uk construction: consolidation ahead - ey_consolidation... · uk construction: consolidation ahead...

TRANSCRIPT

UK construction: consolidation aheadCounterparty risk

UK construction:consolidation aheadCounterparty risk

In this report

p2Executive summary

UK construction: consolidation ahead

p8Construction risks pose a threat to government, real estate and infrastructure investors

p4The UK construction industry

p10What can counterparties to the construction industry do to mitigate these risks today?

UK construction: consolidation ahead

p12Change is on the way – consolidation is likely

p16Conclusion: We see a dramatically different industry by 2020

Executive summaryThe current economic tail wind and more certain project pipeline — including significant opportunities in areas such as infrastructure and house building — should provide a backdrop in which the UK construction industry thrives. This is not, however, the case.

UK construction: consolidation ahead

Industry structure and company-specific challenges remain a barrier to a more operationally and financially robust construction sector. The top 25 UK construction companies turned over £42b last year and delivered an earnings before interest, tax, depreciation and amortization (EBITDA) margin of 2.6%.1 In contrast, Europe’s top 10 operators turned over £132b and recorded an EBITDA margin of 8.4%. Return on invested capital (RoIL)for the UK organisations totalled 0.4% in 2014 with only 3 of 25 participants exceeding 5%. The sector remains handicapped by risk across the contract life cycle, weak portfolio management, poor cash management, margin pressure and flawed structures and procedures.

A weak construction industry poses significant risk to the major counterparties to the sector, including government, real estate and infrastructure owners and investors. Cost escalation and, more importantly, contractor risk are growing concerns. These entities need to incorporate market, stakeholder, operational and capital key performance indicators (KPIs) into their ongoing due diligence procedures.

Without change, these issues will likely be accentuated in coming years as the project pipeline continues to grow for an industry that is ill-equipped to handle the increased workflow.

By 2020, we believe the construction industry will, however, change. We see significant consolidation ahead. This should be led by the handful of high-quality operators that exist today but may be initiated by interest from overseas. Entities from Southeast Asia, Sovereign Wealth Funds or continental European operators are all likely to be interested parties. The result will be a very different industry, one that we believe could contain as few as five leading players, each with revenue in excess of £5b return on invested capital (RoIC), of 5%+ and a likely £50m minimum project threshold.

For counterparties to the sector this consolidation will almost certainly reduce the risk associated with construction. This is likely to come at a financial cost. It may, however, be a financial cost worth bearing if it reduces the downside risks associated with projects running into difficulty. Ultimately, a construction sector that is both financially and operationally stronger will be of benefit to all.

1Source: company accounts analysed by EY

£42bTop 25 UKconstruction companies turnover — 2014

£132bTop 10 Europeconstruction companies turnover — 2014

£5brevenue each,from five leading players

In excess of

3UK construction: consolidation ahead

1.The UK Construction industry

4 UK construction: consolidation ahead

Construction sector still under severe pressure

Industry structure remains a barrier

Construction businesses are the sum of current contracts. Their profitability should be relatively immune to market cycles if contracts are appropriately priced and delivered. The health of the broader economy should then act as a multiplier in periods of growth.

The current economic tail wind and more certain forward order book — including significant opportunities in areas such as infrastructure and house building — should provide a backdrop in which the UK construction industry thrives.

This is not, however, materialising. The industry remains under severe pressure. Rising costs are well documented but we believe the problems extend further and are a combination of industry and company-level issues.

There are 41 UK construction companies that individually turn over in excess of £250m. Of this group, 15 companies turn over more than £1b. Below that, there are 56 entities turning over between £50m and £250m. The industry structure creates a highly competitive bidding process. In the extreme, projects are won on zero-margin terms with an expectation of profiting from add-ons. This may or may not materialise, potentially putting these contracts at risk.

UK construction industry

top 1002

£26bTotal revenue (£1.7b avg)

<£1b—£5bRevenue per company1.7% PBT (Range: -2% to +5%)

... the next

14

£19bTotal revenue (£0.2b avg)

<£1bRevenue per company<1% PBT

... the following

85

£10bRevenue <0% Profit before tax (PBT)

Numberone

company

2Source: EY

5UK construction: consolidation ahead

Company challenges are yet to be resolved

Financial results continue to be disappointing

Construction companies remain handicapped by inefficient supply chains and flawed internal management structures. These issues are accentuated by outdated and inadequate IT systems. We see five prevailing challenges.

