unemployment insurance program overview

TRANSCRIPT

Unemployment Insurance Program Overview

UI Benefit Financing SeminarDivision of Fiscal and Actuarial ServicesU.S. DOL/ETA/OUIOctober 23-26, 2018

2

• The UI Program has 4 goals:– Provide temporary wage replacement for individuals

who lose a job through no fault of their own– Protect employers against dispersal of trained

workforce while temporary shutdowns are necessary– Facilitate reemployment– Help Stabilize the economy

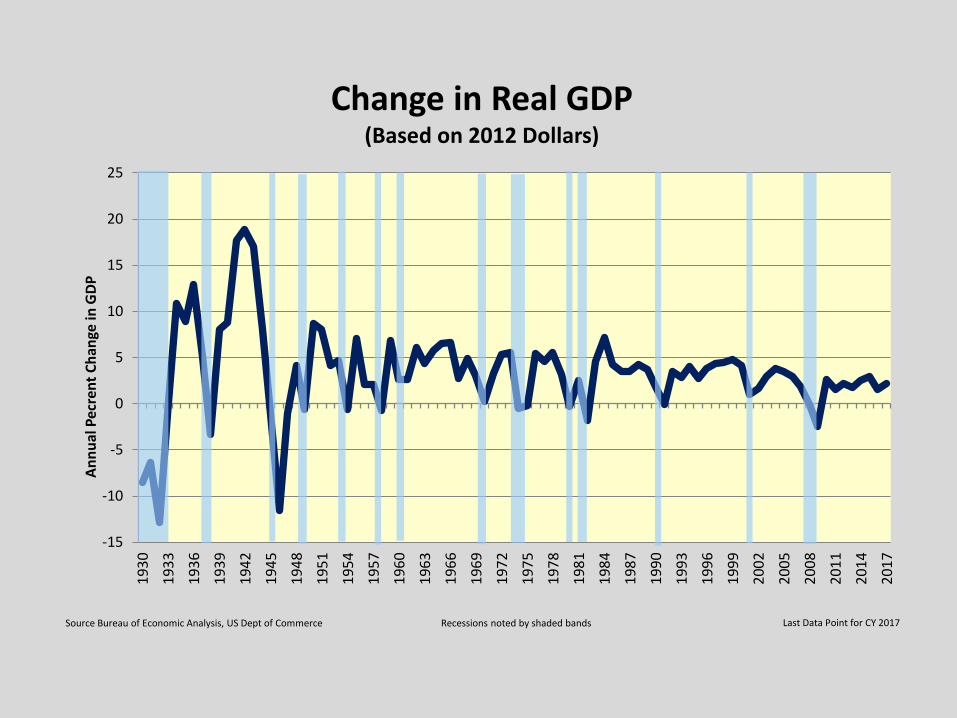

• On average, each $1 spent on UI benefits generates about $2.00 in Gross Domestic Product (GDP) through the multiplier.

• Without the UI program, GDP would decline an additional 15 percent, on average during recessions.

UI Program Goals

-15

-10

-5

0

5

10

15

20

25

1930

1933

1936

1939

1942

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

2017

Annu

al P

ecre

nt C

hang

e in

GDP

Change in Real GDP(Based on 2012 Dollars)

Source Bureau of Economic Analysis, US Dept of Commerce Recessions noted by shaded bands Last Data Point for CY 2017

0.0

0.5

1.0

1.5

2.0

2.519

50

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Perc

ent o

f Tot

al W

ages

Revenues Collected & Benefits Paid

as a Percent of Total Wages

Contributions Collected

Benefits Paid

Recessions noted by shaded bands Last data point for CY2017

5

Unemployment Insurance Program

• Background– Born 1935 as part of the Social Security Act

• Titles III, IX and XII apply

• Designed as Federal/State partnership

6

Unemployment Insurance Program– Origins

• Several states had UI programs -- employers paying taxes at competitive disadvantage

• Call for national legislation

• FDR established Committee on Economic Security

• Report issued in 1935 – basic objectives for UI:

1. Provide benefits for involuntary unemployment

2. Stabilize employment

7

Unemployment Insurance Program– Committee Recommendations

• States free to determine type of UI program

• Federal standards needed to ensure states implement UI programs

• Federal-State system

8

Unemployment Insurance Program– Why Federal-State system?

