value focus - business valuation and financial...

TRANSCRIPT

VALUE FOCUSFOOD AND BEVERAGE

Q1: Non-Alcoholic BeveragesQ2: Alcoholic BeveragesQ3: Food ProcessingQ4: Fast Food & Casual Restaurants

2013

© 2014 Mercer Capital 1 www.mercercapital.com

Segment Focus

2013 Third Quarter

Food Processing

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES

Recent performance and consolidation trends within the food processing industry further highlight the mature state of the industry. Some

segments, such as frozen food processing, are largely defined by price-based competition and little technological development, while

others continue to exhibit growth through innovation. A growing demand for healthier products is also one of the trends that continues

to shape the industry.1 Health concerns have forced bread producers to offer whole grain, low carb, and gluten free options.2 Moreover,

major companies like Tyson have responded to health demands by revamping some of their offerings within the frozen food segment. Tyson

introduced its new “Tyson Deli Market” which relies on a frozen-fresh delivery system that delivers the meals frozen and allows them to be

thawed in-store, ultimately reaching the consumer as a “fresh” product.3 Lastly, growing post-recession disposable incomes are expected

to further spur demand for premium product offerings.

On average, prices for the publicly traded

food processors shown below have

increased 83% over the last five years

(12.9% annually) as recovery from the

recession continued.

Dairy manufacturer Dean Foods strug-

gled to realize similar increases as it

fought weak sales volumes and spun

off its Wisconsin-based milk processing

business.

Public Company Performance

-‐100%

-‐50%

0%

50%

100%

150%

200%

PepsiCo Inc. Tyson Foods Inc. Dean Foods Company ConAgra Foods, Inc. Hormel Foods Corpora@on Unilever NV Grupo Bimbo SAB de CV Sanderson Farms Inc. Nestle SA

5 Year Change in Stock Prices for Publicly Traded Food Processors

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 2 www.mercercapital.com

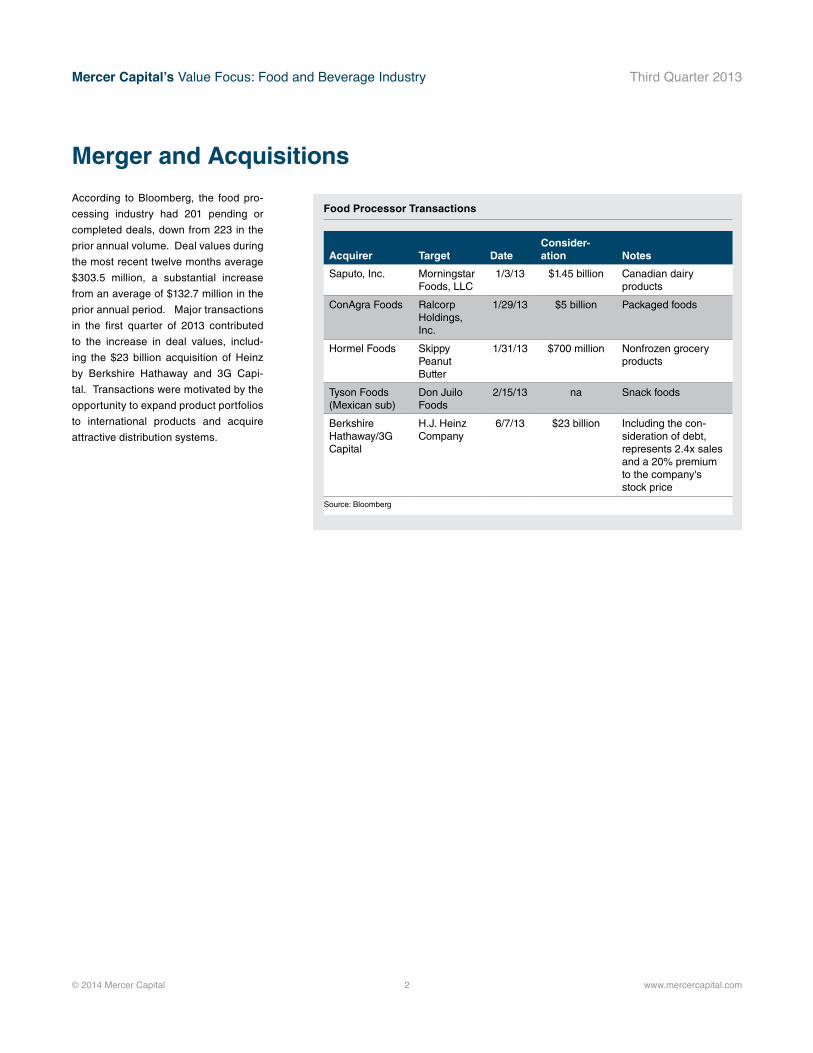

According to Bloomberg, the food pro-

cessing industry had 201 pending or

completed deals, down from 223 in the

prior annual volume. Deal values during

the most recent twelve months average

$303.5 million, a substantial increase

from an average of $132.7 million in the

prior annual period. Major transactions

in the first quarter of 2013 contributed

to the increase in deal values, includ-

ing the $23 billion acquisition of Heinz

by Berkshire Hathaway and 3G Capi-

tal. Transactions were motivated by the

opportunity to expand product portfolios

to international products and acquire

attractive distribution systems.

Merger and Acquisitions

Acquirer Target Date Consider-ation Notes

Saputo, Inc. Morningstar Foods, LLC

1/3/13 $1.45 billion Canadian dairy products

ConAgra Foods Ralcorp Holdings, Inc.

1/29/13 $5 billion Packaged foods

Hormel Foods Skippy Peanut Butter

1/31/13 $700 million Nonfrozen grocery products

Tyson Foods (Mexican sub)

Don Juilo Foods

2/15/13 na Snack foods

Berkshire Hathaway/3G Capital

H.J. Heinz Company

6/7/13 $23 billion Including the con-sideration of debt, represents 2.4x sales and a 20% premium to the company's stock price

Source: Bloomberg

Food Processor Transactions

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 3 www.mercercapital.com

Frozen Food

The United States frozen food sector has

annual revenues of approximately $28

billion and maintains a 5% profit margin.

The sector has endured a long period

of dwindling revenues as consumer

demand for frozen food plummeted.

A rise in disposable incomes among con-

sumers coupled with growing health con-

cerns has been detrimental for the indus-

try as more consumers continue to move

towards fresh food. Accordingly, the

sector attempted to fight falling demand

through new product innovation, ulti-

mately leading to higher marketing costs

and depressed margins.4 More market-

ing efforts from a new product standpoint

and advertising aimed at improving PR

are expected to continue for some time

within the sector.

Overall, sector revenue has been flat

since pre-recession years. If current

trends continue, revenue could fall below

pre-recession numbers during the next

five years.5 Price-based competition has

resulted in a lack of technological inno-

vation and increased layoffs, hamper-

ing the industry’s ability to evolve going

forward. In 2013, Heinz closed down a

major frozen food plant in Idaho in order

to consolidate its operations and improve

efficiency.6 Additionally, in 2012 Nestle

shut down a factory in California as its

trademarked Hot Pockets brand contin-

ued to have declining sales.

