u.s. global investors · 2014-05-14 · the us dollar compound annual rates 1971 - 2008-2.70% vs...

TRANSCRIPT

www.usfunds.com1.800.US.FUNDS

U.S. Global InvestorsSearching for Opportunities, Managing Risk

November 201010-702

Post-Election Update How Will the Results Impact the Markets?Ian McAvity,Author, Deliberations on World Markets

Frank Holmes,CEO and Chief Investment Officer,U.S. Global Investors

www.usfunds.comNovember 2010 10-702 22

Fund Recognition

Winner of 26 Lipper Fund Awards and certificates since 2000

Investment leadership results

in performance

www.usfunds.comNovember 2010 10-702 33

Government Policy Model — Precursor for Change

Ian McAvity’s

DELIBERATIONSOn World Markets

Technical analysis & other perspectives on the major world markets for stocks /bonds /currencies /precious metals

Ian McAvity Toronto, Canada

US Global Web cast 3-Nov-10

Confused? You’re not alone…

As confused as a herd of goats on Astroturf ?

Stock Market

Dollar Gold

The following comments are intended to give bigger

picture perspectives on trends, but are NOT intended as trading advice. Consult your own professional advisors

before acting on any ideas expressed here today.

S&P from 1900 Stocks Always Go Up

S&P Composite (Cowles early data)

1900 - 2020

#3

#2

#1

Jun-49

Mar-00

Aug-82

Jan-66

Oct-21

Sep-29

0.500

1.000

1.500

2.000

2.500

3.000

3.500

Jan-

00

Jan-

10

Jan-

20

Jan-

30

Jan-

40

Jan-

50

Jan-

60

Jan-

70

Jan-

80

Jan-

90

Jan-

00

Jan-

10

Jan-

20

Logs of

price

In the long termStocks ‘always’ go up

But sometimes you have to wait up to 20 years…

22-Oct-10

Secular Uptrends from 1900: 38% of the timeS&P Composite Secular Trends

1900 - 2009

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

3.5000

Jan-

00

Jan-

10

Jan-

20

Jan-

30

Jan-

40

Jan-

50

Jan-

60

Jan-

70

Jan-

80

Jan-

90

Jan-

00

Jan-

10

Jan-

20

1921 / 1929

1949 / 1966

1982 / 2000

Secular UptrendsAverage BEAR Cycle-20% over 34 Weeks

(1949-1966 & 1982-2000)

Logs of

price

"Other" Secular periodsAverage BEAR Cycle-32% over 75 Weeks

(1900/21, 1966/82 & 2000/16?) (Excluding 1929/42)

24-Sep-10

Secular Others from 1900:

62% of the timeS&P Composite"Other"

Secular Phases

62% of the time1900 / 2010

Oct-07

0.000

0.500

1.000

1.500

2.000

2.500

3.000

3.500Ja

n-00

Jan-

10

Jan-

20

Jan-

30

Jan-

40

Jan-

50

Jan-

60

Jan-

70

Jan-

80

Jan-

90

Jan-

00

Jan-

10

Jan-

20

Average BEAR Cycle-32% over 18 Months

(Excluding 1929/32)

Average BEAR Cycle -20% over 7 Months

(1949-1966 & 1982-2000)

Logs of

price22-Oct-10

Political Cycle Gridlock, Nastiness &

a lurch to the right looming?

Politics…Derived from

POLY – meaning MANY&

TICS – Bloodsucking insects

Presidential Election Cycles since 1953

Mid-Term Years (2010) S&P Down 6 of 14 times

Pre-Election Years (2011) S&P Down 0 of 15 times

Q4-10 to Q2-11 are the best 3 quarters of a

Presidents 16 quarter term

Average Qtrly change 1949/2010

31-Mar-09

31-Dec-1031-Mar-11

30-Jun-11

30-Jun-10-4

-2

0

2

4

6

8

10D

ec-0

8M

ar-0

9Ju

n-09

Sep-

09D

ec-0

9M

ar-1

0Ju

n-10

Sep-

10D

ec-1

0M

ar-1

1Ju

n-11

Sep-

11D

ec-1

1M

ar-1

2Ju

n-12

Sep-

12D

ec-1

2

1949 / 2010 Presidential Cycles

Average Quarterly % ChangeS&P 500

31-Mar-10 1.03 Down 9 of 1630-Jun-10 -2.82 Down 9 of 1630-Sep-10 0.06 Down 6 of 1631-Dec-10 7.89 Down 2 of 1531-Mar-11 7.60 Down 1 of 1530-Jun-11 5.63 Down 3 of 1530-Sep-11 2.09 Down 5 of 1531-Dec-11 2.48 Down 5 of 1531-Mar-12 0.68 Down 5 of 15

