us internal revenue service: p595--2000

TRANSCRIPT

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 1/15

ContentsIntroduction ........................................ 1

Important Changes for 2000 ............. 2

Important Dates for 2001 ................... 2

What Is Gross Income FromFishing? ....................................... 2

Which Fishing Expenses Can You

Deduct? ........................................ 2

What Forms Must You File? ............. 3

When Do Fishermen Pay EstimatedTax and File Tax Returns? ......... 5

What Is the Capital ConstructionFund? ........................................... 7

How To Claim Fuel Tax Credits andRefunds ........................................ 9

Schedule C Example .......................... 10

How To Get Tax Help ......................... 11

Index .................................................... 14

IntroductionThis publication highlights some special taxrules that may apply to you if you have yourown fishing trade or business. Those whohave their own fishing trade or business in-clude the following persons.

• Fishing boat owners or operators whouse their boats to fish for profit.

• Certain fishermen who work for a shareof the catch.

• Other individuals who receive gross in-come from fishing.

Generally you report your profit or lossfrom fishing on Schedule C or ScheduleC–EZ of Form 1040. An example with afilled-in Schedule C shown near the end ofthis publication provides details on how tocomplete this form.

This publication does not contain all ofthe tax rules that may apply to your fishingtrade or business. For general informationabout the federal tax laws that apply to indi-viduals who file Schedule C or C–EZ, seePublication 334, Tax Guide for Small Busi- ness. If your trade or business is a partner-ship or corporation, see Publication 541,Partnerships, or Publication 542, Corpo- rations.

RECORDS

If you are just starting out in a fishingbusiness or you need information onkeeping books and records, also see

Publication 583, Starting a Business and Keeping Records.

Please note that this publication uses theterm “fisherman” because it is the commonlyaccepted term in the fishing industry. In thefollowing discussions it represents both menand women.

Comments and suggestions. We welcomeyour comments about this publication andyour suggestions for future editions.

You can e-mail us while visiting our website at www.irs.gov/help/email2.html.

Departmentof theTreasury

InternalRevenueService

Publica tion 595Cat. No. 15171E

Tax H ighlightsfor CommercialFishermen

For use in preparing

2000 Returns

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 2/15

You can write to us at the following ad-dress:

Internal Revenue ServiceTechnical Publications BranchW:CAR:MP:FP:P1111 Constitution Ave. NWWashington, DC 20224

We respond to many letters by telephone.Therefore, it would be helpful if you wouldinclude your daytime phone number, includ-ing the area code, in your correspondence.

Important Changesfor 2000

Paid preparer authorization. Beginning withyour return for 2000, you can check a box andauthorize the IRS to discuss your tax returnwith the paid preparer who signed it. If youcheck the “Yes” box in the signature area ofyour return, the IRS can call your paidpreparer to answer any questions that mayarise during the processing of your return.Also, you are authorizing your paid preparer

to perform certain actions. See your incometax package for details.

Photographs of missing children. TheInternal Revenue Service is a proud partnerwith the National Center for Missing and Ex-ploited Children. Photographs of missingchildren selected by the Center may appearin this publication on pages that would other-wise be blank. You can help bring thesechildren home by looking at the photographsand calling 1–800–THE–LOST (1–800–843–5678) if you recognize a child.

Important Datesfor 2001This section highlights important due dates forfishermen for the 2001 calendar year. Forother important dates, see Publication 509,Tax Calendars for 2001.

January 16Fishermen. If at least two-thirds of your

gross income for either 1999 or 2000 wasfrom fishing, you may want to pay at leasttwo-thirds of your 2000 tax by this date,using Form 1040–ES, to meet your esti-mated tax requirement for 2000. This willallow you to wait until April 16 to file your

2000 Form 1040 and pay any remainingtax without penalty. See March 1, later, ifyou do not pay two-thirds of your tax bythis date.

If less than two-thirds of your grossincome is from fishing, you generally mustmake quarterly estimated tax payments.See Due Dates for Nonqualified Fisher- men, later.

January 31Fishing boat operators. Fishing boat oper-

ators must give a 2000 Form 1099–MISC,Miscellaneous Income, to certain crewmembers who were self-employed.

February 28Fishing boat operators. Use Form 1096,

Annual Summary and Transmittal of U.S.Information Returns, to send Copy A ofForms 1099–MISC to IRS.

March 1Fishermen. If at least two-thirds of your

gross income for either 1999 or 2000 wasfrom fishing, you can file your 2000 Form1040 by this date and pay your tax in full

without penalty.

April 16Fishermen. If you have not filed your Form

1040, you should file it by April 16 and payyour tax in full. If you need more time tofile, you can request an extension of timeto file with Form 4868, Application for Au- tomatic Extension of Time To File U.S.Individual Income Tax Return, or you canget an extension by Internet or phone ifyou pay part or all of your estimate of in-come tax due by direct debit or credit card.

More information. For more information onimportant dates, see Due Dates for Qual- ified Fishermen and Due Dates for Non-

qualified Fishermen, later.

Useful ItemsYou may want to see:

Publication

15 Circular E, Employer's Tax Guide

15–A Employer's Supplemental TaxGuide

15–B Employer's Tax Guide to FringeBenefits

334 Tax Guide for Small Business

378 Fuel Tax Credits and Refunds

463 Travel, Entertainment, Gift, andCar Expenses

505 Tax Withholding and EstimatedTax

533 Self-Employment Tax

535 Business Expenses

583 Starting a Business and KeepingRecords

946 How To Depreciate Property

Form (and Instructions)

Schedule C (Form 1040) Profit or LossFrom Business

Schedule C–EZ (Form 1040) Net ProfitFrom Business

1040–ES Estimated Tax for Individuals

1099–MISC Miscellaneous Income

2210–F Underpayment of Estimated Taxby Farmers and Fishermen

4136 Credit for Federal Tax Paid onFuels

8849 Claim for Refund of Excise Taxes

See How To Get Tax Help near the endof this publication for information about get-ting publications and forms.

What Is Gross IncomeFrom Fishing?Gross income from fishing includes amountsyou receive from catching, taking, harvesting,cultivating, or farming any of the followingaquatic resources.

• Fish.

• Shellfish (such as clams and mussels).

• Crustacea (such as lobsters, crabs, andshrimp).

• Sponges.

• Seaweeds.

• Other aquatic forms of animal or vegeta-ble life.

You will generally figure your gross in-come from fishing in Part I of Schedule C(Form 1040). For more information onSchedule C, see Schedule C (Form 1040)under What Forms Must You File?, later.

Wages. Wages you receive as an employeein a fishing business are not gross incomefrom fishing. This includes wages you receivefrom a corporation even if you are a share-holder in the corporation.

If you work on a boat with an operatingcrew that is normally made up of fewer than10 individuals, you may be considered aself-employed individual instead of an em-ployee. As a self-employed individual youmay receive gross income from fishing. Formore information, see Which fishermen are considered self-employed? under Form 1099–MISC, later.

Patronage dividends. Patronage dividendsyou receive from your fishing business activ-ities are generally included in your gross in-come from fishing. However, do not includein gross income amounts you receive from acooperative association relating to the pur-chase of capital assets or depreciable prop-erty used in your fishing business. You mustreduce the basis of these assets by the divi-dends.

Fuel tax credits and refunds. You mayhave to include fuel tax credits and refundsyou receive from your fishing business activ-ities in your gross income from fishing. Formore information, see Including the Credit or Refund in Income under How To Claim Fuel Tax Credits and Refunds, later.

Which FishingExpenses CanYou Deduct?You can generally deduct your ordinary andnecessary fishing expenses as business ex-penses in Part II of the Schedule C (Form1040). An ordinary fishing expense is onethat is common and accepted in a fishingtrade or business. A necessary fishing ex-pense is one that is helpful and appropriatefor a fishing trade or business. An expensedoes not have to be indispensable to beconsidered necessary.

Page 2

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 3/15

The following discussions give a briefoverview of three types of business expensesthat are of special interest to fishermen: de-preciation, travel, and transportation ex-penses. Business expenses that most smallbusinesses share are listed in Part II ofSchedule C. For more information on busi-ness expenses, see Publication 535. Youmay also find general information on specificbusiness expenses in Publication 334.

DepreciationIf property you acquire to use in your businesshas a useful life that extends substantiallybeyond the year it is placed in service, yougenerally cannot deduct the entire cost as abusiness expense in the year you acquire it.You must spread the cost over more than onetax year and deduct part of it each year. Thismethod of deducting the cost of businessproperty is called depreciation. Use Form4562, Depreciation and Amortization, to re-port depreciation.

Publication 946 contains the rules you willuse to depreciate certain property. The fol-lowing list highlights items that are of specialinterest to fishermen.

• Fishing boats. You can generally de-preciate a fishing boat used in your fish-ing trade or business as 7-year propertyusing Modified Accelerated Cost Recov-ery System (MACRS) depreciation.