The sector as a whole continues to see

unit sales falling in the mid-single digit

range with flat or negative annual reve-

nue growth.7 Many of the same trends in

consolidation, layoffs, and price-based

competition are expected to continue to

define the industry.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

$113

$114

$115

$116

$117

$118

$119

$120

$121

2008 2009 2010 2011 2012

Mar

gins

Sale

s in

Bill

ions

USD

Source: Bloomberg

Sales Gross Margin EBITDA Margin

U.S. Frozen Food Historical Sales and Margins

14%

9.40%

7.80%

3%

2.80%

2.10%

60.90%

Source: IBISWorld

Nestle SA The Schwan Food Co. ConAgra Foods Inc. HJ Heinz Company Kellogg Company McCain Foods Limited Other

U.S. Frozen Food Market Share Data

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 4 www.mercercapital.com

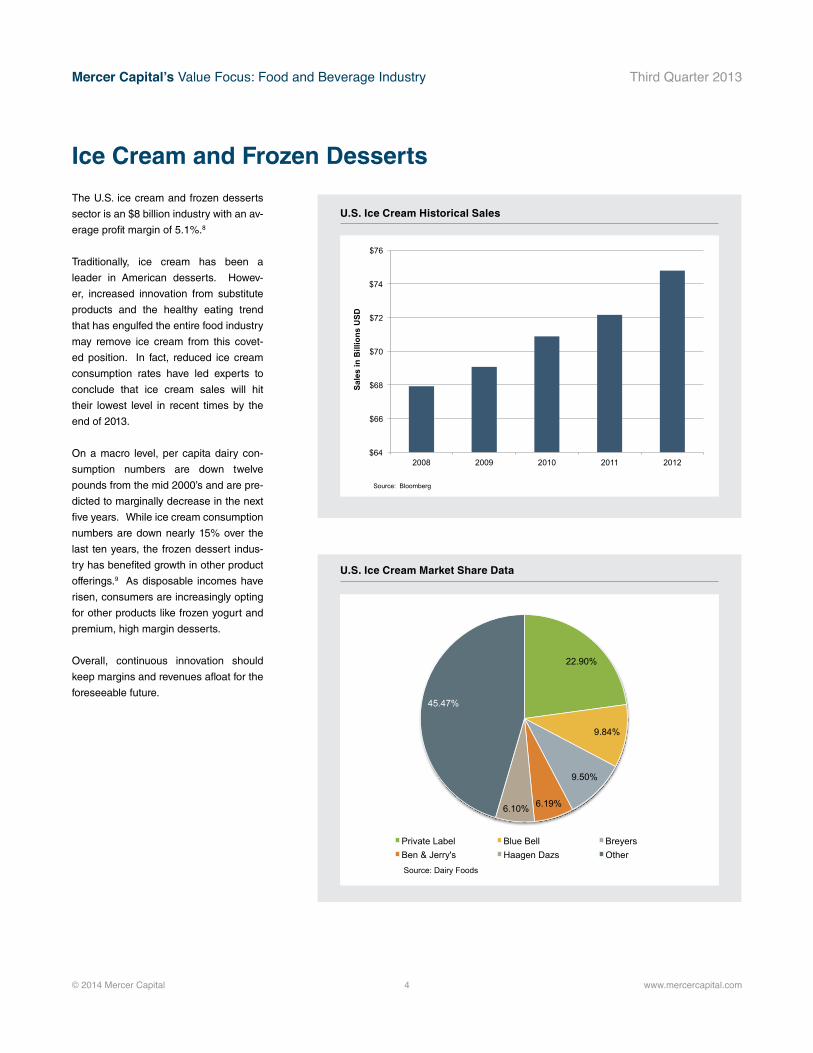

Ice Cream and Frozen Desserts

The U.S. ice cream and frozen desserts

sector is an $8 billion industry with an av-

erage profit margin of 5.1%.8

Traditionally, ice cream has been a

leader in American desserts. Howev-

er, increased innovation from substitute

products and the healthy eating trend

that has engulfed the entire food industry

may remove ice cream from this covet-

ed position. In fact, reduced ice cream

consumption rates have led experts to

conclude that ice cream sales will hit

their lowest level in recent times by the

end of 2013.

On a macro level, per capita dairy con-

sumption numbers are down twelve

pounds from the mid 2000’s and are pre-

dicted to marginally decrease in the next

five years. While ice cream consumption

numbers are down nearly 15% over the

last ten years, the frozen dessert indus-

try has benefited growth in other product

offerings.9 As disposable incomes have

risen, consumers are increasingly opting

for other products like frozen yogurt and

premium, high margin desserts.

Overall, continuous innovation should

keep margins and revenues afloat for the

foreseeable future.

22.90%

9.84%

9.50%

6.19% 6.10%

45.47%

Source: Dairy Foods

Private Label Blue Bell Breyers Ben & Jerry's Haagen Dazs Other

U.S. Ice Cream Market Share Data

$64

$66

$68

$70

$72

$74

$76

2008 2009 2010 2011 2012

Sale

s in

Bill

ions

USD

Source: Bloomberg

U.S. Ice Cream Historical Sales

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 5 www.mercercapital.com

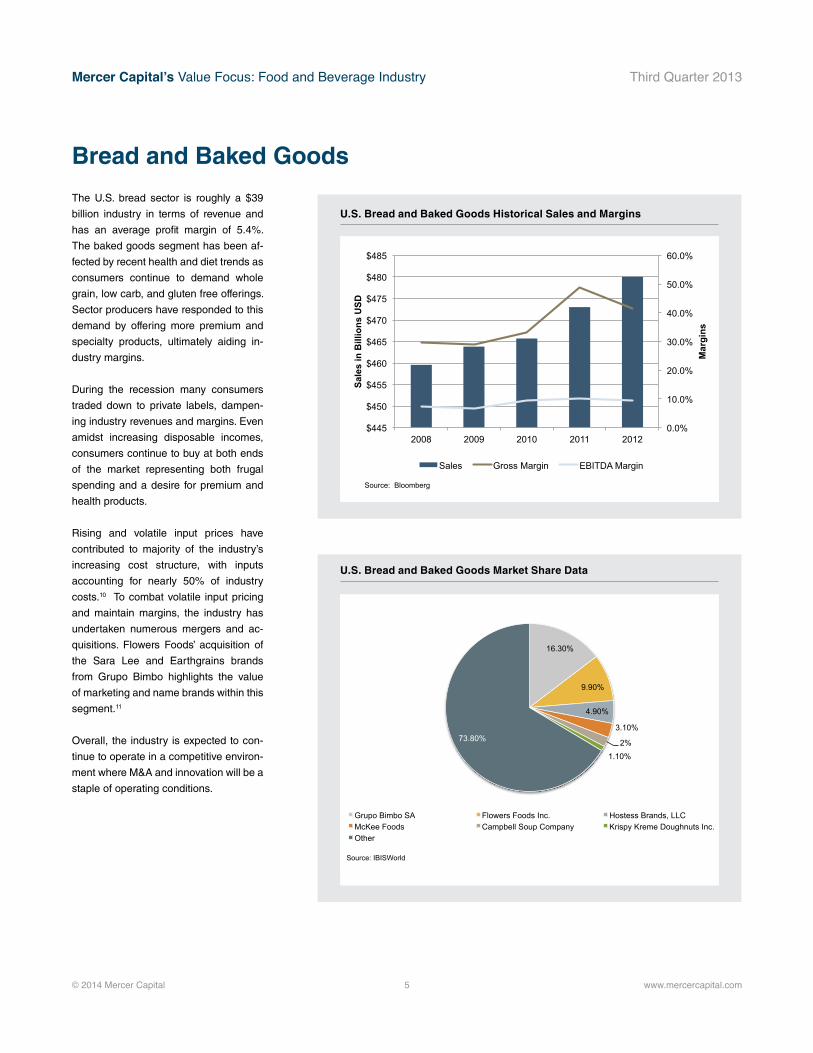

Bread and Baked Goods

The U.S. bread sector is roughly a $39

billion industry in terms of revenue and

has an average profit margin of 5.4%.

