university finances in india

TRANSCRIPT

Higher Education 17:603-635 (1988) �9 Kluwer Academic Publishers, Dordrecht - Printed in the Netherlands

University f inances in India *

A review of problems and prospects

J A N D H Y A L A B. G. T I L A K

The Worm Bank, 1818 H Street, N.W., Washington D.C. 20433, USA

Abstract. There are about 130 universities and 5 thousand colleges in India. About 1/5 of the plan expenditure and 1/3 of total government recurring expenditure on education goes to this sector. While this is not adequate to provide meaningful higher education to the 3.5 million students enrolled, this is also not trivial. The resources that are being poured into the university system have been increasing at a fast rate, faster than the general economic indicators, but the requirements of the universities have been increasing at a much faster rate, widening the gap between the two continuously. This situation of 'increased cost and diminished income', leading to a crisis or a near-crisis has been a basic characteristic of the Indian universities. The present paper presents a critical review some of the crucial aspects of university finances in India, including the pattern of flow of resources into the university system and the pattern of allocation of resources by the university between its different functions and faculties. In sum, the paper, based on a quick review of the macro scene of the university system in India as a whole, and a critical survey of the few case studies that were conducted earlier on individual universities, presents an analysis of growth of university finances in India during the post-independence period, an overall short appraisal of the case studies, and analyses of income and expenditure patterns of the universities and the problems involved therein, including managerial aspects of finances.

"Support of universities is like adherence to a religion or a church - the pay off from doing so is incalculable and problematical, but it is wise to buy insurance against unknown risks."

Harry Johnson (1974: 21)

"Higher Education is essential in the orderly developments of low-income countries. Although the functioning of higher education is seriously impaired by governments in many countries, the achievements in higher education in an increasing number of them are substantial."

Theodore Schultz (1981: 56)

1. Introduction

E d u c a t i o n r e p r e s e n t s o n e o f t h e l a rges t i n d u s t r i e s in I n d i a r u n n i n g a t a n a n n u a l

e x p e n d i t u r e o f a b o u t Rs . 70 ,000 mi l l i on wi th m o r e t h a n 200 m i l l i o n p u p i l s o n

* The author benefited from the reactions of the participants of the Orientation Programmes in the Management of University Finances in India organized by the National Institute of Educational Planning and Administration, New Delhi, to whom the author lectured on the topic, and from the comments of the anonymous referee of the JOURNAL, in the revision of the paper in its present form. However, the views expressed here are those of the author alone and should not necessarily be attributed to any one else, including the World Bank where he is presently working.

604

rolls and 3 million teachers spread over 750 thousand institutions. Huge material and non-material resources go into education; the education process

takes place; and education yields some output. So the education system can be'rightly treated as an industry or a group of industries in the economic sense, producing manpower with a range of skills, young people as the intermediate

products, moving from one part of the education system to another, and the rest of the economy outside the education system can be called the final

recipient of the products of this industry (Tilak, 1980b). In this educational

industry the share of the tertiary level is of crucial importance. There are about 130 universities and 5 thousand colleges in India. About 1/5 of the plan

expenditure and 1/3 of total government recurring (direct) expenditure on education goes to this sector. In a country where 2/3 of the population are

illiterate, universalization of elementary education still eludes, unemployment among the higher educated consistently increases (see Tilak, 1986), where most

research studies clearly indicate that investment in higher education, compared

to other levels of education, pays the least (see Tilak, 1987a), and above all

where public financing of higher education is regressive in nature and effect (see Dasgupta & Tilak, 1983), and thus, where higher education is regarded

as an aristocratic elite sector, it is of crucial significance to thoroughly evaluate

the higher education system in the country. In this process of evaluation, a critical examination of the financial structures of the universities assumes utmost importance (Tilak, 1982: 62). The present paper is an attempt in this

direction. A pertinent question that may arise at the very outset is: what is the

effectiveness of investment in university education in India? While there is reasonable amount of research on rates of return to education, and to higher

education as a whole that shows that rates of return to higher education, both

private and social, are reasonably higher, 1 very little evidence is available specifically on university 2 education. 3 In general the available evidence on

rates of return leads us to conclude that demand for higher education in India

is justified. On the other hand, figures on unemployment and returns to higher

education, in comparison with lower levels of education, lead many to argue that higher education in India is over-invested and that resources need to be reallocated away from higher education and in favour of lower levels of education. It is important to note that returns to higher education are high even after adjusting for unemployment. Hence the unemployment argument may not stand valid. Then, it is only relative to lower levels of education, one finds that higher education is over-invested. But in absolute terms, all levels of education in India suffer from inadequacy of resources. Higher education in general, and university education in particular, is no exception.

Almost all universities in the country, whether central or state, affiliating or non-affiliating, old or new, general or professional, located in rural or

605

metropolitan areas, all have been in financial crisis of various degrees, for

quite sometime; and it is increasingly believed that the crisis will continue

unabated for some time at least in the near future. The resources being poured

into the university system have been increasing at a fast rate, faster than the general economic indicators. But at the same time, the requirements of the universities have been increasing at a much faster rate, widening the gap

between the two continuously. This situation of 'increased cost and diminished income' was forecasted as early as in 1949 by the Radhakrishnan Commission

on university education in India (UEC, 1949: 438). The purpose of the present paper is essentially to review some of the crucial

aspects of university finances in India. The paper analyses the pattern of

flow of resources into the university system on the one hand, and on the other, the pattern of allocation of resources by the university between its different functions and faculties. This two-fold objective of source-wise

analysis of income and object-wise analysis of expenditure of the univer- sity system in India is served here by attempting a quick review of the macro scene of university system in India as a whole, a n d a critical survey

of the few studies that were conducted earlier on individual universities,

some of which were sponsored by the Indian Council of Social Science

Research (ICSSR) in collaboration with the University Grants Commission

(UGC). A couple of caveats of the present paper may have to be noted. The paper

should not be viewed as an exhaustive analysis of the problems of university

finances in India. We are constrained to ignore a few important aspects like the relationship between inputs and outputs of the university system, but for

a brief reference already made to estimates of rates of return to education. Second, the latest year for which detailed data are available refer to 1977-78,

which we use in the present context. Most of the case studies briefly surveyed

here were also conducted in early 1970s. While more recent data would

obviously be valuable, one may not expect significantly different patterns to

emerge from recent data. Third, the crux of the paper relates to patterns of university finances, including patterns of expenditure. In India the role of

UGC is dominant in university finances. At the same time, to discuss exclusive-

ly the role of UGC would cost closely related important dimensions of the problem. Hence it is attempted here to present an analysis of university finances, covering its various aspects, but with special emphasis on the role of UGC.

We start with an analysis of growth of university finances in India during the post-independence period (Section 2). Section 3 presents an overall short appraisal of the case studies. Sections 4 and 5 are respectively devoted to analyses of income and expenditure patterns and the problems involved therein. Section 6 comments on the managerial aspects of finances in the

606

universities, and the paper ends with a few concluding observations (Section 7).

2. A macro view

University education in India has expanded at a very fast rate during the post independence period. Compared to 20 universities at the time of independence, today India has, as already noted, 130 universities, in addition to 16 deemed universities. During the first decade of planning in India, i.e., during 1951-60, 18 new universities, almost 2 a year, were established, followed by a further increase to nearly 4 per year in the second decade of development planning. It is only in the '70s the pace was slightly reduced to 3 per year and during 1981-85 already 14 new universities were opened. Higher education is provided also by 11 institutions of national importance and 5.5 thousand colleges. The total enrollment is about 3.5 million, of which about 15% are enrolled directly in the university departments. The enrollments in the university departments also depict as shown in Fig. 1 a pattern similar to the one referring to the

130' 125'

m I00. ,4--'

E 75"

e -

~ so-

25-

/

s

I i

1 1

i i

s'1 s's 6'1 66 7'i fs gl 8'3 ~s YEARS

Fig. 1. Growth of university education in India.

600

0 0

s 0 0 .o

400~

-300

8

,200 m c-

e -

-I00 ~D

607

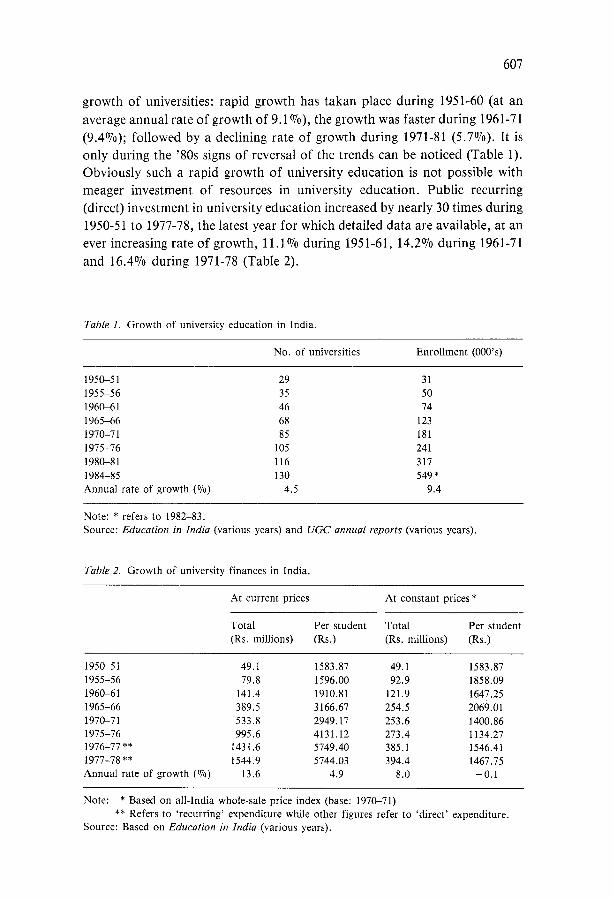

growth of universities: rapid growth has takan place during 1951-60 (at an average annual rate of growth of 9.1%), the growth was faster during 1961-71 (9.4%); followed by a declining rate of growth during 1971-81 (5.7%). It is only during the '80s signs of reversal of the trends can be noticed (Table 1). Obviously such a rapid growth of university education is not possible with meager investment of resources in university education. Public recurring (direct) investment in university education increased by nearly 30 times during 1950-51 to 1977-78, the latest year for which detailed data are available, at an ever increasing rate of growth, 11.1% during 1951-61, 14.2% during 1961-71 and 16.4% during 1971-78 (Table 2).