Risk across the contract life cycle

Portfolio management

Cash management

Margin pressure

Front- and back-office structures and procedures

The result is supply chain failures and business structures that are incapable of providing adequate insight to management around project performance and risk appraisal. While management has been successful at maintaining total revenue in recent years (winning new contracts), without adequate project-level visibility at a central level, businesses continue to be at risk of a handful of failed projects eroding cumulative gains elsewhere. The potential for fraud also remains a real threat.

Cost pressures are accentuating the problem. Contractors, SMEs and civil engineers all report increasing cost pressures, which are squeezing margins. Labour cost is a particular burden, rising 25% in the last 10 years.3

The impact is being seen in financial results. In 2014, the top 25 UK construction companies turned over £42b for an EBITDA margin of 2.6% and a combined profit before tax of £437m (1.0% of turnover). In comparison, the 10 largest European construction companies turned over £132b and delivered a combined EBITDA margin of 8.4%.

Selling, general and administrative (SG&A) costs as a percentage of revenue for the top 20 UK operators improved in FY14 to 6.3%. The ratio improvement was, however, driven more by turnover growth than cost reductions. Absolute costs, for companies where comparable information is available, declined just 3% in FY14. An SG&A ratio for the industry of more than 6% is, in our opinion, still too high.

RoIC for the UK industry totalled just 0.4% in 2014. Only three organisations achieved returns in excess of 5%. This mirrors the longer-term trend; the listed construction sector has not produced an annual RoIC in excess of 3.5% in the last 10 years.

The UK construction industry

1

2

3

4

5

3 Source: Labour costs per hour www.ons.gov.uk

6 UK construction: consolidation ahead

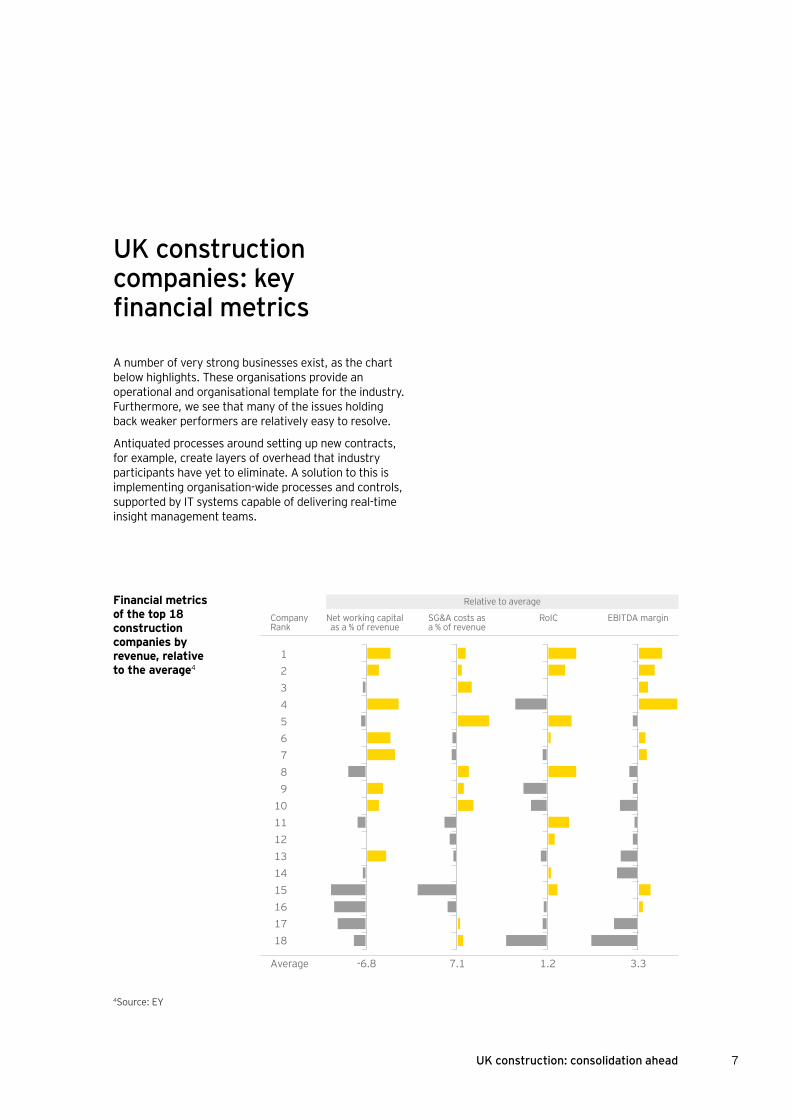

UK construction companies: key financial metrics

A number of very strong businesses exist, as the chart below highlights. These organisations provide an operational and organisational template for the industry. Furthermore, we see that many of the issues holding back weaker performers are relatively easy to resolve.

