update new tax laws and maximise regulations value 2017 18

TRANSCRIPT

18th Annual Tax and Legal Conference

Maximise Shareholder Value 2017

Update new tax laws and regulations

18 October 2016

www.pwc.com/th

PwC

Agenda

PART I

1. Tax rate update

2. Tax measures to encourage a single bookkeeping

3. Additional tax deductions/other deductions

4. Tax exemptions/tax support

5. Extension of period for filing/requesting refund

6. Personal income tax

7. Other

PART II

1. Draft Act to amend the Revenue Code/ Draft of other Acts/ Draft regulations

2. Non-Publicly Accountable Entities (NPAEs)

218 October 2016Maximise Shareholder Value 2017

PwC

PART I

318 October 2016Maximise Shareholder Value 2017

PwC

14

18 October 2016Maximise Shareholder Value 2017

PwC

1. Tax rate update

Purpose: To increase the ability of a corporate entity to compete in the economy of the country

Reduction of corporate income tax rate:

The statutory tax rate permanently reduced from 30% to 20%

Effective date:

For companies and juristic partnerships with accounting periods commencing on or after 1 January 2016.

518 October 2016Maximise Shareholder Value 2017

1.1 Reduction of corporate income tax rate (Act to amend the Revenue Code No.42 dated 3 March 2016)

PwC

1. Tax rate update

Purpose: To relieve the tax burden and increase financial liquidity of SMEs as well as to increase their ability to compete in the country and attract investment

For accounting periods beginning on or after 1 January 2015 but not later than 31 December 2016:

Net profit (Baht) Tax rates0 - 300,000 Nil

Over 300,000 10%

618 October 2016Maximise Shareholder Value 2017

1.2 SME corporate tax rate (Royal Decree No. 603 dated 18 April 2016)

PwC

1. Tax rate update

For accounting periods beginning on or after 1 January 2017:

Net profit (Baht) Tax rates0 -300,000 Nil

300,001 – 3,000,000 15%Over 3,000,000 20%

To be eligible for the reduced rates of tax, the SME must meet the following criteria:

1. Paid-up capital on the last day of any accounting period must not exceed THB 5 million, and2. Income from the “sale of goods and provision of services” must not exceed THB 30 million in

any accounting period.

718 October 2016Maximise Shareholder Value 2017

1.2 SME corporate tax rate (Royal Decree No. 603 dated 18 April 2016) (Cont’d)

PwC

1. Tax rate update

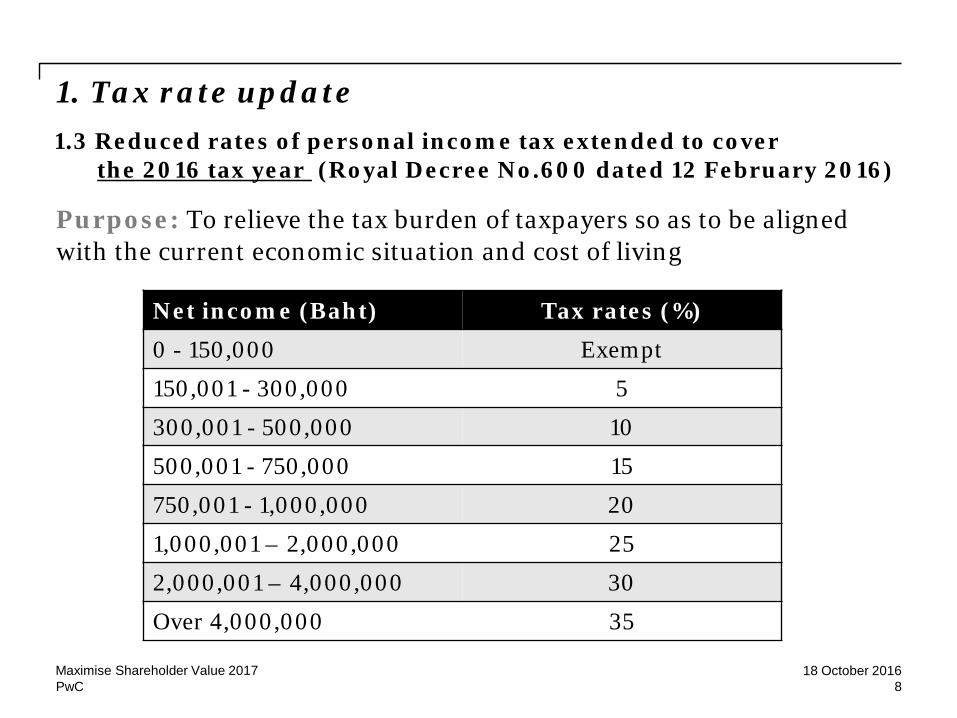

Purpose: To relieve the tax burden of taxpayers so as to be aligned with the current economic situation and cost of living

Net income (Baht) Tax rates (%)

