valuation report for bm&fbovespair.bmfbovespa.com.br/enu/2721/2016 04 15_valuation...

TRANSCRIPT

April 9th, 2016

Valuation Report for BM&FBovespa

1

Table of Contents

Section 1 Executive Summary 2

Section 2 UBS Information and Declarations 10

Section 3 Cetip 16

3.A Company and Sector Overview

3.B Valuation

Section 4 BM&FBovespa 36

4.A Company and Sector Overview

4.B Valuation

Appendix A Selected Comparable Companies for Cetip and BM&FBovespa 50

Appendix B Selected Analyst Estimates for Cetip 56

Appendix C Selected Analyst Estimates for BM&FBovespa 58

Appendix D Additional Materials 60

Appendix E Glossary 63

Appendix F Disclaimer 65

Executive Summary

Section 1

3

In the context of the corporate reorganization involving BM&FBOVESPA S.A. - Bolsa de Valores, Mercadorias e Futuros ("BM&FBovespa") and Cetip S/A – Mercados Organizados ("Cetip") that may result in among other things, the acquisition of Cetip shares by BM&FBovespa and an issuance of shares of BM&FBovespa to Cetip shareholders, which the terms and conditions were disclosed to the market on April 8, 2016 (the "Transaction"), UBS Brasil Serviços de Assessoria Financeira Ltda. ("UBS") was hired by BM&FBovespa to prepare a valuation report (the "Valuation Report")

This Valuation Report was prepared in accordance with the applicable regulation and following market practices of evaluating companies and shall be used exclusively for the benefit of the BM&FBovespa's Board of Directors in the sole purpose of enabling them to evaluate the Transaction

In this Valuation Report, Cetip and BM&FBovespa share prices were assessed according to the following criteria:

Cetip

• Shareholders' equity book value per share as of December 31st, 2015

• Volume weighted average price ("VWAP")

– in the 12-month period ending on November 2nd, 2015 (the day prior to the First Material Fact regarding the transaction) and beginning on November 3rd, 2014

– in the 1-month period ending November 2nd, 2015 (the day prior to the First Material Fact regarding the transaction) and beginning on October 3rd, 2015

– from November 3rd, 2015 (the day of the First Material Fact regarding the transaction) and April 5th, 2016

• Discounted Cash Flow method ("DCF")

• Selected trading multiples methodology

BM&FBovespa

• Shareholders' equity book value per share as of December 31st, 2015

• Volume weighted average price ("VWAP")

– in the 12-month period ending on November 2nd, 2015 (the day prior to the First Material Fact regarding the transaction) and beginning on November 3rd, 2014

– in the 1-month period ending November 2nd, 2015 (the day prior to the First Material Fact regarding the transaction) and beginning on October 3rd, 2015

– from November 3rd, 2015 (the day after the First Material Fact regarding the transaction) and April 5th, 2016

• Selected trading multiples methodology

Except as otherwise stated, all financial information used was prepared according to the International Financial Reporting Standards ("IFRS")

UBS’s analysis does not include all of the pertinent information to determine the appropriateness of the transaction to BM&FBovespa and Cetip¹

Introduction

Note: 1 This Valuation Report does not consider the potential value of synergies, the value of instruments or other elements of the transaction structure, nor any benefits or disadvantages of the

transaction

4

On November 3rd, 2015, BM&FBovespa informed the market that it had engaged in preliminary discussions with Cetip to present their respective Boards of Directors with a proposal for the combination of both companies ("First Material Fact")

on November 13th, 2015, BM&FBovespa informed the market that a non-binding proposal was approved by its Board of Directors consisting on a valuation of R$39.00 per Cetip share (which represented a 15.5% premium compared to Cetip's closing price on October 30th, 2015¹) via a minimum 50% cash and maximum 50% stock transaction

On December 4th, 2015, BM&FBovespa informed the market that it had received correspondence sent by the Board of Directors of Cetip expressing that the non-binding proposal for the combination of the two companies sent by BM&FBovespa did not represent the fair value of Cetip

On February 19th, 2016, BM&FBovespa informed the market that its Board of Directors approved the presentation, to the Board of Directors of Cetip, of a binding proposal for the combination of the operations of the companies

the binding proposal described the terms of a corporate reorganization and adjustment of the previous proposal to R$41.00 per Cetip share, which was to consist in a payment of 75% cash (R$30.75) and 25% stock (R$10.25) with an exchange ratio of 0.8991 ordinary BM&FBovespa's shares for each Cetip share. Based on this exchange ratio, the current shareholders of Cetip would own 11.8% of BM&FBovespa’s capital stock after the transaction²

the amount to be paid in cash would be subject to adjustment to the Certificado de Depósito Bancário—Interbank Deposit Certificate ("CDI") from the date of the general shareholder's meeting of Cetip that would approve the transaction until the date of effective payment of the amount to Cetip's shareholders

On March 2nd, 2016, BM&FBovespa received a communication from Cetip's Board of Directors deciding:

not to accept, in the specific terms presented, the proposal for the acquisition of Cetip's shares submitted by BM&FBovespa on February 19th, 2016

to authorize its financial and legal advisors to initiate discussions about the proposed transaction; and

to authorize the signing, by Cetip’s Management, of a confidentiality agreement related to the aforementioned discussions

Transaction Background

Source: BM&FBovespa's Material Facts Notes: 1 Last day of trading prior to the release of the material fact related to the discussions about a potential combination, adjusted for dividends declared on November 4, 2015 2 The amount of R$ 11.40 per BM&FBovespa share was used, which is the closing price as of October 30, 2015, date that preceded the disclosure of the First Material Fact regarding the transaction

5

On April 8th, 2016, BM&FBovespa and Cetip published a joint material fact announcing a new offer with a floor for Cetip of R$42.00/share and a cap of R$48.51/share. According to the material fact terms, BM&FBovespa and Cetip shareholders will vote to approve a corporate reorganization in which BM&FBovespa will own all the shares issued by Cetip and Cetip shareholders will receive (i) shares of BM&FBovespa in an exchange ratio of 0.8991x for each Cetip share (“Reference Exchange Ratio”) and (ii) R$30.75 in cash (the “Original Reference Value of the Cash Portion”), to be paid in a lump sum no later than forty (40) days after all regulatory approvals required by the legislation have been obtained (“Financial Settlement Date”)

the Original Reference Value of the Cash Portion will be subject to adjustment by the variation in the CDI ("Adjusted Cash Portion") (a) between April 8th, 2016 and the Financial Settlement Date, inclusive, if the call for its General Shareholders Meeting to discuss the Transaction is disclosed by CETIP via CVM’s system by April 15, 2016, so such meeting is held until May 16, 2016 (on first call); or (b) between the date of the General Shareholders Meeting of CETIP that approves the Transaction and the Financial Settlement Date, if the call for the General Shareholders Metting of Cetip to deliberate on the Transaction is disclosed via CVM's system after April 15, 2016

the Adjusted Cash Portion and Reference Exchange Ratio will be adjusted to reflect any dividends, interest on capital and other corporate actions declared and paid by BM&FBovespa between November 4, 20151 , and the date of computing the shareholder base (ex-date) up to the Financial Settlement Date, inclusive (“BM&FBovespa’s Corporate Actions”). The Reference Exchange Ratio will be ajusted so that the product of (i) a new exchange ratio (“Corporate Actions Adjusted Exchange Ratio”) and (ii) the result of subtracting (a) BM&FBOVESPA’s Corporate Actions from (b) R$11.40 is always kept constant at R$10.25

Corporate Actions Adjusted Exchange Ratio on April 8th, 2016, was at 0.9358x and the value of the Adjusted Cash Portion was R$29.90

the value of the stock component to be received by Cetip’s shareholders is subject to a minimum of R$11.25 and maximum of R$17.76

for the purposes of adjustments in the stock component, BM&FBovespa share price ("Average Closing Price") will be calculated using the closing price of the 30 trading days prior to the Financial Settlement Date

final transaction structure regarding cash and stock components will be based on 2 scenarios:

(i) if the product of the Adjusted Exchange Ratio and the Average Closing Price ("Adjusted Price") is higher than the R$17.76, the R$30.75 of cash component will be fixed and the Adjusted Exchange Ratio will be proportionally reduced (“Reduced Exchange Ratio”) until the product of the Reduced Exchange Ratio and the Average Closing Price is R$17.76

(ii) if the Adjusted Price is lower than R$11.25, the R$30.75 of cash component will be raised by an additional amount ("Additional Amount") until it equals 85% of the total amount to be paid to Cetip's shareholders

the Additional Amount will be equal to the amount required to equal R$11.25 by adding the Additional Amount to the Adjusted Price

if, after fixing the cash component at 85% of total amount to be paid to Cetip's shareholders, the R$11.25 threshold is not achieved, the Adjusted Exchange Ratio will be raised to a new exchange ratio (“Augmented Exchange Ratio”) until the sum of (a) product of the Augmented Exchange Ratio and the Transaction Price and (b) Additional Amount equals to R$11.25

Transaction Background (cont'd)

Source: BM&FBovespa's Material Facts Note: 1 BM&FBOVESPA declared interest on capital (IoC) of R$ 0.1765 per share on November 13, 2015, and R$0.2525 per share on December 10, 2015. CETIP declared corporate actions of R$0.3326 per share on November 4, 2015, R$0.0994 per

share on December 18, 2015, R$0.3194 per share on March 2, 2016, and R$0.0843 per share on March 15, 2016

6

Cetip: Description of Valuation Methodologies Stated Herein UBS has performed a multi-approach valuation of Cetip's shares based on different criteria: discounted cash flow, volume weighted average price, book value and selected trading multiples analysis¹