Table 1. Growth of university education in India.

No. of universities Enrollment (000's)

1950-51 29 31 1955-56 35 50 1960-61 46 74 1965-66 68 123 1970-71 85 181 1975-76 105 241 1980-81 116 317 1984-85 130 549* Annual rate of growth (%) 4.5 9.4

Note: * refers to 1982-83. Source: Education in India (various years) and UGC annual reports (various years).

Table 2. Growth of university finances in India.

At current prices At constant prices*

Total Per student Total Per student (Rs. millions) (Rs.) (Rs. millions) (Rs.)

1950-51 49.1 1583.87 49.1 1583.87 1955-56 79.8 1596.00 92.9 1858.09 1960-61 141.4 1910.81 121.9 1647.25 1965-66 389.5 3166.67 254.5 2069.01 1970-71 533.8 2949.17 253.6 1400.86 1975-76 995.6 4131.12 273.4 1134.27 1976-77 ** 1431.6 5749.40 385.1 1546.41 1977-78"* 1544.9 5744.03 394.4 1467.75 Annual rate of growth (~ 13.6 4.9 8.0 - 0 . 1

Note: * Based on all-lndia whole-sale price index (base: 1970-71) �9 * Refers to ' recurring' expenditure while other figures refer to 'direct ' expenditure.

Source: Based on Education in India (various years).

608

1500.

1250

1000

t - O

# 750. c

. w

t Y

500

250

/

/- /

Constant Price__s /

. t

5i 5'6 6'1 6'6 7'1 76 7'7 7S YEARS

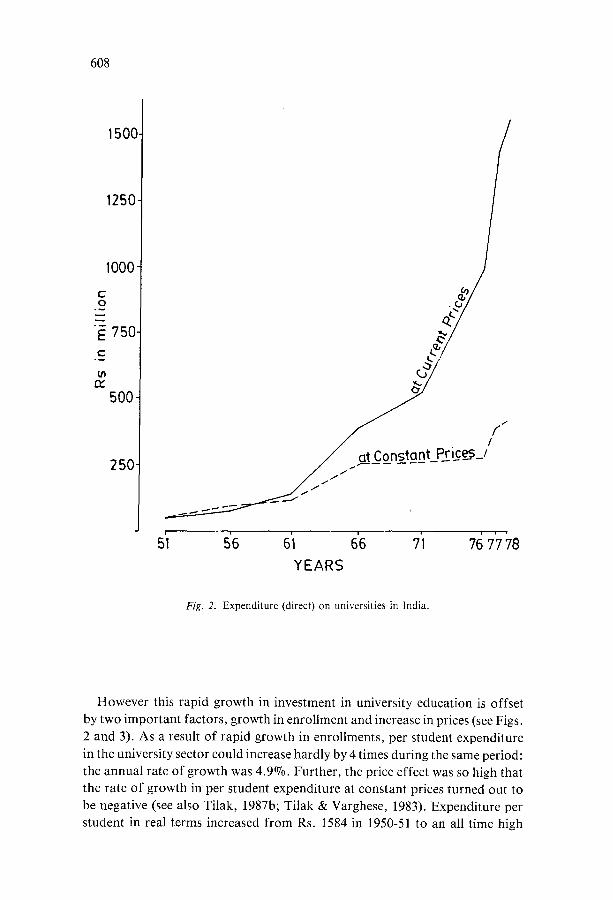

Fig. 2. Expenditure (direct) on universities in India.

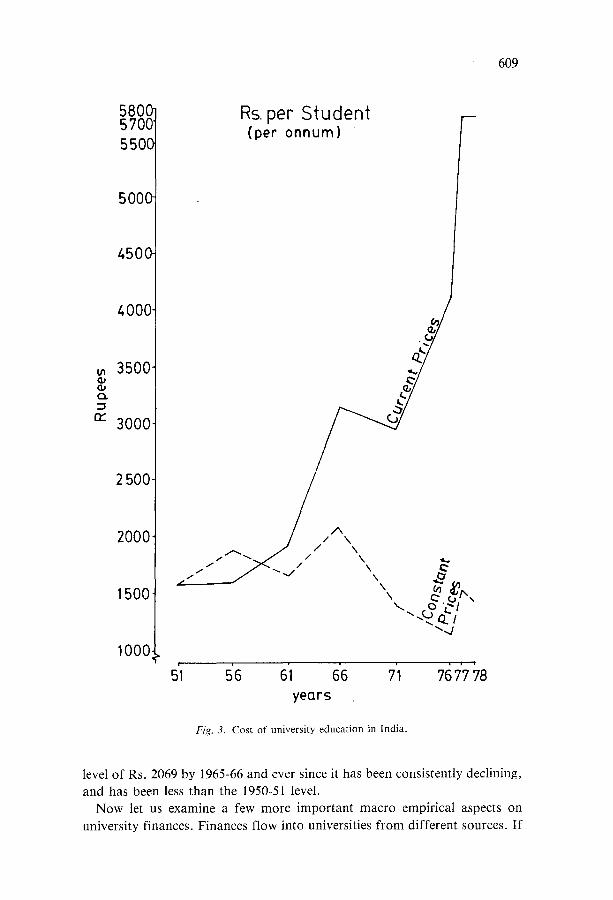

However this rapid growth in investment in university education is offset by two important factors, growth in enrollment and increase in prices (see Figs. 2 and 3). As a result of rapid growth in enrollments, per student expenditure in the university sector could increase hardly by 4 times during the same period: the annual rate of growth was 4.9%. Further, the price effect was so high that the rate of growth in per student expenditure at constant prices turned out to be negative (see also Tilak, 1987b; Tilak & Varghese, 1983). Expenditure per student in real terms increased from Rs. 1584 in 1950-51 to an all time high

609

n,,

5800 5700 5500

5000

4500

4000.

3500

3000'

2 500

2000

1500

1000.

Rs. per Student (per onnum)

f f

f J J

/ /

/ /

\ \

' ~ o , '~/

"-d

5'1 s6 6i 66 years

1

7'1 76 7'7 78

Fig. 3. Cost of university education in India.

level of Rs. 2069 by 1965-66 and ever since it has been consistently declining,

and has been less than the 1950-51 level. Now let us examine a few more important macro empirical aspects on

university finances. Finances flow into universities from different sources. If

610

we ignore students' own expenditure on education (excepting fees) on items such as books, stationery, transport, etc., we can classify the finances into

three categories: governmental sources, students' fees, and endowments and

others, as given in Table 3 (see also Fig. 4). First we notice that the law of ever-increasing state activities applies to

university education as well, the governmental shares in university finances

increasing from about 1/3 at the time of independence to nearly 3/4 within

3 decades. The growing needs of a newly born economy in the form of skilled

manpower and the needs of the economy in terms of original research and

development so that the erstwhile colonized economy becomes self-sufficient in all respects over a period necessitated the government to assume increasing

role in university finances (see also Tilak, 1980a). At the same time the share of fees, including all types of fees paid by the students, 4 in university finances

declined quite significantly from 45% to above 15%. Obviously public in-

tentions to convert the 'elite' inaccessible structures into egalitarian systems

and to make them accessible to socio-economic weaker sections of the society can be noted as an important factor for such a steep decline in the share of students' fees in university finances. In per students terms, it increased

marginally from Rs. 559 in 1950-51 to Rs. 805 in 1977-78. While there is significant progress on the front of equality, still the university education in

India is found to be regressive and inequitable in nature (see Tilak & Varghese, 1985), in which case the fall in fees per student in real prices, or insignificant

increase in current prices is increasingly being questioned. Thirdly, the relative share of endowments and others remained more or less

static with occasional increases and falls. It is being felt, as the case studies

Table 3. University finances in India, by sources.

Years Government Fee Endowment Total & others

1946-47 35.6 44.8 19.6 100 (19.2) 1950-51 40.7 35.3 23.9 100 (49.1) 1955-56 41.4 39.3 19.3 100 (79.8) 1960-61 46.2 37.4 16.4 100 (141.4) 1965-66 64.8 25.1 10.1 100 (389.5) 1970-71 56.3 29.0 14.7 100 (533.8) 1975-76 63.8 * 36.2 100 (995.6) 1976-77"* 67.1 15.0 17.9 100 (1431.6) 1977-78"* 71.5 14.0 15.5 100 (1544.9)

Note: * Included in 'Endowment and others ' . �9 * Refers to 'recurring' expenditure, while others refer to

'direct ' expenditure. () Total Rs. in million.