Antiquated processes around setting up new contracts, for example, create layers of overhead that industry participants have yet to eliminate. A solution to this is implementing organisation-wide processes and controls, supported by IT systems capable of delivering real-time insight management teams.

123456789

101112131415161718

Net working capital as a % of revenue

Relative to averageFinancial metrics of the top 18 construction companies by revenue, relative to the average4

SG&A costs as a % of revenue

RoIC EBITDA marginCompany Rank

Average -6.8 7.1 1.2 3.3

4Source: EY

7UK construction: consolidation ahead

The current condition of many UK construction companies presents a risk that extends beyond the construction industry. We see significant counterparty risk to a wide range of organisations, from government and local authorities

to real estate and infrastructure owners and investors. This will likely be accentuated in coming years as the project pipeline continues to grow for an industry that is ill-equipped to handle the increased workflow.

2.Construction risks pose a threat to government, real estate and infrastructure investors

8 UK construction: consolidation ahead

Cost escalation

Contractor risk

Rising costs, particularly around labour, are a well-documented and valid challenge. The fragmented nature of the construction industry allows investors to lock in favourable terms up front, but bulging order books, staffing challenges and, to a lesser extent the cost of raw materials result in cost and also time overruns being a very real threat.

Both cost and time overruns potentially have material consequences for commercial projects. This is either through eroding returns via additional expenditure or delivering schemes too late into the industry cycle.

We believe the structural change that we see transforming the construction industry will help resolve this (see section 4). Fewer companies, with better operating structures and more pricing power will reduce the need to underbid and subsequently overrun. Ultimately, counterparties will benefit through greater certainty around costs.

Contractor and, in particular subcontractor risk is a greater concern. Too much focus on turnover at the expense of profit and crucial cash flow has contributed to a spate of (sub) contractor insolvencies in recent years. This trend has continued as the macro environment has improved with, for example, two-high profile failures in the last quarter and an ongoing string of profit warnings.5

Contractor insolvencies are typically more disruptive than cost escalation. An insolvent (sub) contractor either means renegotiating project work, which is time-consuming and expensive, or agreeing a cost share between investor and contractor in order to fund the (sub) contractor through to completion.

Where (sub) contractors provide specialist services, it may not be possible to simply bring in a replacement. This will likely delay the entire project. In the worst cases, the contractor and, ultimately the investor, may find itself beholden to a receiver who is able to exert significant influence over the completion of the subcontract. The risk of financial loss as a result of a process outside of your control is very real.

The risks highlighted above are increased within many construction companies by a lack of internal transparency, which is accentuated by poor IT and lack of internal audit controls. Too many layers of internal management mean that group management is often not aware of the details around how a specific project is developing until the contract is beyond remedy. Without a centralised procurement and project management system, leadership is also unlikely to be fully informed of the potential impact of a (sub) contractor failure on their broader portfolio. The only way around this is for construction companies to implement a very strong central office function.

5Source: EY

We see two overarching risks for counterparties to the construction industry:

9UK construction: consolidation ahead

Government, real estate and infrastructure investors are well advised to revisit and potentially extend their due diligence procedures around selecting construction counterparties.

3.What can counterparties to the construction industry do to mitigate these risks today?

