unit 7 foreign collaboration and double taxation relief · foreign collaboration and double...

TRANSCRIPT

150

UNIT 7

FOREIGN COLLABORATION AND DOUBLE TAXATION RELIEF

STRUCTURE OF THE CHAPTER

7.1 Introduction

7.2 Agreement with foreign countries or specified territories [Sec. 90]

7.3 Adoption by Central Government of agreement between specified associations for double

taxation relief [Sec. 90A]

7.4 Countries with which no agreement exists [Sec. 91]

7.5 Summary

7.1 INTRODUCTION

This lesson discusses the tax concepts related to double taxation. To save a person from double

taxation, provisions of section 90, 90A and 91 of Income-tax Act are applicable.

Foreign Income of a person generally becomes liable to tax in two countries, the country in which

income is earned and the country in which the person is resident.

Double taxation of such income is avoided by providing some relief to the tax-payer in the

following forms:

1. Double Taxation Avoidance agreements (DTAAs/ ADTs)

2. Unilateral Relief

7.2 AGREEMENT WITH FOREIGN COUNTRIES OR SPECIFIED TERRITORIES

[SEC. 90]

The Central Government may enter into an agreement with the Government of any country outside

India (or specified territory outside India) and may, by notification in the Official Gazette, make

such provisions as may be necessary for implementing the agreement –

a. for the granting of relief in respect of –

i. income on which have been paid both income-tax under this Act and income-tax in

that country (or specified territory), as the case may be; or

ii. income-tax chargeable under this Act and under the corresponding law in force in

that country (or specified territory), as the case may be, to promote mutual

economic relations, trade and investment; or

b. for the avoidance of double taxation of income under this Act and under the corresponding

law in force in that country (or specified territory), as the case may be; or

c. for exchange of information for the prevention of evasion or avoidance of income-tax

chargeable under this Act or under the corresponding law in force in that country (or

specified territory), as the case may be, or investigation of cases of such evasion or

avoidance; or

d. for recovery of income-tax under this Act and under the corresponding law in force in that

country (or specified territory), as the case may be.

151

Applicability of the provisions –

Where the Central Government has entered into an agreement with the Government of any country

outside India (or specified territory outside India), as the case may be, for granting relief of tax (or

avoidance of double taxation), then, in relation to the assessee to whom such agreement applies,

the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Further, the provisions of this section shall apply to the assessee even if such provisions are not

beneficial to him.

Notes –

1. An assessee, not being a resident, to whom the agreement under section 90 applies, shall

not be entitled to claim any relief under such agreement unless a certificate of his being a

resident in any country outside India (or specified territory outside India), as the case may

be, is obtained by him from the Government of that country (or specified territory).

2. It is to be noted that charge of tax in respect of a foreign company at a rate higher than the

rate at which a domestic company is chargeable, shall not be regarded as less favorable

charge (or levy of tax in respect of such foreign company).

3. The Central Government has notified the following areas outside India as the 'specified

territory' for the purposes of section 90 –

a. Bermuda a British Overseas Territory

b. British Virgin Islands a British Overseas Territory

c. Cayman Islands a British Overseas Territory

d. Gibraltar a British Overseas Territory

e. Guernsey a British Crown Dependency

f. Isle of Man a British Crown Dependency

g. Jersey a British Crown Dependency

h. Netherlands Antilles an Autonomous Part of the Kingdom of Netherlands

i. Macau a Special Administrative Region of The People's Republic

of China

j. Hong Kong a Special Administrative Region of the People's Republic

of China

k. Sint Maarten a part of Kingdom of Netherlands.

Relevant Rulings on Section 90 –

1. In case of conflict between Income-tax Act and provisions of DTAA, provisions of DTAA

would prevail over provisions of Income-tax Act.

2. For claiming exemption under DTAA it is not necessary that assessee should produce proof

of payment of tax.

3. Section 90 provides relief from double taxation where income of assessee is chargeable

under Income-tax Act as well as in corresponding law in force in foreign country; therefore,

assessee would be entitled to take credit of Income-tax paid in a foreign country even in

relation to income which is exempt under section 10A.