Description Relevance

VWAP

Average of the daily prices for Cetip weighted by the daily volumes

from November 3rd, 2014 to November 2nd, 2015 (1 year VWAP to First Material Fact)

from October 3rd, 2015 to November 2nd, 2015 (1 month VWAP to First Material Fact)

from November 3rd, 2015 to April 5th, 2016

Daily share price of Cetip calculated as average of the prices of each trade, weighted by the volume of traded shares

This methodology takes into account current market value of the company

represents market participants' view of overall value

given high liquidity of Cetip’s shares, the volume-weighted historical price of the shares is a reasonable view of the company's value by the market

Book Value Shareholders’ equity according to Cetip's balance sheet under IFRS as of

December 31st, 2015 divided by the total number of shares excluding treasury shares

This methodology only takes into account historical accounting value of the company

does not account for business and operating profile, excluding growth prospects, profitability and future return profile to shareholders

Selected Trading Multiples

Median of price to earnings (P/E) and enterprise value to EBITDA (EV/EBITDA) multiples of selected comparable companies based on consensus analyst estimates for 2016E and 2017E

Comparable companies chosen based on a number of factors including business mix, relative size and market position

Reflects the company's value based on the valuation of comparable companies, without taking into consideration all of the company-specific characteristics

Represents two of the most common valuation multiples for exchanges used by equity investors and research analysts

Discounted Cash Flow (DCF)

Analysis based on long term financial projections of the company

Calculated based on discounted unlevered cash flows to firm and as a stand-alone basis

No potential synergies arising from the transaction were considered

Reflects the best estimates of BM&FBovespa as to the expected future financial performance of Cetip

Captures company's expected performance in the short, medium and long term

Identifies key value creation factors and allows evaluation of the sensitivity to each of these factors

Projections may be affected by subjective considerations

Note: 1 UBS based its analysis and valuation of Cetip exclusively with information publicly available to the market or directly provided by BM&FBovespa

Relevance = Very high = High = Moderate = Low = Very Low

7

VWAP

Nov 3, 2014 to

Nov 2, 2015

Oct 3, 2015 to

Nov 2, 2015

Nov 3, 2015 to

Apr 5, 2016

Book Value

Selected Trading Multiples

EV / EBITDA

P / E

DCF R$41.33

R$37.26

R$35.82

R$6.53

R$38.24

R$34.29

R$33.26

R$45.45

R$40.97

R$39.39

0.00 10.00 20.00 30.00 40.00 50.00 60.00

Valuation Output for Cetip per Methodologies Herein

Valuation Approach

The valuation of Cetip shares herein is based on the following methodologies:

Volume Weighted Average Price

from November 3, 2014 to November 2, 2015 (1 year VWAP to First Material Fact)

from October 3, 2015 to November 2, 2015 (1 month VWAP to First Material Fact)

from November 3, 2015 to April 5, 2016

Book value

book value per share as of December 31, 2015

Selected Trading Multiples

indicative range of 2016E and 2017E EV / EBITDA and P / E trading multiples based on selected comparable companies1

Discounted Cash Flow

free cash flow to the firm and utilizing a perpetuity growth rate for terminal value post 2025

A variety of relevant methodologies may be appropriate. For purposes of this Valuation Report, DCF was adopted as the most relevant methodology given that it reflects BM&F's best estimates of expected future financial performance of Cetip

the valuations herein DO NOT reflect the potential impact of transaction synergies, nor other transaction benefits or disadvantages included in the transaction structure

Note: 1 Includes ASX Limited, Bolsa y Mercados Espanoles, Bolsa Mexicana de Valores, Bursa Malaysia, Deutsche Boerse, Intercontinental Exchange, Singapore Exchange and TMX Group

Valuation Output for Cetip Share Price (R$ per share)

8

BM&FBovespa: Description of Valuation Methodologies Stated Herein

UBS has performed a multi-approach valuation of BM&FBovespa's shares based on different criteria: volume weighted average price, book value and selected trading multiples analysis

Description Relevance

VWAP

Average of the daily prices for BM&FBovespa weighted by the daily volumes

from November 3rd, 2014 to November 2nd, 2015 (1 year VWAP to First Material Fact)

from October 3rd, 2015 to November 2nd, 2015 (1 month VWAP to First Material Fact)

from November 3rd, 2015 to April 5th, 2016

Daily share price of BM&FBovespa calculated as average of the prices of each trade, weighted by the volume of traded shares

This methodology takes into account the market value of the company

represents market participants view of overall value

given high liquidity of BM&FBovespa's shares, the volume-weighted historical price of the shares is a reasonable view of the company's value by the market

Stock consideration for the transaction will be paid with liquid shares

BM&FBovespa is the 6th most liquid stock¹ in Brazilian market with a highly dispersed shareholder base

VWAP captures market's best view of fair value and it's less a biased methodology because company is a true corporation

Based on the Reference Exchange Ratio, the largest shareholder of Cetip will own 1.4%² of the combined company that represents 1.1 days of trading1,2

Book Value Shareholders’ equity according to BM&FBovespa's balance sheet under IFRS as of

December 31st, 2015 divided by the total number of shares excluding treasury shares

This methodology only takes into account historical accounting value of the company

does not account for the business and operating profile, excluding growth prospects, profitability and future return profile to shareholders

Selected Trading Multiples

Median of price to earnings (P/E) and enterprise value to EBITDA (EV/EBITDA) multiples of selected comparable companies based on consensus analyst estimates for 2016E and 2017E

Comparable companies chosen based on a number of factors including business mix, relative size and market position

Reflects the company's value based on the valuation of comparable companies, without taking into consideration all of the company-specific characteristics

Represents two of the most common valuation multiples for exchanges used by equity investors and research analysts

Relevance = Very high = High = Moderate = Low = Very Low

Note: 1 Considering average daily volume traded in number of shares (from April 5, 2015 to April 5, 2016) 2 ICE stake as of as of March 18th, 2016 (last update of Cetip's website) 3 The percentage to be received in cash will not be inferior to 62.7% 4 This Valuation Report does not contain all of the information required to make a determination on the appropriateness, valuation nor structure of the Transaction and does not purport to convey a

recommendation with respect to pursuing or not the Transaction

• A variety of relevant methodologies may be appropriate. For purposes of this Valuation Report, Volume Weighted Average Price was adopted as the most relevant methodology given the transaction structure and that the company is highly traded and well covered by the market and research

• The adoption of same assessment criteria for both companies is only legally required in the case of transactions between related parties, which is justified because of the concern on the reciprocal treatment of non-controlling shareholders of the companies involved

• From the technical point of view (a) BM&FBovespa was evaluated by the VWAP methodology and not by DCF due to the significant portion to be paid in cash³ to Cetip's shareholders, in addition to the fact that such shares will be delivered at market value and could be sold at any time; and (b) the exclusively valuation of Cetip using the discount cash flow method is justified because, with the conclusion of the Transaction, BM&FBovespa's shareholders will become holders of the totality of Cetip's shares, from what arises the need to also know the future cash flows to be generated by a business that will be fully integrated to Bovespa

Considerations on BM&FBovespa Valuation Approach4

9

VWAP

Nov 3, 2014 to

Nov 2, 2015

Oct 3, 2015 to

Nov 2, 2015

Nov 3, 2015 to

Apr 5, 2016

Book Value

Selected Trading Multiples

EV / EBITDA

P / E R$15.43

R$9.18

R$10.30

R$12.52

R$11.67

R$10.73

R$16.97

R$10.09

5.00 8.00 11.00 14.00 17.00 20.00

Note: 1 Includes ASX Limited, Bolsa y Mercados Espanoles, Bolsa Mexicana de Valores, Bursa Malaysia, CBOE Holdings, CME Group, Deutsche Boerse, Intercontinental Exchange, Nasdaq, Singapore Exchange and

TMX Group

Valuation Output for BM&FBovespa per Methodologies Herein

Valuation Approach

The valuation of BM&FBovepa shares is based on the following methodologies:

Volume Weighted Average Price

from November 3, 2014 to November 2, 2015 (1 year VWAP to First Material Fact)

from October 3, 2015 to November 2, 2015 (1 month VWAP to First Material Fact)

from November 3, 2015 to April 5, 2016

Book value

book value per share as of December 31, 2015

Selected Trading Multiples

indicative range of 2016E and 2017E EV / EBITDA and P / E trading multiples based on selected comparable companies1

A variety of relevant methodologies may be appropriate. For purposes of this Valuation Report, Volume Weighted Average Price was adopted as the most relevant methodology given the transaction structure and that the company is highly traded and well covered by the market and research

Valuation Output for BM&FBovespa Share Price (R$ per share)

UBS Information and Declarations

Section 2

11

Information Regarding UBS UBS is a global Investment Banking platform with offices in more than 50 countries, over 50 years of experience in Brazil and 150 years worldwide

Relevant Experience

UBS has significant experience advising large companies in Brazil and globally. Among the recent transactions performed in the financial industry in Brazil, we highlight:

Among the recent transactions performed in the financial industry worldwide, we highlight:

Internal approval process

UBS's internal valuation committee reviewed the analysis performed by the project team. The committee is formed by professionals with experience in M&A and financial advisory. This committee has met with the project team and discussed the main assumptions and aspects related to the valuation methodologies presented in the Valuation Report and approved its release

Recent UBS Experience with Exchanges / FinTech Transactions

July 2015 €599 million

Joint Global Coordinator Initial Public Offering

September 2013 Undisclosed

Minority Investment in ACE Portal

April 2015 $361 million

Joint Bookrunner Initial Public Offering

September 2013 US$750 million

Joint Bookrunner 30-year Fixed Rate Senior Note Offering

May 2014 US$1.5 billion

Joint Active Bookrunner

Initial Public Offering

June 2013 A$553 million

Sole lead manager and underwriter on Equity Offering

February 2013 $500 million

Joint Bookrunner Initial Public Offering

Recent UBS Brazil Experience with Transactions Involving Companies in the Financial Sector