• State-only system not working

• Entirely Federal system would be cumbersome and difficult

• Hybrid system removes disadvantages in interstate competition and allowed wide latitude for experimentation

9

– Federal Level• Statute

– Sets forth broad coverage provisions, some benefit provisions, establishes the Federal tax base and rate, and provides for administrative funding.

– Motivates through incentives.

Unemployment Insurance Program

10

– Federal Level• Federal government functions:

– Ensures conformity and compliance of State laws and operations with Federal law

– Determines and collects the Federal unemployment tax

– Manages the Unemployment Trust Fund.– Responsible for administrative fund

requirements and allocates funds.– Sets broad overall policy for administration of

the program and monitors State performance

Unemployment Insurance Program

11

– State Level• State Statute:

– Sets forth benefit structure for benefit payment:• Qualification requirements, eligibility

(disqualification) provisions, benefit amount, and duration of benefits

– Establishes financing system:• Responsible for tax rate and tax base

Unemployment Insurance Program

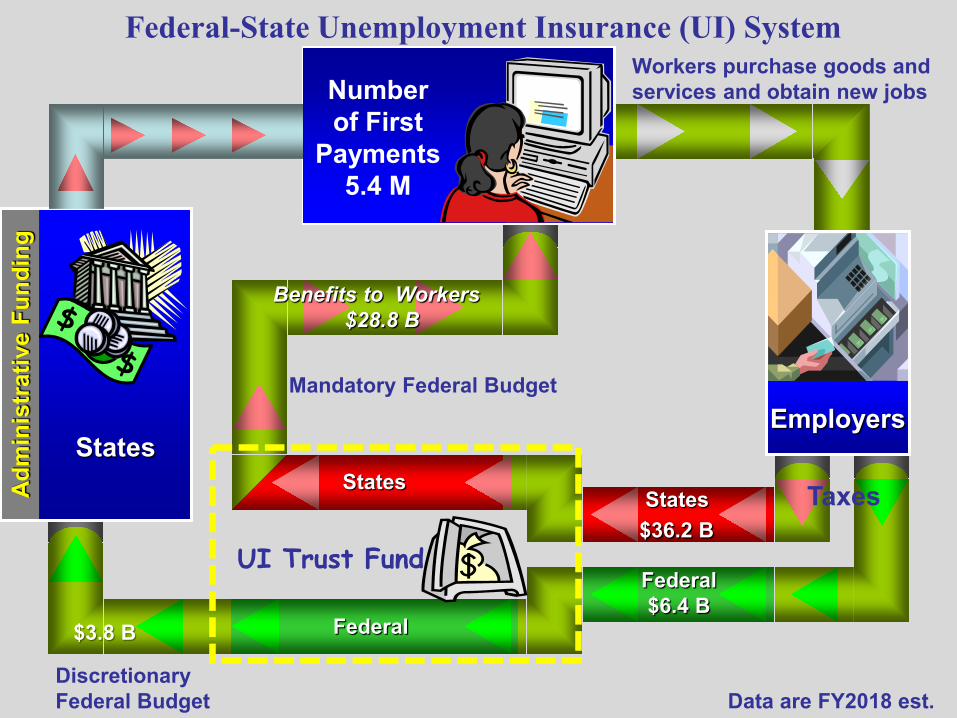

States

Mandatory Federal Budget

Discretionary Federal Budget

Federal

Federal$6.4 B

Workers purchase goods and services and obtain new jobs

UI Trust Fund

Federal-State Unemployment Insurance (UI) System

States $36.2 B

Benefits to Workers$28.8 B

Number of First

Payments5.4 M

Employers

TaxesAdm

inis

trat

ive

Fund

ing

States

$3.8 B

Data are FY2018 est.

