us auto industry - bbvaresearch.com · disruptive trends transforming the auto industry source:...

TRANSCRIPT

AUTO

INDUSTRY

US

1Q 2018

CHARTBOOK

Key Messages

2

1. Economic fundamentals and financial conditions remain

supportive of demand

2. However, increasing off-lease returns will continue to exert

downward pressures on sales and prices of new vehicles

3. The structural shift towards light-trucks has kept transaction

prices high, supporting profitability

4. Sales of electric vehicles hit a record in 2017; a substitution

effect between hybrids and plug-ins is taking place

5. Autonomous driving, shared mobility, connectivity and

electrification will transform the industry in the following years

SALES

Sales

Source: BBVA Research and Haver Analytics 4

U.S. Total light weight vehicle sales (SAAR, million units)

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Total Domestic Imported

Feb-18 = 17.1 Avg. 2004-2007 = 16.6

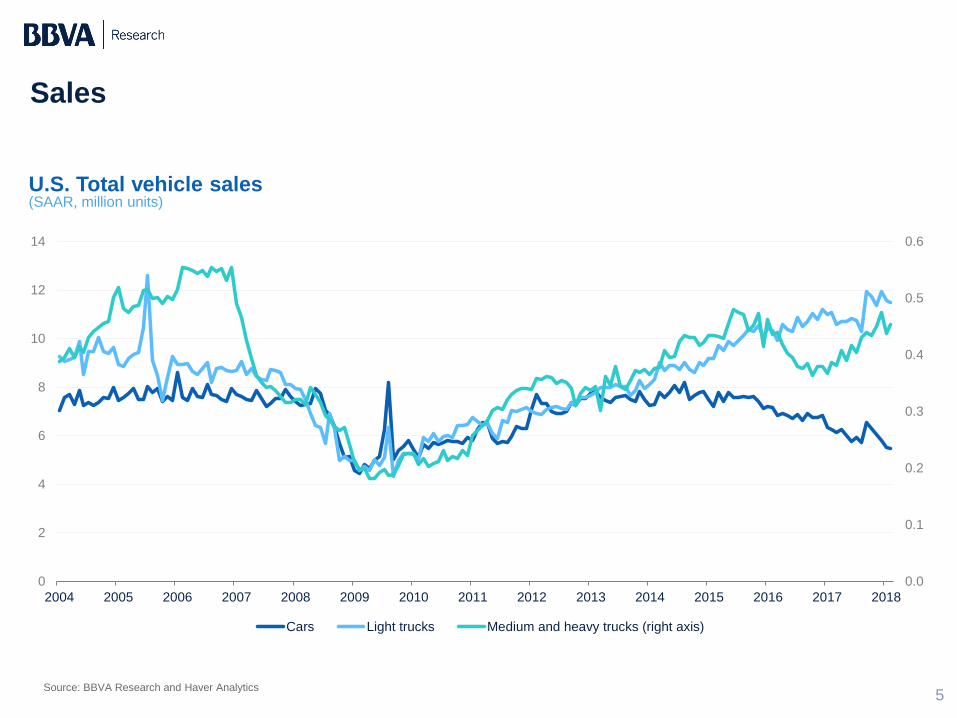

Sales

Source: BBVA Research and Haver Analytics 5

U.S. Total vehicle sales (SAAR, million units)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0

2

4

6

8

10

12

14

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Cars Light trucks Medium and heavy trucks (right axis)

Sales

Source: BBVA Research and Haver Analytics 6

U.S. Total vehicle sales (Share of total)

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Cars Trucks

Sales

Source: BBVA Research and Bloomberg 7

U.S. Auto dealers: revenue (Year-over-year % change, 4Q moving average)

0

5

10

15

20

25

New Vehicle Sales Used Vehicle Sales Parts & Service

Sales

Source: BBVA Research and Haver Analytics 8

U.S. Domestic auto inventory/sales ratio (Seasonally adjusted)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Sales

Source: BBVA Research and Bloomberg 9

U.S. Sales growth by brand and market share (2017, yoy % change and % market share)