24 Dn of 48

6 Dn of 45

15 Dn of 45

S&P 500 Quarterly % Change Average over 16 Cycles since 1949

Mid Term & Pre-election Years

Pre-Election YearMost Bullish

This cycle crashed in the bullish period and rallied in the bearish period…

This cycle 2007/10

Oct-07

Feb-09

Apr-10

1952-2007 Average

70

100

130

160

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Election YearBulish

Pre-Election YearMost Bullish

Mid Term YearMost Bearish

Post Election YearBearish

Average 1980-1999(Blue- Secular Ups)

Average 1964-1983(Green - Secular Others)

Average Presidential

Cycles

SPX Seasonals

+8.8%

-4.7%

+7.9%-5.4%

-8.2%

+1.5%2010 Seasonals have been upside down.

2010 Index % Added

-3.7%

+5.9%

+2.9%

Might thenext 2

becomethe worst?

Chart courtesy of Bianco Research LLC

+3.7%

XX XX XXX

7 of 10 Months = X

HGX IXBK & SPX Topped & failing30-Apr-10

100

1000Se

p-02

Mar

-03

Sep-

03

Mar

-04

Sep-

04M

ar-0

5

Sep-

05M

ar-0

6

Sep-

06M

ar-0

7

Sep-

07

Mar

-08

Sep-

08M

ar-0

9

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Housing Topped July 05

Regional Banks Topped

Dec 06S&P Topped

Oct 07

HGXHousing

Index

IXBKNasdaq

Bank Index

SPXSP 500 Index

29-Oct-10

Weekly Average PricesRebased for visual comparability

A

B

C

D

ABS Issuance Courtesy Jim Bianco Research Chart courtesy of Jim BiancoBianco Research LLC

BKX – 24 Money Center Banks

BKX - BANK Stock Indexwith 40wk MAs

15-Sep-08

14-Jul-08

Feb-07

Oct-07

1.200

1.300

1.400

1.500

1.600

1.700

1.800

1.900

2.000

2.100

2.200D

ec-0

2

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

(Log

s of

Pric

e)

2.2000

2.3000

2.4000

2.5000

2.6000

2.7000

2.8000

2.9000

3.0000

3.1000

3.2000SPX

SP 500 Index

1-Nov-10

Worrisome DivergenceUnderway

Shades of 2007?

Euro BanksEuro Banks Index SX7P.Z

21-Oct-09

50

100

150

200

250

300

350

400

450

500

550Ju

n-02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Even worse looking?

Visa & MasterCard broke sharply last week

and are well below their April/May

highs ---

Any further weakness might

be an early warning of tapped out

consumers pre-Christmas?

The conflict…

-Case for the Bulls: Powerful seasonal time of year and the

Presidential Election Cycle …

But both have been upside down from their ‘normal’ behavior patterns.

- - - - I’ll remain skeptical, cautious and worry

that Housing & Financials are giving an early warning of downside risks that

may overwhelm the bulls.

The FED weather update

Low Bridge surprise…

Just when you think the worst of it is over, and you see a little light at the end of that tunnel......

How’s your day going so far…Too many bulls in the sunshine?

Forex & Gold Post Bretton WoodsBP, US$, Euro/DM & Yen vs. GOLD

(Logs of Monthly Average)

US$/oz

DM-Euro/oz

BP/oz

Yen/oz

0.500

1.000

1.500

2.000

2.500

3.000

3.500

Jan-

46

Jan-

51

Jan-

56

Jan-

61

Jan-

66

Jan-

71

Jan-

76

Jan-

81

Jan-

86

Jan-

91

Jan-

96

Jan-

01

Jan-

06

Jan-

11

Jan-

16

2.500

3.000

3.500

4.000

4.500

5.000

5.500

1971 / 1980

2001 / 2015?

