using data to optimize foresight - … · 12/30/2016 · counterpoint february 2017 1 contributing...

TRANSCRIPT

www.MarshBerry.com

USING DATA TO OPTIMIZE FORESIGHT

The 2017 MarshBerry Market & Financial Outlook Report uncovers insights for growth and engaging the next generation Page 2

F E B R U A R Y 2 0 1 7

THE IMPACT of Service Staff on

New Business Dollars Page 4

Mergers & AcquisitionsUPDATE

Page 6

What it Takes toDOUBLE

REVENUE Page 8

MARSHBERRYlearn. improve. realize.

800.426.2774 MarshBerry.com

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 (440.354.3230).

Marsh, Berry & Company, Inc. is honored to be the investment banking firm that brokered the transactions that brought these 24 agencies and one networking organization together to form Alera Group1, as funded by Genstar Capital.

HAS ACQUIRED A&B Insurance and

Financial, Inc., AB Capital Group, LLC, Insurance

Exchange, LLC, & Smart Choice Health Plans, LLC

dba Florida Health Team, LLC

HAS ACQUIRED C.M. Smith

Agency, Inc.

HAS ACQUIRED Coury Health Services, Inc.

HAS ACQUIRED Hampson

Mowrer Agency, Inc. dba Hampson

Mowrer Kreitz Agency

HAS ACQUIRED K.B. Group

Services, Inc. dba Group

Services, Inc.

HAS ACQUIRED Shirazi Benefits,

LLC

HAS ACQUIRED American Insurance

Administrators, Inc. dba AIA

Benefits Resource Group

HAS ACQUIRED Centennial Group

Benefits and Insurance

Services, Inc.

HAS ACQUIRED Forum

Benefits, Inc.

HAS ACQUIRED HP Planning, LLC (dba CBP and/or Creative Benefit

Planning)

HAS ACQUIRED

Pentra, Inc.

HAS ACQUIRED Shirazi-Miller Benefits, LLC

HAS ACQUIRED Benefit Advisors

Network, LLCdba BAN

HAS ACQUIRED Beacon Retiree Benefits Group,

LLC

HAS ACQUIRED

MFG Retirement Systems, Inc. dba

PWA Insurance Services

HAS ACQUIRED TRUEBenefits,

LLC

HAS ACQUIRED

Benico, Ltd.

HAS ACQUIRED INGROUP

Associates, Inc.

HAS ACQUIRED Robert G. Relph Agency, Inc. (dba

Relph Benefit Advisors) & Flexible

Benefits System, Inc.

HAS ACQUIRED Virtus Benefits,

LLC

HAS ACQUIRED

Brown & Noyes, LLC dba Ardent Solutions

HAS ACQUIRED Corporate Plans, Inc. dba CPI-HR

HAS ACQUIRED GCG Financial,

Inc.

HAS ACQUIRED J.A. Counter &

Associates, Inc.

HAS ACQUIRED Silberstein

Insurance Group, LLC

1 Marsh, Berry & Company, Inc. was financial advisor to the participating selling organizations. These organizations were acquired by Alera Group effective December 30, 2016.

1CounterPoint February 2017

CONTRIBUTING AUTHORSMEGAN BOSMA, Senior Vice President

MOLLY CONNELL, Senior Consultant

DANIEL SOSNAY, Consultant

TOMMY MCDONALD, Vice President

DANI ZHELEZOVA, Data Consultant

COUNTERPOINT EDITORIAL BOARDMEGAN BOSMA, Senior Vice President

LAUREN BYERS, Vice President, Marketing

ALISON WOLF, Director, Research

SOURCES & DISCLAIMERS+ 2017 MarshBerry Market & Financial Retail Outlook Report.

FTE: Full Time Equivalent

PHP: Perspectives for High Performance

ABOUT COUNTERPOINTCounterPoint is the proprietary publication of MarshBerry. The magazine offers eleven editions annually and is published for independent insurance agents and brokers, national brokers, private equity firms, banks & credit unions, insurance carriers and specialty distributors.

A High-Level Look: ISD Specialty Distributor StudyMarshBerry ’s Insurance Services Division (ISD) completed its 2nd annual Market & Financial Outlook for Specialty Distribution.