0 - 150,000 Exempt

150,001 - 300,000 5

300,001 - 500,000 10

500,001 - 750,000 15

750,001 - 1,000,000 20

1,000,001 – 2,000,000 25

2,000,001 – 4,000,000 30

Over 4,000,000 35

818 October 2016Maximise Shareholder Value 2017

1.3 Reduced rates of personal income tax extended to coverthe 2016 tax year (Royal Decree No.600 dated 12 February 2016)

PwC

29

18 October 2016Maximise Shareholder Value 2017

PwC

2. Tax measures to encourage a single bookkeeping

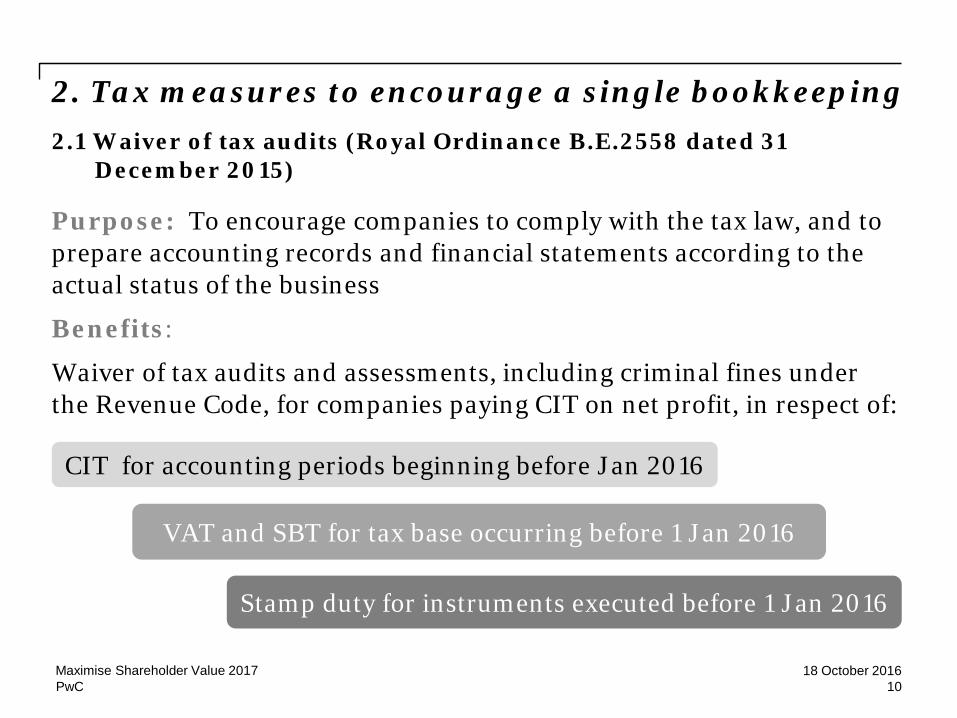

Purpose: To encourage companies to comply with the tax law, and to prepare accounting records and financial statements according to the actual status of the business

Benefits:

Waiver of tax audits and assessments, including criminal fines under the Revenue Code, for companies paying CIT on net profit, in respect of:

CIT for accounting periods beginning before Jan 2016

VAT and SBT for tax base occurring before 1 Jan 2016

Stamp duty for instruments executed before 1 Jan 2016

1018 October 2016Maximise Shareholder Value 2017

2.1 Waiver of tax audits (Royal Ordinance B.E.2558 dated 31 December 2015)

PwC

2. Tax measures to encourage a single bookkeeping

Conditions:

Companies earning revenue not exceeding Baht 500 million in the past full 12-month accounting period which ended on or before 31 Dec 2015

Registration between 15 Jan 2016 and 15 Mar 2016

Tax returns due from Jan 2016 onwards filed and tax paid (if any)

Bookkeeping and financial statements in accordance with the actual status of the business for accounting periods beginning on or after 1 Jan 2016

No action must be taken from 1 Jan 2016 onwards that indicates an evasion of tax

1118 October 2016Maximise Shareholder Value 2017

2.1 Waiver of tax audits (Royal Ordinance B.E.2558 dated 31 December 2015) (Cont’d)

PwC

2. Tax measures to encourage a single bookkeeping

The Ministry of Finance and the Bank of Thailand will perform necessary action to instruct commercial banks to use the accounting records and financial statements filed with the

Revenue Department as evidence for processing financial transactions and requesting banking facilities

With effect from 1 Jan

2019

1218 October 2016Maximise Shareholder Value 2017

2.2 Evidence for borrowing from the banks (Royal Ordinance B.E.2558 dated 31 December 2015)

PwC

2. Tax measures to encourage a single bookkeeping

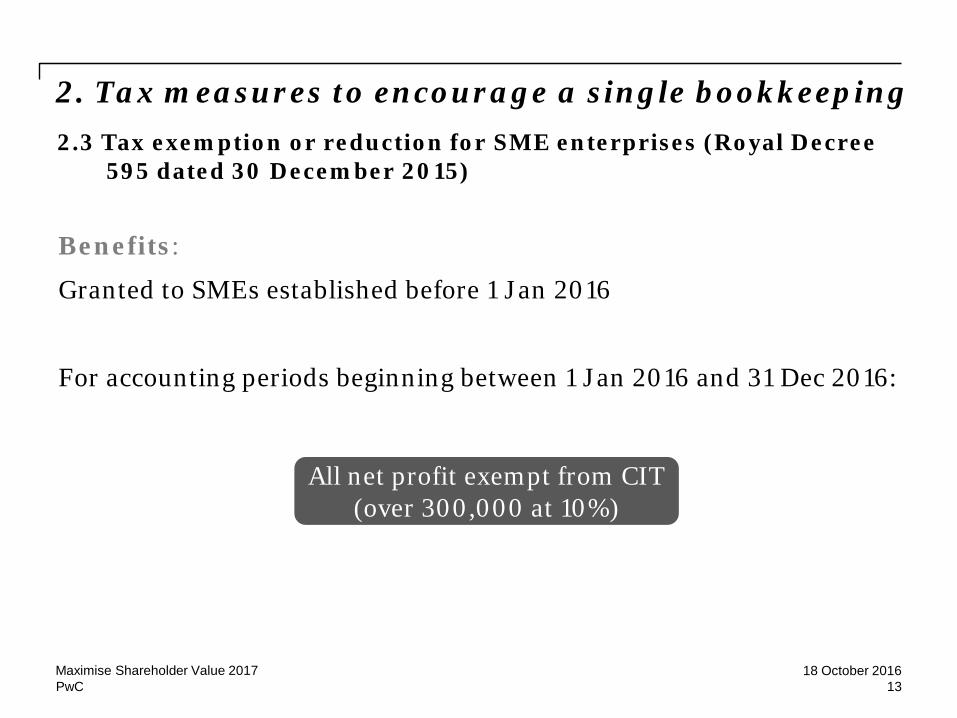

Benefits:

Granted to SMEs established before 1 Jan 2016

For accounting periods beginning between 1 Jan 2016 and 31 Dec 2016:

All net profit exempt from CIT (over 300,000 at 10%)

1318 October 2016Maximise Shareholder Value 2017

2.3 Tax exemption or reduction for SME enterprises (Royal Decree 595 dated 30 December 2015)

PwC

2. Tax measures to encourage a single bookkeeping

Benefits:

For accounting periods beginning between 1 Jan 2017 and 31 Dec 2017:

Net profit (Baht) Tax rates0 - 300,000 Nil

Over 300,000 10%

1418 October 2016Maximise Shareholder Value 2017

2.3 Tax exemption or reduction for SME enterprises (Royal Decree 595 dated 30 December 2015) (Cont’d)

PwC

2. Tax measures to encourage a single bookkeeping

Benefits:

