of discounted free cash flows

Predictive ability Excellent Generally good in short run

Speculative due forecast uncertainty

Key driver/ limitation

Replacement cost is accounting not economic value

Finding comparable transactions

Ability to predict the future

Start-up applicability

Very limited Nice if you can obtain this data

Most often used by sophisticated VCs

The Pre and Post Money Concept

Pre-money Value + Investment = Post-money Value

As a general rule entrepreneurs focus on Post-money Value

Intrinsic Values (sum of FCF) implies available financing and hence is a Post-money concept

If there is NO Investment to fund the business plan then there is only liquidation or NO value

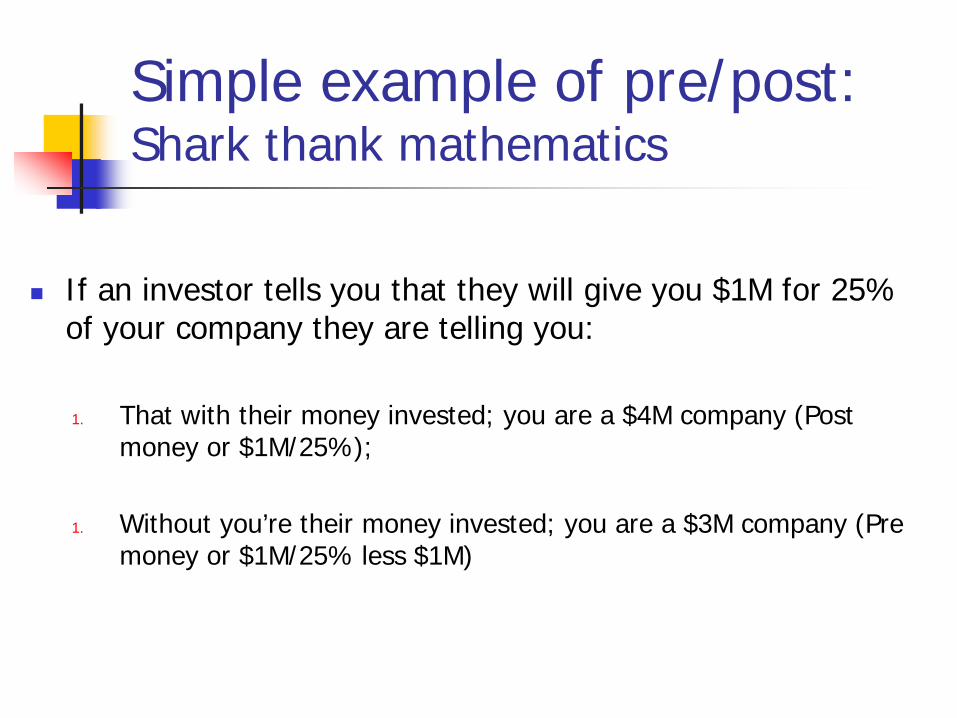

Simple example of pre/post: Shark thank mathematics

If an investor tells you that they will give you $1M for 25% of your company they are telling you: 1. That with their money invested; you are a $4M company (Post

money or $1M/25%); 1. Without you’re their money invested; you are a $3M company (Pre

money or $1M/25% less $1M)

What you can expect

Source: Kaufmann Foundation: http://www.angelcapitalassociation.org/data/Documents/Resources/AngelCapitalEducation/ACEF_-Valuing Pre-revenue Companies.pdf