We define the specialty insurance distribution space to include Managing General Agents, Managing General Underwriters, Program Administrators, (collectively referred to as “MGAs”) and Wholesale Brokers (“Wholesalers”). We recognize that these industry classifications can, at times, be somewhat ambiguous and that various participants in our industry can have varying definitions of each of these categories.

In 2016, we had 123 companies participate in the Study, representing approximately 5% of this market, which MarshBerry estimates at around 2,100. During our Peak Performance conference, held in Park City, UT in January 2017, MarshBerry’s Insurance Services Division shared the results with its attendees.

Four high-level takeaways from our study include:

1 Macro factors are viewed as the greatest challenge almost 2-to-1 to second-listed issue: Over 40% of participants cited economic factors as the greatest challenge to generating commission and fee growth. With the Federal Reserve raising interest rates in December 2016, indicating additional hikes are probable for 2017, and a new administration coming into power in late January, outside industry variables will likley be front-and-center this calendar year as uncertainty looms.

2 Profitability expectations are muted: Over 50% of our Wholesaler and MGA respondents expect their company’s profitability in 2017 to be flat year-over-year. While unclear what the key drivers of this expectation are, the anticipation of public policy changes, big data allowing new competitors to enter the industry who were not previously market participants, and the challenges c-suites face acquiring talent are several of which to be mindful.

3 Wholesalers’ internal strategic plans continue the search for growth: Approximately 40% are targeting new geographies and approximately 35% are expanding into new sectors, respectively. This may be accomplished by building capabilities internally, creating strategic partnerships with firms that have a footprint in the desired geography or risk, or through acquisition with a focus on the integration of new assets.

4 M&A still plays a key role in that search-for-growth mission*: Although M&A in the insurance industry was active in 2016, it was down roughly 10% in volume compared to the previous year. Specialty distributors indicated a greater desire to sell in one to three years (48%) than acquire in 2017 (24%), a flip from our results in 2015 (9% and 40%, respectively). This could be motivated by the need to focus on perpetuation, talent acquisition challenges mentioned earlier or aging owners looking for exit options.

Interested in purchasing MarshBerry’s Market & Financial Outlook for Specialty Distribution? Log on to: www.MarshBerry.com/2017MarketFinancialSpecialty

*Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd, Suite 400, Woodmere, Ohio 44122 440.354.3230

FEBR

UAR

Y SP

OT

LIG

HT

by Megan Bosma, Senior Vice President440.392.6553 | [email protected]

FEBR

UAR

Y F

EA

TU

RE

USING DATA TO OPTIMIZE FORESIGHT

2 February 2017 CounterPoint

The 2017 MarshBerry Retail Market and Financial Outlook Report uncovers talent as a top concern

for growth, and technology as a tool for recruiting, engaging and retaining the next generation.

3CounterPoint February 2017

TECHNOLOGY IS THE KEY TO UNLOCKING SOME OF THE GREATEST CHALLENGES AGENCIES FACE IN OUR INDUSTRY TODAY.

keeping insurance executives up at night, they said: availability of skills, increased tax burden and over-regulation.

With the upcoming Trump Presidency, there is uncertainty about how his administration will affect tax policy and regulation. Will Trump be pro-business as promised? Will tax burden and over-regulation still be the greatest concerns for the insurance industry when we conduct this report next year? These are questions we cannot yet answer.

Political uncertainty is matched with overall economic uncertainty. The economy is experiencing modest growth, and there is quite a bit of pressure on the labor force. Low unemployment rates meet a demand for skilled workers. There’s a skills gap, and the insurance industry is feeling this with recruiting efforts. What’s more, there is lack of education about the career opportunities young people can realize in the insurance industry, which we learned from our LinkedIn study. In this study, only 3% of respondents rated insurance as a desirable job. Technology was the highest with 32%, followed by healthcare and consumer goods at 18%.

In a tentative economic climate with lack of information about what the insurance industry promises for careers, technology is power. We cannot control what happens next in the White House. We do not know if the tax burden will ease up, or otherwise. No one is exactly sure what’s next. But harnessing data and information can help us reach and educate skilled workers, and better direct our performance through metrics. Technology can introduce new, talented people to the industry and define career pathways. And, technology can forward agencies’ success as they focus on growing a sustainable business.

Technology can help us tap into fresh, inspired talent. It can provide performance metrics so employees understand what’s next in their careers, so they recognize where they stand and how they can make a positive impact on the business. And, we know that this is something that Millennials value.