152

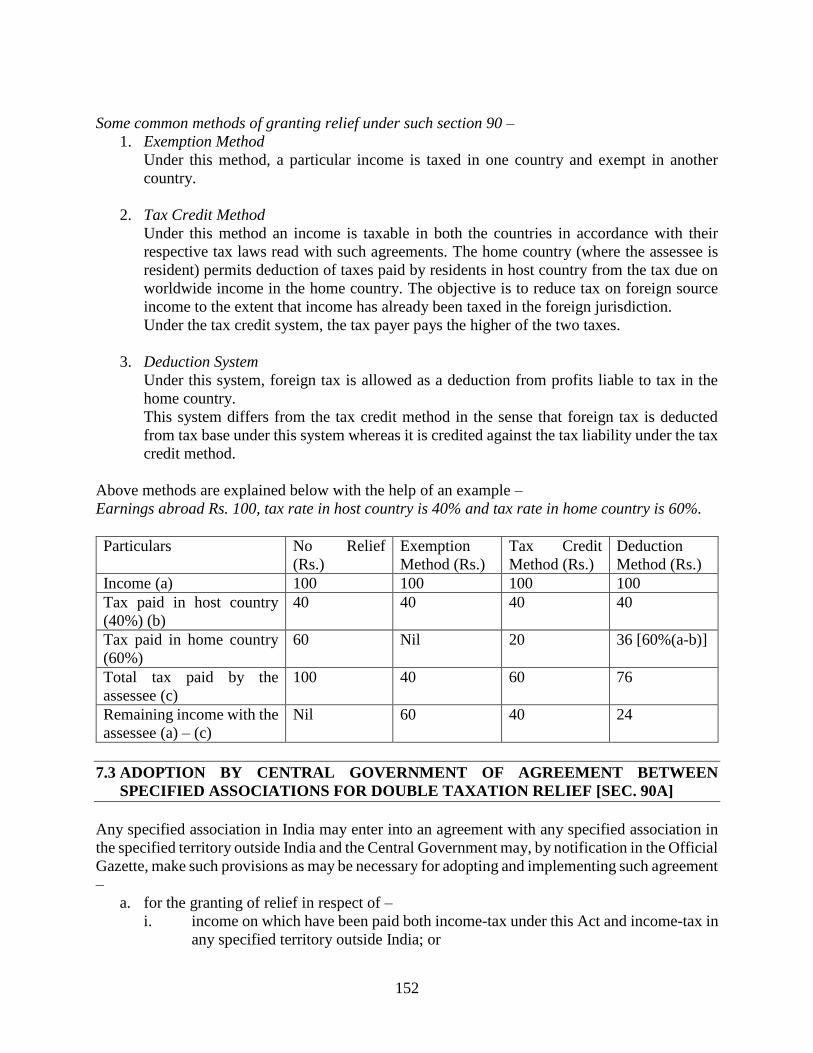

Some common methods of granting relief under such section 90 –

1. Exemption Method

Under this method, a particular income is taxed in one country and exempt in another

country.

2. Tax Credit Method

Under this method an income is taxable in both the countries in accordance with their

respective tax laws read with such agreements. The home country (where the assessee is

resident) permits deduction of taxes paid by residents in host country from the tax due on

worldwide income in the home country. The objective is to reduce tax on foreign source

income to the extent that income has already been taxed in the foreign jurisdiction.

Under the tax credit system, the tax payer pays the higher of the two taxes.

3. Deduction System

Under this system, foreign tax is allowed as a deduction from profits liable to tax in the

home country.

This system differs from the tax credit method in the sense that foreign tax is deducted

from tax base under this system whereas it is credited against the tax liability under the tax

credit method.

Above methods are explained below with the help of an example –

Earnings abroad Rs. 100, tax rate in host country is 40% and tax rate in home country is 60%.

Particulars No Relief

(Rs.)

Exemption

Method (Rs.)

Tax Credit

Method (Rs.)

Deduction

Method (Rs.)

Income (a) 100 100 100 100

Tax paid in host country

(40%) (b)

40 40 40 40

Tax paid in home country

(60%)

60 Nil 20 36 [60%(a-b)]

Total tax paid by the

assessee (c)

100 40 60 76

Remaining income with the

assessee (a) – (c)

Nil 60 40 24

7.3 ADOPTION BY CENTRAL GOVERNMENT OF AGREEMENT BETWEEN

SPECIFIED ASSOCIATIONS FOR DOUBLE TAXATION RELIEF [SEC. 90A]

Any specified association in India may enter into an agreement with any specified association in

the specified territory outside India and the Central Government may, by notification in the Official

Gazette, make such provisions as may be necessary for adopting and implementing such agreement

–

a. for the granting of relief in respect of –

i. income on which have been paid both income-tax under this Act and income-tax in

any specified territory outside India; or

153

ii. income-tax chargeable under this Act and under the corresponding law in force in

that specified territory outside India to promote mutual economic relations, trade

and investment; or

b. for the avoidance of double taxation of income under this Act and under the corresponding

law in force in that specified territory outside India; or

c. for exchange of information for the prevention of evasion or avoidance of income-tax

chargeable under this Act or under the corresponding law in force in that specified territory

outside India, or investigation of cases of such evasion or avoidance; or

d. for recovery of income-tax under this Act and under the corresponding law in force in that

specified territory outside India.

Applicability of the provisions –

Where a specified association in India has entered into an agreement with a specified association

of any specified territory outside India and such agreement has been notified for granting relief of

tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom

such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial

to that assessee.

Further, the above provisions shall apply to the assessee even if such provisions are not beneficial

to him.

Notes –

1. An assessee, not being a resident, to whom the agreement under section 90A applies, shall

not be entitled to claim any relief under such agreement unless a certificate of his being a

resident in any specified territory outside India, is obtained by him from the Government

of that specified territory.

2. It is to be noted that the charge of tax in respect of a company incorporated in the specified

territory outside India at a rate higher than the rate at which a domestic company is

chargeable, shall not be regarded as less favourable charge or levy of tax in respect of such

company.

3. "specified association" means any institution, association or body, whether incorporated or

not, functioning under any law for the time being in force in India or the laws of the

specified territory outside India and which may be notified as such by the Central

Government for the purposes of this section.

7.4 COUNTRIES WITH WHICH NO AGREEMENT EXISTS [SEC. 91]

The relief under section 91 is granted to an assessee who fulfills all the following conditions –

1. The assessee is resident in India in any previous year.

2. His income is accrued (or arose) during that previous year outside India (and which is not

deemed to accrue or arise in India).

3. He has paid tax in that country where the income accrued (or arose).

154

4. There is no agreement with than country under section 90 for the relief or avoidance of

double taxation.

Amount of relief –

Under section 91, the assessee is entitled to the deduction from the Indian income-tax payable by

him of a sum calculated on such doubly taxed income at the Indian rate of tax or the rate of tax of

the said country, whichever is the lower.

Notes –

1. "Indian rate of tax" means the rate determined by dividing the amount of Indian income-

tax after deduction of any relief due under the provisions of this Act but before deduction

of any relief due under section 90, 90A and 91, by the total income.

2. "Rate of tax of the said country" means income-tax and super-tax actually paid in the said

country in accordance with the corresponding laws in force in the said country after

deduction of all relief due, but before deduction of any relief due in the said country in

respect of double taxation, divided by the whole amount of the income as assessed in the

said country.

3. Double taxation relief is allowable on foreign income included in the net taxable income

or net taxable income, whichever is less. In other words, it can be said that relief cannot be

granted on the amount exceeding net taxable income.