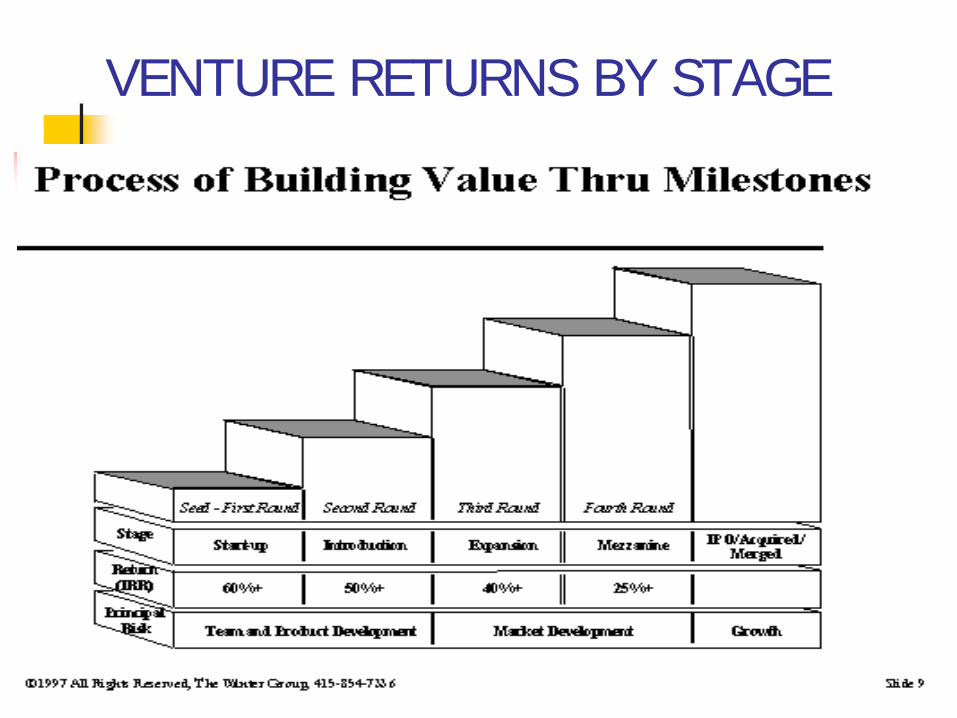

VENTURE RETURNS BY STAGE

Cost Based Approach Theory: Investor values your firm’s assets based upon the

total replacement cost Practicalities:

Difficulties is estimating costs: Gross/Net Book; Economic/technical life, comparability, etc.

Treats everything as a commodity Often ignores the “intangibles”:

Compelling or proprietary use of the assets Value of the team and/or start-up expenses incurred Market window or time to market

Implementation GAAP Balance Sheet analysis: Audit Cash, A/R, A/P, Inventory, etc. Problems with IPR and intangible components

Cost Based Applications

Most often used in special situations Liquidations Mature industries; Patent rich firms or where liabilities are very

significant i.e. Commercial Banking: Net Tangible Book Value

Acquisitions + Replacement (“make vs. buy”) decisions

Rarely for start-ups or pre-revenue firms

Market based Approach Theory: Investor is willing to pay a discount or premium to

prevailing market prices for same item Practicalities:

Difficulties is comparable companies and market transactions Adjustments need to be made for:

Product and/or customer mix Stage of Development/Private v. Public Timing of the transaction

Implementation Identify comparable market transactions (M+A/IPO or Disposition) Develop “multiples” either Price (equity) or Enterprise (equity + debt)

relative to a financial/operating metric for a public firm use to value Financial multiples: Price/Sales; Price/Earnings or Price/Cash flow or Operating multiples: Price/”website hits”, downloads, users, etc. etc.

Benchmarking using market based transactions

Comparison with comparable sales transactions Often must adjust for differences in size or development stage of the

firm Always have to adjust for differences in Public verses Private

Benchmark with quoted sales price of similar companies

For Private firms (early stage) the market value can be based upon: The current investment value after taking into account liquidation

preferences and participation rights Adjusting for lack of liquidity and/or lack of control (if comparing to Public)

