unity infraprojects ltdunityinfra.com/firstcall research.pdf · 1 unity infraprojects ltd buy...

TRANSCRIPT

1

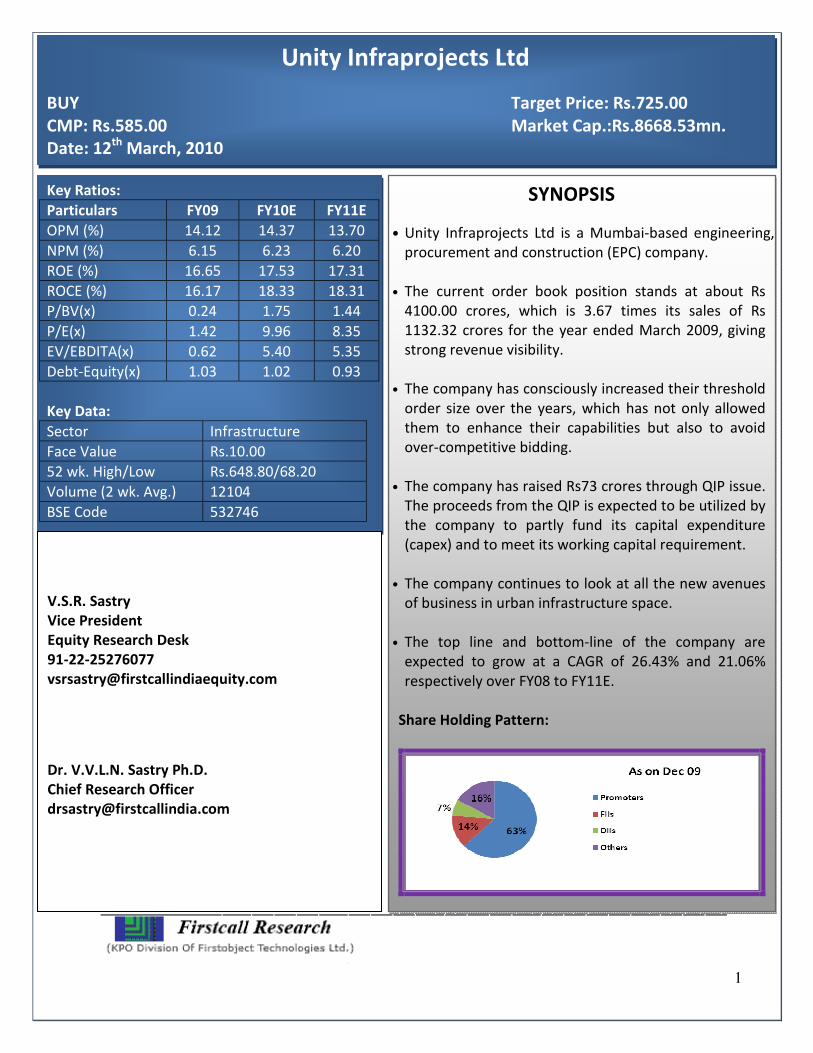

Unity Infraprojects Ltd

BUY Target Price: Rs.725.00

CMP: Rs.585.00 Market Cap.:Rs.8668.53mn.

Date: 12th

March, 2010

Key Ratios:

Particulars FY09 FY10E FY11E

OPM (%) 14.12 14.37 13.70

NPM (%) 6.15 6.23 6.20

ROE (%) 16.65 17.53 17.31

ROCE (%) 16.17 18.33 18.31

P/BV(x) 0.24 1.75 1.44

P/E(x) 1.42 9.96 8.35

EV/EBDITA(x) 0.62 5.40 5.35

Debt-Equity(x) 1.03 1.02 0.93

Key Data:

Sector Infrastructure

Face Value Rs.10.00

52 wk. High/Low Rs.648.80/68.20

Volume (2 wk. Avg.) 12104

BSE Code 532746

SYNOPSIS

• Unity Infraprojects Ltd is a Mumbai-based engineering,

procurement and construction (EPC) company.