Fiat Currenciesvs. Gold

Lose value over time(Pre & Post Bretton Woods)

24-Oct-10

Demise of UK Pound as Reserve Currency£4.24

Sep-31

1-Oct-10£827

Jan-80£322.4

July 1864$12.98

Mar-1985$1.06

Sep-49

Aug-14

1.0

10.0

100.0

1000.0

Nov

-00

Nov

-10

Nov

-20

Oct

-30

Oct

-40

Sep-

50

Sep-

60

Sep-

70

Aug

-80

Aug

-90

Jul-0

0

Jul-1

0

Jul-2

0

0.1

1.0

10.0

100.0

British Poundvs. US$

British Poundvs. Gold

British Pound (Wkly Avg)

Long Term DECLINE vs. US$ & Gold

1860 - 2010

$5.20/$3.15 Range

Brown sells UK Gold $275 Avg

$2.05 / $1.35 Range

Ian McAvity’s DELIBERATIONS on World Markets

1860-1900

Post Bretton Woods Aug 1971 to date

Dollar vs DM/Euro 1971 - 2010US$ vs. Euro (DM pre-1999)

with 40wk MA

Nov-051.1667

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Dec

-70

Dec

-72

Dec

-74

Dec

-76

Dec

-78

Dec

-80

Dec

-82

Dec

-84

Dec

-86

Dec

-88

Dec

-90

Dec

-92

Dec

-94

Dec

-96

Dec

-98

Dec

-00

Dec

-02

Dec

-04

Dec

-06

Dec

-08

Dec

-10

Dec

-12

The US DollarCompound annual rates

1971 - 2008-2.70% vs Euro/DM

-3.74% vs Yen

With 30 Year US Treasury yield of 3.74% pre-tax,those long term currency depreciation rates

make you wonder what Japanese buyers are thinking when they buy Long-dated US T-Bonds.

22-Oct-10

Dollar 2000–2010 basing?US Dollar Index (DX)

with 40 wk MA

60

70

80

90

100

110

120

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

US$ Bottomingto becomeBLHiGF ?

Gold & Dollar 2000 - 2010Logs of Gold & DX Index (Weekly Average Values)

1.7500

1.8000

1.8500

1.9000

1.9500

2.0000

2.0500

2.1000

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

2.4000

2.5000

2.6000

2.7000

2.8000

2.9000

3.0000

3.1000

DXY Index BlueGold INVERTED Red

US$ & Gold NOT

Agreeing

US$ & Gold NOT

Agreeing

29-Oct-10

US$ Vs. GoldRising vs. Paperbut not vs. GoldBLHiGF ?

US$ vs. Euro/DM & Yen from 1967The US Dollar Major Declines 1968 - 2010with Intervening Rebounds

US Dollar vs. Yen#4

Apr'95

#3 Dec'87

Oct-00

Mar-85

#2Dec'79

#1Jul'73

#5?Apr'08 (Euro)

Coming soon Yen?1.800

1.900

2.000

2.100

2.200

2.300

2.400

2.500

2.600

2.700D

ec-6

6

Dec

-70

Dec

-74

Dec

-78

Dec

-82

Dec

-86

Dec

-90

Dec

-94

Dec

-98

Dec

-02

Dec

-06

Dec

-10

Dec

-14

Logs of FxRates

US Dollar vs. Euro (DM prev)

22-Oct-10

The US DollarCompound annual rates

1971 - 2008-2.70% vs Euro/DM

-3.74% vs Yen

Currency HistoryModern history of fiat currency

£ s dto

¥ € $No… they make no ¢

How many versions of Pesos, Marks, Francs & Lira

does it take to learn from history?

They all lose purchasing power over time

Zim Inflation $100 Trillion (2008)

From a South African Public Toilet

Copper from 1900Copper from 1900

London - RedNY - Blue(US$/lb)

Mar-58

Mar-56

Apr-46

Dec-08

Jul-08

0.010

0.100

1.000

10.000

Jan-

00

Jan-

10

Jan-

20

Jan-

30

Jan-

40

Jan-

50

Jan-

60

Jan-

70

Jan-

80

Jan-

90

Jan-

00

Jan-

10

Jan-

20

"Secular Uptrend"Copper 1932 to 19744 1/2 cents to $1.50

?

?

1949 - 56 Breakout from a 50 Year Range, gave back 50% in two years before

continuing the new secular uptrend.

2000 - 06 Broke out of a 40 year range

22-Sep-10

A

B

S&P and SP-GSCI-22Sep10SP-GS Commodity Index & The S&P 500with 65 Wk MAs

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

3.30

Dec

-69

Dec

-73

Dec

-77

Dec

-81

Dec

-85

Dec

-89

Dec

-93

Dec

-97

Dec

-01

Dec

-05

Dec

-09

Dec

-13

Running together ?

Retail & Custom products largely based

on 1980 - 2002

Non-corelation history?