The baked goods segment has been af-

fected by recent health and diet trends as

consumers continue to demand whole

grain, low carb, and gluten free offerings.

Sector producers have responded to this

demand by offering more premium and

specialty products, ultimately aiding in-

dustry margins.

During the recession many consumers

traded down to private labels, dampen-

ing industry revenues and margins. Even

amidst increasing disposable incomes,

consumers continue to buy at both ends

of the market representing both frugal

spending and a desire for premium and

health products.

Rising and volatile input prices have

contributed to majority of the industry’s

increasing cost structure, with inputs

accounting for nearly 50% of industry

costs.10 To combat volatile input pricing

and maintain margins, the industry has

undertaken numerous mergers and ac-

quisitions. Flowers Foods’ acquisition of

the Sara Lee and Earthgrains brands

from Grupo Bimbo highlights the value

of marketing and name brands within this

segment.11

Overall, the industry is expected to con-

tinue to operate in a competitive environ-

ment where M&A and innovation will be a

staple of operating conditions.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

$445

$450

$455

$460

$465

$470

$475

$480

$485

2008 2009 2010 2011 2012

Mar

gins

Sale

s in

Bill

ions

USD

Source: Bloomberg

Sales Gross Margin EBITDA Margin

U.S. Bread and Baked Goods Historical Sales and Margins

16.30%

9.90%

4.90%

3.10%

2%

1.10%

73.80%

Source: IBISWorld

Grupo Bimbo SA Flowers Foods Inc. Hostess Brands, LLC McKee Foods Campbell Soup Company Krispy Kreme Doughnuts Inc. Other

U.S. Bread and Baked Goods Market Share Data

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 6 www.mercercapital.com

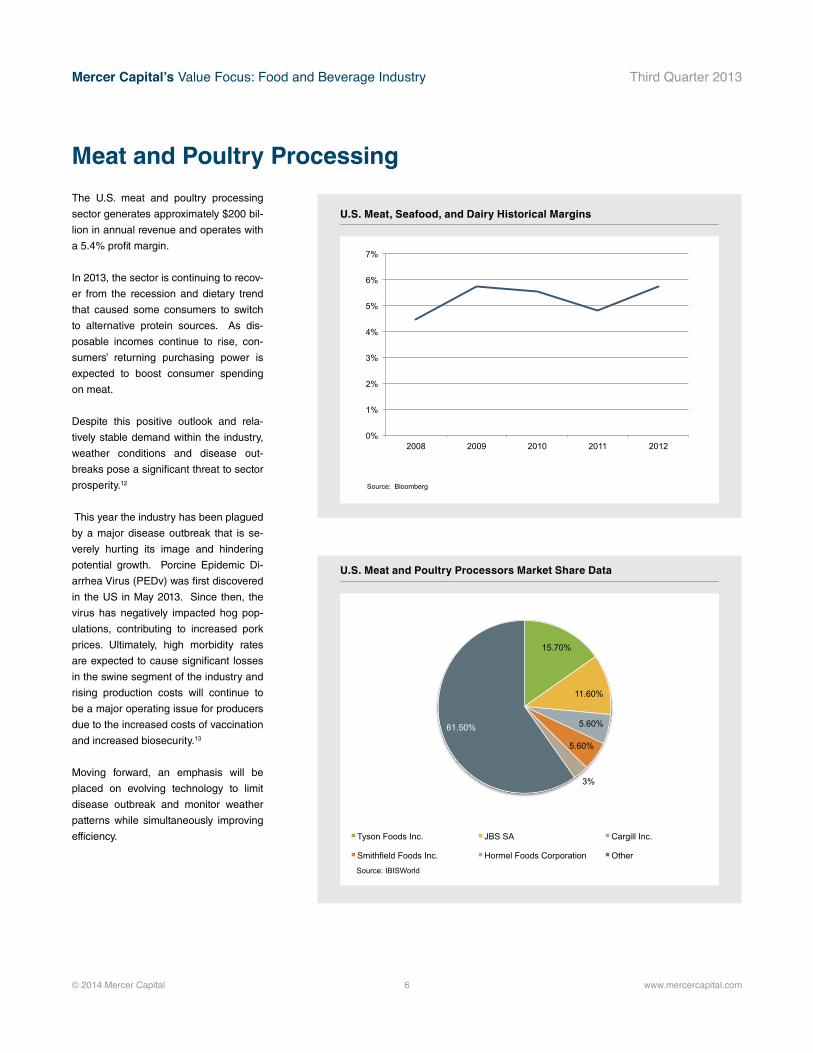

Meat and Poultry Processing

The U.S. meat and poultry processing

sector generates approximately $200 bil-

lion in annual revenue and operates with

a 5.4% profit margin.

In 2013, the sector is continuing to recov-

er from the recession and dietary trend

that caused some consumers to switch

to alternative protein sources. As dis-

posable incomes continue to rise, con-

sumers’ returning purchasing power is

expected to boost consumer spending

on meat.

Despite this positive outlook and rela-

tively stable demand within the industry,

weather conditions and disease out-

breaks pose a significant threat to sector

prosperity.12

This year the industry has been plagued

by a major disease outbreak that is se-

verely hurting its image and hindering

potential growth. Porcine Epidemic Di-

arrhea Virus (PEDv) was first discovered

in the US in May 2013. Since then, the

virus has negatively impacted hog pop-

ulations, contributing to increased pork

prices. Ultimately, high morbidity rates

are expected to cause significant losses

in the swine segment of the industry and

rising production costs will continue to

be a major operating issue for producers

due to the increased costs of vaccination

and increased biosecurity.13

Moving forward, an emphasis will be

placed on evolving technology to limit

disease outbreak and monitor weather

patterns while simultaneously improving

efficiency.

U.S. Meat, Seafood, and Dairy Historical Margins

0%

1%

2%

3%

4%

5%

6%

7%

2008 2009 2010 2011 2012

Source: Bloomberg

EBITDA Margin

15.70%

11.60%

5.60%

5.60%

3%

61.50%

Source: IBISWorld

Tyson Foods Inc. JBS SA Cargill Inc.