• The current order book position stands at about Rs

4100.00 crores, which is 3.67 times its sales of Rs

1132.32 crores for the year ended March 2009, giving

strong revenue visibility.

• The company has consciously increased their threshold

order size over the years, which has not only allowed

them to enhance their capabilities but also to avoid

over-competitive bidding.

• The company has raised Rs73 crores through QIP issue.

The proceeds from the QIP is expected to be utilized by

the company to partly fund its capital expenditure

(capex) and to meet its working capital requirement.

• The company continues to look at all the new avenues

of business in urban infrastructure space.

• The top line and bottom-line of the company are

expected to grow at a CAGR of 26.43% and 21.06%

respectively over FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Company Profile 08

3. Peer Group Comparison 10

4. Key Concerns 10

5. Financials 11

6. Charts & Graph 13

7. Outlook and Conclusion 15

8. Industry Overview 16

3

Investment Highlights

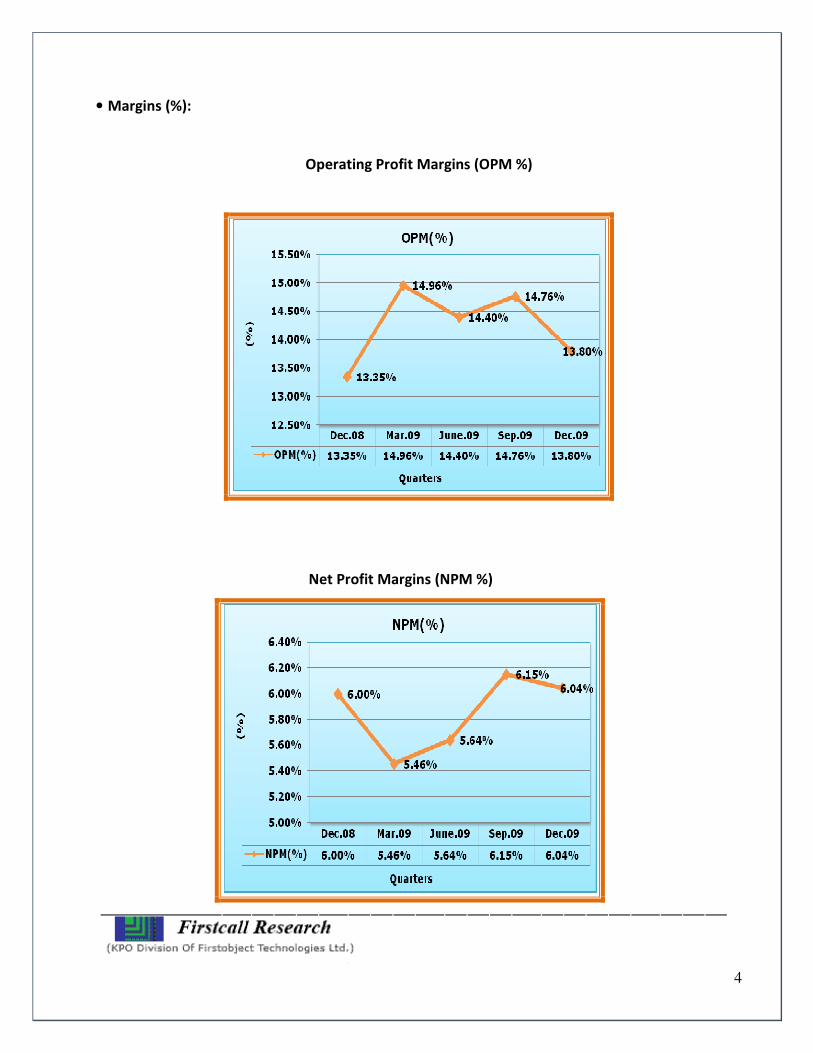

• Results Update (Q3 FY10)

For the quarter ended on December 31, 2009 (Standalone) the company has registered a 37.18 %

(YOY) growth in the net sales and stood at Rs.4036.11 mn from Rs.2942.11 mn of the

corresponding period of the previous year. The operating profit for the quarter stood at