4. Relief under section 91(1) is to be calculated on country-wise basis and not on basis of

aggregation or amalgamation of income of all foreign countries. Therefore, an assessee is

entitled to double income-tax relief under section 91 in respect of income from one country

without adjusting losses from another country.

Steps for calculating unilateral relief under section 91 –

Step 1: Compute the Net Taxable Income (NTI) of an assessee including foreign income.

Step 2: Compute the net tax liability (including surcharge and cess) of the assessee as per the

Income Tax Act, 1961

Step 3: Compute the Indian Rate of Tax (IRT) as well as Foreign Rate of Tax (FRT):

IRT = 𝐼𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1)* 100

FRT = 𝐼𝑛𝑐𝑜𝑚𝑒 𝑡𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝑓𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒* 100

Step 4: Relief under section 91 = Double Taxed Income* Lower of IRT and FRT

Step 5: Computation of net tax liability of the assessee in India:

Tax calculated in step (2) XX

155

minus Relief under section 91 in step (4) XX

Net tax liability of the assessee in India XXX

Case 1 –

A resident individual has derived the following income during the previous year 2015-16:

Amount (Rs.)

Income from profession 4,94,000

Share of profit from a partnership firm in Singapore 50,000

(Tax paid in Singapore for his income in equivalent Rupees is Rs. 10,000)

Interest from bank deposits in India 28,000

He wants to know whether he is eligible for any double tax relief and if so, its quantum. He also

wants to know his final tax liability. India does not have any double taxation avoidance agreement

with Singapore.

In the present case, the assessee satisfies all the given below conditions of section 91 and thus,

entitled for relief under section 91 –

1. The assessee is resident in India in any previous year.

2. His income is accrued (or arose) during that previous year outside India (and which is not

deemed to accrue or arise in India).

3. He has paid tax in that country where the income accrued (or arose).

4. There is no agreement with than country under section 90 for the relief or avoidance of

double taxation.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of the individual for the assessment year 2016-17:

Particulars Amount (Rs.)

Business Income

Income from other sources (Interest on bank deposits)

Indian Income

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under chapter VIA

Net Taxable Income (NTI)

4,94,000

28,000

5,22,000

50,000

5,72,000

Nil

5,72,000

Step 2: Tax on NTI of Rs. 5,72,000 of the individual for the assessment year 2016-17:

Amount (Rs.)

[Rs. 25,000 + 20% (Rs. 5,72,000 - Rs. 5,00,000)] 39,400

Add: Surcharge Nil

Total 39,400

Add: EC @ 2% 788

SHEC @ 1% 394

Net tax liability (Rounded off) 40,580

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

40,580/5,72,000 * 100 = 7.09%

156

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

10,000/50,000 * 100 = 20%

Step 4: Relief under section 91 = Rs. 50,000 * 7.09% = Rs. 3,545

Step 5: Net tax to be paid in India by the individual in the assessment year 2016-17

= Rs. 40,580 – Rs. 3,545 = Rs. 37,040 (Rounded off)

Note –

It is assumed that interest income from bank is earned from fixed deposits.

Case 2 –

Mr. D is a musician deriving income from concerts performed outside India of Rs. 2,50,000. Tax

of Rs. 50,000 was deducted at source in the country where the concerts were held. India does not

have any DTAA with that country. Assuming that the Indian income of D is Rs. 5,00,000, what is

the amount of tax payable by him in India for the assessment year 2016-17?

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of Mr. D for the assessment year 2016-17:

Particulars Amount (Rs.)

Indian Income

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under chapter VIA

Net Taxable Income (NTI)

5,00,000

2,50,000

7,50,000

Nil

7,50,000

Step 2: Tax on NTI of Rs. 7,50,000 of Mr. D for the assessment year 2016-17:

Amount (Rs.)

[Rs. 25,000 + 20% (Rs. 7,50,000 – Rs. 5,00,000)] 75,000

Add: Surcharge Nil

Total 75,000

Add: EC @ 3% 2,250

Net tax liability 77,250

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

77,250/7,50,000 * 100 = 10.30%

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

50,000/2,50,000 * 100 = 20%

Step 4: Relief under section 91 = Rs. 2,50,000 * 10.30% = Rs. 25,750

Step 5: Net tax to be paid in India by Mr. D in the assessment year 2016-17

= Rs. 77,250 – Rs. 25,750 = Rs. 51,500

157

Case 3 –

Professor K, an individual and citizen of India, earned the following remuneration during the

previous year 2015-16:

Amount (Rs.)

Salary from Delhi university for 8 months 4,00,000

Salary from U.S. University 4,00,000

He went to U.S. on leave without pay for four months during the previous year. He returned to

India on 1.1.2016 and brought with him Rs. 3,00,000 in convertible foreign exchange. The foreign

university deducted tax at source Rs. 50,000.

Compute the amount of tax payable for the assessment year 2016-17.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of Professor K for the assessment year 2016-17:

Particulars Amount (Rs.)

Indian Income (Income from salary)

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under chapter VIA

Net Taxable Income (NTI)

4,00,000

4,00,000

8,00,000

Nil

8,00,000

Step 2: Tax on NTI of Rs. 8,00,000 of Professor K for the assessment year 2016-17:

Amount (Rs.)