SP-GS Commodity Index

Logs

S&P 500 Index

Opposite Harmony

1972 - 1982

23-Sep-10

Non-correlated history

S&P and SP-GSCI-22Sep10SP-GS Commodity Index & The S&P 500with 65 Wk MAs

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3.10

3.30

Dec

-69

Dec

-73

Dec

-77

Dec

-81

Dec

-85

Dec

-89

Dec

-93

Dec

-97

Dec

-01

Dec

-05

Dec

-09

Dec

-13

Running together ?

Retail & Custom products largely based

on 1980 - 2002

Non-corelation history?

SP-GS Commodity Index

Logs

S&P 500 Index

Opposite Harmony

1972 - 1982

23-Sep-10

Non-correlated history

Savings Rate & Debt/GDP Ratio

Debt/GDP Ratio (scale left - red) US Personal Savings Rate (scale right - blue)

DEBT/GDP Ratio

Mar-521.30

3.55

1.65

Mar-696.9%

SAVINGS RATE

Mar-082.7%

Mar-556.4%

Dec-8111.9%

Jun-7512.5%

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00D

ec-5

0

Dec

-54

Dec

-58

Dec

-62

Dec

-66

Dec

-70

Dec

-74

Dec

-78

Dec

-82

Dec

-86

Dec

-90

Dec

-94

Dec

-98

Dec

-02

Dec

-06

Dec

-10

Dec

-14

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1982 to 2007Personal Savings Collapsed

& Debt/GDP exploded

1966 to 1982

1951 - 1981

Savings & S&P from 1959S&P (logs) and US Savings Rate (3 Mo MA)

Jul-10

0

2

4

6

8

10

12

14D

ec-5

8

Dec

-62

Dec

-66

Dec

-70

Dec

-74

Dec

-78

Dec

-82

Dec

-86

Dec

-90

Dec

-94

Dec

-98

Dec

-02

Dec

-06

Dec

-10

Dec

-14

1.500

2.000

2.500

3.000

3.500

1958-86 High SavingsRate

1999-2007NO Savings

1982-1999Stocks & Debt

SoaredSavingsSpent

S&P 500

1966-82

1998-2014?

S&P and Debt/GDP Ratio from 1950S&P 500 (Logs of price, scale left)

US DEBT/GDP Ratio (logs, scale right)

Mar-521.30

2.63Jun-00

DEBT/GDPRatio

---Crazy

2001 to 2009

Mar-093.76

Dec-811.65

1.2000

1.7000

2.2000

2.7000

3.2000D

ec-5

0

Dec

-54

Dec

-58

Dec

-62

Dec

-66

Dec

-70

Dec

-74

Dec

-78

Dec

-82

Dec

-86

Dec

-90

Dec

-94

Dec

-98

Dec

-02

Dec

-06

Dec

-10

Dec

-14

0.1000

0.3000

0.5000

0.7000

1982 to 2001Stocks soared

Personal Savings Collapsed

& Debt/GDP exploded

1966 to 1982

1952 to 1965

S&P 500

Debt / US at Waterfall edge?Chart Courtesy of Bianco Research LLC

Deficits don’t matter ?

Who’s going to bail out Uncle Sam? Hu ?

Foreign Reserves

China* $2,648Russia 458Saudi Arabia 435Taiwan 381South Korea 290Brazil 274India 268Hong Kong 266Singapore* 215Thailand 151

$5,386The Economist

22-Oct-10

DJI & DeflatedDJIA in Nominal & Constant Dollars(Deflated by US CPI All Urban Consumers Index)

(Logs of price levels)

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500O

ct-2

8

Oct

-38

Oct

-48

Oct

-58

Oct

-68

Oct

-78

Oct

-88

Oct

-98

Oct

-08

Oct

-18

0.300

0.800

1.300

1.800

2.300

2.800

3.300

3.800

Erosion of purchasing power illustrated by the widening gap between the two regression lines

DJIA in Nominal US$

DJIA in Constant US$based on US CPI

22-Sep-10

Gold Current & Constant$

1.000

1.500

2.000

2.500

3.000

Oct

-28

Oct

-38

Oct

-48

Oct

-58

Oct

-68

Oct

-78

Oct

-88

Oct

-98

Oct

-08

Oct

-18

-0.200

0.300

0.800

1.300

1.800

GOLD in Nominal & Constant US$(Deflated by US CPI All Urban Consumers)

Logs of price

1980 Gold Top in inflation adjusted US$ was $2388

(Sep-10)

Goldin Constant US$based on US CPI

Goldin Nominal US$

based on US CPI

22-Sep-10

Bubble top unlikely without a new high

in nominal & constant $

US Gross Debt & Gold Reserves

US Gross Federal Debt & US Gold Reserves Mar-66 Sep-71 Mar-2010

Mar-2014 Est

US Gross Federal Debt ($ bil) $321 $421 $12,825 $18,350US Gold Reserves (mil oz) 401.9 291.6 261.6 261.6

Valued at: $35.00 $41.22 $1,150 $1,200

Gold value ($ bil) $14 $12 $301 $314

Debt / Gold Reserves Ratio 23 35 43 58

$2,131 $3,050Gold price to revert to 23x

Debt/Gold multiplier

In 1971, US Debt growth prompted a run on US Gold and Nixon closed the gold window. The US Debt/Gold Reserves ratio had

increased 54% from 23x to 35x since 1966.