There’s a beneficial synergy between data and relationships that can give agencies a competitive advantage as they face today’s greatest industry challenges: talent acquisition, government regulation and technology. These findings come from MarshBerry’s annual Retail Market & Financial Outlook Report, a comprehensive study of external and internal factors impacting the insurance environment.

Every year, we take an industry deep-dive, asking Top Executives, independent insurance firms and prospective employees for insights on the market. The Retail Market & Financial Outlook Report looks at the issues keeping agency leaders up at night, threats to growth and challenges they’re facing. We review the economic climate and labor market; then marry MarshBerry data with study results. This year, we also directed questions via LinkedIn to potential employees age 40 and younger. We wanted to know: What attracts young people to certain companies and industries? What types of careers are this next generation of workers interested in pursuing?

The 2016 report findings align with MarshBerry’s focus on data and relationships — an inseparable combination for future success. The study highlights how embracing technology can help insurance firms effectively manage industry and economic challenges.

Following is a summary of the latest report and recommendations on how findings might direct growth, increase profit and improve talent acquisition.

What In The World? An Uncertain Economic ClimateThis year’s reporting took place during a historically turbulent time in our political climate, prior to the November 8 Presidential Election.

Before the election, 55% of respondents thought Sen. Hillary Clinton would win. And when asked about the top concerns

MOST DESIRED INDUSTRY TO WORK IN:

UNDER 40 YEARS OLD+

ME

TR

IC

4 February 2017 CounterPoint

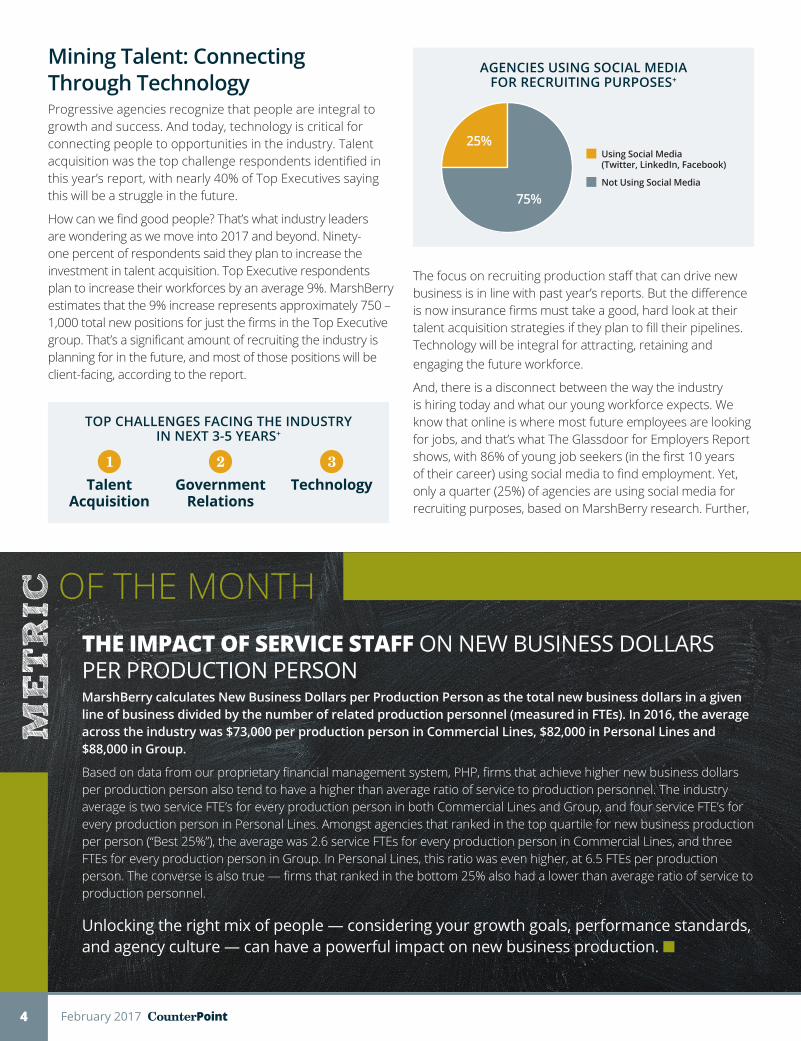

Mining Talent: Connecting Through Technology Progressive agencies recognize that people are integral to growth and success. And today, technology is critical for connecting people to opportunities in the industry. Talent acquisition was the top challenge respondents identified in this year’s report, with nearly 40% of Top Executives saying this will be a struggle in the future.