Rs.557.01 mn from Rs.392.70 mn, for the same quarter of last year. EBITDA margins for the

quarter stood at 13.80 %. The company has reported a net profit of Rs.243.98 mn for the quarter

ended December 31, 2009 as compared to Rs.176.50 mn for the quarter ended December 31,

2008.EPS for the quarter stood at Rs.16.46 per equity share of Rs.10.0

Quarterly Results – Consolidated (Rs in mn)

As at Q3FY09 Q3FY10 %Change

Net Sales 2942.11 4036.11 37.18%

Net Profit 176.50 243.98 38.23%

Basic EPS(Rs) 13.20 16.46 24.70%

4

• Margins (%):

Operating Profit Margins (OPM %)

Net Profit Margins (NPM %)

5

• Strong Order book

The current order book stands at Rs 4150.00 crore providing revenue visibility over the next

three years. Unity currently has L-1 bid of Rs 250 crore. Unity’s average order ticket size has

improved sharply. The average order ticket size has improved to Rs 250-Rs 300 crore compared

to the Rs 50-Rs 100 crore it used to bag earlier. Unity has seen a strong order inflow in the last

few years. The company’s order inflow has grown at a CAGR of 37.9% during FY05-FY09.

Currently, the company’s order book is at Rs 4150.00cr, 3.67x FY09 revenues and 2.90x FY10E

revenues. The strong order book provides revenue visibility over the next two to three years.

Recently the Company have been awarded with the project by Ministry of External Affairs, New

Delhi for "Construction of the Indian High Commission Complex at Baridhara Diplomatic

Encalve, Dhaka, Bangladesh" amounting to Rs. 99.98 crores to be completed in 24 months.

• Combined bids

Unity does not have projects on a build-operate-transfer (BOT) model. Instead, it bids in

consortium with developers as a preferred engineering procurement construction (EPC)

contractor. It, however, does not have in-house design capability and outsources the same.

6

Unity also undertakes projects on a joint-venture basis, secured Rs 1145-crore water supply

tunnel project with IVRCL Infrastructures and Projects. Such partnering with varied developers,

while helping the company secure larger orders or enter new geographical areas, may

eventually provide it with technical qualification to bid on its own. The company has earlier

partnered Nagarjuna Constructions, Patel Engineering and Pratibha Industries, among others.

Unity also has interests in real-estate development which is not a significant contributor to

revenues and plans to go slow on these projects.

• The company’s key business strategies:

Size:

The company has consciously increased their threshold order size over the years, which has not

only allowed them to enhance their capabilities but also to avoid over-competitive bidding.

Focused diversification:

The company has used diversification to not only develop their competencies, but also hedge

against unexpected risks.It has started as a Mumbai Centric Company, but has now executed

projects across the country. As on 31st March 2009,30% of our order book is from North India,

and 12% from South India. Building on their expertise in civil construction, it forayed into

irrigation and transportation, and these now constitute 45% of our order book (as on 31" March

2009), up from 35% last year.

7

Work with reputed developers:

The company is in selective about choosing projects depending upon client reputation and their

financial abilities.

Focus on turnkey projects:

Around 62% of our order book consists of turn key man dates.

De-risking against increase in raw material costs:

Around 90% of the order book has inbuilt price escalation mechanism. This minimizes the effect

of increase in raw material prices.

Maximize opportunities in urban infrastructure space:

The company continues to look at all the new avenues of business in urban infrastructure

space.

• Approved for Stock split

The Board of Directors of the Company approved Sub-division of existing 1, 48, 17,476 equity

Shares of Rs. 10/- each to 7, 40, 87,380 equity Shares of Rs. 2/- each (In the ratio of 5 (Five)

shares of Rs. 2/- each against 1 (One) share of Rs. 10/- each).