For accounting periods beginning on or after 1 Jan 2018:

Net profit (Baht) Tax rates0 -300,000 Nil

300,001 – 3,000,000 15%Over 3,000,000 20%

1518 October 2016Maximise Shareholder Value 2017

2.3 Tax exemption or reduction for SME enterprises (Royal Decree 595 dated 30 December 2015) (Cont’d)

PwC

2. Tax measures to encourage a single bookkeeping

Conditions:

To be eligible for the tax exemption and reduced rates of tax, the SME must meet the following criteria: 1. Paid-up capital on the last day of any accounting period must

not exceed THB 5 million.2. Revenue from the “sale of goods and provision of services” must

not exceed THB 30 million in any accounting period.3. Registration as an operator according to the above Royal

Ordinance B.E. 2558 dated 31 December 2015 4. The waiver of a tax audit according to the above Royal Ordinance

must not have been revoked.

1618 October 2016Maximise Shareholder Value 2017

2.3 Tax exemption or reduction for SME enterprises (Royal Decree 595 dated 30 December 2015) (Cont’d)

PwC

2. Tax measures to encourage a single bookkeeping

SMEs which registered for the waiver of tax audit

SMEs obtain CIT tax exemption for the accounting period beginning between 1 Jan and 31 Dec 2016

WHT still required for

payments subject to WHT to these SMEs

Tax refund

1718 October 2016Maximise Shareholder Value 2017

2.4 Withholding tax still required on payments to SMEs (Clarification of the Revenue Department No. 4, dated 11 April 2016)

PwC

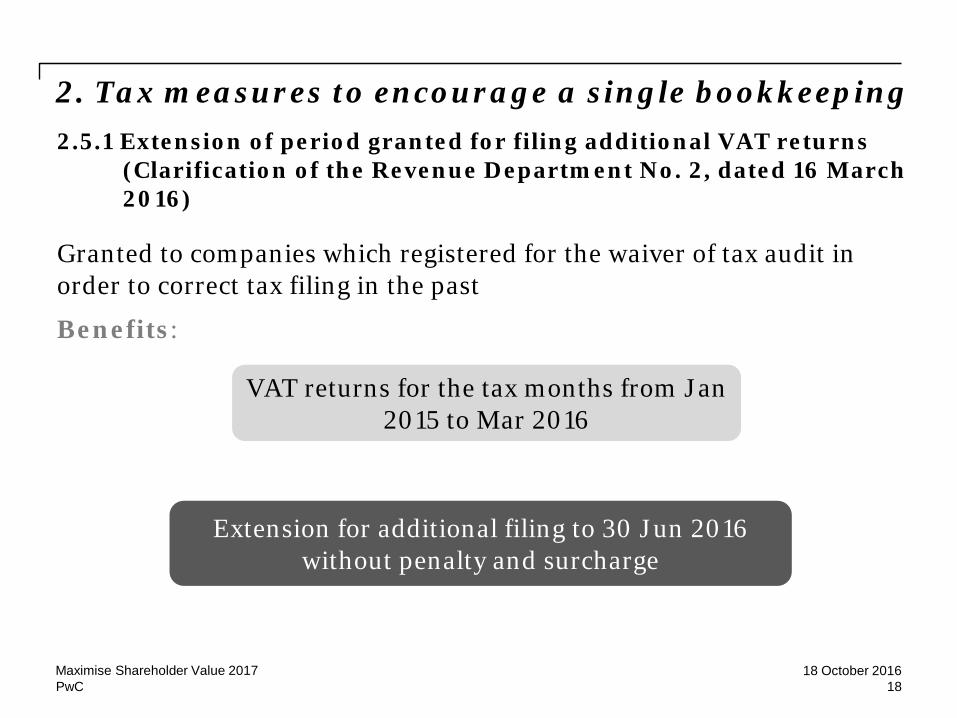

2. Tax measures to encourage a single bookkeeping

Granted to companies which registered for the waiver of tax audit in order to correct tax filing in the past

Benefits:

VAT returns for the tax months from Jan 2015 to Mar 2016

Extension for additional filing to 30 Jun 2016 without penalty and surcharge

1818 October 2016Maximise Shareholder Value 2017

2.5.1 Extension of period granted for filing additional VAT returns (Clarification of the Revenue Department No. 2, dated 16 March 2016)

PwC

2. Tax measures to encourage a single bookkeeping

Benefits:

Monthly tax returns for all types of tax for the tax months from Jan 2015 to Mar

2016

Extension for additional filing to 30 Jun 2016 without penalty and surcharge

WHT tax returns, reverse

charge VAT returns,

SBT returns, stamp duty

returns

1918 October 2016Maximise Shareholder Value 2017

2.5.2 Extension of period granted for filing monthly tax returns for all types of tax (Clarification of the Revenue Department No.3, dated 23 March 2016)

