unlocking asia's trade potential for ireland

DESCRIPTION

Asian markets are experiencing a period of remarkable economic, demographic and technological change that is driving global demand and expanding consumer markets. This specially commissioned economic report by Asia Matters details how Ireland can leverage its competitive advantages in key sectors and targeted markets to further unlock Asia’s trade potential. Authored by leading economist and Newstalk economics editor, Marc Coleman, with contributions by Asia Matters’ team of Asia experts, the report aims to provide Irish business leaders and policy makers with key data and strategic analysis on Asian markets and outlines new ways to win investment and grow exports.TRANSCRIPT

!

UNLOCKING ASIA’S TRADE POTENTIAL FOR IRELAND

!!!!!

!!!!!!

!!!!!!!!

!!!

!!!

An Economic Report by Asia Matters

!

!!Author!

Marc Coleman, Managing Director, Octavian Consulting Limited & Economics Editor, Newstalk, !

in collaboration with the team of experts at Asia Matters. !

!Editorial Team!

Martin Murray, Executive Director, Asia Matters!

Ronan Lenihan, Director for Operations and Development, Asia Matters!

Stephanie FitzGerald-Smith, Director for Marketing & Communications, Asia Matters!

!Special Thanks!

Special thanks to Alan Dukes, Chairman, Asia Matters, and to Tom Hardiman, Chairman, Chester Beatty Museum for their invaluable insights. !

The author would particularly like to thank Kevin Sherry & George Kiely of Enterprise Ireland for sharing their expertise.!

!Published by!

Asia Matters Ltd. Dublin, Ireland, October 2014.!

Copyright © 2014. All rights reserved. No part of this publication may be reproduced without the prior permission of Asia Matters.!

The selection and compilation of statistics and other data contained in the volume are the responsibilities of the author and editorial team.!

The analysis contained in the volume was carried out by the author and editorial team, based on independent research, as well as insights shared in discussions during Asia Business Week Dublin 2014.!

!Disclaimer!

This economic research report has been commissioned by Asia Matters to contribute to thought leadership for the benefit of further developing the Ireland Asia Trade relationship. The information in this report is given in good faith and is not investment advice, which is a matter for professional advisory services. The author and partners to this publication expressly disclaim all liability to any person or corporation in respect of any losses or other claims, whether direct, indirect, incidental, and consequential or otherwise arising in relation to the use of this report as the basis for any business decision or in connection with any advice given to third parties.

© Asia Matters 20142

The author of this report, Marc Coleman, examines the profound impact of Asia on the global economy and how this is creating new trade opportunities for Ireland.!!By commissioning this research, Asia Matters aims to deepen the understanding of this change and help policy-makers and economic agents in Ireland and across Asia to use these insights to contribute constructively towards building lasting connections. !!!

The current economic climate in Asia holds vast potential for Ireland’s open economy which thrives on international cooperation and trade. With Asia’s rising economic power, new markets have opened up to meet the growing consumer demand. Parallel to this, since the crisis, savings rates in Asian economies have remained traditionally high, while European economies have lacked investment. This imbalance has raised the possibility of greater investment into the EU.!!We see enormous opportunities for the development of trade and investment flows both into and out of Asia. This report sets out to identify the nature and possible scale of some of these flows, thus providing deeper insights for influential business and government stakeholders. !!Ireland’s key advantages and market leader status in sectors such as food and agri-tech, education, ICT, financial services and tourism, matched with the growing commitment of Team Ireland in Asia, can see Ireland build influence and establish a valuable brand to drive trade development in key Asian markets. !!With this independent research, Asia Matters looks forward to contributing in a positive way to Ireland’s trade strategy towards key Asian partners. We look forward to engaging further with Asian and Irish stakeholders in our future conferences and publications.!!!!Alan Dukes,!Chairman, Asia Matters!!

3 © Asia Matters 2014

!!Foreword: Mr. Alan Dukes, Chairman, Asia Matters

!

!!!!!!!!!!!!

© Asia Matters 2014�4

Figures !!Figure 1: Population (millions) of selected Asian countries in 2011………………………………. 11 !

Figure 2: Workforce of selected Asian countries (millions) - 2011………………………….….….. 12!

Figure 3: GDP per capita* of selected Asian countries in 2011………………….….….….….…… 13!

Figure 4: Asian convergence: Cumulative growth (%) 2009-2011 and GDP per capita (US$)… 13!

Figure 5: Household consumption as % GDP and GDP per capita - 2011…….….….….……….. 15 !

Figure 6: Asians as adaptors of new technology - 2014………………………….….….….…..…… 16!

Figure 7: Internet users per 100 persons and GDP per capita…………………..….…….….….…. 16!

Figure 8: Asia’s convergence with EU levels of urbanisation (% of population ……………….. 17!

Figure 9: Target export levels and growth for 2019……………….……………………….….……… 20!

Figure 10: Growth trajectory for Irish Food and Drink Exports 2010-2020………….….….…..… 23 !

Figure 11: Food and drink industry share of the Irish economy and Chinese market growth………… 23!

Figure 12: Services exports from Ireland……………….…………………………………………..…. 24!

Figure 13: Growth in imports of services 2009-2013 in selected counties………………………. 25!

Figure 14: Ireland’s goods exports to China in 2013 by main category….………..…………….. 29!

Figure 15: Ireland’s goods exports to India in 2013 by main category..…………..……………… 32!

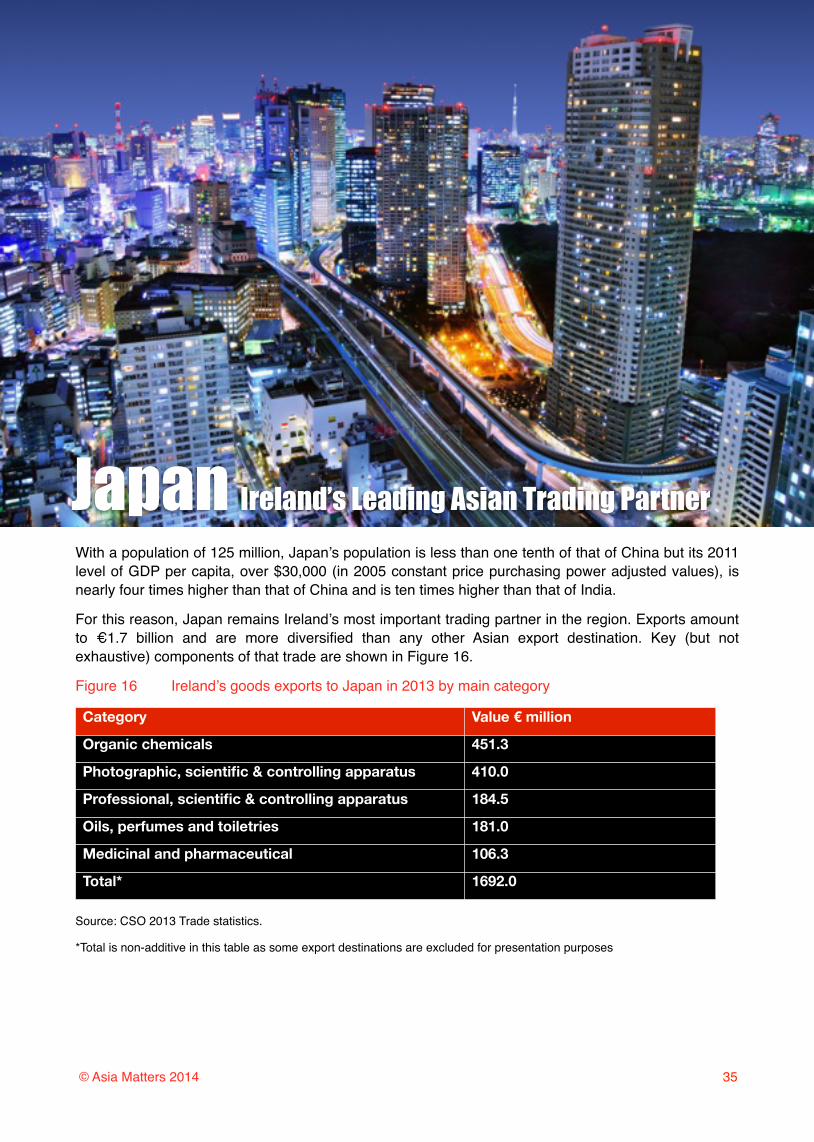

Figure 16: Ireland’s goods exports to Japan in 2013 by main category….…………..………….. 35!

Figure 17: Ireland’s goods exports to South Korea in 2013 by main category…….……..……... 38!

Figure 18: Ireland’s goods exports to Singapore in 2013 by main category…..……….……….. 40!

Figure 19: Ireland’s goods exports to Hong Kong in 2013 by main category….………………... 43!