8

• Raises Rs 73 cr via QIP issue

The company has raised Rs73 crore by private placement of 14.5 lakh shares with qualified

institutional buyers at the price of Rs506 per share. The proceeds from the qualified institutional

placement (QIP) is expected to be utilized by the company to partly fund its capital expenditure

(capex) and to meet its working capital requirement.

Company Profile

Unity Infraprojects is a Mumbai-based engineering, procurement and construction (EPC)

company that focuses on infrastructure projects.The company was originally incorporated as

Unity Builders Ltd in April 1997 to purchase and take over the construction activities of Unity

Construction Company, a partnership firm. Unity Builders Ltd was renamed Unity Infraprojects

Ltd in February 2000 and the business of Unity Construction Company was transferred to it in

August 2000. It has a large fleet of sophisticated construction equipment, including a slipform

concrete paver, a truck-mounted concrete boom placer and high-capacity concrete batching

plants, all of which are owned by the company directly or through joint ventures.

The company caters to various segments of infrastructure such as integrated engineering,

procurement and construction (EPC) services for civil projects (major revenue contributor) which

include commercial and residential buildings, mass housing projects and townships, industrial

structures, information technology parks.

9

The company is intend to continue to target opportunities and pursue more technically complex

projects in this area, including turnkey and design-build projects, to maintain and build on

dominant position.”Activities in the infrastructure projects are mainly related to the

construction of roads and the structures required for irrigation and water supply projects. The

company plans to focus on larger-sized and higher-margin infrastructure contracts. It was also

forayed into the BOT space. way station, stadiums and sports complexes, hotels, hospitals and

universities and educational campuses.The company has received the ISO 9001:2000

certification for the quality management systems it uses while executing projects.

Subsidiaries:

1. Unity Realty and Developers (URDL)

2. Unity Infrastructure Assets Ltd (UIAL)

3. Unity Middle East FZE.

Joint ventures:

1. BSEL Infrastructure Realty Ltd:

2. Backbone Enterprises Ltd:

3. Brahmaputra Infrastructure Ltd

4. Brahmaputra Consortium Ltd (BCL)

10

5. Nagarjuna Constructions

6. Patel Engineering

7. Pratibha Industries

Peer Group Comparison

Name of the

company

CMP(R.s)

(As on 12/3/2010)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E (x) P/BV

(x)

Dividend

(%)

Unity Infra 585.00 8668.53 53.92 10.79 1.86 45.00

HCC Ltd 143.70 43577.00 2.96 48.55 4.38 80.00

Nagarjuna con 158.85 40758.30 6.56 24.21 2.46 55.00

Simplex Infra Ltd 433.20 21431.40 21.53 20.12 2.53 100.00

Key Concerns

• Rising inflation

• High interest rates.

• Government policies

11

Financials

Results update

Profit & Loss Account 12 Months Ended on March 31st (Standalone)

