us midstream and mlps

TRANSCRIPT

US Midstream and MLPs Raising Commodity Price Forecast

Master Limited Partnerships | Increase Target Price

Lifting NGL Price Forecast: We lift our ’21 NGL price forecast to $0.94/gal from

$0.84/gal to reflect the higher than expected 3Q21 M2M, higher natural gas prices, and

the tight NGL supply/demand balance entering the winter season. Absent more aggressive

drilling plans from producers, we believe NGL inventories are at risk of further depletion.

Accordingly, we increase our ’22 and ’23 NGL price forecast 15% and 11% to $0.99/gal

and $0.88/gal. We lifted our ’22 and ’23 ethane price by 26% and 7% to reflect the

higher natural gas price environment supporting elevated ethane prices. Our ’22 and ’23

propane prices increase 8% and 3% to $1.15/gal and $1.03/gal due to risk of stock

depletion as we enter the winter heating season. Notably, weekly US propane inventories

are trending roughly 27 mmbbls (-27%) below average early October levels the past two

years.

Lifting Natural Gas Price Forecast: On October 4th, the CS US E&P team lifted its

4Q21 Henry Hub natural gas price forecasts to $5.75/mmbtu (from $3.50/mmbtu) on

tight supply/demand balances due to below average storage levels entering the withdrawal

season, global pricing incentivizing LNG exports, limits to gas-to-coal fuel switching, and

muted domestic supply growth. ’22 and ’23 price forecasts also increased to $4.00 and

$3.25/mmbtu from $3.00 and $2.75/mmbtu respectively due to recent strength in the

futures curve and an undersupplied US gas market in ’22 and ’23 (Please refer to the US

E&Ps note for more detail).

Target Price Changes: We are raising our target prices for eight stocks: LNG, CQP,

DCP, MPLX, NFE, OKE, TRGP, and WMB.

13 October 2021

Equity Research

Americas | United States

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS,

LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could

affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

13 October 2021

US Midstream and MLPs 2

Click here to enter text.

Altus Midstream Company Maintain Underperform and $45 TP

ALTM

Target price (12M, US$) 45.00

Underperform[V]

Master Limited Partnerships

Maintain Underperform and $45 TP: We maintain Underperform. Our $45 TP is based

on our dividend discount methodology. Our DDM imputes a 12% discount rate on

dividends.

Adjusting Estimates: We raise ‘21e EBITDA <1% to reflect higher G&P volumes.

Our ’22e and ’23e EBITDA increases slightly to reflect the flow-through impacts of higher

G&P volumes.

Risks: Upside risks include greater Alpine High production activity by APA, more

constructive preferred redemption and higher earnings from JV pipelines.

Price (12 Oct 21, US$) 84.20

52-week price range 84.20 - 9.55

Enterprise value (US$ m) 2,646

Adjusted EV -

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 191 269 256 251 Prev Adjusted EBITDA (US$ m) - 267 255 250 Distribution/Unit (US$ m) 0.00 6.00 6.00 6.00 Distribution Coverage (x) 0.00 2.06 2.23 2.19 Earnings/Unit - EPU (US$) 2.57 2.04 7.87 7.65 EV / Adj. EBITDA (x) 35.03 10.89 10.65 10.45 Price/DCF to LPs (x) 6.33 6.55 6.06 6.17

DPU (US$) 6.00 Distribution Yield (%) 7.41 Units Outstanding (m) 16 GP Take (%) - Net Debt Current (US$ m) 558 Net Debt/EBITDA (x) 5.33

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 12-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct12, 2021, 10/12/20 = US$10.31

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 47 44 53 48 2021E 65 69 68 66 2022E 63 64 65 64

13 October 2021

US Midstream and MLPs 3

Altus Midstream Company (ALTM) Analyst: Spiro Dounis Price (12 Oct 2021): US$84.2 Target Price: 45.00 Rating: Underperform [V] Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 191 269 256 251 Prev. Adj. EBITDA - 267 255 250 (-) Maintenance Capex - - - - (-) Cash Interest Expense 10 13 20 18 (+/-) Other Adjustments - - - - (-) General Partner Take - - - - (-) Preferred Dividends 46 37 0 0 Adj. DCF Available to LPs 122 201 217 213

DCF Per LP Unit / Common Share 7.50 12.36 13.36 13.13 Distribution Per Unit / Share .00 6.00 6.00 6.00 Distribution Coverage (x) .00 2.06 2.23 2.19

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 47 44 53 48 2021E 65 69 68 66 2022E 63 64 65 64

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 0.00 7.41 7.41 7.41 Dividend / Distribution Growth (%, YoY) 0.00 0.00 0.00 0.00 DCF Yield (%) 15.80 15.27 16.51 16.22 EV / EBITDA (x) 35.03 10.89 10.65 10.45

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 7.48 5.33 5.10 4.76 Net Debt / Total Capital (%) 39.03 78.00 73.07 68.07

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 148 136 113 99

CoGS and OpEx 38 29 27 23 SGA 13 14 15 14 (+) Other EBITDA - - - - DD&A 16 16 15 15 Other 17 10 25 25 Operating Income 64 67 29 21

Interest 2 13 20 18 Equity Income (Loss) 59 121 157 161 Other Income (Loss) 0 0 0 0 Earnings Before Tax 120 174 167 164

Taxes (1) 0 0 0 Net Income to LPs / Company 42 35 138 136

Earning Per Share / Unit 2.57 2.04 7.87 7.65 Avg. Diluted Shares / Units Outstanding 16 17 18 18

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income 80 188 167 164 DD&A 16 16 15 15 Others 84 34 50 49 Cash Flow from Operations 164 221 217 213

Acquisitions 10 2 0 0 Total Capex (340) (17) (8) (8) Expansion Capex - - - - Maintenance Capex - - - - Others (9) 0 0 0 Cash Flow from Investments (338) (15) (8) (8)

Equity Issuance (Repurchase) 0 0 0 0 Debt Issued 228 760 (195) (110) Dividends / Distributions Paid (23) (145) (97) (97) Others (13) (739) 0 0 Cash Flow from Financing 192 (124) (292) (207)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 24 106 23 21 Other Current Assets 19 23 23 23 Net PPE 196 187 179 172 Other Long-Term Assets 1,561 1,544 1,509 1,474 Total Assets 1,800 1,860 1,734 1,691

Short-Term Debt 0 0 0 0 Other Short Term Liabilities 30 25 25 25 Long-Term Debt 624 1,384 1,189 1,079 Other Long-Term Liabilities 209 90 90 90 Total Liabilities 863 1,499 1,304 1,194

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other - - - - Total Liabilities and Equity 1,800 1,860 1,734 1,691

Company Background

Altus Midstream is a pure-play, Permian midstream C-corp, anchored by

Apache Corporation’s gathering, processing and transportation assets at

Alpine High. Altus also owns options in five gas, NGL, and crude oil

pipeline projects from the Permian Basin.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 50.00) 85.00

Our blue sky scenario of $85 is based on a 5% dividend growth per

annum at a 9% discount rate - 3% lower than base assumptions.

Our Grey Sky Scenario (US$) 32.00

Our grey sky scenario of $32 is based on additional equity issuance in the

future driving declining dividends and discounted back at 15% - 3%

higher than base assumptions.

Share price performance

On 12-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct12, 2021, 10/12/20 = US$10.31

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 4

Cheniere Energy Reiterate Outperform; Increase TP to $116

LNG

Target price (12M, US$) 116.00

Outperform

Master Limited Partnerships

Lifting Estimates on Commodity Tailwinds: We increase our ‘21e EBITDA by ~3%,

driven by macro tailwinds which have resulted in record high LNG prices (JKM and NBP

each breaking >$30/mmbtu in recent months). With LNG margins up ~$7/mmbtu QoQ,

we estimate a ~$140mm 2H21 tailwind to LNG (assuming 20Tbtu of open capacity). We

now expect 2021 EBITDA to come in above Cheniere’s $4.6-$4.9bln guidance range

(most recent guidance points to the high end of the range). Looking to next year, we see

substantial upside into ‘22 with strong LNG margins likely to persist and an estimated

>100TBtu of potential open capacity as SPL T6 comes online. Accordingly, we increase

our ‘22e EBITDA ~5%.

Now Incorporating Stage 3 Into Our Model: We now assume that CCL Stage 3

reaches FID in 2022. We estimate a completion date ~5 years after FID, in-line with

Cheniere guidance, but likely a conservative timeline, in our view. We assume ~$6bln of

capex (50% debt financed) through 2026 and ~$1bln of Stage 3 EBITDA with a 1Q27

ISD, bringing our ‘27e EBITDA to ~$6.9bln, the high end of Cheniere’s run-rate guidance.

Reiterate Outperform; Increase TP to $116 (from $105): We reiterate Outperform and

increase our target price to $116 (from $105). Macro tailwinds and LNG pricing strength

primarily drive the increase; Stage 3 moving forward also contributes. An NPV analysis

drives our $116 TP and implies a 10.65x multiple on our FY22e EBITDA. The current

share price implies an ~11% DCF yield on a 9-train run rate in 2024.

Risks: Downside risks include lower global LNG prices, execution risk and higher US

natural gas pricing.