Source: Based on Education in India (various years).

611

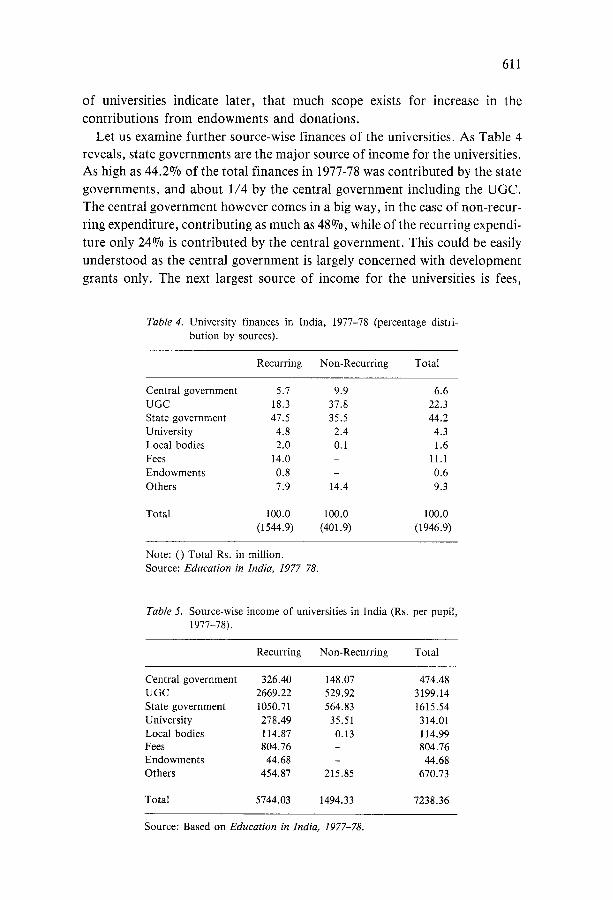

of universities indicate later, that much scope exists for increase in the contributions from endowments and donations.

Let us examine further source-wise finances of the universities. As Table 4 reveals, state governments are the major source of income for the universities. As high as 44.2% of the total finances in 1977-78 was contributed by the state governments, and about 1/4 by the central government including the UGC. The central government however comes in a big way, in the case of non-recur- ring expenditure, contributing as much as 48%, while of the recurring expendi- ture only 24% is contributed by the central government. This could be easily understood as the central government is largely concerned with development grants only. The next largest source of income for the universities is fees,

Table 4. University finances in India, 1977-78 (percentage distri- bution by sources).

Recurring Non-Recurring Total

Central government 5.7 9.9 6.6

UGC 18.3 37.8 22.3

State government 47.5 35.5 44.2

University 4.8 2.4 4.3

Local bodies 2.0 0.1 1.6

Fees 14.0 - 11.1

Endowments 0.8 - 0.6

Others 7.9 14.4 9.3

Total 100.0 100.0 100.0

(1544.9) (401.9) (1946.9)

Note: () Total Rs. in million. Source: Education in India, 1977-78.

Table 5. Source-wise income of universities in India (Rs. per pupil,

1977-78).

Recurring Non-Recurring Total

Central government 326.40 148.07 474.48

UGC 2669.22 529.92 3199.14

State government 1050.71 564.83 1615.54

University 278.49 35.51 314.01

Local bodies 114.87 0.13 114.99 Fees 804.76 - 804.76

Endowments 44.68 - 44.68

Others 454.87 215.85 670.73

Total 5744.03 1494.33 7238.36

Source: Based on Education in India, 1977-78.

612

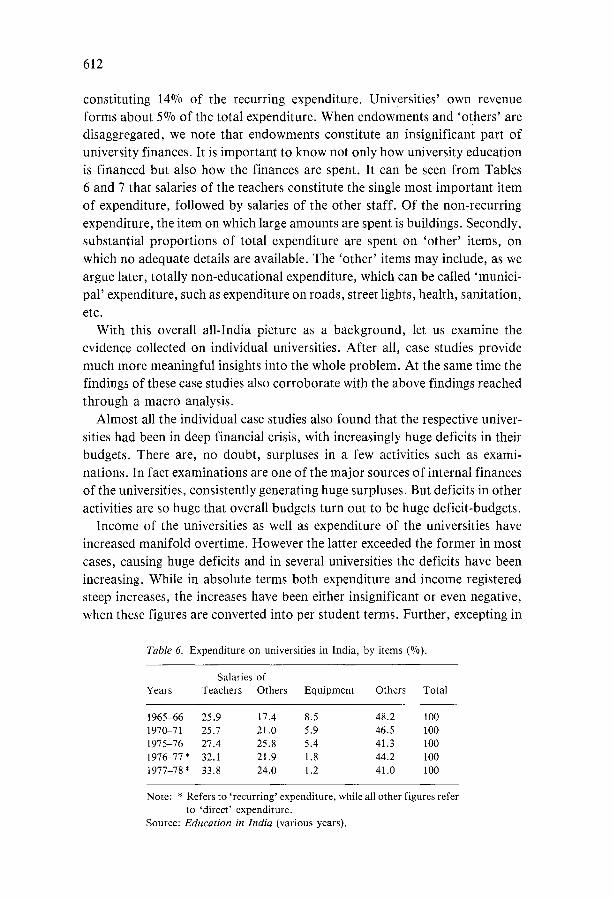

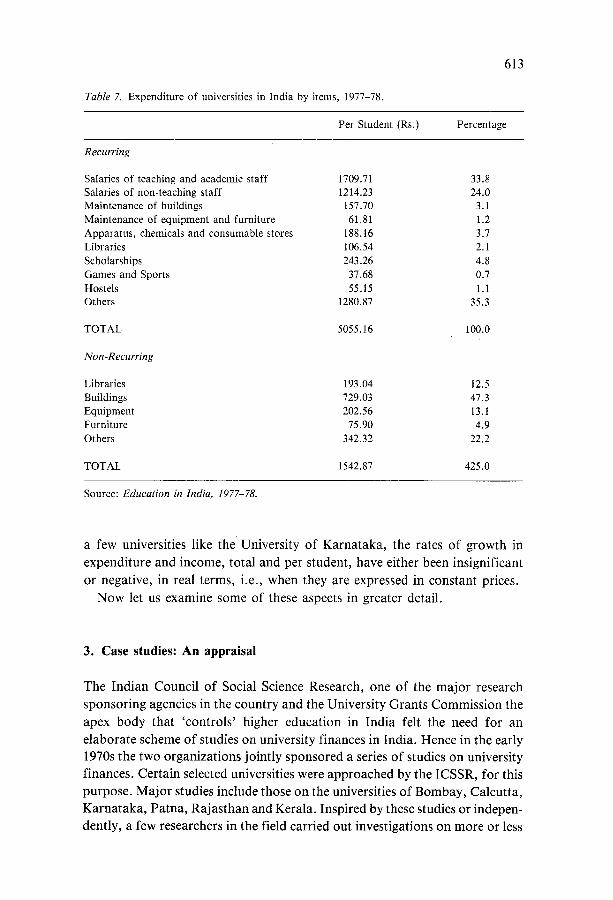

constituting 14~ of the recurring expenditure. Universities' own revenue

forms about 5% of the total expenditure. When endowments and 'others' are disaggregated, we note that endowments constitute an insignificant part of university finances. It is important to know not only how university education

is financed but also how the finances are spent. It can be seen from Tables 6 and 7 that salaries of the teachers constitute the single most important item

of expenditure, followed by salaries of the other staff. Of the non-recurring

expenditure, the item on which large amounts are spent is buildings. Secondly, substantial proportions of total expenditure are spent on 'other ' items, on

which no adequate details are available. The 'other ' items may include, as we argue later, totally non-educational expenditure, which can be called 'munici-

pal' expenditure, such as expenditure on roads, street lights, health, sanitation,

etc. With this overall all-India picture as a background, let us examine the

evidence collected on individual universities. After all, case studies provide

much more meaningful insights into the whole problem. At the same time the findings of these case studies also corroborate with the above findings reached

through a macro analysis.

Almost all the individual case studies also found that the respective univer-

sities had been in deep financial crisis, with increasingly huge deficits in their budgets. There are, no doubt, surpluses in a few activities such as exami-

nations. In fact examinations are one of the major sources of internal finances of the universities, consistently generating huge surpluses. But deficits in other

activities are so huge that overall budgets turn out to be huge deficit-budgets. Income of the universities as well as expenditure of the universities have

increased manifold overtime. However the latter exceeded the former in most

cases, causing huge deficits and in several universities the deficits have been

increasing. While in absolute terms both expenditure and income registered steep increases, the increases have been either insignificant or even negative,

when these figures are converted into per student terms. Further, excepting in

Table 6. Expenditure on universities in India, by items (%).

