underwriting underwriting update with aig success through partnership november 2005

TRANSCRIPT

UnderwritingUnderwriting

Underwriting update with AIGUnderwriting update with AIG

Success through partnership

November 2005

UnderwritingUnderwriting

Update

• AIG process

• What have change

• Why do we rate?

• Hot topic – new immigrant, travel, non resident, financial update

• How to speed the process

UnderwritingUnderwritingOntario Underwriting Team

• Life Product

– Stuart Gray, Barb Cornwall, Judi Scetta, Chantal Lacoste, Janet Nosko, Kirti Sharma, Angèle Houle

• CI Product

– Luc Jodoin

• Policy Changes / Assurance Product

– Christian Ah-Kian

• Helene Chatelain, VP U/W & NB

• Serena Galea, Manager NB

UnderwritingUnderwriting

The process

• Using AIG’s tools – FMIS– NB phone team – Region Team

UnderwritingUnderwriting

What you need to know

• U/W age and amount guidelines per product

• Long App vs. Rapid App?

• Most common inquiry –travel, medical

• Financial guidelines– Income, net worth, financial questionnaire on

long app– Purpose, where premium are coming from,

which sales concept was use…

UnderwritingUnderwriting

What have changes and why– Reinsurance change – Reason why:

• More quota share due to high reserving and capital requirements for direct Co.

• Pricing rates – preferred, etc

• Fight for market shares

• Less risk kept by direct Co

• Changes in reinsurances treaties

• Audits review – claim review

– How do we now manage these changes

UnderwritingUnderwriting

Reinsurance issue• Reinsurance issue• AIG use 3 reinsurers

– Travel issue –product, amount length of time, where.

– Capacity issue

– Shopping issue

– Misrepresentations issue

UnderwritingUnderwritingUnderstanding and Explaining Mortality

and Medical tests

• Why do we rate?

• Height and weight table

• Cholesterol table

• Blood profile

• Urine test

• Saliva testing

• Other test

UnderwritingUnderwriting

Rating why?• Underwriting is the evaluation of medical conditions

and histories that may affect the mortality or morbidity.

• Mortality is the relative incidence of death among a given group of people

• Morbidity is the relative incidence of sickness or disease among a given group of people

• Standard mortality is represented by 100%

• Additional rating indicate the degrees of the extra risk

• The rating needs to compensate for the anticipated increase in mortality or morbidity.

UnderwritingUnderwritingLife Expectancies (75-80 basic tables)