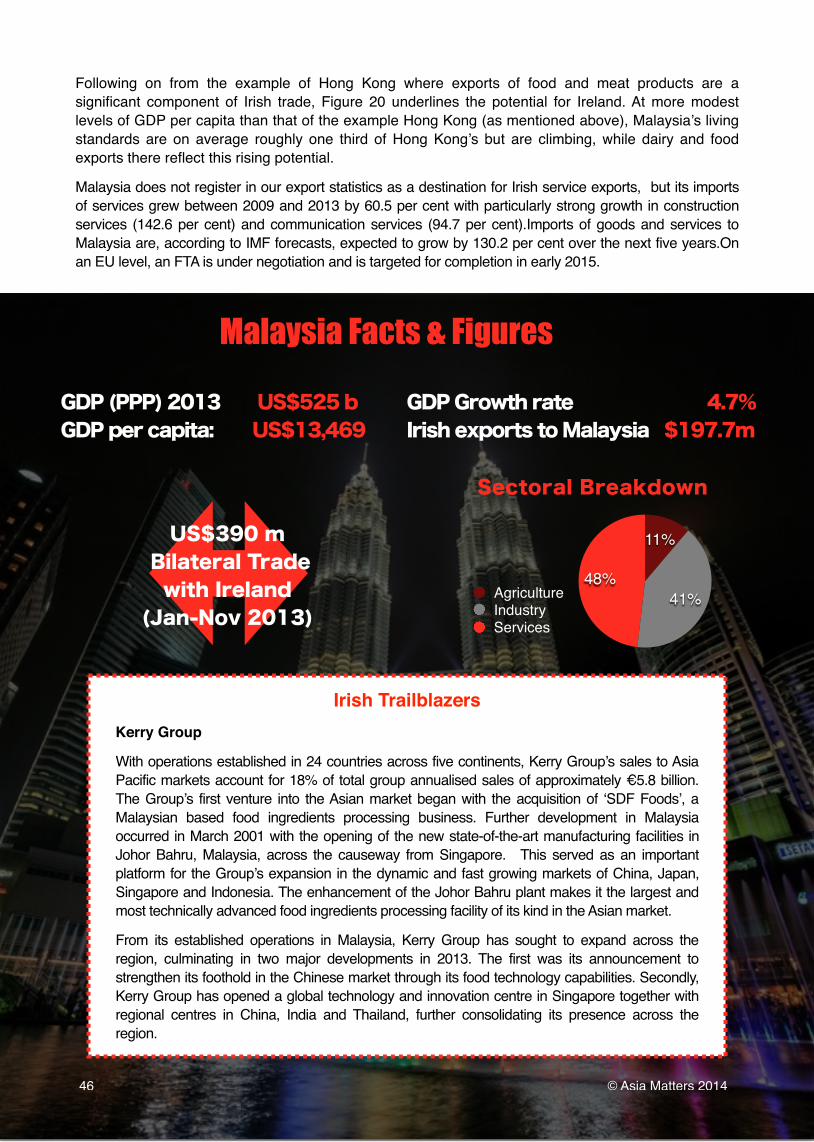

Figure 20: Ireland’s goods exports to Malaysia in 2013 by main category…….………..……….. 45!

Figure 21: Ireland’s goods exports to Thailand in 2013 by main category..…………….……….. 47!

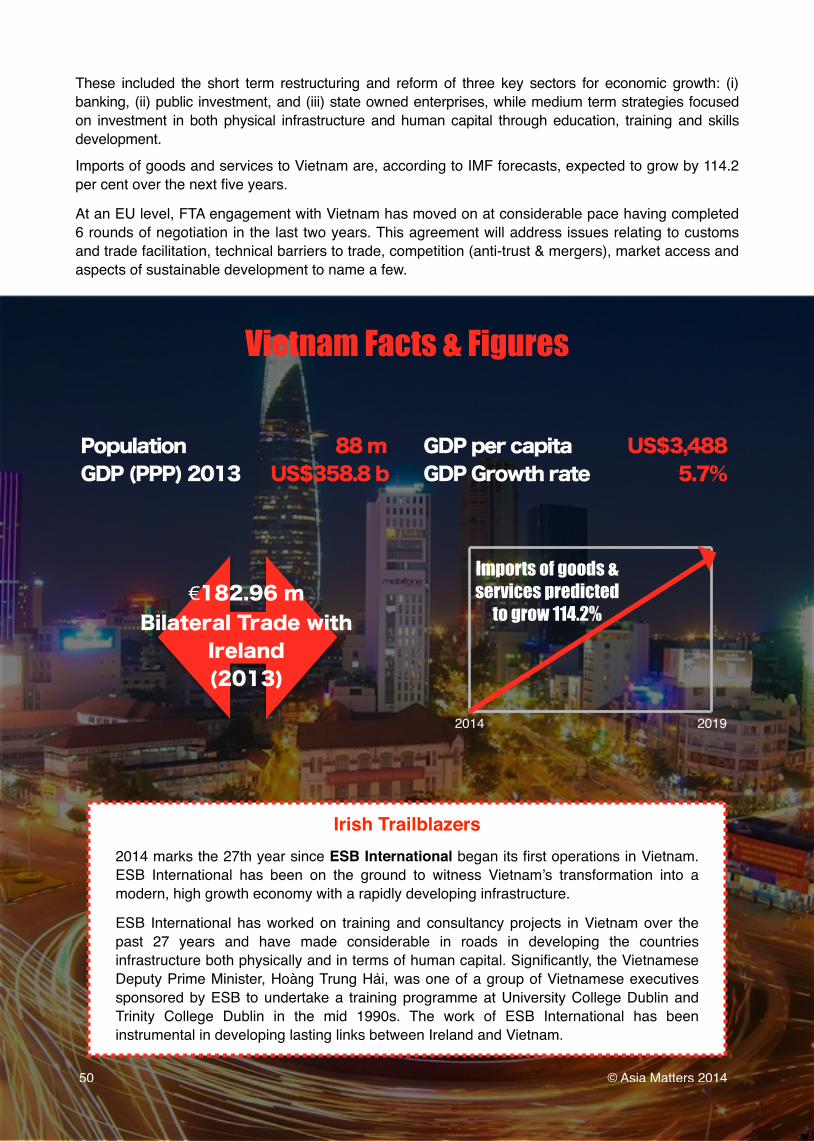

Figure 22: Ireland’s goods exports to Vietnam in 2013 by main category……………………….. 49!

Figure 23: Ireland’s goods exports to The Philippines in 2013 by main category.…………..…. 51!

Figure 24: Ireland’s goods exports to Indonesia by goods category by main category………. 53!

Figure 25: Standard & Poor’s sovereign debt rating….………..……………………………………. 60!

Figure 26: Indicators of economic risk………………………………………..……………………….. 61!

� ! © Asia Matters 20144

© Asia Matters 2014�5 © Asia Matters 2014! ! ! � 5

!Table of Contents!!!List of Figures.……………………………………………………………………………………………….. 4!

About Asia Matters/ About the Author ………………………………………………………………….. 6!

Introduction ………………………………………………………………………………………………….. 7!

An Asian Century ………………………………………………………………………………………….. 11!

Convergence is King …………………………………………………………………………………..….. 13!

Ireland’s Opportunity ……………………………………………………………………………………. 19!

Country by Country overview ………………………………………………………………………….. 28!

Risks ………………………………………………………………………………………………………….. 58!

Conclusions …………………………….……………………………………………………………….….. 62!

Annex: List and status of EU-Asia Free Trade Agreements ……………….…………………….….72!

!

!

This report outlines the significant potential to further develop Irish business connections with key partner countries across Asia, as the key region driving global economic growth and activity. It aims to shed light on key markets and sectors where Ireland has a competitive advantage. It also provides

© Asia Matters 2014�6

!

!About Asia Matters !!!Asia Matters is an economic think tank based in Dublin dedicated to developing Ireland Asia and EU Asia business relations.!

It is an independent, not for profit organisation with a strong educational remit delivered through business briefings, conferences, policy research and publications.!

Within Ireland, Asia Matters provides thought leadership and business connectivity through events such as the annual ‘Asia Business Week Dublin’ summit and publications such as the annual ‘Ireland Asia Business Yearbook’, the book of reference for bilateral trade relations.!

Within Asia, Asia Matters hosts the EU Asia Top Economist Round Table (TERT) series in association with key stakeholders on the ground. In 2014, the TERT series takes place in Tokyo and Beijing.!

Asia Matters works in close partnership with government, business and academic stakeholders in Ireland, the EU and across Asia. The Chairman of Asia Matters is Alan Dukes, the former Irish Minister for Finance.

!!!About the Author!!Marc Coleman is a leading national economic commentator in Ireland with a weekly economics column in Ireland’s largest selling broadsheet newspaper, the Sunday Independent, and an award winning radio show on Newstalk 106-108fm. Marc is the Managing Director of Octavian Consulting Limited (www.octavian.ie), which provides economic and business research and analysis to the highest international standards.!

Previously an economist with the European Central Bank and Irish Ministry of Finance, Marc was also Economics Editor of the Irish Times and is a leading figure on Ireland’s public speaking circuit. He holds a scholarship MBA from Ireland’s leading business school, an honours economics degree from Trinity College, a Master’s economics degree from University College Dublin and also a prestigious Advanced Studies Programme qualification from the Kiel Institute of World Economics.!

As well as Asia Matters, Marc has worked with Ernst & Young, the European Central Bank (ECB), KPMG, the Irish German Chamber of Commerce and a list of other prestigious organisations.

� ! ! © Asia Matters 20146

This report outlines the significant potential to further develop Irish business connections with key partner countries across Asia, as the key region driving global economic growth and activity. It aims to shed light on key markets and sectors where Ireland has a competitive advantage. It also provides data and analysis outlining ambitious targets for government and business stakeholders to meet in their engagement with key partners in Asia.!

!Renaissance or Revolution - Asia’s Economic Rise!

Between 2009 and 2011, while most of Europe and the US was gripped in recession, the Chinese economy grew by 20 per cent, the Indian economy grew by 25 per cent and the Indonesian economy grew by 18 per cent. This is no mere accident of economic survival. It is a long, deep and strong process, no less than an economic renaissance. In 2011, the Asian Development Bank reported on the scale of the region’s economic potential: “Asia is in the middle of a historic transformation. If it continues to follow its recent trajectory … Asia would regain the dominant economic position it held some 300 years ago, before the Industrial Revolution”. !1

This revolution is not confined to China or India. Although dominant at present, the opportunities for exporters presented by China and India are complemented by the rise of ASEAN, a bloc of ten countries 2

who promote closer ties with each other and neighbouring economies in the fields of economic cooperation, free trade, energy, pollution and migration. ASEAN alone has been cited by a McKinsey report as having the potential to become 3

the world’s 4th largest economy by 2050, while Indonesia – the regions largest

economy – could be the world’s 7th-largest economy by 2030, overtaking Germany and the United Kingdom, according to a separate McKinsey report . 4

Interestingly, Myanmar – an ASEAN member currently undergoing rapid development with huge economic potential – will have more than half the world’s consuming class living within a five hour flight of its commercial capital Yangon by 2025 and will be the centre of a road and rail network linking China, India and Southeast Asia . While there are recent signs of 5

challenges ahead in some Asian countries, as well as debt related risks familiar to us in Ireland, Asia’s medium to long term potential for Ireland is significant.!