-10

-5

0

5

-5 0 5

Q3

Q4

Share

0.5

1.0

1.5

2.0

Brand

Audi

BMW

Land Rover

Mazda

Mercedes-Benz

Mini

Mitsubishi

Porsche

VolksWagen

Volvo

-10

-5

0

5

-5 0 5

Q3

Q4

Share

5

10

15

Brand

Fiat Chrysler

Ford

GM

Hyundai

Kia

Subaru

Toyota

Prices

Source: BBVA Research and Haver Analytics 10

U.S. Consumer price index: cars and trucks (yoy % change)

-15%

-10%

-5%

0%

5%

10%

15%

20%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

New Used

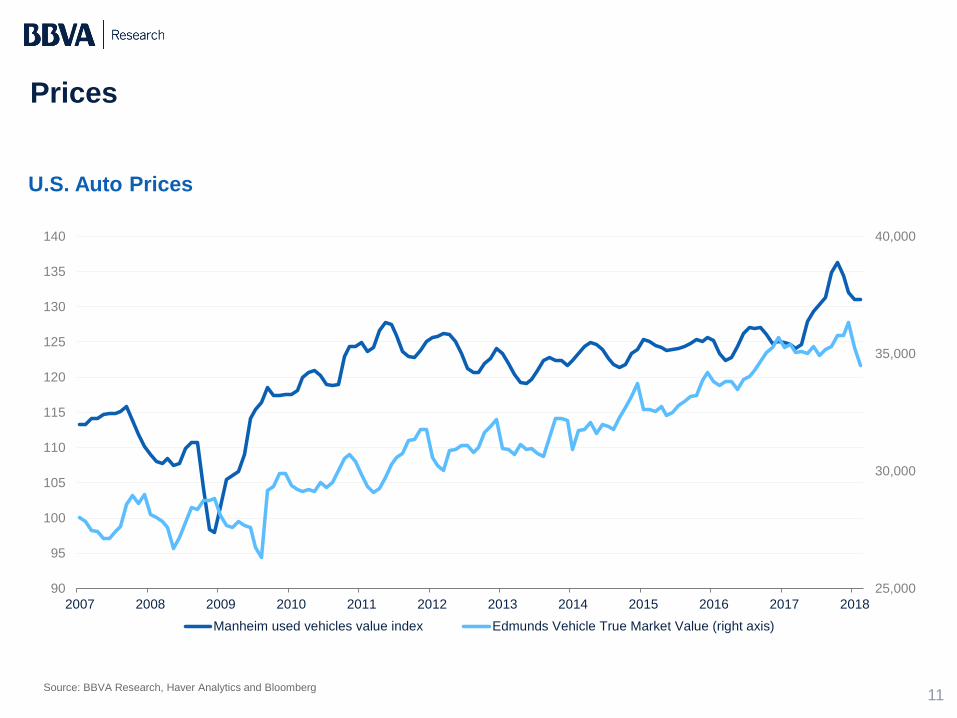

Prices

Source: BBVA Research, Haver Analytics and Bloomberg 11

U.S. Auto Prices

25,000

30,000

35,000

40,000

90

95

100

105

110

115

120

125

130

135

140

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Manheim used vehicles value index Edmunds Vehicle True Market Value (right axis)

Financial conditions

Source: BBVA Research and Haver Analytics 12

U.S. Interest rates (yoy % change)

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016 2017 2018

48-month new car loan 36-month used car loan 60-month new car

Financial conditions

Source: BBVA Research and Haver Analytics 13

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

U.S. Newly originated installment auto loans ($ billion, eop, 4-qtr moving avg.)

Financial conditions

Source: BBVA Research and Haver Analytics 14

U.S. Auto loan 90+ days delinquent (% of balance)

0

1

2

3

4

5

6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Leasing

Source: BBVA Research and Bloomberg 15

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

U.S. Leasing penetration rate (%)

Leasing

*Assumes 36-month lease terms

Source: BBVA Research and Bloomberg 16

2.81

3.21

4.01

4.45

4.98

5.35

0

1

2

3

4

5

6

2014 2015 2016 2017f 2018f 2019f

Off-Lease returns and supply* (Fiscal years, millions units)

Gasoline

Source: BBVA Research and Haver Analytics 17

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

U.S. Spot price (cents per gallon)

CONSUMERS

Consumers

Source: BBVA Research and Haver Analytics 19

U.S. Consumer sentiment index

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Current economic conditions Consumer expectations

