unbundling of costs within post trade

TRANSCRIPT

Rob Scott | 2nd Post Trade Forum & Trade Show | Sep 2015

“Redefining Models & Understanding Competitive Advantage”

Unbundling of costs within Post Trade

1 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

1 Industry Backdrop

2 Leading Independent Research & Conclusions

3 Business Backdrop – Capital Markets

4 Collaboration & Partnership

Contents

2 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

1 Industry Backdrop

2 Leading Independent Research & Conclusions

3 Business Backdrop – Capital Markets

4 Collaboration & Partnership

Converging Factors

Impact of regulatory & Market Forces

Contents

3 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Front Office View

The market is developing at a

rapid pace. The ability to

recognise your differentiation

and adapt quickly in the cost

profile is becoming both crucial

and critical

This has led to banks’ interests

converging, especially in the

need to rationalise aspects of

business both front and back

which help to ensure cost

savings through the whole

value chain

Market conditions are forcing

banks to redefine their models

and exit unprofitable business

lines. No longer wil banks be

all things to all men, in all

markets and products.

Increased

Regulation

Technology

evolution and

dependencies

Investor

demand Reduced

leverage

Increased

transparency and

interconnected-

ness

Convergence of

bank value chains

(execution &

post trade)

Convergence Factors in the Market

Emergence

of new risks Emergence of

disruptive

technologies

4 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Impact of Market & Regulatory Forces on the Industry

The impact on the industry

provides much to think about

for C&M

Many assumptions built into

current planning should be re-

visited to ascertain whether

they remain valid or need to be

reassessed

Given volume is not materially

increasing. Margin

compression and competition

remain constant. The need to

tackle the cost base is the

primary focus of C&M business

lines. Industry trends towards

25-40% overall reduction

Capital, liquidity and Balance

sheet usage is forcing banks to

review their business models.

Demand for products &

services, generating new

revenues Shift of existing revenue-

generating activities

between participants

Cost reduction efforts

creating revenues for

insourced solution

providers

Increased price

transparency on liquid

instruments

Unbundling of services

like research from

execution / brokerage

Burdensome capital &

funding requirements on

illiquid instruments

Likely growth of agency

models as market-makers

withdraw capacity

Increase in cleared

volumes, and clients

interacting directly with

CCPs, not via clearers IM requirements >$1tn

by 2018; collateral

management critical Unlocking of dormant

assets held by institutions

& more demand for tri-

party repo Core custody moves to

utility model; revenues

from trade reporting &

provision of BO services

5 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

1 Industry Backdrop

2 Leading Independent Research & Conclusions

3 Business Backdrop – Capital Markets

4 Collaboration & Partnership

Macro Backdrop research papers

Moving up the value chain

Contents

6 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

External References

References Key relevant findings Found in

McKinsey&

Company

ROE for Core Capital Market Businesses decreases from 20% Pre-

regulation to 7% Post-regulation, but increases to 11-12% Post-Mitigation

McKinsey& Company [2014] in

“Global Corporate and Investment Banking: An

Agenda for a Change” (p. 15)

Oliver Wyman Firms re-aligning business models

Securities Ecosystem in 2013 circa $330bn, $70bn post trading

Pressure on profitability

Capital, Balance-Sheet, liquidity and collateral constraints

Greater transparency

Conduct scrutiny

The Capital Markets Industry

“The Times they are a-changin’”

http://www.oliverwyman.com/content/dam/oliver-

wyman/global/en/files/insights/financial-

services/2015/March/The_Capital_Markets_Indu

stry.pdf

Boston

Consulting

Group (BCG)

ROE in the CMIB industry fell to 11 percent in 2013, a decline of 1

percentage point from the previous year

The industry ROE has not returned to its precrisis levels, and the range of

ROE outcomes for individual institutions has widened

Transaction Banking 2013 revenues of $1trn ($750bn retail, $260bn

wholesale) to double by 2023

Emerging markets to account for 75% of revenues

Boston Consulting Group (BCG) [2014] in

“Global Capital Markets 2014: The Quest for

Revenue Growth” via:

https://www.bcgperspectives.com/content/article

s/financial_institutions_corporate_strategy_portf

olio_management_global_capital_markets_2014

_quest_revenue_growth/?chapter=2

Boston Consulting Group (BCG) [2014] in “What

lies ahead in Transaction Banking? Insights

from the Boston Consulting Group (BCG)”

Pricewaterhouse

Coopers (PWC)

A bank’s share typically trades at 6 to 8 times earnings. In contrast the price-

to-earnings ratio of a processing business is usually more than 20 times.