• Nets, pots, and traps. You can generallydepreciate a net, pot, or trap used in yourfishing trade or business as 7-year prop-erty using MACRS depreciation. How-ever, if based on your own experience,you determine that any of these itemswill not be used for more than one yearin your business, you may be able todeduct the cost as a business expense.

• Repair or improvement. If a repair orreplacement increases the value of yourproperty, makes it more useful, orlengthens its life, it is an improvement.You must depreciate its cost. If the repairor replacement does not increase thevalue of your property, make it moreuseful, or lengthen its life, it is a repair.You deduct the cost as a business ex-pense.

Section 179 deduction. Instead of depreci-ating property, you can choose to deduct alimited amount (up to $20,000 for 2000) of thecost of certain depreciable property in theyear you buy it for use in your business. Thisdeduction is known as the “section 179 de-duction.” For more information, see Publica-tion 946.

Travel and TransportationThis section briefly explains some of the rulesfor deducting travel and transportation ex-penses. For more information about traveland transportation expenses, see Publication463. That publication also explains whatrecords to keep.

Local transportation expenses. Localtransportation expenses include the ordinaryand necessary costs of getting from oneworkplace to another in the course of yourbusiness when you are traveling within thecity or general area that is your tax home.

Tax home. Generally, your tax home isyour regular place of business, regardless ofwhere you maintain your family home. It in-cludes the entire city or general area inwhich your fishing business is located.

CAUTION

!Commuting expenses. You cannot deduct the costs of traveling between your home and your main or regular

place of business. These costs are personal commuting expenses. You cannot deduct commuting expenses no matter how far your home is from your regular place of business.

You cannot deduct commuting expenses even if you work during the trip.

Travel expenses. For tax purposes, travelexpenses are the ordinary and necessarycosts of traveling away from home for yourbusiness, profession, or job. You are travelingaway from home if you meet the followingrequirements.

1) Your duties require you to be away fromthe general area of your tax home (de-fined earlier) substantially longer than anordinary day's work.

2) You need to get sleep or rest to meet thedemands of your work while away fromhome.

Meals – limited deduction. You can gener-ally deduct only 50% of the costs of the fol-lowing meals.

• Meals you provide to either employeesor self-employed individuals who provideservices to your fishing trade or business.

• Your own meals while you are travelingaway from home for business.

Exceptions to meal deduction limit.

You can deduct the full costs of the followingmeals.

• Meals that qualify as a de minimis fringebenefit as discussed in chapter 2 ofPublication 15–B. This generally includesmeals you provide to employees at yourplace of business if more than half ofthese employees are provided the mealsfor your convenience.

• Meals whose value you include in anemployee's wages. For more information,see chapter 2 in Publication 15–B.

• Meals whose value you include in the in-come of a self-employed individual whoperforms services for your business. You

must generally include the value of mealsyou furnish to that individual in his or herincome. To deduct 100% of these meals,you must report their value on any Form1099–MISC you must file to report yourpayments for services.

• Meals you are required by federal law tofurnish to crew members of certain com-mercial vessels (or would be required toprovide if the vessels were operated atsea).

CAUTION

!The federal law that generally re- quires meals to be furnished to crew members of commercial vessels does

not apply to fishing vessels.

What Forms MustYou File?If you have a fishing trade or business, youmay need to file the following forms.

Schedule C (Form 1040)Use Schedule C (Form 1040) to figure yournet profit or loss from a fishing business youoperate or a trade you practice as a self-employed individual. To figure your net profitor loss, subtract your deductible fishing ex-penses from your gross income from fishing.File Schedule C with your Form 1040.

TIPYou may be able to use the simpler Schedule C–EZ (Form 1040) instead of Schedule C if you made a profit and

had fishing expenses of $2,500 or less. For more information, see Part I of Schedule C – EZ.

Who is self-employed? You are self-employed if you own an unincorporated busi-ness or practice a trade by yourself. You donot have to carry on regular full-time businessactivities to be self-employed. Your trade orbusiness may consist of part-time work, in-cluding work you do on the side in addition toyour regular job.

If you work on a fishing boat with an op-erating crew that is normally made up of fewerthan 10 individuals, you may be consideredself-employed. For more information, seeWhich fishermen are considered self- employed? under Form 1099 – MISC, later.

What is a trade or business? A tradeor business is generally an activity that is yourlivelihood or that you do in good faith to make

a profit. The facts and circumstances of eachcase determine whether or not an activity isa trade or business. Regularity of activitiesand transactions and the production of in-come are important elements. You do notneed to actually make a profit to be in a tradeor business as long as you have a profit mo-tive. You do need, however, to make ongoingefforts to further the interests of your busi-ness.

Husband and wife partners. You and yourspouse may operate a fishing business as apartnership. If you and your spouse join to-gether in the conduct of a business and sharein the profits and losses, you have created apartnership. You and your spouse must reportthe business income and expenses on Form1065, U.S. Return of Partnership Income . Theincome should not be reported on a ScheduleC. For more information, see Publication 541,Partnerships.

CAUTION

!Not-for-profit fishing. You must fish to make a profit in order to report your fishing income and expenses on

Schedule C. You do not need to actually make a profit as long as you are making a good faith effort. If you are not fishing for profit, report your fishing income and ex- penses as explained under Not-for-Profit Ac-tivities in chapter 1 of Publication 535.

Page 3

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 4/15

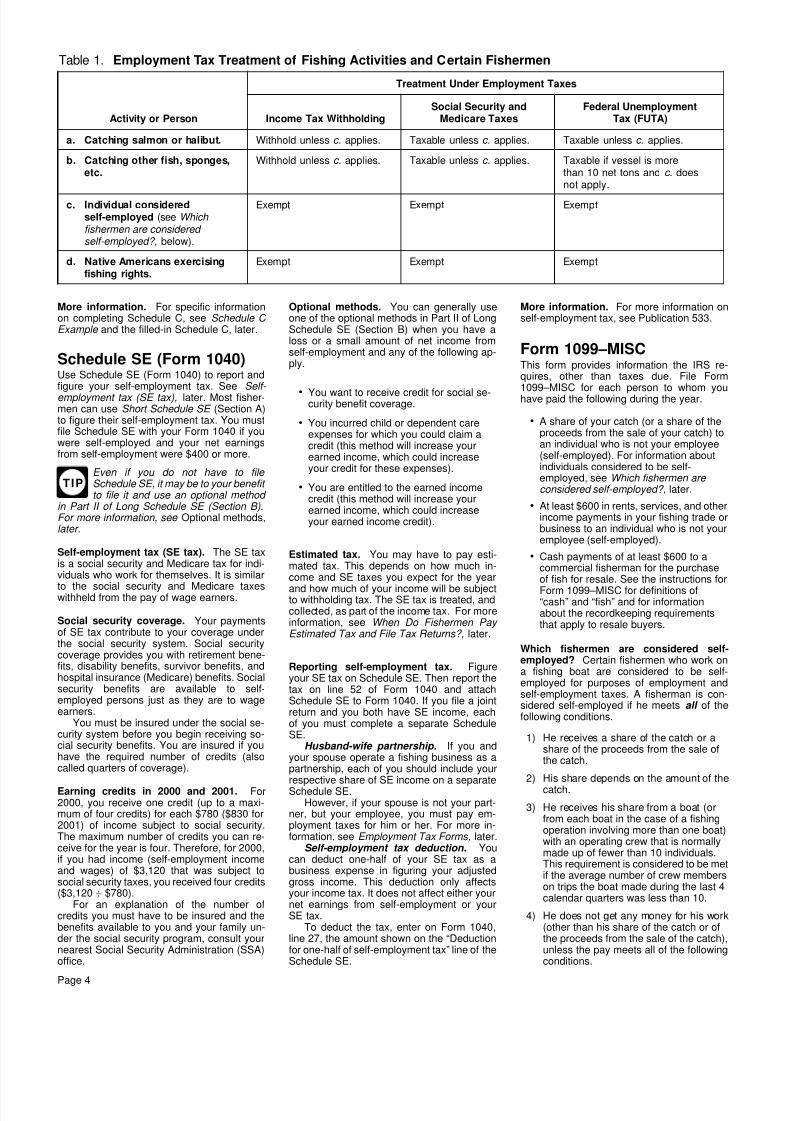

Table 1. Employment Tax Treatment of Fishing Activities and Certain Fishermen

Activity or Person Income Tax WithholdingSocial Security and

Medicare TaxesFederal Unemployment

Tax (FUTA)

a. Catching salmon or halibut.

b. Catching other fish, sponges,etc.

c. Individual consideredself-employed (see Which fishermen are considered self-employed?, below).

d. Native Americans exercisingfishing rights.

Withhold unless c. applies.

Exempt

Taxable unless c. applies.

Taxable if vessel is morethan 10 net tons and c. doesnot apply.

Exempt Exempt

Taxable unless c. applies.

Withhold unless c. applies. Taxable unless c. applies.

Exempt Exempt Exempt

Treatment Under Employment Taxes

More information. For specific informationon completing Schedule C, see Schedule C Example and the filled-in Schedule C, later.