Salaries of Years Teachers Others Equipment Others Total

1965-66 25.9 17.4 8.5 48.2 100 1970-71 25.7 21.0 5.9 46.5 100 1975-76 27.4 25.8 5.4 41.3 100 1976-77 * 32.1 21.9 1.8 44.2 100 1977-78 ' 33.8 24.0 1.2 41.0 100

Note: * Refers to 'recurring' expenditure, while all other figures refer to 'direct ' expenditure.

Source: Education in India (various years).

Table 7. Expenditure of universities in India by items, 1977-78.

Per Student (Rs.) Percentage

Recurring

613

Salaries of teaching and academic staff 1709.71 33.8 Salaries of non-teaching staff 1214.23 24.0 Maintenance of buildings 157.70 3.1 Maintenance of equipment and furniture 61.81 1.2 Apparatus, chemicals and consumable stores 188.16 3.7 Libraries 106.54 2.1 Scholarships 243.26 4.8 Games and Sports 37,68 0.7 Hostels 55.15 1.1 Others 1280.87 35.3

T O T A L 5055.16 100.0

Non-Recurring

Libraries 193.04 12.5 Buildings 729.03 47.3 Equipment 202.56 13.1 Furniture 75.90 4.9 Others 342.32 22.2

T O T A L 1542.87 425.0

Source: Education in India, 1977-78.

a few universities like the University of Karnataka, the rates of growth in expenditure and income, total and per student, have either been insignificant or negative, in real terms, i.e., when they are expressed in constant prices.

Now let us examine some of these aspects in greater detail.

3. Case studies: An appraisal

The Indian Council of Social Science Research, one of the major research sponsoring agencies in the country and the University Grants Commission the apex body that 'controls' higher education in India felt the need for an elaborate scheme of studies on university finances in India. Hence in the early 1970s the two organizations jointly sponsored a series of studies on university finances. Certain selected universities were approached by the ICSSR, for this purpose. Major studies include those on the universities of Bombay, Calcutta, Karnataka, Patna, Rajasthan and Kerala. Inspired by these studies or indepen- dently, a few researchers in the field carried out investigations on more or less

614

similar lines on the universities of Baroda, Delhi, Punjab and the universities in the states of Gujarat and Bihar. Besides, studies on costs of university education do provide some important insights into the problem of finances. 5

Almost all the ICSSR-UGC sponsored studies adopted a similar pattern in methodology, scope etc. It might be essentially because these details were worked out in a meeting of the project directors at the ICSSR. However, some variations in methodology and scope were not totally ruled out, as we notice later. Largely based on university budgets, annual reports, minutes of the meetings of various bodies and university handbooks, many of these studies attempted a temporal analysis of university income and expenditure covering a period of more than 10 years ending by around 1970-71, and a more detailed analysis of the data relating to the latest year (around 1970-71 in most cases). All the studies presented an analysis of income and expenditure of the university, the former by sources and the latter by objects and faculties. Both current and capital accounts and both plan and non-plan accounts are taken into account. Source-wise analysis presents an account of relative contri- butions of state government, UGC and university's own funds. The grants include both block grants and specific grants. The own sources include students' fee and contributions from auxiliary services. The fee contributions are further broken down for analysis into tuition fee, examination fee and other fees. The auxiliary services include hostels, buildings, publications (press), etc. The total income has also been classified into general fund, and other fund including endowment funds. Expenditure on education has been analyzed by faculties and by different objects. Besides classifying the whole expenditure into current and capital, and plan and non-plan categories, the different heads by which the expenditure is classified and analyzed include general administration, examinations, academic departments, scholarships, works, miscellaneous items, etc. Expenditure is also broken into components such as teacher' salaries (pay, dearness allowances, other allowances), salaries of others, youth welfare, buildings, furniture, equipment, library (books, journals, etc.), other contingencies and so on.

While this is the general scope and approach followed by all the ICSSR-UGC sponsored studies, a few of them did go beyond this general framework and did enlarge the scope of their studies and made some significant contributions both to the approach and to the empirical analysis. 6 The several studies, on the whole, provided valuable insights into the problems of university finances in general, and those of the specific universities in particular. However, almost all these studies, having adopted a rigid overall framework, suffer from a few major limitations. For instance, "without relating the finances to something that the universities are supposed to achieve, no critical appraisal of their financial aspects is possible" (Mukherjee, 1981: 32). But no single study on university finances touches this aspect. After all, costs of higher education can

615

be reckoned readily than can its value. Secondly, it is very important to know

the resource base of the main funding agency of the university, viz., the government, how is the resource-base of the government built? What are the

components of this base? Who contributed to this base? What are their respective shares? and who receives benefits from university education and in what proportions? Unfortunately no single study refers to these aspects. 7

Third, the working of the agencies like the Finance Commission or the Planning Commission in allocating resources to universities has been kept

outside the purview of all the studies, even though the more directly concerned agencies like the UGC and its mechanism have been studied, s Lastly, any analysis of financial aspects require a clear understanding of the requirement

of the universities in physical terms, i.e., physical requirements per pupil or

per university. Such physical norms are absolutely essential first for costing education in the university and secondly to examine the adequacy of resources

that flow into the system. Most studies commented upon the problem of adequacy (or inadequacy) without presenting any idea of the physical norms.

With the help of these and other studies, we shall describe in the following

sections, the mechanism of financing and pattern of expenditure in universities in India, so that a few possible lines of action can be taken up for discussion

towards the end of the paper.

4. Income of the universities

The sources of income for the university can be divided in a variety of ways.

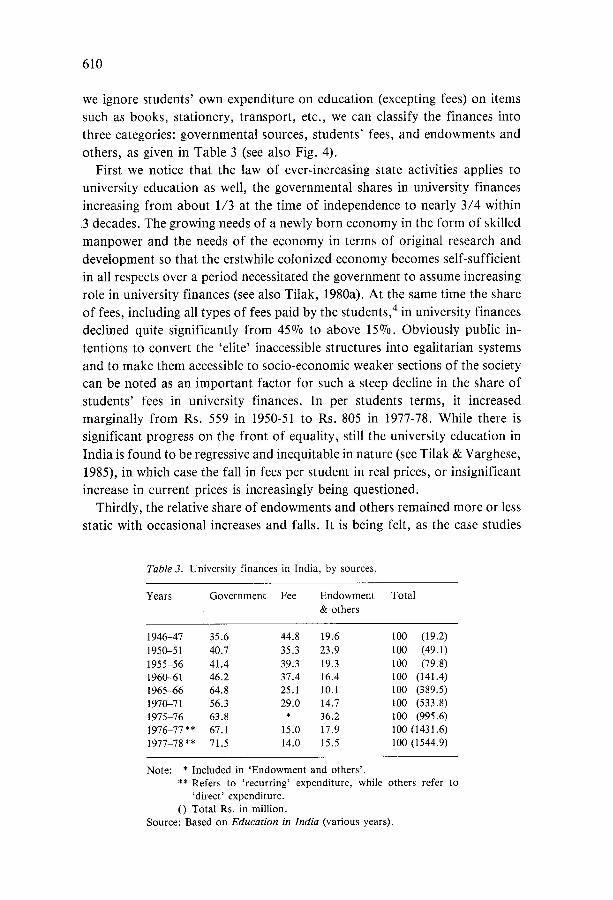

An elaborate classification is given in Fig. 4. Generally, income is classified as follows:

a) Grants: state government grant, federal government (UGC) grants b) Students' contributions: fees c) Internal resources: auxiliary services, e.g., hostels, press, computers, etc.

d) Other resources: endowments, donations, etc.

The above categories are also often clubbed into two groups, viz., government sources and internal sources. While a above forms government sources, b, c

and d together form internal or non-government sources. The government is

an important source of income for the universities in India. There are indeed few private universities. As the development of universities in India is a joint responsibility of state (provincial) and federal governments, the grants receiv- ed by the universities comprise state government grants and federal govern- ment grants (referred hereafter, for brevity, respectively as state grants and federal grants). For the central universities, the government sources consist of only federal grants. The federal grants to the state or central universities flow largely through the UGC. Therefore, state government and the UGC can be

SOUR

CES

OF

UNIV

ERSI

TY FI

NANC

ES

"

I

I St

ate

Gov

ernm

ent G

rant

s

Rura

l ]

Text

In

stns

Book

Pr

oduc

tion

in R

egio

nal

Lang

uage

s

I O

ther

Org

anisa

tions

( C

SSR,

ICAR

, ICHR

etc.

)

Unive

rsity

Gra

nts

Com

miss

ion (

U.G

.C.)

Unas

signe

d Gra

nts

(e.g

. Cen

tent

ary

Gra

nts)

Bloc

k Gra

nt

Mai

nten

ance

Gra

nt

I De

velo

pmen

t G

rant

(M

atch

ing G

rant

)

Oth

ers

(Don

atio

ns,

Endo

wmen

ts et

c.)

Auxil

iary

Serv

ices j

(P

ress

, Com

pute

r, W

orks

hop e

tc.)

I I H

oste

l Cha

rges

I

] Vi

sitin

g Fel

low-

sh

ips/

Exch

ange

Pr

ogra

mm

es

] No

n-Re

curri

ng

Gra

nts

Stat

ulo~

Gra

nt

I ~

(Fou

ndat

ion F

und,

I

�9

lEnd

....

. t F

und e

tc.)

I ~

.