Consumers

Source: BBVA Research and Haver Analytics 20

U.S. Plans to buy a car within 6 months (% of respondents)

8

9

10

11

12

13

14

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Consumers

Source: BBVA Research and Haver Analytics 21

U.S. Employment and real disposable personal income (yoy % change)

-6%

-4%

-2%

0%

2%

4%

6%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Real disposable personal income Nonfarm payroll Average RDI 2010 - 1Q18

Consumers

Source: BBVA Research and Haver Analytics 22

U.S. Household equity and home prices

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

0

2000

4000

6000

8000

10000

12000

14000

16000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Owners equity in real estate (NSA billion $, left axis) FHFA house price index (yoy change, right axis)

PRODUCTION

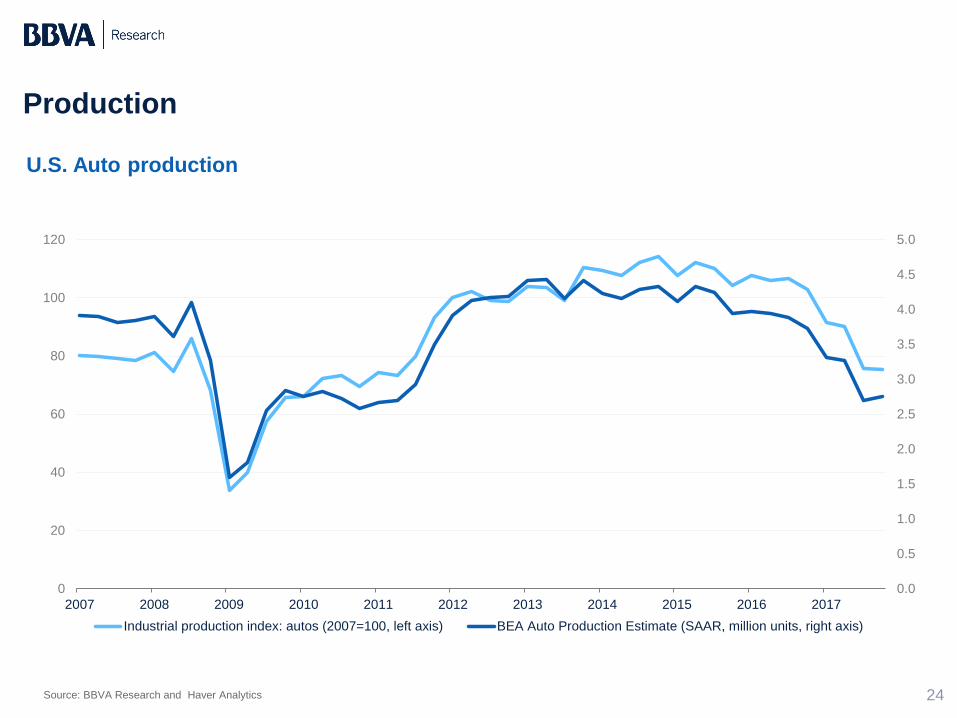

Production

Source: BBVA Research and Haver Analytics 24

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Industrial production index: autos (2007=100, left axis) BEA Auto Production Estimate (SAAR, million units, right axis)

U.S. Auto production

STRUCTURAL

Fundamentals

Source: BBVA Research and Haver Analytics 26

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

2016: 11.6

Mean age of passenger cars in operation (years)

Vehicle miles of travel (total and adjusted by labor force)

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

0

2000

4000

6000

8000

10000

12000

14000

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

20

15

Millio

n m

iles

Miles p

er

cap

ita

Population adjusted (left axis) Total (right axis)