In short, Asia is not just a region of growth potential for Ireland. Rather, Asia’s rise is a new global reality for which business and government must prepare strategic responses.!

!!

7 © Asia Matters 2014

!!Introduction

Asian Development Bank, 2011 “Asia 2050: Realising the Asian Century”1

ASEAN was founded in 1967 and its current membership includes Indonesia, Malaysia, Philippines, Singapore, Thailand, 2

Brunei, Vietnam, Cambodia, Laos, Myanmar

Vinayak HV, Fraser Thompson and Oliver Tonby, McKinsey 2014 “Understanding Asean: Seven things you need to know”3

Raoul Oberman, Richard Dobbs, Arief Budiman, Fraser Thompson and Morten Rosse, McKinsey, 2012 “The archipelago 4

economy: Unleashing Indonesia’s potential

ibid 45

Asian Opportunities!

With a combined population touching 3 billion people, Asia’s growth represents a 6

unique economic opportunity for Ireland. Since 1999, Asia has been on the government’s radar screen with the launch of the 1999 - 2009 Asia Strategy, a comprehensive plan to build substantial trade and investment links across Asia. The growth in opportunities for Irish business in Asia since the end of this strategy period has, despite recession, not abated. The trajectory of growth referred to by the Asian Development Bank in 2011 has not just been maintained but, as this report shows, promises to continue – albeit more moderately – for the next 5 years and beyond.!

The projected macroeconomic growth in Asia significantly understates the potential for trade gains in the region for Ireland. Thanks to both demographic and economic factors, demand in many sectors is growing at even faster rates than the overall economy. Whether macroeconomic or sectoral, Asia’s potential comes with associated political, governance, legal and cultural risks and challenges. The failure to sustain growth potential - either due to poor economic policies or to external market shocks - is a lso a major vulnerability. This is particularly the case where long term economic planning is absent or weak and where the transition from resource driven growth (low cost labour and capital) to technology and productivity driven growth is uneven or stalled. Asia will continue to be a key global competitor for scarce energy resources.!

These problems merely underscore the importance of fully engaging with the Asian challenge. Home to half the world’s population, Asia should aspire to account for a more appropriate share of global economic output in the coming decades and close the gap in terms of per capita incomes to those of Europe and the US.

While not the case at the moment, Asia’s rapid pace of growth means that the coming decades will see greater convergence with European and US living standards for the growing Asian middle classes. As that happens, Ireland must not be left behind.!

This emerging middle class, accompanied by massive urbanisation and a transformation of financial services, represent major potential for Ireland across Asia as demand rapidly rises for products and services, such as dairy and meat products. These are areas in which Ireland has a competitive advantage and should use this advantage accordingly.!

!Asia’s Growth Story !

In some cases, demand is growing exponentially. However, this is mostly due to “low base” effects, whereby imports are starting from a very low level. Nonetheless this does not alter the fact that the speed of growth offers huge potential for those ready to respond to rising demand. For instance, meat imports in 2013 rose by a staggering 248 per cent and 390 per cent higher in China and Thailand respectively from their 2009 levels. Demand for fish imports in Pakistan, grew by 1089 per cent between 2009 and 2013. While these growth rates must be qualified by their very low base, the reality is that the rate at which Asian demand is rising in specific areas presents huge opportunities for Irish business as new consumer markets open and mature. !

Even more mundane growth rates are strong enough to offer sustained returns to those who devote the time and resources to enter key Asian markets.!

Growth in internationally traded service sectors is impressively fast. In China, demand for financial services imports rose by 427 per cent between 2009 and 2013. In India, demand for imported commercial services rose by 60 per cent, while in Indonesia demand for imported government services rose 126.3 per cent during the same period.!

In the construction sector where doubts have emerged about China’s rate of building, there are new growth centres emerging to replace demand. For instance, in Malaysia, construction imports rose by 142.5 per cent between 2009 and 2013, while in Hong Kong, they rose by 171 per cent in the same period.

© Asia Matters 20148

For the purposes of this report ‘Asia’ refers to 16 countries, namely, China, Japan, India, Pakistan, Bangladesh, South 6

Korea, and the 10 ASEAN states mentioned above.

Each of these categories represent areas where Irish companies are doing well and can continue to succeed.!

!Targeting Growth!

Efforts by successive governments to expand trade in the region have proved highly successful. In 2011, the Irish Exporters Association, through their Asia Trade Forum programme, set out their plan, entitled “Trading with the Asia Pacific Region 2011-2015”. At the time it described the number of Irish companies with significant presence in Asia as “disappointingly low”. Initiatives contained within the plan - some short term such as a “visa review” for selected Asian countries, some long term such as the “increased Government funding, practical commitment and resources” - are seeing positive outcomes.!

Last year, indigenous exports to the region grew by 17 per cent. However, Ireland’s share of exports remains much lower than it should be. Asia, as defined by this report, accounts for one quarter of global GDP, nearly a third of global trade flows and half of the global population. Despite these facts, the region makes up just 6.2 per cent of our total exports. Although, we are certainly making progress in unlocking Asia’s vast potential, there is much further to go.!

HSBC, in a recent report on Ireland’s trade forecast, estimate that ‘the fastest growing markets for Irish exports are expected to be in China, Vietnam and Malaysia, with double digit export growth to these countries expected out to 2030’. The report goes on to encourage ‘endeavours to diversify trade towards fast-growing emerging economies’ with particular attention paid to leveraging Ireland’s competitive advantage and capacity in food and agribusiness . !7

To illustrate, by merely keeping pace with projected import growth rates in the region, we could see Ireland’s exports to the region nearly double over the next 5 years, this would result in many positive implications for employment, tax revenue and domestic demand spill over effects. By strategically targeting that growth to zone in on sectors that are poised for particularly strong growth, we could do even better than this.!

This can be achieved. The success of indigenous entrepreneurs, combined with the work of Enterprise Ireland and a host of government led supports have enabled a significant expansion in the region. However, as this report sets out to illustrate, multiplying that effort could yield significant returns. The good news is that while demand is moderating in some Asian countries the region is expected to remain a powerhouse of demand. According to 2014 IMF forecasts, import demand across Asia over the 2014 – 2019 horizon is expected to rise and maintain pace with the impressive rates of the past 5 years.!

Unlike any other part of the world and no other time in history, Asia presents Irish exporters with the opportunity for sustained and significant growth. By focusing attention on key sectors and demographics, particularly in urban areas, companies can grasp these opportunities. By giving Asia adequate status in terms of resources and attention via policy supports, government and government agencies can strongly assist their success.!

Such efforts should be informed by Ireland’s areas of strong competitive advantage such as food and agri-tech, business services, tourism and the education sector. A brief glance at two of these traditional sectors is enough to illustrate the enormity of opportunities which exist for Ireland.!

!Food and Agri-tech!

In the food sector, the government has formed the strategic objective of growing Ireland’s capacity to supply food to 50 million people by 2020, thus raising food exports to €12 billion by 2020 , while HSBC 8

estimates agricultural exports to rise by 40 per cent by 2030 . As the analysis below confirms, food demand 9

9 © Asia Matters 2014

HSBC Global Connections, September 2014, ‘Ireland Trade Forecast Report’7

Department of Agriculture, Fisheries and Food July 2010 “Food Harvest 2020”8

ibid 79

in Asia is rising so rapidly that the region has the capacity to absorb most if not all of the increased exports envisaged in that target period. Potential links extend far beyond food supply, following a high level Chinese delegation visit to Ireland in June 2013, Vice Agriculture Minister Zhang Taolin remarked, “Ireland is leading the whole world in terms of agriculture, in part icular agricultural science and technological advancement” . Across 10

Asia, Ireland can play a leading role in assisting the transition from traditional to modern agricultural methods.!

!Tourism!

The Asian view of Ireland’s tourism potential is equally positive with China’s largest online travel agent Ctrip recently naming Ireland the “best potential destination” for 2014. Combined with the strong personal connections and positive impressions, created by Ireland in the hearts and minds of Chinese residents and visitors, this is an excellent basis for a dramatic increase in tourist activity from a new and vibrant source. Indeed, Ireland’s valuable soft power elements, such as the global success of Riverdance and other popular and traditional culture icons have made a meaningful contribution to Ireland’s attractiveness as a tourism destination.

© Asia Matters 201410 Alison Healy, Irish Times, June 4th 201310

The resilience of Asia in defying the global crisis in the last five years has been impressive. Indeed it is hard to exaggerate the scale of growth in the region in the last three decades. From just under 1 billion people in 1980, the Chinese population has risen by approximately 300 million to over 1.3 billion and continues to rise. From some 700 mil l ion in 1980, India’s population rise has been even more dramatic, with a rise of over half a billion to a current level of 1.24 billion. In lesser populated countries, growth has been remarkable, so much so that the combined population of the “Next 11” now exceeds 11

1 billion, as Figure 1 illustrates. !

