unclaimed property: what you need to know ~ part 1creditcongress.nacm.org/pdfs/handouts/25084... ·...

TRANSCRIPT

Unclaimed Property: What

You Need to Know

~ Part 1 ~

Heela Popal & Troy Wangen

June 15, 2016

2:00p – 3:00p

25084

Legal Disclaimer

This presentation does not constitute legal, financial, accounting or any other type of advice. It is provided solely for educational and informational purposes for the attendees of this webinar which is

sponsored by UPPO. Attendees are urged to consult with their own attorneys and other advisors about their particular facts and circumstances. The analysis and opinions expressed herein are those of the

presenters and do not necessarily represent the views of their employers, the Unclaimed Property Professionals Organization, or its officers, directors or members.

Anti-Trust Statement UPPO members and/or meeting attendees cannot come to understandings, make agreements, or

otherwise concur on positions or activities that in any way tend to raise, lower or stabilize prices or fees. Members and/or attendees can discuss pricing models, methods, systems, and applications, as well as

certain cost matters that do not lead to an agreement or consensus on prices or fees to be charged. However, there can be no discussion as to what constitutes a reasonable, fair or appropriate price or fee

to charge for any service or product. Information may be presented with regard to historical pricing activities so long as such information is general in nature and does not include data on current prices or fees being charged in any trade area. Any discussion of current or future prices, fees, discounting, and

other terms and conditions of sale, which may lead to an agreement or consensus on prices or fees to be charged, is strictly prohibited. Any questions about UPPO’s antitrust policy should be directed to UPPO’s

Executive Director.

• Unclaimed Property Overview

• Common Terms

• Property Types

• Jurisdictional Priority Rules

• Reporting Requirements

• Recent Trends in Enforcement, Reform & Legislation

Today’s Agenda

Unclaimed Property Overview

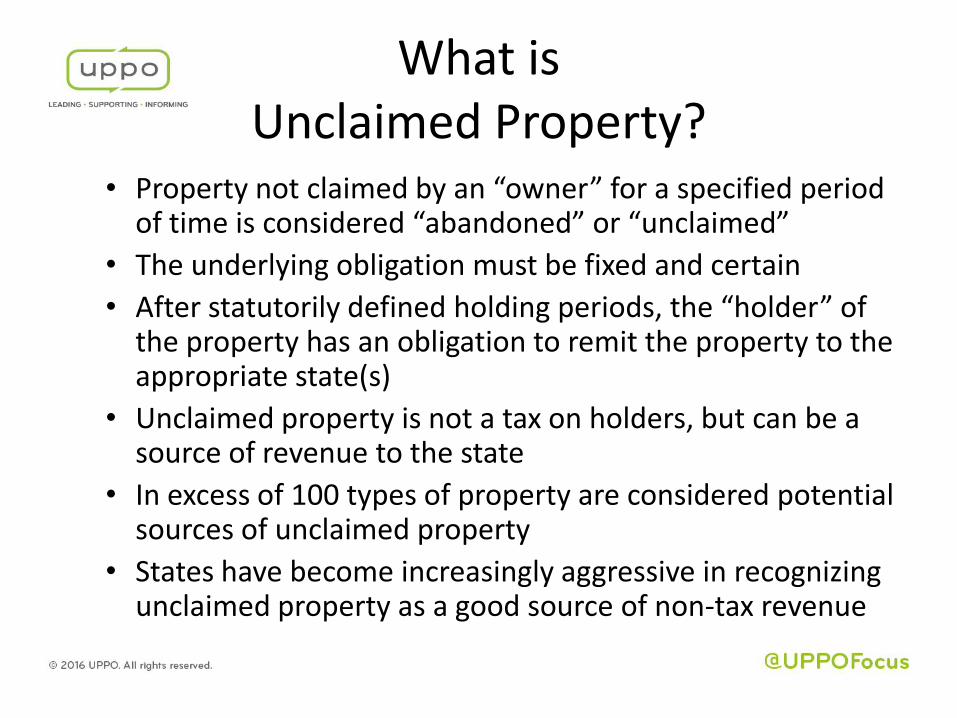

• Property not claimed by an “owner” for a specified period of time is considered “abandoned” or “unclaimed”

• The underlying obligation must be fixed and certain

• After statutorily defined holding periods, the “holder” of the property has an obligation to remit the property to the appropriate state(s)

• Unclaimed property is not a tax on holders, but can be a source of revenue to the state

• In excess of 100 types of property are considered potential sources of unclaimed property

• States have become increasingly aggressive in recognizing unclaimed property as a good source of non-tax revenue

What is Unclaimed Property?