Previous target price (12M, US$) 105.00

Price (11 Oct 21, US$) 101.63

52-week price range 102.30 - 47.05

Enterprise value (US$ m) 53,298

Adjusted EV -

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 3,961 5,000 5,450 5,500 Prev Adjusted EBITDA (US$ m) - 4,850 5,168 5,410 Distribution/Unit (US$ m) 0.00 0.66 1.34 1.41 Distribution Coverage (x) 0.00 13.19 7.14 7.04 Earnings/Unit - EPU (US$) 3.04 6.81 8.40 9.05 EV / Adj. EBITDA (x) 11.83 11.15 9.91 9.61 Price/DCF to LPs (x) 11.82 11.52 10.16 9.84

DPU (US$) 1.32 Distribution Yield (%) 0.66 Units Outstanding (m) 254 GP Take (%) - Net Debt Current (US$ m) 27,875 Net Debt/EBITDA (x) 5.58

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$49.03

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,039 1,393 477 1,052 2021E 1,452 1,023 1,123 1,402 2022E 1,116 1,493 1,455 1,386

13 October 2021

US Midstream and MLPs 5

Cheniere Energy (LNG) Analyst: Spiro Dounis Price (11 Oct 2021): US$101.63 Target Price: (from 105.00) 116.00 Rating: Outperform Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 3,961 5,000 5,450 5,500 Prev. Adj. EBITDA - 4,850 5,168 5,410 (-) Maintenance Capex 0 0 0 0 (-) Cash Interest Expense (570) (677) (801) (942) (+/-) Other Adjustments (3,189) (3,473) (3,833) (3,976) (-) General Partner Take - - - - (-) Preferred Dividends - - - - Adj. DCF Available to LPs 1,342 2,205 2,417 2,467

DCF Per LP Unit / Common Share 5.08 8.65 9.61 9.93 Distribution Per Unit / Share .00 .66 1.34 1.41 Distribution Coverage (x) .00 13.19 7.14 7.04

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,039 1,393 477 1,052 2021E 1,452 1,023 1,123 1,402 2022E 1,116 1,493 1,455 1,386

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 0.00 0.66 1.38 1.44 Dividend / Distribution Growth (%, YoY) DCF Yield (%) 0.00 0.66 1.38 1.44 EV / EBITDA (x) 11.83 11.15 9.91 9.61

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 7.21 5.58 4.87 4.68 Net Debt / Total Capital (%) 92.94 89.93 85.20 80.94

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 9,358 9,656 7,389 7,499

CoGS and OpEx 3,946 2,829 0 0 SGA 302 328 345 360 (+) Other EBITDA - - - - DD&A 932 979 971 989 Other 1,257 1,621 1,709 1,756 Operating Income 2,921 3,899 4,363 4,395

Interest 1,525 1,457 1,456 1,422 Equity Income (Loss) - - - - Other Income (Loss) 0 0 0 0 Earnings Before Tax 1,396 2,442 2,908 2,973

Taxes 43 58 145 149 Net Income to LPs / Company 767 1,726 2,112 2,249

Earning Per Share / Unit 3.04 6.81 8.40 9.05 Avg. Diluted Shares / Units Outstanding 252 253 252 248

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income 501 1,624 2,762 2,824 DD&A 932 979 971 989 Others (499) (340) 0 0 Cash Flow from Operations 1,265 3,042 3,733 3,813

Acquisitions 0 68 0 0 Total Capex (1,839) (1,130) (1,060) (1,840) Expansion Capex (1,839) (1,130) (1,060) (1,840) Maintenance Capex 0 0 0 0 Others (108) (11) 0 0 Cash Flow from Investments (1,947) (1,073) (1,060) (1,840)

Equity Issuance (Repurchase) (155) (50) (300) (300) Debt Issued 883 (374) (560) (560) Dividends / Distributions Paid 0 (84) (337) (346) Others (963) (742) (666) (708) Cash Flow from Financing (235) (1,249) (1,863) (1,914)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 1,628 2,797 3,607 3,665 Other Current Assets 1,092 1,435 1,435 1,435 Net PPE 30,421 30,493 30,582 31,433 Other Long-Term Assets 2,107 2,799 2,799 2,799 Total Assets 35,697 37,523 38,422 39,332

Short-Term Debt 372 949 949 949 Other Short Term Liabilities 1,824 2,577 2,577 2,577 Long-Term Debt 30,471 29,372 28,812 28,252 Other Long-Term Liabilities 812 1,542 1,542 1,542 Total Liabilities 33,479 34,440 33,880 33,320

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 2,409 2,421 2,405 2,272 Total Liabilities and Equity 35,697 37,523 38,422 39,332

Company Background

Cheniere is a general partner holding company, primarily engaged in

LNG-related businesses, that owns 100% of the general partner interest

in Chenier Partners and a majority stake in Cheniere Holdings.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 115.00) 127.00

Our Blue Sky scenario of $127 assumes 10% higher margins on CMI,

which would be driven by better global LNG spot pricing and/or better

short/medium-term contract rates, as well as 10% better margins on

sourcing, which would reflect better natural gas differentials capture. We

also assume a 0.25x improvement in its EV/EBITDA multiple to reflect for

the better macro environment.

Our Grey Sky Scenario (US$) (from 72.00) 81.00

Our Grey Sky scenario of $81 assumes 25% lower margins on CMI,

which would be driven by lower global LNG spot pricing and/or weaker

short/medium-term contract rates, as well as 25% worse margins on

sourcing, which would reflect more difficult natural gas differentials

capture. We also assume a 1.0x degradation in its EV/EBITDA multiple

to reflect for the tougher macro environment.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$49.03

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 6

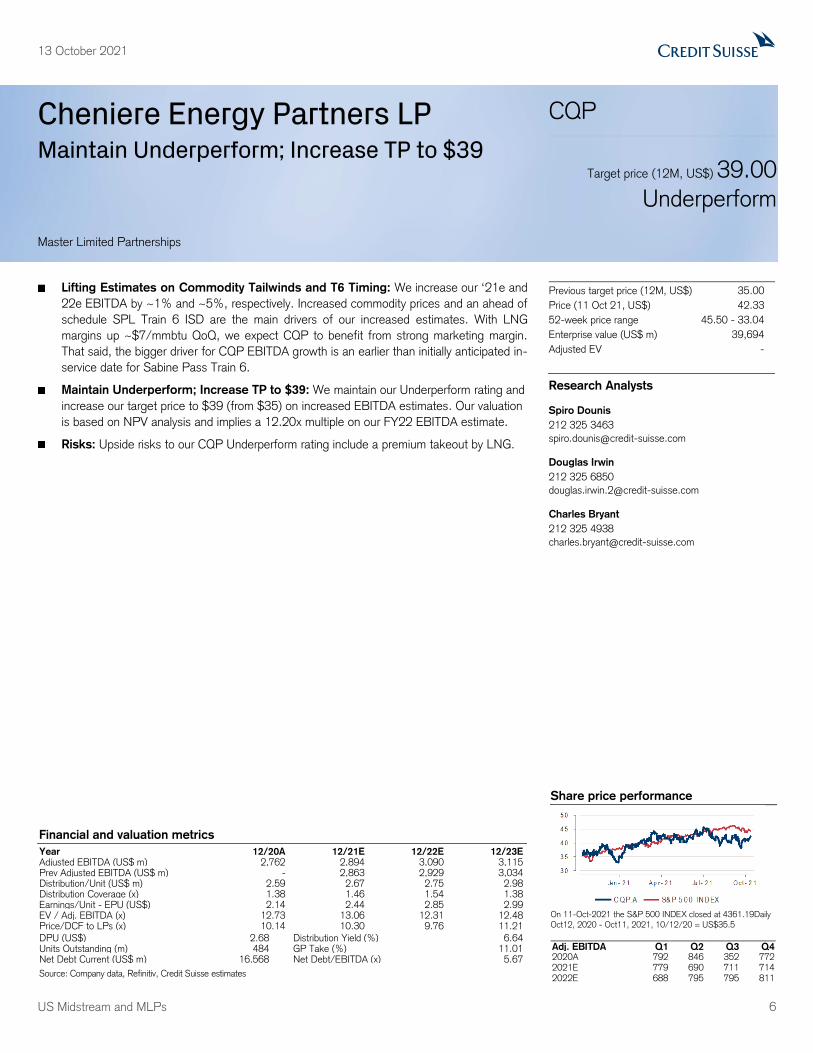

Cheniere Energy Partners LP Maintain Underperform; Increase TP to $39

CQP

Target price (12M, US$) 39.00

Underperform

Master Limited Partnerships

Lifting Estimates on Commodity Tailwinds and T6 Timing: We increase our ‘21e and

22e EBITDA by ~1% and ~5%, respectively. Increased commodity prices and an ahead of

schedule SPL Train 6 ISD are the main drivers of our increased estimates. With LNG

margins up ~$7/mmbtu QoQ, we expect CQP to benefit from strong marketing margin.

That said, the bigger driver for CQP EBITDA growth is an earlier than initially anticipated in-

service date for Sabine Pass Train 6.

Maintain Underperform; Increase TP to $39: We maintain our Underperform rating and

increase our target price to $39 (from $35) on increased EBITDA estimates. Our valuation

is based on NPV analysis and implies a 12.20x multiple on our FY22 EBITDA estimate.

Risks: Upside risks to our CQP Underperform rating include a premium takeout by LNG.

Previous target price (12M, US$) 35.00

Price (11 Oct 21, US$) 42.33

52-week price range 45.50 - 33.04

Enterprise value (US$ m) 39,694

Adjusted EV -

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 2,762 2,894 3,090 3,115 Prev Adjusted EBITDA (US$ m) - 2,863 2,929 3,034 Distribution/Unit (US$ m) 2.59 2.67 2.75 2.98 Distribution Coverage (x) 1.38 1.46 1.54 1.38 Earnings/Unit - EPU (US$) 2.14 2.44 2.85 2.99 EV / Adj. EBITDA (x) 12.73 13.06 12.31 12.48 Price/DCF to LPs (x) 10.14 10.30 9.76 11.21

DPU (US$) 2.68 Distribution Yield (%) 6.64 Units Outstanding (m) 484 GP Take (%) 11.01 Net Debt Current (US$ m) 16,568 Net Debt/EBITDA (x) 5.67

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$35.5

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 792 846 352 772 2021E 779 690 711 714 2022E 688 795 795 811

13 October 2021

US Midstream and MLPs 7

Cheniere Energy Partners LP (CQP) Analyst: Spiro Dounis Price (11 Oct 2021): US$42.33 Target Price: (from 35.00) 39.00 Rating: Underperform Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 2,762 2,894 3,090 3,115 Prev. Adj. EBITDA - 2,863 2,929 3,034 (-) Maintenance Capex 0 0 0 0 (-) Cash Interest Expense (909) (844) (837) (812) (+/-) Other Adjustments 0 0 0 0 (-) General Partner Take 121 160 199 310 (-) Preferred Dividends - - - - Adj. DCF Available to LPs 1,732 1,890 2,055 1,994

DCF Per LP Unit / Common Share 3.58 3.90 4.24 4.12 Distribution Per Unit / Share 2.59 2.67 2.75 2.98 Distribution Coverage (x) 1.38 1.46 1.54 1.38

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 792 846 352 772 2021E 779 690 711 714 2022E 688 795 795 811

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 7.14 6.64 6.64 6.45 Dividend / Distribution Growth (%, YoY) DCF Yield (%) 9.86 9.78 10.63 10.32 EV / EBITDA (x) 12.73 13.06 12.31 12.48

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 5.81 5.67 5.27 5.04 Net Debt / Total Capital (%) 96.81 96.75 95.75 95.29