[Rs. 25,000 + 20% (Rs. 8,00,000 - Rs. 5,00,000)] 85,000

Add: Surcharge Nil

Total 85,000

Add: Cess @ 3% 2,550

Net tax liability 87,550

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

87,550/8,00,000 * 100 = 10.94%

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

50,000/4,00,000 * 100 = 12.5%

Step 4: Relief under section 91 = Rs. 4,00,000 * 10.94% = Rs. 43,760

Step 5: Net tax to be paid in India by Professor K in the assessment year 2016-17

= Rs. 87,550 – Rs. 43,760 = Rs. 43,790

Case 4 –

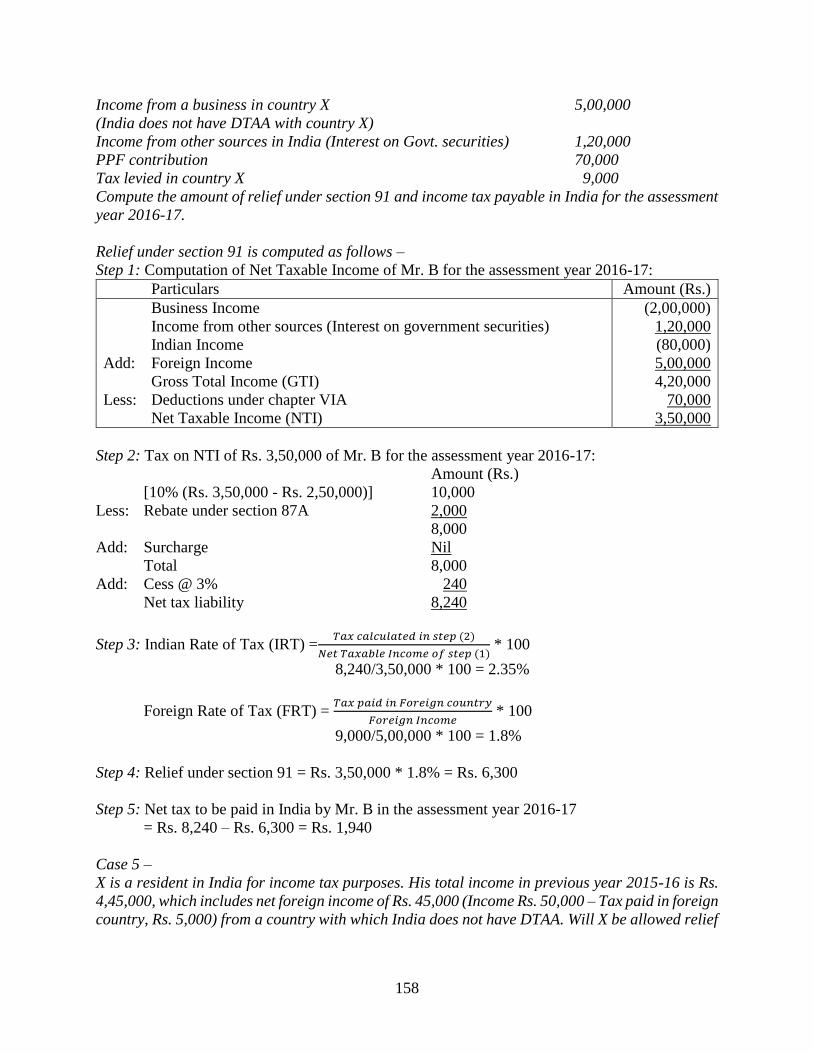

Mr. B is resident in India. The following points are noted for the previous year 2015-16 from the

books of account:

Amount (Rs.)

Income from a business in India (-) 2,00,000

158

Income from a business in country X 5,00,000

(India does not have DTAA with country X)

Income from other sources in India (Interest on Govt. securities) 1,20,000

PPF contribution 70,000

Tax levied in country X 9,000

Compute the amount of relief under section 91 and income tax payable in India for the assessment

year 2016-17.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of Mr. B for the assessment year 2016-17:

Particulars Amount (Rs.)

Business Income

Income from other sources (Interest on government securities)

Indian Income

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under chapter VIA

Net Taxable Income (NTI)

(2,00,000)

1,20,000

(80,000)

5,00,000

4,20,000

70,000

3,50,000

Step 2: Tax on NTI of Rs. 3,50,000 of Mr. B for the assessment year 2016-17:

Amount (Rs.)

[10% (Rs. 3,50,000 - Rs. 2,50,000)] 10,000

Less: Rebate under section 87A 2,000

8,000

Add: Surcharge Nil

Total 8,000

Add: Cess @ 3% 240

Net tax liability 8,240

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

8,240/3,50,000 * 100 = 2.35%

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

9,000/5,00,000 * 100 = 1.8%

Step 4: Relief under section 91 = Rs. 3,50,000 * 1.8% = Rs. 6,300

Step 5: Net tax to be paid in India by Mr. B in the assessment year 2016-17

= Rs. 8,240 – Rs. 6,300 = Rs. 1,940

Case 5 –

X is a resident in India for income tax purposes. His total income in previous year 2015-16 is Rs.

4,45,000, which includes net foreign income of Rs. 45,000 (Income Rs. 50,000 – Tax paid in foreign

country, Rs. 5,000) from a country with which India does not have DTAA. Will X be allowed relief

159

from double taxation? If so, what are the conditions prescribed for the purpose and what will be

the amount of relief and tax paid in India?