• Male-Non-Smoker• Age 100% 200% 400

• 30 50 43 37

• 50 32 26 20

• 65 20 15 12

• Male Smoker• 30 44 36 30

• 50 26 20 15

• 65 17 12 9

UnderwritingUnderwriting

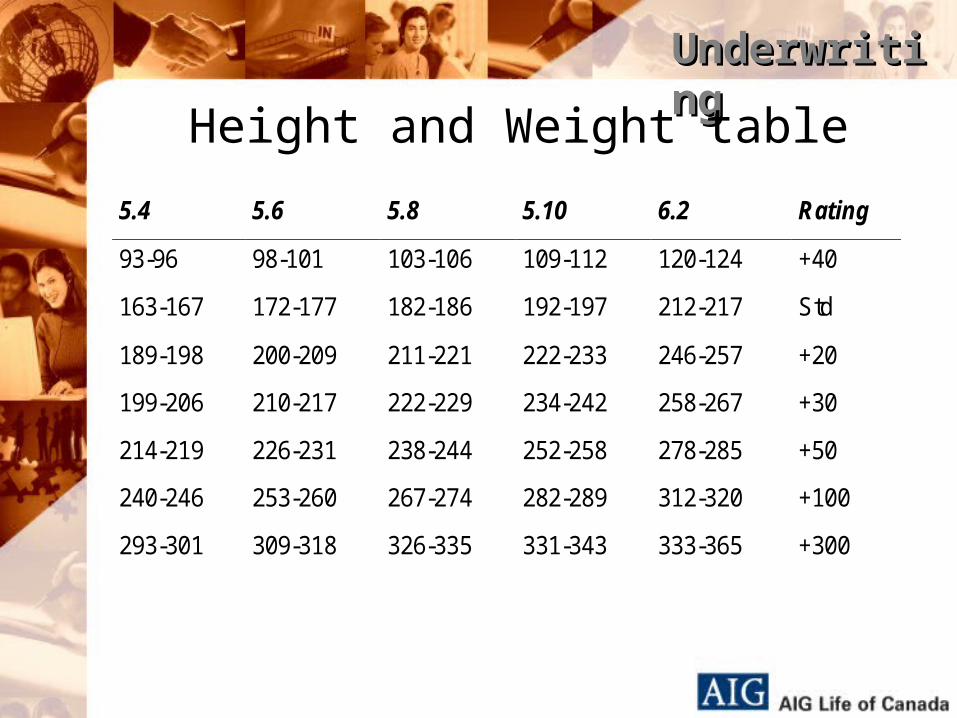

Height and Weight table

5.4 5.6 5.8 5.10 6.2 Rating

93-96 98-101 103-106 109-112 120-124 +40

163-167 172-177 182-186 192-197 212-217 Std

189-198 200-209 211-221 222-233 246-257 +20

199-206 210-217 222-229 234-242 258-267 +30

214-219 226-231 238-244 252-258 278-285 +50

240-246 253-260 267-274 282-289 312-320 +100

293-301 309-318 326-335 331-343 333-365 +300

UnderwritingUnderwriting

Cholesterol table

CHOL/HDL LDL/HDL CHOL CHOL Rating

<8.0 <4 <250mg/dl <6.47mmol/l +0

8.0-9.5 4.0-6.3 250-299 6.47-7.75 +25

9.6-15 6.4-8.5 300-349 7.76-9.04 +50

15.1-20 8.6-12.0 350-400 9.05-10.34 +100

>20 >12.0 >400 >10.34 IC

UnderwritingUnderwriting

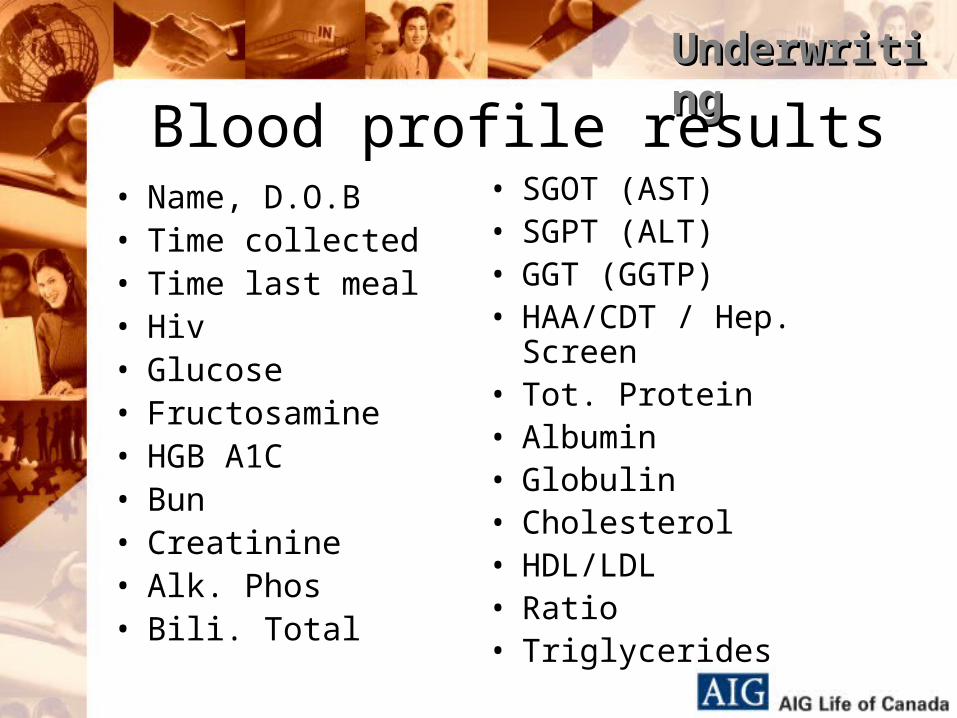