• To protect the interests and property rights of a lost owner

• Relieve the holders from the expense and liability associated with holding and tracking the property

• Ensure the economic windfalls from unclaimed property benefit the public, not an individual owner

Purpose of Unclaimed Property Laws

• Derivative Rights Doctrine – The state’s rights are “derivative” in nature. This is commonly referred to as “the state standing in the shoe of the owner.”

• Nexus does not apply, i.e., a physical presence is not required for reporting.

• The majority of states do not provide relief for reach-back based on a “statute of limitations.” • Where “statute of limitations” provisions exist, the limitation

period is typically longer than that applicable in taxation.

• Failure to report or the filing of a fraudulent report generally eliminates reach-back relief afforded by limitation provisions.

• Few states provide for a traditional administrative appeals process/remedy.

It’ Not a Tax

• The US Supreme Court has created federal common law rules which determine when a state has the right and jurisdiction to claim unclaimed property. Once it has been determined under these rules that a state has the right to claim a particular type of property, that state’s laws then apply to determine if and when the property is reportable.

• Many states have modeled their statutes after one of the Uniform Acts adopted by the National Conference of Commissioners on Uniform State Laws (NCCUSL) in 1954, 1966, 1981, and 1995. • NCCUSL’s goal is to promote fair and adequate treatment among the

states and provide uniform laws for the benefit of multistate businesses. • One of the Uniform Acts has been adopted at least in part by all but six

states (DE, KY, MA, NY, OH, TX). • The current Uniform Act is in the process of being rewritten and the final

draft is scheduled to be released in Summer 2016.

Governing Laws

• States only take custody of unclaimed property, not title.

• Uniform priority rules.

• Criteria for a presumption of abandonment.

• Requires a minimum effort to locate owner.

• Annual reporting and remittance requirements.

• Record retention rules.

• Interest and penalties for noncompliance.

Elements of the Uniform Acts

Common Terms

• Unclaimed Property – Liabilities held by one person, but owed to another; interchangeable with abandoned property.

• Escheat Property – Technically refers to property where title is taken by the state when a person dies intestate and without heirs; in practice, interchangeable with abandoned or unclaimed property.

• Dormancy Period – Period of time property remains inactive before it is presumed abandoned.

• Holder – Person in possession of property. • Owner – Individual entitled to the property. • Due Diligence – Process whereby the holder must contact

owner prior to remitting property to the state.