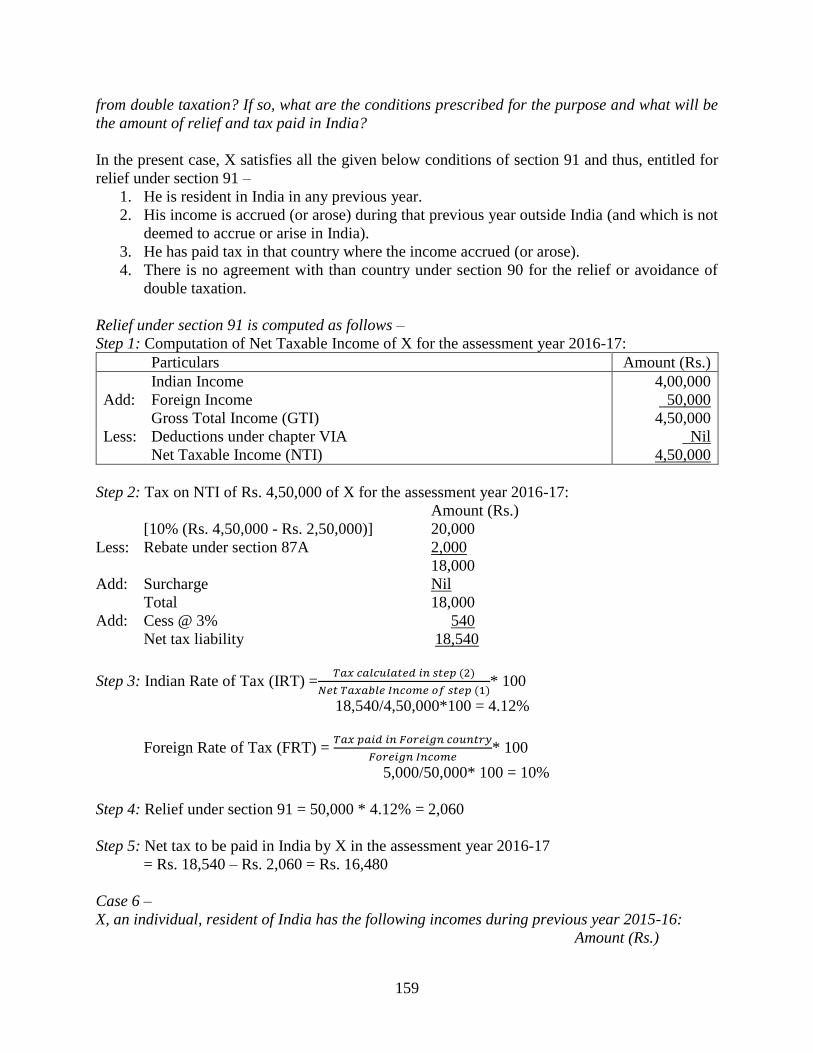

In the present case, X satisfies all the given below conditions of section 91 and thus, entitled for

relief under section 91 –

1. He is resident in India in any previous year.

2. His income is accrued (or arose) during that previous year outside India (and which is not

deemed to accrue or arise in India).

3. He has paid tax in that country where the income accrued (or arose).

4. There is no agreement with than country under section 90 for the relief or avoidance of

double taxation.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of X for the assessment year 2016-17:

Particulars Amount (Rs.)

Indian Income

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under chapter VIA

Net Taxable Income (NTI)

4,00,000

50,000

4,50,000

Nil

4,50,000

Step 2: Tax on NTI of Rs. 4,50,000 of X for the assessment year 2016-17:

Amount (Rs.)

[10% (Rs. 4,50,000 - Rs. 2,50,000)] 20,000

Less: Rebate under section 87A 2,000

18,000

Add: Surcharge Nil

Total 18,000

Add: Cess @ 3% 540

Net tax liability 18,540

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1)* 100

18,540/4,50,000*100 = 4.12%

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒* 100

5,000/50,000* 100 = 10%

Step 4: Relief under section 91 = 50,000 * 4.12% = 2,060

Step 5: Net tax to be paid in India by X in the assessment year 2016-17

= Rs. 18,540 – Rs. 2,060 = Rs. 16,480

Case 6 –

X, an individual, resident of India has the following incomes during previous year 2015-16:

Amount (Rs.)

160

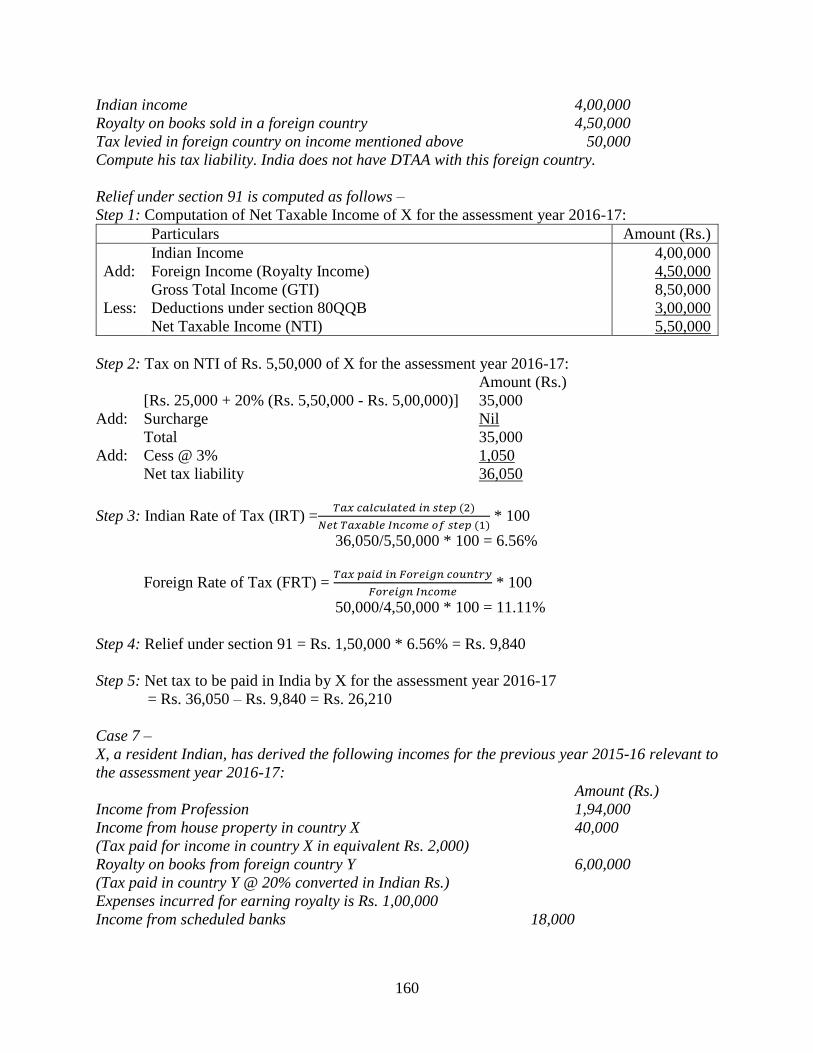

Indian income 4,00,000

Royalty on books sold in a foreign country 4,50,000

Tax levied in foreign country on income mentioned above 50,000

Compute his tax liability. India does not have DTAA with this foreign country.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of X for the assessment year 2016-17:

Particulars Amount (Rs.)