Blood profile results• Name, D.O.B• Time collected• Time last meal• Hiv• Glucose• Fructosamine• HGB A1C• Bun• Creatinine • Alk. Phos• Bili. Total

• SGOT (AST)• SGPT (ALT)• GGT (GGTP)• HAA/CDT / Hep. Screen• Tot. Protein• Albumin• Globulin• Cholesterol• HDL/LDL• Ratio• Triglycerides

UnderwritingUnderwriting

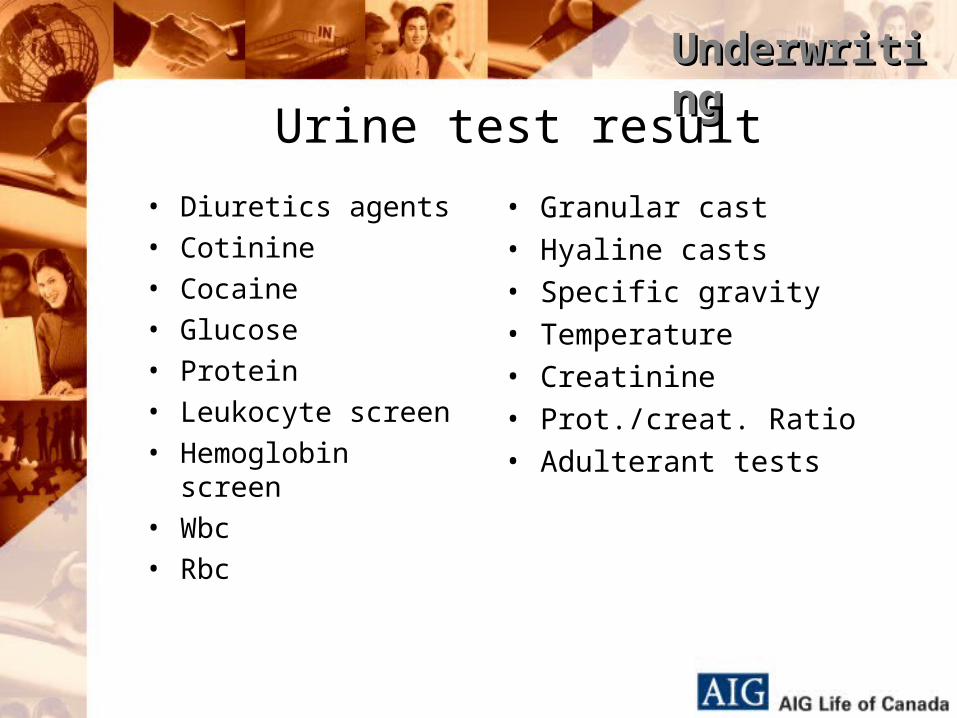

Urine test result

• Diuretics agents

• Cotinine

• Cocaine

• Glucose

• Protein

• Leukocyte screen

• Hemoglobin screen

• Wbc

• Rbc

• Granular cast

• Hyaline casts

• Specific gravity

• Temperature

• Creatinine

• Prot./creat. Ratio

• Adulterant tests

UnderwritingUnderwriting

Common problems in underwriting

• Diabetes

• Myocardial Infarction

• Cancer

• Life style – travel, financial

UnderwritingUnderwriting

MYOCARDIAL INFARCTIONMYOCARDIAL INFARCTION

• NUMBER OF EPISODES• CHEST PAIN• SURGERY / BYPASS• CURRENT CONDITION• SMOKING• AGE AT ONSET• OTHER IMPAIRMENT ( BP, CHOL, SMOK...)