How can we find good people? That’s what industry leaders are wondering as we move into 2017 and beyond. Ninety-one percent of respondents said they plan to increase the investment in talent acquisition. Top Executive respondents plan to increase their workforces by an average 9%. MarshBerry estimates that the 9% increase represents approximately 750 – 1,000 total new positions for just the firms in the Top Executive group. That’s a significant amount of recruiting the industry is planning for in the future, and most of those positions will be client-facing, according to the report.

The focus on recruiting production staff that can drive new business is in line with past year’s reports. But the difference is now insurance firms must take a good, hard look at their talent acquisition strategies if they plan to fill their pipelines. Technology will be integral for attracting, retaining and engaging the future workforce.

And, there is a disconnect between the way the industry is hiring today and what our young workforce expects. We know that online is where most future employees are looking for jobs, and that’s what The Glassdoor for Employers Report shows, with 86% of young job seekers (in the first 10 years of their career) using social media to find employment. Yet, only a quarter (25%) of agencies are using social media for recruiting purposes, based on MarshBerry research. Further,

THE IMPACT OF SERVICE STAFF ON NEW BUSINESS DOLLARS PER PRODUCTION PERSONMarshBerry calculates New Business Dollars per Production Person as the total new business dollars in a given line of business divided by the number of related production personnel (measured in FTEs). In 2016, the average across the industry was $73,000 per production person in Commercial Lines, $82,000 in Personal Lines and $88,000 in Group.

Based on data from our proprietary financial management system, PHP, firms that achieve higher new business dollars per production person also tend to have a higher than average ratio of service to production personnel. The industry average is two service FTE’s for every production person in both Commercial Lines and Group, and four service FTE’s for every production person in Personal Lines. Amongst agencies that ranked in the top quartile for new business production per person (“Best 25%”), the average was 2.6 service FTEs for every production person in Commercial Lines, and three FTEs for every production person in Group. In Personal Lines, this ratio was even higher, at 6.5 FTEs per production person. The converse is also true — firms that ranked in the bottom 25% also had a lower than average ratio of service to production personnel.

Unlocking the right mix of people — considering your growth goals, performance standards, and agency culture — can have a powerful impact on new business production. n

OF THE MONTH

AGENCIES USING SOCIAL MEDIA

FOR RECRUITING PURPOSES+

TOP CHALLENGES FACING THE INDUSTRY

IN NEXT 3-5 YEARS+

1

Talent Acquisition

2 Government

Relations

3 Technology

5CounterPoint February 2017

when asked about connecting technologies that drive return on investment, only 15% of business leaders noted that their firm would focus investment dollars on social media.

Meanwhile, our report indicated insurance firms investing equally among internal operating systems, customer relationship management systems and data analytics. Data investments are important in these areas — but investments should also support technology to recruit employees, especially given talent acquisition as the industry’s top concern.

So, what do young people know about insurance? Not much, we learned. The employees of the future reported that technology fields are most appealing (38%). A lack of interest in insurance jobs shows us that we can do a better job of educating young people about the opportunities to grow a career and succeed in agency positions. Technology will be the key to reaching this younger generation and cultivating an engaging work environment for them once they are recruited.

Why? Because 72% of respondents in the 40 and younger age group indicated that they plan to stay at an organization for three to five years. They’re already thinking about what’s next. And taking compensation off the table, their No. 1 consideration for joining an organization is an opportunity to grow.

Young employees want their performance metrics laid out so they can see those opportunities for growth. They want to know what it takes to move to the next level. Beyond benchmarking, insurance firms need to use data as a performance metric and “what’s next” tool to show their people how their progress benefits the organization at large, and how their contributions will pay off professionally, personally and from a business standpoint. Without technology interwoven into the organization, what will attract the next generation, let alone inspire them to stay?

Raising The Future — A Call To Action The year 2016 was marked by political stress, modest overall economic growth, and a tightening labor market. Successful businesses understand that talent is integral to their success. People are everything.

The old ways of hiring and developing leaders needs an overhaul to align with expectations of the future workforce. They want to know what’s in it for them — how can they grow? — before they’ll consider signing on. Future employees expect a plan, they want to know, “How am I doing?” And they’re looking for career opportunities online and through social media. They value the reputation and image of their employers. Future employees want to be a part of something good. That means insurance firms must engage, educate, and demonstrate the career potential this industry offers. Because based on the report, young prospective employees have no idea.