Value(Rs. in million) FY08A FY09A FY10E FY11E

Description 12m 12m 12m 12m

Net Income 8,501.95 11,323.28 14319.62 17183.55

Other Income 121.87 155.67 109.14 120.06

Total Income 8,623.82 11,478.95 14428.76 17303.60

Expenditure -7,433.47 -9,880.22 -12371.52 -14949.68

Operating Profit 1,190.35 1,598.73 2057.24 2353.92

Interest -206.31 -400.44 -593.94 -651.03

Gross Profit 984.04 1,198.29 1463.30 1702.89

Depreciation -73.03 -159.12 -172.40 -181.02

PBT 911.01 1,039.17 1290.90 1521.86

Tax -310.56 -342.65 -398.55 -456.56

Profit after Tax 600.45 696.52 892.35 1065.30

Net profit 600.45 696.52 892.35 1065.30

Equity Capital 133.68 133.68 148.18 148.18

Reserves 3,422.68 4,048.83 4941.18 6006.49

Face Value 10 10 10.00 10.00

Total No. of Shares 13.368 13.368 14.82 14.82

EPS(Rs) 44.91 52.10 60.22 71.89

12

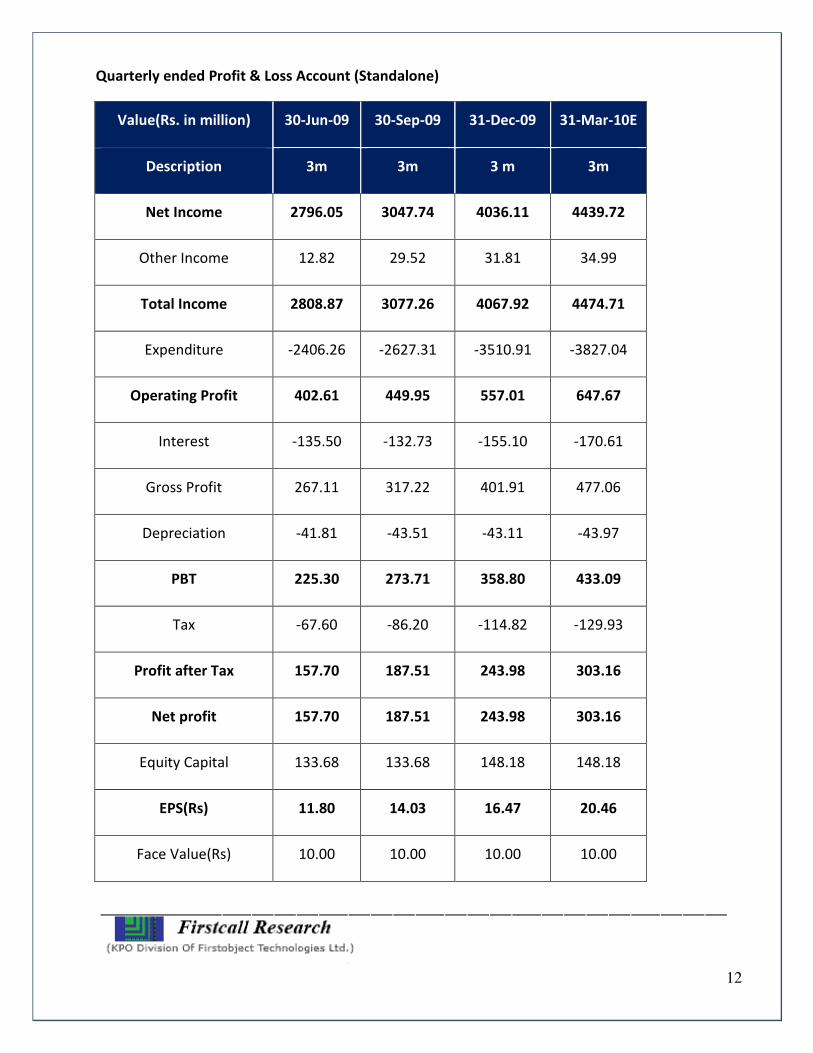

Quarterly ended Profit & Loss Account (Standalone)