As is later explored in this report, it is in some of the “Next 11” countries that the most exciting opportunities for growth are occurring, for instance, the Vietnamese population has risen from 54 to 88 million s ince 1980, whi le the Indonesian population has risen from 151 to over 250 million since 1980. The impact on demand in key sectors of potential Irish interest, such as food and business services, in the “Next 11” is significant. Once again drawing an example from Vietnam, since 2009 Ireland has exported €5 million worth of goods to Vietnam in the dairy products sector, a sector that has seen demand rise by 68 per cent in that period. Speaking during Asia Business Week Dublin in June 2014, H.E. Bui Thanh Son, Vice Minister for Foreign Affairs offered more insights into sectors where Ireland might benefit from higher demand: “The strengths of Ireland lie in energy, agricultural exports, dairy and pharmaceutical products. These are also the items for which Vietnam has demand”. IMF forecasts for total import volumes up to 2019 in Vietnam indicate

massive opportunities for those entering the market now to make significant gains. This will be addressed in later sections of the report.!!Figure 1! Population (millions) of Selected Asian Countries in 2011*!

Source: Penn Wold Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World Table”. Data for 2011.!

* US and Ireland are used as reference points throughout the report!

!Those opportunities are weighed heavily in favour of the growth in Asia’s workforce and accompanying growth in spending power. According to McKinsey , 12

the class of consumers – defined as those enjoying a disposable level of income of over $10 a day - is set 13

to rise to 4.2 billion persons by 2025 and most of this growth will occur in urban Asia. This equates to a rise of approximately $15 trillion in world consumption over the next decade . !14

As Figure 2 shows, China will contain a strong plurality of this rise in demand by virtue of the sheer size of its relative workforce, which exceeds those of

11 © Asia Matters 2014

The ‘Next 11’ refers to Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, 11

Hong Kong and Singapore. The ‘Next 11’ have a combined population exceeding 1 billion.

McKinsey Quarterly 2012 Number 4 “Emerging Markets on the Move”12

On Purchasing Power Parity basis, that is adjusting for differing relative prices of consumer goods in different countries13

Source: The author’s interpolation of McKinsey estimates.14

!!An Asian Century

India, Indonesia and the US put together. Chinese cities in particular – not just megacities such as Beijing, Shanghai and Shenzhen but a multiplicity of medium sized cit ies – wil l represent huge opportunities in this regard as the government emphasises sustainable economic development in the regions. For consumer goods, China also represents a further opportunity as its relatively advanced retail sector is conducive to consolidation and economies of scale in terms of logistics and distribution. Factors that are important considerations for exporters from a small island nation like Ireland.!

As will be illustrated later in this report, China, India and the “Next 11” are all expected to have import growth of at least 30 per cent between now and 2019 with most of these markets expected to grow significantly faster.!

Another key element shaping the Asian century will be the leadership shown across the region. Xi Jinping has established a strong anti-corruption stance, in part to prepare for far reaching economic reforms. Abenomics has seen major reforms in an effort to kickstart growth in Japan. The three arrows - fiscal stimulus, monetary easing, structural reforms - has been seen as a proactive attempt to jolt the Japanese economy out of a two decade long slump. The election of Narendra Modi in India and Joko “Jokowi” Widodo in Indonesia sees two major emerging powers take on reform minded new governments that have raised expectations considerably. In India, opt imism is high that Modi ’s new government can deliver on its mantra of ‘less government, more governance’ and will be more result-oriented, target driven and accountable in laying the foundations for India to become a global economic powerhouse. Similarly, Indonesia’s Jokowi has been charted as the right man to take on the many challenges facing Indonesia, s u c h a s i n e q u a l i t y, i n a d e q u a t e infrastructure, and restrictive labor laws, while also building the institutions to

sustain Indonesia’s remarkable economic rise.!

Figure 2! Workforce of Selected Asian Countries (millions) - 2011!

Source: Penn World Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World “. Data for 2011

© Asia Matters 201412

784.4%%

495.7%%

141.8%%

109.5%%

61.9%%

53.2%%

50.4%%

49.4%%

40.1%%

34.6%%

24.1%%

12.4%%

3.6%%

3.1%%

1.8%%

%442.4%%

0.0%% 100.0%% 200.0%% 300.0%% 400.0%% 500.0%% 600.0%% 700.0%% 800.0%% 900.0%%

China%

India%

US%

Indonesia%

Japan%

Pakistan%

Bangladesh%

Vietnam%

Thailand%

Philippines%

South%Korea%

Malaysia%

Hong%Kong%

Singapore%

Ireland%

The%"Next%11"%

Workforce%(millions)%

How can the most exciting opportunities be grasped by Irish companies? Spotting them is the first challenge and the “convergence story” is an essential prerequisite to doing that. Singapore has the highest GDP per capita, followed by Hong Kong, Japan and South Korea. This pecking order reflects the order in which open market economies were adopted in each country, with Singapore and Hong Kong leading the way as historic trading ports, while Japan and South Korea following quickly as they adapted new economic paradigms in the post war era. It is little surprise that following these nations are Malaysia, Thailand, China, Indonesia and India, whose levels of GDP per capita relative to one another closely resemble their relative positions with regards to embracing economic reforms. In other words, despite a rough and occasionally uneven process, there is a clear process of convergence over time, with lower income countries playing “catch up”. See Figure 3 for the GDP per capita of the countries analysed in this report. !

Figure 3 GDP per capita* of Selected Asian Countries in 2011!

Source: Penn World Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World Table“. Data for 2011!

*PPP adjusted 2005 $US!

** US and Ireland used as a reference point!

Figure 4 confirms this process of convergence by illustrating how, generally, countries with lower levels of GDP per capita have avoided recession to produce significantly higher rates of growth than most developed economies. The chart below gives historic growth data (2009 to 2011) but IMF projections for import growth suggest this relationship is also set to continue into the future, as shown further below. There are of course exceptional countries like Singapore, Hong Kong and South Korea that – despite already high living standards – are maintaining solid growth.!

Figure 4 Asian Convergence: Cumulative Growth (%) 2009-2011 and GDP per capita (US$)!

BG: Bangladesh, CH: China, HK: Hong Kong, IE: Ireland, IND: India, INDO: Indonesia, JP: Japan, ML: Malaysia, PH: Philippines, PK: Pakistan, SI: Singapore, SK: South Korea, TH: Thailand, VT: Vietnam !

Sources: Penn World Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World Table” !

!

13 © Asia Matters 2014

SG#

US#

HK#

IE#JP#

SK#ML#TH#

CH#

INDO#

IND#

PH#

VT#

PK#

BG#

45.00%#

0.00%#

5.00%#

10.00%#

15.00%#

20.00%#

25.00%#

30.00%#

0# 10,000# 20,000# 30,000# 40,000# 50,000# 60,000#

!!Convergence is King

Three convergence factors working in Ireland’s favour!Aside from growth in income per capita, three other “convergence” factors are working towards Ireland’s advantage as an exporter to the region. First, we should examine the challenges Ireland has faced as an exporting nation.!

As a small island whose indigenous exporters mostly lack critical mass to exploit large markets immediately, we have been at a historical disadvantage. Even adapting to scale requirements in our nearest trading partner, the UK, can present challenges for Irish SMEs. !

One good reason why Ireland’s share of exports to Asia is lower than it should be, may relate to the nature of growth in a developing country’s early stages of development. It is usually highly capital intensive and the profile of exports to that country are therefore necessarily highly weighted in sectors – heavy engineering, transport goods and industrial equipment – in which Ireland does not yet have a comparative advantage.!

A good example of this can be seen in Bangladesh where imports of rolling stock and shipping stock has risen by 2,700 per cent and 937 per cent respectively between 2009 and 2013. But as countries converge with higher levels of GDP per capita, consumption tends to replace investment as the leading component of growth. This, in turn, gives relatively more opportunities to SMEs compared to large c o n g l o m e r a t e s a n d t o c o u n t r i e s specialising in consumables compared to heavy industrial goods.!

!

1. Emerging consumers: “Hidden Tigers, Crouching Dragons”!!A determining factor in the extent in which consumer demand is ready to “take off” can be gauged by key elements, the level of GDP per capita as mentioned above and, secondly, the share of consumption in a country’s GDP.!

India is in this respect a “Hidden Tiger” in that its level of GDP per capita is low relative to that of China. Indian consumers will emerge but not just yet. China by contrast is a “crouching” (i.e. ’ready to pounce’) dragon in that - unlike India - its level of GDP per capita is now at or above the threshold at which consumers begin to enjoy goods and services taken for granted in the west.!

China is still “crouching” because like India the share of household consumption of GDP is still relatively low at 28 per cent, see Figure 5. Significantly lower in fact than peer countries in Asia. In Hong Kong, for instance, household consumption accounted for 62.5 per cent of GDP in 2011, more than double China’s level. In Japan the equivalent figure is 59.5 per cent. If China targets a level of consumption even half way between these peer benchmarks and its current level of consumption, the consequences for Chinese demand in coming decades for consumer goods will be profoundly positive.!

On March 14 2014, the National People’s Congress directed that consumer spending in China must rise. This gives rise to an intriguing opportunity in that not only are economic forecasts pointing to continued (albeit moderating in overall terms) economic growth, but government policy is set to concentrate this growth not in investment (where small countries like Ireland are at a relative disadvantage) but towards consumption (where small countries and SMEs can better leverage unique competitive advantages).!

!

© Asia Matters 201414

2. Etail revolution!!A key factor in grasping this opportunity will be technology and, in particular, the e-tail revolution. As shown in Figure 6, while earlier developers such as Hong Kong and South Korea have familiar patterns of telephone line subscription per 100 persons (60+) , someth ing new is happening in countries that were late developers. Malaysia, Thailand, Indonesia, the Philippines and Vietnam are leap frogging over some of their western counterparts through bypassing old technologies and embracing new ones with rates of cell subscriptions that are already over 100 per 100 persons.!

!