Schedule SE (Form 1040)Use Schedule SE (Form 1040) to report andfigure your self-employment tax. See Self- employment tax (SE tax), later. Most fisher-men can use Short Schedule SE (Section A)to figure their self-employment tax. You mustfile Schedule SE with your Form 1040 if youwere self-employed and your net earningsfrom self-employment were $400 or more.

TIPEven if you do not have to file Schedule SE, it may be to your benefit to file it and use an optional method

in Part II of Long Schedule SE (Section B).For more information, see Optional methods,later.

Self-employment tax (SE tax). The SE taxis a social security and Medicare tax for indi-viduals who work for themselves. It is similar

to the social security and Medicare taxeswithheld from the pay of wage earners.

Social security coverage. Your paymentsof SE tax contribute to your coverage underthe social security system. Social securitycoverage provides you with retirement bene-fits, disability benefits, survivor benefits, andhospital insurance (Medicare) benefits. Socialsecurity benefits are available to self-employed persons just as they are to wageearners.

You must be insured under the social se-curity system before you begin receiving so-cial security benefits. You are insured if youhave the required number of credits (alsocalled quarters of coverage).

Earning credits in 2000 and 2001. For2000, you receive one credit (up to a maxi-mum of four credits) for each $780 ($830 for2001) of income subject to social security.The maximum number of credits you can re-ceive for the year is four. Therefore, for 2000,if you had income (self-employment incomeand wages) of $3,120 that was subject tosocial security taxes, you received four credits($3,120 ÷ $780).

For an explanation of the number ofcredits you must have to be insured and thebenefits available to you and your family un-der the social security program, consult yournearest Social Security Administration (SSA)office.

Optional methods. You can generally useone of the optional methods in Part II of LongSchedule SE (Section B) when you have aloss or a small amount of net income fromself-employment and any of the following ap-ply.

• You want to receive credit for social se-curity benefit coverage.

• You incurred child or dependent careexpenses for which you could claim acredit (this method will increase yourearned income, which could increaseyour credit for these expenses).

• You are entitled to the earned incomecredit (this method will increase yourearned income, which could increaseyour earned income credit).

Estimated tax. You may have to pay esti-mated tax. This depends on how much in-come and SE taxes you expect for the year

and how much of your income will be subjectto withholding tax. The SE tax is treated, andcollected, as part of the income tax. For moreinformation, see When Do Fishermen Pay Estimated Tax and File Tax Returns?, later.

Reporting self-employment tax. Figureyour SE tax on Schedule SE. Then report thetax on line 52 of Form 1040 and attachSchedule SE to Form 1040. If you file a jointreturn and you both have SE income, eachof you must complete a separate ScheduleSE.

Husband-wife partnership. If you andyour spouse operate a fishing business as apartnership, each of you should include yourrespective share of SE income on a separateSchedule SE.

However, if your spouse is not your part-ner, but your employee, you must pay em-ployment taxes for him or her. For more in-formation, see Employment Tax Forms, later.

Self-employment tax deduction. Youcan deduct one-half of your SE tax as abusiness expense in figuring your adjustedgross income. This deduction only affectsyour income tax. It does not affect either yournet earnings from self-employment or yourSE tax.

To deduct the tax, enter on Form 1040,line 27, the amount shown on the “Deductionfor one-half of self-employment tax” line of theSchedule SE.

More information. For more information onself-employment tax, see Publication 533.

Form 1099–MISCThis form provides information the IRS re-quires, other than taxes due. File Form

1099–MISC for each person to whom youhave paid the following during the year.

• A share of your catch (or a share of theproceeds from the sale of your catch) toan individual who is not your employee(self-employed). For information aboutindividuals considered to be self-employed, see Which fishermen are considered self-employed? , later.

• At least $600 in rents, services, and otherincome payments in your fishing trade orbusiness to an individual who is not youremployee (self-employed).

• Cash payments of at least $600 to acommercial fisherman for the purchaseof fish for resale. See the instructions for

Form 1099–MISC for definitions of“cash” and “fish” and for informationabout the recordkeeping requirementsthat apply to resale buyers.

Which fishermen are considered self-employed? Certain fishermen who work ona fishing boat are considered to be self-employed for purposes of employment andself-employment taxes. A fisherman is con-sidered self-employed if he meets all of thefollowing conditions.

1) He receives a share of the catch or ashare of the proceeds from the sale ofthe catch.

2) His share depends on the amount of thecatch.

3) He receives his share from a boat (orfrom each boat in the case of a fishingoperation involving more than one boat)with an operating crew that is normallymade up of fewer than 10 individuals.This requirement is considered to be metif the average number of crew memberson trips the boat made during the last 4calendar quarters was less than 10.

4) He does not get any money for his work(other than his share of the catch or ofthe proceeds from the sale of the catch),unless the pay meets all of the followingconditions.

Page 4

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 5/15

a) He does not get more than $100per trip.

b) He is paid only if there is someminimum catch.

c) He is paid solely for additional du-ties (such as for services performedas mate, engineer, or cook) forwhich additional cash payments aretraditional in the fishing industry.

Example 1. You hire a captain, a mate,

an engineer, a cook, and five other crewmembers to work on your fishing boat. Theproceeds from the sale of the catch offsetboat operating expenses such as bait, ice,and fuel. You divide 60% of the balance be-tween the captain, the mate, and the crewmembers. You divide the other 40% betweenyourself and the captain. The mate, the engi-neer, and the cook also each receive an extra$100 for each trip that brings back a certainminimum catch. The crew members do notreceive any additional pay between voyages,but they must do certain work, such as re-pairing nets, splicing cable, and transportingthe catch.

For purposes of employment and self-employment taxes, each crew member (in-cluding the captain, mate, engineer, and

cook) is considered self-employed. You mustfile Form 1099–MISC to report amounts youpay to them.

Example 2. The facts are the same as inExample 1 except that all the crew membersbut the captain receive an extra $100 for eachtrip that brings back a certain minimum catch.

For purposes of employment and self-employment taxes, the captain, the mate, theengineer, and the cook are self-employed in-dividuals. The other five crew members whoreceive this extra payment in addition to theproceeds from the sale of the catch are em-ployees. They are employees because the$100 payment is not paid solely for additionalduties for which additional cash pay is tradi-

tional in the fishing industry.

Employment Tax FormsYou are generally required to withhold federalincome tax from the wages of your employ-ees. You may also be subject to social secu-rity and Medicare taxes under the FederalInsurance Contributions Act (FICA) and fed-eral unemployment tax under the FederalUnemployment Tax Act (FUTA). If you haveemployees, you will need to file forms to re-port these employment taxes. For more in-formation, see Publication 15. That publica-tion explains your tax responsibilities as anemployer.

To help you determine whether the people

working for you are your employees, seePublication 15–A. That publication has infor-mation to help you determine whether an in-dividual is an independent contractor or anemployee.

CAUTION

!If you incorrectly classify an employee as an independent contractor, you can be held liable for employment

taxes for that worker plus a penalty.

An independent contractor is someonewho is self-employed. You do not generallyhave to withhold or pay any taxes on pay-ments to an independent contractor.

Individuals you employ to work on a boatthat normally has an operating crew of fewer

than 10 individuals may be considered self-employed. For more information, see Which fishermen are considered self-employed? under Form 1099 – MISC, earlier.

Table 1. See Table 1 for information on thespecial employment tax treatment of fishingactivities and certain fishermen.

When Do Fishermen

Pay Estimated Taxand File Tax Returns?When you must pay estimated tax and fileyour tax return depends on whether you re-ceive at least two-thirds of your total grossincome from fishing in the current or prioryear. Gross income is discussed later.

General Rule For MakingEstimated Tax PaymentsYou must make estimated tax payments for2000 if you expect to owe at least $1,000 intax for 2000, after subtracting your withhold-ing and credits, and you expect your with-

holding and credits to be less than the smallerof the following.

1) 90% of the tax to be shown on your 2000tax return.

2) 100% of the tax shown on your 1999 taxreturn. Your 1999 tax return must coverall 12 months.

If at least two-thirds of your gross income for1999 or 2000 is from fishing, substitute662 / 3% for 90% in (1) above.

What Is Gross Income?Gross income is all income you receive in theform of money, goods, property, and services

that is not exempt from tax. Gross income is not the same as total income shown online 22 of Form 1040. On a joint return, youmust add your spouse's gross income to yourgross income. To decide whether two-thirdsof your gross income for 2000 was from fish-ing, use as your gross income the totalamount of the following income (not loss) items from your tax return.

• Wages, salaries, tips, etc.

• Taxable interest.

• Ordinary dividends.

• Taxable refunds of state and local taxes.

• Alimony received.

• Gross business income from ScheduleC (Form 1040), line 7 (includes grossfishing income).

• Gross business receipts from ScheduleC–EZ (Form 1040), line 1 (includes grossfishing income).

• Capital gains from Form 1040, line 13,and Schedule D (Form 1040). Lossescannot be netted against gains.

• Gains on sales of business property fromForm 4797 and shown on Schedule D.

• Taxable IRA distributions, pensions, an-nuities, and social security benefits.