February 2010 US$600 million

Sole Financial Advisor Commercial and Direct Investment into CME

October 2009 US$447 million

Joint Global Coordinator and Bookrunner Initial Public Offering

Pending ~US$3 billion

Global Coordinator and Financial Advisor IPO

April 2013 US$5.1 bn

Joint Lead Manager IPO

March 2016 €27 billion

Financial Advisor to London Stock Exchange on its merger with Deutsche Börse

12

Information Regarding UBS

Source: UBS CCS

Experience in transactions involving Brazilian listed companies in the last 4 years

Company Date

December 2015

February 2015

April 2014

October 2012

August 2012

June 2012

January 2012

Transaction Value

US$187 million

US$3.5 billion

US$6.5 billion

US$120 million

Undisclosed

US$880 million

US$215 million

Transaction Description

Financial advisor to SALIC (Saudi Agricultural and Livestock Investment Company) in a private capital increase in Minerva SA

Financial Adviser to British American Tobacco to acquire the remaining stake in Souza Cruz following delisting process from the Brazilian Stock Exchange

Financial adviser and fairness opinion provider to Santander Group on its voluntary offer to acquire the minority interests in Santander Brasil

Financial Advisor to Camargo Corrêa SA to acquire the remaining stake in CCDI following delisting process from the Brazilian Stock Exchange

Advised Casino in the change of control of Grupo Pão de Açúcar

Advisor to Alphaville Urbanismo S.A. on the sale of Alphaville Participações S.A. to Gafisa

Advisor to the Independent Committee of CCR on the acquisition of three airports located in Costa Rica, Curaçao and Ecuador

13

UBS Team Responsible for the Valuation Report

Vik Hebatpuria

Managing Director—Head of Financial Technology & Services, Americas

• Vik Hebatpuria is Head of Financial Technology & Services, Americas. Prior to joining UBS in 2013, Mr. Hebatpuria was a senior banker in the Financial Institutions Group at Credit Suisse, focusing on financial technology and insurance brokerage. Before joining Credit Suisse, Mr. Hebatpuria spent 5 years as a Vice President at Marsh & McLennan developing risk management solutions related to mergers and acquisitions

• He has worked on transactions such as: the $9.1bn sale of SunGard to Fidelity National Information Services, the €599mm IPO of Flow Traders, the $1.1bn refinancing for AlixPartners, the $361mm IPO of Virtu Financial, the $1.3bn IPO of Markit, the $1.1bn refinancing for ION Trading, the $13.5bn acquisition of BGI by BlackRock, several financings for Virtu Financial, the $300mm dividend recap for BATS Global Markets and many others

• Mr. Hebatpuria received his MBA from the Stern School of Business at New York University, an MS in Environmental Engineering from the University of Cincinnati and a B.S. in Civil Engineering from VJTI, University of Bombay

Jose Luis Martinez

Managing Director—Head of LatAm M&A

• Jose Luis Martinez is Head of UBS‘s Latin America M&A practice. Mr. Martinez joined UBS in 2016 after 20 years at J.P. Morgan and predecessor Bear Stearns, where he held a number of senior roles , including Managing Director and Head of Latin America Investment Banking at Bear Stearns from 2005 – 2008, and several regional and industry leadership positions at JP Morgan between 2008 and 2016, including Head of Latin America Power & Utilities

• Mr. Martinez has executed over 100 transactions, including more than US$150 billion in mergers and acquisitions as well as billions in fixed income and equity financings

• Mr. Martinez is fluent in Spanish and Portuguese. He obtained a Bachelor of Science in Business Administration degree with distinction from the University of North Carolina at Chapel Hill, and an MBA with distinction from the Kellogg Graduate School of Management - Northwestern University

Daniel Bassan

Managing Director—Brazil

• Daniel Bassan joined UBS in March 2016 as Managing Director after 5 years as Managing Director at Credit Suisse. He was resposible for the coverage of Real Estate, TMT, Metals and Mining, Financial Sponsors and Education. Previously he worked at BTG Pactual for 11 years

• Daniel has participated in many different transactions in M&A, equity and debt issuances and restructurings. His most relevant transactions include financial advisory for Vivendi in the sale of its subsidiary GVT to Telefonica, sale of IBMEC group to DeVry Education Group, Sale of Tijuca shopping Mall, Multiplan IPO, Even IPO and many others

• He graduated in Civil Engineering from Pontifícia Universidade Católica Rio de Janeiro and is fluent in Portuguese and English

Eugene Kim

Executive Director—Americas M&A

• Eugene Kim joined UBS in 2006, and has over 10 years of investment banking experience. Eugene has advised on transactions across a variety of industries, including the Financial Institutions, Real Estate, Telecom, and Technology sectors

• Mr. Kim has worked on transactions such as: the €21.2bn sale of Visa Europe to Visa Inc, Equifax's $1.9bn acquisition of Veda Group, Sprint's US$21.6bn sale of control to Softbank, Leucadia National Corp.’s $3.8bn stock-for-stock merger with Jefferies Group

• Eugene graduated from the Wharton School at the University of Pennsylvania with concentrations in Accounting and Finance

Gaurav Mehta

Director—Financial Technology & Services

• Gaurav Mehta is a Director in UBS's Financial Institutions Group specializing in Financial Technology & Services

• Prior to joining UBS, Mr. Mehta was a Vice President in the Financial Institutions Group at Credit Suisse focusing on financial technology and specialty finance. Previously, Mr. Mehta spent five years as an Associate at Bank of America and as a consultant with a focus on the financial services sector companies

• Mr. Mehta has worked on transactions such as: the €21.2bn sale of Visa Europe to Visa Inc., the $16.2bn acquisition of Alico by Metlife, Equifax's $1.9bn acquisition of Veda Group, the $1.3bn IPO of Markit, the $1.1bn refinancing for AlixPartners, the $923mm IPO of Air Lease, the $670mm LBO of Duff & Phelps by Carlyle and many others

• Mr. Mehta received his MBA from the Stern School of Business at New York University and a Bachelor in Technology in Electrical Engineering from Indian Institute of Technology Delhi

André Laloni

Managing Director—Head of CCS Brazil and Southern Cone

• André Laloni joined UBS Investment Bank as Managing Director and Head of Brazil & Southern Cone for CCS based in São Paulo. André was most recently Head of Corporate Finance for Barclays in Brazil, where he's worked since 2009. Prior to joining Barclays, he held coverage roles at Goldman Sachs and Unibanco in Brazil, and similar roles at UBS in New York

• His relevant advisory transactions include: Oi on five consecutive M&A divestiture assignments in the last 18 months totaling ~$1.7bn, Vale on its sale of selected assets in Chile, Group 1 Automotive in its $200mm acquisition of UAB Motors, Oi on its $17.2bn corporate restructuring, Intercement in the acquisition of the remaining 67% it did not own in Cimpor ($5.4bn) and many others

• André holds an MBA from University of Virginia, a degree in Mechanical Engineering from the Unicamp-Universidade de Campinas. He is fluent in Portuguese and English

14

UBS Team Responsible for the Valuation Report

Anderson Brito

Director—Brazil

• Anderson Brito is a Director of UBS Investment Bank in Brazil. Prior to joining UBS in January 2011, he worked in the Americas M&A Group at Standard Bank in 2010. Prior to this position he worked at the business consulting firm Bain & Company from 2008 to 2010 as Associate Consultant

• Mr. Brito has executed over 30 transactions, including more than R$75 billion in merger and acquisitions and capital markets

• Anderson holds a Bachelor of Science in Aeronautical Infrastructure Engineering from Instituto Tecnológico de Aeronáutica (ITA). He is fluent in Portuguese and English

Bradford Lo Gatto

Associate Director—Financial Technology & Services

• Bradford Lo Gatto is an Associate Director in UBS’s Financial Institutions group specializing in Financial Technology & Services

• Prior to joining UBS, Mr. Lo Gatto spent 7 years on the buy-side as a portfolio manager and research analyst. He has worked on transactions including: the €21.2bn sale of Visa Europe to Visa Inc., and the $361mm IPO of Virtu Financial

• Mr. Lo Gatto received his MBA with distinction from the Johnson Graduate School of Management at Cornell University and a Bachelor of Arts in Economics from Cornell University. He has also earned the right to use the CFA designation

Bruno Davila

Analyst—Brazil

• Bruno Davila joined UBS Investment Bank in 2013. He works in the São Paulo office as an analyst in investment banking

• His relevant transaction experience includes: Financial Advisor to SALIC on its US$187 million investment in Minerva, Financial Advisor to Grupo Colombo on the merger with GGAC

• Bruno holds Bachelor of Business Administration from Fundação Getulio Vargas FGV—EAESP

Mikhail Neto

Analyst—Brazil

• Mikhail Neto joined UBS Investment Bank in 2015. He works in the São Paulo office as an analyst in investment banking. Prior to joining UBS, Mikhail worked at Hyundai Glovis in the Seoul office

• His relevant transaction experience includes: Financial Advisor to SALIC on its US$187 million investment in Minerva

• Mikhail graduated in Industrial Engineering from Universidade Federal de São Carlos (UFSCar)

UBS Brasil Serviços de Assessoria Financeira Ltda.