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 6,167 5,755 3,989 4,052

CoGS and OpEx 2,537 1,927 0 0 SGA 110 84 63 57 (+) Other EBITDA - - - - DD&A 551 557 563 549 Other 759 851 836 879 Operating Income 2,210 2,337 2,527 2,566

Interest 909 844 837 812 Equity Income (Loss) - - - - Other Income (Loss) 7 0 0 0 Earnings Before Tax 1,308 1,492 1,690 1,755

Taxes 0 0 0 0 Net Income to LPs / Company 998 1,182 1,380 1,445

Earning Per Share / Unit 2.14 2.44 2.85 2.99 Avg. Diluted Shares / Units Outstanding 467 484 484 484

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income 1,183 1,468 1,690 1,755 DD&A 551 557 563 549 Others 17 56 0 0 Cash Flow from Operations 1,751 2,082 2,253 2,304

Acquisitions 0 0 0 0 Total Capex (972) (906) (140) (120) Expansion Capex (972) (906) (140) (120) Maintenance Capex 0 0 0 0 Others 0 0 0 0 Cash Flow from Investments (972) (906) (140) (120)

Equity Issuance (Repurchase) 0 0 0 0 Debt Issued (5) 12 24 (576) Dividends / Distributions Paid (1,359) (1,436) (1,510) (1,675) Others (70) (64) (24) (24) Cash Flow from Financing (1,434) (1,488) (1,510) (2,275)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 1,210 930 1,533 1,442 Other Current Assets 828 741 741 741 Net PPE 16,723 17,099 16,675 16,246 Other Long-Term Assets 287 289 289 289 Total Assets 19,145 19,123 19,303 18,783

Short-Term Debt 0 654 654 654 Other Short Term Liabilities 883 852 852 852 Long-Term Debt 17,580 16,947 16,971 16,395 Other Long-Term Liabilities 143 111 111 111 Total Liabilities 18,606 18,564 18,588 18,012

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 0 0 0 0 Total Liabilities and Equity 19,145 19,123 19,303 18,783

Company Background

Cheniere Energy Partners is anMLP which owns and operates the Sabine

Pass LNG terminal through its wholly owned subsidiary, SPLNG.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 45.00) 50.00

Our Blue Sky of $50 scenario assumes 20% higher margin to SPL from

CMI, which would be driven by better pricing at CMI (when netbacks are

below $3/mmbtu) or higher volumes at CMI / outperformance on SPL

utilization above SPA volumes, as well as 20% better margins on

sourcing, which would reflect better natural gas differentials capture. We

also assume a 1.25x improvement in its EV/EBITDA multiple to reflect for

the better macro environment.

Our Grey Sky Scenario (US$) (from 28.00) 32.00

Our Grey Sky scenario of $32 assumes 50% lower margins to SPL from

CMI, which would be driven by weaker pricing at CMI or lower excess

production at SPL beyond SPA volumes, as well as 50% worse margins

on sourcing, which would reflect worse natural gas differentials capture.

We also assume a 0.2x degradation in its EV/EBITDA.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$35.5

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 8

DCP Midstream LP Maintain Neutral; Increase TP to $34

DCP

Target price (12M, US$) 34.00

Neutral[V]

Master Limited Partnerships

Commodity Strength Drives Higher Estimates: We increase our ‘21e and ‘22e

EBITDA by ~3%/4% to reflect a stronger than expected commodity environment. As a

result, we continue to view the high-end of DCP’s $1.12-$1.26bln ‘21 EBITDA guidance

as very achievable. Based on guided sensitivities, we estimate an >$60mm 2H21 tailwind,

which would likely push EBITDA above the high-end of the range on commodity strength

alone. We also see continued upside on elevated producer activity.

Capital Return Options Materializing: We expect DCP to move below 4.0x leverage in

3Q21 and below the long-term 3.5x target by 3Q22. We view leverage as the primary

hurdle to establish a capital return framework that should result in more capital being

returned to equity holders. With an improved line of sight toward this goal in the current

commodity environment, we wouldn’t be surprised if management begins to outline a

possible framework with 4Q earnings in February, which is when DCP typically provides

full-year guidance. As far as what this framework could look like, we estimate ~$350mm

of 2H22 FCF (post-distribution) that could be allocated toward further debt reduction,

buybacks, or increased distributions once leverage targets are reached.

Maintain Neutral; Increase TP to $34: We increase our TP to $34 (from $30) to reflect

increased EBITDA estimates in an improved commodity environment. Our TP is NPV-

derived, implying a multiple of 8.5x on ‘22 EBITDA. We maintain our Neutral rating.

Catalysts & Risks: Sustained NGL price strength is the main catalyst given DCP’s

commodity exposure and capacity to recover additional ethane volumes across the NGL

footprint. Downside risks include weaker commodity pricing and a slower than expected

uptick in producer activity.

Previous target price (12M, US$) 30.00

Price (11 Oct 21, US$) 30.83

52-week price range 31.69 - 12.10

Enterprise value (US$ m) 11,845

Adjusted EV -

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 1,252 1,349 1,464 1,427 Prev Adjusted EBITDA (US$ m) - 1,310 1,410 1,398 Distribution/Unit (US$ m) 1.56 1.56 1.56 1.56 Distribution Coverage (x) 2.62 2.84 3.27 3.28 Earnings/Unit - EPU (US$) 1.88 2.46 3.22 3.13 EV / Adj. EBITDA (x) 8.17 9.36 8.16 7.89 Price/DCF to LPs (x) 4.55 6.95 6.02 6.01

DPU (US$) 1.56 Distribution Yield (%) 5.07 Units Outstanding (m) 208 GP Take (%) 0.00 Net Debt Current (US$ m) 5,590 Net Debt/EBITDA (x) 4.02

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$12.47

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 321 311 331 289 2021E 275 333 359 382 2022E 363 357 364 380

13 October 2021

US Midstream and MLPs 9

DCP Midstream LP (DCP) Analyst: Spiro Dounis Price (11 Oct 2021): US$30.83 Target Price: (from 30.00) 34.00 Rating: Neutral [V] Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 1,252 1,349 1,464 1,427 Prev. Adj. EBITDA - 1,310 1,410 1,398 (-) Maintenance Capex (45) (67) (69) (67) (-) Cash Interest Expense - - - - (+/-) Other Adjustments - - - - (-) General Partner Take - - - - (-) Preferred Dividends 59 59 60 60 Adj. DCF Available to LPs 850 922 1,064 1,066

DCF Per LP Unit / Common Share 4.07 4.42 5.11 5.12 Distribution Per Unit / Share 1.56 1.56 1.56 1.56 Distribution Coverage (x) 2.62 2.84 3.27 3.28

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 321 311 331 289 2021E 275 333 359 382 2022E 363 357 364 380

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 8.42 5.07 5.07 5.07 Dividend / Distribution Growth (%, YoY) (50.00) 0.00 0.00 0.00 DCF Yield (%) 22.00 14.38 16.60 16.64 EV / EBITDA (x) 8.17 9.36 8.16 7.89

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 4.45 4.02 3.24 2.83 Net Debt / Total Capital (%) 48.72 48.11 43.33 38.25

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 6,359 4,539 0 0

CoGS and OpEx 5,461 4,475 643 625 SGA 253 219 235 201 (+) Other EBITDA - - - - DD&A 376 368 360 349 Other 19 0 0 0 Operating Income 250 334 413 350

Interest 302 303 271 234 Equity Income (Loss) 508 545 594 599 Other Income (Loss) 0 0 0 0 Earnings Before Tax 456 577 735 716

Taxes 0 0 0 0 Net Income to LPs / Company 393 514 671 652

Earning Per Share / Unit 1.88 2.46 3.22 3.13 Avg. Diluted Shares / Units Outstanding 209 208 208 208

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income (302) 577 735 716 DD&A 376 368 360 349 Others 1,401 295 462 481 Cash Flow from Operations 1,099 872 1,197 1,197

Acquisitions 2 0 0 0 Total Capex (267) (127) (129) (117) Expansion Capex (222) (60) (60) (50) Maintenance Capex (45) (67) (69) (67) Others 6 0 0 0 Cash Flow from Investments (259) (127) (129) (117)

Equity Issuance (Repurchase) 0 0 0 0 Debt Issued (306) (120) (739) (670) Dividends / Distributions Paid (470) (386) (385) (385) Others (9) 0 0 0 Cash Flow from Financing (785) (506) (1,124) (1,055)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 56 85 29 54 Other Current Assets 952 1,516 1,516 1,516 Net PPE 7,993 7,739 7,509 7,277 Other Long-Term Assets 3,956 3,874 3,772 3,639 Total Assets 12,957 13,214 12,825 12,486

Short-Term Debt 505 354 354 354 Other Short Term Liabilities 1,116 1,454 1,454 1,454 Long-Term Debt 5,119 5,152 4,413 3,743 Other Long-Term Liabilities 356 407 407 407 Total Liabilities 7,096 7,367 6,628 5,958

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 778 781 785 789 Total Liabilities and Equity 12,957 13,214 12,825 12,486

Company Background

DCP Midstream is a diversified master limited partnership with natural gas

gathering and processing assets covering the Mid-Con, DJ Basin,

Permian, and East Texas, as well as integrated NGL pipelines and

fractionation.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 35.00) 39.00

Our blue sky price of $39 is based on 3.0% higher EBITDA and a 0.5x

higher EV multiple on our FY22 estimates vs. our base case on stronger

than anticipated commodity prices and improved producer activity.

Our Grey Sky Scenario (US$) (from 21.00) 24.00

Our grey sky price of $24 is based on 5% lower EBITDA and a 1.25x

lower EV multiple on our FY22 estimates vs. our base case on a weaker

commodity environment, and E&P counterparty risk.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$12.47

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 10

MPLX LP Maintain Outperform; Increase TP to $34

MPLX

Target price (12M, US$) 35.00

Outperform

Master Limited Partnerships

Commodity Strength Drives Higher Estimates: We lift our ‘22 EBITDA estimate by

1% on a higher NGL price forecast. On MPLX’s guided sensitivities, our $0.13/gal

increase in ‘22 NGL prices drives a ~$50mm EBITDA increase vs our prior estimates. Our

21e EBITDA estimate falls ~1% despite commodity tailwinds into the back half of the year.

Increased cost estimates in 2H21 drive the reduction – MPLX guided to ~$75mm higher

project expenses in 2H21 relative to 1Q21 levels.