Indian Income

Add: Foreign Income (Royalty Income)

Gross Total Income (GTI)

Less: Deductions under section 80QQB

Net Taxable Income (NTI)

4,00,000

4,50,000

8,50,000

3,00,000

5,50,000

Step 2: Tax on NTI of Rs. 5,50,000 of X for the assessment year 2016-17:

Amount (Rs.)

[Rs. 25,000 + 20% (Rs. 5,50,000 - Rs. 5,00,000)] 35,000

Add: Surcharge Nil

Total 35,000

Add: Cess @ 3% 1,050

Net tax liability 36,050

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

36,050/5,50,000 * 100 = 6.56%

Foreign Rate of Tax (FRT) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

50,000/4,50,000 * 100 = 11.11%

Step 4: Relief under section 91 = Rs. 1,50,000 * 6.56% = Rs. 9,840

Step 5: Net tax to be paid in India by X for the assessment year 2016-17

= Rs. 36,050 – Rs. 9,840 = Rs. 26,210

Case 7 –

X, a resident Indian, has derived the following incomes for the previous year 2015-16 relevant to

the assessment year 2016-17:

Amount (Rs.)

Income from Profession 1,94,000

Income from house property in country X 40,000

(Tax paid for income in country X in equivalent Rs. 2,000)

Royalty on books from foreign country Y 6,00,000

(Tax paid in country Y @ 20% converted in Indian Rs.)

Expenses incurred for earning royalty is Rs. 1,00,000

Income from scheduled banks 18,000

161

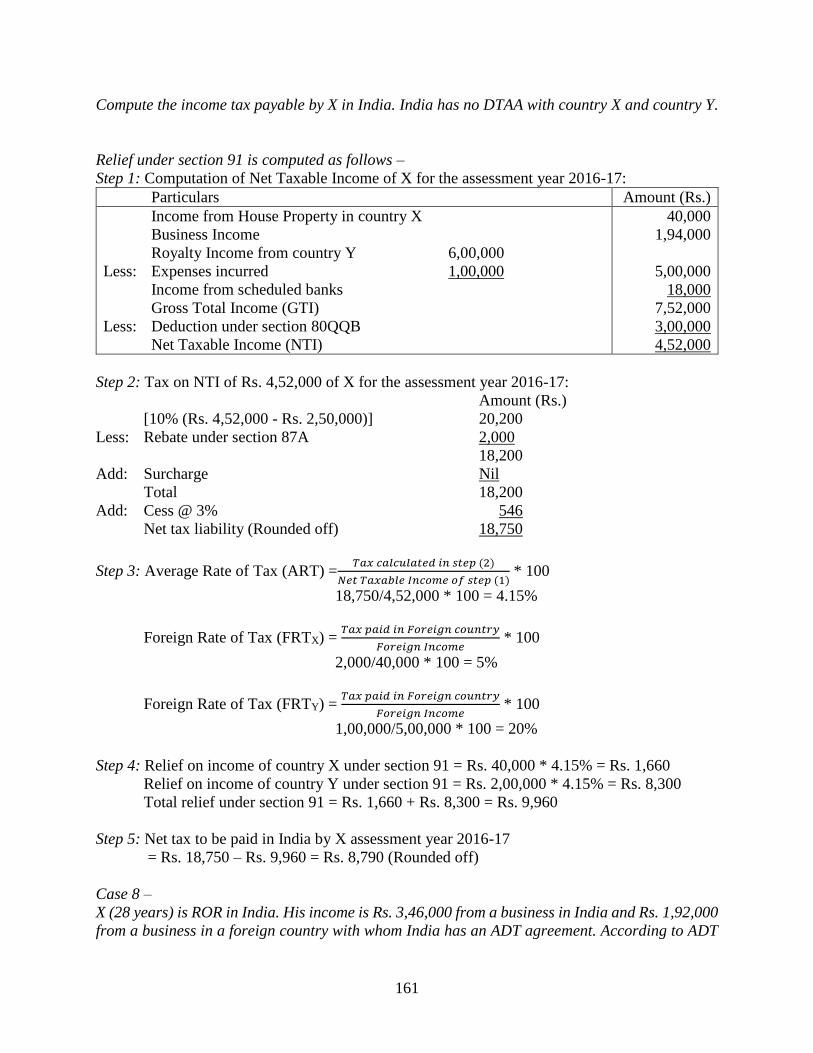

Compute the income tax payable by X in India. India has no DTAA with country X and country Y.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of X for the assessment year 2016-17:

Particulars Amount (Rs.)

Income from House Property in country X

Business Income

Royalty Income from country Y 6,00,000

Less: Expenses incurred 1,00,000

Income from scheduled banks

Gross Total Income (GTI)

Less: Deduction under section 80QQB

Net Taxable Income (NTI)

40,000

1,94,000

5,00,000

18,000

7,52,000

3,00,000

4,52,000

Step 2: Tax on NTI of Rs. 4,52,000 of X for the assessment year 2016-17:

Amount (Rs.)