!!This ties in with a related and even more exciting development, internet usage, which in many low to middle income Asian countries is already higher than in some western countries. Figure 6 shows three broad groupings. In the case of high to medium GDP per capita countries (Hong Kong, South Korea, Malaysia), internet penetration is already very high. In the case of medium to low GDP per capita countries (China, Thailand, Vietnam and the Philippines), it is catching up. In the case of lower income per capita countries, it remains in its early stage of take-up. But a clear pattern of convergence and catch up seems apparent.

! © Asia Matters 201416

CountryGDPPC (2005) US$ Household consumption (% of GDP)

Singapore 51,644 33.1

US 42,646 75.9

Hong Kong 38,569 62.6

Japan 30,427 59.5

South Korea 27,522 51.0

Malaysia 13,469 52.2

Thailand 8,491 52.8

China 8,069 27.9

Indonesia 4,339 58.0

India 3,602 51.8

Philippines 3,521 75.8

Vietnam 3,448 47.5

Pakistan 2,473 71.0

Bangladesh 1,554 70.7

Figure 5! Household consumption as % GDP and GDP per capita - 2011

Source: Penn World Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World Table”

Figure 6! Asians as Adaptors of New Technology - 2014!

Source: Asian Development Bank, Basic Statistics 2014 !For Irish companies in selected markets for whom in previous times the logistics of exporting to Asia would have been prohibitive, this is a very significant development. For higher income and more developed consumer markets – particularly those characterised by consumers with a curiosity and taste for western brands – a whole world of opportunity is arising. Just one example of success in this regard is Inis Meáin, a company using web-marketing to sell high quality knitwear around the world, including to high income purchasers in Japan, South Korea and Hong Kong.!!As Figure 7 shows, hundreds of millions more consumers in Asia will enter this space over the coming decade. As one wou ld expec t , mo re wes te rn i sed economies like Hong Kong, South Korea and Malaysia are already at high levels of internet usage per 100 persons. However other countries, such as Thailand, China, Philippines and Vietnam, are catching up quickly, while countries like Bangladesh, Pakistan, India and Indonesia – countries with a combined population of almost 2 billion – are at the start of this journey. !

!

Figure 7! Internet Users per 100 persons and GDP per capita!

BG: Bangladesh, CH: China, HK: Hong Kong, IE: Ireland, IND: India, INDO: Indonesia, JP: Japan, ML: Malaysia, PH: Philippines, PK: Pakistan, SI: Singapore, SK: South Korea, TH: Thailand, VT: Vietnam !

Source: Penn World Table version 8.1, Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2013), “The Next Generation of the Penn World Table” !Asian Development Bank, Basic Statistics 2014!!However, it is important to point out that much like the leapfrogging of old technologies seen with the uptake of mobile phones over fixed lines, users in Asia are bypassing fixed line internet with smartphone penetration growing at a rapid rate. Looking at Indonesia as an example, mobile Internet has the

© Asia Matters 201416

SG#HK#

SK#

ML#

TH#

CH#

INDO#IND#

PH#VT#

PK#BG#

0#

10#

20#

30#

40#

50#

60#

70#

80#

90#

0# 10,000# 20,000# 30,000# 40,000# 50,000# 60,000#

Internet#Users#per#100#persons#&#GDP#Per#Capita#

High#internet#usage#

Catching#up#

GeKng#started#

Country! Telephone linesper 100 persons

Cell subscriptionsper 100 persons

Hong Kong 61.29 229.24South Korea 61.42 109.43Malaysia 15.69 141.33Thailand 9.51 127.29China 20.2 80.76Indonesia 15.39 114.22India 2.51 69.92Philippines 4.07 106.51Vietnam 11.22 147.66Pakistan 3.24 67.06Bangladesh 0.62 62.82

potential to transform the lives of the population by providing them with affordable access to the web. Estimates in 2011, outlined that mobile internet accounts for over 70 per cent of internet usage in Indonesia , the relative 15

affordability of smart phones has seen ownership rise to 21.3 per cent of mobile owners in 2014 and is expected to double over the next 5 years to 42.6 per cent .!16

The growing mobile internet infrastructure and ownership rate in highly populated countries like Indonesia and India will open up huge opportunities in the etail sector, online banking and other areas where mobile technologies can allow consumers to access new services and products.!

For far sighted business strategies leveraged on good use of internet technology, Asia is a key place to be. And perhaps the most interesting place to be right now is in the centre of the chart shown in Figure 7 where both income per capita and levels of internet use are both poised at the “take off” thresholds for many goods and services.!

!3. Urbanisation!!Another obstacle for any small country exporting over distance relates to the logistical challenges of distributing goods. There are many facets to this challenge but a cr i t i ca l one is the lack o f urbanisation. Asia’s population has always been vast. But compared to the EU - where over 70 per cent of consumers live in well clustered urban centres – Asia’s population has historically been diffused in rural communities and hard to reach. Until now, that is, Figure 8 charts the rise in urbanisation in China and Indonesia. !

Figure 8 ! Asia’s Convergence with EU Levels of Urbanisation (% of population)!

Source: World Bank (World Development Indicators), 2014!

As well as converging with higher income per capita, Asia’s population is now rapidly converging with western levels of urbanisation. According to a recent report by the United Nations Development Agency , 17

China surpassed the 50 per cent share of population living in urban areas in 2011 for the first time. Moreover this report estimates that in a development that is “unprecedented in human history” some 310 million Chinese will have migrated to urban areas by 2030. Indonesia’s rate of urbanisation will also see an impressive rise by 2030. Both China and Indonesia are now at the average global level of urbanisation but likely to surpass this in the coming decade. And while slower and more subtle in form, the process of urbanisation in India is also significant as the spread of road, rail, internet, satellite television and more diverse forms of employment brings “urban life” to many smaller villages and towns previously defined by subsistence agriculture. In varying degrees, these processes are also significant in the “Next 11” countries identified in the report. While in all cases they offer profound opportunities for Irish business.!

Asian urbanisation has also seen the birth of many new mega cities with more expected before 2030. These massive urban centres are now considered economies in their own right given their scale. With

17 © Asia Matters 2014

Deloitte - Access Economics Report - ‘The Connected Archipelago: The Role of the Internet in Indonesia’s Economic 15

Development’ - December 2011

Statista - ‘Share of population in Indonesia that use a smartphone from 2012 to 2018’ - 201416

China National Human Development Report 2013 “Sustainable and Liveable Cities: Toward Ecological Civilisation”, UNDP 17

2013

0

20

40

60

80

1960 1970 1980 1990 2000 2010

China European Union Indonesia IndiaWorld

unique characteristics, they offer unique opportunities for trade and investment. !

Support from government agencies has been crucial in achieving the progress made to date and will remain so in the future. Co-location between Enterprise Ireland, the IDA, Bord Bia, Tourism Ireland and the Department of Foreign Affairs has enabled the government to pursue a “Team Ireland” approach to assist Irish companies in the region. Support offices currently exist in Beijing, Shanghai, Hong Kong, Seoul, Tokyo, Singapore, Delhi, while new embassies have been opened in Indonesia and Thailand, as well as a consulate in Hong Kong. Enterprise Ireland’s “Pathfinders” programme assists firms in guiding access to new markets by providing valuable connections and expertise for a key “bandwidth” of sectors in which I re land has comparat ive advantage. !

Targets for securing new customers, inward buyers and new FDI from the region have also been worked into the Action Plan for Jobs with state agencies and departments called upon to diversify export markets and deliver 10,000 new jobs from new FDI including from emerging markets. The influence of the UK in Asia has also been successfully leveraged by facilitating joint mission visits by the UK Trade and Industry department, Invest Northern Ireland and Enterprise Ireland to

Singapore last February, with government visits planned for ASEAN (Indonesia and Malaysia) and China before the end of 2014. !

Another way to unlock the potential of urbanisation is to fully exploit the business potential of twinning arrangements between Irish and Asian cities. Dublin, Galway, Cork and Fingal are twinned, respectively, with Beijing, Qingdao, Shanghai and Chengdu in China. The potential of twinning with cities with strong connections to Ireland, such as Dalian (where a large number of Chinese migrants to Ireland come from) should be explored. Twinning and partnerships should also expand beyond China, to include other major urban centres across Asia. Capital city twinning relationships offer particular opportunity as the national gateways to drive investment, education and tourism.!

The Dublin Beijing Business Summit of June 2014 is just one example of where such agreements can create foundations for strong business links. Such agreements can underpin regional advantages and opportunities. Dublin has, for instance, been relatively recent in pioneering the development of a strong financial services industry and have preserved it through a difficult crisis. Knowledge and skills developed in Dublin’s financial services sector are highly relevant to Asian countries, who are adapting their own financial services sectors to meet the needs of growing consumer and business activity. The financial services sector holds many opportunities in terms of service exports for Ireland including aviation finance, along with regulatory, compliance and fund administration management. !

!!

© Asia Matters 201418

!!With Irish goods exports to the countries identified in this report accounting for just over 6 per cent of total exports, there is huge scope, even within goods markets, to expand significantly. This 6 per cent of total exports is still dominated by trade from multinational companies. For indigenous exporters, as measured by those working with Enterprise Ireland, total exports to the Asia Pacific region last 18

year amounted to just over €1 billion or just over 1 per cent of total trade.!Even taking the total export figure, the scope for expansion is considerable. It can be quantified by taking IMF forecasts for growth in a selection of 13 Asian country imports from the rest of the world and considering the question, “what would happen to Ireland’s exports to those countries if they simply kept pace with the forecasted import growth?” !

As a country which is “underweight” in exports to the region, Ireland should be aiming to beat these growth rates rather than simply keeping pace with them. For instance in their most recent forecast on Irish exports, HSBC have predicted that the share of Irish exports to China will double between now and 2030 . With this level of forecasted growth, it would be easy to set lofty targets for the entire 19

region. Whereas, adopting a conservative benchmark by simply keeping pace with export growth would secure a substantial gain, see Figure 9 for a full breakdown. !