PwC

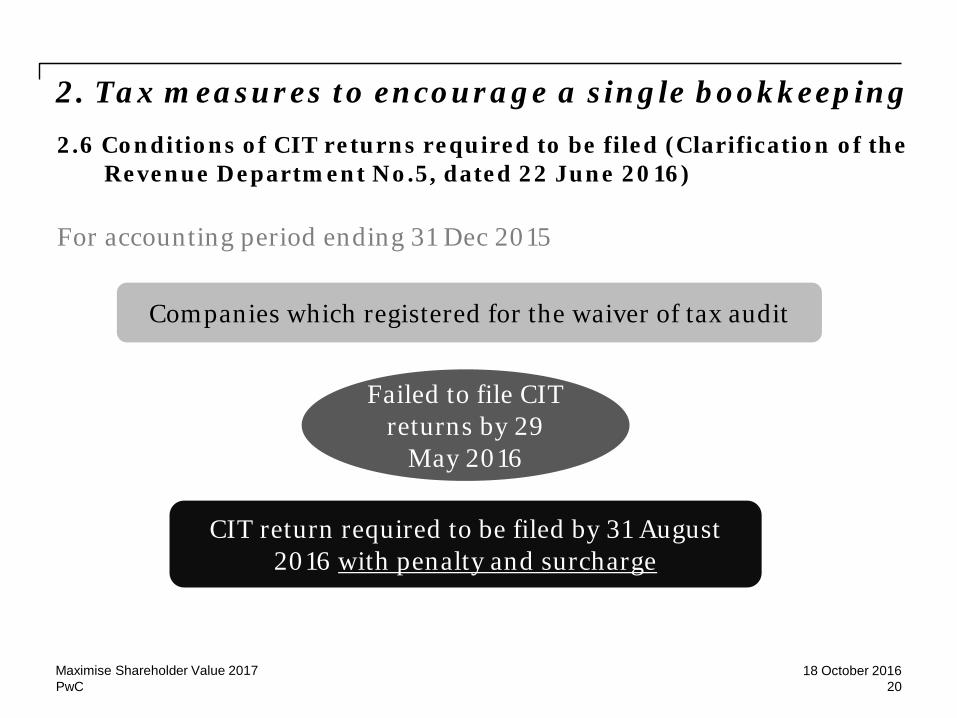

2. Tax measures to encourage a single bookkeeping

For accounting period ending 31 Dec 2015

Companies which registered for the waiver of tax audit

Failed to file CIT returns by 29

May 2016

CIT return required to be filed by 31 August 2016 with penalty and surcharge

2018 October 2016Maximise Shareholder Value 2017

2.6 Conditions of CIT returns required to be filed (Clarification of the Revenue Department No.5, dated 22 June 2016)

PwC

2. Tax measures to encourage a single bookkeeping

For accounting period beginning between 1 Jan and 31 Dec 2015

Companies which registered for the waiver of tax audit

Failed to file CIT returns

Due date for filing CIT returns - same as half-year CIT return of following accounting period,with penalty and surcharge (+ 3 months)

2118 October 2016Maximise Shareholder Value 2017

2.6 Conditions of CIT returns required to be filed (Clarification of the Revenue Department No.5, dated 22 June 2016) (Cont’d)

PwC

2. Tax measures to encourage a single bookkeeping

Companies which registered for the waiver of tax audit

Incorrect accounting records found after filing 2015 audited financial statements with the

DBD

- Amend 2015 accounting records to be in line with the actual circumstances- Revised financial statements to be signed by CPA and re-filed with the DBD

Requirements

2218 October 2016Maximise Shareholder Value 2017

2.7 Conditions of Accounts and financial statements required to be in line with the actual circumstances of the business (Clarification of the Revenue Department No. 6, dated 9 August 2016)

PwC

2. Tax measures to encourage a single bookkeeping

Purpose:

To promote SMEs to prepare bookkeeping correctly

Benefits:

Double deduction granted to SMEs for expenses relating to the hire of students who currently study accounting for handling accounting matters

Eligible accounting periods:

Accounting periods commencing on or after 1 January 2016 until 31 December 2018 (3 years)

SME means companies or juristic partnerships established under Thai law that have fixed assets, excluding land, with a value of not more than THB 200

million and no more than 200 employees

2318 October 2016Maximise Shareholder Value 2017

2.8 Additional deduction of hiring students who currently study accounting (Royal Decree No.607 dated 11 May 2016)

PwC

324

18 October 2016Maximise Shareholder Value 2017

PwC

3. Additional tax deductions/other deductions

Purpose: To continue promotion of education support

Benefits:

Extension of period of double deduction for donations to educational institutions (either public or private sector)

Exemption from income tax, VAT, SBT and stamp duty on proceeds from transfer of property or instruments executed in respect of such donations (cost of property may not be included as a tax deductible expense)

Granted to:

Individuals or corporate entities

Period:

1 January 2016 to 31 December 2018

2518 October 2016Maximise Shareholder Value 2017

3.1 Donations to educational institutions (Royal Decree No. 616 dated 30 June 2016)

PwC

3. Additional tax deductions/other deductions

Purpose: To continue promotion of sports support

Benefit:

Extension of period of double deduction for donations to sports organizations

Exemption from income tax, VAT, SBT and stamp duty on proceeds from transfer of property or instruments executed in respect of such donations (cost of property may not be included as a tax deductible expense)

Granted to:

Individuals or corporate entities

Period:

1 January 2016 to 31 December 2018

2618 October 2016Maximise Shareholder Value 2017

3.2 Donations to sport organizations (Royal Decree No. 596 dated 25 January 2016)

PwC

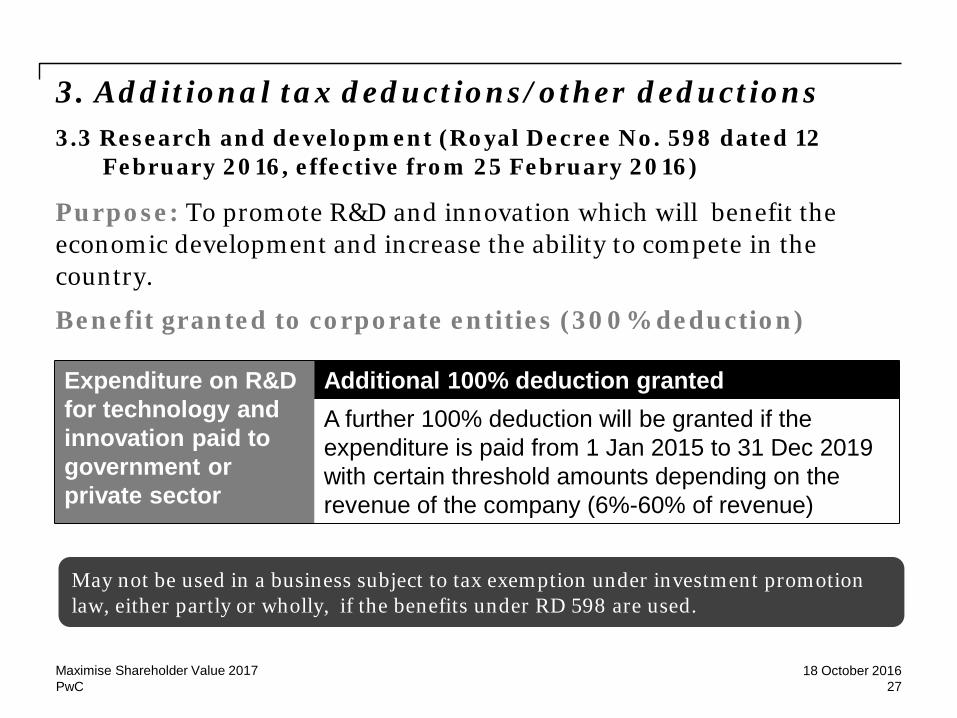

3. Additional tax deductions/other deductions

Purpose: To promote R&D and innovation which will benefit the economic development and increase the ability to compete in the country.

