update on international operations financial performance ... · update on international operations...

TRANSCRIPT

UPDATE ON INTERNATIONAL OPERATIONS FINANCIAL PERFORMANCE AND OUTLOOK

JÁNOS SZABÓ Chief Financial Officer

UPDATE ON INTERNATIONAL OPERATIONS

KEY MARKET DEVELOPMENTS

#1 fixed and mobile voice positions

Continued leadership in mobile and fixed BB

Mobile revenues under pressure due to aggressive price competition

Increasing TV market share

Fighting back in residential segment with advanced bundles and focused investments

High level of profitability – EBITDA margin above 40%

MACEDONIA – CURRENT SNAPSHOT

Romania

Bulgaria

Hungary

Croatia

Serbia

Macedonia

Bulgaria

Hungary

Croatia

Macedonia

Hungary

Croatia

BiH Serbia

Albania

Greece

Macedonia

Kosovo

Czech Rep.Slovakia

Austria

Slovenia

Montenegro

Macedonia

Mobile BB 44%

Fixed BB 45%

TV 19%

Mobile voice 48%

Fixed voice 71%

All market share figures as of June 30, 2013 except mobile BB (as of March 31, 2013) 3

MACEDONIA – OPPORTUNITIES IN THE CURRENT CHALLENGING ENVIRONMENT

ALL IP TRANSFORMATION

PSTN to IMS migration

Following the 800 MHz and 1800 MHz spectrum acquisition, LTE launch before YE 2013

EXTENSION OPPORTUNITIES

Customer centric products

Growth potential in near-core (ICT) and non-core (M-wallet) services

INCREASE INTERNAL EFFICIENCY

Legal merger to be completed

New and leaner organization

KEEP MOBILE VOICE MARKET SHARE ABOVE 48% SUCCESSFUL MERGER

4

KEY MARKET DEVELOPMENTS

#1 fixed voice, broadband (mobile and fixed) and TV positions maintained

Leader in the postpaid mobile market

FTTH rollout to maintain long-term competitiveness in BB, TV and 3Play

Stable financial performance despite industry commoditization, competition and SIM and IPTV subscription based taxes

Mobile BB 39%

Fixed BB 82%

TV 41%

Mobile voice 35%

Fixed voice 98%

MONTENEGRO – CURRENT SNAPSHOT

Romania

Bulgaria

Hungary

Croatia

Serbia Bulgaria

Hungary

Croatia

Macedonia

Hungary

Croatia

BiH Serbia

Albania

Greece

Macedonia

Kosovo

Czech Rep.Slovakia

Austria

Slovenia

Montenegro

Montenegro

All market share figures as of June 30, 2013 5

MONTENEGRO – ADDRESSING THE CHALLENGES

INITIATIVES TO DEFEND THE CORE

FTTH rollout

Mobile BB (HSPA/LTE) focus

Evolving 4Play

Multiscreen propositions

GROWTH OPPORTUNITIES IN NEAR AND BEYOND CORE

ICT and cloud solutions

Digital push

M-payment opportunities

Smart Telco (M2M)

INCREASE SALES AND OPERATIONAL EFFICIENCY

Increasing the role of e-care and e-sale

All IP migration

E2E processes review

Cost optimization

2017 TARGET: KEEP REVENUES ABOVE EUR 100MN 2017 TARGET: KEEP EBITDA

ABOVE EUR 40MN

6

Improve sales capacity and productivity

ICT and cloud solutions

Focus on automation and e-care

7

MONTENEGRO – STRATEGIC ANSWERS TO THE CURRENT ENVIRONMENT

e-SALES: 20% SHARE IN 2017 (3% IN 2013)

OVERALL TARGET FOR 2017: KEEP REVENUES ABOVE EUR 100M

First choice provider for digital lifestyle and business solutions

Flexible and lean operating model to succeed in fast-changing world

New organizational model with reinforced performance culture

State-of-the-art IT infrastructure

Cost optimization

Exploit M2M opportunities

Future organizational model based on lean, functionally oriented organization

Effective performance managment system

Minimized bureacracy

e-COMPANY: 50% LESS PAPER UNTIL 2017

LEAN AND EFFICIENT OPERATION

FINANCIAL PERFORMANCE AND OUTLOOK

DIVIDEND POLICY MAINTAINED

8

DIVIDEND POLICY MAINTAINED

Maintain net debt ratio (net debt/total capital) target of 30% - 40% reflecting the current unpredictable environment

Dividend payment potential dependent on upcoming frequency auction

DIVIDEND PAYMENT AND POLICY

74

50 50 50

0%

10%

20%

30%

40%

50%

0

10

20

30

40

50

60

70

80

Dividend per share (HUF) Net debt ratio

2012

34.3%

2011

34.1%

2010

32.7%

2009

30.8%

June 2013

41.8%

Dividend payment Net debt ratio

Target

8

GROUP REVENUE DEVELOPMENTS

EVOLVING SALES MIX DRIVING REVENUE GROWTH

9

Core ca. 56%

Near core ca. 26%

Beyond core ca. 18%

Core ca. 84%

Near core ca. 16%

0

200

400

600

800

CAGR: ca. +2%

HUF bn

CAGR: 0%

2017E 2014E 2012 2010

Fixed voice

TV Mobile voice

Fixed BB

Mobile BB

Other core SI/IT

Equipment (fixed and mobile)

Beyond core (incl. energy)

9

DISCIPLINED COST MANAGEMENT, DECLINING CAPEX

0

250

200

150

100

50

CAGR: ca. -2% CAGR: -4%

2017E 2012 2010

HUF bn

INDIRECT OPEX* DEVELOPMENTS

*Indirect OPEX excluding D&A, SEC/DOJ investigation-related costs, special, telecom and utility taxes **Capex excluding spectrum license fees