!!!

19 © Asia Matters 2014

Refers to countries in the Asia-Pacific that are not included in the list of countries in this report.18

HSBC, March 2014 “Ireland’s Trade Confidence soars as Export Growth of 6% predicted”19

!!

!!

!!!

Ireland’s Opportunity

Figure 9! Target Export levels and growth for 2019 !20

Source: IMF World Economic Outlook 2014, CSO Trade Statistics 2014!As Figure 9 shows, the expected growth in the next five years, i.e. between 2014 and 2019, is as impressive as trends seen in the previous five years between 2009 and 2013. Over the next five years, Ireland’s major trading partners in East Asia are expected to see solid growth in exports with China expected to grow by 53 per cent, Japan by 41 per cent, while in South Korea import demand is expected to grow by 122 per cent. In South Asia, demand in

India (78.9 per cent growth), Pakistan (42.6 per cent) and Bangladesh (122.3 per cent) is expected to grow considerably. Similarly, Southeast Asia is expected to see solid export growth, with Vietnam (114.2 per cent) and the Philippines (96 per cent) the standouts in terms of growth rates, while Singapore (56.7 per cent), Indonesia (52.2 per cent) and Malaysia (30.2 per cent) are expected to see solid growth also. These higher rates of growth reflect the low base from which many emerging Asian economies’ import levels are starting. Notwithstanding, whether from a low

© Asia Matters 201420

Our

exports 2013

(€ million)

Share of countries

listed

Relative

size (GDP) of

countries listed

Average forecast for growth in

demand for imports

2014-2019

Total forecast for growth in

demand for imports

(2014-2019)

Benchmark export level

2019!(€ million)

Bangladesh5.6 0.1% 1.0% 12.1% 122.3% 12.4

China 1418.2 26.2% 44.2% 6.3% 53.4% 2175.5

Hong Kong 521.2 9.6% 1.1% 7.8% 68.8% 886.5

India 281.3 5.2% 18.5% 8.7% 78.9% 503.2

Indonesia 75.6 1.4% 4.3% 6.2% 52.2% 115.1

Japan 1692.1 31.2% 15.9% 5.0% 41.0% 2385.7

Malaysia 197.7 3.6% 1.6% 3.8% 30.2% 257.4

Pakistan 28.4 0.5% 1.8% 5.2% 42.6% 40.5

Philippines 79.8 1.5% 1.4% 10.1% 96.0% 156.4

Singapore 559.9 10.3% 1.1% 6.6% 56.7% 877.4

South Korea 321.4 5.9% 5.4% 9.7% 90.6% 612.6

Thailand 137.6 2.5% 2.4% 4.2% 33.8% 184.1

Vietnam 94.5 1.8% 1.3% 11.5% 114.2% 202.4

Total 5413.2 100.0% 100.0% - 58.5% 8635.3

Of the 16 countries considered in this report, 4 (Cambodia, Laos, Mongolia, Myanmar) are omitted from the above chart 20

and from some later analysis due to inconsistent data availability.

base or not, rates of growth of this magnitude represent major opportunities for Irish exporters.!

Many of the countries listed above are developing countries with which Ireland does very little trade at the moment. This is partly due to the relative early stage of economic development and the lack of historical relations. During these early stages, growth tends to depend more on capital investment and less on consumer demand. By contrast more developed economies such as Japan, Singapore and Hong Kong – which are among the leading Irish trade partners in the region - are markets where consumer demand is well developed and constitutes a larger share of overall economic output.!

One possible benchmark to set targets for Ireland’s exports to the region over the next 5 years, is to take the value of Ireland’s current exports to Asian countries and assume that this value grows in line with that country’s expected import growth between now and 2019. If Irish exports keep pace with expected import growth, we should expect to see the total value of exports to the countries listed reach a total of €8.6 billion. One might expect import demand in Asia to be weighted towards “inter-Asian” trade and therefore this benchmark approach might overstate Ireland’s potential. This underlines the importance of focussing on areas where Ireland’s comparative advantages are well developed – education, food production, technology and its tourist potential.!

In 2013, Ireland exported ten times the targeted value of goods (€8.69 billion) – a total of €86.9 billion - to the rest of the world, one and a half times that amount to Great Britain and Northern Ireland (€14.0 billion), four times that amount to Other (Non UK) EU states (€35.6 billion) and over twice that amount to the NAFTA 21

countries (€19.9billion). Assuming some growth in the total of Irish exports to Asia between now and 2019, Ireland would by

2019 still be in a position of exporting less than one tenth of all its exports to a region that will account for over one third of global GDP. !

The situation raises some key points for reflection:!!Should we in Ireland be satisfied with this level of exports to Asia? !If not, what can be done about it?!!The answer to the first question is arguably no, which clearly means the challenges raised by the second question need to be addressed.!!Assuming even modest growth in Irish goods exports between now and 2019, from last year’s €86.9 billion to €100 billion, Ireland should be targeting an Asian export share of at least 15 per cent. That would still leave Ireland relatively “underweight” in Asia when benchmarked against Asia’s weight in world trade which, by 2019, is likely to exceed one third. That would be consistent with a targeted level of exports of roughly €15 billion in total, or nearly double the target suggested by the analysis above. For instance compared to the €1.4 billion exported from Ireland to China last year, Denmark – a country of comparable size to Ireland - exported over €2.6 billion to China last year. Denmark has set itself ambitious goals with Chinese exports targeted to grow to over €7 billion (over half of which are from Food and Agricultural sectors) by 2017 .!22

Is such an ambitious goal possible? Yes it is, and a sectoral analysis of Asian country imports provides substantial evidence of the potential for growth. In both goods and services markets, the extent of growth in specific sectors far outstrips the rate of both macroeconomic growth in Asian countries and their overall import growth. Unlike Ireland’s dominant trading partners, most of whom are steady-state developed countries – many Asian countries are undergoing rates of demographic and microeconomic change that are so rapid as to create opportunities of an unprecedented scale. This is attracting the attention of export oriented economies seeking to benefit from these rapid changes. The challenge for

21 © Asia Matters 2014

US, Canada and Mexico21

www.denmark.dk - Focus Denmark no. 3 - ‘Danish exports to China’ 201222

Ireland is to be one of the first movers in this process before competitor nations gain an early advantage. Ambitious targets are worth setting, given that within the SME sector there are smart sustainable Irish companies with unique global USP that can find partners and new business within niche sectors of Asian markets.!

!Goods exports - Focus on Food!Despite an economy that has diversified and modernised substantially from its agricultural base, an obvious area of export opportunity for Ireland, and a sector in which Ireland remains “underweight” in terms of exports to Asia, is food. Ireland produces 15% of the global supply of baby formula, it is the 4th largest global exporter of beef (1st in the EU), and has the capacity to feed 50 million people, as well as being the only country in the world to score zero per cent in the UNs water s t ress ra t i ng conduc ted by Ya le University . Recognising the opportunity 23

in the sector, Ireland has set ambitious targets to increase dairy production by 50% in the next five years following the lifting of the EU dairy quotas, the growing demand for dairy products across Asia is an obvious market for this increased production. !

For instance, a total of €3 billion was exported from Ireland in 2013 under the heading “meat and meat preparations”. Realistically, logistics confine the feasibility of meat exports to Asia to a subset of this total. Nonetheless, the fact that a mere €90 million was exported to the 13 economies listed in Figure 9 - just 3 per cent of total meat exports – suggests a relative underperformance in a market that is growing rapidly. Between 2009 and 2013, demand for meat imports rose by 95 per cent in India, by 248 per cent in China and by a staggering 390 per cent in Thailand. Despite starting from a low base meaning that per capita consumption in

these sectors significantly below western levels, there is still considerable capacity for rapid scale growth. In spite of this recent growth, recent CSO trade statistics list no exports to any other country but 24

China under the exportable chilled and frozen meat categories which in 2013 were worth over €330 million combined. A factor in this could be the Japanese ban on beef imports, which was lifted in December 2013 during the Taoiseach’s visit to Tokyo. The Japanese beef export market is valued at an initial €15 million with further growth forecasted.

© Asia Matters 201422

Water Stress Index, Yale University, 201023

Trade statistics 2013, Central Statistics Office, March 201424

Figure 10! Growth Trajectory for Irish Food and Drink Exports 2010-2020!

Source: Bord Bia - “Exports Performance Prospects” 2014!Similarly, out of the €1.9 billion total of dairy products exported by Ireland to the world in 2013, the amount exported to the aforementioned Asian countries in the same year was just €101.5 million, or just 0.5 per cent of total exports in the sector.!

From an examination of two of Ireland’s most traditional and long established export sectors, meat and dairy products, it is clear that Ireland’s full potential in the region has yet to be achieved. Measures are being put in place through the efforts of state agencies to support the food and agri-tech industries. Bord Bia for instance have targeted greater demand in the Chinese and Indian markets in their ‘Pathways for Growth’ programme, which sets out ambitious growth targets for food and drink sector export growth by 2020 (see Figure 10). The programme aims to leverage Ireland’s natural advantage, the top international standard of quality assurance in its food production and a combination of growing consumer demand and supply challenges in emerging

markets. Thus far, the programme has set up a China hub (in Shanghai) to support food and drink exports into China. Exports to !

China grew by over 40%, with values trebling over the last three years to reach €390 million in 2013. In terms of international markets these significant increases to China and parts of South East Asia have offset reduced exports to the United States, Saudi Arabia and South Africa.!

Figure 11! Food and Drink Industry Share of the Irish Economy and Chinese Market Growth!

� !

Source: Bord Bia - “Exports Performance Prospects” 2014 !

Fourth Year of Consecutive Growth

6

7.5

9

10.5

12

2009 2010 2011 2012 2013 20207.1bn

7.88bn8.85bn9.1bn

10bn

12bn

23 © Asia Matters 2014

!!!