UnderwritingUnderwriting

Cancer

• Age at Onset

• Type / Grade

• Localized / Metastasis

• Treatment / date of last treatment

• Surgery

• Recurrence

UnderwritingUnderwriting

Medical Underwriting: Additional issues

• Repeat testing and Rechecks• Smoker – Non Smoker • Saliva vs. Urine• Travel issue• Life style issue• Medical reconsideration• Medical Underwriting Appeals• Clinical medicine vs Insurance Underwriting• Privacy Issue

UnderwritingUnderwriting

Most common inquiryNon Resident?

• A Canadian Citizen living outside of Canada?• Needs to have a Canadian Residence Status

– Paying Canadian Income Tax (T4)– Residing in Canada for 183 consecutives days.

UnderwritingUnderwritingMost common inquiry

New immigrants (Life vs. CI)

• Canadian Resident Status• Paramedical• Blood test including Hep. B & C• Financial Quest.• Need to have landed status• Covering letter explaining the purpose of

insurance and explanation of the source of the deposits.– Only Canadian assets will be considered.

UnderwritingUnderwriting

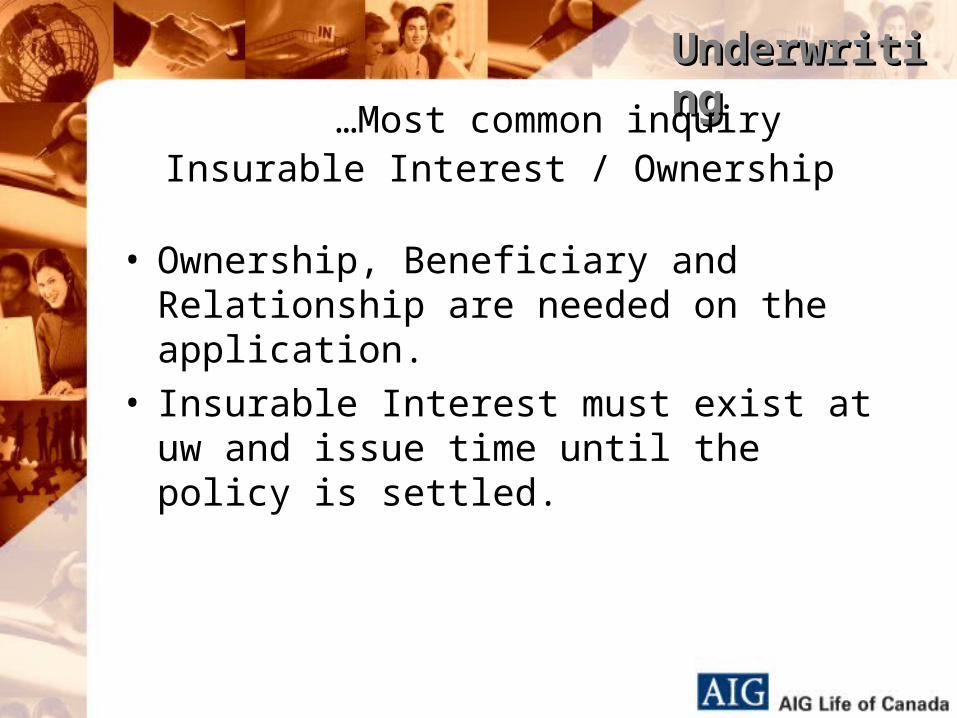

…Most common inquiryInsurable Interest / Ownership

• Ownership, Beneficiary and Relationship are needed on the application.

• Insurable Interest must exist at uw and issue time until the policy is settled.

UnderwritingUnderwriting

Financial underwriting Why?

• Establishes need• Reduces anti-selection• Reduces moral hazard• Reduces speculation

UnderwritingUnderwriting

Insurable Interest / Why ?