Gold Now vs. Then

$732May-06

$1436Dec'74

$5479Jan'80

$786Aug'76

100

1000

10000

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

100

1000

10000

Jan 1970 - $34.85 (Wkly Avg)= Apr 2001 $259 (Wkly Avg)

GOLD: "Now vs. Then" The Post-2000 Run

vs 1968-1980

Rebasing Jan. 1970 to Apr. 2001

29-Oct-10$1358

Apr

-201

1 ?

Oct'78DollarCrisis(Low)

May'10EuroCrisis

(UpsideBreakout)

Euro/DM Crisis Oct 1978 and Gold Rush3-Nov-78

0.700

0.800

0.900

1.000

1.100

1.200

Dec

-75

Dec

-76

Dec

-77

Dec

-78

Dec

-79

Dec

-80

Dec

-81

Dec

-82

100

1000

US$ Crisis Swaps & Intervention to stop it

Euro/DMvs. US$

GOLD$243

to $193then up to $850

B

A

Oct’78: US$ intervention bottom – Gold then ran $160 to $850

Logs of Gold & DX Index (Weekly Average Values)

1.8500

1.9000

1.9500

2.0000

2.0500

2.1000

2.1500

2.2000

2.2500

Dec

-76

Dec

-77

Dec

-78

Dec

-79

Dec

-80

Dec

-81

Dec

-82

Dec

-83

Dec

-84

Dec

-85

Dec

-86

Dec

-87

Dec

-88

2.1000

2.2000

2.3000

2.4000

2.5000

2.6000

2.7000

2.8000

2.9000

DXY Index - Blue(scale magnified)

Gold - Red

US$ & Gold NOT Agreeing

US$ & Gold NOT

Agreeing

1978/80Dollar Bottoming

while Gold ran from

$160 to $850

Gold and Interest Rates 1976 - 1982Interest Rates 1976 - 82

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00D

ec-7

5

Dec

-76

Dec

-77

Dec

-78

Dec

-79

Dec

-80

Dec

-81

Dec

-82

100

1000Series1Series2Series4Series6

T-Bills - Green10 Yr US - BlackBaa Bonds - RedGOLD - Blue

Jun'78 to Jun'80

T-Bill Yields above 10 Yr

Both above 9%As Gold

Crosses $400

Gold “still” lousy Barron’s Oct’09

2.800

2.900

3.000

3.100

3.200

3.300

3.400

3.500

3.600D

ec-0

2

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

S&P 500 (red) & Comex Gold (blue)Weekly Averages

rebased to Dec 31, 2002Logs of price for visual comparability

29-Oct-10

GOLD

S&P 500

•Deflationary crash •Hyper-inflationary

"Gold Is Still a Lousy Investment!"Barron's Insight - 4-Oct-09

Does "STILL" exclude the past 7 years?

Gold Breakout RunsThe Gold Bull Comex - Logs of Price Weekly

Key Breakout Runs

2.300

2.500

2.700

2.900

3.100

3.300

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Logs

of P

rice

A

B

C

D?

Possibilitiesimplied

from B & C?

$1459 ?2-Apr-10

$1584?7-May-10

Didn't happen in terms of time.

29-Oct-10

$300/$328

$428/$454

$726/$732

$1020/$1030

Low DateLow Price High Date

High Price Wks

% Change

2-Aug-02 300 2-Apr-04 433 A 87 45% 300/328 Breakout

15-Jul-05 418 12-May-06 732 B 43 75% 428/454 Breakout

29-Jun-07 641 21-Mar-08 1034 C 38 61% 726/732 Breakout

So far…10-Jul-09 905 15-Oct-10 1388 D 66 53% 1020/1030 Breakout

IF Repeat of A 11-Mar-11 $1,308 87 45%

IF Repeat of B 7-May-10 $1,584 43 75%

IF Repeat of C 2-Apr-10 $1,459 38 61%

The Breakout Runs (Comex price)