• Gross rental income from Schedule E(Form 1040), line 3.

• Gross royalty income from Schedule E(Form 1040), line 4.

• Taxable net income from an estate ortrust, Schedule E (Form 1040), line 36.

• Income from a REMIC reported onSchedule E (Form 1040), line 38.

• Gross farm rental income from Form4835, line 7 (includes gross fishing in-come from Schedule E (Form 1040)).

• Gross farm income from Schedule F(Form 1040), line 11.

• Your distributive share of gross incomefrom a partnership or limited liabilitycompany treated as a partnership fromSchedule K–1 (Form 1065).

• Your pro rata share of gross income froman S corporation from Schedule K–1(Form 1120S).

• Unemployment compensation as re-ported on Form 1099–G.

• Other income reported on Form 1040,line 21, not reported with any of the itemslisted above.

Percentage From FishingFigure your gross income from all sources aslisted earlier. Then figure your gross incomefrom fishing. Divide your fishing gross incomeby your total gross income to determine thepercentage of gross income from fishing.

Example 1. James Smith had the follow-ing total gross income and fishing gross in-come in 2000.

Schedule D showed gain from the sale ofa rental house carried over from Form 4797($5,000) in addition to a loss from the sale ofcorporate stock ($2,000). However, that lossis not netted against the gain to figure Mr.Smith's total gross income or his gross fishingincome. His gross fishing income is 60% ofhis total gross income ($75,000 ÷ $125,000= .60). Therefore, based on his 2000 income,he does not qualify to use the special esti-mated tax payment and return due dates for2000, discussed next. However, he doesqualify if at least two-thirds of his 1999 grossincome was from fishing.

Example 2. Assume the same facts as

in Example 1 except that Mr. Smith receivedonly $23,000, instead of $43,000, taxable in-terest. This made his total gross income$105,000. He qualifies to use the special es-timated tax payment and return due datesdiscussed next, since 71.4% (at least two-thirds) of his gross income is from fishing($75,000 ÷ $105,000 = .714).

Due Dates forQualified FishermenIf at least two-thirds of your gross income for1999 or 2000 was from fishing, you are aqualified fisherman and can choose either ofthe following options for your 2000 tax.

Gross Income

Total Fishing

Taxable interest ......................... $43,000Dividends ................................... 500Rental income (Sch E) .............. 1,500Fishing income (Sch C) ............ 75,000 $75,000Schedule D ................................ 5,000

Total .......................................... $125,000 $75,000

Page 5

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 6/15

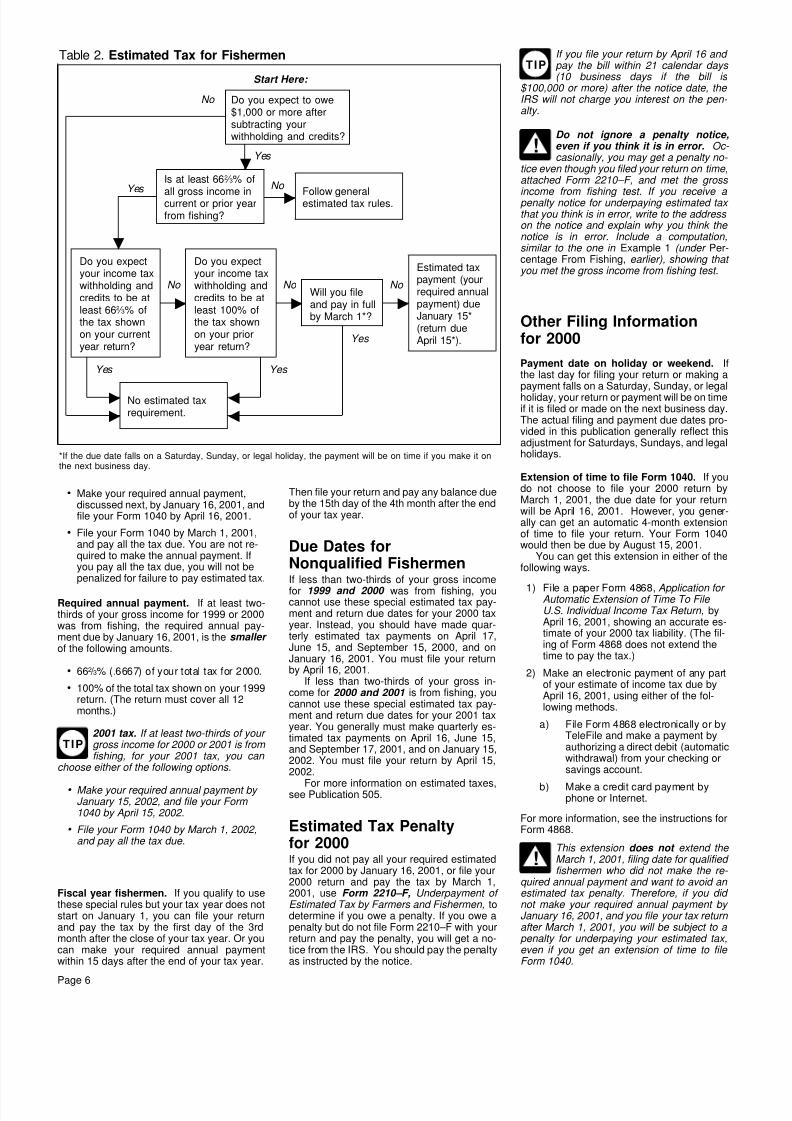

Table 2. Estimated Tax for Fishermen

Start Here:

*If the due date falls on a Saturday, Sunday, or legal holiday, the payment will be on time if you make it onthe next business day.

Do you expect to owe$1,000 or more aftersubtracting yourwithholding and credits?

Do you expectyour income taxwithholding andcredits to be atleast 100% ofthe tax shownon your prioryear return?

No estimated taxrequirement.

Do you expectyour income taxwithholding andcredits to be atleast 662 ⁄ 3% ofthe tax shownon your currentyear return?

Will you fileand pay in fullby March 1*?

Estimated taxpayment (yourrequired annualpayment) dueJanuary 15*(return dueApril 15*).

Is at least 662 ⁄ 3% of

all gross income incurrent or prior yearfrom fishing?

Follow generalestimated tax rules.

Yes

No

Yes

No

No

No

Yes

Yes

Yes

No

TIPIf you file your return by April 16 and pay the bill within 21 calendar days (10 business days if the bill is

$100,000 or more) after the notice date, the IRS will not charge you interest on the pen- alty.

CAUTION

!Do not ignore a penalty notice,even if you think it is in error. Oc- casionally, you may get a penalty no-

tice even though you filed your return on time,attached Form 2210 – F, and met the gross

income from fishing test. If you receive a penalty notice for underpaying estimated tax that you think is in error, write to the address on the notice and explain why you think the notice is in error. Include a computation,similar to the one in Example 1 (under Per-centage From Fishing, earlier), showing that you met the gross income from fishing test.

Other Filing Informationfor 2000

Payment date on holiday or weekend. Ifthe last day for filing your return or making apayment falls on a Saturday, Sunday, or legalholiday, your return or payment will be on timeif it is filed or made on the next business day.The actual filing and payment due dates pro-vided in this publication generally reflect thisadjustment for Saturdays, Sundays, and legalholidays.

Extension of time to file Form 1040. If youdo not choose to file your 2000 return byMarch 1, 2001, the due date for your returnwill be April 16, 2001. However, you gener-ally can get an automatic 4-month extensionof time to file your return. Your Form 1040would then be due by August 15, 2001.

You can get this extension in either of thefollowing ways.

1) File a paper Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return, byApril 16, 2001, showing an accurate es-timate of your 2000 tax liability. (The fil-ing of Form 4868 does not extend thetime to pay the tax.)

2) Make an electronic payment of any partof your estimate of income tax due byApril 16, 2001, using either of the fol-lowing methods.

a) File Form 4868 electronically or byTeleFile and make a payment byauthorizing a direct debit (automaticwithdrawal) from your checking orsavings account.

b) Make a credit card payment byphone or Internet.

For more information, see the instructions forForm 4868.

CAUTION

!This extension does not extend the March 1, 2001, filing date for qualified fishermen who did not make the re-

quired annual payment and want to avoid an estimated tax penalty. Therefore, if you did not make your required annual payment by January 16, 2001, and you file your tax return after March 1, 2001, you will be subject to a penalty for underpaying your estimated tax,even if you get an extension of time to file Form 1040.

• Make your required annual payment,discussed next, by January 16, 2001, andfile your Form 1040 by April 16, 2001.

• File your Form 1040 by March 1, 2001,and pay all the tax due. You are not re-quired to make the annual payment. Ifyou pay all the tax due, you will not bepenalized for failure to pay estimated tax.

Required annual payment. If at least two-thirds of your gross income for 1999 or 2000was from fishing, the required annual pay-ment due by January 16, 2001, is the smaller of the following amounts.

• 662 / 3% (.6667) of your total tax for 2000.

• 100% of the total tax shown on your 1999return. (The return must cover all 12months.)