Positioned for Growth in 2022: MPLX remains one of the few midstream operators with

meaningful growth projects slated to come online. We’d point to Whistler (entered service

3Q21), Wink-to-Webster (contracts fully ramp 2022), the Permian NGL JV (4Q21) and

the Preakness and Tornado 2 Permian processing plants (2022 ISDs). In addition to these

projects we expect increased producer activity driven by an improved macro environment to

result in strong Permian volume growth in 2022. We see this translating to a ~13% FCF

yield in 2022.

Maintain Outperform; Increase TP to $35: We reiterate our Outperform rating and

increase our target price to $35 (from $34) on increased EBITDA estimates. Our target

price is based on NPV analysis, implying a 9.8x EBITDA multiple on our FY22 estimate.

Risks: Near-term catalysts include higher commodity prices, refined product recovery, and

share buybacks. Risks to our Outperform rating include lower commodity prices, declining

refined product demand, and adverse sponsor actions.

Previous target price (12M, US$) 34.00

Price (11 Oct 21, US$) 30.31

52-week price range 31.14 - 16.75

Enterprise value (US$ m) 50,331

Adjusted EV -

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 5,211 5,483 5,654 5,729 Prev Adjusted EBITDA (US$ m) - 5,513 5,601 5,712 Distribution/Unit (US$ m) 2.75 2.75 2.75 2.75 Distribution Coverage (x) 1.41 1.54 1.57 1.61 Earnings/Unit - EPU (US$) 2.54 1.05 2.99 3.10 EV / Adj. EBITDA (x) 7.63 9.04 8.75 8.43 Price/DCF to LPs (x) - - - -

DPU (US$) 2.75 Distribution Yield (%) 9.66 Units Outstanding (m) 1,026 GP Take (%) 0.00 Net Debt Current (US$ m) 19,267 Net Debt/EBITDA (x) 3.55

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$17.26

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,294 1,227 1,335 1,355 2021E 1,352 1,374 1,370 1,387 2022E 1,335 1,425 1,457 1,437

13 October 2021

US Midstream and MLPs 11

MPLX LP (MPLX) Analyst: Spiro Dounis Price (11 Oct 2021): US$30.31 Target Price: (from 34.00) 35.00 Rating: Outperform Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 5,211 5,483 5,654 5,729 Prev. Adj. EBITDA - 5,513 5,601 5,712 (-) Maintenance Capex (147) (156) (165) (160) (-) Cash Interest Expense (854) (854) (851) (796) (+/-) Other Adjustments (10) (16) (124) (124) (-) General Partner Take 0 0 0 0 (-) Preferred Dividends 122 124 124 124 Adj. DCF Available to LPs 4,200 4,457 4,514 4,649

DCF Per LP Unit / Common Share 4.00 4.34 4.43 4.56 Distribution Per Unit / Share 2.75 2.75 2.75 2.75 Distribution Coverage (x) 1.41 1.54 1.57 1.61

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,294 1,227 1,335 1,355 2021E 1,352 1,374 1,370 1,387 2022E 1,335 1,425 1,457 1,437

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 13.94 9.66 9.66 9.66 Dividend / Distribution Growth (%, YoY) 2.23 0.00 0.00 0.00 DCF Yield (%) EV / EBITDA (x) 7.63 9.04 8.75 8.43

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 3.85 3.55 3.30 3.04 Net Debt / Total Capital (%) 58.06 58.55 56.68 54.13

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 5,560 5,753 5,940 6,041

CoGS and OpEx 0 1,862 0 0 SGA 363 339 382 386 (+) Other EBITDA 134 202 231 210 DD&A 1,377 1,318 1,354 1,394 Other 121 132 136 136 Operating Income 3,699 2,101 4,068 4,125

Interest 867 854 851 796 Equity Income (Loss) - - - - Other Income (Loss) (1) 0 0 0 Earnings Before Tax 2,831 1,247 3,217 3,329

Taxes 2 3 5 5 Net Income to LPs / Company 2,674 1,083 3,048 3,157

Earning Per Share / Unit 2.54 1.05 2.99 3.10 Avg. Diluted Shares / Units Outstanding 1,051 1,028 1,020 1,020

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income 1,478 2,995 3,213 3,324 DD&A 1,377 1,318 1,354 1,394 Others 3,043 1,667 1,586 1,604 Cash Flow from Operations 4,521 2,800 4,798 4,928

Acquisitions 56 74 0 0 Total Capex (1,326) (841) (821) (682) Expansion Capex (1,179) (685) (656) (522) Maintenance Capex (147) (156) (165) (160) Others 8 0 0 0 Cash Flow from Investments (1,262) (767) (821) (682)

Equity Issuance (Repurchase) (33) (509) 0 0 Debt Issued (198) (401) (1,030) (1,281) Dividends / Distributions Paid (3,006) (2,974) (2,929) (2,929) Others (22) 15 0 0 Cash Flow from Financing (3,259) (3,869) (3,959) (4,210)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 15 41 59 96 Other Current Assets 1,500 1,469 1,469 1,469 Net PPE 21,218 20,203 19,670 18,957 Other Long-Term Assets 13,681 13,973 13,742 13,532 Total Assets 36,414 35,687 34,940 34,055

Short-Term Debt 0 0 0 0 Other Short Term Liabilities 2,086 1,727 1,727 1,727 Long-Term Debt 19,375 19,286 18,256 16,975 Other Long-Term Liabilities 968 1,049 1,049 1,049 Total Liabilities 22,429 22,062 21,032 19,751

GP Equity 0 0 0 0 LP Equity 12,161 11,803 12,086 12,481 Non-Controlling Interests & Other 1,824 1,822 1,822 1,822 Total Liabilities and Equity 36,414 35,687 34,940 34,055

Company Background

MPLX is a sponsored master limited partnership under Marathon

Petroleum, a US independent refiner. MPLX owns gathering, processing,

and fractionation assets across the Northeast and Southwest, as well as

pipelines and terminals serving MPC.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 39.00) 40.00

Our blue sky price of $40 is based on 4.0% higher EBITDA and a 0.50x

higher EV multiple on our FY22 estimates vs. our base case, assuming

stronger than anticipated ethane prices and increased producer activity.

Our Grey Sky Scenario (US$) 19.00

Our grey sky price of $19 is based on 5.0% lower EBITDA and a 2.5x

lower EV multiple on our FY22 estimates vs. our base case on

persistently lower gas and NGL prices.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$17.26

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 12

New Fortress Energy Reiterate Outperform; Raise TP to $38

NFE

Target price (12M, US$) 38.00

Outperform[V]

Infrastructure

Lifting TP to $38 from $34: We lift our TP to $38 from $34 to reflect higher ’21 and ’22

revenues from selling LNG cargoes in the tight international market (+$2/share). The

stronger cash position and alleviation of capex financing pressure also drives +$2/share.

Net Long LNG Position Strengthens Cash Flows: NFE addressed a central near-term

investor concern: potentially being short LNG in a record high price environment. Through a

combination of actions, NFE is now net long LNG in 2021 and 2022, generating a cash

windfall (+$300mm) into next year. While the cash flows are non-recurring, NFE was able

to de-risk the near-term while also providing funding for its $1.6bln growth capital backlog.

Fast LNG Still The Long-Term Solution: Fast LNG remains NFE’s primary solution to

address its short LNG position starting in 2023. Management expects to finalize a

commercial agreement with an upstream counterparty before year-end and reiterated YE22

in-service timing. We believe the market continues to heavily discount this supply option

and its viability given perceived complications in securing a fixed price supply structure. That

said, we see a term LNG deal as an ongoing viable back up option that largely preserves

NFE’s margin and returns.

Adjusting Estimates: We raise our ’21 EBITDA by 52% to reflect NFE’s updated outlook.

Our ’22 EBITDA increases 12% to reflect NFE’s net long cargo position and +$100mm

outlook revision.

Risks: Downside risks include slow commercial progress, equity raises, demand

destruction and large secondary offerings from GLNG/Stonepeak.

Valuation: We reiterate Outperform and lift our TP to $38 from $34 based on our NPV

methodology. Our NPV imputes a 3% long term growth rate, 1% terminal growth rate, a

3x return multiple long term, and a 10% discount rate.

Previous target price (12M, US$) 34.00

Price (11 Oct 21, US$) 33.01

52-week price range 59.18 - 24.60

Enterprise value (US$ m) 9,666

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 10 594 900 1,200 Prev Adjusted EBITDA (US$ m) - 392 803 1,166 Distribution/Unit (US$ m) 0.20 0.40 0.40 0.48 Distribution Coverage (x) - - - - Earnings/Unit - EPU (US$) -0.55 1.07 1.91 3.36 EV / Adj. EBITDA (x) 9,92.83 16.65 11.55 8.15 Price/DCF to LPs (x) .00 .00 .00 .00

Dividend (current, US$) .4 Dividend yield (%) 1.2 Net debt (current, US$) 3,401.0 Net debt/tot eq (Next Qtr., %) 167.6 BV/share (Next Qtr., US$) 8.7 GIC (12/21E, US$ m) 5,051.4 EV qtr/GIC (x) 2.8 Current WACC (%) - Free float (%) 372.5 Number of shares (m) 206.7

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$46.22

Adj. EBITDA Q1 Q2 Q3 Q4 2020A -24 -16 20 29 2021E 10 87 165 332 2022E 257 161 213 269

13 October 2021

US Midstream and MLPs 13

New Fortress Energy (NFE) Analyst: Spiro Dounis Price (11 Oct 2021): US$33.01 Target Price: (from 34.00) 38.00 Rating: Outperform [V] Earnings 12/20A 12/21E 12/22E 12/23E

EBITDAX margin (%) 2.2 41.3 31.7 32.6 EBIT Margin (%) (5.8) 21.5 19.4 22.4 Net Income Margin (%) (7.2) 15.7 13.9 18.9 Tax Burden (%) (5.0) 1.4 0.0 0.0

Adj. EBITDA Q1 Q2 Q3 Q4 2020A -24 -16 20 29 2021E 10 87 165 332 2022E 257 161 213 269

Valuation 12/20A 12/21E 12/22E 12/23E

Dividend yield (%) 0.6 1.2 1.2 1.5 FCF yield (%) (8.9) (10.8) (4.7) 11.0 EV/EBITDAX (x) 372.9 16.5 11.2 7.9