Demographics

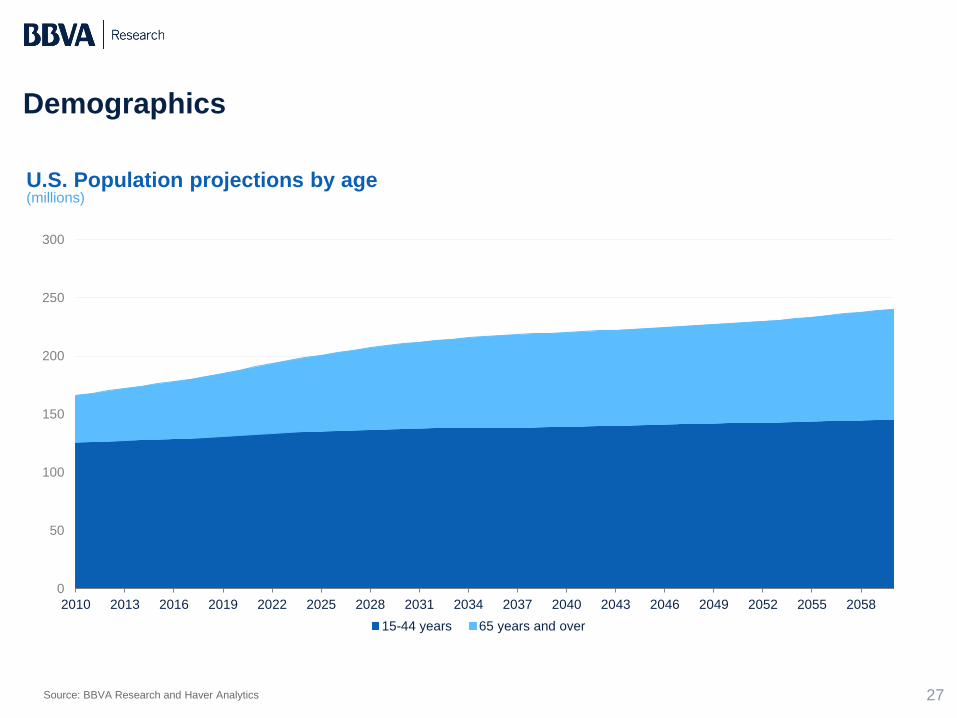

Source: BBVA Research and Haver Analytics 27

0

50

100

150

200

250

300

2010 2013 2016 2019 2022 2025 2028 2031 2034 2037 2040 2043 2046 2049 2052 2055 2058

15-44 years 65 years and over

U.S. Population projections by age (millions)

Electric vehicles

Source: BBVA Research and Haver Analytics 28

U.S. Electric vehicle sales (units)

0

2000

4000

6000

8000

10000

12000

0

5000

10000

15000

20000

25000

30000

35000

40000

Apr-

14

Jun-1

4

Aug-1

4

Oct-

14

De

c-1

4

Feb

-15

Apr-

15

Jun-1

5

Aug-1

5

Oct-

15

De

c-1

5

Feb

-16

Apr-

16

Jun-1

6

Aug-1

6

Oct-

16

De

c-1

6

Feb

-17

Apr-

17

Jun-1

7

Aug-1

7

Oct-

17

De

c-1

7

Hybrids Plug-in Hybrid (right axis) Battery Electric Vehicle (right axis)

Disruptive trends transforming the auto industry

Source: Heineke, Kersten; Moller, Timo; Padhi, Asutosh, and Tschiesner, Andreas (2017), “The automotive revolution is speeding up”,

McKinsey & Company, September. 29

Autonomous Driving

80% of the top OEMs have announced

plans for highly autonomous

technology to be ready for the road by 2025

Shared Mobility

$32 billion had been invested in

ridesharing start-ups alone. US customers

expect usage of shared mobility to increase by around 80%

once robo-taxis are available

Connectivity

The percentage of consumers

ready and willing to

change car brands for better connectivity has

doubled over the past two

years

Electrification

Many mass-market OEMs are planning to add ten or more EV models as they can reach potential sales of up to 600K

units in the next five years

FORECASTS

Forecast

Source: BBVA Research 31

2015 2016 2017 2018 2019 2020 2021 2022

Auto sales (millions units)

17.5 17.5 17.3 16.6 16.8 17.1 17.3 17.3

Real GDP growth (% change)

2.9 1.5 2.3 2.8 2.8 2.5 2.3 2.2

Unemployment rate (% avg.)

5.3 4.9 4.4 3.9 3.6 3.7 4.0 4.3

Fed funds (%, eop)

0.50 0.75 1.5 2.5 3.0 3.0 3.0 3.0

5-year Treasuries (%, avg)

1.5 1.3 1.9 2.7 3.2 3.4 3.6 3.7

AUTO

INDUSTRY

US

1Q 2018

CHARTBOOK