Common Terms

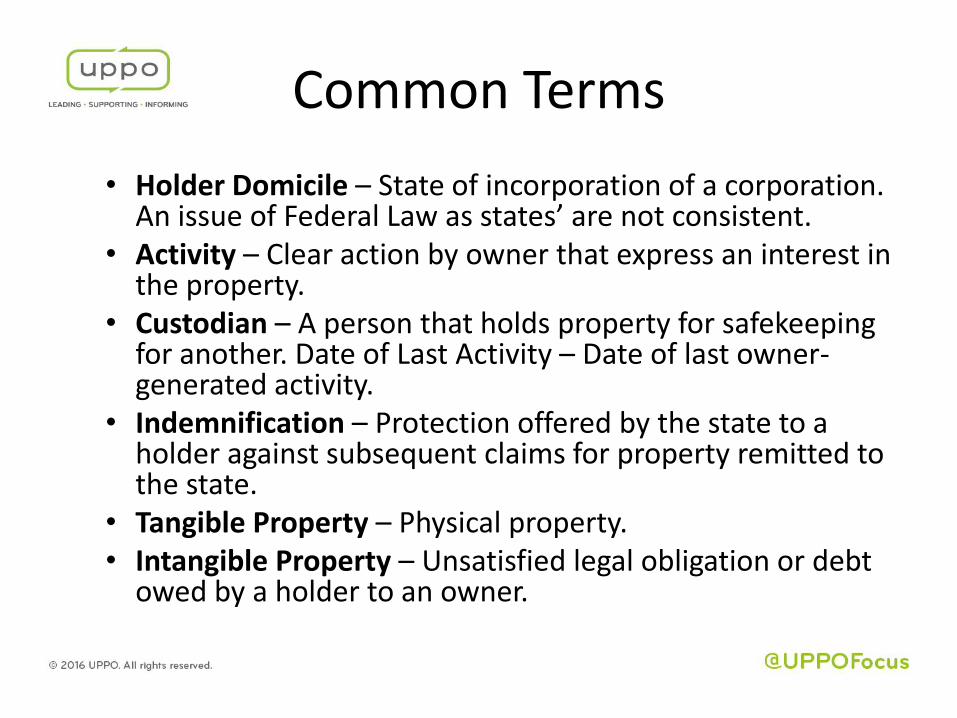

• Holder Domicile – State of incorporation of a corporation. An issue of Federal Law as states’ are not consistent.

• Activity – Clear action by owner that express an interest in the property.

• Custodian – A person that holds property for safekeeping for another. Date of Last Activity – Date of last owner-generated activity.

• Indemnification – Protection offered by the state to a holder against subsequent claims for property remitted to the state.

• Tangible Property – Physical property. • Intangible Property – Unsatisfied legal obligation or debt

owed by a holder to an owner.

Common Terms

Property Types

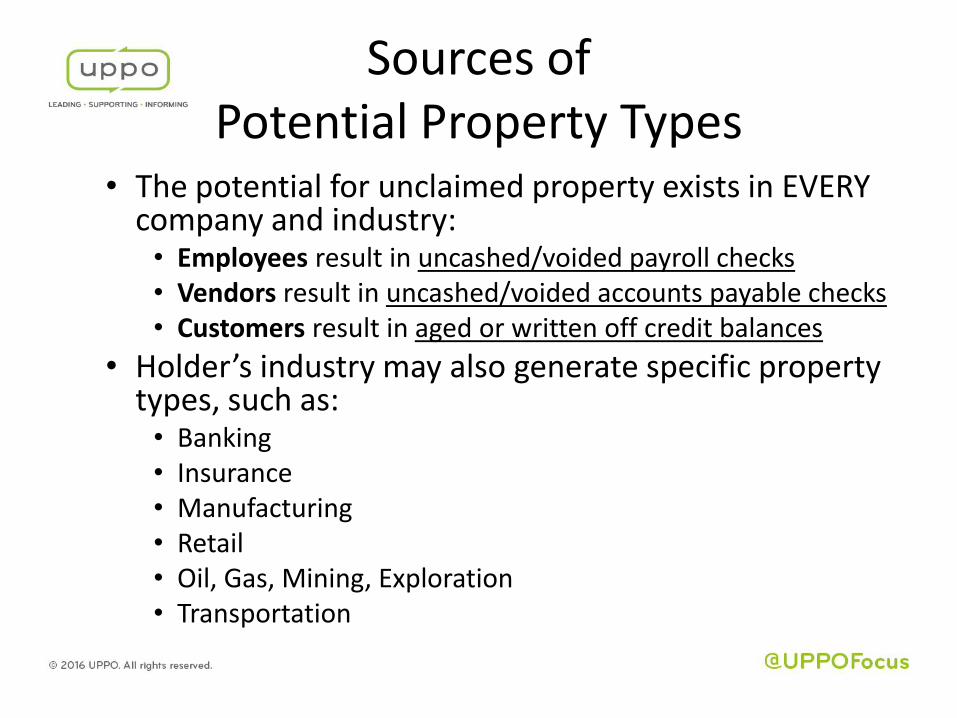

• The potential for unclaimed property exists in EVERY company and industry: • Employees result in uncashed/voided payroll checks • Vendors result in uncashed/voided accounts payable checks • Customers result in aged or written off credit balances

• Holder’s industry may also generate specific property types, such as: • Banking • Insurance • Manufacturing • Retail • Oil, Gas, Mining, Exploration • Transportation