13

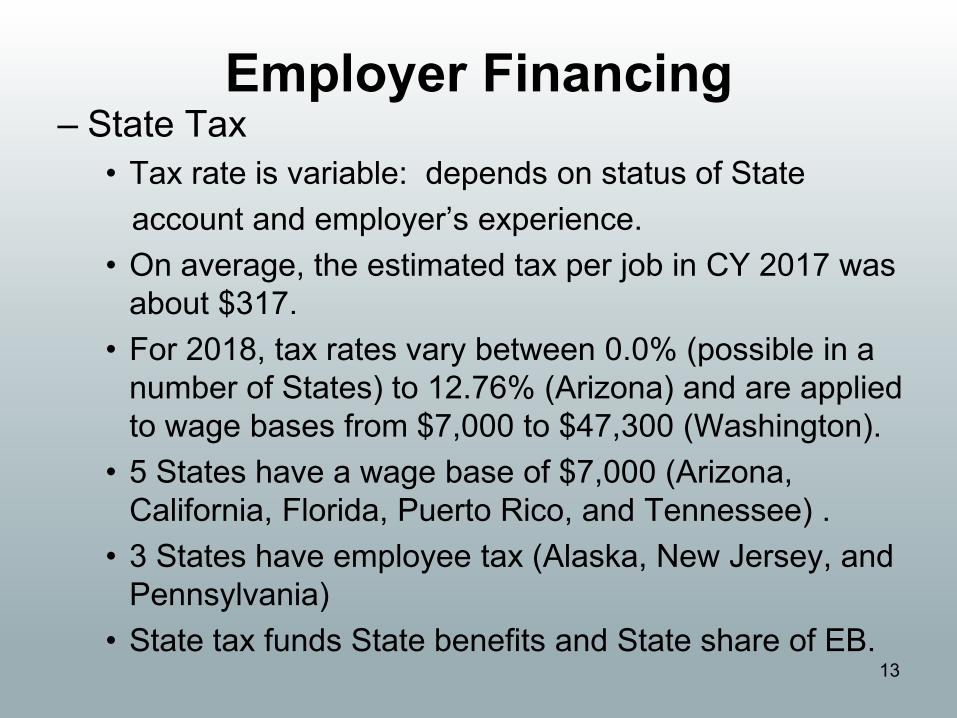

– State Tax• Tax rate is variable: depends on status of State

account and employer’s experience.• On average, the estimated tax per job in CY 2017 was

about $317.• For 2018, tax rates vary between 0.0% (possible in a

number of States) to 12.76% (Arizona) and are applied to wage bases from $7,000 to $47,300 (Washington).

• 5 States have a wage base of $7,000 (Arizona, California, Florida, Puerto Rico, and Tennessee) .

• 3 States have employee tax (Alaska, New Jersey, and Pennsylvania)

• State tax funds State benefits and State share of EB.

Employer Financing

14

- Federal• Uniform• 6.0% of first $7,000 of each covered employee’s wages

(5.4% FUTA tax credit results in a net tax of 0.6%) • $42 maximum per covered employee• Pays for State and National/Regional Office

Administration for UI and the Employment Service, Federal share of Extended Benefits (EB), loans to States, Veterans Employment and Training Services, and Certain Labor Market Information activities.

Employer Financing

15

Federal Unemployment Tax ActFUTA

• FUTA establishes the financing framework • Section 3301 establishes the payroll tax rate

at 6.0%• Section 3302(c)(1) & Section 3302(d)(1)

provide for a credit of up to 5.4%• Section 3302(a)(1) and Section 3302(b)(1)

split the credit into two parts: “normal” credit & “additional” credit

16

Federal Unemployment Tax ActFUTA

• Normal credit– Amount of money paid in state UI taxes– Allowable if conditions in 3304 are met for the

12 month period ending on October 31– Conditions in 3304 primarily deal with deposit

and withdrawal standards and when compensation is payable

– One way Federal law provides for incentives

17

Federal Unemployment Tax ActFUTA

• Additional credit– Amount of money determined by taking the highest

tax rate any employer could receive during the taxable year or 5.4%, which ever is lower, applying that rate to the federal taxable wage base, and subtracting from the result the amount of an employer’s normal credit

18

Federal Unemployment Tax ActFUTA

• Additional credit– Allowable if conditions in 3303(a) are met for the

12 month period ending on October 31

– A key condition: employer tax rates are determined by “experience with respect to unemployment or other factors bearing a direct relation to unemployment risk”