[10% (Rs. 4,52,000 - Rs. 2,50,000)] 20,200

Less: Rebate under section 87A 2,000

18,200

Add: Surcharge Nil

Total 18,200

Add: Cess @ 3% 546

Net tax liability (Rounded off) 18,750

Step 3: Average Rate of Tax (ART) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

18,750/4,52,000 * 100 = 4.15%

Foreign Rate of Tax (FRTX) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

2,000/40,000 * 100 = 5%

Foreign Rate of Tax (FRTY) = 𝑇𝑎𝑥 𝑝𝑎𝑖𝑑 𝑖𝑛 𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑢𝑛𝑡𝑟𝑦

𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝐼𝑛𝑐𝑜𝑚𝑒 * 100

1,00,000/5,00,000 * 100 = 20%

Step 4: Relief on income of country X under section 91 = Rs. 40,000 * 4.15% = Rs. 1,660

Relief on income of country Y under section 91 = Rs. 2,00,000 * 4.15% = Rs. 8,300

Total relief under section 91 = Rs. 1,660 + Rs. 8,300 = Rs. 9,960

Step 5: Net tax to be paid in India by X assessment year 2016-17

= Rs. 18,750 – Rs. 9,960 = Rs. 8,790 (Rounded off)

Case 8 –

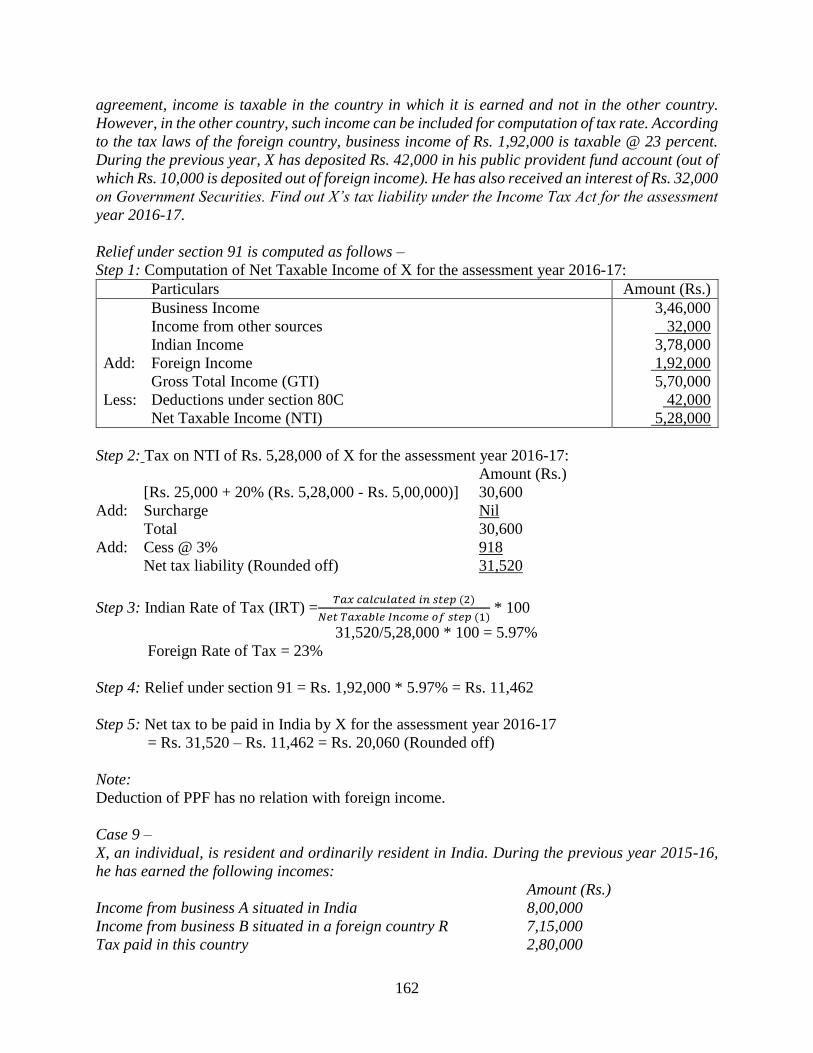

X (28 years) is ROR in India. His income is Rs. 3,46,000 from a business in India and Rs. 1,92,000

from a business in a foreign country with whom India has an ADT agreement. According to ADT

162

agreement, income is taxable in the country in which it is earned and not in the other country.

However, in the other country, such income can be included for computation of tax rate. According

to the tax laws of the foreign country, business income of Rs. 1,92,000 is taxable @ 23 percent.

During the previous year, X has deposited Rs. 42,000 in his public provident fund account (out of

which Rs. 10,000 is deposited out of foreign income). He has also received an interest of Rs. 32,000

on Government Securities. Find out X’s tax liability under the Income Tax Act for the assessment

year 2016-17.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of X for the assessment year 2016-17:

Particulars Amount (Rs.)

Business Income

Income from other sources

Indian Income

Add: Foreign Income

Gross Total Income (GTI)

Less: Deductions under section 80C

Net Taxable Income (NTI)

3,46,000

32,000

3,78,000

1,92,000

5,70,000

42,000

5,28,000

Step 2: Tax on NTI of Rs. 5,28,000 of X for the assessment year 2016-17:

Amount (Rs.)

[Rs. 25,000 + 20% (Rs. 5,28,000 - Rs. 5,00,000)] 30,600

Add: Surcharge Nil

Total 30,600

Add: Cess @ 3% 918

Net tax liability (Rounded off) 31,520

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

31,520/5,28,000 * 100 = 5.97%

Foreign Rate of Tax = 23%

Step 4: Relief under section 91 = Rs. 1,92,000 * 5.97% = Rs. 11,462

Step 5: Net tax to be paid in India by X for the assessment year 2016-17

= Rs. 31,520 – Rs. 11,462 = Rs. 20,060 (Rounded off)

Note:

Deduction of PPF has no relation with foreign income.