Exports to China were almost!

40%!higher at!

€390m!which means trade !

has trebled !with China since 2010

The agri-food and drink sector accounts for!

7%!of Ireland’s economy!

wide GVA!

11% !of Ireland’s exports and !

8.6% !of total employment

In terms of strategically developing Ireland’s potential here, China is a priority country, as outlined by Bord Bia’s long term strategy. This is due to the relatively advanced state of urbanisation, the better consolidation and concentration of retail markets and an improved infrastructure a n d c o n n e c t e d n e s s o f d i f f e r e n t submarkets. A particularly interesting market is that for baby formula which, due to difficulties with indigenous production in Asia in recent years has given Ireland a major opportunity. With names like Danone, Pfizer and Abbott located here, Ireland is a leading global supplier in baby formula as it produces 15% of global output. The Chinese government’s recent decision to relax the one child policy can only enhance opportunities here. !

In this sector and the wider dairy sector Ireland faces stiff competition from other s m a l l o p e n e c o n o m i e s s u c h a s Switzerland and New Zealand, whose food giants, Nestle and Fonterra have made substantial inroads to meet demand in the sector. Significantly both countries have signed bilateral trade agreements with China, putting them at a distinct advantage over Ireland. In terms of EU competition, as stated previously, Denmark has set itself ambitious targets of over €7 billion worth of exports to China by 2017 (over half of which from Food and Agricultural sectors) and has mobi l ised major resources on the ground in China through its embassy and network of consulates to support these efforts.!

In India, the requirement to fully or partially co-locate production remains an obstacle to direct engagement, as does the more fragmented nature of the population and the retail sector. However, India has its own and differing potential for Ireland as outlined in the country by country overview section (on page 28). !

!!

Services exports!For obvious reasons, i.e. the lesser or non-existence of logistical obstacles for internationally traded services, Ireland is making faster progress in the area of services exports. In fact, Asia’s share of Ireland’s total services exports, 12 per cent, is double the share of goods exports. The distribution between Asian countries reflects a better performance of China as a recipient country with nearly one quarter of all exports, some €2.4 bil l ion, destined there. Nonetheless, 12 per cent of total services exports remains a relatively underweight share when consideration is given to the rapid rates of growth in Asian country service imports. !

Figure 12 shows the level of services exports to selected (mainly higher income) countries. Growth in such exports has, over the last half decade, been in complete defiance of the global recession. While country by country analysis is conducted in the next section, in overall terms, it is already clear that these markets – which are more accessible via greater internet penetration and the growth of e-commerce – present strong opportunities across a range of sectors.!

Figure 12! Services exports from Ireland!

Source: Exports and Imports of Services Classified by Geographic Location, CSO 2014 !

*Total is non-additive in this table as some export destinations are excluded for presentation purposes!

It is also clear from Figure 13 that the strategic selection of target areas is significant. For instance, construction in mainland China experienced a decline, between 2009 and 2013 (inclusive), due to the base effects of a very large emphasis on capital investment in years preceding the recession (annual investment flows nonetheless remain huge and offer opportunities regardless of these declines). In contrast,

To t a l s e r v i c e s exports (€ million)

To t a l s e r v i c e s exports (% of total)

Europe 55,028 60.9%

North America

9,195 10.2%

Asia 10,854 12.0%

Other* 15,218 16.9%

Total 90,295 100.0%

© Asia Matters 201424

neighbouring Hong Kong’s construction service imports grew by 170 per cent b e t w e e n 2 0 0 9 a n d 2 0 1 2 (inclusive).Financial services growth in mainland China, at 427 per cent, reflects the powerful demographic impact of a rising financially conscious middle class. While tourist markets in traditional high

value countries, such as Japan, have been hit by exchange rates and other economic factors, China, Indonesia, Malaysia, Singapore and South Korea continue to show strong growth in demand for overseas travel.!

!!!

Figure 13! Growth in Imports of Services 2009-2013 in Selected Countries of a Rising Financially Conscious Middle Class. !

!Sources: ITC, UNCTAD, TWO ("Trade Map (or Market Access Map, Investment Map and Standards Map, respectively), International Trade Centre, www.intracen.org/marketanalysis".) !

*Data for Hong Kong up to 2012 for some sectors!

25 © Asia Matters 2014

China Hong Kong

India Indonesia Japan Malaysia Singapore South Korea

Total services 107.9% 36.1% 59.5% 50.4% 9.5% 60.5% 48.3% 33.4%

Transportation 102.5% 37.9% 65.3% 99.1% 15.9% 52.3% 45.4% 21.7%

Travel 194.4% 35.1% 26.6% 37.5% -12.5% 82.6% 48.4% 44.5%Communications services* 33.5% 106.2% -5.3% 53.8% 20.2% 94.7% N/A 47.4%Construction services* -33.3% 170.7% 24.1% 6.8% -41.5% 142.6% 107.9% 38.4%Insurance services 95.4% 61.2% 58.4% -20.0% 24.9% 34.3% 70.7% 8.4%

Financial services 426.9% 34.7% 35.9% 18.5% 18.5% 31.1% 79.0% 31.5%Computer and information services* 83.7% 4.4% 14.8% 32.6% 31.9% 40.2% N/A 56.6%Royalties and license fees* 89.6% 18.8% 112.2% 10.5% 5.3% 24.6% 42.6% 33.5%Other business services* 39.1% 32.5% 72.0% 38.5% 28.9% 59.5% 40.4% 35.4%

Personal, cultural and recreational services* 166.7% 18.8% 118.9% 110.4% 7.5% -7.4% 7.7% 54.3%Government services, n.i.e.* 38.2% 14.3% 45.2% 126.3% 4.1% -28.0% 3.5% 54.5%Commercial services 108.3% 36.2% 59.6% 49.5% 9.5% 61.2% 48.4% 33.2%

Travel and Tourism!A tantalising prospect for Ireland is that Asia generated just €47 million euro in revenue during 2013 under the “tourism and travel” category, much of which reflects the large number of students from China in Ireland.!

This is just 1.5 per cent of total tourism and travel revenues. With the tourism spend of the Asia-Pacific region expected to grow substantially over the next 10 years, driven to a large degree by the rapid demand from Chinese tourists, the region will increase its share of global tourism spend to 40% in 2023 from the 25% share in 2012. This will see the spend reaching over $750 billion by 2023 .!25

Asia’s relatively small share of Irish tourist revenues combined with ongoing and expected future growth in per capita incomes suggests significant potential for Ireland provided its distinctive brand can be highlighted and leveraged accordingly. S t r ong l i n ks deve loped be tween immigrants and students from India, China and other countries in the region are an asset in this regard. While Migration flows between Ireland and Asia are also a potential source of future business relations in areas beyond tourism. Speaking at the ‘Dublin Beijing Business Summit’ at Asia Business Week Dublin 2014, Kevin Toland, CEO, Dublin Airport Authority, detailed the potential of greater air connectivity to Beijing and the wider Asian region in both tourism and trade. According to IATA Airport IS database, demand for Ireland-China flights is on the rise with 46,000 two way passengers estimated in 2013 and a market that “can exceed 105,000 passengers by 2017 at current growth rates” , according to Mr. 26

Toland. This link will target key markets beyond Beijing and its surrounding areas, as the city plans to expand its aviation infrastructure to have two state of the art

airports by 2018 to serve as a centre for air connectivity in the Asia Pacific.!

!Financial Services !In financial services (where Ireland has a small presence in China), insurance (where it has a small presence in Japan and an even smaller one in China and South Korea) and legal, architectural, accounting and management services (where our export presence is low or negligible) Ireland is arguably not utilising our innate strengths. This is especially so in Singapore and Malaysia, which will be important hubs for such activities in the pivotal ASEAN region in the future. !

Though small in scale by Asian standards, the financial services sector in Ireland has many positive attributes to attract Asian investment and cooperation. Ireland can offer Asian financial institutions best in class services as an EU centre for fund management and compliance. Asian banks and investors are already entering Ireland via the Aviation Finance sector, where Ireland’s core expertise is making it a significant global hub. It is estimated that 50% of the world’s commercial aircraft fleet is now managed from Ireland, this amounts to €83 billion in assets and over 1,000 high skilled jobs. In addition, Ireland is home to 9 of the top 10 global aircraft lessors, with significant Asian financial institutions setting up in Ireland, these include Sumitomo Mitsui Banking Corporation (SMBC), Industrial and Commercial Bank of China, Bank of China, and Mitsubishi UFJ. !

With Aviation Finance being of considerable strength for Ireland, other new areas are being explore, these include Islamic Finance, where the Irish stock exchange has seen a rise in Shariah compliant funds and sukuks, and Green Finance, itself an emerging sector. Finally, in terms of financial services skills and professional standards, Irish institutions, such as the ‘Institute of Bankers’, offer top class industry training and professional competency training for expanding Asian financial institutions.

© Asia Matters 201426

According to a report commissioned by travel technology firm Amadeus in 201425

Asia Matters: ‘Summary Report - Dublin Beijing Business Summit’, 2014 26

Education and Skills!Areas where this is beginning to change is in the areas of education, business services and software. Looking at education as an example, University College Dublin and Trinity College Dublin, have already established respective brand presence in China and India, with the Dublin-Beijing International College receiving many plaudits for the quality of its programmes and engagement in China. Dublin Institute of Technology, Ireland’s largest third level institute, opened its own office in Hainan in 2013 to coordinate its efforts on the ground in China. The office marks a significant step to building DITs partnerships across China. !