TIP2001 tax. If at least two-thirds of your gross income for 2000 or 2001 is from fishing, for your 2001 tax, you can

choose either of the following options.

• Make your required annual payment by January 15, 2002, and file your Form 1040 by April 15, 2002.

• File your Form 1040 by March 1, 2002,and pay all the tax due.

Fiscal year fishermen. If you qualify to usethese special rules but your tax year does notstart on January 1, you can file your returnand pay the tax by the first day of the 3rdmonth after the close of your tax year. Or youcan make your required annual paymentwithin 15 days after the end of your tax year.

Then file your return and pay any balance dueby the 15th day of the 4th month after the endof your tax year.

Due Dates forNonqualified FishermenIf less than two-thirds of your gross income

for 1999 and 2000 was from fishing, youcannot use these special estimated tax pay-ment and return due dates for your 2000 taxyear. Instead, you should have made quar-terly estimated tax payments on April 17,June 15, and September 15, 2000, and onJanuary 16, 2001. You must file your returnby April 16, 2001.

If less than two-thirds of your gross in-come for 2000 and 2001 is from fishing, youcannot use these special estimated tax pay-ment and return due dates for your 2001 taxyear. You generally must make quarterly es-timated tax payments on April 16, June 15,and September 17, 2001, and on January 15,2002. You must file your return by April 15,2002.

For more information on estimated taxes,see Publication 505.

Estimated Tax Penaltyfor 2000If you did not pay all your required estimatedtax for 2000 by January 16, 2001, or file your2000 return and pay the tax by March 1,2001, use Form 2210 – F, Underpayment of Estimated Tax by Farmers and Fishermen, todetermine if you owe a penalty. If you owe apenalty but do not file Form 2210–F with yourreturn and pay the penalty, you will get a no-tice from the IRS. You should pay the penaltyas instructed by the notice.

Page 6

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 7/15

What Is the CapitalConstruction Fund?The Capital Construction Fund (CCF) is aspecial investment program administered bythe National Marine Fisheries Service(NMFS) and the Internal Revenue Service(IRS). This program allows fishermen to deferpaying income tax on certain income they in-vest in a CCF account and later use to ac-quire, build, or rebuild fishing vessels.

The following sections discuss CCF ac-counts and the types of bookkeeping ac-counts that you must maintain when you in-vest in a CCF account. They also discuss theincome tax treatment of CCF deposits,earnings, and withdrawals.

CCF AccountsThis section explains who can open a CCFaccount and how to use the account to deferincome tax.

Opening a CCF account. If you are a U.S.citizen and you own or lease one or more el-igible vessels (defined later), you can open aCCF account. Before you open your CCFaccount, you must enter into an agreementwith the Secretary of Commerce through theNMFS. This agreement will establish the fol-lowing.

• Agreement vessels. These are any eli-gible vessels contained in the agreementthat will be the basis for the deferral ofincome tax.

• Planned use of withdrawals. The useof the money in your CCF account toacquire, build, or rebuild a vessel is aplanned use of withdrawals.

• CCF depository. This is where your CCFfunds will be held.

You can request an application kit orget additional information from NMFSat the following address.

CCF ProgramFinancial Services Division (F/SF2)NOAA/National Marine Fisheries Service1315 East-West Highway, 13th FloorSilver Spring, MD 20910–3282

You can call NMFS to request an ap-plication kit or get additional informa-tion at (301) 713–2393. The fax

number is (301) 713–1306.

Eligible vessels. There are two types ofvessels that may be considered eligible, those

weighing 5 tons or more and those weighingless than 5 tons. For each type, certain re-quirements must be met.

Vessel weighing 5 tons or more. Thisis a vessel that must meet all the followingrequirements to be considered eligible. Thevessel must be:

• Built or rebuilt in the United States.

• Documented under the laws of the UnitedStates.

• Used commercially in the fisheries of theUnited States.

• Operated in the foreign or domesticcommerce of the United States.

Vessel weighing less than 5 tons. Asmall vessel, one weighing at least 2 net tonsbut less than 5 net tons, must meet all thefollowing requirements to be considered eli-gible. The vessel must:

• Be built or rebuilt in the United States.

• Be owned by a U.S. citizen.

• Have a home port in the United States.

• Be used commercially in the fisheries ofthe United States.

Deferring tax on CCF deposits andearnings. You can use a CCF account todefer income tax by taking the followingactions.

• Making deposits to your CCF account.

• Excluding from income tax deposits thatare assigned to certain accounts (dis-cussed later).

• Making withdrawals from your CCF ac-count when you acquire, build, or rebuildfishing vessels.

• Reducing the tax basis of fishing vesselsyou acquire, build, or rebuild to“recapture” the amounts that were previ-

ously excluded from tax.

TIPReporting requirements. Beginning with the tax year in which you estab- lished your agreement, you must re-

port annual deposit and withdrawal activity to the NMFS on NOAA Form 34 – 82. This form is due within 30 days after you file your fed- eral income tax return even if no deposits or withdrawals are made. For more information,contact the NMFS at the address or phone number given earlier.

Types of Accounts You

Must Maintain Within a CCFThis section discusses the three types ofbookkeeping accounts you must maintainwhen you invest in a CCF account. Your totalCCF deposits and earnings for any given yearare limited to the amount that can be attri-buted for that year to these three accounts.

Capital account. The capital account con-sists primarily of amounts attributable to thefollowing items.

1) Allowable depreciation deductions foragreement vessels.

2) Any nontaxable return of capital from ei-ther (a) or (b), below.

a) The sale or other disposition ofagreement vessels.

b) Insurance or indemnity proceedsattributable to agreement vessels.

3) Any tax-exempt interest earned on stateor local bonds in your CCF account.

Capital gain account. The capital gain ac-count consists of amounts attributable to thefollowing items reduced by any capital lossesfrom assets held in your CCF account formore than 6 months.

1) Any capital gain from either of the fol-lowing sources.

a) The sale or other disposition ofagreement vessels held for morethan 6 months.

b) Insurance or indemnity proceedsattributable to agreement vesselsheld for more than 6 months.

2) Any capital gain from assets held in yourCCF account for more than 6 months.

Ordinary income account. The ordinary in-come account consists of amounts attribut-

able to the following items.

1) Any earnings (without regard to thecarryback of any net operating or netcapital loss) from the operation ofagreement vessels in the fisheries of theUnited States or in the foreign or do-mestic commerce of the United States.

2) Any capital gain from the followingsources reduced by any capital lossesfrom assets held in your CCF account for6 months or less.

a) The sale or other disposition ofagreement vessels held for 6months or less.

b) Insurance or indemnity proceeds

attributable to agreement vesselsheld for 6 months or less.

c) Any capital gain from assets held inyour CCF account for 6 months orless.

3) Any ordinary income (such as depreci-ation recapture) from either of the fol-lowing sources.

a) The sale or other disposition ofagreement vessels.

b) Insurance or indemnity proceedsattributable to agreement vessels.

4) Any interest (not including tax-exemptinterest from state and local bonds),

most dividends, and other ordinary in-come earned on the assets in your CCFaccount.

Tax Treatment of CCFDepositsThis section explains the tax treatment of in-come that you use as the basis for CCF de-posits.

Capital gains. Do not report on your incometax return any transaction that produces acapital gain if you deposit the net proceedsinto your CCF account. This treatment appliesto either of the following transactions.

• The sale or other disposition of anagreement vessel.

• The receipt of insurance or indemnityproceeds attributable to an agreementvessel.

Depreciation recapture. Do not report onyour income tax return any transaction thatproduces depreciation recapture if you de-posit the net proceeds into your CCF account.This treatment applies to either of the follow-ing transactions.

• The sale or other disposition of anagreement vessel.

Page 7

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 8/15

• The receipt of insurance or indemnityproceeds attributable to an agreementvessel.

Earnings from operations. Report earningsfrom the operation of agreement vessels onyour Schedule C or C–EZ (Form 1040) evenif you deposit part of these earnings into yourCCF account. Subtract any part of theearnings that you deposited into your CCFaccount from the amount that you wouldnormally enter as taxable income on line 39

(Form 1040). In the margin to the left of line39, write “CCF” and the amount of these de-posits. Do not deduct these CCF deposits onSchedule C or C–EZ (Form 1040).

CAUTION

!If you deposit earnings from oper- ations into your CCF account and you must complete other forms such as

Form 6251 or a worksheet for Schedule D,you will need to make an extra computation.When the other form instructs you to use the amount from line 37, Form 1040, do not use that amount. Instead, add lines 38 and 39,Form 1040, and use that amount.

Self-employment tax. You must use yournet profit or loss from your fishing business

to figure your self-employment tax. Do not reduce your net profit or loss by any earningsfrom operations you deposit into your CCFaccount.

TIPPartnerships and S corporations.The deduction for partnership earnings from operations that are de-

posited into a CCF account is separately stated on Schedule K (Form 1065), line 11,and allocated to the partners on Schedule K – 1 (Form 1065), line 11.