Smithfield Foods Inc. Hormel Foods Corporation Other

U.S. Meat and Poultry Processors Market Share Data

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 7 www.mercercapital.com

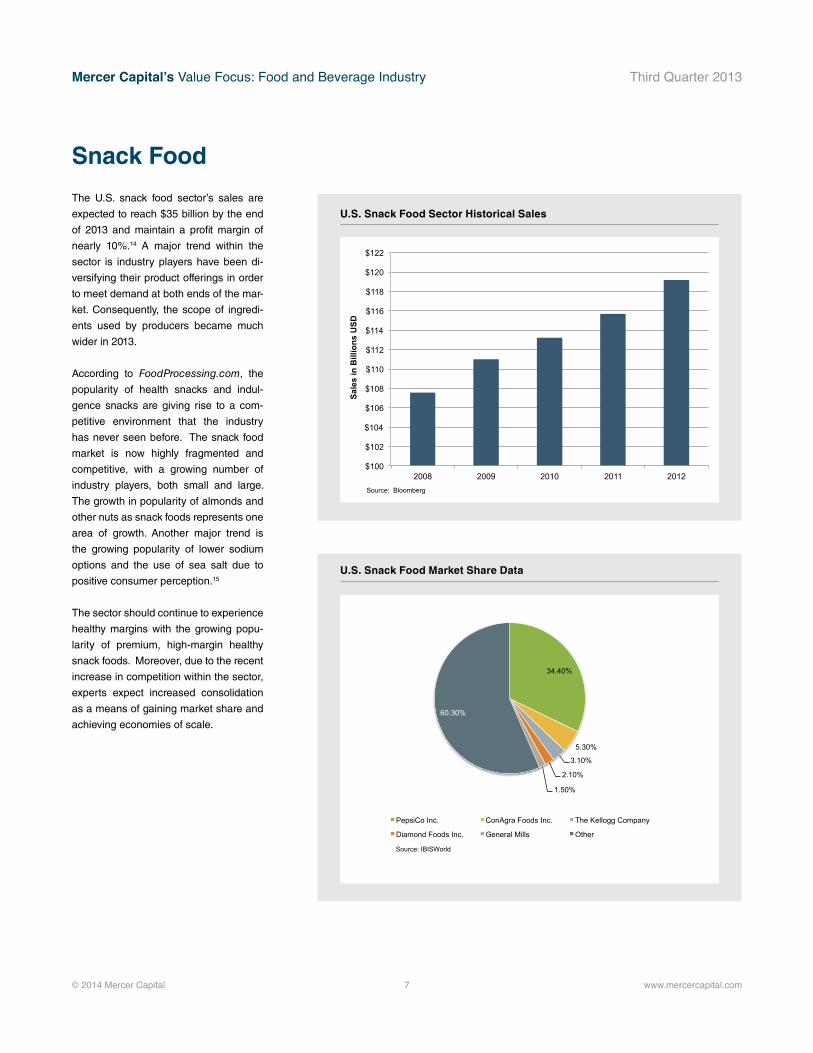

Snack Food

The U.S. snack food sector’s sales are

expected to reach $35 billion by the end

of 2013 and maintain a profit margin of

nearly 10%.14 A major trend within the

sector is industry players have been di-

versifying their product offerings in order

to meet demand at both ends of the mar-

ket. Consequently, the scope of ingredi-

ents used by producers became much

wider in 2013.

According to FoodProcessing.com, the

popularity of health snacks and indul-

gence snacks are giving rise to a com-

petitive environment that the industry

has never seen before. The snack food

market is now highly fragmented and

competitive, with a growing number of

industry players, both small and large.

The growth in popularity of almonds and

other nuts as snack foods represents one

area of growth. Another major trend is

the growing popularity of lower sodium

options and the use of sea salt due to

positive consumer perception.15

The sector should continue to experience

healthy margins with the growing popu-

larity of premium, high-margin healthy

snack foods. Moreover, due to the recent

increase in competition within the sector,

experts expect increased consolidation

as a means of gaining market share and

achieving economies of scale.

$100

$102

$104

$106

$108

$110

$112

$114

$116

$118

$120

$122

2008 2009 2010 2011 2012

Sale

s in

Bill

ions

USD

Source: Bloomberg

U.S. Snack Food Sector Historical Sales

U.S. Snack Food Market Share Data

34.40%

5.30%

3.10%

2.10%

1.50%

60.30%

Source: IBISWorld

PepsiCo Inc. ConAgra Foods Inc. The Kellogg Company

Diamond Foods Inc. General Mills Other

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 8 www.mercercapital.com

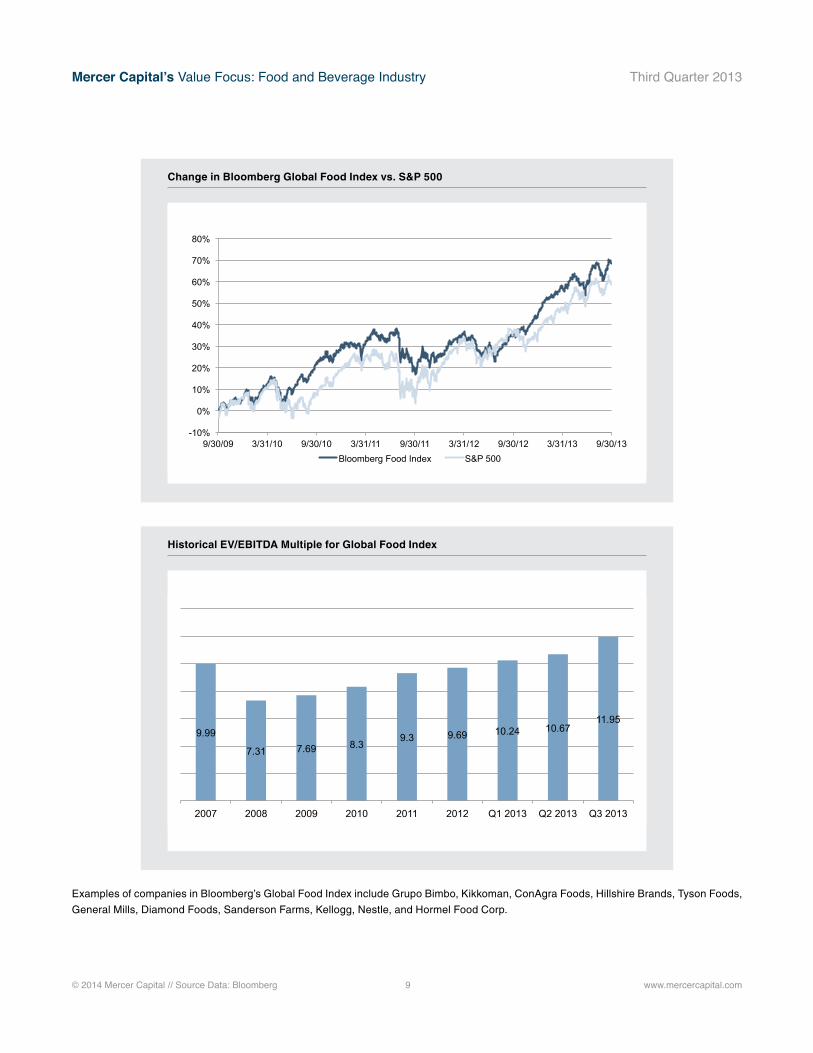

In third quarter 2013 food and beverage companies continued to

recover from the recession. As indicated by the Bloomberg Bever-

age and Global Food Indices, recovery for the beverage sector has

generally outpaced the processed food sector. However, the bever-

age sector underperformed the S&P 500 in the most recent quarter

while the Bloomberg Global Food Index was up 6.4% for the quarter

(compared to 4.7% for the S&P). Likewise, EBITDA multiples for food

companies saw an improvement in the third quarter while multiples

for beverage companies relaxed in comparison to the prior quarter.