10 UK construction: consolidation ahead

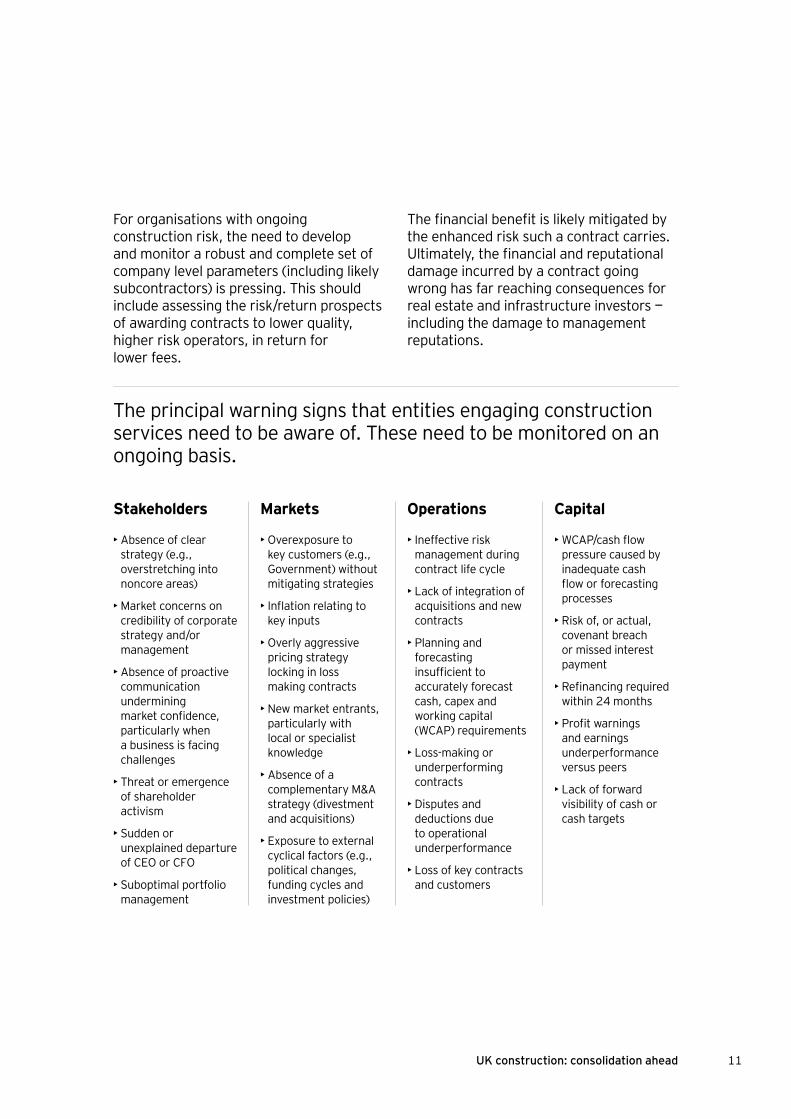

Stakeholders

• Absence of clear strategy (e.g., overstretching into noncore areas)

• Market concerns on credibility of corporate strategy and/or management

• Absence of proactive communication undermining market confidence, particularly when a business is facing challenges

• Threat or emergence of shareholder activism

• Sudden or unexplained departure of CEO or CFO

• Suboptimal portfolio management

Markets

• Overexposure to key customers (e.g., Government) without mitigating strategies

• Inflation relating to key inputs

• Overly aggressive pricing strategy locking in loss making contracts

• New market entrants, particularly with local or specialist knowledge

• Absence of a complementary M&A strategy (divestment and acquisitions)

• Exposure to external cyclical factors (e.g., political changes, funding cycles and investment policies)

Operations

• Ineffective risk management during contract life cycle

• Lack of integration of acquisitions and new contracts

• Planning and forecasting insufficient to accurately forecast cash, capex and working capital (WCAP) requirements

• Loss-making or underperforming contracts

• Disputes and deductions due to operational underperformance

• Loss of key contracts and customers

Capital

• WCAP/cash flow pressure caused by inadequate cash flow or forecasting processes

• Risk of, or actual, covenant breach or missed interest payment

• Refinancing required within 24 months

• Profit warnings and earnings underperformance versus peers

• Lack of forward visibility of cash or cash targets

The principal warning signs that entities engaging construction services need to be aware of. These need to be monitored on an ongoing basis.

For organisations with ongoing construction risk, the need to develop and monitor a robust and complete set of company level parameters (including likely subcontractors) is pressing. This should include assessing the risk/return prospects of awarding contracts to lower quality, higher risk operators, in return for lower fees.

The financial benefit is likely mitigated by the enhanced risk such a contract carries. Ultimately, the financial and reputational damage incurred by a contract going wrong has far reaching consequences for real estate and infrastructure investors — including the damage to management reputations.

11UK construction: consolidation ahead

We believe that something has to change and indeed will change over the next five years. For counterparties to the construction industry, this will likely fundamentally transform the risk associated with construction.