Anderson Brito Bruno Davila Vik Hebatpuria Daniel Bassan Jose Luis Martinez Eugene Kim André Laloni

15

UBS Declarations

In accordance with the provision set forth in Annex III of Rule No. 361 of the Brazilian Securities and Exchange Commission ("CVM" and "CVM Rule 361", respectively), UBS declares that:

as of March 28, 2016 UBS, its parent company and related parties, held under its discretionary management 5,271,408 shares issued by BM&FBovespa SA - Bolsa de Valores Mercadorias e Futuros and 1,575,302 shares issued by CETIP SA - Mercados Organizados

it does not have any commercial or credit information of any kind that can impact the Valuation Report

does not have any conflict of interest that can reduce the independency required for the performance of its functions

in the last 12-month period until the present date, UBS has received no remuneration from either BM&FBovespa or from Cetip (not considering the compensation to be received due to the issuance of this Valuation Report)

Cetip

Section 3

Cetip

Section 3.A

Company and Sector Overview

18

Registration 9%

Custody 28%

Monthly Fee 14%

Auto Financing Unit 31%

Transaction Fee 11%

Others 7%

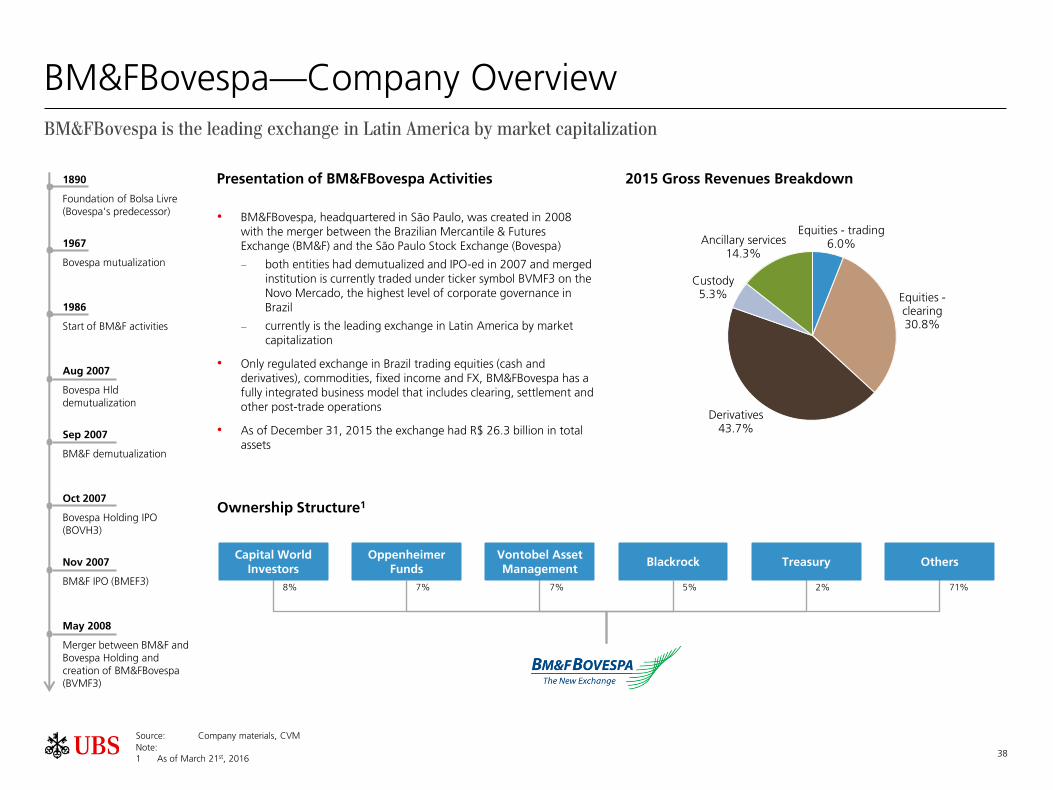

Cetip—Company Overview Cetip is Latin America’s largest depositary of private fixed income securities and Brazil’s largest private asset clearinghouse

2015 Gross Revenues Breakdown

Established in 1984 as a not-for-profit by the participants of the Brazilian private fixed income market, with the support of the Central Bank

Became a public company in 2009; its shares are traded on BM&FBovespa under ticker symbol CTIP3; part of the Ibovespa and IBrX-50 Index

Today, Cetip operates in two distinct businesses: – the Securities Unit is Brazil’s leader in the registration,

custody, and settlement of private fixed income securities – the Financing Unit offers an electronic system for the entry of

financial restrictions related to vehicle financing transactions with local DMVs (Sircof), covering all of such registrations in Brazil and the custody of such information (SNG)

Intercontinetal Exchange, Inc. ("ICE") purchased 12% stake from Advent International for US$512mm on July 24th, 2011

Presentation of Cetip Activities

Ownership Structure1

Others ICE Board and

Management

88% 12% < 1%

1984

Cetip is established as a not-for-profit organization

1988

Agreement with Anbima to operate SND (National System of Debentures)

2008

Demutualization process: creation of Cetip S.A.

2009

Advent becomes a shareholder with a 32% stake

IPO and listing at Novo Mercado of

BMF Bovespa

2011

Cetip’ s brand repositioning

ICE becomes a shareholder with 12.4% stake (from Advent)

2010

Acquisition of the Financing Unit (GRV Solutions) financed by the company’s first issuance of debentures

2012

Cetip’s shares are included in the IBOVESPA and IBrX-50 indexes

2013

Amendment of the company’s bylaws, seeking to improve Cetip’s corporate governance

Launching, in partnership with FNC, of the real estate appraisal platform

2015

Cetip Trader becomes Bacen’s dealer platform (Brazilian Central Bank)

Source: Company materials, CVM

Note: 1 As of March 18th, 2016

19

36% 36% 35% 31%

20% 21%

23% 28% 15% 15%

15% 14%

11%

11%

10% 9%

10%

10%

10%

11%

8%

8%

7%

7%

917

1,076

1,222 1,376

2012A 2013A 2014A 2015A

Auto financing unit Custody Monthly fee Registration Transaction Others

Net Revenues (R$mm) Gross Revenues (R$mm) and Gross Revenues Breakdown

Cetip—Financial Highlights

Source: Company filings Note: 1 Excludes equity in the results of associate

Net Income (R$mm) EBITDA1 (R$mm) and EBITDA Margin Net Debt (R$mm¹) and Net Debt/EBITDA

791 909

1,016 1,125

2012A 2013A 2014A 2015A

550 632

699 770

69.5% 69.6% 68.8% 68.4%

2012A 2013A 2014A 2015A

275 361

427 498

2012A 2013A 2014A 2015A

416

261 199

498

0.8x

0.4x

0.3x

0.6x

2012A 2013A 2014A 2015A

20

Cetip—Historical Financial Analysis

Balance Sheet—Assets

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A

Current 399 505 741 1,008

Cash and cash equivalents 0 0 1 2

Financial investments - available and restricted 295 382 590 802

Accounts receivable 81 93 107 118

Recoverable taxes and contributions 17 17 17 64

Other receivables 3 7 18 15

Prepaid expenses 3 6 8 7

Non-current 2,192 2,231 2,258 2,489

Long-term receivables 77 86 136 374

Financial investments - available and restricted 73 80 128 249

Derivatives — — — 121

Judicial deposits 0 0 0 0

Prepaid expenses 3 4 6 3

Other receivables 0 2 2 2

Investments 6 5 6 7

Investment in associate 5 4 5 6

Other investments 1 1 1 1

Property and equipment 41 41 50 48

Intangible assets¹ 2,069 2,098 2,066 2,061

Total assets 2,591 2,736 2,999 3,497

Source: Company fillings, CVM Notes: 1 Intangible assets are composed mostly by goodwill and contractual relations 2 Includes R$83 million of additional dividends proposed

Balance Sheet—Liabilities and Equity

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A

Current 375 337 240 340

Suppliers 18 26 23 54

Labor obligations and social charges 37 48 57 68

Taxes payable 11 13 15 18

Income tax and social contribution 1 1 2 8

Dividends and interest on own capital payable 25 46 80 110

Purchase price—deferred payments 215 — — —

Debentures issued 66 156 17 21

Loans and finance lease obligations 3 4 3 7

Derivatives — — — 12

Deferred revenues — 44 43 40

Other liabilities 0 0 0 0

Non- current 789 709 1,012 1,461

Suppliers — 4 2 8

Deferred income tax and social contribution 143 176 196 136

Provision for contingencies and legal obligations

3 3 5 6

Debentures issued 629 475 498 499

Loans and finance lease obligations 13 9 271 775

Deferred revenues — 42 41 37

Shareholders’ equity 1,428 1,690 1,746 1,6962

Total liabilities and shareholders' equity 2,591 2,736 2,999 3,497

21

Cetip—Historical Financial Analysis

Source: Company fillings, CVM Note: 1 Excludes equity in the results of associate

Profit & Loss

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A '12—'15 CAGR

Net revenue from services 791 909 1,016 1,125 12.5%

Revenue growth — 14.9% 11.8% 10.7%

(Operating expenses)/other operating income (308) (352) (400) (448) 13.3%

Margin (38.9%) (38.7%) (39.4%) (39.8%)

Personnel expenses (118) (139) (164) (184)

Share-based remuneration with no cash disbursement (26) (20) (16) (20)

Depreciation and amortization (67) (76) (83) (93)

Outsourced services (63) (75) (87) (100)

General and administrative expenses (32) (36) (41) (40)

Equipment and systems rental (1) (2) (3) (3)

Board members' compensation (2) (2) (2) (2)

Taxes and fees (1) (1) (2) (1)

Other operating expenses (1) (1) (2) (5)

Other operating income 1 0 1 0

Equity in the results of associate 0 0 1 1

(=) EBIT 483 557 616 677

(+) Depreciation and Amortization 67 76 83 93

(=) EBITDA1 550 632 699 770 11.9%

Margin 69.5% 69.6% 68.8% 68.4%

Financial result (96) (44) (59) (111) 5.0%

Financial income 39 34 59 294 96.1%

Financial expenses (135) (77) (118) (406) 44.3%

Income before taxation 387 513 558 567 13.6%

Income tax and social contribution (112) (152) (131) (70) (14.5%)