Gearing 12/20A 12/21E 12/22E 12/23E

Net debt/equity (%) 162.7 128.8 130.8 86.1 Interest coverage ratio (X) (0.4) 1.9 2.1 3.3

Income Statement 12/20A 12/21E 12/22E 12/23E

EBITDAX (US$ m) 10 594 900 1,200

EBITDA (US$ m) 10 594 900 1,200 EBIT (m) (26) 308 551 824

Net interest income (exp) 66 165 264 250 Net non operating inc (exp) (5) (0) 0 0 Share of associates/JVs' equity - 104 128 143 Exceptionals (5) (0) 0 0 Profit before tax (US$ m) (97) 248 414 717

Taxes 5 4 0 0 Profit after tax (102) 244 414 717 Extraordinary gain/(loss) 0 0 0 0 Non-controlling interest (minority) (69) 19 19 22 Preferred dividends - - - - EBIDAX (US$ m) 5 590 900 1,200 Adjusted net income (US$ m) (32) 225 395 695

Cash Flow 12/20A 12/21E 12/22E 12/23E

DD&A 32 92 110 124 Change in working capital 23 (71) 0 0 Other cash and non-cash items (122) (39) (58) (14) Cash flow from operations (126) 198 493 810 Capex (157) (944) (817) (60) Exploration expense - - - - Free cashflow to the firm (283) (746) (324) 750 Acquisitions - - - - Divestments 0 (675) 0 0 Other investment/(outflows) Cashflow from investment (158) (1,620) (817) (60) Operating cash flow (125.6) 198.2 493.0 810.2

Depreciation & Amortization 32.4 92.2 109.5 124.4

Balance Sheet 12/20A 12/21E 12/22E 12/23E

Cash and cash equivalents 629 1,118 695 762 Other current assets 148 275 275 275 Total current assets 777 1,393 970 1,038

Total fixed assets 990 2,465 3,172 3,108 Other assets 141 3,174 3,211 3,248 Total assets 1,908 7,032 7,353 7,394

Total current liabilities 191 635 635 635 Long-term debt 1,240 3,756 3,771 3,221 Other Liabilities 102 432 438 445

Total liabilities 1,533 4,823 4,845 4,301

Shareholders' equity 367 1,969 2,269 2,853 Minority interest 8 240 240 240 Total equity and liabilities 1,908 7,032 7,353 7,394

Company Background

New Fortress Energy is a global energy infrastructure company that

funds, builds and operates liquefied natural gas infrastructure and

logistics.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 45.00) 50.00

$50 Blue Sky: Our blue sky scenario assumes NFE reaches its 18mm

gpd volume run-rate, which includes the Ireland project and 1 FLNG rig.

Our Grey Sky Scenario (US$) (from 17.00) 19.00

$19 Grey Sky: Our Grey Sky scenario assumes only current committed

volumes (<5mm gpd) and 1 FLNG rig and excludes Sri Lanka and Ireland

projects.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$46.22

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 14

ONEOK Inc Maintain Neutral; Increase TP to $62

OKE

Target price (12M, US$) 62.00

Neutral

Master Limited Partnerships

Lifting Estimates on Strong Volume and Margin Trends: We see an opportunity for

OKE to achieve >$3.6bln of EBITDA in ‘22 amid an improved commodity and macro

environment. OKE messaged toward the high-end of the $3.05-$3.35bln ‘21 EBITDA

guidance range, which we view as an achievable hurdle. We expect the strong macro

backdrop to provide momentum into ‘22 due to a number of factors. First, we expect the

start-up of the Bear Creek II processing plant and several third party plants to continue to

drive a mix shift toward the Rockies, supporting strong G&P margins. Second, these plant

additions should feed additional NGL volumes onto the Elk Creek. Third, ethane recovery

likely remains a tailwind; ethane alone could provide a $500mm opportunity if the system

were to move into full recovery. Finally, an improving gas-oil-ratio should continue to

contribute outsized volume growth in the Rockies. Over a 7-year period, OKE highlight as

much as 1.3bcfd of incremental gathering volumes and +150kbpd of C3+ in a flat crude oil

environment.

Maintain Neutral; Increase TP to $62: We maintain Neutral but increase our TP to $62

(from $56); strong volume trends, GoRs, ethane recovery, and a higher price environment

drive the stronger outlook. Our TP is NPV-derived, implying a multiple of 11.1x FY22

EBITDA, which is in the first quartile among peers- hence our Neutral rating. We continue

to expect OKE to surpass the high-end of 2021 guidance.

Risks: Downside risks include declining commodity prices, weaker ethane recovery

economics, and subdued Bakken activity. Upside risks include supportive NGL prices and

increased producer activity in the Bakken.

Previous target price (12M, US$) 56.00

Price (11 Oct 21, US$) 61.90

52-week price range 61.90 - 26.89

Enterprise value (US$ m) 40,911

Adjusted EV -

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 2,724 3,388 3,628 3,697 Prev Adjusted EBITDA (US$ m) - 3,365 3,550 3,570 Distribution/Unit (US$ m) 3.74 3.74 3.74 3.74 Distribution Coverage (x) 1.16 1.48 1.66 1.73 Earnings/Unit - EPU (US$) 2.87 3.47 4.03 4.27 EV / Adj. EBITDA (x) 10.53 11.93 10.94 10.49 Price/DCF to LPs (x) - - - -

DPU (US$) 3.74 Distribution Yield (%) 6.16 Units Outstanding (m) 446 GP Take (%) - Net Debt Current (US$ m) 13,602 Net Debt/EBITDA (x) 3.93

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$29.17

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 701 534 747 742 2021E 866 801 845 875 2022E 868 904 928 928

13 October 2021

US Midstream and MLPs 15

ONEOK Inc (OKE) Analyst: Spiro Dounis Price (11 Oct 2021): US$61.9 Target Price: (from 56.00) 62.00 Rating: Neutral Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 2,724 3,388 3,628 3,697 Prev. Adj. EBITDA - 3,365 3,550 3,570 (-) Maintenance Capex (137) (189) (188) (187) (-) Cash Interest Expense - - - - (+/-) Other Adjustments - - - - (-) General Partner Take - - - - (-) Preferred Dividends - - - - Adj. DCF Available to LPs 1,881 2,476 2,753 2,827

DCF Per LP Unit / Common Share 4.35 5.55 6.22 6.48 Distribution Per Unit / Share 3.74 3.74 3.74 3.74 Distribution Coverage (x) 1.16 1.48 1.66 1.73

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 701 534 747 742 2021E 866 801 845 875 2022E 868 904 928 928

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 11.12 6.16 6.16 6.16 Dividend / Distribution Growth (%, YoY) 5.95 0.00 0.00 0.00 DCF Yield (%) 12.95 9.14 10.24 10.67 EV / EBITDA (x) 10.53 11.93 10.94 10.49

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 5.03 3.93 3.58 3.38 Net Debt / Total Capital (%) 69.41 69.40 69.85 69.63

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 3,432 4,249 4,542 4,638

CoGS and OpEx 0 0 0 0 SGA - - - - (+) Other EBITDA - - - - DD&A 579 633 635 632 Other 876 973 1,034 1,060 Operating Income 1,977 2,644 2,872 2,946

Interest 713 735 674 640 Equity Income (Loss) 143 125 132 131 Other Income (Loss) 25 (14) (12) (12) Earnings Before Tax 1,432 2,021 2,319 2,425

Taxes 190 471 533 558 Net Income to LPs / Company 1,242 1,549 1,785 1,866

Earning Per Share / Unit 2.87 3.47 4.03 4.27 Avg. Diluted Shares / Units Outstanding 432 447 443 437

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income - - - - DD&A 579 633 635 632 Others - - - - Cash Flow from Operations 1,899 2,676 2,952 3,025

Acquisitions 0 0 0 0 Total Capex (2,195) (614) (558) (488) Expansion Capex (2,058) (425) (370) (301) Maintenance Capex (137) (189) (188) (187) Others (75) (0) 0 0 Cash Flow from Investments (2,271) (614) (558) (488)

Equity Issuance (Repurchase) 970 16 (400) (400) Debt Issued 1,568 (358) (575) (800) Dividends / Distributions Paid (1,605) (1,667) (1,655) (1,630) Others (57) (18) 0 0 Cash Flow from Financing 875 (2,027) (2,630) (2,830)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 524 560 323 30 Other Current Assets 1,345 1,631 1,631 1,631 Net PPE 19,155 19,152 19,075 18,931 Other Long-Term Assets 2,054 2,009 1,985 1,961 Total Assets 23,079 23,352 23,014 22,553

Short-Term Debt 8 536 536 536 Other Short Term Liabilities 1,337 1,858 1,858 1,858 Long-Term Debt 14,228 13,348 12,773 11,973 Other Long-Term Liabilities 1,463 1,733 2,240 2,742 Total Liabilities 17,036 17,476 17,408 17,110

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 0 0 0 0 Total Liabilities and Equity - - - -

Company Background

ONEOK is a diversified midstream C-corp with gathering, processing,

fractionation, and pipeline assets covering the Bakken, Mid-Con,

Permian, and Gulf Coast.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 66.00) 73.00

Our blue sky price of $73 is based on 3% higher EBITDA and a 1.0x

higher EV multiple on our FY22 estimates vs. our base case, which would

be driven by a higher than expected utilization, faster ramp on projects

and a better than expected ethane recovery.