Benefit granted to corporate entities (300% deduction)

Expenditure on R&D for technology and innovation paid to government or private sector

Additional 100% deduction grantedA further 100% deduction will be granted if the expenditure is paid from 1 Jan 2015 to 31 Dec 2019 with certain threshold amounts depending on the revenue of the company (6%-60% of revenue)

May not be used in a business subject to tax exemption under investment promotion law, either partly or wholly, if the benefits under RD 598 are used.

2718 October 2016Maximise Shareholder Value 2017

3.3 Research and development (Royal Decree No. 598 dated 12 February 2016, effective from 25 February 2016)

PwC

3. Additional tax deductions/other deductions

Purpose: To promote investment in the country so as to benefit the economy in the short-term and to increase the ability to compete in the country over the long-term

Benefits:

P/O, purchase agreement, application for construction, etc. - dated between 3 Nov 2015 and 31 Dec 2016

Payment made between 3 Nov 2015 and 31 Dec 2016

Assets ready for use between 3 Nov 2015 and 31 Dec 2016 except for machinery and permanent buildings that may be ready for use after 31 Dec 2016

100% additional deduction for investment in new assets

The additional deduction must be averaged equally over each accounting period.

If

2818 October 2016Maximise Shareholder Value 2017

3.4 Investment in new assets (Royal Decree No. 604 dated 18 April 2016, Royal Decree No.622 dated 24 August 2016)

PwC

3. Additional tax deductions/other deductions

Eligible assets:Type of asset Number of accounting

periods to be used for the additional deduction

1. Machinery, components, equipment, tools, furniture and fixtures

5

2. Computer programs 3

3. Registered vehicles under the law, excluding passenger cars with not more than 10 seats which are not acquired for use in a leasing business (cars used in leasing business can use this benefit.)

5

4. Permanent buildings, excluding land and permanent buildings used for residential purposes

20

2918 October 2016Maximise Shareholder Value 2017

3.4 Investment in new assets (Royal Decree No. 604 dated 18 April 2016, Royal Decree No. 622 dated 24 August 2016) (Cont’d)

PwC

3. Additional tax deductions/other deductions

Purpose: To continue promotion of domestic travel so as to benefit the economy and to assist operators in the travel business

Benefits:

Extension of period of double deduction for expenses for seminar rooms, accommodation, transportation and other expenses related to domestic seminars and training for employees or expenses for such seminars and training paid to tourism operators under the law

Granted to:

Corporate entities

Eligible period:

1 January 2016 to 31 December 2016

3018 October 2016Maximise Shareholder Value 2017

3.5 Expenses paid for domestic seminars and training (Royal Decree No.611 dated 19 May 2016, DG Notification No.267)

PwC

3. Additional tax deduction /other deductions

Purpose: To promote learning, maintenance of religion, arts and culture and to attract donors for these funds

Benefits:

Double deduction granted for donations to Safe and Creative Media Development fund and funds relating to art, culture, archives and archaeology, with a limit on the amounts deductible

Granted to:

Individuals and corporate entities

Effective date:

6 July 2016

3118 October 2016Maximise Shareholder Value 2017

3.6 Donations to various cultural funds (Royal Decree No.615 dated 30 June 2016)

PwC

3. Additional tax deductions/other deductions

Purpose: To attract donors for the Technology Development Fund for Education which is of benefit to the education and learning of Thai people

Benefits:

Deduction for donations to the Technology Development Fund for Education established by the Ministry of Education, with a limit on the amount

Granted to:

Individuals and corporate entities

Effective date:

6 August 2016

3218 October 2016Maximise Shareholder Value 2017

3.7 Donations to the Technology Development Fund for Education (Royal Decree No.619 dated 1 August 2016)

PwC

433

18 October 2016Maximise Shareholder Value 2017

PwC

4. Tax exemptions/tax support

Purpose: To encourage multinational companies to set up more IHQs in Thailand

Previously, SBT exemption was granted to qualified IHQs only on interest received from loans to the associated enterprises according to Royal Decree No. 586 dated 28 April 2015.

New Benefits:

To extend the tax base for SBT exemption for qualified IHQs to be all remuneration received from treasury management services provided to associated enterprises

Effective date:

From 2 May 2015

3418 October 2016Maximise Shareholder Value 2017

4.1 SBT exemption for treasury management (Royal Decree No. 612 dated 31 May 2016)

PwC

4. Tax exemptions/tax support

Purpose: To promote investment in property through REIT instead of property funds

Benefits:

Exemption from income tax for unit holders of property funds on income from the conversion of investment units to REIT trust certificates

Exemption from VAT, SBT and stamp duty for property funds for the transfer of property due to the conversion to REIT

Effective date:

Between 25 February 2016 and 31 December 2016

3518 October 2016Maximise Shareholder Value 2017

4.2 Tax exemption for conversion of property fund to Real Estate Investment Trust (REIT)(Royal Decree No. 599 dated 12 February 2016)

PwC

4. Tax exemptions/tax support

Purpose: To promote target activities that use technology as the basis for the production process and services

4.3.1 Benefits for SME operators (Royal Decree No. 602 dated 18 April 2016)

CIT exemption granted to SME on profit derived from 10 target activities approved by the NSTD for five accounting periods under prescribed conditions

SME must meet the following criteria: 1. A company or juristic partnership must be established between 1 October 2015 and 31 December 2016 including obtains approval from the Director General of the Revenue Department.2. Paid-up capital on the last day of any accounting period must not exceed THB 5 million, and3. Revenue from the “sale of goods and provision of services” must not exceed THB 30 million in any accounting period.