Value(Rs. in million) 30-Jun-09 30-Sep-09 31-Dec-09 31-Mar-10E

Description 3m 3m 3 m 3m

Net Income 2796.05 3047.74 4036.11 4439.72

Other Income 12.82 29.52 31.81 34.99

Total Income 2808.87 3077.26 4067.92 4474.71

Expenditure -2406.26 -2627.31 -3510.91 -3827.04

Operating Profit 402.61 449.95 557.01 647.67

Interest -135.50 -132.73 -155.10 -170.61

Gross Profit 267.11 317.22 401.91 477.06

Depreciation -41.81 -43.51 -43.11 -43.97

PBT 225.30 273.71 358.80 433.09

Tax -67.60 -86.20 -114.82 -129.93

Profit after Tax 157.70 187.51 243.98 303.16

Net profit 157.70 187.51 243.98 303.16

Equity Capital 133.68 133.68 148.18 148.18

EPS(Rs) 11.80 14.03 16.47 20.46

Face Value(Rs) 10.00 10.00 10.00 10.00

13

Charts

A) Net sales & Net Profit Chart

B) EV/EBITDA(x) chart

14

C) P/E(X) Chart

D) P/BV(X) chart

15

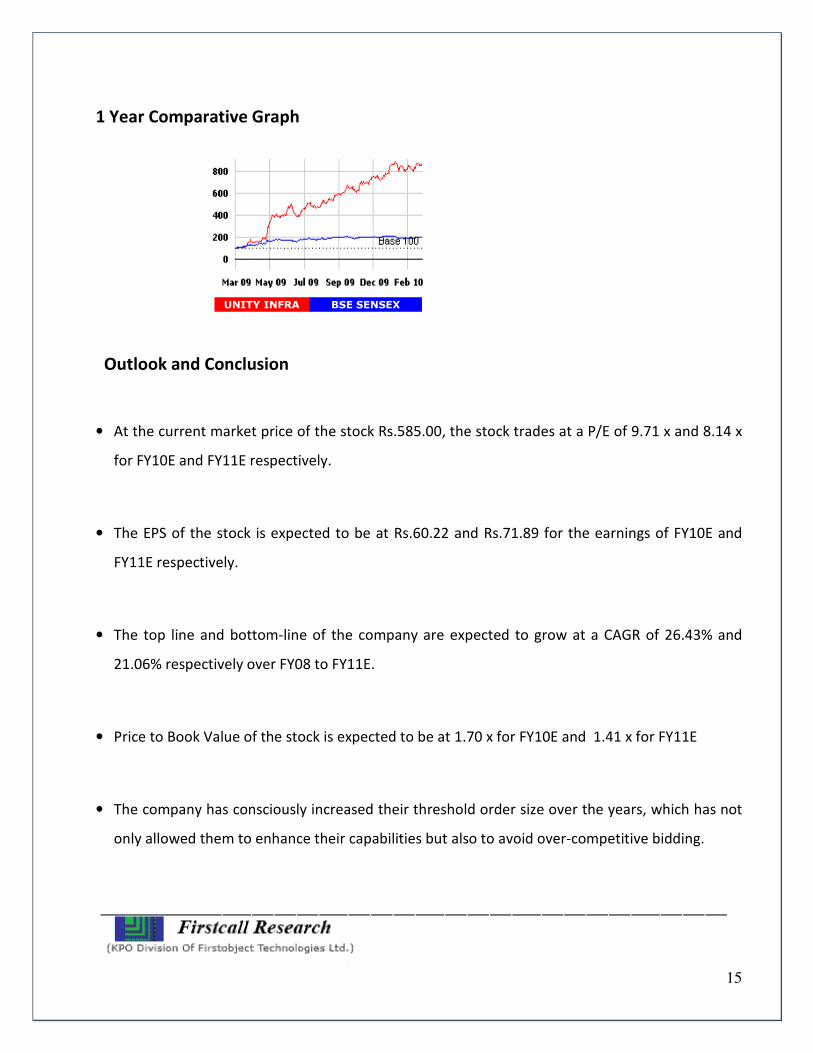

1 Year Comparative Graph

Outlook and Conclusion

• At the current market price of the stock Rs.585.00, the stock trades at a P/E of 9.71 x and 8.14 x

for FY10E and FY11E respectively.

• The EPS of the stock is expected to be at Rs.60.22 and Rs.71.89 for the earnings of FY10E and

FY11E respectively.

• The top line and bottom-line of the company are expected to grow at a CAGR of 26.43% and

21.06% respectively over FY08 to FY11E.

• Price to Book Value of the stock is expected to be at 1.70 x for FY10E and 1.41 x for FY11E

• The company has consciously increased their threshold order size over the years, which has not

only allowed them to enhance their capabilities but also to avoid over-competitive bidding.

UNITY INFRA BSE SENSEX

16

• The company has used diversification to not only develop their competencies, but also hedge

against unexpected risks.

• The company continues to look at all the new avenues of business in urban infrastructure space.

• Around 90% of the order book has inbuilt price escalation mechanism. This minimizes the effect

of increase in raw material prices.

• We recommend ‘BUY’ in this particular scrip with a target price of Rs.725.00 for Medium to Long

term investment.