Our Grey Sky Scenario (US$) (from 35.00) 41.00

Our grey sky price of $41 is based on 5% lower EBITDA and a 2.0x

lower EV multiple on our FY22 estimates vs. our base case driven by

delays in projects, lower than expected utilization and increased ethane

rejection.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$29.17

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 16

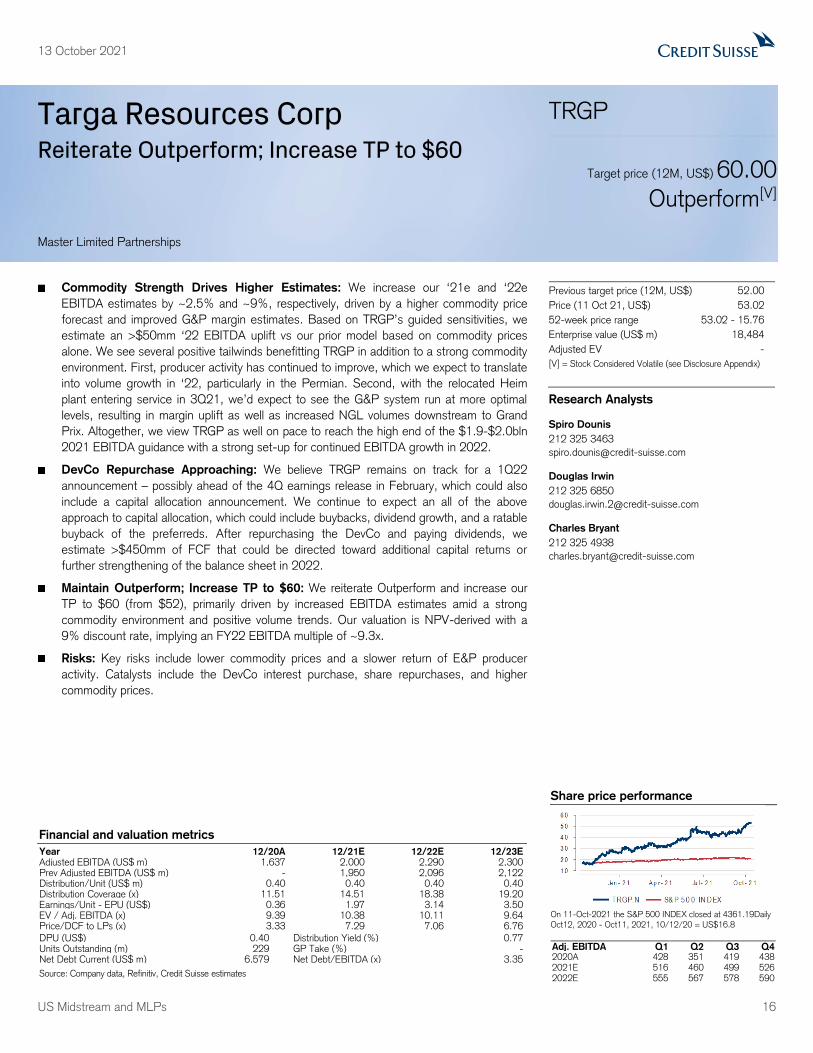

Targa Resources Corp Reiterate Outperform; Increase TP to $60

TRGP

Target price (12M, US$) 60.00

Outperform[V]

Master Limited Partnerships

Commodity Strength Drives Higher Estimates: We increase our ‘21e and ‘22e

EBITDA estimates by ~2.5% and ~9%, respectively, driven by a higher commodity price

forecast and improved G&P margin estimates. Based on TRGP’s guided sensitivities, we

estimate an >$50mm ‘22 EBITDA uplift vs our prior model based on commodity prices

alone. We see several positive tailwinds benefitting TRGP in addition to a strong commodity

environment. First, producer activity has continued to improve, which we expect to translate

into volume growth in ‘22, particularly in the Permian. Second, with the relocated Heim

plant entering service in 3Q21, we’d expect to see the G&P system run at more optimal

levels, resulting in margin uplift as well as increased NGL volumes downstream to Grand

Prix. Altogether, we view TRGP as well on pace to reach the high end of the $1.9-$2.0bln

2021 EBITDA guidance with a strong set-up for continued EBITDA growth in 2022.

DevCo Repurchase Approaching: We believe TRGP remains on track for a 1Q22

announcement – possibly ahead of the 4Q earnings release in February, which could also

include a capital allocation announcement. We continue to expect an all of the above

approach to capital allocation, which could include buybacks, dividend growth, and a ratable

buyback of the preferreds. After repurchasing the DevCo and paying dividends, we

estimate >$450mm of FCF that could be directed toward additional capital returns or

further strengthening of the balance sheet in 2022.

Maintain Outperform; Increase TP to $60: We reiterate Outperform and increase our

TP to $60 (from $52), primarily driven by increased EBITDA estimates amid a strong

commodity environment and positive volume trends. Our valuation is NPV-derived with a

9% discount rate, implying an FY22 EBITDA multiple of ~9.3x.

Risks: Key risks include lower commodity prices and a slower return of E&P producer

activity. Catalysts include the DevCo interest purchase, share repurchases, and higher

commodity prices.

Previous target price (12M, US$) 52.00

Price (11 Oct 21, US$) 53.02

52-week price range 53.02 - 15.76

Enterprise value (US$ m) 18,484

Adjusted EV -

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 1,637 2,000 2,290 2,300 Prev Adjusted EBITDA (US$ m) - 1,950 2,096 2,122 Distribution/Unit (US$ m) 0.40 0.40 0.40 0.40 Distribution Coverage (x) 11.51 14.51 18.38 19.20 Earnings/Unit - EPU (US$) 0.36 1.97 3.14 3.50 EV / Adj. EBITDA (x) 9.39 10.38 10.11 9.64 Price/DCF to LPs (x) 3.33 7.29 7.06 6.76

DPU (US$) 0.40 Distribution Yield (%) 0.77 Units Outstanding (m) 229 GP Take (%) - Net Debt Current (US$ m) 6,579 Net Debt/EBITDA (x) 3.35

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$16.8

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 428 351 419 438 2021E 516 460 499 526 2022E 555 567 578 590

13 October 2021

US Midstream and MLPs 17

Targa Resources Corp (TRGP) Analyst: Spiro Dounis Price (11 Oct 2021): US$53.02 Target Price: (from 52.00) 60.00 Rating: Outperform [V] Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 1,637 2,000 2,290 2,300 Prev. Adj. EBITDA - 1,950 2,096 2,122 (-) Maintenance Capex (123) (120) (124) (122) (-) Cash Interest Expense 389 384 365 292 (+/-) Other Adjustments - - - - (-) General Partner Take - - - - (-) Preferred Dividends - - - - Adj. DCF Available to LPs 1,073 1,405 1,709 1,795

DCF Per LP Unit / Common Share 4.60 5.80 7.35 7.68 Distribution Per Unit / Share .40 .40 .40 .40 Distribution Coverage (x) 11.51 14.51 18.38 19.20

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 428 351 419 438 2021E 516 460 499 526 2022E 555 567 578 590

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 1.88 0.77 0.77 0.77 Dividend / Distribution Growth (%, YoY) (89.01) 0.00 0.00 0.00 DCF Yield (%) 21.63 11.19 14.17 14.80 EV / EBITDA (x) 9.39 10.38 10.11 9.64

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 4.64 3.35 2.86 2.27 Net Debt / Total Capital (%) 54.77 49.78 46.03 37.12

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 2,857 3,270 3,521 3,527

CoGS and OpEx 6,107 6,222 836 854 SGA 255 253 286 285 (+) Other EBITDA - - - - DD&A 865 849 874 859 Other 0 0 0 0 Operating Income 1,032 1,421 1,525 1,551

Interest 391 381 362 289 Equity Income (Loss) 73 50 51 51 Other Income (Loss) 3 (1) 0 0 Earnings Before Tax 716 1,090 1,214 1,312

Taxes 47 75 109 118 Net Income to LPs / Company 85 477 731 818

Earning Per Share / Unit 0.36 1.97 3.14 3.50 Avg. Diluted Shares / Units Outstanding 233 242 233 234

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income (1,325) 926 1,104 1,194 DD&A 865 849 874 859 Others 3,070 1,376 939 925 Cash Flow from Operations 1,745 2,301 2,044 2,120

Acquisitions 199 2 (925) 0 Total Capex (952) (520) (474) (350) Expansion Capex (829) (400) (350) (228) Maintenance Capex (123) (120) (124) (122) Others 15 12 0 0 Cash Flow from Investments (738) (506) (1,399) (350)

Equity Issuance (Repurchase) (97) (9) 0 0 Debt Issued (23) (867) (750) (1,356) Dividends / Distributions Paid (396) (185) (185) (185) Others (578) (443) (192) (192) Cash Flow from Financing (1,095) (1,504) (1,126) (1,733)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 243 535 53 90 Other Current Assets 1,218 1,109 1,109 1,109 Net PPE 12,174 11,896 12,421 11,911 Other Long-Term Assets 2,242 2,063 1,998 1,932 Total Assets 15,876 15,602 15,580 15,041

Short-Term Debt 369 372 372 372 Other Short Term Liabilities 1,411 1,730 1,730 1,730 Long-Term Debt 7,387 6,524 5,774 4,418 Other Long-Term Liabilities 505 560 560 560 Total Liabilities 9,671 9,185 8,435 7,080

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 3,551 4,205 4,490 4,777 Total Liabilities and Equity 15,876 15,602 15,580 15,041

Company Background

Targa Resources is a midstream C-corp that owns and operates an

integrated asset base from gathering and processing assets across the

Permian, Mid-Con, Bakken, and Eagle Ford to NGL fractionation and

export assets on the Gulf Coast.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 61.00) 70.00

Our blue sky price of $70 is based on 5.0% higher EBITDA and a 0.50x

higher EV multiple on our FY22 estimates vs. our base case on a

stronger commodity environment and increased Permian production.

Our Grey Sky Scenario (US$) (from 31.00) 37.00

Our grey sky price of $37 is based on 10% lower EBITDA and a 1.5x

lower EV multiple on our FY22 estimates vs. our base case on steeper

legacy asset declines and weaker commodity environment.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$16.8