In terms of earnings, Q3 had mixed results. While Kraft fell short of

earning’s expectations following the spinoff of its global snack food

brands to Mondelez International, Pepsi exceeded expectations, in

part due to cost-cutting and productivity improvements. While global

firms generally benefited from recovery in the US and growth in Latin

America, weak growth in China and slow recovery in Europe con-

tinue to be areas of concern. Consensus estimates for consumer

staples for the remainder of 2013 reflect modest growth in the fourth

quarter and annual growth of 5.5%. Looking into 2014, earnings are

expected to growth 9.3% with revenue growth of 4.1%.16

For restaurants, Q3 was largely disappointing. Same store sales

growth remained modest, while traffic continued to decrease. Con-

cerns about the budget crisis in Washington are believed to partially

account for the sector’s lackluster performance. Fast-food remained

a bright spot with operators reporting a 0.8% increase in traffic during

the month of September. Going forward, 55% of restaurant operators

surveyed have a positive outlook going into Q4.17

According to Bloomberg, the food processing industry had 201

pending or completed deals, down from 223 in the prior annual vol-

ume. Deal values during the most recent twelve months average

$303.5 million, a substantial increase from an average of $132.7 mil-

lion in the prior annual period. As shown below, major transactions

in the first quarter of 2013 contributed to the increase in deal values,

including the $23 billion acquisition of Heinz by Berkshire Hathaway

and 3G Capital. Transactions were motivated by the opportunity

to expand product portfolios to international products and acquire

attractive distribution systems.

General Food & Beverage Overview

1 “Frozen Food Production in the US,” IBISWorld, May 2014.2 “Bread Production in the US,” IBISWorld, July 2014.3 “Product Development: Frozen Food Sales’ Decline Paves the

Way for Fresh Food Innovation,” Food Processing, Online,

Available http://www.foodprocessing.com/articles/2013/frozen-

to-fresh/?start=1, Accessed July 15, 2014. 4 “Frozen Food Production in the US,” IBISWorld, May 2014.5 Ibid.6 “Heinz Plant to Close: 410 to Lose Jobs as Frozen-Food Facility

Shuts Down Incrementally,” Idaho State Journal, Online, Avail

able http://www.idahostatejournal.com/members/heinz-plant-to-

close-to-lose-jobs-as-frozen-food/article_425a8036-4d70-11e3-

a95c-0019bb2963f4.html, Accessed July 22, 2014.7 “Why Hot Pockets is Struggling and About to Lay Off a Bunch of

Workers,” Business Insider, Online, Available http://business

insider.com/hot-pockets-layoffs-2012-1, Accessed June 24,

2014. 8 “Ice Cream Production in the US,” IBISWorld, June 2014. 9 “Can the Struggling Ice Cream Industry Survive?,” Dairy Herd

Management, Online, Available http://www.dairyherd.com/dairy-

news/Survival-lessons-from-the-ice-cream-industry-212790671.

html, Accessed June 26, 2014.

10 “Bread Production in the US,” IBISWorld, July 2014.11 “Flowers Foods Completes Acquisition of Sara Lee and

Earthgrains Assets in California,” Vending Marketwatch, Online,

Available http://www.vendingmarketwatch.com/news/10884327/

flowers-foods-completes-acquisition-of-sara-lee-and-earth

grains-assets-in-california, Accessed June 27, 2014. 12 “Meat, Beef, and Poultry Processing in the US,” IBISWorld, July

2014. 13 “Porcine Epidemic Diarrhea (PED),” USDA, Online, Available

https://www.aasv.org/aasv%20website/Resources/Diseases/

Por

cineEpidemicDiarrhea.php, Accessed July 10, 2014.14 “Snack Food Production in the US,” IBISWorld, April 2014.15 “Snack Trends 2013: Health and Indulgences Square Off,” Food

Processing, Online, Available http://www.foodprocessing.com/

articles/2013/snack-trends/?start=0, Accessed July 11, 2014.16 “Consumer Staples Stock Outlook – October 2013,” Zacks,

Online, Available http://www.zacks.com/commentary/29555/con

sumer-staples-stock-outlook---oct-2013.17 “Government shutdown takes toll on restaurant sales, traffic,”

Nation’s Restaurant News, Online, Available http://nrn.com/miller

pulse/government-shutdown-takes-toll-restaurant-sales-traffic.

References and Data Sources

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital // Source Data: Bloomberg 9 www.mercercapital.com

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

9/30/09 3/31/10 9/30/10 3/31/11 9/30/11 3/31/12 9/30/12 3/31/13 9/30/13 Bloomberg Food Index S&P 500

9.99

7.31 7.69 8.3 9.3 9.69 10.24 10.67

11.95

2007 2008 2009 2010 2011 2012 Q1 2013 Q2 2013 Q3 2013

Change in Bloomberg Global Food Index vs. S&P 500

Historical EV/EBITDA Multiple for Global Food Index

Examples of companies in Bloomberg’s Global Food Index include Grupo Bimbo, Kikkoman, ConAgra Foods, Hillshire Brands, Tyson Foods,

General Mills, Diamond Foods, Sanderson Farms, Kellogg, Nestle, and Hormel Food Corp.

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

Examples of companies in Bloomberg’s Global Food Index include Grupo Bimbo, Kikkoman, ConAgra Foods, Hillshire Brands, Tyson Foods,

General Mills, Diamond Foods, Sanderson Farms, Kellogg, Nestle, and Hormel Food Corp.