4.Change is on the way — consolidation is likely

12 UK construction: consolidation ahead

We expect the top 15 companies to increase their market share. This is partly as a result of scale advantages but mainly because a handful of organisations have well-run businesses that are able to deliver strong and consistent returns on invested capital. These organisations are backed by relatively healthy balance sheets and sector-leading platforms.

Equity and debt capital should migrate towards these entities. This will enable them to grow disproportionately through both organic and inorganic means.

The top 15 construction organisations have

c60% of market share by revenueWe expect this to increase

Post-recession UK construction is becoming a sellers’ market. Prices are strong, demand is rising and skills are in short supply. This is a favourable backdrop to consolidation.

Questions remain around whether entities have the financial capacity, capability and desire to undertake a major transaction. A further barrier may be the

impact that consolidation will have on government framework agreements. However, balance sheets have largely been restored, and investors have shown loyalty to the sector. Provided management teams are prepared to entertain transactions, we believe deals will be done.

Buoyant market with diminished regulatory risk following highways commitments, AMP6 and ongoing momentum in property and infrastructure

Significant scale advantages from access to labour in a market that is short of skills and value-adding capabilities

Strong business models that enable market leaders to deliver 5% returns while minimising risk contrasting sharply with other participants that struggle to drive return on invested capital

Need to invest in plant, technology and innovative solutions, which benefits larger

players with strong balance sheets

Major construction contracts are

increasing in size and complexity

e.g. Crossrail, HS2, nuclear,

requiring companies that can handle large and complex projects

“Corporatisation” economies of scale

We see the potential for a wave of consolidation in the sector.

Market conditions look well-suited to consolidation

Specific drivers of this will likely be:

13UK construction: consolidation ahead

There are few truly global construction companies that could disrupt this consolidation process. There is, however, a number of other organisations that may be interested participants. Many have very deep pockets and a motivation to acquire the type of

skills prevalent in the UK construction market. A move from an external organisation could kick- start a wave of transactions as incumbents risk being left behind.

Global capital could be the catalyst to transactions

We see four likely sources of external capital

Entities in Southeast Asia and China in particular are undoubtedly interested. Many of the UK organisations would be natural extensions of major domestic entities (both state and otherwise) with obvious scope for both cost synergies (particularly on raw materials) and sharing of best practices.

Private equity is less likely to be a source of capital or an obvious partner, particularly with the current limitations around delivering the type of strong and robust cash flows so favoured by investors; but the industry is awash with dry powder and the scope to drive operational improvement through better financial management clearly exists; amid a wave of consolidation a well-run, operationally efficient midsize construction organisation would be an attractive bolt on to one of the industry behemoths that we believe will emerge.

Sovereign wealth funds more broadly, again with non-financial interests such as transferring project expertise to domestic markets being an added incentive.

Continental European players Large cap companies could acquire a UK entity and add its operations to their existing platform.

UK construction: consolidation ahead 14

15UK construction: consolidation ahead

By 2020, we expect as few as five of the leading players could survive.