PricewaterhouseCoopers (PWC) [2009] in

“Transaction banking takes off“ (p. 5)

7 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

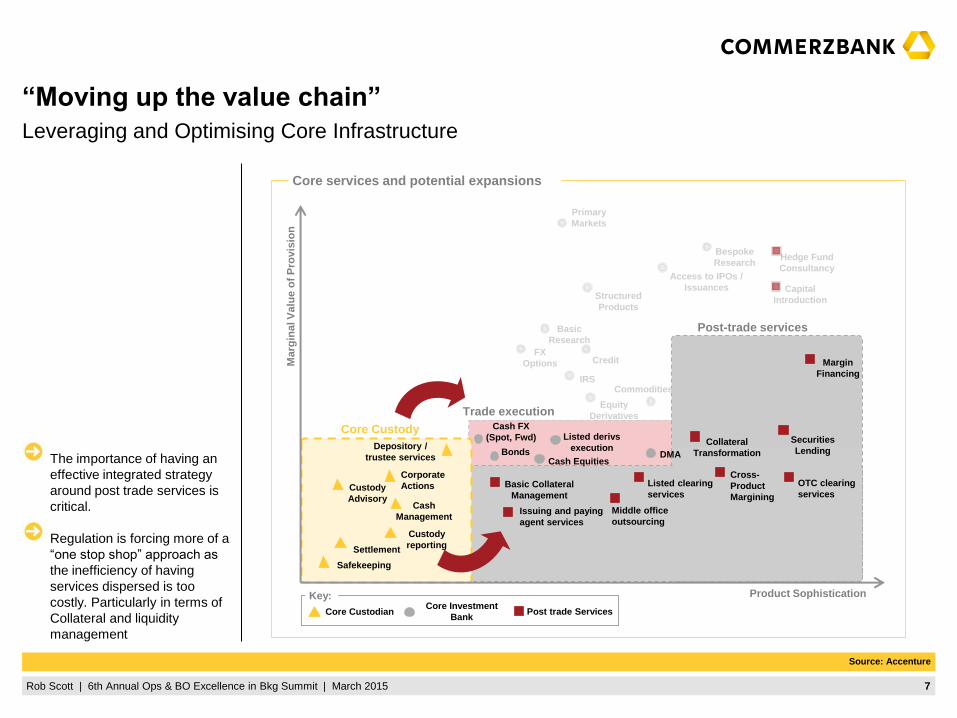

“Moving up the value chain”

Leveraging and Optimising Core Infrastructure

The importance of having an

effective integrated strategy

around post trade services is

critical.

Regulation is forcing more of a

“one stop shop” approach as

the inefficiency of having

services dispersed is too

costly. Particularly in terms of

Collateral and liquidity

management

Trade execution

Basic

Research

Post trade Services Core Investment

Bank Core Custodian

Key:

Safekeeping

Settlement

Cash

Management

Bespoke

Research

Primary

Markets

Access to IPOs /

Issuances

Hedge Fund

Consultancy

Marg

ina

l V

alu

e o

f P

rovis

ion

Capital

Introduction

Core services and potential expansions

Core Custody

Corporate

Actions

Custody

reporting

Custody

Advisory

IRS Commodities

Credit FX

Options

Equity

Derivatives

Structured

Products

Post-trade services

Depository /

trustee services

Margin

Financing

Cash FX

(Spot, Fwd)