Sources of Potential Property Types

Common Property Types

• Payroll

• Credit Balances

• Deposits

• Interest & Dividends

• Self-Insured Benefits

• Dormant Bank Accounts

• Royalties

• Mineral Interests

• Accounts Payable

• Overpayments

• Customer Refunds

• Unidentified Remittance

• Layaways

• Gift Cards/Certificates

• Merchandise Credits

• Stock/Underlying Shares

Jurisdictional Priority Rules

• First Priority: State of Owner’s last known address as shown on the Holder’s books and records

• Second Priority: If no Owner address on the Holder’s books and records, or if the state of the Owner’s last known address does not have applicable unclaimed property statute, then the Holder’s state of incorporation may claim the property

• Third Priority: Holder’s state of incorporation or domicile if address of Owner is in a foreign country and Holder is incorporated or domiciled in the US

• Throwback Rule: In the event the jurisdiction of the Owner’s last known address does not escheat the property, then the state of incorporation may claim the property

Texas v. New Jersey (1965)

Reporting Requirements

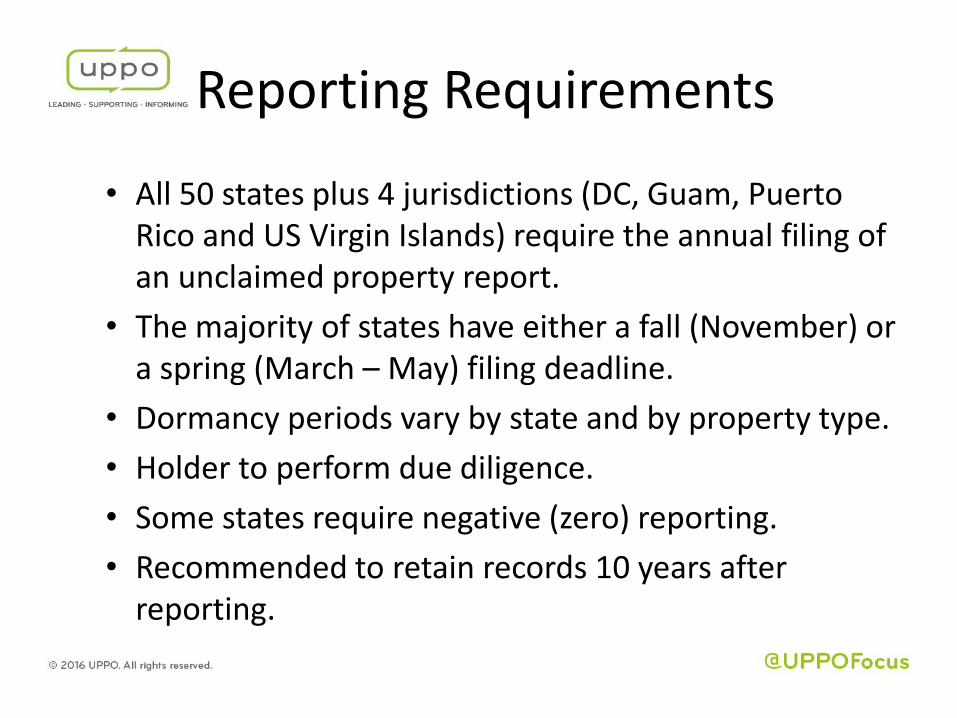

• All 50 states plus 4 jurisdictions (DC, Guam, Puerto Rico and US Virgin Islands) require the annual filing of an unclaimed property report.

• The majority of states have either a fall (November) or a spring (March – May) filing deadline.

• Dormancy periods vary by state and by property type.

• Holder to perform due diligence.

• Some states require negative (zero) reporting.

• Recommended to retain records 10 years after reporting.