5.Conclusion: We see a dramatically different industry by 2020

16 UK construction: consolidation ahead

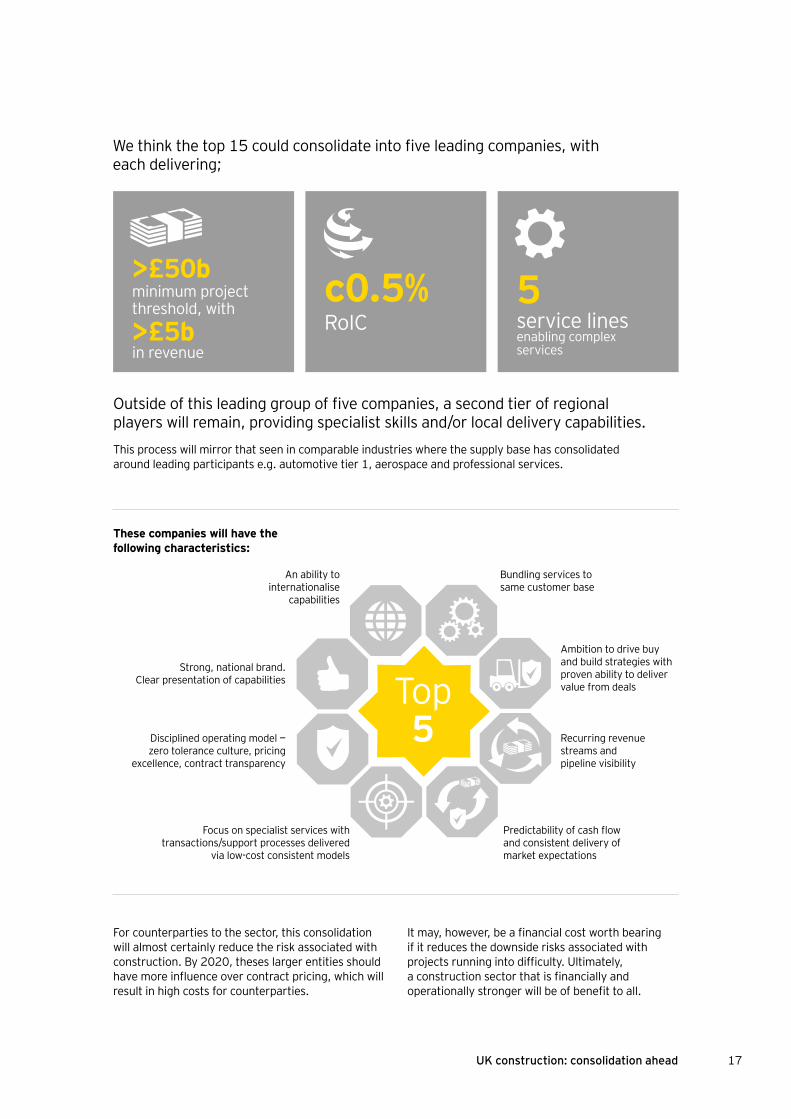

We think the top 15 could consolidate into five leading companies, with each delivering;

These companies will have the following characteristics:

Outside of this leading group of five companies, a second tier of regional players will remain, providing specialist skills and/or local delivery capabilities.This process will mirror that seen in comparable industries where the supply base has consolidated around leading participants e.g. automotive tier 1, aerospace and professional services.

For counterparties to the sector, this consolidation will almost certainly reduce the risk associated with construction. By 2020, theses larger entities should have more influence over contract pricing, which will result in high costs for counterparties.

It may, however, be a financial cost worth bearing if it reduces the downside risks associated with projects running into difficulty. Ultimately, a construction sector that is financially and operationally stronger will be of benefit to all.

Bundling services to same customer base

An ability to internationalise

capabilities

Predictability of cash flow and consistent delivery of market expectations

Focus on specialist services with transactions/support processes delivered

via low-cost consistent models

Disciplined operating model — zero tolerance culture, pricing

excellence, contract transparency

Strong, national brand. Clear presentation of capabilities

Ambition to drive buy and build strategies with proven ability to deliver value from deals

Recurring revenue streams and pipeline visibility

Top 5

>£50b minimum project threshold, with

>£5bin revenue

c0.5% RoIC

5service lines enabling complex services

17UK construction: consolidation ahead

Key contactsRussell GardnerHead of Real Estate, Hospitality & Construction, UK&I

[email protected] + 44 [0] 20 7951 5947

Fraser GreenshieldsHead of Real Estate, Hospitality & Construction Transaction Advisory Services, UK&I

[email protected] + 44 [0] 20 7951 7151

Malcolm BairstowHead of Infrastructure, UK&I

[email protected] + 44 [0] 20 7951 3685

Henry StrattonReal Estate Analyst

[email protected] + 44 [0] 20 7980 0666

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Global Real Estate SectorToday’s real estate sector must adopt new approaches to address regulatory requirements and financial risks while meeting the challenges of expanding globally and achieving sustainable growth. EY’s Global Real Estate Sector brings together a worldwide team of professionals to help you succeed — a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Sector team works to anticipate market trends, identify their implications and develop points of view on relevant sector issues. Ultimately, this team enables us to help you meet your goals and compete more effectively.

Ernst & Young LLPThe UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

© 2015 Ernst & Young LLP. Published in the UK. All Rights Reserved.

EYG no: DF0229 ED 0115

Artwork by JDJ Creative Ltd.

In line with Ernst & Young’s commitment to minimise its impact on the environment, this document has been printed on paper with a high recycled content.

Information in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.

ey.com/uk

EY | Assurance | Tax | Transactions | Advisory