Case 9 –

X, an individual, is resident and ordinarily resident in India. During the previous year 2015-16,

he has earned the following incomes:

Amount (Rs.)

Income from business A situated in India 8,00,000

Income from business B situated in a foreign country R 7,15,000

Tax paid in this country 2,80,000

163

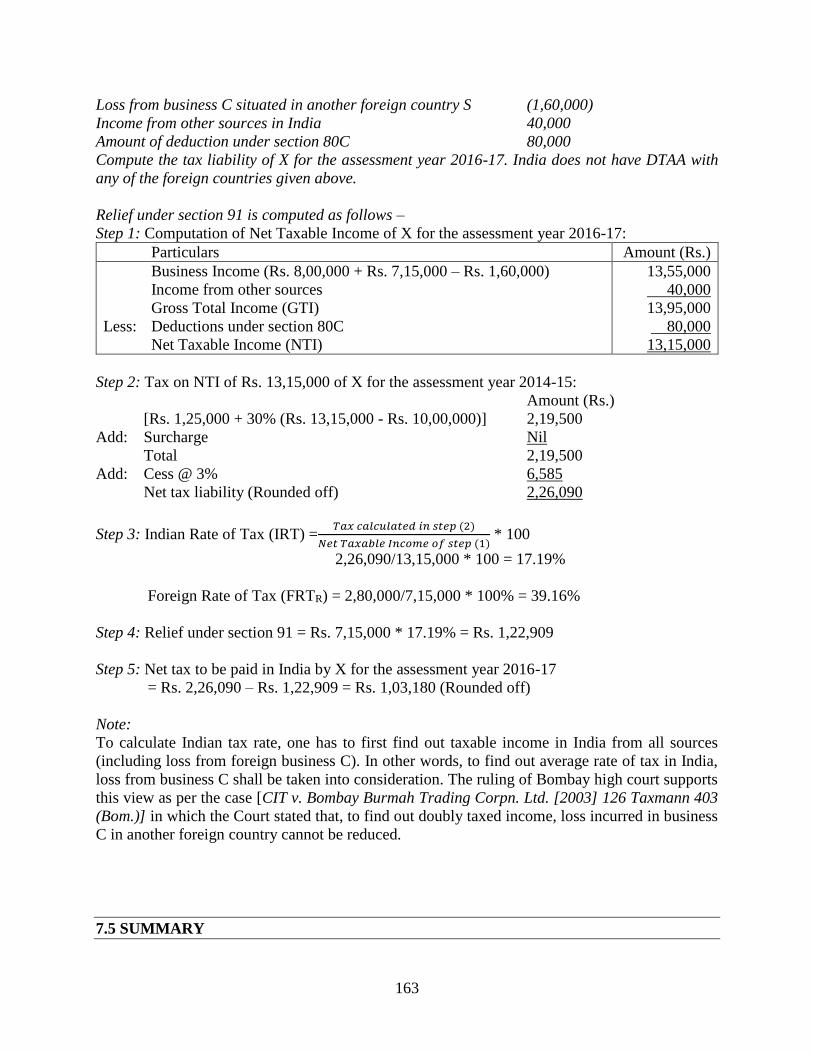

Loss from business C situated in another foreign country S (1,60,000)

Income from other sources in India 40,000

Amount of deduction under section 80C 80,000

Compute the tax liability of X for the assessment year 2016-17. India does not have DTAA with

any of the foreign countries given above.

Relief under section 91 is computed as follows –

Step 1: Computation of Net Taxable Income of X for the assessment year 2016-17:

Particulars Amount (Rs.)

Business Income (Rs. 8,00,000 + Rs. 7,15,000 – Rs. 1,60,000)

Income from other sources

Gross Total Income (GTI)

Less: Deductions under section 80C

Net Taxable Income (NTI)

13,55,000

40,000

13,95,000

80,000

13,15,000

Step 2: Tax on NTI of Rs. 13,15,000 of X for the assessment year 2014-15:

Amount (Rs.)

[Rs. 1,25,000 + 30% (Rs. 13,15,000 - Rs. 10,00,000)] 2,19,500

Add: Surcharge Nil

Total 2,19,500

Add: Cess @ 3% 6,585

Net tax liability (Rounded off) 2,26,090

Step 3: Indian Rate of Tax (IRT) =𝑇𝑎𝑥 𝑐𝑎𝑙𝑐𝑢𝑙𝑎𝑡𝑒𝑑 𝑖𝑛 𝑠𝑡𝑒𝑝 (2)

𝑁𝑒𝑡 𝑇𝑎𝑥𝑎𝑏𝑙𝑒 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑠𝑡𝑒𝑝 (1) * 100

2,26,090/13,15,000 * 100 = 17.19%

Foreign Rate of Tax (FRTR) = 2,80,000/7,15,000 * 100% = 39.16%

Step 4: Relief under section 91 = Rs. 7,15,000 * 17.19% = Rs. 1,22,909

Step 5: Net tax to be paid in India by X for the assessment year 2016-17

= Rs. 2,26,090 – Rs. 1,22,909 = Rs. 1,03,180 (Rounded off)

Note:

To calculate Indian tax rate, one has to first find out taxable income in India from all sources

(including loss from foreign business C). In other words, to find out average rate of tax in India,

loss from business C shall be taken into consideration. The ruling of Bombay high court supports

this view as per the case [CIT v. Bombay Burmah Trading Corpn. Ltd. [2003] 126 Taxmann 403

(Bom.)] in which the Court stated that, to find out doubly taxed income, loss incurred in business

C in another foreign country cannot be reduced.

7.5 SUMMARY

164

This lesson discussed the concept of double taxation. Relevant sections of Income-tax Act, 1961

which deals with double taxation relief have been discussed in detail along with practical cases.