~uild

ing/

Host

el I

~

~ !

Gran

t 3

I Gr

ant

L I

Gran

tl

Fig

. 4.

S

ourc

es o

f u

niv

ersi

ty f

inan

ces.

O~

617

listed as two important sources of revenue for the state universities. The third major source is university's own funds. However, they comprise of students' contributions such as fees, (including tuition fee, examination fees, regis- tration fees, etc.) which is also sometimes separately listed, and income from auxiliary services like hostels, press and publications, buildings, etc. Lastly, universities may also mobilize resources from private individuals or organi- zations in the form of donations and endowments. Of all, grants constitute the largest item of finances for the university; and state grants are bulkier in size than the federal grants. In a good number of universities [e.g., Baroda (Shah & Srikantiah, 1981); Punjab (Garg, 1985)] it has been noted that the contribution of each of these sources per pupil declined overtime in real terms.

4.1. Grants

A n important area where universities face severe problems which are adequate- ly noted relates to grants-in-aid policies of the state and federal governments. The state grants are of three categories: (i) maintenance/block grants, which are basically for the day-to-day functioning of the institution; (ii) development grants, which are given largely on a matching basis to UGC grants, and (iii) non-recurring grants for buildings, equipment, etc. 9 Of the total grants made by the state governments to the universities, the maintenance grants are also made by the state governments towards foundation fund, etc. The federal grants are made to the universities by the central government through the UGC for developmental purposes, m The intermediary, viz., the UGC was felt necessary because "it is not desirable that the government should deal directly with the universities" (Education Commission, 1966: 144).

Almost all the studies concluded that there is a lot to be improved with regard to both state and federal grants-in-aid policies to the universities in India. The grants-in-aid policy "smacks away, the dynamism of the universi- ty" (Reddy, 1978: 15). The system of grants, both federal and state, is characterized by a high degree of complexity. It is said to be so complex that many a time it results in non-utilization and lapsing of the grants. If one evaluates soundness of a system with the help of the measure of elegance,ll Indian system of grants-in-aid receives a poor score. In this context, let us examine the state grants first and the federal grants next.

4.1.1. State government grants

Inadequacy of state grants has been repeatedly emphasized by almost all the studies. Some studies (e.g., Nanjundappa, 1976; Panchamukhi, 1977) also

618

noted that no consideration for equality has been shown by state governments in making grants. The result being even in smaller states glaring inter-university inequalities in financial situation can be found. Thirdly, absence of any proper suitable time-schedule with respect to release of grants has also been felt (Nanjundappa, 1976). Financial situation of universities is not uniform at all periods during a year. With respect to Bombay University, Panchamukhi (1977) has noted that normally the financial difficulties are maximum after the end of September every year at least for about three months. More than half of the size of the grants is to be received during the last quarter of the year. Generally the situation is managed with the help of fee receipts from the students, or from the accumulated surpluses of the previous year (Mathew, 1980). To reasonably maintain the financial position of a university throughout the year, it is suggested that 90% of all types of grants be released during the first three quarters of the financial year, the maximum to be released during the third quarter (Panchamukhi, 1977: 215).

While the block grants are expected to take care of 'deficits' (deficits, defined as approved expenditure minus approved income), they fail in doing so, essentially because of the defects of the system. The system does not treat various important items of expenditures as 'approved' items; and the system neither encourages efficiency in the management of grants, nor works as a disincentive for inefficient management.

Basically the grants-in-aid policies of the state government exhibit lack of concern for balanced expansion of university education in the state. In this context, a few major weaknesses have been found. They relate to vague specifications, less meaningful definitions of 'approved' expenditure, time lag between the establishment of institutions and release of grants, and above all, lack of dynamism, favoring rigid patterns of institutional development (Azad, 1975: 141-7).

In some universities like Baroda (see Shah & Srikantiah, 1981), the state grants per pupil declined over time in constant prices. Further not only the rate of growth of state grants has been low, but also their proportion even in current prices, declined relative to contributions of other sources like in the University of Kerala (Mathew, 1980). From such a trend to conclude that universities have been becoming increasingly self-reliant (see e.g., Mathew, 1980) is perhaps not totally proper. On the other hand, it may be suggestive essentially of 'insuf- ficiency of grants' and their declining trends.

To improve the mechanism with respect to the state grants-in-aid, it has been suggested that an autonomous body in the form of University Grants Com- mittee should be set up by the state government (Nanjundappa, 1974; Nigam, 1974). Such a committee would ensure better flow of funds from state governments to universities and among all universities in the state. However the committee need not adopt a dull uniform policy towards all universities

619

in the state. The suggestion is similar to the suggestion made by the University Education Commission (1949: 434) in favour of constituting grants allocation committees in each state along with UGC at the national level. In fact, it was also argued that a state level committee could take care of both plan and maintenance grants (Parikh, 1979). 12 However, setting up of any state level University Grants Committee was not favored by many, including the Edu- cation Commission (1966). Some of those who do not favor establishment of such a committee, however, argue that a committee should however be constituted for a year before the grants are made and that the committee should recommend inter-university allocations on a rational basis, based on enrollments, types of courses, etc., (Bose, 1976). A few others (e.g., Jha, 1976) suggested that at least a grant revision committee should be constituted periodically, say, every five years to see that the state grants correspond to the increasing needs of universities over time.

Further it has been argued that state grants should not be tied down. A degree of flexibility is badly needed with respect to these grants. Replacement of ad hoc grants (released on year-to-year basis) by block grants for five-year periods in universities like Rajasthan did not solve all the problems (Nigam, 1974). Particularly the stringent conditions attached with block grants proved to be a great deterrent. State grants should fully take care of the recurring needs of universities, as well as uncovered expenditures in the development schemes sanctioned by the UGC. Frequent resort to over-draft from banks and their resultant increase in financial burden of universities by way of interest payment is often due to either uncertainty regarding the payment of final block grants or delay on the part of the state government in meeting its matching share in development schemes (see Lakdawala & Shah, 1978). All this can be easily avoided with the help of better methods of financial planning and adminis- tration.

4.1.2. Federal (UGC) grants

Grants-in-aid policies of the UGC also have not escaped criticism. Primarily as they relate to plan period only "there is an element of uncertainty and adhocism" (Panchamukhi, 1977: 105). The UGC grants create a pressure on the university finances on two counts: (i) The UGC takes the responsibility of creation of capital like buildings and equipment, while its maintenance is the responsibility largely of the university. (ii) While the UGC's assistance is not only non-recurring in nature, the grants are also matching, the contribution generally varying in between 50% to 100%. The residual is to be met by the university either from the state grant or from its own resources. Many a time it is found to be difficult. As a result, full advantage of UGC assistance could

620

not be taken. Hence in this context it is suggested that at least a few activities like quality improvement programmes in post-graduate education and research be assisted on 100% basis, so that they are implemented in a 'uniform' manner by all universities (UGC, 1977b: 6). Further, UGC's assistance to new depart- ments is confined to the teaching staff. Specifically UGC does not provide grants for non-teaching staff except laboratory attendants. Expenditure on these staff is not approved even for state grants. Another problem with respect to the UGC grants, as reported by Panchamukhi (1977) is that they are released on 'account' basis, rather than on 'due' basis, i.e., they are released after the submission of the accounts of the expenditure. In other words, the university has to incur the expenditure first from its own resources, and the grants are received much later. Yet another kind of time lag is between the establishment of a university and the release of UGC grants.

The other defects we have noted relating to state grants also are applicable to the UGC grants. For instance, the inequitable financial assistance given by the UGC has been pointed out often. 13 No consideration of inter-university and/or inter-state equality in university education/finances have ever received any attention of the UGC in formulating its grants-in-aid policies. In this context, some (e.g., Azad, 1975:117) have argued for opening regional offices of UGC in different regions of the country, so that planning and financing functions of the universities are decentralized. 14

Another problem universities face with respect to the UGC (and also with respect to state) grants is about internal allocation. UGC gives development grants to universities for pre-determined and approved purposes and the universities have to use the grants exectly in the same way, i.e., reallocation of the resources is not within the powers of the university. 15 This is 'the person who pays the piper calls the tune' attitude. In fact the person who pays the piper is quite unlikely to have a satisfactory creative sense regarding developing a worthwhile tune (Mukherjee, 1981: 39). 16 The problem is more serious because no proper guidelines exist for optimal inter-functional allocation of funds (Nanjundappa, 1976).

The policy followed with respect to federal grants largely flowing from the UGC is also found to be far from satisfactory. Federal grants are meant for developmental purpose, initiated during a plan period. Continuation of these developmental programmes depends upon the level of state grants, and the UGC cannot under the present practice, ensure it. In other words, the revenue needs are satisfied by the state government and the capital needs by the UGC. Gripped as they are in the financial crisis, universities fail in many cases to take care of such programmes. Thus the division of responsibilities between the UGC and state government appears to be based on no rational criteria. To improve the UGC's mechanism of grants-in-aid, it has been suggested that UGC's assistance should be extended to non-plan activities also. Not only the

621

creation of capital, but also its maintenance should be the responsibility of the

UGC. Basically, the UGC's assistance has remained mainly 'responsive' rather

than 'promotional' in character (Azad, 1984: 83). In other words, UGC reacts to the proposals submitted by the universities, rather than taking any initiative on its own in planning university education and providing finances for the same. It has been argued that the character of the UGC's financing policies should change in this respect, from 'responsive' to 'promotional'.