Current (51) (90) (111) (130)

Deferred (61) (61) (20) 60

Net income for the period 275 361 427 498 21.9%

Net income margin 34.8% 39.7% 42.0% 44.3%

22

Credit Expansion (R$ bn and % of GDP) Credit Growth (YoY Growth)

OTC Derivatives Volume Outstanding (R$ bn) Fixed Income Volume Outstanding (R$ bn)

Brazil fixed income instruments and OTC derivatives grew at a CAGR 2010-'15 of 9.4% and 36.9%, respectively

Credit volume grew at a CAGR 2010-'15 of 14.7%, but at a lower pace than in the previous years

Cetip—Sector Overview

30.7%

15.1%

20.6% 18.8%

16.4% 14.7%

11.3%

6.7%

2008 2009 2010 2011 2012 2013 2014 2015

1,234 1,421

1,731 2,034

2,368

2,715 3,018

3,218

35.1%

40.5%

45.4% 49.1%

53.7% 52.6% 54.7% 54.3%

2008 2009 2010 2011 2012 2013 2014 2015

Source: Brazilian Central Bank, Cetip

29% 29% 33% 33% 34% 36%

12% 12%

15% 16%

16% 17%

30% 23%

19% 16%

13% 11%

21% 23% 18%

17% 15%

11%

1% 5%

7% 8%

8% 9%

7%

8%

8%

11% 14%

15%

2,828

3,182 3,454

3,769

4,133 4,435

2010 2011 2012 2013 2014 2015Investment Fund Debentures CDB

DI Letra Financeira Other

70% 69% 74% 70% 58%

46% 22%

25%

21% 22% 29%

22%

8%

6%

5%

8% 13%

32%

427

584

848

1,034 1,117

2,054

2010 2011 2012 2013 2014 2015

Swap Forward Contracts Other Derivatives

Brazilian Fixed Income, Derivatives and Credit Overview

23

Vehicle Acquisition Loans—Total Outstanding (R$ bn)

Vehicle Acquisition Loans—Total Outstanding ('000) In the automotive sector,

acquisition loans have been decreasing since 2008 in number of vehicles, but increased in volume of loans at a CAGR 2008-15 of 9.8%

In Brazil, mortgages grew at a CAGR 2008-15 of 35.4%

Cetip—Sector Overview

Population Debt by Credit Type (%) Mortgages for Individuals—Total Outstanding (R$ bn and % of GDP)

60 84

131

189

255

341

432

500

2.0% 2.6%

3.5%

4.6%

5.8%

7.0% 7.8%

8.4%

2008 2009 2010 2011 2012 2013 2014 2015

Source: Brazilian Central Bank, Sistema Nacional de Gravames, Fenabrave

3,489 3,269 3,937 3,870 3,590 3,517 3,160

2,339

4,461

3,541

3,920 3,815 3,359 3,241

3,233

2,973

7,950

6,810

7,857 7,685

6,949 6,758 6,393

5,312

2008 2009 2010 2011 2012 2013 2014 2015

New Vehicles Used Vehicles

89.5% 89.7%

90.9%

89.7% 89.6% 89.9% 90.7%

90.7% 10.5%

10.3%

9.1%

10.3%

10.4% 10.1% 9.3%

9.3%

92 105

154

198

216 213 203

177

2008 2009 2010 2011 2012 2013 2014 2015Personal Loans Corporate Loans

84

82

76

75

74

58

50

24

1

2

3

12

3

6

8

24

4

2

1

6

2

23

4

11

14

20

7

21

36

19

48

Mortgages Auto Credit Card Others

Brazilian Automotive and Real Estate Financing Overview

Cetip

Section 3.B

Valuation

25

Valuation by Volume Weighted Average Price (1/2) VWAP for the last 12 months prior to the First Material Fact is R$33.26 and R$38.24 from the First Material Fact to April 5th, 2016

Source: Bloomberg as of April 5, 2016

Historical VWAP Price of Cetip Prior to the First Material Fact (from November 3rd, 2014 to November 2nd, 2015)

Historical VWAP Price of Cetip Since the First Material Fact (from November 3rd, 2015 to April 5th, 2016)

33.99

33.26

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0.00

10.00

20.00

30.00

40.00

50.00

Nov-14 Jan-15 Mar-15 Jun-15 Aug-15 Oct-15

Vo

lum

e (

mm

)

Pri

ce V

WA

P (

R$

)

Volume Price VWAP (R$) VWAP

Material Fact Released on November 3rd, 2015

November 13th, 2015 NBO Date

February 19th, 2016 BO Date

March 2nd, 2016 Declined BO

December 3rd, 2015 Declined NBO

40.41

38.24

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0.00

10.00

20.00

30.00

40.00

50.00

Nov-15 Dec-15 Feb-16 Apr-16

Vo

lum

e (

mm

)

Pri

ce V

WA

P (

R$

)

Volume Price VWAP (R$) VWAP

NBO: Non-Binding Offer BO: Binding Offer

26

Valuation by Volume Weighted Average Price (2/2) VWAP for the periods of 1, 30, 60, 90, 180 trading days and 1 year before the First Material Fact and for the period since the date of the First Material Fact until April 5th, 2016

Source: Bloomberg as of April 5, 2016

Price VWAP (R$)

Trading Days Prior to the First Material Fact Release Weighted by Trading Volume

1 33.99

30 33.73

60 33.31

90 33.91

180 33.44

12 months (from November 3rd, 2014 to November 2nd, 2015) 33.26

Since the First Material Fact (from November 3rd, 2015 to April 5th, 2016) 38.24

Summary of VWAP for Selected Periods

27

Valuation by Shareholders' Equity Book Value

Source: Company filings

R$ million, unless otherwise indicated As of December 31st, 2015

Total Assets 3,497

Total Liabilities 1,801

Shareholders' Equity 1,696

Outstanding Shares (mm) 260

Common Shares 263

Treasury Shares 3

Equity Book Value per Share (R$) 6.531

Note: 1 Shareholders' Equity / Outstanding Shares

Equity Book Value per Share

Equity book value per share is R$6.53 for Cetip, as of December 31st, 2015

28

Cetip—Selected Trading Multiples Methodology

UBS has used the trading multiples valuation approach in order to estimate the economic value of Cetip

Selected Trading Multiples is a relative valuation method which estimates the value of a company using ratios of market valuation to financial metrics of similar publicly traded companies; traditional trading multiples include P/E and EV/EBITDA

Trading multiples of Cetip’s comparable companies were calculated based on the EBITDA and net income forecasts from market analysts for the years 2016 and 2017, and applied over the EBITDA and net income forecasts for Cetip over the same years, given that forecasts from market analysts are generally limited to two years

Selected comparable companies are international exchanges sharing several aspects in common with Cetip, including the following1:

• business model

• revenue mix

• product and service offerings

• size and scale of operations

• monopolistic position within its home country in certain market segments the comparable company operates in

• emerging market exposure

Selected Trading Comparables

Note: 1 Not every aspect applicable for each selected comparable company. See Appendix A for more details on selection of comparable companies

29

Cetip—Selected Trading Multiples¹

Market Value

(R$bn)

EV/EBITDA Price / EPS

Headquarters April 5, 2016

Price (R$) Enterprise Value

(R$bn) CY'16E

(x) CY'17E

(x) CY'16E

(x) CY'17E

(x)

United States 869.83 104.7 129.5 12.5 11.4 16.8 15.1

Germany 302.75 56.2 64.6 11.0 10.1 15.9 14.1

Australia 114.43 22.2 19.3 12.0 11.6 18.8 18.1

Singapore 21.02 21.8 20.4 15.5 14.4 22.7 21.1

Spain 113.25 9.5 8.6 8.7 8.8 13.0 13.3

Canada 128.38 7.0 9.6 10.2 9.6 12.6 11.4

Malaysia 8.19 4.4 4.3 14.8 13.9 22.4 21.0

Mexico 5.73 3.6 3.3 10.9 9.9 18.5 16.5

Mean 11.9 11.2 17.6 16.3

Median 11.5 10.7 17.6 15.8

Min 8.7 8.8 12.6 11.4

Max 15.5 14.4 22.7 21.1

Source: FactSet as of April 5, 2016 Note: 1 R$ / US$ exchange rate of 3.67 as of April 5, 2016, fully diluted shares using treasury stock method

30

Cetip Valuation Based on Selected Trading Multiples

Min. Range Max. Range

(R$ mm) CY'16E CY'17E Mid-Point ("MP") MP-4.75% MP+4.75%

EV/EBITDA Multiple (sample median) 11.5x 10.7x

EBITDA (consensus)¹ 871 981

Implied Enterprise Value 10,034 10,519 10,277 9,789 10,765

(-) Net Debt 443 443

(-) Minorities - -

Implied Equity Value 9,592 10,076 9,834 9,367 10,301

Total Shares Outstanding (mm)2 261 261

Share Price (R$) 36.68 38.54 37.61 35.82 39.39

Min. Range Max. Range

(R$ mm) CY'16E CY'17E Mid-Point ("MP") MP-4.75% MP+4.75%

P/E Multiple (sample median) 17.6x 15.8x

Net Income (consensus)¹ 577 651

Implied Equity Value 10,173 10,282 10,228 9,742 10,714

Total Shares Outstanding (mm)2 261 261

Share Price (R$) 38.91 39.32 39.11 37.26 40.97

EV / EBITDA Analysis

Price to Earnings Analysis

Source: FactSet, Research reports Note: 1 FactSet (as of April 5, 2016) 2 Fully diluted shares using treasury stock method