Reporting Requirements

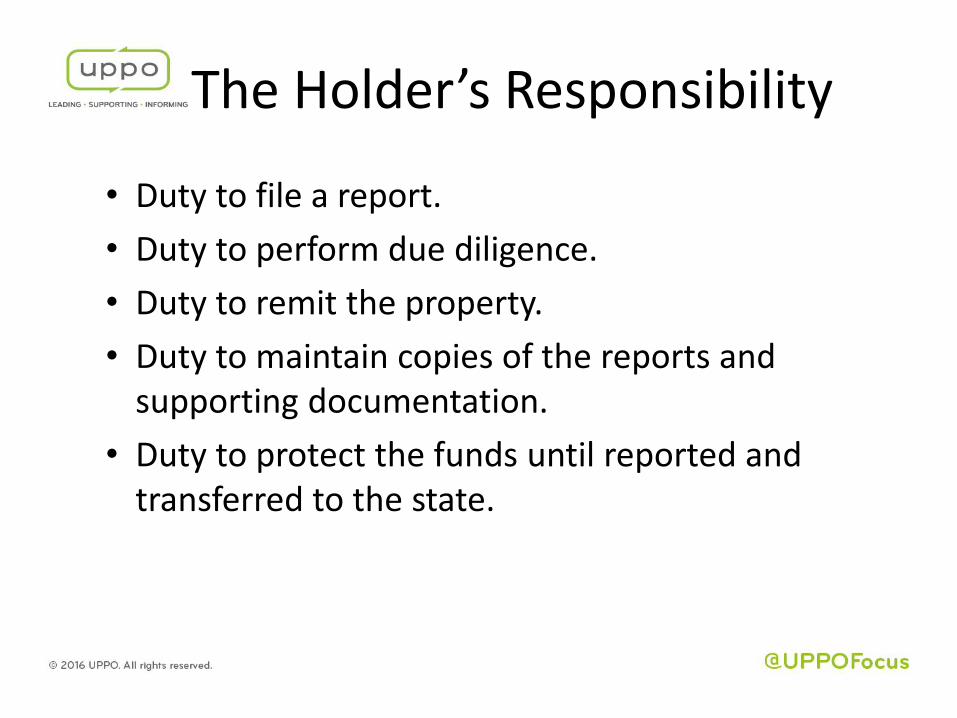

• Duty to file a report.

• Duty to perform due diligence.

• Duty to remit the property.

• Duty to maintain copies of the reports and supporting documentation.

• Duty to protect the funds until reported and transferred to the state.

The Holder’s Responsibility

• Release and indemnify the Holder from liability

• Secure the funds in a custodial capacity

• Make efforts to locate the Owners

• Pay claims in a timely manner

The States’ Responsibility

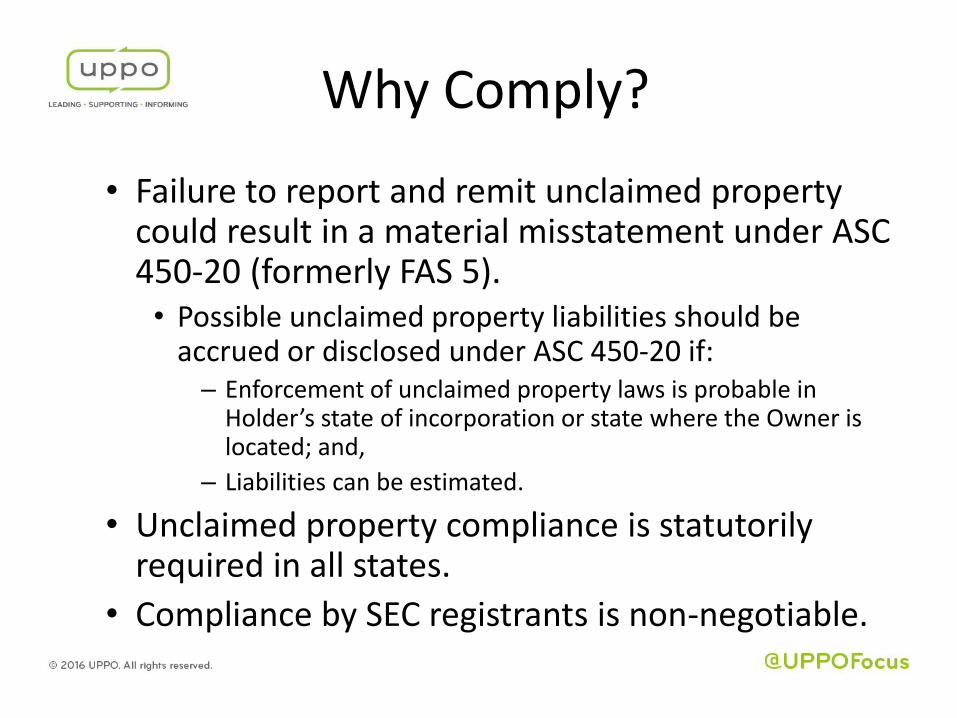

• Failure to report and remit unclaimed property could result in a material misstatement under ASC 450-20 (formerly FAS 5). • Possible unclaimed property liabilities should be

accrued or disclosed under ASC 450-20 if: – Enforcement of unclaimed property laws is probable in

Holder’s state of incorporation or state where the Owner is located; and,

– Liabilities can be estimated.