© 2014 Mercer Capital // Data Source: Bloomberg 10 www.mercercapital.com

-20%

0%

20%

40%

60%

80%

100%

120%

9/30/09 3/31/10 9/30/10 3/31/11 9/30/11 3/31/12 9/30/12 3/31/13 9/30/13

Bloomberg Beverage Index S&P 500

Historical EV / EBITDA MultipleBloomberg Beverage Index

8.51 9.57

10.96 10.29 10.81 11.89 12.42

10.94

2008 2009 2010 2011 2012 Q1 2013 Q2 2013 Q3 2013

Change in Bloomberg Beverage Index vs. S&P 500

Historical EV/EBITDA Multiple for Beverage Index

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

© 2014 Mercer Capital 11 www.mercercapital.com

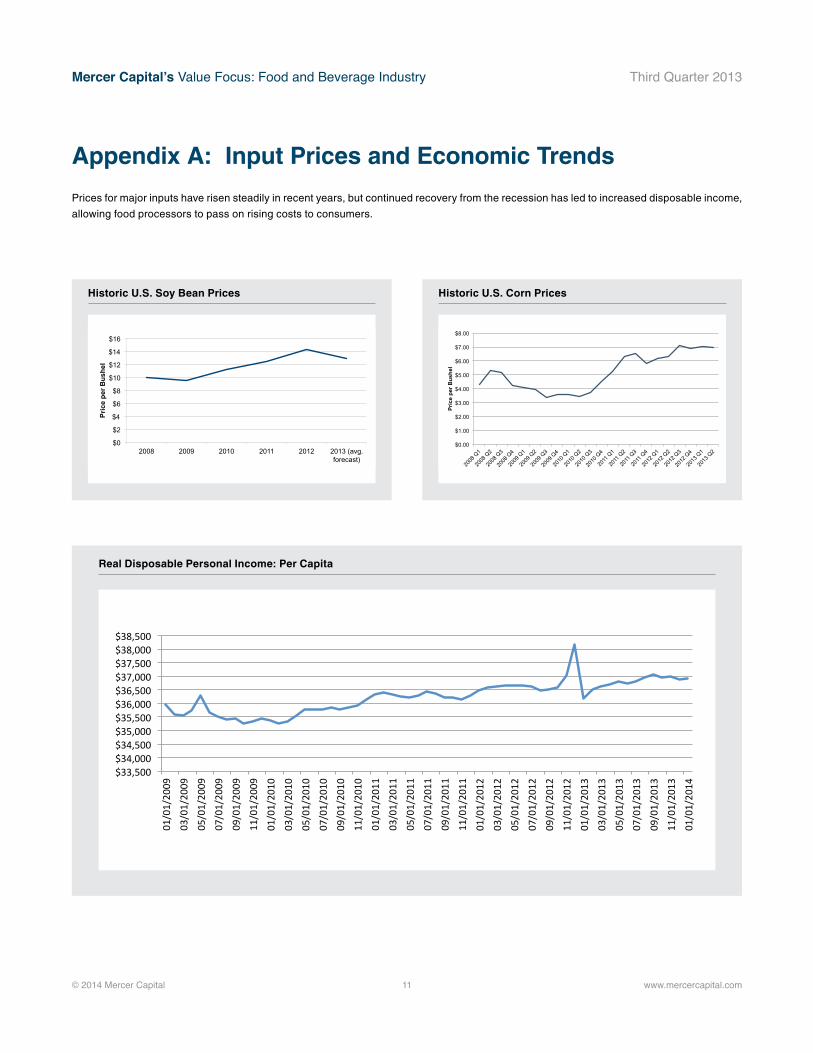

Prices for major inputs have risen steadily in recent years, but continued recovery from the recession has led to increased disposable income,

allowing food processors to pass on rising costs to consumers.

Appendix A: Input Prices and Economic Trends

$33,500 $34,000 $34,500 $35,000 $35,500 $36,000 $36,500 $37,000 $37,500 $38,000 $38,500

01/01/20

09

03/01/20

09

05/01/20

09

07/01/20

09

09/01/20

09

11/01/20

09

01/01/20

10

03/01/20

10

05/01/20

10

07/01/20

10

09/01/20

10

11/01/20

10

01/01/20

11

03/01/20

11

05/01/20

11

07/01/20

11

09/01/20

11

11/01/20

11

01/01/20

12

03/01/20

12

05/01/20

12

07/01/20

12

09/01/20

12

11/01/20

12

01/01/20

13

03/01/20

13

05/01/20

13

07/01/20

13

09/01/20

13

11/01/20

13

01/01/20

14

Real Disposable Personal Income: Per Capita

$0

$2

$4

$6

$8

$10

$12

$14

$16

2008 2009 2010 2011 2012 2013 (avg. forecast)

Pric

e pe

r Bus

hel

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

Pric

e pe

r Bus

hel

Historic U.S. Soy Bean Prices Historic U.S. Corn Prices

© 2014 Mercer Capital // www.mercercapital.com 12

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

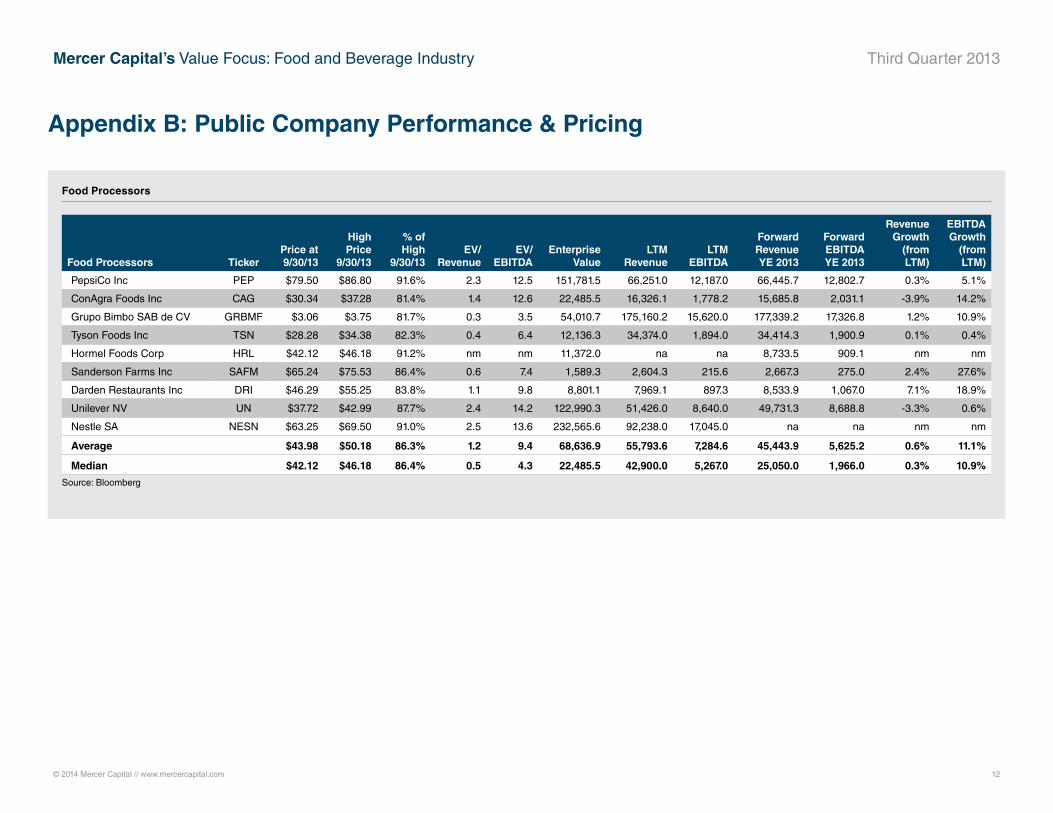

Appendix B: Public Company Performance & Pricing

Food Processors

Food Processors TickerPrice at 9/30/13

High Price

9/30/13

% of High

9/30/13EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2013

Forward EBITDA YE 2013

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

PepsiCo Inc PEP $79.50 $86.80 91.6% 2.3 12.5 151,781.5 66,251.0 12,187.0 66,445.7 12,802.7 0.3% 5.1%

ConAgra Foods Inc CAG $30.34 $37.28 81.4% 1.4 12.6 22,485.5 16,326.1 1,778.2 15,685.8 2,031.1 -3.9% 14.2%

Grupo Bimbo SAB de CV GRBMF $3.06 $3.75 81.7% 0.3 3.5 54,010.7 175,160.2 15,620.0 177,339.2 17,326.8 1.2% 10.9%

Tyson Foods Inc TSN $28.28 $34.38 82.3% 0.4 6.4 12,136.3 34,374.0 1,894.0 34,414.3 1,900.9 0.1% 0.4%