The division of responsibilities between the UGC and the state government has not been found to be conducive for university development. A rational division of responsibilities can be as follows: all expenditure pertaining to maintenance and improvement of standards in education in the universities (e.g., expenditure on academic staff, academic equipment, buildings etc.) should be met from UGC grants, and all expenditure on running the establish- ment should be met from state grants (see Panchamukhi, 1977). This also seems to be consistent with the constitutional provisions regarding the center's role in higher education (see Tilak, 1987c). It may be noted that when long ago the Sargent Commission (see CABE, 1944: 48) recommended the consti- tution of UGC for Indian Universities on the lines of the British pattern, it was expected that the UGC would take the major, if not total, responsibility of all universities, central and state alike.

The grants-in-aid policies should have three main objectives, viz., supple- mentation, stimulation and equalization (Panchamukhi, 1977). 17 Grants should supplement the resources of the university; they should improve internal efficiency and they should reduce inter-university inequalities in financial strength. We note that none of these objectives is being met by the present grants-in-aid policies.

Further state grants and UGC grants are neither related to each other suggesting that they do not necessarily supplement each other, nor have any relationship with deficits/surpluses of the university, besides not having been based on any consideration for equity (Purohit, 198l), while the state block grants are expected to be based upon the net deficits in the budgets and the rise in costs, indicating that they do not work as an incentive (or disincentive) for better (or poor) financial management.

Basically for both types of grants, state and federal, financial accounting becomes more important than achievement of academic excellence. Lack of coordination between the state government and the UGC hampers the progress of the university substantially. Empirically it is found that the UGC grants do not have any relationship with the state grants received by the universities (see Azad, 1975: 83; Purohit, 1981). 18 Matching assistance offered by the UGC is not accepted in all cases, as the university or state government has to provide a matching grant. Even the grants made by the UGC on 100070 basis are also

622

not totally welcomed, as state grants have to take care of these activities after the end of the plan period. Thus "the utilization of plan funds by the state universities remains inadequate or is sometimes delayed by the fact that state universities are required to give matching contribution and also an assurance from state governments regarding the maintenance after the assistance from the Commission ceases" (UGC, 1977a: 102). Therefore as Bose (1976: 127) rightly concludes, "lot of financial difficulties could have been tackled if there were proper coordination" between the UGC and the state governments. In fact, for meaningful and balanced development of university education coordination between the state government, the UGC and the universities is absolutely essential (see Parikh, 1970).

The problem does not lie totally with the state government and the UGC. The universities are also partly responsible for the inadequacy of the financial resources. For instance, in the case of University of Kerala, Mathew (1980) notes that there exists satisfactory relationship between the university and the state government and between the university and the UGC; the basic problem is that the university does not have a proper planning machinery (p. 95); "the university has not been exercising sufficient care and forethought" in the formulation of proposals submitted to the UGC and state government (p. 116). The development plans of the university are mostly characterized by adhocism; they are not based on any clear perspective of the development needs of university education in the state (p. 96). Consequently there has been wide gap between the proposals of the university and the grants it receives.

In this context, Ghosh (1981) suggests that the universities should prepare and submit their development plans to the UGC two years before the expiry of the current plan period; or the university should prepare and submit ten-year plans in two parts, so that after examining the schemes of the first part, i.e., of one five-year plan, the UGC may consider the second part of the ten-year plan, at least two years before the current five-year plan period is over. This will also help the university to have ten-year plans with greater perspec- tives and coordination. The need for perspective planning has been well noted. For instance, it was clearly observed: "There seems to be a lack of planning consciousness as well as adequate machinery at the university level with a few notable exceptions. The universities need a new vision of perspective planning spread over 15-20 years with well-defined goals and objectives. The planning process should also have the fullest participation of teachers, students, admin- istrators and citizens of the area" (UGC, 1981: 109). Secondly, preparation of 10-year plans also cuts down costly delays. Otherwise, by the time the UGC approves plan proposals, based on reports of the UGC visiting committees, in general about 1-2 year time of the current plan period is over; and another period of 6 months to 1 year is needed to obtain final approval of the state government for matching shares.

623

4.2. Internal resource: Fee

It has been pointed out that the financial position of the universities becomes precarious due to grants-in-aid policy and inelastic fee structure (Reddy, 1978). Now that we have examined the first, let us take up the fee structure in the universities.

Based on detailed analyses of the fee income of the universities in India, many studies (e.g., Reddy, 1978; Shah & Srikantiah, 1981) concluded that the ratio of per student expenditure to per student fee income has been greater than one. Not only the cost-fee disparity has been quite high and positive, it has also been found that fee per student has been declining over time (Panchamuk- hi, 1977). Noting that universities should be self-sufficient in the long run, it has been unanimously concluded that there is much scope for revision of fee structure. It has been felt that there can be straightaway a steep upward revision in the fee structure along with a proper system of scholarships for the weaker sections.

Though tuition fee as such forms a small proportion of the total recurring cost of university education (4.6%), total fee (including all types of fees paid by the students) constitutes significantly a large proportion of the recurring costs. It was as high as 27% in 1976-77 (see AIU, 1983). 19 While some argue for increase in tuition fee, a few others argue for increase in all fees. For instance, even though it has been found that examinations are generating large surpluses of revenue in Bombay University, Panchamukhi (1977: 152) argues that "there is an urgent need to revise the examination fee." But one may feel that a rise in all kinds of fee may not be justified. Similarly, even though it was noted that inter-faculty variations are significant in the cost-fee disparities, few have suggested selectiveness in increasing the fees. Further though the heterogeneity of the student population with respect to socio-economic con- ditions has been highlighted (Lakdawala & Shah, 1978), again few have suggested discriminatory fee structure based on household income levels.

While there exists scope for raising the internal resources, through reforming the fee structure, it should not be through a general rise in fee rates. Rather fee rise should be selective. As we argued elsewhere (Tilak & Varghese, 1985), a discriminatory fee structure, based on (a) costs of education, and (b) ability to pay by the students would be more advantageous, generating more resources for education and at the same time reducing the regressive character of university education significantly.

There also exists much scope for the universities to generate more resources on their own, besides rationalizing the fee structure. Auxiliary services like hostels have an inelastic demand to price. Hence they can be made self-suf- ficient. Other auxiliary services like press, computer, etc., can be viewed as a business proposition and even can be made autonomous (Lakdawala & Shah,

624

1978: 112). It is also suggested that the university can put to commercial use not only its computers and press, but also several other services. The science and engineering departments can as well manufacture scientific equipment for commercial sale; the technological and engineering departments may render professional services to the business and industrial sectors in research and consultancy and so on (see Basargekar, 1978).

To mobilize resources from charitable trusts and other organizations, and more particularly to see that they are not concentrated in a few universities, but are fairly distributed among all the needy universities and thus help in strengthening the financial position of the universities and reduce inter-univer- sity inequalities, some (e.g., Bombay University, 1981) have suggested that an Inter-University Financial Corporation might be set up.

5. Expenditure of the universities

Expenditure of a university is made up of expenditure on activities directly related to academic work as well as expenditure on administration and munici- pal services like housing, roads, water, electricity, sanitation, health, etc. In this context, expenditure is classified in a variety of ways. Essentially, the whole expenditure can be classified into recurring and non-recurring. Recur- ring expenditure includes (a) expenditure on academic activities, viz., teach- ing, research, library, publications, etc., (b)general services like adminis- tration, examinations, and hostels, (c) student and staff welfare activities and (d) others. Non-recurring expenditure includes expenditure on buildings, equipment and others. A rather exhaustive classification is given in Fig. 5. This, particularly the classification of recurring expenditure, is generally known as the functional classification of the university expenditure. On the other hand, the whole expenditure can also be classified into two categories: academic activities and other activities.

A tentative analysis of a central university shows that the share of the expenditure associated with non-academic activities approximates to 47~ in 1980-81 and it had gone up from 41~ in 1970-71 (Raza et al., 1985: 137). In the case of the University of Karnataka, expenditure on academic services constitute just 40~ of the total university expenditure in 1972-73 (Nanjundap- pa, 1976: 276). Evidence from other universities is also similar. Analysis of Bombay University data shows that salaries of non-academic staff outweigh those of the academic staff, the respective proportions being 60~ and 40~ in 1970-71, while the corresponding proportions were 54~ and 46~ in 1950-51.20

Thus when non-academic expenditure exceeds or equals the academic expen- diture in a university, can the total expenditure on the universities be called

J UN

IVERS

ITY

EXPE

NDITU

RE, BY ITE

MS

]

I Non

-Re0

u,~

I

reae

hing

~

' Adm

inistra

tion ] [ E

xami

:ation

s ] ~

~

~S~h

o,~shos

~

~ ~

~ ~

'-

~

Fig

. 5.

U

nive

rsity

exp

endi

ture

by

item

s.

1-o

626

expenditure on university 'education'? An important point to be noted is that the expenditure on non-academic activities not only exceeds that on academic activities but during the last few years the gap is widening, with the expenditure on non-academic activities increasing at a fast rate. 21 Further, one can not only deduce a law of increasing university expenditures, but also note that the "university expenditures increase in spurts, hence there is a displacement effect. The expenditure on administration and unallocable items have a tendency to grow faster than total expenditure of the university" (Panchamuk- hi, 1977: 231).