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 18

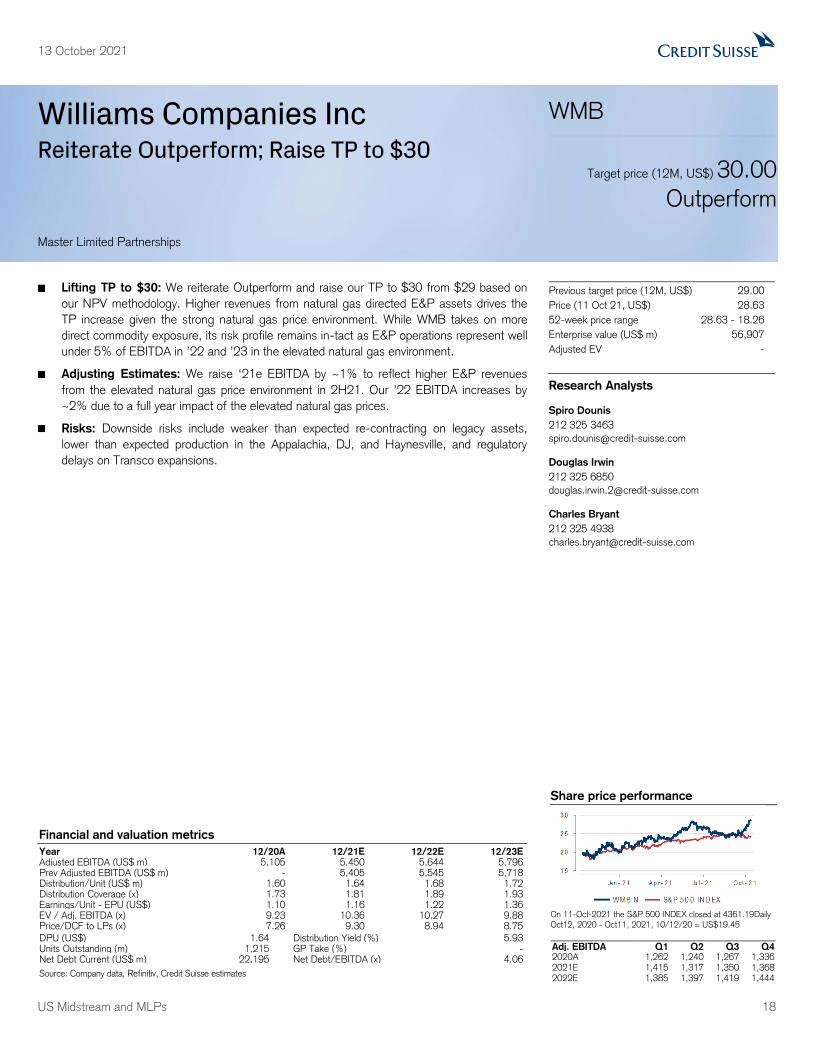

Williams Companies Inc Reiterate Outperform; Raise TP to $30

WMB

Target price (12M, US$) 30.00

Outperform

Master Limited Partnerships

Lifting TP to $30: We reiterate Outperform and raise our TP to $30 from $29 based on

our NPV methodology. Higher revenues from natural gas directed E&P assets drives the

TP increase given the strong natural gas price environment. While WMB takes on more

direct commodity exposure, its risk profile remains in-tact as E&P operations represent well

under 5% of EBITDA in ’22 and ’23 in the elevated natural gas environment.

Adjusting Estimates: We raise ‘21e EBITDA by ~1% to reflect higher E&P revenues

from the elevated natural gas price environment in 2H21. Our ’22 EBITDA increases by

~2% due to a full year impact of the elevated natural gas prices.

Risks: Downside risks include weaker than expected re-contracting on legacy assets,

lower than expected production in the Appalachia, DJ, and Haynesville, and regulatory

delays on Transco expansions.

Previous target price (12M, US$) 29.00

Price (11 Oct 21, US$) 28.63

52-week price range 28.63 - 18.26

Enterprise value (US$ m) 56,907

Adjusted EV -

Research Analysts

Spiro Dounis

212 325 3463

Douglas Irwin

212 325 6850

Charles Bryant

212 325 4938

Financial and valuation metrics

Year 12/20A 12/21E 12/22E 12/23E Adjusted EBITDA (US$ m) 5,105 5,450 5,644 5,796 Prev Adjusted EBITDA (US$ m) - 5,405 5,545 5,718 Distribution/Unit (US$ m) 1.60 1.64 1.68 1.72 Distribution Coverage (x) 1.73 1.81 1.89 1.93 Earnings/Unit - EPU (US$) 1.10 1.16 1.22 1.36 EV / Adj. EBITDA (x) 9.23 10.36 10.27 9.88 Price/DCF to LPs (x) 7.26 9.30 8.94 8.75

DPU (US$) 1.64 Distribution Yield (%) 5.93 Units Outstanding (m) 1,215 GP Take (%) - Net Debt Current (US$ m) 22,195 Net Debt/EBITDA (x) 4.06

Source: Company data, Refinitiv, Credit Suisse estimates

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$19.45

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,262 1,240 1,267 1,336 2021E 1,415 1,317 1,350 1,368 2022E 1,385 1,397 1,419 1,444

13 October 2021

US Midstream and MLPs 19

Williams Companies Inc (WMB) Analyst: Spiro Dounis Price (11 Oct 2021): US$28.63 Target Price: (from 29.00) 30.00 Rating: Outperform Distributable Cash Flow (DCF) 12/20A 12/21E 12/22E 12/23E

Adjusted EBITDA 5,105 5,450 5,644 5,796 Prev. Adj. EBITDA - 5,405 5,545 5,718 (-) Maintenance Capex (393) (428) (434) (437) (-) Cash Interest Expense - - - - (+/-) Other Adjustments - - - - (-) General Partner Take - - - - (-) Preferred Dividends - - - - Adj. DCF Available to LPs 3,356 3,620 3,857 4,035

DCF Per LP Unit / Common Share 2.76 2.97 3.17 3.31 Distribution Per Unit / Share 1.60 1.64 1.68 1.72 Distribution Coverage (x) 1.73 1.81 1.89 1.93

Adj. EBITDA Q1 Q2 Q3 Q4 2020A 1,262 1,240 1,267 1,336 2021E 1,415 1,317 1,350 1,368 2022E 1,385 1,397 1,419 1,444

Key Valuation Metrics 12/20A 12/21E 12/22E 12/23E

Dividend / Distribution Yield (%) 7.98 5.93 5.93 5.93 Dividend / Distribution Growth (%, YoY) 5.26 2.50 2.44 2.38 DCF Yield (%) 13.77 10.76 11.19 11.43 EV / EBITDA (x) 9.23 10.36 10.27 9.88

Leverage Ratios 12/20A 12/21E 12/22E 12/23E

Net Debt / EBITDA (x) 4.33 4.06 3.86 3.66 Net Debt / Total Capital (%) 60.36 60.96 60.46 59.44

Income Statement 12/20A 12/21E 12/22E 12/23E

Revenue (US$ m) 7,719 9,576 9,144 8,963

CoGS and OpEx 1,613 3,284 2,922 2,615 SGA 497 445 415 424 (+) Other EBITDA - - - - DD&A 1,721 1,827 1,840 1,822 Other 1,311 1,405 1,328 1,358 Operating Income 2,577 2,616 2,687 2,891

Interest 1,172 1,178 1,130 1,101 Equity Income (Loss) - - - - Other Income (Loss) (5) 0 0 0 Earnings Before Tax 1,848 1,979 2,122 2,355

Taxes 454 500 548 608 Net Income to LPs / Company 1,342 1,416 1,491 1,655

Earning Per Share / Unit 1.10 1.16 1.22 1.36 Avg. Diluted Shares / Units Outstanding 1,215 1,217 1,217 1,217

Cash Flow 12/20A 12/21E 12/22E 12/23E

Net Income - - - - DD&A 1,721 1,827 1,840 1,822 Others - - - - Cash Flow from Operations 3,496 4,023 4,215 4,404

Acquisitions (361) (182) 0 0 Total Capex (1,239) (1,603) (1,508) (1,449) Expansion Capex (846) (1,175) (1,074) (1,012) Maintenance Capex (393) (428) (434) (437) Others 42 33 0 0 Cash Flow from Investments (1,558) (1,752) (1,508) (1,449)

Equity Issuance (Repurchase) 9 3 0 0 Debt Issued 58 (51) (584) (652) Dividends / Distributions Paid (1,941) (1,994) (2,045) (2,094) Others (211) (198) (191) (191) Cash Flow from Financing (2,085) (2,240) (2,821) (2,937)

Balance Sheet (US$) 12/20A 12/21E 12/22E 12/23E

Cash & Cash Equivalents 142 173 59 77 Other Current Assets 1,287 1,358 1,358 1,358 Net PPE 28,929 29,425 29,093 28,719 Other Long-Term Assets 13,807 13,514 13,373 13,232 Total Assets 44,165 44,469 43,882 43,386

Short-Term Debt 893 2,143 2,143 2,143 Other Short Term Liabilities 1,426 1,616 1,616 1,616 Long-Term Debt 21,451 20,153 19,569 18,917 Other Long-Term Liabilities 5,812 6,392 6,392 6,392 Total Liabilities 29,582 30,304 29,720 29,068

GP Equity - - - - LP Equity - - - - Non-Controlling Interests & Other 2,814 2,662 2,471 2,280 Total Liabilities and Equity - - - -

Company Background

WMB is a midstream c-corp with one reportable segment, Williams

Partners, which owns gathering, processing, and transmission assets

across the Eastern US, Gulf Coast, and Rockies.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) (from 34.00) 35.00

Our blue sky price of $35 is based on 5.0% higher EBITDA and a 0.5x

higher EV multiple on our FY22 estimates vs. our base case on higher

than expected utilization on Transco and additional projects receiving FID.

Our Grey Sky Scenario (US$) 23.00

Our grey sky price of $23 is based on 4.0% lower EBITDA and a 1.0x

lower EV multiple on our FY22 estimates vs. our base case driven by

legacy asset declines and delays in projects.

Share price performance

On 11-Oct-2021 the S&P 500 INDEX closed at 4361.19

Daily Oct12, 2020 - Oct11, 2021, 10/12/20 = US$19.45

Source: FTI, Company data, Refinitiv, Credit Suisse Securities (EUROPE) LTD. Estimates

13 October 2021

US Midstream and MLPs 20

Valuation Methodology and Risks

Target Price and Rating Valuation Methodology and Risks: (12 months) for Altus Midstream Company (ALTM.OQ)

Method: Our $45 TP is based on a dividend discount methodology, discounted back at 12%. Our Underperform rating is due to our expectations that ALTM will perform worse than peers.

Risk: Upside risks to our $45 TP and Underperform rating include better Alpine High execution at APA and higher earnings from the JV pipes.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Cheniere Energy (LNG.A)

Method: Our Outperform rating and $116 target price for LNG are based on NPV analysis, implying a 10.65x EV/EBITDA multiple on our FY22 EBITDA estimate. We rate LNG Outperform as we expect it to appreciate more than its peers.

Risk: Downside risks to our Outperform rating and $116 target price for LNG are execution, global LNG oversupply, lower global LNG prices, higher US HH natural gas prices.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Cheniere Energy Partners LP (CQP.A)

Method: Our Underperform rating and $39 target price for CQP are based on a 12.2x EV/EBITDA multiple on our FY22 EBITDA estimates. We rate CQP Underperform as we expect its total return to be below its peers.

Risk: Risks to our Underperform rating and $39 TP include: upside - better SPL-CMI SPA terms, a high-multiple buyout by LNG; downside - lower global LNG (liquefied natural gas) demand and prices, higher US HH (Henry Hub) natural gas prices, and a low-multiple buyout by LNG.