Cash Equities

Basic Collateral

Management

Middle office

outsourcing

Bonds

Listed derivs

execution

Product Sophistication

Cross-

Product

Margining

OTC clearing

services

Issuing and paying

agent services

DMA

Listed clearing

services

Securities

Lending Collateral

Transformation

Source: Accenture

8 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

1 Industry Backdrop

2 Leading Independent Research & Conclusions

3 Business Backdrop

4 Collaboration & Partnership

Macro Business summary

Emergence of Credible Providers & Alternatives

Contents

Market & Competitor Landscape Redefinition

9 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Macro Business Consideration Summary

High Cost Income Ratios

Innovation and Change the Bank budgets challenged

Partnership, Collaboration, Cooperation agreements for success

Declining volumes, continued margin compression

Cost arbitrage of off-shoring exists but largely exploited

Aged Technologies

Inefficient process

Continued regulatory and market change

High fixed costs. Need to move to variable cost models

Chalenged business models

Need for less proprietary

thinking

Fundamental need to drive

costs and inefficiency out of

process

Consider combining or

partnering resource for

success. Ops/IT/Front Office

10 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Macro Business Considerations

Entrance of non bank firms

with substantial capital

resource

Non business competitive

entrants

Outsourcing prevalent for next

5 years

Importance of Partnerships,

Collaborations, Cooperation

agreements by smaller players

to pool scale

Accenture

WIPRO

IBM

TCS -Bancs

Euroclear

Markit – KYC utility

Goldman Sachs – Colin

(Bilateral Collateral) Clearstream – Alfred

(Bilateral Collateral)

Bank Consortium – (Static

data)

DTCC – (Static Data)

CAPCO - FIS

Emergence of credible service providers to manage the cost challenge

11 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Market & Competitor Landscape Redefining

During 2014, larger

competitors have tried to

create similar Market Services

businesses by combining a

wider range of services

Custody is often still separate

More competitors have brought

their OTC, ETD and FXPB

businesses together

Agency Derivative Service

(FXPB, ETD, OTC CCP)

Full post trade solution for

platinum clients only

ECLIPSE (Execution, Clearing,

Liquidity & Portfolio Services) Agency Derivative Service

(FXPB, ETD, OTC CCP)

Full post trade solution for

platinum clients only

Combined OTC & ETD

Investor Services, inc:

ACCE (Agency Clearing,

Collateral Mgt & Execution)

Custody & Fund Services

Financing & PB (HF focus)

Sales

Combined Custody, prime

finance, sec lending, fund

services, ETD & OTC

Exited FX PB

New FXPB players

Collateral & Custody combined

Exited Clearing due to reg. delays

Frozen FX PB

ABN derivatives clearing combined

with NT Custody & Collateral

Service Provider Overview

Recent Market Developments

DB tie up with HP

DTCC-Euroclear

Global Colleteral Ltd

Goldman Sachs utility

for BiLateral Collateral

Barclays outsource

ETD to Sungard

Markit KYC Utility

Imminent

utility/outsourced

annoncments

Banks & OpenGamma

Bilateral Collateral

Outsourcing USD

82.9bn 2013

12 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Contents

1 Industry Backdrop

2 Leading Independent Research & Conclusions

3 Business Backdrop – Capital Markets

4 Collaboration & Partnership

Old/New Technologies : Key to Success/Path Forward

Ops & Technology Central to Success

Outsourcing considerations

Path for success

13 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Old Technologies 25 years ago

Core Securities platforms 19-

25_years old

High dependency on manual

processing

Inefficiency in processes and

internal connectivity

14 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

New Technologies

Need for newer, scalable

technologies

Technology the driver and

differentiator of the future

Need for further automation of

processes and increased user

experience

15 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Old Mobile Technologies

16 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

This is mobile technology today

We live in a digital age. Speed

efficiency, information and

transparency drivers of

success

Most modern day phones today

can perform more processing

than the computers 25 years

ago

We need to adapt and have

ability to be nimble in execution

17 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Working in true partnership and collaboration. Business & Support groups