• Unclaimed property compliance is statutorily required in all states.

• Compliance by SEC registrants is non-negotiable.

Why Comply?

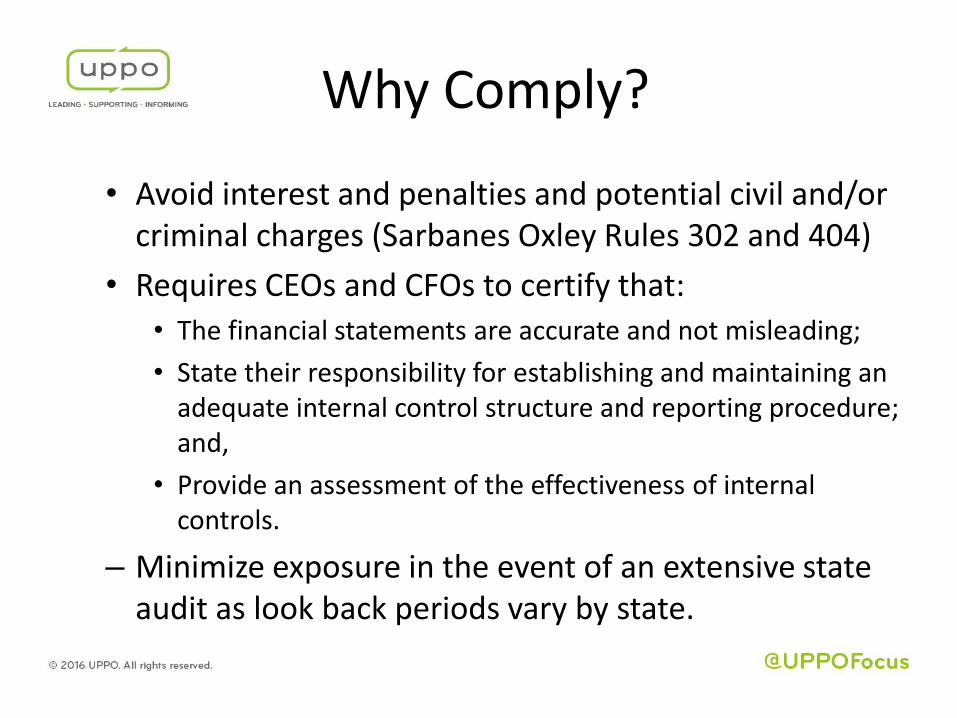

• Avoid interest and penalties and potential civil and/or criminal charges (Sarbanes Oxley Rules 302 and 404)

• Requires CEOs and CFOs to certify that:

• The financial statements are accurate and not misleading;

• State their responsibility for establishing and maintaining an adequate internal control structure and reporting procedure; and,

• Provide an assessment of the effectiveness of internal controls.

– Minimize exposure in the event of an extensive state audit as look back periods vary by state.

Why Comply?