Industry overview

Infrastructure Industry Structure and Development

The existence and development of adequate infrastructure is an essential requirement for

sustaining the growth momentum and to ensure required growth rate. With the rapid growth of

the economy in recent years, the importance and urgency of removing infrastructure constraints

have increased. Traditionally, power, roads, railways, ports, airports and telecommunications were

the exclusive domain of the government.

17

Infrastructure investment requires huge initial capital outlay, which was considered to be a big

hurdle in the past due to prohibition or lesser private participation on infrastructure projects. Even

in the present situation it is not possible on the part of the Government to provide the

infrastructure on its own and is under the pressure of rising gaps between demand and supply of

infrastructure. Consequently, the government is encouraging more private sector participation

through Public Private Partnership (PPPs) concept, which is fast evolving in all the aspects of

infrastructure development.

Involvement of private investments not only suffice funding requirement of the projects but it has

also other advantages like improvement in competitiveness of the projects, more efficient

execution, better offerings, etc. Out of the total outlay on infrastructure sector during 11th five

year plan, government expects 29.7% of total outlay to come from private participation and

balance (79.1%) through public funding.

The government has shown greater commitment to accelerate the infrastructure development as

indicated by its plans to raise infrastructure spending during 11th five year plan. According to 11th

five year plan, investment in infrastructure sector is likely to increase to around 8% of GDP

compared to 4.6% in 10th plan period. It is estimated that infrastructure spending of around Rs

23,850 billion is planned during the 11th Plan period. The total spending on infrastructure during

11th five year plan is almost 2.7 times bigger than anticipated spending on infrastructures during

10th five year plan. This spending is planned across the segments, with power likely to see the

maximum spending of 30.4% of total outlay during 11th five year plan. Other sectors to see major

outlay of total infrastructure spending are roads, railways and telecom with total infrastructure

outlay of 15.4%, 12.7%, 13.2% respectively.

18

Roads

Indian road network, forms 15% of India's Infrastructure investment in the 11th plan and is also

one of the busiest road networks in the world. While India has one of the longest road system in

the world, only a very small fraction of this is comparable to world standard in terms of width and

quality. About 65% of freight and 87% of passenger traffic is carried by roads in India. Traffic on

Indian roads has been increasing by 7-10% per annum which has led to about 25-30% of national

and state highways being heavily congested with truck speeds of around 25-40 km/hr. India's road

network has witnessed rapid traffic growth, which has far outstripped the capacity increase of the

road network.

The government has successfully experimented participation of private sector in road development

and expects the share of private investments to go up from 5% in 10th plan to 36% in 11th plan.

Driven by the initiatives of National Highways Authority of India (NHAI) as well as the state bodies,

the 11th plan is expected to generate investments of Rs 3,14,200 crore into the roads sector,

representing an increase of more than 110% over the corresponding investment in the 10th plan.

The 11th plan focuses on harnessing investments from the private sector, with such investments

set to increase by more than 14% over the corresponding 10th plan investments. Currently, 60

NHAI road projects are under implementation by private developers. On the other hand,

contribution from the Central and State sectors is expected to grow by just over 50%.

19

Railways

Indian Railways has been the prime mover of the nation and has the distinction of being the largest

railway system in Asia and the second largest railway system in the world under single

management. Recognizing the need for substantial financial and managerial capital, the Railways

have been actively seeking and encouraging increased private sector participation. Railways are

targeting Rs 1,20,000 crore of public-private partnership (PPP) investment and will be focused on

the modernization of metro rail stations, logistics, parks and container depots, the establishment of

manufacturing facilities for modern rolling stock and dedicated freight and high-speed passenger

corridors.

Power

The Indian power sector has grown manifold in size and capacity since independence. The per

capita power consumption has increased to approximately 612 kWh (as per Key world energy

statistics 2007) vs 1,802 kWh in China, 2,980 kWh in Middle East countries and 8,365 kWh in OECD

countries. The growth in generation capacity has been witnessed across the regions and has been

made possible by tapping into several energy sources.