3618 October 2016Maximise Shareholder Value 2017

4.3 Tax support for target activities using technology as the basis for the production process and services approved by the NSTD

PwC

4. Tax exemptions/tax support

4.3.2 Benefits for venture capital (Royal Decree No. 597 dated 10 February 2016)

CIT exemption granted to venture capital companies for ten accounting periods on:

Dividends derived from an operating company

performing target activities

Gain on the transfer of shares in an operating company that earns at least 80% of its income

from target activities

Thai company doing target activities andnot listed in the SET

Operating Company

3718 October 2016Maximise Shareholder Value 2017

4.3 Tax support for target activities using technology as the basis for the production process and services approved by the NSTD (Cont’d)

PwC

4. Tax exemptions/tax support

4.3.3 Benefits for shareholders and unit holders in venture capital trust (Royal Decree No. 597 dated 10 February 2016)

Individual/corporate shareholders or unit holders of venture capital company or private equity trust

PIT and CIT exemptions granted for ten accounting periods

To

DividendsGain on

transfer of shares/trust

units

Gain on dissolution of

venture capital company/private

equity trust

3818 October 2016Maximise Shareholder Value 2017

4.3 Tax support for target activities using technology as the basis for the production process and services approved by the NSTD (Cont’d)

PwC

4. Tax exemptions/tax support

10 Target activities: Food and agriculture

Energy saving, energy replacement and clean energy

Bio-technology base

Medical and public health

Tourism, services and creative economics

Advanced materials

Textiles, clothes and accessories

Vehicles and parts

Electronics, computers, software and information technology services

Research, development and innovation or new industries

3918 October 2016Maximise Shareholder Value 2017

4.3 Tax support for target activities using technology as the basis for the production process and services approved by the NSTD (Cont’d)

PwC

4. Tax exemptions/tax support

Purpose: To promote social enterprises so as to raise the quality of life of the people and to assist the private sector in coordinating with the government to project the community and society

4.4.1 Benefits of qualified social enterprises:

Corporate tax exemption on net profit

All the net profits of each accounting period must be

reinvested or used for the benefit of farmers, the poor, the disabled

or for other public benefit.

No dividend or any deemed income from reduction of

capital can be paid to shareholders or partners out

of the profit.

and

If

4018 October 2016Maximise Shareholder Value 2017

4.4 Tax exemption granted to social enterprises, investors and donators (Royal Decree No. 621 dated 24 August 2016)

PwC

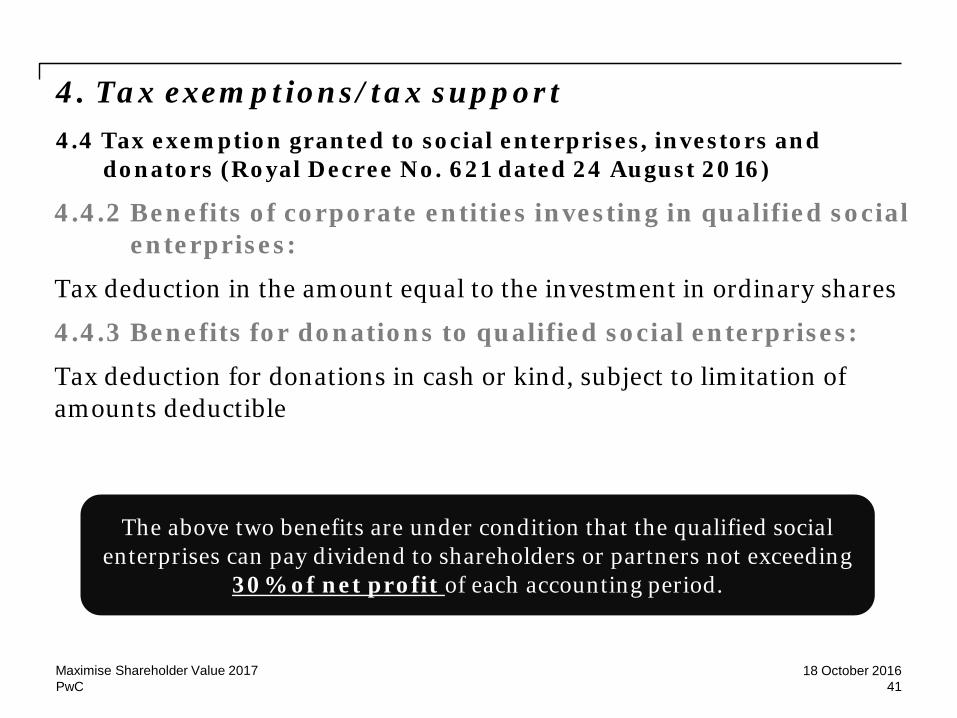

4. Tax exemptions/tax support

4.4.2 Benefits of corporate entities investing in qualified social enterprises:

Tax deduction in the amount equal to the investment in ordinary shares

4.4.3 Benefits for donations to qualified social enterprises:

Tax deduction for donations in cash or kind, subject to limitation of amounts deductible

The above two benefits are under condition that the qualified social enterprises can pay dividend to shareholders or partners not exceeding

30% of net profit of each accounting period.

4118 October 2016Maximise Shareholder Value 2017

4.4 Tax exemption granted to social enterprises, investors and donators (Royal Decree No. 621 dated 24 August 2016)

PwC

4. Tax exemptions/tax support

Purpose: To promote debt restructuring of financial institutions under the criteria of the Bank of Thailand (continued from RD No. 581)

Benefits:

Tax exemption granted to debtors of financial institutions for income from the debts forgiven by the financial institutions which have executed the debt restructuring under the criteria of the Bank of Thailand from 1 January 2015

4218 October 2016Maximise Shareholder Value 2017

4.5 Debt restructuring (Royal Decree No. 623 dated 30 August 2016)

PwC

543

18 October 2016Maximise Shareholder Value 2017

PwC

5. Extension of period for filing/requesting refund

Benefits

Extension to 15 August 2016 with no penalty and surcharge for:

- CIT filing

- Request for refund of penalty and surcharge

Granted to:

BOI companies with multiple promoted projects which failed to compute income and expenditure of all promoted projects using net off method as required by the Board of Taxation Decision no. 38/2552, including those whose case was final.

4418 October 2016Maximise Shareholder Value 2017

5.1 CIT filing for BOI companies with multiple promoted projects (BOI net-off issue) (Order of the National Council for Peace and Order No. 45/2559 dated 29 July 2016)

PwC

5. Extension of period for filing/requesting refund

Benefits

Extension to 1 August 2016 for claiming a stamp duty refund

Conditions Instruments executed between 5 April 2015 and 31 January 2016

requiring stamp duty to be paid in cash, but stamp duty was already affixed

Refund can be claimed only if the stamp duty has been correctly paid in cash.