50 Day MA vs. 200 Day MA

GOLD50 DMA Below 200 DMA in Red

100

1000

Jun-

80Ju

n-82

Jun-

84Ju

n-86

Jun-

88Ju

n-90

Jun-

92Ju

n-94

Jun-

96Ju

n-98

Jun-

00Ju

n-02

Jun-

04Ju

n-06

Jun-

08Ju

n-10

Jun-

12

100

1000

29-Oct-10

Still on 4th ‘signal’ since 200111-Feb-09 at $944.50

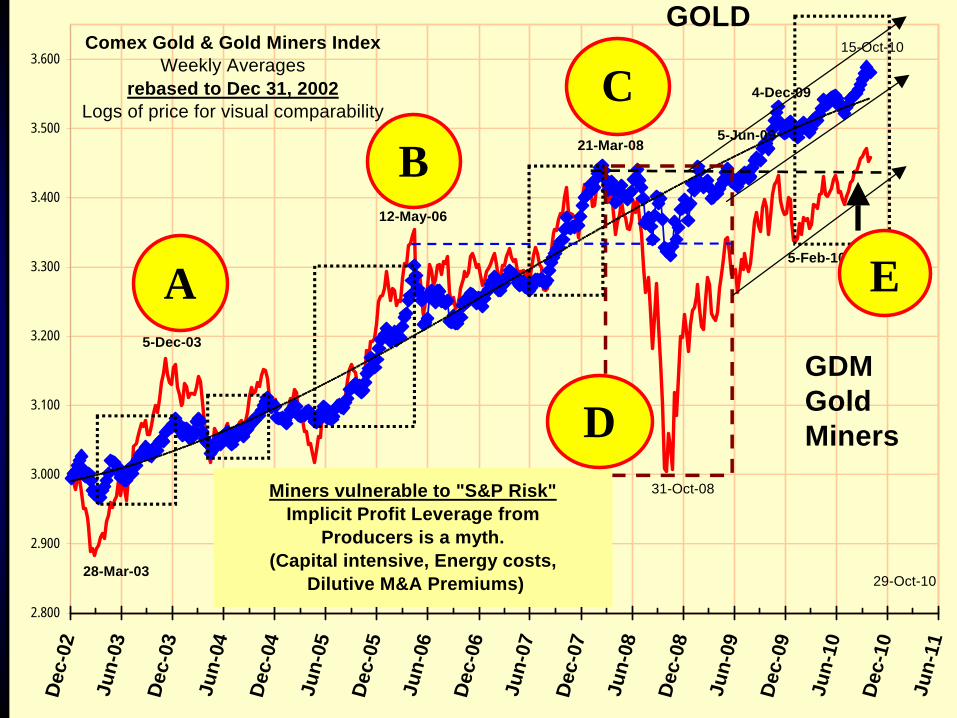

Gold and GDM Gold & GDM from Dec’024-Dec-09

21-Mar-085-Jun-09

15-Oct-10

12-May-06

5-Dec-03

31-Oct-08

5-Feb-10

28-Mar-03

2.800

2.900

3.000

3.100

3.200

3.300

3.400

3.500

3.600D

ec-0

2

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Comex Gold & Gold Miners Index Weekly Averages

rebased to Dec 31, 2002Logs of price for visual comparability

29-Oct-10

GOLD

Miners vulnerable to "S&P Risk"Implicit Profit Leverage from

Producers is a myth.(Capital intensive, Energy costs,

Dilutive M&A Premiums)

GDMGold MinersD

C

B

A E

Gold and GDM/Gold Sh/Met RatioGold Weekly& GDM Miners/Metal Ratio

Bre-XMay-96

1.500

1.700

1.900

2.100

2.300

2.500

2.700

2.900

3.100

Dec

-67

Dec

-71

Dec

-75

Dec

-79

Dec

-83

Dec

-87

Dec

-91

Dec

-95

Dec

-99

Dec

-03

Dec

-07

Dec

-11

Logs

of P

rice

Leve

l

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Gold Miners vs. Metal Ratio

Gold Weekly, logs of rice

with 52wk MA

B

A C

Gold vs Gold Shares from 1934

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

Dec

-33

Dec

-38

Dec

-43

Dec

-48

Dec

-53

Dec

-58

Dec

-63

Dec

-68

Dec

-73

Dec

-78

Dec

-83

Dec

-88

Dec

-93

Dec

-98

Dec

-03

Dec

-08

Dec

-13

0.000

0.500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500GDM (pre'93 TSEG-US$)