• Must be determined at the time of underwriting• Purpose of the insurance?• What is the financial loss if the insured dies?• Does the amount make sense?

UnderwritingUnderwriting

How? / Communication is the key

• Communication between underwriter & broker & administrator

• Communication between underwriter & reinsurer

• Was FQ completed giving income and NW?

• Financial or medical explanation

– What are we trying to accomplish or achieve

– What are you looking for?

– Was the case shop elsewhere?

UnderwritingUnderwriting

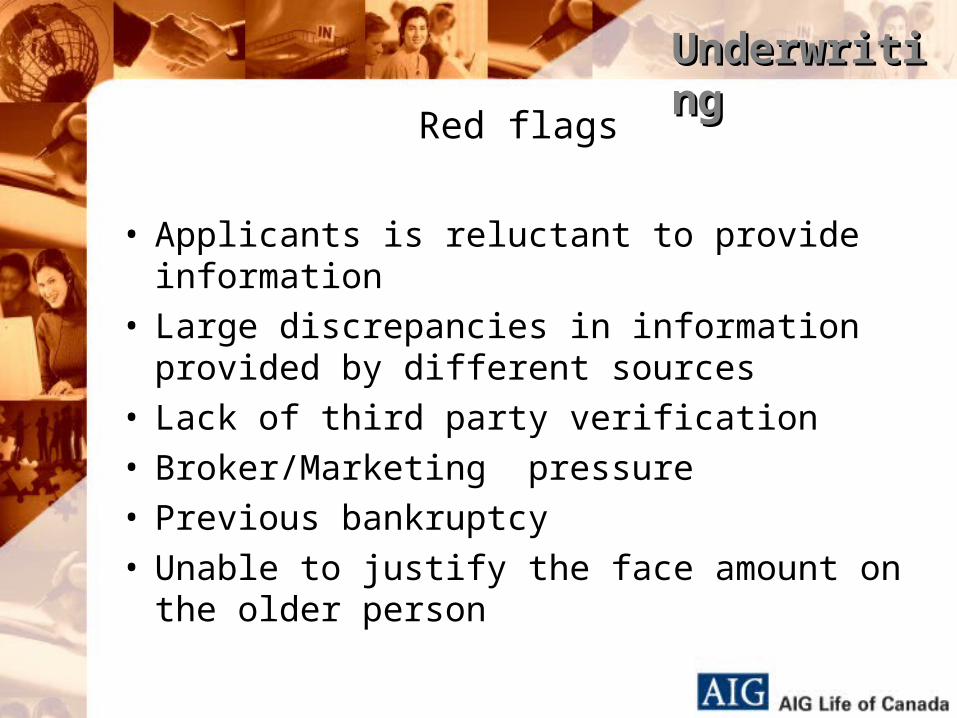

Red flags

• Applicants is reluctant to provide information• Large discrepancies in information provided by

different sources• Lack of third party verification• Broker/Marketing pressure• Previous bankruptcy• Unable to justify the face amount on the older

person

UnderwritingUnderwriting

How do we make it happen !

• Reinsurer is taking majority of the risk• 3 way relationship• Set expectations• Communication is the key!• Presenting your case.

UnderwritingUnderwritingYour best tool?

To accelerate the U/W process!• Did the producer provide a covering

letter explaining the following: – the purpose of the insurance – How was the amount

determined?– Where is the deposit coming

from?– Explaining the concept use– Was sales presentation made if

yes is it attached to the application.

• Is the client aware of all requirements needed.