The deduction for S corporation earnings that are deposited is separately stated on Schedule K (Form 1120S), line 10, and allo- cated to the shareholders on Schedule K – 1(Form 1120S), line 10.

Nontaxable return of capital. Do not reporton your income tax return any transaction thatproduces a nontaxable return of capital if youdeposit the net proceeds into your CCF ac-count. This treatment applies to either of thefollowing transactions.

• The sale or other disposition of anagreement vessel.

• The receipt of insurance or indemnityproceeds attributable to an agreementvessel.

Tax Treatment of CCFEarningsThis section explains the tax treatment of theearnings from the assets in your CCF accountwhen the earnings are redeposited or left inyour account. However, if you choose towithdraw the earnings in the year earned, youmust generally pay income tax on them.

Capital gains. Do not report on your incometax return any capital gains from the sale ofcapital assets held in your CCF account. Thisincludes capital gain distributions reported toyou on Form 1099–DIV or a substitute state-ment. However, you should attach a state-

ment to your tax return to list the payers andthe amounts and to identify the capital gainsas “CCF account earnings.”

Interest and dividends. Do not report onyour income tax return any ordinary income(such as interest and dividends) you earn onthe assets in your CCF account. However,you should attach a statement to your returnto list the payers and the amounts and toidentify them as “CCF account earnings.”

If you are required to file Schedule B

(Form 1040), you can add these earnings tothe list of payers and amounts on line 1 or line5 and identify them as “CCF earnings.” Thensubtract the same amounts from the list andidentify them as “CCF deposits.”

Tax-exempt interest. Do not report onyour federal income tax return tax-exempt in-terest from state or local bonds you held inyour CCF account. You are not required toreport this interest on line 8b of Form 1040.

Tax Treatment of CCFWithdrawalsThis section discusses the tax treatment ofamounts you withdraw from your CCF ac-count during the year.

Qualified WithdrawalsA qualified withdrawal from a CCF account isone that is approved by NMFS for either ofthe following uses.

• Acquiring, building, or rebuilding qualifiedvessels (defined next).

• Making principal payments on the mort-gage of a qualified vessel.

Qualified vessel. This is any vessel thatmeets all the following requirements.

• The vessel was built or rebuilt in the

United States.• The vessel is documented under the laws

of the United States.

• The person maintaining the CCF accountagrees with the Secretary of Commercethat the vessel will be operated in theUnited States foreign, Great Lakes, ornoncontiguous domestic trade or in thefisheries of the United States.

How to determine the source of qualifiedwithdrawals. When you make a qualifiedwithdrawal, the amount you withdraw istreated as being made in the following orderfrom your accounts.

• First, from the capital account.• Second, from the capital gain account.

• Third, from the ordinary income account.

Excluding qualified withdrawals from tax.Do not report on your income tax return anyqualified withdrawals from your CCF account.

Reducing the tax basis of acquired, built,or rebuilt vessels. You must reduce thedepreciable basis of fishing vessels you ac-quire, build, or rebuild when you make aqualified withdrawal that is treated as madefrom either the capital gain account or theordinary income account.

Nonqualified WithdrawalsA nonqualified withdrawal from a CCF ac-count is generally any withdrawal that is nota qualified withdrawal. Qualified withdrawalsare defined under Qualified Withdrawals,earlier.

Examples. Examples of nonqualified with-drawals include the following amounts fromthe ordinary income account or the capitalgain account.

• Amounts remaining in a CCF accountupon termination of your agreement withNMFS.

• Amounts you withdraw and use to makeprincipal payments on the mortgage of avessel if the basis of that vessel and thebases of other vessels you own have al-ready been reduced to zero.

• Amounts determined by IRS to causeyour CCF account balance to exceed theamount that is appropriate to meet yourplanned use of withdrawals. (You willgenerally be given 3 years to revise yourplans to cover this excess balance.)

• Amounts you leave in your account formore than 25 years. (There is a gradu-

ated schedule under which the percent-age that is applied to determine theamount of the nonqualified withdrawalincreases from 20% in the 26th year to100% in the 30th year.)

How to determine the source of nonqual-ified withdrawals. When you make a non-qualified withdrawal from your CCF account,the amount you withdraw is treated as beingmade in the following order from your ac-counts.

• First, from the ordinary income account.

• Second, from the capital gain account.

• Third, from the capital account.

Paying tax on nonqualified withdrawals.In general, nonqualified withdrawals are taxedseparately from your other gross income andat the highest marginal tax rate in effect forthe year of withdrawal. However, nonqualifiedwithdrawals that are treated as made from thecapital gain account are taxed at a rate thatcannot exceed 20% for individuals and 34%for corporations.

TIPPartnerships and S corporations.Taxable nonqualified partnership withdrawals are separately stated on

Schedule K (Form 1065), line 24, and allo- cated to the partners on Schedule K – 1 (Form 1065), line 25. Taxable nonqualified with- drawals by an S corporation are separately stated on Schedule K (Form 1120S), line 21,and allocated to the shareholders on Sched- ule K – 1 (Form 1120S), line 23.

Interest. You must pay interest on the addi-tional tax due to nonqualified withdrawals thatare treated as made from either the ordinaryincome account or the capital gain account.The interest period begins on the last date forpaying tax for the tax year for which you de-posited the amount that you withdrew fromyour CCF account. The period ends on thelast date for paying tax for the tax year inwhich you make the nonqualified withdrawal.The interest rate on the nonqualified with-

Page 8

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 9/15

drawal is simple interest. The rate is subjectto change annually and published in theFederal Register.

The current interest rate can also beobtained by calling NMFS at (301)713–2393.

Interest deduction. You can deduct theinterest you pay on a nonqualified withdrawalas a trade or business expense.

Reporting the additional tax and interest.Attach a statement to your income tax returnto show your computation of both the tax andinterest on a nonqualified withdrawal. Includethe tax and interest on the nonqualified with-drawal on line 57 of Form 1040. To the leftof line 57, write the amount of tax and interestand “CCF.”

Tax benefit rule. If any portion of your non-qualified withdrawal is properly attributable tocontributions (not earnings on the contribu-tions) you made to the CCF account that didnot reduce your tax liability for any tax yearprior to the withdrawal year, the following taxtreatment applies.

• The part that did not reduce your tax li-ability for any year prior to the withdrawalyear is not taxed.

• That part is allowed as a net operatingloss deduction.

More InformationThis section briefly discussed the CCF pro-gram. For more detailed information, see thefollowing legislative authorities.

• Section 607 of the Merchant Marine Actof 1936, as amended (46 U.S.C. 1177).

• Chapter 2, Part 259 of title 50 of the Codeof Federal Regulations (50 C.F.R., Part259).

• Subchapter A, Part 3 of title 26 of theCode of Federal Regulations (26 C.F.R.,Part 3).

• Section 7518 of the Internal RevenueCode (IRC 7518).

The application kit you can obtain from NMFSat the address or phone number given earliermay contain copies of some of these sourcesof additional information.

How To Claim FuelTax Credits andRefundsYou may be eligible to claim a credit on yourincome tax return for federal excise tax im-posed on certain fuels used for a nontaxableuse. You may also be eligible to claim aquarterly refund of the fuel taxes during theyear, instead of waiting to claim a credit onyour income tax return.

Instead of paying the fuel tax and filing fora credit or refund, you may be able to buycertain fuel tax free. For more information,see How To Buy Fuel Tax Free, later.

Nontaxable UsesThis section discusses the nontaxable usesthat are of particular interest to fishermen. Forinformation about credits and refunds for fuelsused for nontaxable uses not discussed inthis section, see Publication 378.

Commercial fishing. You may be eligible toclaim a credit or refund of excise tax on gas-oline used in a boat engaged in commercialfishing.

Boats engaged in commercial fishing in-clude only watercraft used in taking, catching,processing, or transporting fish, shellfish, orother aquatic life for commercial purposes,such as selling or processing the catch, on aspecific trip basis. They include boats used inboth fresh and salt water fishing. They do notinclude boats used for both sport fishing andcommercial fishing on the same trip.

CAUTION

!Fuel used in aircraft to locate fish is not fuel used in commercial fishing.

Off-highway business use. You may beeligible to claim a credit or refund of excisetax on fuel if you use the fuel in an off-highway business use.

What is off-highway business use? Off-highway business use is any use of fuelin a trade or business or in any income-producing activity. It does not include use ina highway vehicle registered or required tobe registered for use on public highways.Off-highway business use includes fuels usedin the following ways.

• In stationary engines to operate genera-tors, compressors, and similar equip-ment.

• For cleaning purposes.

CAUTION

!Do not consider any use in a boat as an off-highway business use.

How To Claima Credit or RefundThis section tells you when and how to claima credit or refund of excise taxes on fuels youuse for a nontaxable use.

Credit or refund. A credit is an amount thatreduces the tax on your income tax returnwhen you file it at the end of the year. If youmeet certain requirements (discussed later),you can claim a refund during the year in-stead of waiting until you file your tax return.

Credit only. The following taxes can onlybe claimed as a credit.