Target Price and Rating Valuation Methodology and Risks: (12 months) for DCP Midstream LP (DCP.N)

Method: Our Neutral rating and target price of $34 is NPV based, implying an 8.5x EV multiple on our FY22 EBITDA.

Risk: Risks to our $34 PT and Neutral rating include: Downside risks include lower NGL prices / demand, lower DJ production, ENB divestiture, and long-term Colorado legislation risk. The key upside risk is a stronger than expected recovery in commodity prices.

Target Price and Rating Valuation Methodology and Risks: (12 months) for MPLX LP (MPLX.N)

Method: Our Outperform rating and $35 target price for MPLX are based on 9.8x our FY22 EBITDA estimate. We rate MPLX Outperform as we expect its total return to exceed its peers.

Risk: Risks to our Outperform rating and $35 target price for MPLX include macro headwinds and potentially dilutive actions from the sponsor.

Target Price and Rating Valuation Methodology and Risks: (12 months) for New Fortress Energy (NFE.OQ)

Method: Our Outperform Rating and $38 TP is based on an NPV methodology. Our TP is based on ~10% discount rate and a return multiple of 3.0x long term.

Risk: Downside risks to our Outperform Rating and $38 TP include project delays, demand destruction, and slower commercial success.

Target Price and Rating Valuation Methodology and Risks: (12 months) for ONEOK Inc (OKE.N)

Method: Our Neutral rating and target price of $62 are based on an NPV analysis, implying a 11.1x EV multiple on our FY22 EBITDA estimate.

Risk: Risks to our $62 PT and Neutral rating include: Downside - lower NGL prices/demand and increased ethane rejection. Upside - a faster than anticipated return to growth in the Bakken.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Targa Resources Corp (TRGP.N)

Method: We rate TRGP Outperform. Our $60 TP is based on an NPV analysis and implies a 9.3x EV multiple on our FY22 EBITDA estimate.

13 October 2021

US Midstream and MLPs 21

Risk: Risks to our $60 TP and Outperform rating include slower than expected Permian growth, greater than expected funding needs, lower NGL prices / demand, growing competition from private equity.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Williams Companies Inc (WMB.N)

Method: Our Outperform rating and target price of $30 are based on our NPV methodology. Our NPV imputes a 9% discount rate.

Risk: Risks to our $30 TP and Outperform rating include: weaker-than-expected re-contracting on legacy assets, lower-than-expected production in the Appalachia and DJ, regulatory delays on Transco expansions, and expensive M&A.

13 October 2021

US Midstream and MLPs 22

Companies Mentioned (Price as of 12-Oct-2021) Altus Midstream Company (ALTM.OQ, $84.2, UNDERPERFORM[V], TP $45.0) Cheniere Energy (LNG.A, $102.52, OUTPERFORM, TP $116.0) Cheniere Energy Partners LP (CQP.A, $41.99, UNDERPERFORM, TP $39.0) DCP Midstream LP (DCP.N, $31.48, NEUTRAL[V], TP $34.0) MPLX LP (MPLX.N, $30.13, OUTPERFORM, TP $35.0) New Fortress Energy (NFE.OQ, $33.67, OUTPERFORM[V], TP $38.0) ONEOK Inc (OKE.N, $62.95, NEUTRAL, TP $62.0) Targa Resources Corp (TRGP.N, $53.77, OUTPERFORM[V], TP $60.0) Williams Companies Inc (WMB.N, $28.93, OUTPERFORM, TP $30.0)

Disclosure Appendix

Analyst Certification

I, Spiro Dounis, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Altus Midstream Company (ALTM.OQ)

ALTM.OQ Closing Price Target Price

Date (US$) (US$) Rating

04-Jan-19 162.20 220.00 O *

28-Feb-19 122.40 180.00

17-Apr-19 108.40 160.00

19-Aug-19 51.60 80.00

16-Oct-19 45.80 70.00

31-Oct-19 44.00 50.00 N

11-Mar-20 20.40 30.00

01-Apr-20 13.35 10.00 U

11-Dec-20 45.99 45.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

U N D ERPERFO RM

3-Year Price and Rating History for Cheniere Energy (LNG.A)

LNG.A Closing Price Target Price

Date (US$) (US$) Rating

12-Nov-18 61.69 89.00 O

18-Dec-18 58.43 85.00

15-Jan-19 64.89 84.00

29-May-19 63.95 81.00

09-Sep-19 62.45 R

11-Sep-19 63.71 81.00 O

25-Nov-19 61.35 79.00

11-Mar-20 39.34 58.00

19-Nov-20 55.27 69.00

08-Mar-21 73.20 86.00

07-May-21 82.65 103.00

20-Jul-21 83.60 105.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

REST RICT ED

13 October 2021

US Midstream and MLPs 23

3-Year Price and Rating History for Cheniere Energy Partners LP (CQP.A)

CQP.A Closing Price Target Price

Date (US$) (US$) Rating

12-Nov-18 34.94 35.00 U

18-Dec-18 36.58 34.00

12-Mar-19 43.88 39.00

09-Sep-19 44.41 R

11-Sep-19 44.72 39.00 U

25-Nov-19 39.63 38.00

11-Mar-20 28.55 31.00 N

19-Nov-20 38.50 32.00 U

07-May-21 41.31 35.00

* Asterisk signifies initiation or assumption of coverage.

U N D ERPERFO RM

REST RICT ED

N EU T RA L

3-Year Price and Rating History for DCP Midstream LP (DCP.N)

DCP.N Closing Price Target Price

Date (US$) (US$) Rating

19-Nov-18 36.59 50.00 O

18-Dec-18 30.00 43.00

21-Feb-19 32.28 40.00

09-Jul-19 30.58 39.00

14-Aug-19 24.57 32.00

03-Oct-19 26.11 31.00

11-Nov-19 23.17 28.00

18-Feb-20 19.86 26.00

11-Mar-20 6.92 13.00

23-Mar-20 4.20 10.00

01-Apr-20 3.89 7.00 N

12-May-20 8.10 9.00

01-Jul-20 10.93 12.00

13-Aug-20 14.57 16.00

17-Dec-20 19.29 21.00

17-Feb-21 22.15 24.00

13-May-21 24.91 27.00

20-Jul-21 27.73 28.00

11-Aug-21 27.09 30.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

3-Year Price and Rating History for MPLX LP (MPLX.N)

MPLX.N Closing Price Target Price

Date (US$) (US$) Rating

26-Nov-18 32.78 45.00 O

15-Jan-19 33.20 44.00

12-Mar-19 33.67 39.00

09-Jul-19 31.89 38.00

12-Aug-19 26.97 33.00

19-Nov-19 22.63 29.00

10-Feb-20 22.39 25.00 N

11-Mar-20 15.41 21.00

01-Apr-20 11.40 18.00 O

13-May-20 17.34 22.00

17-Dec-20 22.98 28.00

27-May-21 28.74 34.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

13 October 2021

US Midstream and MLPs 24

3-Year Price and Rating History for New Fortress Energy (NFE.OQ)

NFE.OQ Closing Price Target Price

Date (US$) (US$) Rating

25-Feb-19 14.00 17.00 N *

28-May-19 12.91 16.00

18-Nov-19 15.36 17.00

11-Mar-20 11.02 16.00

08-Sep-20 31.89 28.00

10-Nov-20 35.04 37.00

26-Jan-21 44.84 50.00

24-Mar-21 48.11 52.00

02-Jun-21 41.92 50.00

19-Aug-21 27.64 34.00 O

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

3-Year Price and Rating History for ONEOK Inc (OKE.N)

OKE.N Closing Price Target Price

Date (US$) (US$) Rating

07-Nov-18 64.07 74.00 N

18-Dec-18 56.47 72.00

13-Mar-19 67.31 70.00

07-Aug-19 66.76 72.00

14-Jan-20 75.97 79.00

11-Mar-20 35.94 50.00 O

01-Apr-20 19.20 30.00

05-May-20 29.93 30.00 N

11-Jun-20 35.33 R

12-Jun-20 35.33 30.00 N

01-Jul-20 32.18 33.00

24-Jul-20 28.72 R

27-Jul-20 28.02 33.00 N

30-Oct-20 29.00 34.00

17-Dec-20 40.73 44.00

03-Mar-21 47.77 49.00

11-May-21 53.27 53.00

20-Jul-21 52.38 54.00

09-Aug-21 51.75 56.00

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

REST RICT ED

13 October 2021

US Midstream and MLPs 25

3-Year Price and Rating History for Targa Resources Corp (TRGP.N)

TRGP.N Closing Price Target Price

Date (US$) (US$) Rating

18-Dec-18 39.07 60.00 N

09-Jan-19 43.79 60.00 O

13-Mar-19 40.78 52.00

04-Apr-19 40.26 50.00

09-Jul-19 40.52 49.00

15-Aug-19 33.08 44.00

14-Jan-20 40.89 47.00

11-Mar-20 14.45 27.00

18-Mar-20 4.73 21.00

01-Apr-20 5.89 13.00 N

12-May-20 14.42 16.00

01-Jul-20 19.19 19.00

11-Aug-20 19.61 22.00

16-Nov-20 21.58 25.00 O

17-Dec-20 27.75 34.00

04-Mar-21 33.40 40.00

13-May-21 37.48 43.00

20-Jul-21 41.47 46.00

10-Aug-21 44.40 52.00

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

3-Year Price and Rating History for Williams Companies Inc (WMB.N)

WMB.N Closing Price Target Price

Date (US$) (US$) Rating

13-Nov-18 24.32 35.00 O

25-Feb-19 27.35 33.00

08-Aug-19 24.03 30.00

16-Oct-19 22.81 29.00

08-Nov-19 22.09 25.00

14-Jan-20 23.84 26.00

11-Mar-20 16.02 20.00

12-May-20 19.08 20.00 N

12-Aug-20 21.61 22.00

17-Dec-20 21.80 27.00 O

05-Mar-21 24.26 28.00

18-May-21 26.33 29.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months. Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months. Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months. *Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less at tractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as Eur opean (excluding Turkey) ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the an alyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin America, Turkey and Asia (excluding Japan and Australia), stock ratings are based on a stock’s total return relative to the average to tal return of the relevant country or regional benchmark (India - S&P BSE Sensex Index); prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12-month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

13 October 2021

US Midstream and MLPs 26

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time. Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.