Market Based: Transaction Multiples

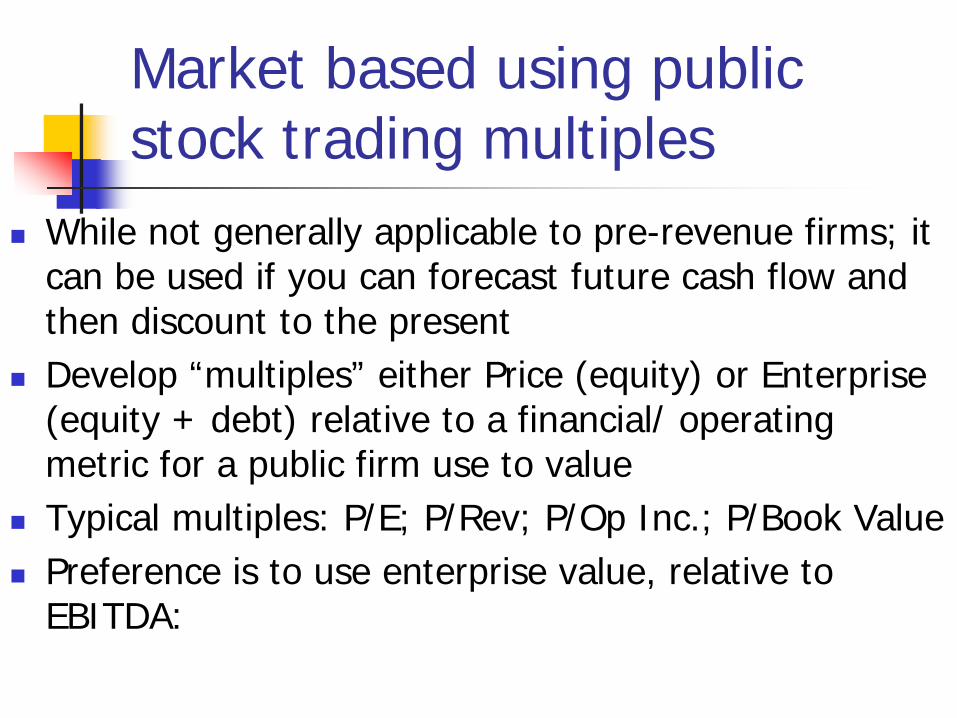

Market based using public stock trading multiples

While not generally applicable to pre-revenue firms; it can be used if you can forecast future cash flow and then discount to the present

Develop “multiples” either Price (equity) or Enterprise (equity + debt) relative to a financial/ operating metric for a public firm use to value

Typical multiples: P/E; P/Rev; P/Op Inc.; P/Book Value Preference is to use enterprise value, relative to

EBITDA:

15

Enterprise Value Economic Value Balance Sheet

PV of future cash from business operations Or ASSET VALUE

$1500

Cash $200 Debt $650

Marketable securities $150 Equity $1200

$1850 $1850

Enterprise Value

Remember Enterprise Value = Assets which = Debt +Equity

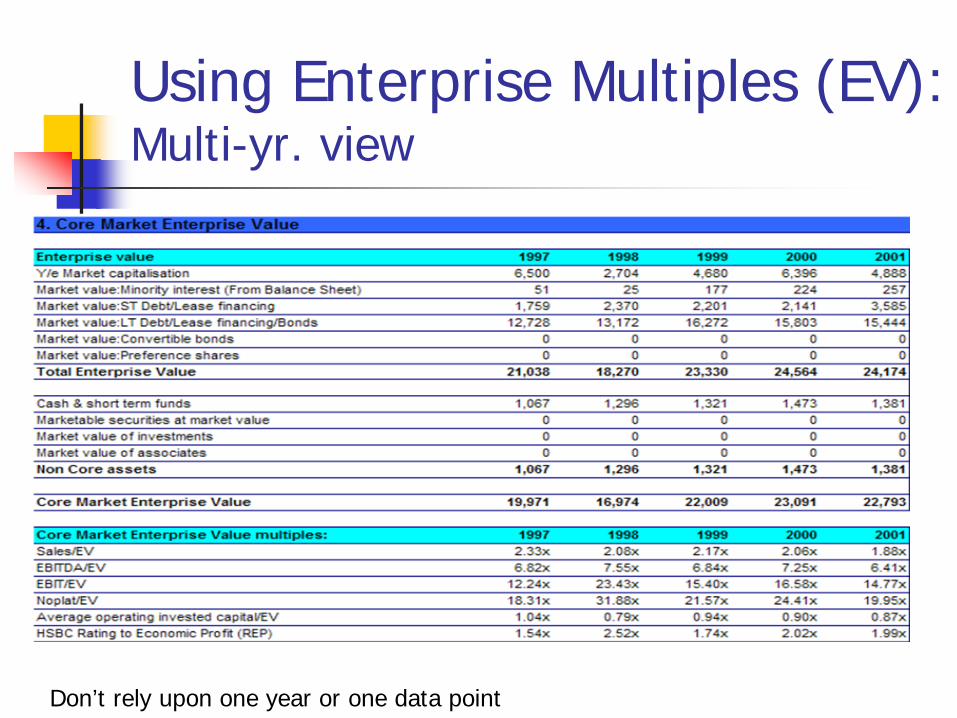

Using Enterprise Multiples (EV): Multi-yr. view

Don’t rely upon one year or one data point

Incomes or Earnings Approach Theory: Investor values your firm’s assets based upon how

much cash flow can be generated in “today’s $ terms” Practicalities:

Values highly dependent upon future cash flow and “discount rate” estimates

Difficult and complex calculations Must be supported by a comprehensive business plan Yields a “private” value for 100% of the assets and ignores the

“haircuts” that investors give to lack of liquidity and lack of control

Implementation Forecast Free Cash Flow = NOPAT less CAPEX +/- change in Wkg, Cap Develop estimates of discount rates (expected Investors ROR)

Financial Analysis - Objectives

The “Incomes” or DCF Model

Template for Free Cash Flow “In

com

e S

tate

men

t”

Working capital

Year 0 1 2RevenueCostsDepreciation of equipment Noncash itemProfit/Loss from asset sales Noncash item

Taxable incomeTaxNet oper proft after tax (NOPAT)Depreciation Adjustment forProfit/Loss from asset sales for non-cash

Operating cash flowChange in working capitalCapital Expenditure Capital itemsSalvage of assetsFree cash flow

Forecasting Operating Cash Flows (INTEL EX)

Preparing Free Cash Flow projections (INTEL EX)

Choosing discount factors WAAC (INTEL EX)

Discount rates used by VC’s

Determining exit Multiple EV/EBIT (INTEL EX)

Final Valuation Determination (INTEL EX)