With respect to utilization of funds, it has been noted that a significant amount of endowment funds remain unutilized (Panchamukhi, 1977; Mukher- ji, 1976). For example, the University of Calcutta had a large corpus fund of the trust funds, with a large amount of income flowing from it, equivalent to half the total (excluding trust) funds. Mukherji (1976) clearly observed that the University of Calcutta could meet twice the then deficit by running down certain special corpus funds available with it. Budget deficits could not, however, be met out of such funds, as the sanctity of the endowments was to be recognized and only the specific purpose for which an endowment fund was created, was to be met out of this fund. Even with respect to the University of Bombay, the same was noted.

6. Management of university finances

Several limitations of university budgets, as prepared currently, are sufficient- ly well noted. For instance, Nigam (1974) argues that the conventional budget estimates do not help in understanding its revenue-expenditure pattern from the point of view of economics of education. The frame of the university budget is fairly detailed and comprehensive; but it does not incorporate a budget analysis nor the essential aspects of educational finance. The budgets do not show at a glance some important details such as total income and expenditure under heads like academic, non-academic, educational, non-edu- cational, etc. For want of proper planning, budgeting has been quite loose, as Nanjundappa (1976) has shown. The situation in the University of Kerala (Mathew, 1980: 95-6) makes this point even clearer; at the university level, there is "virtual lack of planning at the different stages of formulation of proposals. Development plans of the university are mostly characterized by adhocism, they are not based on any clear perspectives of the development needs of university education in the state." For this very reason Jha (1979) argues for direct methods of budget making through direct participation of different units of the university in preparing budgets.

Classification of the budget accounts should be so arranged (i) to facilitate

I G

ross

Phy

sica

l C

apita

l For

mat

ion

~oac~e

rs' J Sa

larie

s l

Sala

ries

[ of

Cap

ital

Item

s

UN

IVER

SITY

EXP

END

ITU

RE,

BY

NAT

UR

E I

Fig

. 6.

U

nive

rsit

y ex

pend

itur

e by

nat

ure.

Ref

unds

, In

tere

st

Paym

ents

et

c.

628

programme formulation, (ii) to contribute to effective budget execution, and (iii) to secure accountability. For this purpose one can choose (a) economic classification, or (b) functional classification, or (c) economic-cum-functional classification, or (d) performance approach. Economic classification of the budget clearly brings out the magnitude of expenditure on economically significant categories such as (i) consumption expenditure (e.g., salaries of teachers), (ii)expenditure on capital formation (e.g., expenditure on buildings), (iii) transfer payments, and (iv) miscellaneous expenditure (see also Azad, 1975: 51). This has been rarely used in any analysis of university budgets. On the other hand, functional classification of the budget emphasizes the functions that expenditures are intended to perform or the purposes which refer to the type of services provided; and facilitates programme formulation and its review. Under such a system, different items of expenditure are grouped in terms of broad purposes they serve. The classification may include (i) gener- al services, (ii) academic services, (iii) auxiliary services, and (iv) welfare ser- vices. Most of the expenditure on administration goes to the category of general services, salaries of teachers to the category of academic services; expenditure on press, hostels, etc., forms an important item of expenditure on auxiliary services, and the expenditure on scholarships, etc., may form welfare expenditure.

Performance budget has been argued for by some (e.g., Jha, 1979) to check some of the weaknesses in the preparation of budgets. Performance budget is based on performance of the activities, and facilitates easy or quick review of the activities in terms of expenditure. 22 On the other hand, Nanjundappa (1976) suggests a thorough reclassification of the budget with the help of what he calls a hybrid approach of economic-cum-functional classification of the budget, with the help of which, he showed how several interesting details can be brought into focus, which are essential for better policy formulation. Economic-cure-functional classification of the university budget, obviously is found to be more useful than either functional or economic classification. A general format of the economic-cum-functional classification of the university budgets is given in Fig. 6 (see also Nanjundappa, 1976: 276).

Basically there is need for a standard format for the preparation of budgets and maintenance of accounts. Needed improvements in the budget format are too many. University accounts are to be maintained on income and expendi- ture basis rather than on the basis of receipts and payments, as Mukherji (1976) argued. In the latter case, accruals and deferred expenditures are not accounted for. This is particularly serious, as a substantial part of the financial manage- ment of the university consists in selectively deferring payments for liabilities incurred, often for books purchased, repairs and maintenance undertaken and SO o n .

The need for precise balance sheets, rather than mere income-expenditure

629

statements is clearly felt (e.g., Panchamukhi, 1977; Shah & Inamdar, 1980).

Universities do not present their balance sheets. Mere income-expenditure

statements do not give a complete idea of the financial strength of a particular institution. It is necessary to have an idea of the overall assets and liabilities. These will help one in the estimation of capital costs, and the amount of depreci- ation, which may in turn assist in the depreciation grant policy, if any. This also

gives an idea of the funds required for maintenance and repairs of these assets.

Mukherji (1976) also feels that there is need for maintaining a resting or capital

account. Otherwise neither expenditure by way of depreciation or maintenance of capital, nor realization of dues or bad debts can be properly allowed for and this affects the maintenance work of the university in a big way.

In addition, several suggestions were also made on accounting, auditing and related practices. As the case of Patna University revealed both internal and external audit are found to be defective. There is need for an effective internal

system of audit, which should be free from executive control (Jha, 1979). Further regular concurrent audit of university accounts should be made to introduce efficiency in auditing university accounts.

In this context, the need for cash flow analysis is also felt (Basargekar, 1978).

It not only highlights the seasonal and erratic character of flow of financial

resources into the university, their time schedule, etc., but it also helps in

estimating the minimum account of cash basically required to run the system,

below which the system just collapses. Mukherjee (1976) suggests that balanc- ing of cash and bank accounts needs to be routed through the general ledger. On the other hand, when it is done directly, as has been the case, it puts tremendous pressure on the treasurer/pro-vice-chancellor for business affairs

and finances. In short lack of delegation of financial powers is widely felt. A proper

delegation is absolutely essential to gear up efficiency in financial manage-

ment, besides creating a sense of belonging and of pride together with a

determination to work hard and sincerely.

7. Conclusion

A balance sheet of a university, which gives details on the revenue, the expenditure, and the surplus/deficit explains the financial soundness of a university. Increase or decrease in per pupil expenditure in real terms in a university over the years explains the growth of the university with respect to financial soundness. These two, however partial they are, are vital to unders- tand the financial condition of a university. On both these counts, we find that most of the universities in India are financially in unsatisfactory conditions, and that the conditions are deteriorating.

630

Universities' financial soundness can be evaluated with the help of principles of (a) autonomy, (b) adequacy and (c) built-in-flexibility. The excessive re- liance of the universities in India on state or federal grants speaks about the lack of financial autonomy the universities suffer from. In no state/central university the state/UGC grants constitute less than half of its total income/ expenditure. In fact it has been concluded that internal resources of the universities are insignificant and that the governments have to be the main sources of revenue. The earmaking of the grants restrains the autonomy to a greater extent. The continued deficits in the budgets of several universities, along with figures of accumulated deficits over time indicate how inadequate the universities are with respect to financial resources. Even if there are surpluses in the budgets of a university in a year, they are counter-balanced by huge deficits in the preceding and following years. Lastly, we note that the growth in the revenue of the university from any single source or all sources, has no relationship with variations in enrollments, size of academic faculty, etc. Neither the grants policy nor the pricing policy of universities has any built-in flexibility to take care of increase in enrollments and corresponding increase in the needs of the universities. Thus one arrives at an unpleasant finding that most of the universities in India are financially in unsound position, if not in financial crisis, due to (a) inadequate resources, and (b) improper financial planning and management both at macro as well as university levels.

We wish to conclude this paper by making a few major suggestions, all not necessarily flowing from the preceding analysis: 1. Financial planning in universities need to be attempted not in current prices,

but necessarily in real prices. Otherwise costly misconceptions in planning can not be avoided.

2. Under normal circumstances, the per student expenditure in a university, in real terms, in a year should not be allowed to be less than that in the preceding year, unless there is a drastic change in the technology of the university system and thereby in internal efficiency. This should be regard- ed as a basic or essential condition for the development of university education in India.

3. Financial responsibilities between the partners of the 'trio' viz., the univer- sity, state government and federal government should be properly divided. For instance, expenditure on core academic activities may be taken up as the responsibility of the UGC, running of establishment as that of the state government, and expenditure on students and other activities such as hostels and scholarships should be met by the university from its own resources. It also calls for effective coordination between the three partners.

4. Both the state and the UGC grants should be based upon certain well-defin- ed rational criteria. University activities should be properly costed; and unit

631

costs should form an important instrument in the grants-in-aid mechanism. No doubt there are certain activities in a university which may not be related to the number of students. But a sizeable part of the total activities do have some correspondence with the size of enrollments.

5. All sources, particularly the grants-giving authorities should see not just that the deficits in the budgets are met, but that adequate resources are maintained by the university for good housekeeping purposes and to encourage innovations, etc. Every university must have some discretionary funds at its disposal for experimentation and the government must earmark certain funds over and above the specific grants.