• Was a NB cover sheet submitted?• Was the case sent to other carrier?• What are we trying to achieve

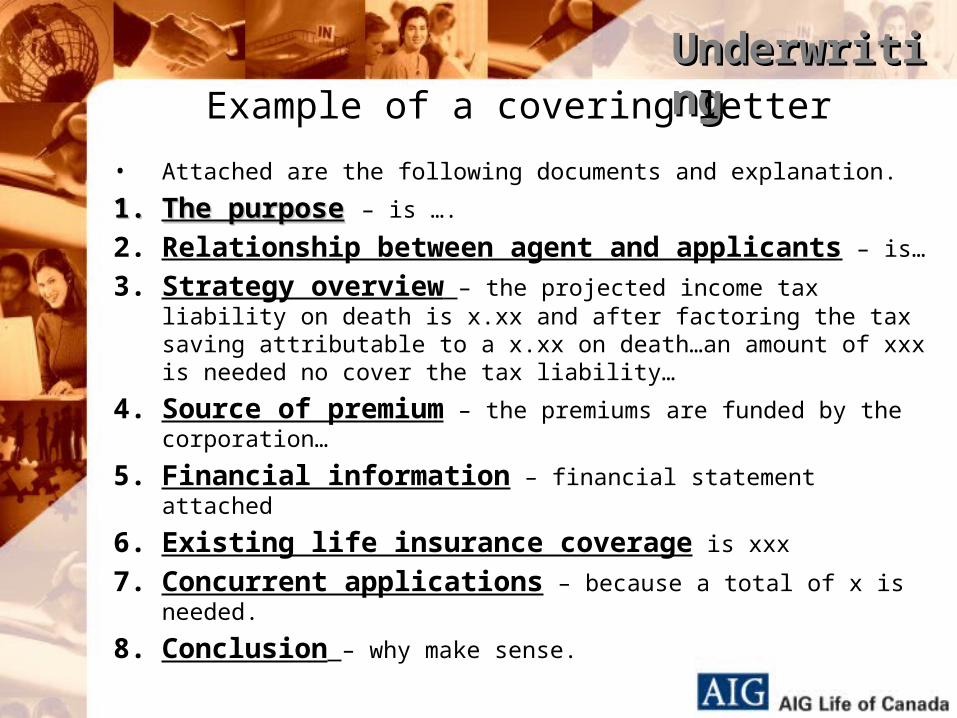

UnderwritingUnderwritingExample of a covering letter

• Attached are the following documents and explanation.

1.1. The purposeThe purpose – is ….

2. Relationship between agent and applicants – is…

3. Strategy overview – the projected income tax liability on death is x.xx and after factoring the tax saving attributable to a x.xx on death…an amount of xxx is needed no cover the tax liability…