Other opportunities are available in key markets in the education sector, for instance, Indonesia with a population of 250 million (and an average age of 28 years old) spend 20% of their annual budget on education and skills. Ireland and I ndones ia have r ecen t l y opened d iscuss ions fo r a government to g o v e r n m e n t M e m o r a n d u m o f Understanding (MOU) in the field of education. This will facilitate students on Indonesian government scholarships to study in Ireland. The opening of a new embassy in Jakarta will provide an impetus to successfully conclude this bilateral agreement. In other areas, transport for instance, Dublin Airport Authority is active in p rov id ing av ia t ion and a i rpor t management services in India, Dublin Port are providing training and assistance in Indonesia.!

In other sectors, companies like Taxback and China HR are successful in providing services in the areas of taxation, human resource management and recruitment. Meanwhile, twinning agreements between Ireland and China are beginning to generate business opportunities and connections through events such as the Dub l i n -Be i j i ng Bus iness Summi t , highlighting the role of Dublin city in driving na t iona l economic g rowth . Other agreements, like those between Cork-Shanghai, Fingal-Chengdu, Galway-

Qingdao, illustrate the vast potential in city to city e n g a g e m e n t a s r a p i d u r b a n i s a t i o n a n d internationalisation have seen periods of rapid economic growth.

27 © Asia Matters 2014

!A clear overview of key markets for Ireland underlines how our trade with Asia remains in an early stage of development relative to potential. This section examines the extent of Ireland’s exports to significant Asian export destination countries, the key components of those exports, provides a brief commentary on the rate at which key sectors have grown in recent years and the rate at which overall imports demanded by the relevant countries are expected to grow. As information related to services exports for individual countries is limited, the information provided below is for goods only. Note also that GDP per capita data is cited for the year 2011 .!27

The country by country reports also feature key leveraging points giving Irish businesses an advantage in each country, while also highlighting the success stories of ‘trailblazing’ companies and individuals on the ground in each country.!

!!

© Asia Matters 201428

To enhance comparability and ensure that GDP estimates are as free from possible retrospective revision as possible, 27

2011 data are used to compare countries income per capita levels.

Country by country overview

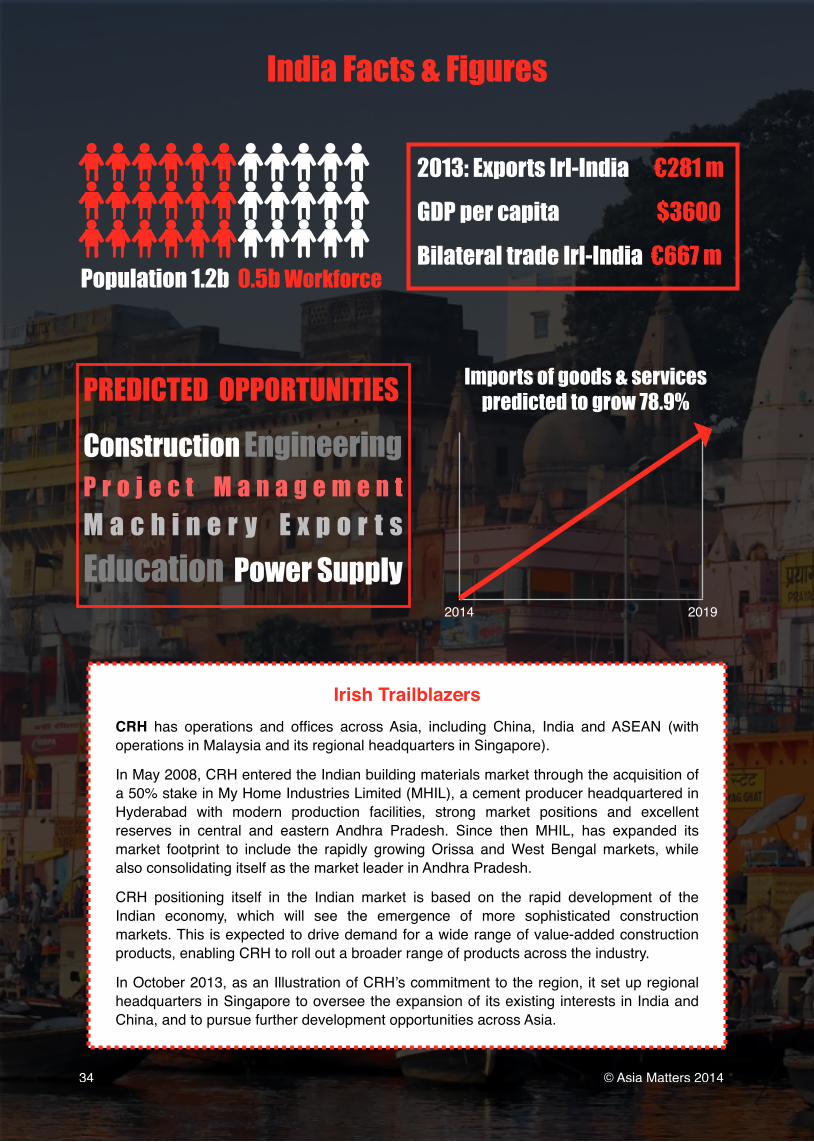

!With a population of over 1.3 billion, over half of whom are in the workforce and with a 2011 GDP per capita level of over $8,000 (in 2005 constant price purchasing power adjusted values), China is without doubt the largest potential market for Ireland. In 2013, Irish exports to China amounted to €1.4 billion or about one quarter of all exports to the region but only 1.5 per cent of total global exports. Key (but not exhaustive) components of that trade are shown in Figure 14.!

!!Figure 14! Ireland’s goods exports to China in 2013 by main category!

Source: CSO 2013 Trade statistics, March 2014!

*Total is non-additive in this table as some export destinations are excluded for presentation purposes!

!

Category Value € million

Electrical machinery & appliances 320.6

Organic chemicals 208.0

Office Machines & data processing 170.6

Medicinal & pharmaceutical products 145.9

Miscellaneous food products & preparations 110.4

Meat preparations & Dairy products 109.6

Total* 1,418.3

29 © Asia Matters 2014

China A Rising Giant

A clear profile of dominance by multinational sectors is evident from this profile and given the foregoing analysis, there is major untapped potential for indigenous exports to grow significantly. Demand for meat and dairy products rose, respectively, by 248 per cent and 401 per cent in China between 2009 and 2013. However, our total exports in these categories do not fully reflect this potential. There are also many sectors in which Ireland has no presence but where Chinese demand is growing strongly. For example, demand for fish products, where Ireland has demonstrated capacity, grew by 66 per cent between 2009 and 2013. Demand for beverages, confectionary and glassware all exhibited high rates of growth well over 100 per cent over the period.!

In the area of services, financial services grew by a robust 427 per cent and with the exception of construction services, which declined, all other services witnessed robust annualised growth rates in excess of 5 per cent a year and most in excess of 10 per cent a year between 2009 and 2013. Unlike manufacturing, trade in financial services remains affected by the fragmented structure of international agreements. Investment relations between China and the EU are governed by a patchwork of 26 separate treaties negotiated by individual member states since the 1980s. As well as direct bilateral efforts to boost trade, such as the effective Ireland-China double taxation agreement in place since 2001. This is a reminder of the importance of working within the EU context to achieve a consolidated common approach such as with the EU-China Investment Agreement currently under negotiation. Given Ireland’s status as a leader in Foreign Direct Investment, it could make a meaningful contribution to the negotiations. !

In terms of more traditional industries, imports of goods and services to China are, according to IMF forecasts, expected to grow by 53.4 per cent between 2014 and 2019.!

!“Ireland’s status as a friendly neutral country, with a relatively large number of Chinese students, an English speaking country, a member of the euro zone and it’s competitive and pro-business economic model, may signal Ireland’s potential future as an entry port to the rest of the EU for this emerging giant”!

!In February 2012, the current President of China Xi Jinping visited Ireland in his capacity as Vice President. There are three immediate significances of this visit and one longer term significance. In the immediate term, Ireland was the only EU country visited by the Chinese delegation. Xi Jinping is a student of agricultural method with a deep interest in modernising this sector in China. With milk quotas set to cease in 2015, Ireland is set to produce vast quantities of dairy products to meet China’s rapidly expanding demand. In the longer term, Ireland’s status as a friendly neutral country, with a relatively large number of Chinese students, an English speaking country, a member of the euro zone and it’s competitive and pro-business economic model, may signal Ireland’s potential future as an entry port to the rest of the EU for this emerging giant. In addition to these factors, Ireland received a huge amount of positive media coverage in China surrounding the visit, helping to shape a positive image of Ireland among the Chinese public.!

At an EU level, as mentioned above, negotiations of the landmark EU China Investment Agreement was launched in November 2013. China is the EU's biggest source of imports and has also become one of the EU's fastest growing export markets. China and the EU now trade well over €1 billion a day. Investment flows show great untapped potential, especially considering the size of the two respective economies. China accounts for just 2-3% of overall European investments abroad, whereas Chinese investments in Europe have risen rapidly since the global financial crisis, despite starting from a low base. This comprehensive agreement aims to tap into this potential to create better market access and protection for investors on both sides.

© Asia Matters 201430

!

!!!

!

!!!!!

!!!

!!

© Asia Matters 201430

€1bworth of trade b e t w e e n E U and China on a daily basis

Imports of goods & services predicted to grow 53.4%

between 2014 - 2019

Irish Trailblazers !PCH International was founded in Cork in 1996 by Liam Casey with just $20,000 capital investment, today it is a global company with a staff of 2,800 employees. Its corporate headquarters are in Cork, while its operational headquarters are in Shenzhen, China. !

PCH started as a small sourcing company and in just a few years had evolved far beyond merely importing products. PCH has become a key enabler, turning ideas into a physical product in the hands of the consumer while optimising quality, cost, and time-to-market in their production cycle. PCH is the partner behind-the-scenes responsible for some of the most successful consumer electronics accessories on the global market. They combine an end-to-end services with a unique understanding of China and the Chinese market.