19

Federal Unemployment Tax ActFUTA

• Section 3306(b)(1) establishes the Federal taxable wage base

• Federal wage base is currently $7,000

20

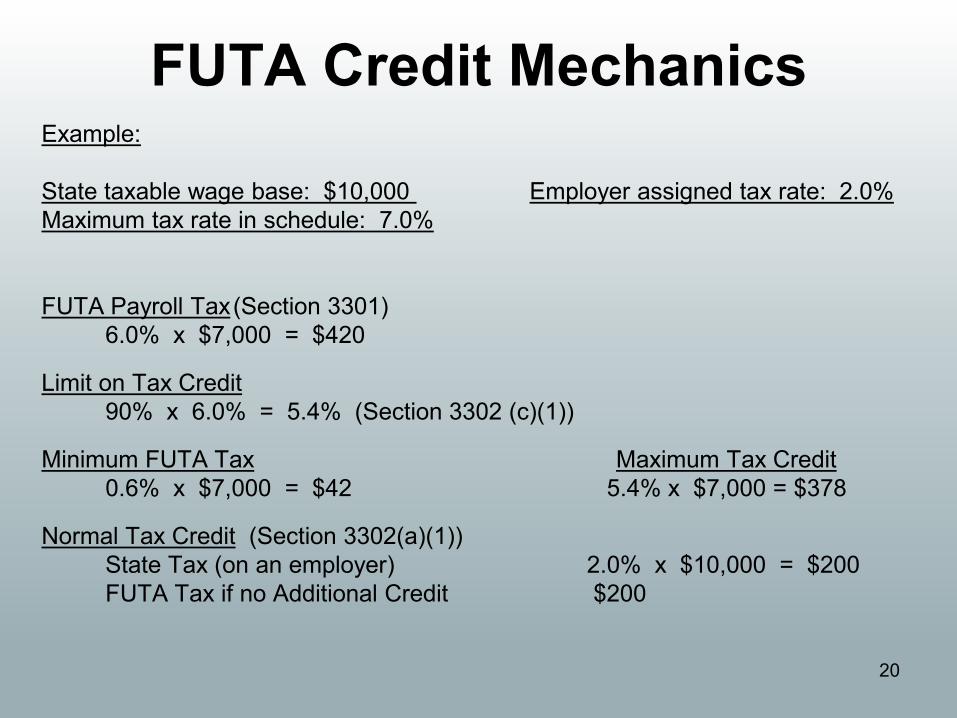

FUTA Credit MechanicsExample:

State taxable wage base: $10,000 Employer assigned tax rate: 2.0%Maximum tax rate in schedule: 7.0%

FUTA Payroll Tax(Section 3301)6.0% x $7,000 = $420

Limit on Tax Credit90% x 6.0% = 5.4% (Section 3302 (c)(1))

Minimum FUTA Tax Maximum Tax Credit0.6% x $7,000 = $42 5.4% x $7,000 = $378

Normal Tax Credit (Section 3302(a)(1))State Tax (on an employer) 2.0% x $10,000 = $200FUTA Tax if no Additional Credit $200

21

FUTA Credit MechanicsAdditional Tax Credit (Section 3302(b))

Multiply the lower of the state maximum tax rate or 5.4% times the federal 5.4% x $7,000 = $378taxable wage base.

Normal Credit (Actual State Contribution) 2.0% x $10,000 = $200Additional Credit $178

Total Credit Total Tax$200 + $178 = $378 $420 - $378 = $42Maximum credit = $378

22

FUTA Credit Mechanics with 5% Max State Tax

Additional Tax Credit (Section 3302(b))Multiply the lower of the state maximum tax rate or 5.4% times the federal 5.0% x $7,000 = $350taxable wage base.

Normal Credit (Actual State Contribution) 2.0% x $10,000 = $200Additional Credit $150

Total Credit Total Tax$200 + $150 = $350 $420 - $350 = $70Maximum credit = $378

23

Unemployment Trust Fund

Unemployment Trust FundPays 1/2 cost of extended

benefitsCeiling = .5% of total wages

In covered employment prior CY

Makes loans to insolvent state accounts when needed

Ceiling = .50% of total wages In covered employment

prior CY

Pays for stateadministrative costsCeiling = 40% of current

year’s appropriation

When all 3 Federal accounts reach/exceed their ceilings on Sept. 30, the amount in excess of the ceiling is distributed to

state accounts on Oct. 1.