Gold Price PM Fix

Shs Metal Ratio US$

Poly. (Shs Metal Ratio US$)

1986 to 2008Range

1968 to 1980Run

Logsofprice

1-Oct-10

Gold Miners /Metal Ratio(scale right - not log scale)

Gold (blue) & Gold Miners (US$) (red)

from 1934

Shares LaggedMetal

1968 / 80

Gold and GDM/Gold Sh/Met RatioComex Gold (logs of price) & GDM Shares vs. Metal Ratio

1.97601.9996

1.700

1.900

2.100

2.300

2.500

2.700

2.900

3.100Se

p-93

Sep-

94

Sep-

95

Sep-

96

Sep-

97

Sep-

98

Sep-

99

Sep-

00

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

0.60

1.00

1.40

1.80

2.20

2.60

3.00

3.40

Gold Shares Vs. Metal Ratio

(Not semi-log scaled)

Comex Gold Near Active

29-Oct-10

$350

$250

$425

$725

$250

A

DC

B

$1000

D

E

$420

E

$1380

$1200F

F

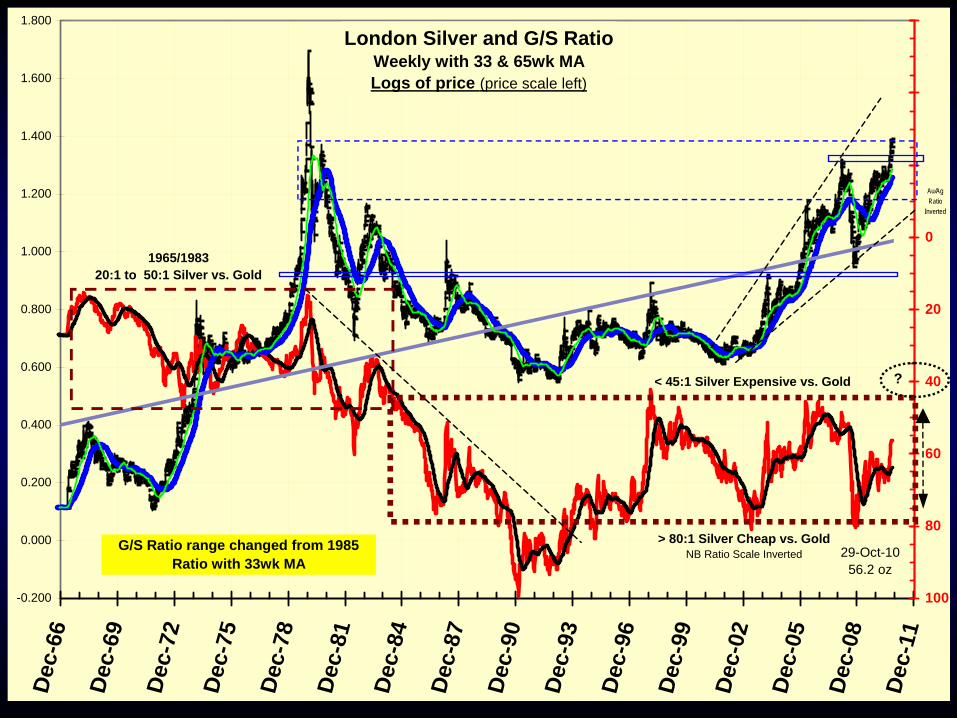

Silver and Ag/Au RatioLondon Silver and G/S Ratio Weekly with 33 & 65wk MALogs of price (price scale left)

-0.200

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

Dec

-66

Dec

-69

Dec

-72

Dec

-75

Dec

-78

Dec

-81

Dec

-84

Dec

-87

Dec

-90

Dec

-93

Dec

-96

Dec

-99

Dec

-02

Dec

-05

Dec

-08

Dec

-11

-60

-40

-20

0

20

40

60

80

100

< 45:1 Silver Expensive vs. Gold

> 80:1 Silver Cheap vs. GoldNB Ratio Scale Inverted

1965/1983 20:1 to 50:1 Silver vs. Gold

29-Oct-1056.2 oz

G/S Ratio range changed from 1985Ratio with 33wk MA

?

Au/Ag Ratio

Inverted

Heli Ben at work…

Dow Gold Ratio from 1885DJIA Vs. Gold

from 1885

7.1xMar-09

43.7xSep'99

27.7xFeb'66

18.3xSep'29

Jan'801.0x

Aug'961.0x

Jul'322.0x

1

10

100

Apr

-01

Apr

-09

May

-17

May

-25

May

-33

May

-41

May

-49

May

-57

May

-65

Jun-

73

Jun-

81

Jun-

89

Jun-

97

Jun-

05

Jun-

13

From Jan 1885Weekly

27Oct-108.4 Oz

DJ 11,126Gold $1,324

Median Ratio1968-2009 = 9.8x1900-2009 = 5.5x

2 or3 Oz?