4518 October 2016Maximise Shareholder Value 2017

5.2 Stamp duty refund (Clarification of the Revenue Department dated 25 July 2016)

PwC

646

18 October 2016Maximise Shareholder Value 2017

PwC

6. Personal income tax

Purpose: To relieve tax burden for taxpayer who buys a residence within December 2016

Benefits:

Amount paid for purchase of a house with land or a condominium unit as a residence

Value of property ≤ 3 million Baht

A deduction of 20% for five tax years – same amount for each year

4718 October 2016Maximise Shareholder Value 2017

6.1 Tax deduction for purchase of first residence(Ministerial Regulation No. 313 dated 5 February 2016)

PwC

6. Personal income tax

Purpose: To encourage savings for security of the aged who do not obtain benefit from the government

Benefits:

Actual contribution paid to the National Savings Fund granted as allowance for personal income tax, subject to a maximum of Baht 500,000

Income tax exemption for benefit obtained from the National Savings Fund as a result of reaching the age of 60, becoming incapacitated or death

Effective date: For assessable income from 2015 onwards

The contribution to a National Savings Fund, a registered provident fund, a retirement mutual fund or a qualified pension life insurance premium - either one fund or several funds

– allowance subject to a maximum of Baht 500,000 in total for each tax year

4818 October 2016Maximise Shareholder Value 2017

6.2 Contribution to the National Savings Fund(Ministerial Regulation No. 314 dated 11 April 2016)

PwC

6. Personal income tax

Purpose: To encourage people to invest on a long-term basis and maintain the stability of the Securities Exchange of Thailand

Benefits:

Investment in long-term investment fund (LTF) allowed for tax deduction up to 15% of assessable income received which is subject to income tax, with a maximum of Baht 500,000 in any tax year

Gain from redemption of investment units in the above LTF exempted from income tax

Eligible periods: 1 January 2016 to 31 December 2019

LTF must be held for at least seven calendar years, except in case of

incapacity or death

4918 October 2016Maximise Shareholder Value 2017

6.3 Extension of tax deduction for investments in LTF(Ministerial Regulation No. 317 dated 28 June 2016)

PwC

6. Personal income tax

Purpose: To continue the promotion of domestic travel so as to benefit the economy of the country and assist tourism operators

Benefits:

Deduction of up to Baht 15,000 granted for domestic travel and hotel expenses

Eligible period:1 January 2016 to 31 December 2016

5018 October 2016Maximise Shareholder Value 2017

6.4 Deduction for expenses on domestic travelling and hotels (Ministerial Regulation No. 316 dated 17 June 2016)

PwC

6. Personal income tax

Purpose: To promote OTOP products

Benefits:

Deduction of up to Baht 15,000 granted for amounts paid to operators of registered One Tambol One Product (OTOP) businesses

(Operator must have registered for VAT)

Eligible period:

Between 1 and 31 August 2016

5118 October 2016Maximise Shareholder Value 2017

6.5 Deduction for spending on OTOP products(Ministerial Regulation No. 318 dated 29 July 2016)

PwC

752

18 October 2016Maximise Shareholder Value 2017

PwC

7. Other

Purpose: To increase competition potential in the motor vehicle industry in the country and attract investment to make Thailand the centre of R&D and testing of prototype vehicles in the region

7.1.1 Benefits – VAT exemption (Royal Decree No. 613 dated 10 June 2016)

VAT exemption granted on import of prototype cars or motorcycles for R&D and testing which are approved to be exempted from excise tax under the law

Effective date:

1 January 2016

Importers – being approved by the Director-General of the Excise Department to carry on R&D or testing of vehicles

5318 October 2016Maximise Shareholder Value 2017

7.1 Prototype cars or motorcycles for R&D and testing

PwC

7. Other

7.1.2 Benefits – Depreciation of prototype cars (Royal Decree No. 620 dated 1 August 2016)

Total cost of prototype cars allowed to be the base for depreciation (not limited to Baht 1 million)

Effective date:

The prototype cars must be acquired from 1 January 2016 onwards.

Prototype cars used for research, development or testing and approved to be exempted from excise

tax under the law

5418 October 2016Maximise Shareholder Value 2017

7.1 Prototype cars or motorcycles for R&D and testing (Cont’d)

PwC

7. Other

7.1.3 Benefits – No VAT on prototype cars or motorcycles produced (Notification on VAT No.210)

No VAT imposed on prototype cars or motorcycles produced to businesses carrying on research, development or testing which obtain approval from the Director-General of the Excise Department

Effective date:

1 January 2016

Prototype cars or motorcycles used for research, development or testing and approved to be

exempted from excise tax under the law

5518 October 2016Maximise Shareholder Value 2017

7.1 Prototype cars or motorcycles for R&D and testing (Cont’d)

PwC

7. Other

7.2.1 Ministerial Regulation No. 319 dated 3 August 2016

Benefits:

Bad debts written off are tax deductible without the need to follow the procedures under MR 186 under conditions.

Effective date:

Accounting periods beginning on or after 1 January 2011

Bad debts written off by non-life insurance company for re-insurance compensation due from the flooding in

Thailand from 1 July to 31 December 2011

5618 October 2016Maximise Shareholder Value 2017

7.2 Bad debts written off – need not follow procedures under Ministerial Regulation No. 186

PwC

7. Other

7.2.2 Debt restructuring (Ministerial Regulation No. 321 dated 12 September 2016)

Benefits:

Bad debts written off are tax deductible without the need to follow the procedures under MR 186 under conditions.