Data and relationships are central to success. Firms that capitalize on technology for recruiting, and put performance metrics to work for growing young leaders, will realize that powerful connection. We believe the future of insurance firms depends on bringing this synergy to life in their organizations. n

AVERAGE NEW BUSINESS DOLLARS

PER PRODUCTION PERSON

BRINGING TECHNOLOGY INTO THE INSURANCE ENVIRONMENT IS PARAMOUNT TO SUCCESS IN TALENT ACQUISITION AND MANAGEMENT.

MarshBerry proprietary financial management system, Perspectivesfor High Performance (PHP).

6 February 2017 CounterPoint

DEA

LMAK

ERS

DIA

LO

GU

EMergers & Acquisitions Updateby Molly Connell, Senior Consultant 440.392.6584 | [email protected]

The ravenous Merger & Acquisition (M&A) appetite continued in 2016 with 443 announced U.S. based transactions, falling only 13 deals short of 2015’s record breaking year (the year that shattered all prior years’ activity by over 100 deals). 2016 is the second strongest deal activity year in the last decade.

Continuing to drive M&A activity are the private equity backed buyers with 242 transactions in 2016, followed by the independent agencies with 107 transactions. Independent agencies often times find it difficult to compete on price but in our experience, we have seen that they are able to stay competitive by offering more flexible and creative deal structures. The makeup of the sellers consists of 44% property and casualty firms, 38% multi-line firms (i.e., both property and casualty and employee benefits) and 18% employee benefits and consulting firms with an 84%/16% split between retail and specialty distributors.

AGENCIES NEED TO DRIVE NEW BUSINESS SIGNIFICANTLY IN ORDER TO GROW ORGANICALLY IN THIS RATE ENVIRONMENT.

TOTAL ANNOUNCED U.S. TRANSACTIONS

Source: SNL Financial, Insurance Journal, and other publicly available sources. All transactions in this presentation are announced deals involving public company acquirers, banks, and private equity groups as well as private company acquirers. All targets are U.S. only. This data displays a snapshot at a particular point in time and has not been updated to reflect subsequent changes in prior years, if any. MarshBerry estimates that only 15%-30% of all transactions are actually made public. Past performance is not necessarily indicative of future results.

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd, Suite 400, Woodmere, Ohio 44122 440.354.3230

7CounterPoint February 2017

In the meantime, companies will likely continue to seek ways to supplement slow organic growth through M&A opportunities.

Organic GrowthThe property and casualty rate environment continues to decline while health premiums continue to rise. According to MarshBerry’s 2017 Market & Financial Retail Outlook Report, with flat new business as a percentage of prior year commissions and fees, it comes as no surprise that average agency organic growth has held relatively flat in 2016 with estimated organic growth of approximately 3.9% in 2016.

Private Equity2016 brought fewer buyers to the table with 167 buyers compared to 188 total in 2015. Private equity-backed firms remained the dominant buying group, representing over half of all announced transactions (55%) in 2016. Accounting for only 16% of total buyers, Private equity-backed firms are the only buying group to increase in count with an additional five buyers compared to 2015. Of the 242 transactions completed in 2016 by private equity-backed firms, 33 transactions were completed by seven first-time acquirers, 24 of which were completed by newly formed Alera Group. Of the seven new buyers, three focused in retail distribution and four focused in the specialty distribution markets.

ValuationsMarshBerry continues to see a seller’s market for quality firms that demonstrate a history of predicable, profitable, organic growth as well as continuous reinvestment in people and technology. We are seeing deal values, expressed as a multiple of Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA), plateauing at their peak levels, but not declining.

It remains unclear the impact President Trump’s policies will have on the M&A environment. However, in our opinion, what has been driving valuations higher (i.e., interest rates, leverage ratios, and the rate environment) are at risk in the current market. n

All deal count metrics are inclusive of completed deals with U.S. targets only, unless otherwise specified. MarshBerry estimates that only 15-30% of all transaction are actually made public. Past performance is not indicative of future results

Source: SNL Financial, Insurance Journal, and other publicly available sources.

Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd, Suite 400, Woodmere, Ohio 44122 440.354.3230

PEER EXCHANGE NETWORK NEWS

INTERESTED IN LEARNING MORE ABOUT OUR PEER EXCHANGE NETWORKS? Please contact Tommy McDonald today at [email protected]

2017 spring network summits are right around the corner!

BANK/TASCMarch 6-8 Omni Scottsdale Resort & Spa at Montelucia, Scottsdale, AZOur theme for the spring BANK/TASC summit is Turning Data into Knowledge: Using YOUR Data as a Market Differentiator.

What to watch for:

n THE STATE OF THE INDUSTRY presented by John Wepler, Chairman & CEO

MarshBerry examines the landscape of current factors affecting the insurance industry, providing our outlook and what to expect in the year ahead.

n USING YOUR DATA TO CREATE COMPETITIVE ADVANTAGE presented by Christina Rouse, Chief Architect, Incisive Analytics Over the last several years, Incisive Analytics has helped many businesses put power behind their business intelligence endeavors. Employing a team of sophisticated data scientists, the firm shares the latest insights and case studies from the front lines of data innovation and implementation.

Register now! www.MarshBerry.com/SP17BANKTASC

8 February 2017 CounterPoint

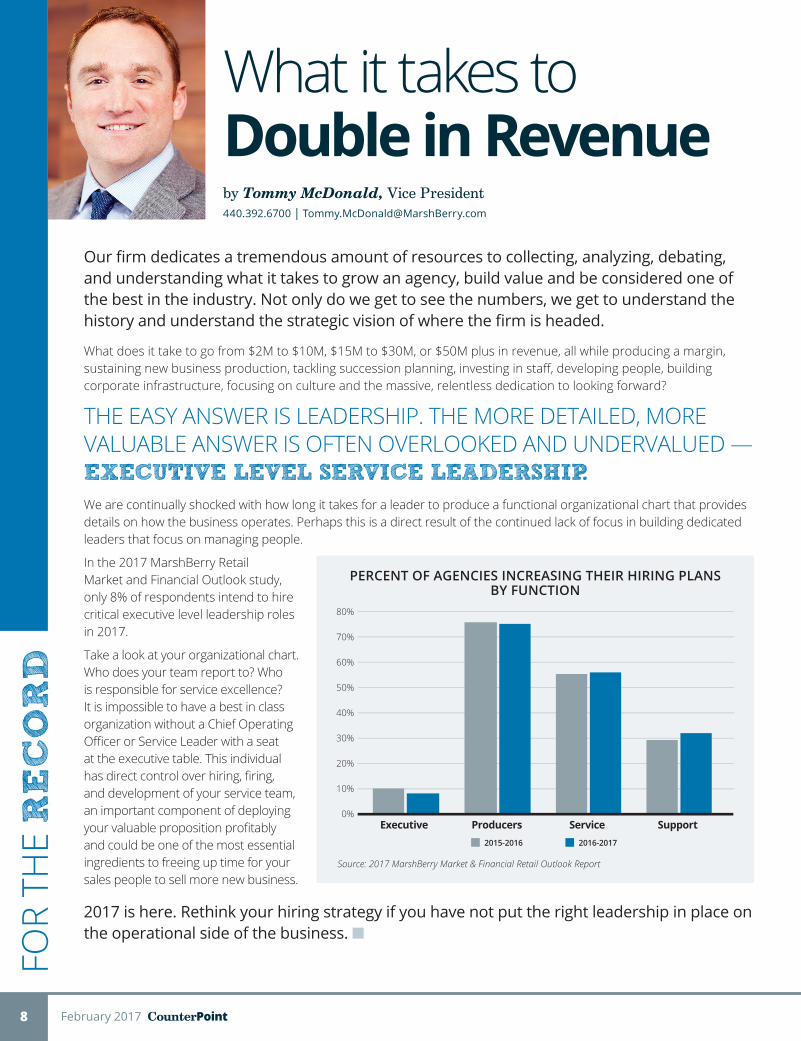

What it takes to Double in Revenueby Tommy McDonald, Vice President 440.392.6700 | [email protected]

Our firm dedicates a tremendous amount of resources to collecting, analyzing, debating, and understanding what it takes to grow an agency, build value and be considered one of the best in the industry. Not only do we get to see the numbers, we get to understand the history and understand the strategic vision of where the firm is headed.