• Tax on fuels you used for nontaxableuses if the total for the tax year is lessthan $750.

• Tax on fuel you did not include in anyclaim for refund previously filed for the taxyear.

Claiming a CreditYou make a claim for credit on Form 4136 and attach it to your income tax return. Donot claim a credit for any amount for whichyou have filed a refund claim.

When to claim a credit. You can claim a fueltax credit on your income tax return for theyear you used the fuels.

CAUTION

!Once you have filed a Form 4136, you cannot file an amended return to show an increase in the number of

gallons of fuel reported on a line of that form.See the following discussion for when you can file a claim on an amended return.

Fuel tax claim on amended return. Youmay be able to make a fuel tax claim on an

amended return for the year you used thefuel. Generally, if you are allowed to file anamended return, you must file it by the later of 3 years from the date you filed your originalincome tax return or within 2 years from thetime you paid the income tax. A return filedearly is considered to have been filed on thedue date.

You can file an amended return to claima fuel tax credit if any of the following apply.

• You did not claim any credit for fuel taxeson Form 4136 for the tax year.

• Your credit is for gasohol blending, asdiscussed in Publication 378.

• Your credit is for a claim group, explained

next, for which you did not previously filea claim on Form 4136 for the tax year.

Claims on Form 4136 (other than for gas-ohol blending) are separated into seven claim groups . Once you file Form 4136 with a claimfor a group, you cannot file an amended re-turn with another claim for that group. How-ever, you can file an amended return with aclaim for another group.

Claim group table. The following tableshows which claims are in each group. Thenumbers in the second column refer to theline numbers on Form 4136. The numbers inthe third column are from the Type of Use Table in the Form 4136 instructions.

For each tax year, you can make only oneclaim for each group.

Example. You file your income tax returnand claim a fuel tax credit. Your Form 4136shows an amount on line 1c for use of gaso-line in a boat engaged in commercial fishing.This is a Group IV claim. You cannot amendyour return to claim a credit for an amount online 1d for use of gasohol in a boat engagedin commercial fishing (Type of Use 4), sincethat is also a Group IV claim. However, if youused the gasohol in an off-highway businessuse, you can amend your return to claim thecredit for that fuel tax because that would bea Group II claim reported on line 1d (Type ofUse 2).

How to claim a credit. As an individual, youclaim the credit on line 64 of Form 1040.Check box “b” on line 64. If you would nototherwise have to file an income tax return,you must do so to get a fuel tax credit.

Group Line No. Type of Use

I 1b, 1d-f, 2b 1

II 1a, 1d-f 2

2a See line instructions

III 1c-f 5, 7

IV 1c-f, 2b 3, 4, 9

V 3c, 7 5, 7

VI 3a-b, 4, 5, 6 See line instructions

VII 2b 10

Page 9

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 10/15

Claiming a RefundYou can file a claim for refund for any quarterof your tax year for which you can claim $750or more. This amount is the excise tax on allfuels used for any nontaxable use during thatquarter or any prior quarter (for which noother claim has been filed) during the taxyear.

If you cannot claim at least $750 at theend of a quarter, you carry the amount overto the next quarter of your tax year to deter-mine if you can claim at least $750 for that

quarter. If you cannot claim at least $750 atthe end of the fourth quarter of your tax year,you must claim a credit on your income taxreturn, using Form 4136. Only one claim canbe filed for a quarter.

Form 8849. You make a claim for a refundon Form 8849. File the claim by filling outSchedule 1 (Form 8849) and attaching it toForm 8849. Send it to the address shown inthe instructions.

When to file a quarterly claim. You mustfile a quarterly claim by the last day of the firstquarter following the last quarter included inthe claim. If you do not file a timely refundclaim for the fourth quarter of your tax year,

you will have to claim a credit for that amounton your income tax return, as discussed ear-lier.

Including the Creditor Refund in IncomeInclude any credit or refund of excise taxeson fuels in your gross income if you includedthe cost of the fuel as an expense deductionthat reduced your income tax liability.

If you use the cash method of accountingand file a claim for refund, include the refundin your gross income for the tax year in whichyou receive the refund. If you claim a credit on your income tax return, include the creditin gross income for the tax year in which you

file Form 4136. If you file an amended return and claim a credit, include the credit in grossincome for the tax year in which you receivethe credit.

Example. Ed Brown, a cash basis fish-erman, filed his 1999 Form 1040 on March1, 2000. On his Schedule C, Ed deducted thetotal cost of gasoline (including $110 of excisetaxes) used in his boat while engaged incommercial fishing operations. Then, onForm 4136, Ed claimed the $110 as a credit.Ed reports the $110 as additional income onhis 2000 Schedule C.

How To Buy Fuel Tax FreeInstead of paying the fuel tax and filing aclaim for credit or refund when the fuel is usedfor a nontaxable use, you may be eligible tobuy it tax free.

Gasoline. Your supplier may be able to sellyou gasoline at a tax-free price only for usein a boat engaged in commercial fishing.

Your supplier may be eligible to claim acredit or refund of the excise tax on the gas-oline sold to you at a tax-free price. Referyour supplier to Credits and Refunds underGasoline in Publication 510, Excise Taxes for 2001, for details.

To buy gasoline at a tax-free price, giveyour supplier a signed certificate identifyingyou and stating how you will use the gasoline.

Table 3. Sample Exemption Certificate

Name and Address of Seller

EXEMPTION CERTIFICATE

(To support vendor’s claim for credit or payment under section 6421 of the Internal Revenue Code)

The undersigned buyer (“Buyer”) hereby certifies the following under penalties ofperjury:

s Buyer has not and will not claim a refund or credit under section 6421 of the InternalRevenue Code for the excise tax on the gasoline to which this certificate relates.

Signature and Date Signed

Printed or Typed Name and Title of Buyer

Name, Address, and Taxpayer Identification Number of Buyer

A. Buyer will use the gasoline to which this cert ificate relates in a boat engaged in

commercial fishing.

C.

1.

This certificate applies to the following (complete as applicable):

If this is a single purchase certificate, check here and enter the numberof gallons of gasoline

2. If this is a certificate covering all purchases, check here .

s If Buyer uses the gasoline to which this certificate relates for a use other thanstated in the certificate, Buyer will so notify the person to whom Buyer gives thiscertificate.

s Buyer understands that the fraudulent use of this certificate may subject Buyer

and all parties making such fraudulent use of this certificate to a fine orimprisonment, or both, together with the costs of prosecution.

B. Buyer bought or will buy the gasoline to which this certificate relates from the abovenamed seller at a price that does not include the excise tax.

You do not need to renew the certificate aslong as the information it contains continuesto be correct. An acceptable exemption cer-tificate is shown in Table 3 .

Schedule C ExampleFrank Carter is a sole proprietor who ownsand operates a fishing boat. He uses the cashmethod of accounting and files his return ona calendar year basis. He keeps his businessrecords with a single-entry bookkeeping sys-tem, similar to the sample record system il-lustrated in Publication 583.

Frank has two crew members, Bill Brownand Joe Green, who are considered self-employed for social security, Medicare, andfederal income tax withholding purposes. Af-ter certain boat operating expenses are paid,the proceeds from the sale of the catch are

divided 75% to Frank and 25% to his crewmembers.Frank figures his net profit or loss from his

fishing business by subtracting his fishingexpenses from his gross income from fishingon Schedule C. He then reports the net profitor loss on line 12, Form 1040.

Schedule C (Form 1040)First, Frank fills in the information required atthe top of Schedule C. On line A, he enters“Fishing” and on line B, he enters 114110, the6-digit business code for commercial fishingshown in the instructions for Schedule C. Hethen completes items C through H.

Part I—IncomeFrank figures his gross income from fishingin Part I.

Line 1. Frank had sales of $60,288 for theyear. This includes all the fish he caught andsold during the year. He enters his total saleson line 1.

Line 3. Because Frank did not have any re-turns and allowances to report on line 2, line3 is the same as line 1.

Line 5. Because Frank did not have any costof goods sold to report on line 4, line 5 is thesame as line 3.

Line 6. Frank's entry of $712 represents a$612 patronage dividend he received from hislocal cooperative and a $100 fuel tax credithe claimed on the 1999 Form 1040 he filedon March 1, 2000. The patronage dividendwas reported to him on Form 1099–PATR,Taxable Distributions Received From Coop- eratives.

Line 7. Frank's gross income from fishingincludes his gross profit from line 5 and hisother income from line 6.

Part II—ExpensesFrank enters his fishing expenses in Part II.

Line 10. Frank used his truck 80% for busi-ness during the year. He spent a total of $505for gas, oil, insurance, tags, repairs, and up-keep. He can deduct $404 (80% × $505), the

Page 10

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 11/15

business portion of these expenses, on line10.

Line 13. Frank enters $6,534 depreciationfrom Form 4562 (not shown).

Line 15. Frank's $3,291 deduction is for in-surance on his business property (80% of histruck insurance is included on line 10). Thededuction is only for premiums that give himcoverage for the year.