4. Source of premium – the premiums are funded by the corporation…

5. Financial information – financial statement attached

6. Existing life insurance coverage is xxx

7. Concurrent applications – because a total of x is needed.

8. Conclusion – why make sense.

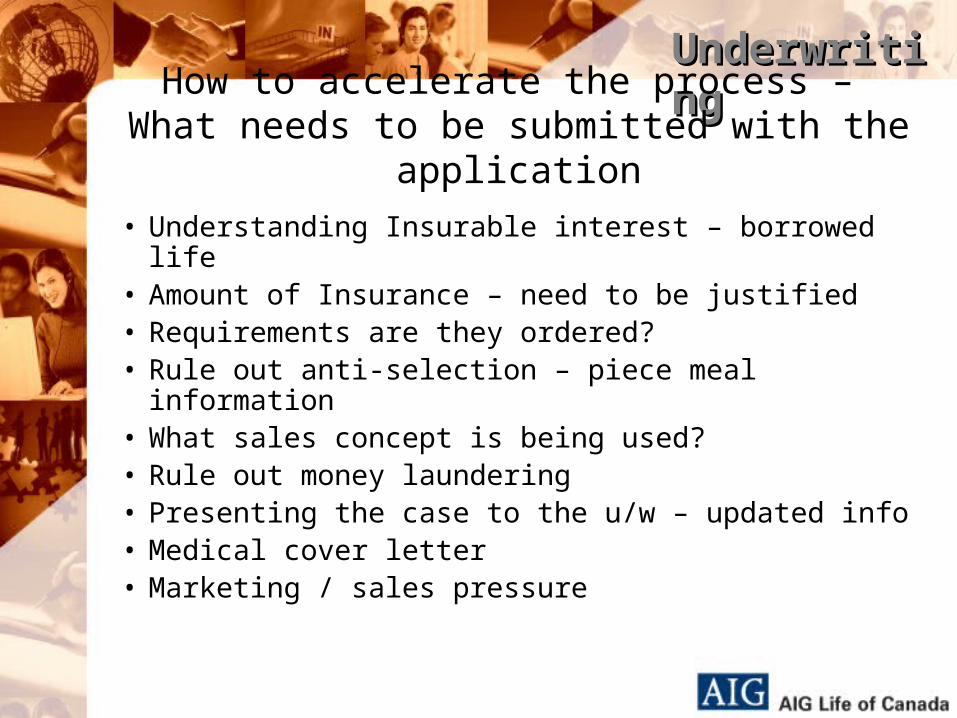

UnderwritingUnderwritingHow to accelerate the process –

What needs to be submitted with the application

• Understanding Insurable interest – borrowed life• Amount of Insurance – need to be justified• Requirements are they ordered?• Rule out anti-selection – piece meal information• What sales concept is being used?• Rule out money laundering• Presenting the case to the u/w – updated info• Medical cover letter• Marketing / sales pressure

UnderwritingUnderwriting

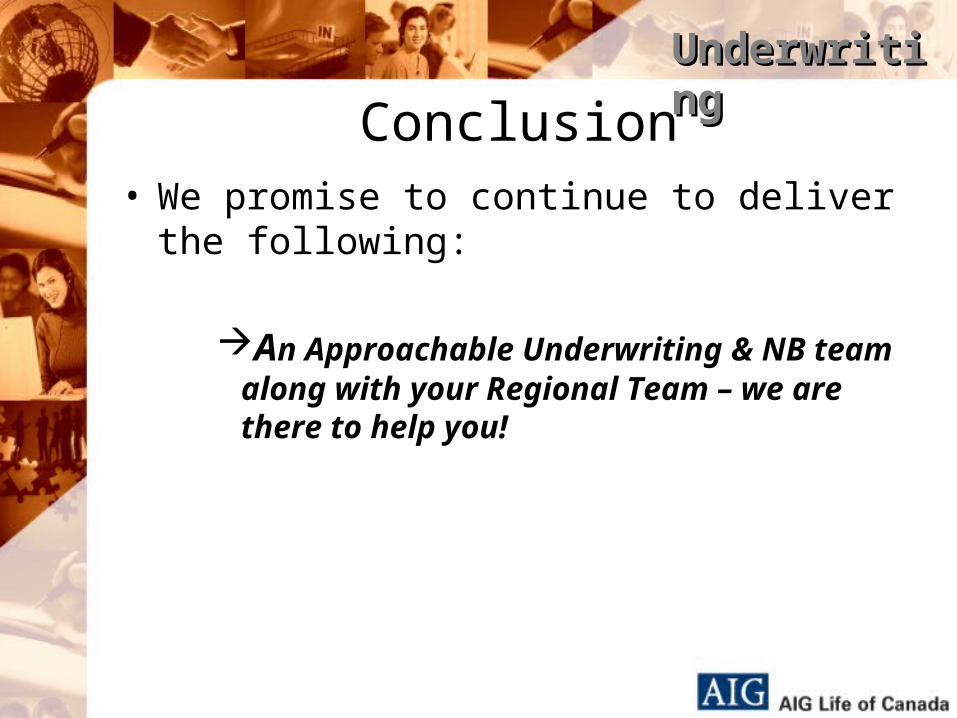

Conclusion• We promise to continue to deliver the following:

An Approachable Underwriting & NB team along with your Regional Team – we are there to help you!

UnderwritingUnderwriting

Questions?

• Thank you for your business!