While new capacity has been added, demand has far outstripped the supply leading to a widening

gap. The access to electricity has improved tremendously with electrification of almost 87% villages

and energisation of 65% pump sets. The capacity of transmission and distribution lines has also

increased but lot more need to be done. The Ministry of Power has set a vision of "providing

reliable, affordable and quality power for all by 2012".

20

From the facts above, it is clear that this provides a tremendous investment opportunity in the

Indian power sector for both the public and the private players. It is clear that the biggest

fundamental issue hampering the viability of the Indian Power Sector is the sheer volume or level

of Transmission and Distribution (T&D) losses that amount to over 30%, a very high level by any

standard. To make the matters worse, indirect calculations show T&D losses to be much higher in

the range of 40-50%. In addition, the distribution system in India is often characterized by

inefficiency, low productivity, frequent interruption in supply and poor voltage. The surge in

interest in adding new power capacity has been driven by rising power shortages, electricity

reforms initiated in 2003, deregulation of electricity sector and potential for higher returns, gradual

improvement in financial situation of some state utilities, allocation of captive blocks to private and

government companies, and initiatives like UMPP at central and state levels.

Over the past few years, the government has taken a number of steps beginning with the Electricity

Act 2003 and securitization of State Electricity Board dues to reform the private sector and attract

more private investments. Distribution reforms were brought under focus and power theft was

made a punishable offence, Accelerated Power Development and Reform programme (APDRP) was

launched to improve T&D infrastructure in the country and electricity regulatory commission has

been set up at the state level to delineate tariff setting from politics.

21

Real estate

The Indian real estate sector plays a significant role in the country's economy. Almost 5% of the

country's GDP is contributed to by the housing sector. In the next five years, this contribution to

the GDP is expected to rise to 6%. According to industry players, housing accounts for 4.5% of gross

domestic product (GDP) with urban housing accounting for 3.13%.It has also been suggested that

India's property sector could begin to improve from late 2009 and may attract up to US$ 12.11

billion in real estate investment over a five-year period.

The Indian real estate market is worth around US$ 40-45 billion and can be segregated into

residential, commercial and the retail and hospitality segments. The residential sector forms 90-

95% of the Indian reality space, while commercial segment forms 4-5% and organised retail around

1 %. The IT and ITES sector alone is estimated to require 150 million sq ft of office space across

urban India by 2010.

The organized retail industry is likely to require an additional 220 million sq ft by 2010. Moreover,

growth is not restricted to a few towns and cities but is pan-India, covering nearly all tier-l and tier-

ll cities Investments in commercial real estate are likely to increase three-fold in five years over the

previous five years. According to the Tenth Five-Year-Plan, there is a shortage of 22.4 million

dwelling units. Thus, over the next 10 to 15 years, 80 to 90 million housing dwelling units will have

to be constructed with a majority of them catering to middle and lower-income groups. Urban

housing is expected to grow at a CAGR of 14% and is expected to reach US$ 97.5 billion by 2010.

22

Irrigation

The irrigation spends by States have not seen any significant slow down until now, thanks to the

political sensitivity in lowering the spending in this sector. IVRCL is the undisputed leader in

irrigation projects across the country and irrigation projects continue to be a bulk of our water

sector portfolio. IVRCL has, in recent times, bagged some of its biggest lift irrigation projects in

Andhra Pradesh, Madhya Pradesh and Maharashtra, besides exploring the potential opportunities

emerging in other States as well.

_________________________________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase

or sale of any financial instrument or as an official confirmation of any transaction. The information

contained herein is from publicly available data or other sources believed to be reliable but we do not

represent that it is accurate or complete and it should not be relied on as such. Firstcall India Equity Advisors

Pvt. Ltd. or any of it’s affiliates shall not be in any way responsible for any loss or damage that may arise to

any person from any inadvertent error in the information contained in this report. This document is provide

for assistance only and is not intended to be and must not alone be taken as the basis for an investment

decision.

23

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com