Bad debts written off by financial creditors due to debt restructuring framework prescribed by the Bank

of Thailand executed from 1 January 2015

5718 October 2016Maximise Shareholder Value 2017

7.2 Bad debts written off – need not follow procedures under Ministerial Regulation No. 186 (Cont’d)

PwC

7. Other7.3 Amendment of certain criminal punishments under the Revenue Code (The Revenue Code Amendment Act No.41 dated 10 Feb 2016)Purpose: To cover certain criminal offences and increase the punishment rate to be appropriate Effective date: 25 February 2016

Section Previous punishment Amendment

35 For only late filing of CIT return under sec. 17, fine under Sec 35 is not exceeding Bht 2,000.

To add fine of not exceeding Bht 2,000 under sec. 35 for not filing documents necessary to compute CIT together with the audited financial statements under Sec 69 (Total fine of not exceeding Bht 4,000)

37, 90/4(6)

To give false statement, fraud, deception or any other similar method to evade tax payment is subject to imprisonment from three months to seven years and fine of Baht 2,000 to Baht 200,000

To include the request for tax or VAT refund

37 bis Intentionally failure to file a return with a view to evading payment of tax and duty is subject to fine of not exceeding Baht 5,000 or imprisonment not exceeding 6 months or both

To increase punishment:

fine of not exceeding Baht 200,000 or imprisonment not exceeding one year or both

5818 October 2016Maximise Shareholder Value 2017

PwC

7. Other

Method and due date: 7.4.1 Stamp duty must be paid in cash within 15 days from the date on which

certain instruments are executed in Thailand

Instruments in this category include the following:

Lease of land, buildings, other construction or floating rafts with rental

of THB 1 million or more

Hire of work agreement with remuneration of THB 1 million or more

5918 October 2016Maximise Shareholder Value 2017

7.4 Method and due date for stamp duty to be paid in cash for certain instruments (Notification re: stamp duty No. 55 dated 26 August 2016)

PwC

7. Other

Method and due date: 7.4.2 Stamp duty paid in cash twice a month:

1. By the 22nd of the month for instruments executed during the first half of the month.

2. By the 7th of the following month for instruments executed during the second half of the prior month.

Instruments in this category include the following:

Hire-purchase of property for lessors who are juristic persons, financial institutions or operators of personal loan business under supervision

Suretyship for which a financial institution (excluding insurance company) is a party to the contract

Loan of money or agreement for bank overdraft

6018 October 2016Maximise Shareholder Value 2017

7.4 Method and due date for stamp duty to be paid in cash for certain instruments (Notification re: stamp duty No. 55 dated 26 August 2016) (Cont’d)

PwC

7. Other

Method and due date:

7.4.3 Stamp duty must be paid in cash on the registration date for the following instruments:

Receipt issued in connection with a sale, sale with right of redemption, hire-purchase or transfer of ownership of a vehicle registered under the law, whereby both the seller and the hire-purchaser of the vehicle are juristic persons. Used vehicles are not included in this regulation.

6118 October 2016Maximise Shareholder Value 2017

7.4 Method and due date for stamp duty to be paid in cash for certain instruments (Notification re: stamp duty No. 55 dated 26 August 2016) (Cont’d)

PwC

7. Other

Previous method New methodPublicly Accountable Entity (PAE)

GAAP GAAP

NPAE Subsidiary ofPAE

Contract, installment or percentage of completion

GAAP

Other NPAE Contract, installment or percentage of completion

Contract, installment or percentage of completion

6218 October 2016Maximise Shareholder Value 2017

7.5 Real estate development business (Taw Paw 262/2559, effective date 31 August 2016)

PwC

PART II

6318 October 2016Maximise Shareholder Value 2017

PwC

1. Draft Act to amend the Revenue Code/ Draft of other Acts/Draft regulations

Cabinetresolution

Subject

13 Sep 2016 7% VAT rate extension for one more year from 1 October 2016 until 30 September 2017

23 Aug 2016 To amend the Investment Promotion Act, Drafts of Special Economic Zone Act, Draft of Act regarding increasing the ability of target industries to compete in Thailand

9 Aug 2016 Tax measures to promote individuals operating a business as a juristic person

2 Aug 2016 -To amend the Revenue Code for e-tax filing, e-withholding tax, e-tax invoices and receipts and electronic information remittance (E-payment plan)-Double deduction for expenses to support SME and investment in rural areas

26 July 2016 Deposits with nature similar to life insurance can be claimed as an allowance in PIT computation

12 July 2016 Extension of tax reduction (0.1% - 3%) for business operators located in specific development zones (Narathiwat, Pattani, Yala and part of Songkha) for three years from 1 January 2018 to 31 December 2020and double deduction of the CCTV costs in these zones

6418 October 2016Maximise Shareholder Value 2017

PwC

1. Draft Act to amend the Revenue Code/Draft of other Acts/Draft regulations (Cont’d)

Cabinetresolution

Subject

7 June 2016 Draft of Land and House Tax law so as to replace House and Land Tax Act B.E. 2475 including Local Development Act B.E.2508

10 May 2016 To amend Sec 41 bis (transferor is taxpayer) to be consistent with Sec 42(26), (27):Parent as transferor of ownership or possessory right in immovable property without remuneration is exempt from tax on the portion of income not exceeding Baht 20 million for each legitimate child.

26 Apr 2016 Anti-tax evasion and fraud according to the Financial Action Task Force (FATF) –temporarily seize and attach property, treated as AML offence, etc

19 Apr 2016 Restructure of Personal income tax: tax rates, tax allowances and deductions, minimum annual income required for filing personal income tax return

1 Mar 2016 Law on international coordination for exchange of information for tax collection purposes

7 May 2015 Draft of transfer pricing law

6518 October 2016Maximise Shareholder Value 2017

PwC

2. Non-Publicly Accountable Entities (NPAEs)

Non-complex NPAEs

Adopt only part of TFRS for SMEs No TAS 12

Complex NPAEs Apply full set of TFRS for SMEs

TAS 12 extensions to 2019

NPEs

6618 October 2016Maximise Shareholder Value 2017

PwC

2. Non-Publicly Accountable Entities (NPAEs) (Cont’d)

PAEs

NPAEs

NPAEs

PAEs

NPAEs

NPAEsAssociate company, Subsidiary, Joint venture

Associate company, Subsidiary, Joint venture

Associate company, Subsidiary, Joint venture

Complex NPAEs

6718 October 2016Maximise Shareholder Value 2017

PwC

Contact

Somsak AnakkaselaPartnerTel: +66 (0) 2344 [email protected]

6818 October 2016Maximise Shareholder Value 2017

Thank you

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2016 PricewaterhouseCoopers Legal & Tax Consultants Ltd. All rights reserved. PwC refers to the Thailand member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.