53 State Accounts

Excess flows to ESAA Sept. 30 Excess flows to ESAA Sept. 30

25

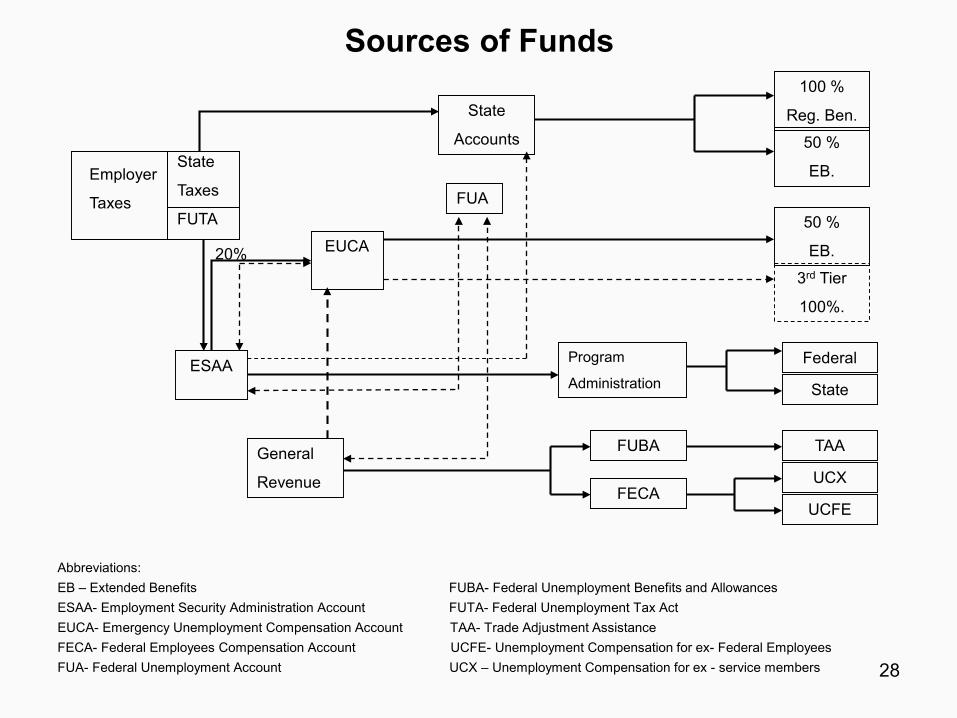

• Title IX of the SSA establishes the Unemployment Trust Fund (UTF) which contains the accounts relevant to the UI Program:

– Accounts for each of the 53 UI jurisdictions from which UI benefits are paid.

– Employment Security Administration Account (ESAA) from which administrative funds are appropriated for UI, the Employment Service, Labor Market Information, and the Veterans Employment and Training Services. Receives 80 percent of FUTA tax

Unemployment Trust Fund

26

– Extended Unemployment Compensation Account (EUCA) from which the Federal share of Extended Benefits (EB) is paid. Receives 20 percent of FUTA tax.

– Federal Unemployment Account (FUA) provides advances to States whose State UI account becomes insolvent. Receives overflow from ESAA & EUCA.

Unemployment Trust Fund

27

– Federal Employee Compensation Account (FECA) acts as a revolving fund from which benefits to ex-service persons and former Federal employees are paid benefits. The appropriate agency is then charged the amount of the benefits to replenish the account. Initially funded from general revenue.

Unemployment Trust Fund

28

Sources of Funds100 %

Reg. Ben.

50 %

EB.

50 %

EB.3rd Tier

100%.

Federal

State

TAA

UCX

UCFE

State

Accounts

FUA

EUCA

Program

Administration

FUBA

FECA

General

Revenue

ESAA

Employer

Taxes

State

Taxes

FUTA

Abbreviations:EB – Extended Benefits FUBA- Federal Unemployment Benefits and AllowancesESAA- Employment Security Administration Account FUTA- Federal Unemployment Tax ActEUCA- Emergency Unemployment Compensation Account TAA- Trade Adjustment AssistanceFECA- Federal Employees Compensation Account UCFE- Unemployment Compensation for ex- Federal EmployeesFUA- Federal Unemployment Account UCX – Unemployment Compensation for ex - service members

20%

StateUI

Reduced Credits to Loan Fund

(FUA)

.120 to EUCA

.456SESAGrants

.024 Fed

Admin

50%EB

50%EB

Claimant SESAAdmin. Cost

State Tax* FUTA

Employer

TreasuryIRS UTF

DOL UI ES VETS BLS

* Deposited in State agency bank account for transfer directly State Trust Fund account. Access only by State to pay benefits.