Gold vs. Dow from 1980

Daily DJI / Gold Ratioinverted to trend with Gold

with 200 day MA1980 - 2010

19-Oct-87

7.0 Oz6-Mar-09

1.1 Oz22-Jan-80

16.0 Oz12-May-06

44.64 Oz25 Aug 99

21.1 Oz4-Feb-03

1

10

100

Nov

-79

Nov

-81

Nov

-83

Nov

-85

Nov

-87

Nov

-89

Nov

-91

Nov

-93

Nov

-95

Nov

-97

Nov

-99

Nov

-01

Nov

-03

Nov

-05

Nov

-07

Nov

-09

Nov

-11

The EquityBubble M k t

40

20

6 Oz

8.4 Oz27-Oct-10

2 Oz

Comex Gold Dec

Conclusions - 1

S&P 500 ? Despite this cyclical bullish phase,

I’m nervous about Housing & Financialsdiverging again, and choose to be cautious.

I would put a greater weight on capital preservation…(Bear in mind I’m NOT a short term trader…)

In a big picture sense, I expect to see the March 2009 lows tested

before we see the October 2007 highs again.

Conclusions - 2Gold & Silver:

More to go in this leg, in my view, but we will need a corrective / digestive phase to sustain the orderly trend of the past decade.

A “disorderly run” does lie ahead in my view, and could occur almost any time.

Stick with the secular uptrend if you’re a concerned investor as opposed to a shorter term trader.

Silver & Junior Miners firming up relative to gold tells me we’re getting to the later stages of this leg,

but too many people calling tops…

Silver is becoming poor man’s gold,or gold on steroids… but volatility works both ways…

Conclusions - 3

The Dollar & US Bond Market ?

I suspect foreign holders may flex some muscleon both the US$ and the long end of the bond market.

Great expectations that US$ Index can avoid breaking 70 may get a downside surprise,

and then get ‘that’ rebound…Forget about seeing the old 2000 top around 120,

not likely in my lifetime…

If 30-Year Treasury Bond prices break below 129, that would be a loud warning bell….

30 Yr Bond price (136/129 range?)

A break below 129 could be a bellwether

of a major trend turn

CNBC &

Politics &

Wall Street

Patience My Ass, I’m Going to Kill Something !

‘Opportunity’ rarely

happens at your

convenience

Bad buying causes losses

www.usfunds.comNovember 2010 10-702 64

MFEA Awards-Brand Recognition

64

www.usfunds.comNovember 2010 10-702 6565

Come Visit Us at…

Facebook: www.facebook.com/usfunds

Twitter: www.twitter.com/usfunds

Frank Talk: www.usfunds.com/franktalk

Investor Alert: www.usfunds.com/alert

www.usfunds.comNovember 2010 10-702 66

Disclosures

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

The S&P 1500 Composite is a broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, S&P 500, and the S&P 600. The index was developed with a base value of 100 as of December 30, 1994. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The NASDAQ Bank Index is a broad-based capitalization-weighted index of domestic and foreign common stocks of banks that are traded on the Nasdaq National Market System as well as the SmallCap Market. The PHLX Housing Sector Index is a modified capitalization-weighted index currently composed of members whose primary lines of business are construction, development, support and sales relating to the residential housing industry. The KBW Bank Index is a modified capitalization- weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions. The index is intended to reflect the evolving financial sector. The STOXX 600 Banks (Price) Index (SX7P) is a capitalization- weighted index which includes European companies that are involved in the bank sector. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P GSCI Spot index tracks the price of the nearby futures contracts for a basket of commodities. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The NYSE Arca Gold Miners Index (GDM) is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The index benchmark value was 500.0 at the close of trading on December 20, 2002. Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

The following securities mentioned in the presentation were held by one or more of U.S. Global Investors’ Funds as of 9/30/2010: Market Vectors Gold Miners ETF, SPDR Gold Shares, Market Vectors Junior Gold Mine ETF, Walmart.

Although Lipper makes reasonable efforts to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Lipper. Users acknowledge that they have not relied upon any warranty, condition, guarantee, or representation made by Lipper. Any use of the data for analyzing, managing, or trading financial instruments is at the user's own risk. This is not an offer to buy or sell securities.

66