Line 16b. Frank had borrowed money to buyhis fishing boat. The interest on this loan was$800 for the year.

Line 20b. His rent for his mooring space was$50 a month, or $600 for the year.

Line 21. He spent $3,600 for boat repairsand $993 for gear repairs for a total cost of$4,593.

Line 22. He spent $1,713 for galley suppliesand $4,751 for bait and ice for a total cost of$6,464.

Line 23. Frank renewed his fishing license.He enters the $35 state fee on this line.

Line 26. Frank paid his crew members totalcrew shares of $10,992 for the year. He doesnot include any amount he paid to himself orwithdrew from the business for his own use.

Line 27. Frank enters the total of his otherfishing expenses on this line. These expensesare not included on lines 8–26. He lists thetype and the amount of the expenses sepa-rately in Part V of page 2 (not shown) andcarries the total entered on line 48 to line 27.His only entry on this line is the $6,367 hespent on fuel for his fishing boat.

Line 28. Frank adds all his expenses listedin Part II and enters the total on this line.

Line 29. He subtracts his total expenses,$40,080 (line 28) from his gross income fromfishing, $61,000 (line 7). Frank has a tentativeprofit of $20,920.

Line 30. Frank did not use any part of hishome for business, so he does not make anentry here.

Line 31. Frank has a net profit of $20,920(line 29 minus line 30). He enters his net profithere, on line 12 of Form 1040, and on line 2,Section A of Schedule SE (Form 1040), notshown.

How To Get Tax HelpYou can get help with unresolved tax issues,order free publications and forms, ask taxquestions, and get more information from theIRS in several ways. By selecting the methodthat is best for you, you will have quick andeasy access to tax help.

Contacting your Taxpayer Advocate. If youhave attempted to deal with an IRS problemunsuccessfully, you should contact your Tax-payer Advocate.

The Taxpayer Advocate represents yourinterests and concerns within the IRS by

protecting your rights and resolving problemsthat have not been fixed through normalchannels. While Taxpayer Advocates cannotchange the tax law or make a technical taxdecision, they can clear up problems that re-sulted from previous contacts and ensure thatyour case is given a complete and impartialreview.

To contact your Taxpayer Advocate:

• Call the Taxpayer Advocate at1–877–777–4778.

• Call the IRS at 1–800–829–1040.

• Call, write, or fax the Taxpayer Advocateoffice in your area.

• Call 1–800–829–4059 if you are aTTY/TDD user.

For more information, see Publication1546, The Taxpayer Advocate Service of the IRS.

Free tax services. To find out what servicesare available, get Publication 910, Guide to Free Tax Services. It contains a list of free taxpublications and an index of tax topics. It alsodescribes other free tax information services,including tax education and assistance pro-grams and a list of TeleTax topics.

Personal computer. With your per-sonal computer and modem, you canaccess the IRS on the Internet at

www.irs.gov. While visiting our web site, youcan select:

• Frequently Asked Tax Questions (locatedunder Taxpayer Help & Ed) to find an-swers to questions you may have.

• Forms & Pubs to download forms andpublications or search for forms andpublications by topic or keyword.

• Fill-in Forms (located under Forms &Pubs) to enter information while the form

is displayed and then print the completedform.

• Tax Info For You to view Internal Reve-nue Bulletins published in the last fewyears.

• Tax Regs in English to search regulationsand the Internal Revenue Code (underUnited States Code (USC)).

• Digital Dispatch and IRS Local News Net (both located under Tax Info For Busi- ness) to receive our electronic newslet-ters on hot tax issues and news.

• Small Business Corner (located underTax Info For Business) to get informationon starting and operating a small busi-

ness.

You can also reach us with your computerusing File Transfer Protocol at ftp.irs.gov.

TaxFax Service. Using the phoneattached to your fax machine, you canreceive forms and instructions by

calling 703–368–9694. Follow the directionsfrom the prompts. When you order forms,enter the catalog number for the form youneed. The items you request will be faxed toyou.

Phone. Many services are availableby phone.

• Ordering forms, instructions, and publi- cations. Call 1–800–829–3676 to ordercurrent and prior year forms, instructions,and publications.

• Asking tax questions. Call the IRS withyour tax questions at 1–800–829–1040.

• TTY/TDD equipment. If you have access

to TTY/TDD equipment, call 1–800–829–4059 to ask tax questions or to orderforms and publications.

• TeleTax topics. Call 1–800–829–4477 tolisten to pre-recorded messages coveringvarious tax topics.

Evaluating the quality of our telephone services. To ensure that IRS representativesgive accurate, courteous, and professionalanswers, we evaluate the quality of our tele-phone services in several ways.

• A second IRS representative sometimesmonitors live telephone calls. That persononly evaluates the IRS assistor and doesnot keep a record of any taxpayer's name

or tax identification number.

• We sometimes record telephone calls toevaluate IRS assistors objectively. Wehold these recordings no longer than oneweek and use them only to measure thequality of assistance.

• We value our customers' opinions.Throughout this year, we will be survey-ing our customers for their opinions onour service.

Walk-in. You can walk in to manypost offices, libraries, and IRS offices

to pick up certain forms, instructions,and publications. Also, some libraries and IRSoffices have:

• An extensive collection of products avail-able to print from a CD-ROM or photo-copy from reproducible proofs.

• The Internal Revenue Code, regulations,Internal Revenue Bulletins, and Cumula-tive Bulletins available for research pur-poses.

Mail. You can send your order forforms, instructions, and publicationsto the Distribution Center nearest to

you and receive a response within 10 work-days after your request is received. Find theaddress that applies to your part of thecountry.

• Western part of U.S.:Western Area Distribution CenterRancho Cordova, CA 95743–0001

• Central part of U.S.:Central Area Distribution CenterP.O. Box 8903Bloomington, IL 61702–8903

Page 11

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 12/15

• Eastern part of U.S. and foreign ad-dresses:Eastern Area Distribution CenterP.O. Box 85074Richmond, VA 23261–5074

CD-ROM. You can order IRS Publi-cation 1796, Federal Tax Products on CD-ROM, and obtain:

• Current tax forms, instructions, and pub-lications.

• Prior-year tax forms, instructions, andpublications.

• Popular tax forms which may be filled inelectronically, printed out for submission,and saved for recordkeeping.

• Internal Revenue Bulletins.

The CD-ROM can be purchased fromNational Technical Information Service (NTIS)

by calling 1–877–233–6767 or on the Internetat www.irs.gov/cdorders. The first releaseis available in mid-December and the finalrelease is available in late January.

IRS Publication 3207, The Business Re- source Guide, is an interactive CD-ROM thatcontains information important to small busi-nesses. It is available in mid-February. Youcan get one free copy by calling1–800–829–3676 or visiting the IRS websiteat www.irs.gov/prod/bus_info/sm_bus/smbus-cd.html.

Page 12

8/14/2019 US Internal Revenue Service: p595--2000

http://slidepdf.com/reader/full/us-internal-revenue-service-p595-2000 13/15

1 1 1 0 0 1 1 1 1

4 1 1 0

1 0 9 9 9 9 9 9 9

FRANK CARTER

FISHING

CAP’N FRANK’S215 Seagull DriveHomet own, OR 973 31

60,288

60,288

60,288712

6 1,0 0 0

6 0 04,5936,464

35

10 ,99 2

6,36740,080

20,920

20,920

40 4

6,534

3,291

8 0 0

1 1

OMB No. 1545-0074SCHEDULE C(Form 1040)

Profit or Loss From Business(Sole Proprietorship)

Partnerships, joint ventures, etc., must file Form 1065 or Form 1065-B.Department of the TreasuryInternal Revenue Service

AttachmentSequence No. 09 Attach to Form 1040 or Form 1041. See Instructions for Schedule C (Form 1040).

Name of proprietor Social security number (SSN)

A Principal business or profession, including product or service (see page C-1 of the instructions) B Enter code from pages C-7 & 8

D Employer ID number (EIN), if anyBusiness name. If no separate business name, leave blank.C

Accounting method:

E

F

Yes NoG

H

Did you “materially participate” in the operation of this business during 2000? If “No,” see page C-2 for limit on losses

If you started or acquired this business during 2000, check here

Income

Gross receipts or sales. Caution. If this income was reported to you on Form W-2 and the “Statutory

employee” box on that form was checked, see page C-2 and check here

11

22 Returns and allowances

33 Subtract line 2 from line 1

44 Cost of goods sold (from line 42 on page 2)

5Gross profit. Subtract line 4 from line 35

6Other income, including Federal and state gasoline or fuel tax credit or refund (see page C-2)6

7 Gross income. Add lines 5 and 6 7

Expenses. Enter expenses for business use of your home only on line 30.

8

21Repairs and maintenance21

Advertising8

22Supplies (not included in Part III)22

Bad debts from sales or

services (see page C-3)

9

23

9

Taxes and licenses23

10

Travel, meals, and entertainment:24

Car and truck expenses

(see page C-3)

10

24a

11

Travela

Commissions and fees11

12Depletion12

Meals and

entertainment

b