Unemployment Trust Fund

Federal/State UI SystemResources and Distribution Employer FUTA 6.0%

Credit for State 5.4%Net FUTA tax 0.6%

Tax = 0.6% of $7000 on each employee

1. Additional Tax credit reduction to loan

0.6 % Tax to ESAA.120 to EUCA.456 to SWA.024 to Fed

29

Program Environment

31

The Long-Term Unemployed still need assistance

Source: Bureau of Labor and Statistics: Current Population Survey

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

(Tho

usan

ds o

f Per

sons

)

Incidence of Long Term Unemployed

July 2018 Long-Term Unemployment22.7% of Unemployed Population

1.4 Million People

Unemployed over 27 Weeks

Unemployed under 27 Weeks

32

Job Growth and Unemployment Rate

SOURCE: Bureau of Labor Statistics

0

2

4

6

8

10

12

100

105

110

115

120

125

130

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Une

mpl

oym

ent R

ate

%

Priv

ate

Payr

oll E

mpl

oym

ent (

Mill

ions

)

Private Payroll Employment

Unemployment Rate

0%

10%

20%

30%

40%

50%

60%

70%

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Calendar Year

U.S. Recipiency Rates(All Programs, Annual, 1978 - 2017)

Unemployment Rates by StateSeasonally Adjusted, August 2018

(U.S. Rate = 3.9% )

0% to 3%3% to 4%4% to 5%5% and greater

Total Number of States that have Borrowed

Number of States with Outstanding Balances August 30,

2018

Peak Amount

Advanced to States

Outstanding Advance Balance

August 30, 2018

36

1

$47.2 B

$68.6 M

Total borrowing over time and projected borrowing through 2024

0

200

400

600

800

1,000

1,200

1,400

0

5

10

15

20

25

30

35

40

45

50

Milli

ons

Bill

ions

$

End of FY Borrowing

Actual Forecast

Private Borrowing Private BorrowingForecast

Interest Paid on Title XII Advances

37

Middle Class Tax Relief and Jobs Creation Act P.L. 112-96

• Short Time Compensation

• Self Employment Assistance

38

Short Time Compensation

• Federal law gives states authority to provide a reduced UI weekly benefit amount to individuals whose work weeks have been reduced.

• 27 states have an enacted law • P.L. 112-96 modified STC and added

3306(v) FUTA

39

Self-Employment Assistance

• Federal law gives states authority to establish an SEA program under 3306(t) FUTA.

• 5 states have enacted programs• P.L. 112-96 permits states to establish

programs for EB and EUC claimants.

Reemployment Services and Eligibility Assessments

• The Bipartisan Budget Act of 2018, Public Law 115-123 established permanent authorization for the RESEA program by adding Section 306 to Title III of the Social Security Act.

• Federal Register Notice forthcoming to request suggestions on how to allocate administrative funds.

41

Glossary• Benefit Payment Account – An account with a bank into which a

State transfers funds from its UTF account in order to pay benefits.• Clearing Account - An account with a bank into which a State

deposits UI tax collections.• ESAA - Employment Security Administration Account. Provides

administrative grants to States for UI, ES, some Veterans Employment and Training Programs, and Labor Market Information. Also pays for Federal administrative costs.

• EUCA - Extended Unemployment Compensation Account. Pays for Federal share of Extended Benefits (EB).

• FECA - Federal Employees Compensation Account. Pays benefits to ex-Federal workers and ex-service persons.

• FUA - Federal Unemployment Account. Makes repayable advances to insolvent State trust funds.

• FUBA - Federal Unemployment Benefit Allowances. Appropriation which provides for Trade Adjustment Assistance.

42

Glossary• FUTA - Federal Unemployment Tax Act. Authorizes Federal

government to impose a payroll tax on employers for each employee.• NASWA - National Association of State Workforce Agencies.• RJM - Resource Justification Model. A data collection instrument used

in the budget process.• RESEA – Reemployment Services and Eligibility Assessments• UCFE - Unemployment Compensation for former Federal Employees• UCX - Unemployment Compensation for ex-servicemen• UTF - Unemployment Trust Fund. Includes State and Federal

Accounts.• UWC, Inc. - Unemployment and Workers’ Compensation, Inc. An

organization representing employers on unemployment and workers’ compensation matters.E