31

Cetip’s Revenues Assumptions

Gross Revenues (by segment)

Securities Segment

Registration

– fixed income security registration product long-term volume growth rate of approximately 10% - 14%, pricing fixed at 2015 levels

– derivatives security registration product long-term volume growth rate of approximately 10% - 14%, pricing fixed at 2015 levels

Custody

– debentures, bank funding instruments, OTC contracts, structured notes and other securities custody product with a long-term volume growth of ~10% and maintenance of the registration fee (bps), pricing fixed at 2015 levels

– end users: monthly fee per user adjusted by Broad National Consumer Price Index ("IPCA") and number of users with a long-term growth rate of approximately 8% - 9%

Transactions: cost per transaction adjusted by 50% of IPCA and number of transactions with a long-term growth rate of ~10%

Monthly utilization: average cost adjusted by IPCA and average number of users with a long-term growth rate of ~2%

Others1: long-term growth rate of ~10%

New projects: launch of an integrated trading platform focused on government and corporate bonds and bank securities targeting

an increase of market share from current 13% (Cetip Trader) to 20% — to be fully operational in 2020

Financing Segment

SNG (Communication of liens to DMV): Average ticket adjusted by IPCA and number of financed vehicles with a long-term growth rate of approximately 2% to 3%

Sircof (Registration of vehicle financing contracts): % of financed vehicles registered kept constant, pricing fixed at 2015 levels and

average ticket adjusted by IPCA

Market data and solution development: long-term growth rate of ~9%

New projects:

– electronic appraisal: report for used cars targeting a market share of 75% (total numbers of used cars financed in 2018) — to

be fully operational in 2020

– electronic formalization: electronic information flow for vehicle financing targeting a market share of 40% (total numbers of used cars financed in 2018) — to be fully operational in 2020

Real estate appraisal:

– services of real estate appraisal with average fee of R$125.00 (base 2016) per unit adjusted by IPCA

– price already net of costs associated with this service

– total number of financed units of 450 thousand (base 2016) with 2% CAGR ('16–'25) and Cetip market share of 62.5% in 2016, 70% in 2017–2019 and 80% from 2020 onwards

Taxes and Revenue Deductions

17.4% of the gross revenue (realized in the 2015)

Assumes 3 p.p reduction in the Securities segment deductions from 2017 onwards

Source: BM&FBovespa Management Note: 1 Other revenue are derived primarily from services rendered to Interbank Payments Chamber for processing interbank financial transfers. The Company has been engaged by CIP to process electronic

cash transfers as well as to handle the financial settlement of credit documents and collection slips

32

Cetip—Expenses and Other Assumptions

Source: BM&FBovespa Management Note: 1 Before adjustment for interest on own capital payment, an alternative to making dividend payments to shareholders

Expenses

Adjusted by IPCA + 2%

Expenses with personnel, share option plan (SOP), auditors’, consultants and legal fees, board compensation, general and administrative expenses, support and maintenance of systems, equipment expenses and rent

Adjusted by IPCA

Maintenance and cleaning of facilities, maintenance of machinery and equipment, reception, security and surveillance, media relations, marketing, recruitment, other operating expenses and other operating income

Estimated as % of Revenues

Taxes and fees, regulatory costs, registration costs and other services

All based on the % of 9M15. Adjustments in regulatory costs and registration costs in order to reflect the change in the accounting of the contract system in São Paulo as of 2Q'15

Working Capital Considers no change in net working capital

Taxes 34% of adjusted results before taxes1

Capex Maintained at approximately 6% of net revenues, based on the average capex as % of net revenues in the prior 4 years

One-off capex increase in 2016 due to new projects expected to start in 2020

33

Historical Projected CAGR (%)

(R$mm) 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E '12 - '15 '16E - '25E

Net Revenues 791 909 1,016 1,125 1,267 1,437 1,584 1,743 2,197 2,410 2,638 2,888 3,162 3,539 12.5% 12.1%

EBITDA1 550 632 699 770 881 1,021 1,136 1,262 1,607 1,779 1,965 2,171 2,397 2,704 11.4% 13.3%

% Margin 69.5% 69.6% 68.8% 68.4% 69.6% 71.0% 71.7% 72.4% 73.1% 73.8% 74.5% 75.2% 75.8% 76.4%

Less: Depreciation & Amortization

(67) (76) (83) (93) (104) (118) (97) (107) (134) (147) (161) (177) (193) (216)

EBIT 483 557 616 678 777 902 1,039 1,156 1,472 1,631 1,804 1,994 2,204 2,488 11.4% 13.8%

Financial Revenues and Expenses

(96) (44) (59) (111) (76) (34) 18 61 111 175 248 330 424 530

EBT 387 513 558 567 701 868 1,057 1,217 1,583 1,806 2,052 2,324 2,627 3,018 12.8% 17.6%

Less: Taxes (112) (152) (131) (70) (202) (253) (310) (355) (469) (531) (599) (674) (756) (866)

Net Income 275 361 427 498 499 615 747 862 1,114 1,275 1,453 1,651 1,871 2,152 20.7% 17.6%

Cetip—Financial Summary

Source: BM&FBovespa Management Note: 1 Historical data excludes equity in the results of associate

34

Cetip—Discounted Cash Flow

Methodology

Unlevered discounted cash flow method

Projection of the unlevered cash flows to firm

Cash flows are discounted using the weighted average cost of capital (WACC) to calculate their present value using

mid-year convention

Valuation prepared on a stand-alone basis, not including operating, financial, or strategic benefits or losses, if any, that

Cetip may have upon conclusion of the potential Transaction

Currency

Projections in nominal R$

Converted to US$ using Central Bank of Brazil projections through 2020; R$ further depreciated through 2025 by ratio

of each countries' stated inflation target based on Economist Intelligence Unit projections

Discounted

cash flow

Base date: December 31, 2015

Projection period: annual projections from 2016 to 2025

Discounted cash flow in nominal US$

Discount Rate Calculated based on: (i) risk-free return rate per US 10 year Treasury bonds rate adjusted to Brazil US$ government bond

rate, (ii) market risk premium, (iii) leveraged beta of the sector, and estimated cost of debt for assumed US$ issuance

Perpetuity Growth Rate

Represents 3.0% estimated long-term nominal growth for Cetip

Source: BM&FBovespa Management

35

Cetip—Discounted Cash Flow

Calendar Year Ended December 31,

(R$mm, unless noted) 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E Cetip EBITDA 881 1,021 1,136 1,262 1,607 1,779 1,965 2,171 2,397 2,704

Less: Depreciation & Amortization (104) (118) (97) (107) (134) (147) (161) (177) (193) (216)

Cetip EBIT 777 902 1,039 1,156 1,472 1,631 1,804 1,994 2,204 2,488

Less: Interest On Own Capital 1 (127) (146) (169) (197) (229) (271) (319) (373) (435) (506)

Taxable EBIT 2 650 756 870 959 1,243 1,360 1,485 1,621 1,768 1,983

Tax Rate 34.0% 34.0% 34.0% 34.0% 34.0% 34.0% 34.0% 34.0% 34.0% 34.0%

Taxes 221 257 296 326 423 463 505 551 601 674

Cetip EBIT 777 902 1,039 1,156 1,472 1,631 1,804 1,994 2,204 2,488

Less: Taxes (221) (257) (296) (326) (423) (463) (505) (551) (601) (674)

Plus: Depreciation & Amortization 104 118 97 107 134 147 161 177 193 216

Less: Total Capex (129) (88) (97) (107) (134) (147) (161) (177) (193) (216)

Plus: (Increase) / Decrease in Working Capital 0 0 0 0 0 0 0 0 0 0 Unlevered Free Cash Flows 531 676 743 830 1,050 1,169 1,299 1,443 1,602 1,814

R$/US$ Average Rate 3 3.74 4.25 4.50 4.70 4.90 5.02 5.14 5.27 5.40 5.53

US$ Free Cash Flows 142 159 165 177 214 233 253 274 297 328

Notes: 1 Represents payment to shareholders characterized as interest on own capital 2 Interest on own capital reduces taxable income basis 3 Sourced from Central Bank of Brazil projections through 2020; R$ depreciated throughout balance of projection period by

differential in long-term inflation targets of 4.5% for Brazil and 2.0% for the US, according to Economist Intelligence Unit projections for 2025

4 Terminal value considering a perpetuity growth rate of 3.0% 5 Converted at R$/US$ exchange rate of 3.67 as of April 5, 2016 6 Represents balance sheet data as of 12/31/15 7 Represents cash and cash equivalents plus financial investments (available and restricted, current and non-current) less dividends

and interest on own capital payable and additional dividends proposed 8 Diluted shares based on treasury stock method of vested shares at R$40.65 per share as of April 5, 2016 9 Discounted to 12/31/15 at a discount rate of 10.2% 10 Minimum and maximum represents a +/-4.75% range from R$43.39

Free Cash Flow to Firm

Present Value of the Cash Flows US$mm 1,331

Present Value of the Terminal Value 4 US$mm 1,871

Enterprise Value US$mm 3,202

Exchange Rate R$/US$ 4/5/2016 3.67

Enteprise Value 5 R$mm 11,740

Less: Debt 6 R$mm (1,302)

Plus: Cash 6,7 R$mm 860

Equity Value R$mm 11,298

Diluted Shares Outstanding 8 mm 260

Equity Value per Share 9 R$ / share 43.39

Minimum Range 10 R$ / share 41.33

Maximum Range 10 R$ / share 45.45

Source: BM&FBovespa Management

BM&FBovespa

Section 4

BM&FBovespa

Section 4.A

Company and Sector Overview

38

2015 Gross Revenues Breakdown Presentation of BM&FBovespa Activities

BM&FBovespa—Company Overview BM&FBovespa is the leading exchange in Latin America by market capitalization