What does it take to go from $2M to $10M, $15M to $30M, or $50M plus in revenue, all while producing a margin, sustaining new business production, tackling succession planning, investing in staff, developing people, building corporate infrastructure, focusing on culture and the massive, relentless dedication to looking forward?

THE EASY ANSWER IS LEADERSHIP. THE MORE DETAILED, MORE VALUABLE ANSWER IS OFTEN OVERLOOKED AND UNDERVALUED — EXECUTIVE LEVEL SERVICE LEADERSHIP. We are continually shocked with how long it takes for a leader to produce a functional organizational chart that provides details on how the business operates. Perhaps this is a direct result of the continued lack of focus in building dedicated leaders that focus on managing people.

In the 2017 MarshBerry Retail Market and Financial Outlook study, only 8% of respondents intend to hire critical executive level leadership roles in 2017.

Take a look at your organizational chart. Who does your team report to? Who is responsible for service excellence? It is impossible to have a best in class organization without a Chief Operating Officer or Service Leader with a seat at the executive table. This individual has direct control over hiring, firing, and development of your service team, an important component of deploying your valuable proposition profitably and could be one of the most essential ingredients to freeing up time for your sales people to sell more new business.

2017 is here. Rethink your hiring strategy if you have not put the right leadership in place on the operational side of the business. n

FOR

THE

RE

CO

RD

PERCENT OF AGENCIES INCREASING THEIR HIRING PLANS

BY FUNCTION

Source: 2017 MarshBerry Market & Financial Retail Outlook Report

in Partnership with Insurance JournalMarshBerry and Insurance Journal have joined forces to bring a series of online technical training courses designed specifically to provide new producers in the Property & Casualty insurance industry the knowledge they need to develop a foundation for success.

This 15-hour, 8-week program is authored and instructed by Christopher J. Boggs, CPCU, ARM, ALCM, one of the top insurance educators in the country. In addition to the 8-week program, subscribers also have access to the entire catalog of courses and live webinars.

For more information, and to view a current training curriculum, visit: www.MarshBerry.com/training-portal

9CounterPoint February 2017

MarshBerry has released its 31st Annual Retail Market & Financial Outlook Report. The study compiles qualitative and quantitative agency information including financial, market, carrier and technology data and incorporates information from MarshBerry’s proprietary financial management system Perspectives for High Performance (“PHP”). Responses are anonymized and the findings are then summarized in a State of the Industry Outlook report.

The complete report enables independent insurance agencies to highlight key agent and broker performance trends from 2007–2016. The five core chapters offer a market overview and outlook. Charts in each section provide information on:

n External Factors — Economy — Market Dynamicsn Merger & Acquisitions* n Growth n ExpenseManagement&Profitn Operations & Productivity

THE FULL REPORT IS AVAILABLE TO PURCHASE ONLINE AT WWW.MARSHBERRY.COM/2017MARKETFINANCIAL FOR $399.

NOW AVAILABLE

Property & Casualty Insurance Training for New Producers

*Securities offered through MarshBerry Capital, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Blvd, Suite 400, Woodmere, Ohio 44122 440.354.3230

28601 Chagrin Blvd., Ste. 400 Woodmere, OH 44122

www.MarshBerry.com

@marshberryinc

facebook.com/MarshBerry

linkedin.com/company/ MarshBerry

Mark your calendars!

MARCH 20173.6-8 • BANK/TASC Summit, Scottsdale, AZ

APRIL 20174.24-25 • Build Your 2020 Organic Growth Vision, Austin, TX4.25-28 • APPEX Summit, Austin, TX

MAY 2017 2017 MarshBerry 3605.09 • New Orleans, Harrah’s New Orleans5.11 • New York, Convene at 237 Park Avenue5.23 • Chicago, Swissotel Chicago5.25 • Las Vegas, The Cosmopolitan of Las Vegas

Register at www.MarshBerry.com/360 by February 24 and save 50%!

JUNE 20176.15-16 • SalesPro-Producer Performance Workshop,

Cleveland, OH6.15-16 • Organic Growth Leadership Seminar,

Cleveland, OH

MARSHBERRY28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122

ENGAGE WITH MARSHBERRY

HORIZON

ON

TH

E

Log on to www.MarshBerry.com to register for events, view latest news and read back issues of CounterPoint.

WE WANT TO HEAR FROM YOU!

We want to make sure we’re providing the content you

want to read and want feedback on the articles we’re publishing.

Please send an email to us at [email protected]

to share your thoughts!