Hormel Foods Corp HRL $42.12 $46.18 91.2% nm nm 11,372.0 na na 8,733.5 909.1 nm nm

Sanderson Farms Inc SAFM $65.24 $75.53 86.4% 0.6 7.4 1,589.3 2,604.3 215.6 2,667.3 275.0 2.4% 27.6%

Darden Restaurants Inc DRI $46.29 $55.25 83.8% 1.1 9.8 8,801.1 7,969.1 897.3 8,533.9 1,067.0 7.1% 18.9%

Unilever NV UN $37.72 $42.99 87.7% 2.4 14.2 122,990.3 51,426.0 8,640.0 49,731.3 8,688.8 -3.3% 0.6%

Nestle SA NESN $63.25 $69.50 91.0% 2.5 13.6 232,565.6 92,238.0 17,045.0 na na nm nm

Average $43.98 $50.18 86.3% 1.2 9.4 68,636.9 55,793.6 7,284.6 45,443.9 5,625.2 0.6% 11.1%

Median $42.12 $46.18 86.4% 0.5 4.3 22,485.5 42,900.0 5,267.0 25,050.0 1,966.0 0.3% 10.9%

Source: Bloomberg

© 2014 Mercer Capital // www.mercercapital.com 13

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

Appendix B: Public Company Performance & Pricing

Restaurants

Restaurants TickerPrice at 9/30/13

High Price

9/30/13

% of High

9/30/13EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2013

Forward EBITDA YE 2013

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

Frisch's Restaurants Inc FRS $24.13 $26.44 91.3% 0.7 6.1 137.5 204.3 22.4 202.0 na -1.1% nm

Ruby Tuesday Inc RT $7.50 $9.90 75.8% 0.6 18.8 735.0 1,213.2 39.1 1,266.0 95.0 4.3% 142.9%

Darden Restaurants Inc DRI $46.29 $55.25 83.8% 1.1 9.8 8,801.1 7,969.1 897.3 8,533.9 1,067.0 7.1% 18.9%

Denny's Corp DENN $6.11 $7.51 81.4% 1.6 10.0 721.4 464.3 72.3 463.9 77.3 -0.1% 6.9%

Bob Evans Farms Inc/DE BOBE $57.27 $60.22 95.1% 1.3 11.3 1,790.4 1,336.2 157.8 1,590.3 189.5 19.0% 20.1%

DineEquity Inc DIN $69.00 $85.74 80.5% 4.1 10.3 2,650.1 641.2 257.2 642.3 267.3 0.2% 3.9%

Red Robin Gourmet Burgers Inc RRGB $71.10 $86.83 81.9% 1.1 10.5 1,096.7 998.6 104.4 1,017.8 106.3 1.9% 1.8%

Cracker Barrel Old Country Store Inc CBRL $103.18 $118.63 87.0% 1.1 10.7 2,855.3 2,644.6 267.6 2,648.0 271.6 0.1% 1.5%

Average $48.07 $56.31 84.6% 1.4 10.9 2,348.4 1,934.0 227.3 2,045.5 296.3 3.9% 28.0%

Median $51.78 $57.73 82.8% 1.1 10.4 1,443.5 1,105.9 131.1 1,141.9 189.5 1.0% 6.9%

Source: Bloomberg

© 2014 Mercer Capital // www.mercercapital.com 14

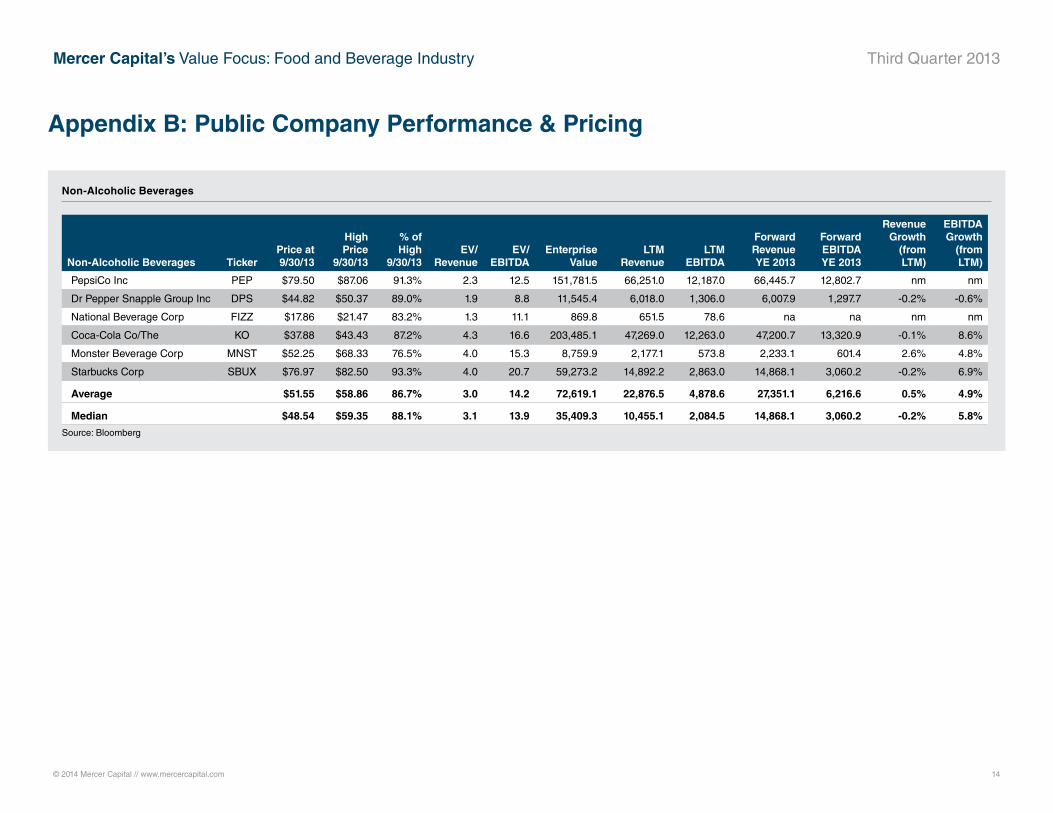

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

Non-Alcoholic Beverages

Non-Alcoholic Beverages TickerPrice at 9/30/13

High Price

9/30/13

% of High

9/30/13EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2013

Forward EBITDA YE 2013

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

PepsiCo Inc PEP $79.50 $87.06 91.3% 2.3 12.5 151,781.5 66,251.0 12,187.0 66,445.7 12,802.7 nm nm

Dr Pepper Snapple Group Inc DPS $44.82 $50.37 89.0% 1.9 8.8 11,545.4 6,018.0 1,306.0 6,007.9 1,297.7 -0.2% -0.6%

National Beverage Corp FIZZ $17.86 $21.47 83.2% 1.3 11.1 869.8 651.5 78.6 na na nm nm

Coca-Cola Co/The KO $37.88 $43.43 87.2% 4.3 16.6 203,485.1 47,269.0 12,263.0 47,200.7 13,320.9 -0.1% 8.6%

Monster Beverage Corp MNST $52.25 $68.33 76.5% 4.0 15.3 8,759.9 2,177.1 573.8 2,233.1 601.4 2.6% 4.8%