100

80

60

40

20

0

HUF bn

2017E 2014E

CAGR: ca. -3%

2012

CAPEX** DEVELOPMENTS

10

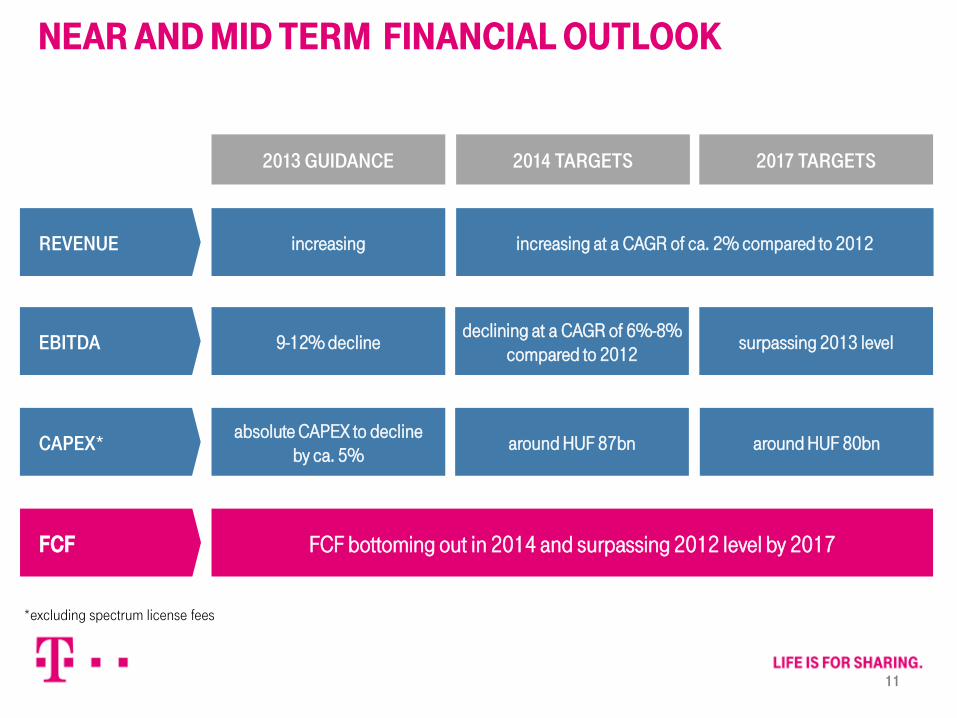

NEAR AND MID TERM FINANCIAL OUTLOOK

REVENUE

EBITDA

CAPEX*

increasing at a CAGR of ca. 2% compared to 2012

surpassing 2013 level

around HUF 80bn

declining at a CAGR of 6%-8% compared to 2012

around HUF 87bn

**excluding spectrum license fee

increasing

9-12% decline

absolute CAPEX to decline by ca. 5%

2013 GUIDANCE 2014 TARGETS 2017 TARGETS

FCF FCF bottoming out in 2014 and surpassing 2012 level by 2017

*excluding spectrum license fees

11

This presentation contains forward-looking statements. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. These statements are based on current plans, estimates and projections, and therefore should not have undue reliance placed upon them. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events. Forward-looking statements involve inherent risks and uncertainties. We caution you that a number of important factors could cause actual results to differ materially from those contained in any forward-looking statement. Such factors are described in, among other things, our annual financial statements for the year ended December 31, 2012, available on our website at http://www.telekom.hu which have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and adopted by the European Union.

Abbreviations: #: Number, 2G: Second Generation, 3G: Third Generation, 4G: Fourth Generation, ADSL: Asymmetric Digital Subscriber Line, App.: Application, ARPU: Average Revenue Per User, AVG: Average, B2B2C: Business to Business to Consumer, BB: Broadband, Bn: Billion, CAGR: Compound Annual Growth Rate, CAPEX: Capital Expenditures, COAX: Coaxial Cable, CRM: Customer Relationship Management, DL: Downlink, DPS: Dividend per Share, DT: Deutsche Telekom, E2E: End-to-End, EBITDA: Earnings Before Interest, Taxes, Deprecation and Amortization, EDGE: Enhanced Data for Global Evolution, ERP: Enterprise Resource Planning FCF: Free Cash Flow, FDD: Frequency-Division Duplexing, FTTB: Fiber to the Building, FTTC: Fiber to the Cabinet, FTTH: Fiber to the Home, GDP: Gross Domestic Product, GSM: Global System for Mobile communication, GPRS: General Pocket Radio Service, H1: First half, HH: Household, HSPA: High-Speed Packet Access, HUF: Hungarian Forint, HW: Hardware, ICT: Info-Communication Technology, IMS: IP Multimedia Subsystem, IP: Internet protocol, IT: Information technology, K: Thousand, KPI: Key Performance Indicator, LTE: Long Term Evolution, Min: minute, M2M: Machine-to-Machine, M-: Mobile-, Mbps: Mega Bit Per Second, MHz: Mega Hertz, Mn: Million, OPEX: Operating Expenses, OS: Operating System, OTT: Over The Top, PSTN: Public Switched Telephone Network, SAT: Satellite, SI: System Integration, SIM: Subscriber Identity Module, SMB: Small Medium Enterprises, SOHO: Small office home office, SW: Software, T2M: Time to Market, TDD: Time-Division Duplexing, TV: Television, TWM: Total Workforce Management, UL: Uplink, UMTS: Universal Mobile Telecommunication System, USP: Universal Service Provider, VDSL: Very high bit rate Digital Subscriber Line, yr: year