QUESTIONS

Following Charts are All Back-Up

DEAL STRUCTURE

Finding a VC

The Pitch

Evaluating a Business Plan

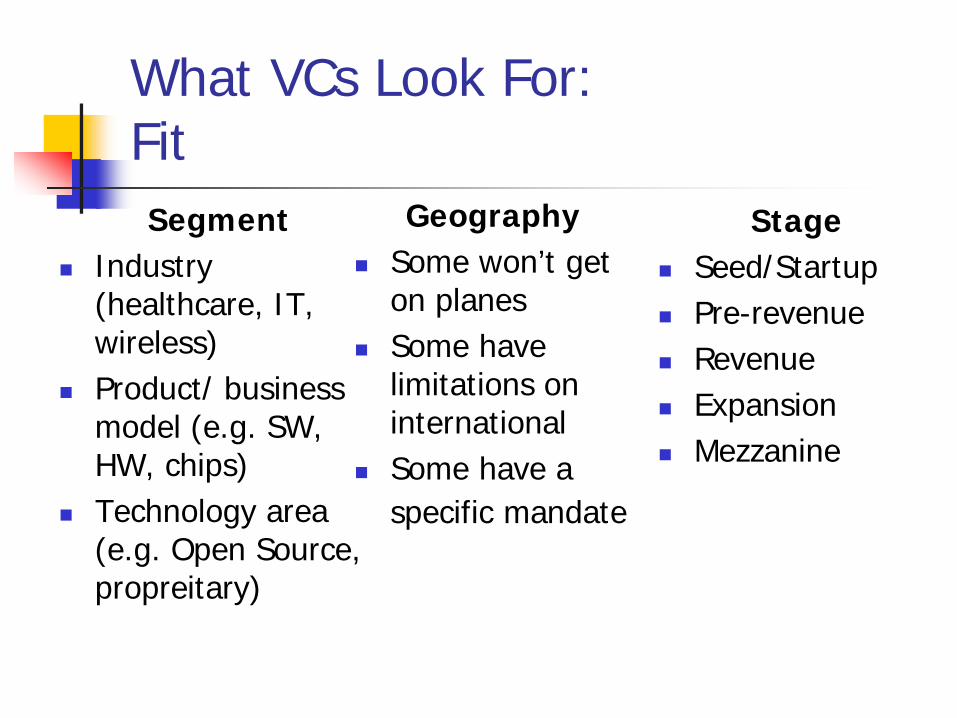

What VCs Look For: Fit Segment

Industry (healthcare, IT, wireless)

Product/ business model (e.g. SW, HW, chips)

Technology area (e.g. Open Source, propreitary)

Geography Some won’t get

on planes Some have

limitations on international

Some have a specific mandate

Stage Seed/Startup Pre-revenue Revenue Expansion Mezzanine

Employee Ownership

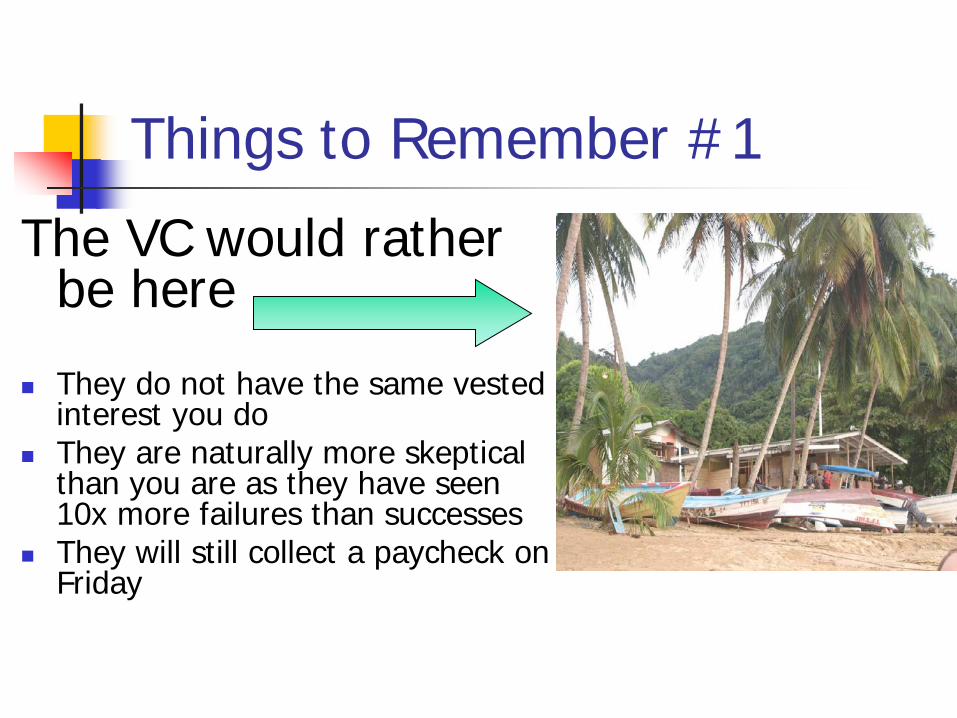

Things to Remember #1

The VC would rather be here

They do not have the same vested

interest you do They are naturally more skeptical

than you are as they have seen 10x more failures than successes

They will still collect a paycheck on Friday

Economics of Private Equity (VC)

%

Deal Investment Return Gain/Loss

1 5,000,000 50,000,000 900%

2 5,000,000 30,000,000 500%

3 5,000,000 12,500,000 150%

4 5,000,000 0 0%

5 5,000,000 -2,500,000 -50%

6 5,000,000 -3,500,000 -70%

7 5,000,000 -3,500,000 -70%

8 5,000,000 -5,000,000 -100%

9 5,000,000 -5,000,000 -100%

10 5,000,000 -5,000,000 -100%

Total 50,000,000 68,000,000 36%