Client service models likely to change as more products are integrated together

more as business units redefine themselves

Clear delineation of roles and responsibilities ie, Collateral Mgt

Making client central to how we measure success

Timely response to changing support models. Being nimble and effective in

both our adaptability to change and nimble in our investments

Operations and technology central to success

Considerations

The need to continually challenge ourselves. Automate, proactivity. Willingness

to adapt

Quick identification and acceptance of key differentiation

Ability to move fixed cost into Variable cost models

18 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

Multi platform, Multi operating system support

Pre-Define services and how delivered

Pro-active monitoring and alerting tools

Implementation of latest industry standards and practices

Effective service level management and defined liability regime

Outsourcing Top 10 Considerations

Benefits

Regular and effective management meetings

Skilled Technical staff

Strategic partnerships

Comprehensive Documentation

Achieving significant ROI

19 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

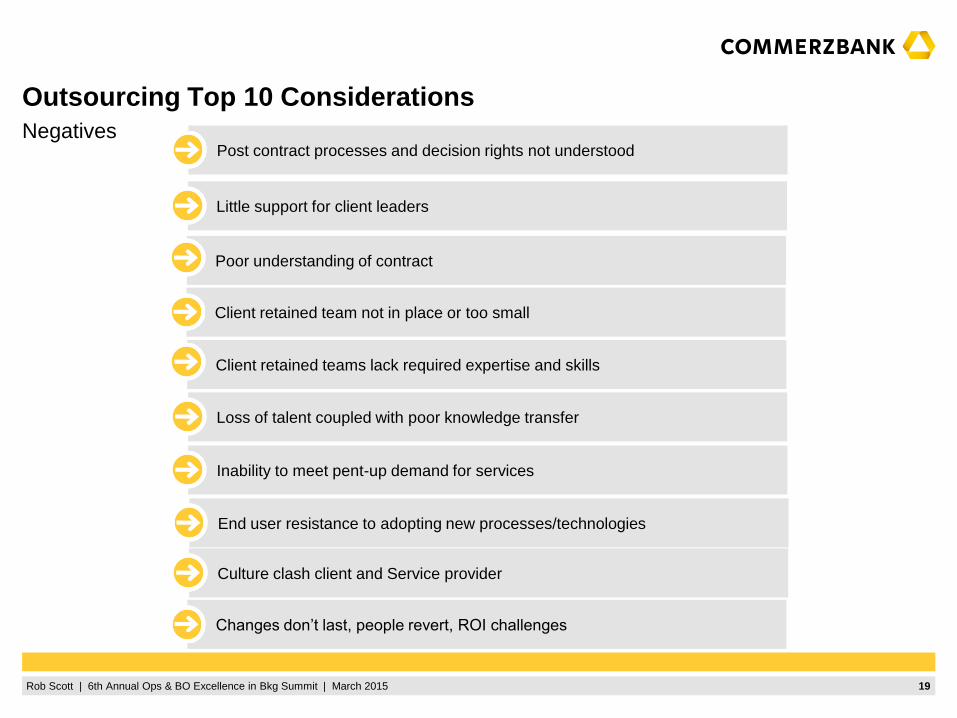

Little support for client leaders

Poor understanding of contract

Client retained team not in place or too small

Client retained teams lack required expertise and skills

Loss of talent coupled with poor knowledge transfer

Outsourcing Top 10 Considerations

Negatives

Inability to meet pent-up demand for services

Post contract processes and decision rights not understood

End user resistance to adopting new processes/technologies

Culture clash client and Service provider

Changes don’t last, people revert, ROI challenges

20 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

In other words

Understanding differentiation,

not delaying redefining cost

base

Ensuring outsourcing is a true

partnership that lives and

evolves over time

Be wary of retaining suitable

experience, expertise and

watch morale

By adopting latest technology

and process, business and

client service can be

transformed.

Timeline

Continuity Liability /penalty

regime Relationship client

and provider

Process familiarity

What is the real

cost

Be careful to understand…………

Morale prioritisiation

Control

21 Rob Scott | 6th Annual Ops & BO Excellence in Bkg Summit | March 2015

The Path Forward

How Post Trade will become a “Business As Usual”, integral part of the bank

Understanding

Clients

Understand

differentiation

Cooperation

Agreements

Partnerships

Leveraging

what we have

Collaborations Transforming

from a service

to a business

Remain

competative

through cost

control