Above all, "it must be understood that the provision of financial assistance from the state government as also the central agencies to university institutions is not an act of benevolence grudgingly undertaken by the indifferent bureaucracy. It is an essential pre-requisite for the socio-economic develop- ment in that it helps in flowering of the intellect of the young men and women, who come under the charge of these institutions at the most formative stages of their lives. From that point of view, the grants-in-aid system should not only provide the much needed assistance to the educational institutions, but should also have the potentiality to direct the development of university institutions into desired channels" (Azad, 1984: 71).

Notes

1. The social return to higher education was estimated in mid-1960s to range between 7-12% [around 7% (Nalla-Goundan, 1967), around 10% (Kothari, 1967), 12% (Selowsky, 1967), and 9070 (Blaug et al., 1969)] and in the late 1970s to be about 10% (Tilak, 1987a). See Tilak (1987a) for an exhaustive review of rates of return to education in India.

2. Unless otherwise stated, university education throughout the paper refers to education in universities only. More clearly it excludes education in the deemed universities, institutions of national importance, and colleges for higher education.

3. Even some of the studies on university graduates (e.g., Chaudri & Rao, 1970) included under-graduate education provided in the colleges.

4. Tuition fee forms as low as 4% of total recurring income of the universities, but as a proportion of total fee income it was 45 % in 1976-77. In a good number of universities tuition fee forms an insignificant part of the total fee income, sometimes about 0.2%. Of the various components of fees, examination fees forms the largest item, followed by 'other' fees, and hostel fees; and tuition fee the least (see AIU, 1983).

5. In all, universities on which studies are available include Karnataka (Nanjundappa, 1976), Bombay (Panchamukhi, 1977), Rajasthan (Nigam, 1974), Baroda (Reddy, 1978), Kerala (Mathew, 1980), Calcutta (Mukherjee, 1976), Patna (Jha, 1979), Delhi (Balvir Singh & Pal, 1981), Punjab (Garg, 1985), and the universities in Gujarat (Lakdawala & Shah, 1978), Maharashtra (Panchamukhi, 1977) and Bihar (Singh, 1982).

6. For instance, Panchamukhi's (1977) study on Bombay University is totally distinct from other studies. Besides presenting an elaborate analysis of income and expenditure of the university, he explained the economic aspects of the behavior of the university as a non-profit institution, and in the process developed certain important general principles of financing education in

632

general, and university education in particular, and corresponding principles of resource mobilization and utilization. In the economic framework of supply and demand, the motives that influence the individuals/trusts to make endowment funds available to universities, and the factors that influence the demand for such funds by the universities, the pricing or fee policies in education, optimal grantsqn-aid system etc., are discussed in detail. Lastly, Panchamukhi also described the principles of financial soundness of a university. These are indeed quite significant aspects, which no other study has referred to. See Tilak (1980b) for an appreciation of the study. Similarly Nanjundappa (1976) in his study on the University of Karnataka, introduced economic-cum-functional classification of the university budget. The study also explored the scope for introduction of an indirect system of finances whereby repayable loans ar.e to be given directly to the students, instead of the existing method of grants to universities. See Tilak (1978) for a review of the study. The study of the finances of the Calcutta University by Mukherji (1976) presents a detailed analysis of trust funds as a subsidiary part. Since the University of Calcutta enjoys no formal legal claim on government funds, as it has been obliged to depend on its own funds by its constitution/act, the subsidiary study has provided some interesting aspects on this problem.

7. They are left because perhaps, they are larger questions, raising a number of major issues in respect of university education as a whole, not specific to financing problems of universities.

8. As an aside, it may be noted that in the present system of working of the Planning Commission and the Finance Commission, financial requirements of the individual units of the users of the funds do not appear explicitly at all. The question of monitoring of the use of funds by the individual recipients of these funds has been highlighted more than once by these agencies, viz., the Planning Commission and the Finance Commission. However, there is no mechanism of integrating this requirement in the actual working of the institutional framework at present.

9. The Ministry of Education of the central government also gives financial assistance to rural institutions and under a few schemes, like book production in regional languages and national scholarships.

10. Under the amended UGC Act of 1972, UGC also acquired powers to make maintenance grants to universities.

11. The measure of elegance (E) is defined as a ratio of what a method accomplishes (A) and its complexity (C), i.e., E = A / C . See Pratt (1982).

12. Parikh (1970) in fact suggests that such a committee can assume the total role of UGC at the state level, and the UGC at the centre can keep only central universities under its purview.

13. The unequal treatment received by the state universities vis-a-vis central universities has been well documented. See e.g., Azad (1975: 69-70).

14. It is to be noted that countries like UK and Canada preferred decentralized committees to a centralized UGC (Azad, 1975).

15. In contrast, the UGC in England grants powers of reallocation of resources to universities themselves.

16. It may be noted that while the 'earmarked' grants constitute the bulk of UGC grants, UGC also makes 'unassigned', grants which could be utilized by the universities for various purposes without reference to the UGC. However, the items for which these grants are admissible are specified by the UGC.

17. See also Tilak (1987c) for principles of allocation of resources by the centre to the states for education.

18. Coefficients of correlation estimated by Azad (1975) indicate that financial resources contri- buted by no two sources are strongly related.

19. It is based on a sample of about 70 universities. 20. See also Raza et al. (1985) who cite a similar example in case of another university where the

corresponding proportions are 56070 and 44070 in 1980, compared to 48% and 52% in 1976. Again, in a few universities like the University of Punjab (Garg, 1985) a reverse order can be noted where the proportion of salaries of the teachers increased overtime in the total salary bill.

21. It is only in a few universities a reverse trend can be noted. For instance, in the University

633

of Punjab expenditure on teaching functions increased from 33% in 1952-56 to 54~ in 1981-82, and the share of expenditure on general administration correspondingly declined from 62070 to 30% (Garg, 1985; see also Verma, 1984).

22. See Dean (1987) for a review of the performance budgeting in India.

References

Azad, J.L. (1975). Financing of Higher Education in India. New Delhi: Sterling. Azad, J.L. (1984). Government Support for Higher Education and Research. New Delhi:

Concept. AIU: Association of Indian Universities (1983). University Finance: A Statistical Profile. New

Delhi. Basargekar, S.S. (1978). "Problems of financing administration of an Indian university",

University Administration 5(2) December: 32-52. Blaug, M., Layard, P.R.G. and Woodhall, M. (1969). The Causes of Graduate Unemployment

in India. London, Allen Lane the Penguin. Bombay University (1981). "Financing of universities", University News 19(1) March: 127-9. Bose, A.N. (1976). "A few guidelines to overcome financial problems faced by universities in West

Bengal", in Kumar, B. et al., Management of Education in India. Calcutta: Indian Institute of Management (mimeo).

CABE: Central advisory Board of Education (1944). Post-War Educational Development in India: Report of the Central Advisory Board of Education 1944. Sargent Report. New Delhi: Government of India. [Reprint, 1964].

Chaudhri, D. P. and Rao, P. (1970). "Private and social returns to higher education: a case study of Delhi university graduates", Economic and Political Weekly 5 (14) 4 April: 605-08.

Dasgupta, A. K. and Tilak, J. B. G. (1983). "Distribution of education among income groups: an empirical analysis", Economic and Political Weekly 18 (33) 13 August: 1442-47.

Dean, P. N. (1987). "Performance budgeting in India", Public Finance 42 (2): 181-92. Education Commission [Chairman: D. S. Kothari] (1966). Education and NationaI Development:

Report of the Education Commission (1964-66). New Delhi: Ministry of Education [Reprint, New Delhi: National Council of Educational Research and Training, 1971].

Garg, V. P. (1985). Cost Analysis in Higher Education. Delhi: Metropolitan. Ghosh, D. K. (1981). "Financing of universities", University News 19(14) 14 July: 382-83-93. Jha, D. (1979). Report of a Study of the Finances o f the Patna University. Patna: University of

Patna (unpublished). Johnson, H. G. (1974). "The university and the social welfare: A taxonomic exercise", in Lunsden

K. G. (ed.), Efficiency in Universities: The Lapaz Papers. Amsterdam: Elsevier, pp. 21-49. Kothari, V. N. (1967). "Returns to education in India", in Singh, B. (ed.), Education as

Investment. Meerut: Meenakshi Prakashan, pp. 127-40. Lakdawala, D. T. and Shah, K. R. (1978). Optimum Utilization of Educational Expenditure in

Gujarat. Ahmedabad: Sardar Patel Institute of Economic and Social Research. Mathew, E. T. (1980). University Finances in India: A Case Study of the Kerala University. New

Delhi: Sterling. Mukherjee, M. (1981). "Financing Indian universities: an extreme view", in Singh and Sharma,

1981 : 32-40. Mukherji, K. (1976). Study of the Finances of the Calcutta University. Calcutta: Firma KLM Pvt.

Ltd. Nalla-Goundan, A. M. (1967). "Investment in education in India", Journal o f Human Resources

2 (3) Summer: 347-58. Nalla-Goundan, A. M. and Loganathan, V. (1982). Unit Costs in General Higher Education.

Madras: University of Madras (unpublished). Nanjundappa, D. M. (1976). Working of University Finances. New Delhi: Sterling.

634