Recent Trends in Enforcement, Reform and Legislation

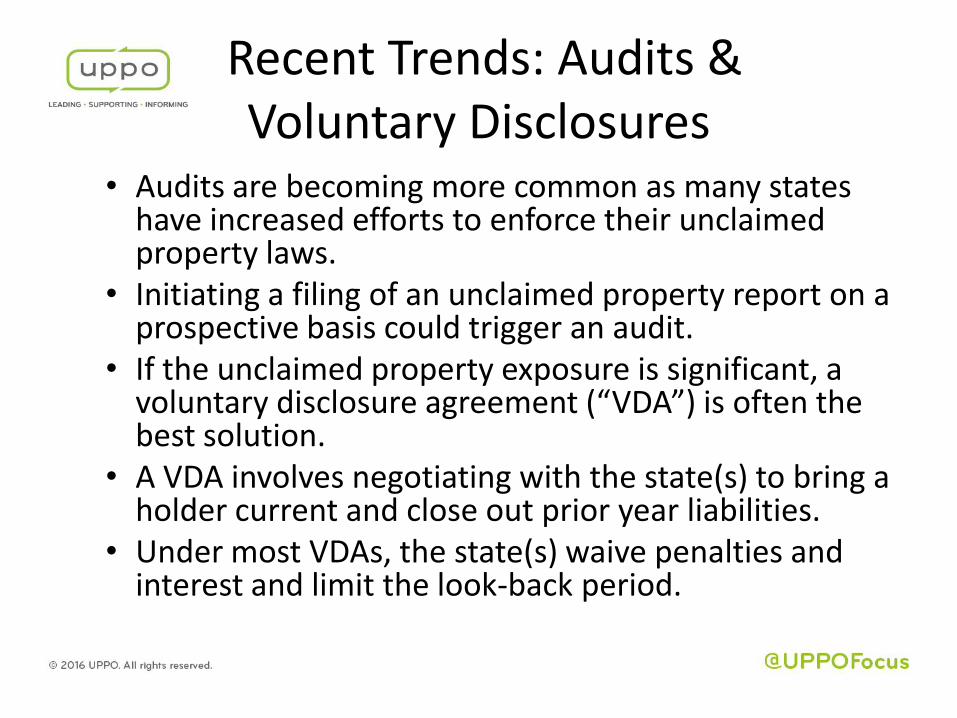

• Audits are becoming more common as many states have increased efforts to enforce their unclaimed property laws.

• Initiating a filing of an unclaimed property report on a prospective basis could trigger an audit.

• If the unclaimed property exposure is significant, a voluntary disclosure agreement (“VDA”) is often the best solution.

• A VDA involves negotiating with the state(s) to bring a holder current and close out prior year liabilities.

• Under most VDAs, the state(s) waive penalties and interest and limit the look-back period.

Recent Trends: Audits & Voluntary Disclosures

• No filing history in state of incorporation or where Holder has a large presence

• Filing tax returns but not filing unclaimed property reports

• Unusually large or small remittances relative to size of company or past reports

• Established company filing for the first time without past due property

• Merger & Acquisition activity

Recent Trends: Common Audit Triggers

• Previous versions of the UUPA: 1954, 1966, 1981, 1995 (current)

• ULC agreed to create the UUPA drafting committee in 2013. Since that time the drafting committee has met five times with the most recent meeting held in February 2016.

• ULC drafting committee’s UUPA completion goal is summer 2016.

• ULC meeting scheduled July 8-14 in Vermont for the final reading • Late 2016 – Early 2017: If approved by ULC, UUPA to be submitted

to ABA House of Delegates for vote

• 2017 and Later: If approved, UUPA is officially promulgated for consideration by the states

Recent Trends: Uniform Law Commission

• Delaware Senate Bill 141 • Division of Revenue no longer has the authority to

unilaterally select holders for audit

• Holders must receive an express written invitation to enter Delaware’s Voluntary Disclosure program

• If Holder declines to participate or does not reply within 60 days, Holder will be referred to the Division of Revenue for potential unclaimed property audit

• Reduced reach-back period and beginning January 1, 2017, will begin a rolling 22-year reach back period

• Reinstates the ability to assess interest on past due property and audit assessments

Recent Trends: Delaware Legislation

• Temple Inland v. Cook • Current case in Delaware challenging Delaware’s audit

methodology, specifically estimations

• National Freight, Inc. v. Sidamon-Eristoff • Current case in New Jersey challenging AR B2B property and

federal preemption

• Michigan • New law created holder friendly audit process for companies

with a large presence in the state

• Nevada • Currently does not accept consolidated reports; UPPO

working with state to try to rectify their limitations

Recent Trends: Notes of Interest

Questions and

Answers

Contacts

Heela Popal

2016-17 UPPO President

Director, State and Local Tax

PricewaterhouseCoopers LLP

Phone: 678.419.1462

Troy Wangen

2016-17 UPPO Midwest Region Vice President

Senior Manager

True Partners Consulting LLC

Phone: 312.588.3430