Ownership Structure1

8% 7% 7% 2% 71%

Capital World Investors

Vontobel Asset Management

Blackrock Treasury Others

1890

Foundation of Bolsa Livre (Bovespa's predecessor)

1967

Bovespa mutualization

1986

Start of BM&F activities

Aug 2007

Bovespa Hld demutualization

Sep 2007

BM&F demutualization

Oct 2007

Bovespa Holding IPO (BOVH3)

Nov 2007

BM&F IPO (BMEF3)

May 2008

Merger between BM&F and Bovespa Holding and creation of BM&FBovespa (BVMF3)

Equities - trading 6.0%

Equities - clearing 30.8%

Derivatives 43.7%

Custody 5.3%

Ancillary services 14.3%

Oppenheimer Funds

5%

Source: Company materials, CVM

Note: 1 As of March 21st, 2016

• BM&FBovespa, headquartered in São Paulo, was created in 2008 with the merger between the Brazilian Mercantile & Futures Exchange (BM&F) and the São Paulo Stock Exchange (Bovespa)

– both entities had demutualized and IPO-ed in 2007 and merged institution is currently traded under ticker symbol BVMF3 on the Novo Mercado, the highest level of corporate governance in Brazil

– currently is the leading exchange in Latin America by market capitalization

• Only regulated exchange in Brazil trading equities (cash and derivatives), commodities, fixed income and FX, BM&FBovespa has a fully integrated business model that includes clearing, settlement and other post-trade operations

• As of December 31, 2015 the exchange had R$ 26.3 billion in total assets

39

Net Revenues (R$mm) Gross Revenues (R$mm) and Gross Revenues Breakdown

BM&FBovespa—Financial Highlights

Source: Company filings

Net Income (R$mm) EBITDA (R$mm) and EBITDA Margin Net Cash (R$mm)

11% 8% 7% 6%

35% 35% 36% 31%

38% 39% 39% 44%

4% 5% 5%

5% 13% 13%

13% 14%

2,289 2,370 2,250

2,459

2012A 2013A 2014A 2015AEquities - trading Equities - clearing Derivatives Custody Ancillary services

2,065 2,127 2,030 2,217

2012A 2013A 2014A 2015A

1,353 1,455 1,345 1,477

65.5% 68.4% 66.3% 66.6%

2012A 2013A 2014A 2015A

1,074 1,081 978

2,203

2012A 2013A 2014A 2015A

2,019

2,609

885

5,845

2012A 2013A 2014A 2015A

BM&FBovespa sold R$1.2 billion worth of CME in September 2015 and reclassified R$4.8 billion to available for sale financial securities. Also includes R$1.3 billion of collateral for transactions

High increase due to growth on financial income, FX and one-off profit from the sale of CME

40

BM&FBovespa—Historical Financial Analysis

Balance Sheet — Assets

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A

Current assets 3,536 4,319 2,785 8,674

Cash and cash equivalents 44 1,197 501 441

Financial investments and marketable securities 3,233 2,853 1,962 7,7991

Accounts receivable 57 54 58 75

Other receivables 4 79 72 158

Taxes recoverable and prepaid 180 120 166 175

Prepaid expenses 18 16 26 26

Noncurrent assets 20,611 21,577 22,478 17,635

Long-term receivables 809 1,135 1,523 1,961

Financial investments and marketable securities 574 821 1,393 1,816

Judicial deposits 132 203 — —

Other receivables 98 109 120 141

Prepaid expenses 2 2 2 2

Investments 3 1 7 3

Investments in associates 2,929 3,346 3,761 31

Investment in subsidiaries 2,894 3,313 3,729 —

Investment properties 35 34 32 31

Property and equipment 361 423 421 453

Intangible assets 16,512 16,672 16,773 15,190

Goodwill 16,064 16,064 16,064 14,402

Software and projects 448 608 709 788

Total assets 24,147 25,897 25,263 26,309

Balance Sheet — Liabilities and Equity

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A

Current liabilities 1,661 2,711 1,892 2,097

Collateral for transactions 1,134 2,073 1,322 1,338

Earnings and rights on securities in custody 44 50 46 49

Suppliers 61 45 66 43

Salaries and social charges 74 75 72 117

Provision for taxes and contributions payable 28 26 25 35

Income tax and social contribution 3 1 2 5

Interest payable on debt issued abroad 37 42 47 70

Dividends and interest on equity payable 2 1 2 3

Other liabilities 278 397 308 437

Noncurrent liabilities 3,073 3,887 4,383 5,860

Debt issued abroad 1,242 1,426 1,619 2,384

Deferred income tax and social contribution 1,740 2,296 2,585 3,272

Provisions for tax, civil and labor contingencies 63 89 103 119

Obligation with post-retirement health care benefit

28 26 28 26

Other liabilities — 50 48 58

Equity 19,414 19,299 18,988 18,352

Non-controlling interests 16 15 9 10

Total liabilities and equity 24,147 25,897 25,263 26,309

Source: Company materials, CVM Note: 1 BM&FBovespa sold R$1.2 billion worth of CME in September 2015 and reclassified R$4.8 billion to available for sale financial securities. Includes R$1.3 billion of collateral for transactions

41

BM&FBovespa—Historical Financial Analysis

Source: Company materials, CVM

Profit & Loss

Fiscal year ended in December 31st

R$mm 2012A 2013A 2014A 2015A '12—'15 CAGR

Revenue 2,065 2,127 2,030 2,217 2.4%

Revenue growth — 3.0% (4.6%) 9.2%

Expenses (763) (791) (804) (861) 3.7%

Margin 36.9% 37.2% 39.6% 38.4%

Administrative and general

Personnel and related charges (354) (352) (354) (443)

Data processing (103) (110) (124) (122)

Depreciation and amortization (94) (120) (119) (111)

Third-party services (51) (46) (40) (41)

Maintenance in general (11) (12) (12) (14)

Communications (18) (17) (13) (6)

Promotion and publicity (19) (15) (11) (12)

Taxes (42) (56) (56) (8)

Board and committee members’ compensation (7) (8) (9) (9)

Sundry (65) (56) (66) (84)

Impairment of assets — — — (1,663)

Equity pickup 149 171 212 136

Equity method discontinuation — — — 1,735

Gain on disposal of investment in associates — — — 724

(=) EBIT 1,302 1,336 1,226 1,366 1.6%

(+) Depreciation and Amortization 51 120 119 111

(=) EBITDA 1,353 1,456 1,345 1,477 3.0%

Margin 65.5% 68.4% 66.3% 66.6%

Financial result 209 181 208 509 34.5%

Financial income 297 299 362 746

Financial expenses (88) (118) (154) (237)

Income before income tax and social contribution 1,660 1,688 1,647 2,807 19.1%

Income tax and social contribution (586) (607) (661) (604) 1.0%

Current (67) (60) (104) (46)

Deferred (518) (546) (557) (558)

Net income from continuing operations 1,074 1,081 986 2,203 27.1%

Net income (loss) from discontinued operations — (0) (8) —

Net income for the year 1,074 1,081 978 2,203 27.1%

Margin 52.0% 50.8% 48.2% 99.4%

42

# of Listed Companies Average Market Capitalization and Turnover Velocity (R$ trillion, %)

Breakdown of ADTV by Investor Type Average Daily Trading Value "ADTV" (R$ million) BM&FBovespa is the only equities; derivatives (equity, fixed income and commodities) trading venue in Brazil

Foreign investors participation in the average equities daily trading value accounted for 54% in 2015

Average market capitalization in 2015 was R$2.2 trillion and Bovespa had 440 listed companies as of December 31st, 2015

BM&FBovespa—Sector Overview

6,492

7,251 7,418 7,293 6,793

2011A 2012A 2013A 2014A 2015A

Cash Options Forward

2.4 2.4 2.4 2.4 2.2

64.2%

70.0%

72.9% 72.4% 72.9%

2011A 2012A 2013A 2014A 2015A

34.8% 40.3% 43.8% 50.7% 53.7%

33.3% 31.9%

32.9% 28.8% 26.9%

21.2% 18.1% 15.1% 13.7% 13.4% 9.1% 8.3% 6.8% 5.5% 4.5%

1.5% 1.4% 1.4% 1.4% 1.5%

2011A 2012A 2013A 2014A 2015A

Foreign Institutional Retail FinancialInstitutions

Others

274 262 255 250 236

182 178 187 192 192

10 12 12 13 12

466 452 454 455 440

2011A 2012A 2013A 2014A 2015A

Traditional Special Segment BDR

BM&FBovespa

Section 4.B

Valuation

44

11.43

10.73

0.0

10.0

20.0

30.0

40.0

50.0

0.00

4.00

8.00

12.00

16.00

Nov-14 Jan-15 Mar-15 Jun-15 Aug-15 Oct-15

Vo

lum

e (

mm

)

Pri

ce V

WA

P (

R$

)

Volume Price VWAP (R$) VWAP

Valuation by Volume Weighted Average Price (1/2) VWAP for the last 12 months prior to the First Material Fact is R$10.73 and R$12.52 from the First Material Fact to April 5th, 2016

Historical VWAP Price of BM&FBovespa Prior to the First Material Fact (from November 3rd, 2014 to November 2nd, 2015)

Historical VWAP Price of BM&FBovespa Since the First Material Fact (from November 3rd, 2015 to April 5th, 2016)

Source: Bloomberg as of April 5, 2016

Material Fact Released on November 3rd, 2015

15.58

12.52

0.0

10.0

20.0

30.0

40.0

50.0

0.00

4.00

8.00

12.00

16.00

Nov-15 Dec-15 Feb-16 Apr-16

Vo

lum

e (

mm

)

Pri

ce V

WA

P (

R$

)

Volume Price VWAP (R$) VWAP

November 13th, 2015 NBO Date

February 19th, 2016 BO Date

March 2nd, 2016 Declined BO

December 3rd, 2015 Declined NBO

NBO: Non-Binding Offer BO: Binding Offer

45

Valuation by Volume Weighted Average Price (2/2) VWAP for the periods of 1, 30, 60, 90, 180 trading days and 1 year before the First Material Fact and for the period since the date of the First Material Fact until April 5th, 2016

Source: Bloomberg as of April 5, 2016

Price VWAP (R$)

Trading Days Prior to the Material Fact Release Weighted by Trading Volume

1 11.43

30 11.41

60 10.99

90 11.03

180 11.15

12 months (from November 3rd, 2014 to November 2nd, 2015) 10.73

Since the First Material Fact (from November 3rd, 2015 to April 5th, 2016) 12.52

Summary of VWAP for Selected Periods

46

Valuation by Shareholders' Equity Book Value

Source: Company filings

R$million, unless otherwise indicated As of December 31st, 2015

Total Assets 26,309

Total Liabilities 7,957

Shareholders' Equity 18,352

Outstanding Shares (mm) 1,782

Common Shares 1,815

Treasury Shares 33

Equity Book Value per Share (R$) 10.301

Note: 1 Shareholders' Equity / Outstanding Shares

Equity Book Value per Share

Equity book value per share is R$10.30 for BM&FBovespa, as of December 31st, 2015

47

BM&FBovespa—Selected Trading Multiples Methodology

UBS has used the trading multiples valuation approach in order to estimate the economic value of BM&FBovespa

Selected Trading Multiples is a relative valuation method which estimates the value of a company using ratios of market valuation to financial metrics of similar publicly traded companies; traditional trading multiples include P/E and EV/EBITDA

Trading multiples of BM&FBovespa’s comparable companies were calculated based on the EBITDA and net income forecasts from market analysts for the years 2016 and 2017, and applied over the EBITDA and net income forecasts for BM&FBovespa over the same years, given that forecasts from market analysts are generally limited to two years

Selected comparable companies are international exchanges sharing several aspects in common with BM&FBovespa, including the following1:

• business model

• revenue mix

• product and service offerings

• size and scale of operations

• monopolistic position within its home country in certain market segments the comparable company operates in

• emerging market exposure

Selected Trading Comparables

Note: 1 Not every aspect applicable for each selected comparable company. See Appendix A for more details on selection of comparable companies

48

BM&FBovespa—Selected Trading Multiples¹

Market Value (R$bn)

EV/EBITDA Price / EPS

Headquarters April 5, 2016

Price (R$) Enterprise Value

(R$bn) CY'16E

(x) CY'17E

(x) CY'16E

(x) CY'17E

(x)

United States 869.83 104.7 129.5 12.5 11.4 16.8 15.1

United States 346.63 118.1 120.1 12.9 11.9 22.0 20.5

Germany 302.75 56.2 64.6 11.0 10.1 15.9 14.1

United States 238.28 40.6 48.2 11.4 10.6 17.3 15.7

Singapore 21.02 21.8 20.4 15.5 14.4 22.7 21.1

United States 240.04 19.7 19.4 13.8 12.8 25.7 23.8

Australia 114.43 22.2 19.3 12.0 11.6 18.8 18.1

Canada 128.38 7.0 9.6 10.2 9.6 12.6 11.4

Spain 113.25 9.5 8.6 8.7 8.8 13.0 13.3

Malaysia 8.19 4.4 4.3 14.8 13.9 22.4 21.0

Mexico 5.73 3.6 3.3 10.9 9.9 18.5 16.5

Mean 12.2 11.4 18.7 17.3

Median 12.0 11.4 18.5 16.5

Min 8.7 8.8 12.6 11.4

Max 15.5 14.4 25.7 23.8

Source: FactSet as of April 5, 2016 Note: 1 R$ / US$ exchange rate of 3.67 as of April 5, 2016, fully diluted shares using treasury stock method

49

BM&FBovespa Valuation Based on Comparable Trading Multiples

Min. Range Max. Range

(R$ mm) CY'16E CY'17E Mid-Point ("MP") MP-4.75% MP+4.75%

EV/EBITDA Multiple (sample median) 12.0x 11.4x

EBITDA (consensus)¹ 1,582 1,758

Implied Enterprise Value 19,004 19,973 19,488 18,563 20,414

(-) Net Debt 2,179 2,179

(-) Minorities 10 10

Implied Equity Value 16,815 17,784 17,299 16,478 18,121

Total Shares Outstanding (mm)2 1,796 1,796

Share Price (R$) 9.36 9.90 9.63 9.18 10.09

Min. Range Max. Range

(R$ mm) CY'16E CY'17E Mid-Point ("MP") MP-4.75% MP+4.75%

P/E Multiple (sample median) 18.5x 16.5x

Net Income (consensus)¹ 1,565 1,773

Implied Equity Value 28,900 29,270 29,085 27,703 30,466

Total Shares Outstanding (mm)2 1,796 1,796

Share Price (R$) 16.09 16.30 16.20 15.43 16.97

EV / EBITDA Analysis

Price to Earnings Analysis

Source: FactSet, Research reports Note: 1 FactSet as of April 5, 2016 2 Fully diluted shares using treasury stock method

Selected Comparable Companies for Cetip and BM&FBovespa

Appendix A

51

Peer Key Financials Comments

Headquartered in New York, Nasdaq is a provider of trading, clearing, exchange technology, regulatory, securities listing, information and public company services across six continents with over 3,800 employees

With c.10,000 corporate clients, Nasdaq has around 3,700 listed companies with market cap of ~US$9.6 trillion

Revenue mix for operating segments: Market Services (61.2%), Technology Solutions (16.0%), Information Services (15.0%) and Listing services (7.8%)

On March 9, 2016, entered into a definitive agreement to International Securities Exchanges for US$1.1bn

On February 12, 2016, announced to acquire Marketwired, a newswire operator and press release distributor for US$200mm

Headquartered in Toronto, TMX Group operates cash & derivative markets for multiple asset classes including equities, fixed income and energy with over 1,100 employees

Revenue mix for operating segments: Efficient Markets & Market Solutions (29.5%), Market Insights (29.4%), Capital Formation (25.1%), Derivatives (14.6%) and Others (1.5%)

Has a combined market share (including TSX, Alpha, and TMX Select) of the total volume traded in Canadian based interlisted issues of 34%

In February 2016, introduced two integrated products: TMX Insights and TMX Analytics

In June & November 2015, announced launch of AgriClear (online platform & payment service for US and Canadian cattle buyers & sellers) and NAVex (a fund transfer platform) respectively

Headquartered in Madrid, BME is an operator of Spain's stock market and financial systems with over 700 employees

Has additional significant presence in LatAm

Revenue mix for operating segments: Equity (46.8%), Settlement & Registration (24.3%), Information (11.4%), Clearing (5.4%), IT & Consulting (5.4%), Derivatives (3.6%), Fixed Income (2.9%)

On February 29, 2016, announced acquisition of remaining stake (50%) it didn't already own in Infobolsa SA from Deutsche Börse AG's for US$9.2mm in cash

Selected Comparable Companies for BM&FBovespa and Cetip

R$bn

Share Price (R$) 238.28

Fully-Diluted Shares (mm) 170.6

Equity Value 40.6

Excess Cash¹ 1.1

Debt 8.7

Enterprise Value 48.2

2016 EV/EBITDA 11.4x

2016 P/E 17.3x

R$bn

Share Price (R$) 128.38

Fully-Diluted Shares (mm) 54.4

Equity Value 7.0

Excess Cash¹ 0.4

Debt 3.1

Enterprise Value 9.6

2016 EV/EBITDA 10.2x

2016 P/E 12.6x

R$bn

Share Price (R$) 113.25

Fully-Diluted Shares (mm) 83.9

Equity Value 9.5

Excess Cash¹ 0.9

Debt 0.0

Enterprise Value 8.6

2016 EV/EBITDA 8.7x

2016 P/E 13.0x

Mature Market Exchanges

Source: Company Information—Market data as of April 5, 2016; R$ / US$ exchange rate of 3.67 as of April 5, 2016 Note: 1 Excess Cash as per the latest financial statement excluding financial investments, restricted cash, regulatory capital requirements and customer balances, as appropriate and to the extent available

52

Peer Key Financials Comments

Headquartered in Singapore, SGX is a multi asset exchange that provides listing, trading, clearing, settlement, depository and data services with over 700 employees

About 40% of listed companies and 90% of listed bonds originate from outside of Singapore

Revenue mix for operating segments: Derivatives (40.3%), Securities (25.4%), Depository services (13.7%),Market data & Connectivity (10.3%) Issuer services (10.2%), and Others (0.1%)

In February 2016, was in talks to buy Baltic Exchange, which could bolster its derivatives business and strengthen Singapore as a maritime hub

Planning to introduce a derivative product that would allow investors to trade futures on Indian sector-specific indexes

Headquartered in Australia, ASX offers a full suite of services, including listings, trading, clearing and settlement, across a comprehensive range of asset classes with over 500 employees

Revenue mix of operating segments: Derivatives & OTC markets (34.5%), Listings & issuer services (26.2%), Trading services (23.8%), Equity post trade services (13.1%), Other revenue (2.4%)

On March 1, 2016, announced collaboration with Nasdaq to replace ASX’s existing clearing technology platforms with Nasdaq’s Genium INET Clearing Platform

On January 22, 2016, bought minority stake in Digital Asset, a blockchain start up for US$10.5mm