Starbucks Corp SBUX $76.97 $82.50 93.3% 4.0 20.7 59,273.2 14,892.2 2,863.0 14,868.1 3,060.2 -0.2% 6.9%

Average $51.55 $58.86 86.7% 3.0 14.2 72,619.1 22,876.5 4,878.6 27,351.1 6,216.6 0.5% 4.9%

Median $48.54 $59.35 88.1% 3.1 13.9 35,409.3 10,455.1 2,084.5 14,868.1 3,060.2 -0.2% 5.8%

Source: Bloomberg

Appendix B: Public Company Performance & Pricing

© 2014 Mercer Capital // www.mercercapital.com 15

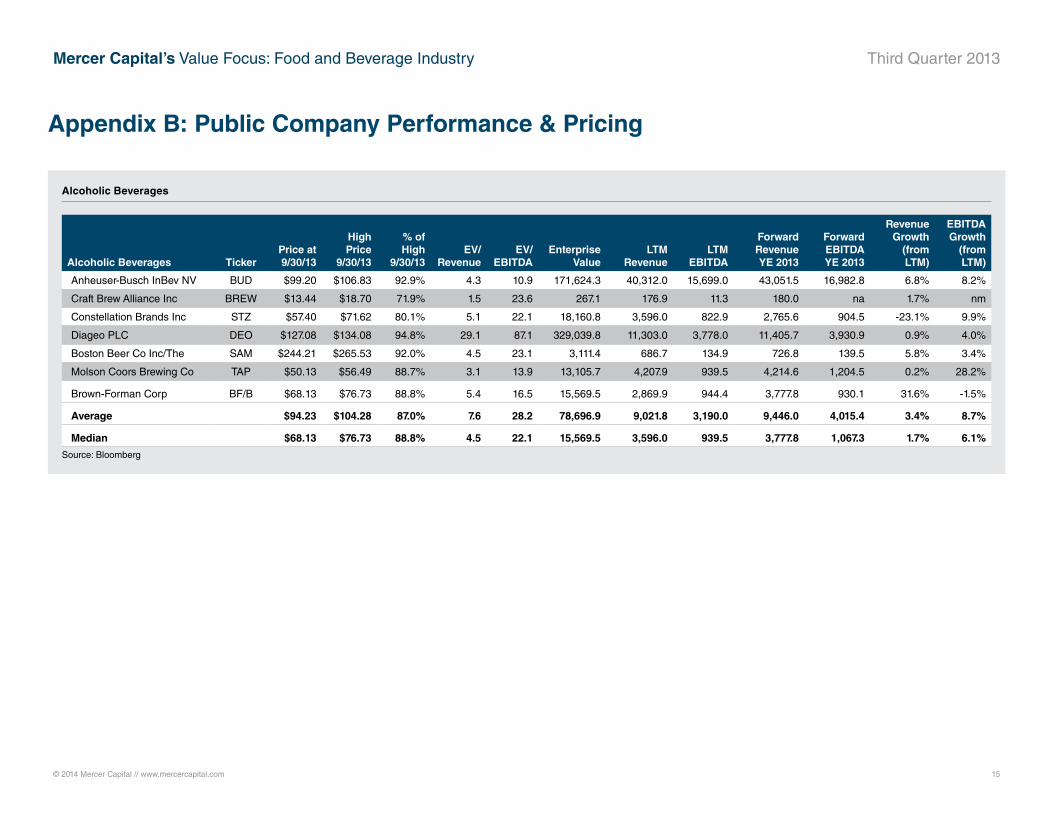

Mercer Capital’s Value Focus: Food and Beverage Industry Third Quarter 2013

Alcoholic Beverages

Alcoholic Beverages TickerPrice at 9/30/13

High Price

9/30/13

% of High

9/30/13EV/

RevenueEV/

EBITDA Enterprise

Value LTM

RevenueLTM

EBITDA

Forward Revenue YE 2013

Forward EBITDA YE 2013

Revenue Growth

(from LTM)

EBITDA Growth

(from LTM)

Anheuser-Busch InBev NV BUD $99.20 $106.83 92.9% 4.3 10.9 171,624.3 40,312.0 15,699.0 43,051.5 16,982.8 6.8% 8.2%

Craft Brew Alliance Inc BREW $13.44 $18.70 71.9% 1.5 23.6 267.1 176.9 11.3 180.0 na 1.7% nm

Constellation Brands Inc STZ $57.40 $71.62 80.1% 5.1 22.1 18,160.8 3,596.0 822.9 2,765.6 904.5 -23.1% 9.9%

Diageo PLC DEO $127.08 $134.08 94.8% 29.1 87.1 329,039.8 11,303.0 3,778.0 11,405.7 3,930.9 0.9% 4.0%

Boston Beer Co Inc/The SAM $244.21 $265.53 92.0% 4.5 23.1 3,111.4 686.7 134.9 726.8 139.5 5.8% 3.4%

Molson Coors Brewing Co TAP $50.13 $56.49 88.7% 3.1 13.9 13,105.7 4,207.9 939.5 4,214.6 1,204.5 0.2% 28.2%

Brown-Forman Corp BF/B $68.13 $76.73 88.8% 5.4 16.5 15,569.5 2,869.9 944.4 3,777.8 930.1 31.6% -1.5%

Average $94.23 $104.28 87.0% 7.6 28.2 78,696.9 9,021.8 3,190.0 9,446.0 4,015.4 3.4% 8.7%

Median $68.13 $76.73 88.8% 4.5 22.1 15,569.5 3,596.0 939.5 3,777.8 1,067.3 1.7% 6.1%

Source: Bloomberg

Appendix B: Public Company Performance & Pricing

Mercer CapitalFood & Beverage Industry Services

Contact Us

Copyright © 2014 Mercer Capital Management, Inc. All rights reserved. It is illegal under Federal law to reproduce this publication or any portion of its contents without the publisher’s permission. Media

quotations with source attribution are encouraged. Reporters requesting additional information or editorial comment should contact Barbara Walters Price at 901.685.2120. Mercer Capital’s Industry

Focus is published quarterly and does not constitute legal or financial consulting advice. It is offered as an information service to our clients and friends. Those interested in specific guidance for legal or

accounting matters should seek competent professional advice. Inquiries to discuss specific valuation matters are welcomed. To add your name to our mailing list to receive this complimentary publication,

visit our web site at www.mercercapital.com.

Mercer Capital has expertise providing business valuation and financial advisory services to companies in the food and beverage industry.

Industry Segments

Mercer Capital serves the following industry segments:

• Food processing

• Restaurants

• Nonalcoholic Beverages

• Malt, Wine, and Spirits

Services Provided

• Valuation of food and beverage industry companies

• Transaction advisory for acquisitions and divestitures

• Valuations for purchase accounting and impairment testing

• Fairness and solvency opinions

• Litigation support for economic damages and valuation and shareholder disputes

Contact a Mercer Capital professional to discuss your needs in confidence.

Matthew R. Crow, CFA, [email protected]

Timothy R. Lee, [email protected]

Nicholas J. Heinz, [email protected]

Travis W. Harms, CFA, CPA/[email protected]

Mercer Capital5100 Poplar Avenue, Suite 2600Memphis, Tennessee 38137901.685.2120 (P)

www.mercercapital.com

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES