©ufs confidential joseph w. jordan senior vice-president national sales organization lessons...

TRANSCRIPT

©UFS

CONFIDENTIAL

Joseph W. JordanSenior Vice-President

National Sales Organization

Lessons Learned MDRT GreeceNovember 25, 2009

Metropolitan Life Insurance Company, 200 Park Ave., New York, NY 10166

CONFIDENTIAL

WORLDWIDE INSURANCE MARKETS

CONFIDENTIAL

High GDP

Growth /Low Life

Penetration

- China

- India

- Russia

- Brazil

- SE Asia

- Poland

- Saudi Arabia

- Kuwait

- UAE

Moderate GDP

Growth/Low Life

Penetration

- Mexico

- Chile

- Argentina

- Greece

- Czech Republic

- Turkey

Low GDP

Growth/High Life

Penetration

- US

- UK

- Western Europe

- Japan

- South Korea

- Taiwan

GDP growth and insurance penetrate levels will impact the life insurance growth rates

Source: EIU, Swiss Re

CONFIDENTIAL

International markets are growing more rapidly than the U.S.

Markets of Today

Markets of Tomorrow

W. Europe

$1,069 12%

Premiums $B

Premium Growth

Japan

$367

-0.3%

Premiums $B

Premium Growth

U.S.

$578

4%

China

$95

24%

India

$49

29%

Greece

$3.5

12.5%

CEE

$29

28%

Data provided by MetLife International Research

CONFIDENTIAL

Opportunities for Greece

• The aging of Greece in general offers an excellent environment for annuity products as people will be required to make provisions for retirement themselves and not rely on an inadequate pension system

• With a low life insurance penetration, gradual disintegration of the joint family structure, and inadequate state pension system Greece offers a potential market for attractive retirement income and savings products

CONFIDENTIAL

WORLDWIDE ECONOMIES

CONFIDENTIAL

ISI Economic Diffusion Index: United States

Source: ISI Group

Charts provided with

permission by

CONFIDENTIAL

ISI Economic Diffusion Index: Foreign Economies

Source: ISI Group

Charts provided with

permission by

CONFIDENTIAL

ISI Economic Diffusion Index: Emerging Economies

Source: ISI Group

Charts provided with

permission by

CONFIDENTIAL

ISI Economic Diffusion Index: Global Economy

Synchronized global recovery lead by

emerging counties

Source: ISI Group

Charts provided with

permission by

CONFIDENTIAL

Earnings Revisions by Region

Au

g-0

9

Charts provided with

permission by

CONFIDENTIAL

CRISIS

CONFIDENTIAL

Wall Street Journal – March 3, 2009

©2009 Dow Jones & Company, Inc.

CONFIDENTIAL

Joe’s Tip

CONFIDENTIAL

Wall Street Journal – October 1, 2009

©2009 Dow Jones & Company, Inc.

The Dow Jones Industrial Average jumped 15% in the latest three months for its biggest quarterly gain since the fourth quarter of 1998 and its best third quarter since 1939.

CONFIDENTIAL

Great Depression vs. Great Recession

Great Depression

Great Recession

Bank Failures9,096

50% of banks57

0.6% of banks

Unemployment Rate 25% 9.4%

Economic Decline (drop in inflation adjusted GDP)

-26.5% -3.3%

Changes in Prices -25% +0.5%

Source: LIMRA – New Normal: Myth or Reality

CONFIDENTIAL 17

Is this time any different?

August 1979S&P 500 closed at 109

October 30, 2009S&P 500 closed at 1,036

CONFIDENTIAL 18

Same Story Different Day…

November 2, 1987S&P 500 closed at 255

October 9, 2009S&P 500 closed at 1,036

CONFIDENTIAL

No bear market feels “average” — or even normal — while you’re going through it.

It feels like the end of the world.

CONFIDENTIAL

History of the Bear (Post World War II)

Source: Nick Murray : Impact of the Bear October 2009

Market Peak Market Trough % Return Duration Market Peak Market Trough

05/29/46 06/13/49 -30% 36.5 months 19.3 13.6

08/02/56 10/22/57 -22 14.5 months 49.7 39.0

12/12/61 06/26/62 -28 6.5 months 72.6 52.3

02/09/66 10/07/66 -22 8.0 months 94.1 73.2

11/29/68 05/26/70 -36 18.0 months 108.4 69.3

01/11/73 10/03/74 -48 20.5 months 120.2 62.3

09/21/76 03/06/78 -19 17.5 months 107.8 86.9

11/28/80 08/12/82 -27 20.5 months 140.5 102.4

08/25/87 12/24/87 -34 4.0 months 336.8 223.9

07/16/90 10/11/90 -20 3.0 months 369.0 295.5

07/17/98 08/31/98 -19 1.5 months 1186.8 957.3

03/24/00 10/09/02 -49 30.5 months 1527.5 776.7

10/09/07 03/09/09 -57 17.0 months 1565.1 676.5

13.6

676.5

The march of equities between bear markets

CONFIDENTIAL

Left Brain – Right Brain

CONFIDENTIAL

CONFIDENTIAL

Managing Behavior

Principles

1) Faith

2) Patience

3) Discipline

Behaviors

1) Asset Allocation

2) Diversification

3) Rebalancing

© 2008 Nick Murray All rights reserved. Used with permission. From Nick Murray's book Behavioral Investment Counseling www.nickmurray.com

CONFIDENTIAL

LESSONSLEARNED

CONFIDENTIALUsed by permission: New York Public Library

CONFIDENTIAL

IMPACT ON

OTHERS

CONFIDENTIAL

CONFIDENTIAL

Everyone Dies!

Interesting and Amazing Stuff

CONFIDENTIAL

TIMEAugust 30, 2004

People Will Live Longer

© 2009 Time Inc.

CONFIDENTIAL

Many people greatly underestimate the time they will spend in retirement

The Risks

50% Chance of living beyond

25% Chance of living beyond

Male (age 65) 85 92

Female (age 65) 88 94

50% Chance of living beyond

25% Chance of living beyond

50% Chance of living beyondAt least one person has a:

Couple (both age 65) 9792

25% Chance of living beyond

Source: U.S. 2000 Actuarial Male and Female Tables

CONFIDENTIAL

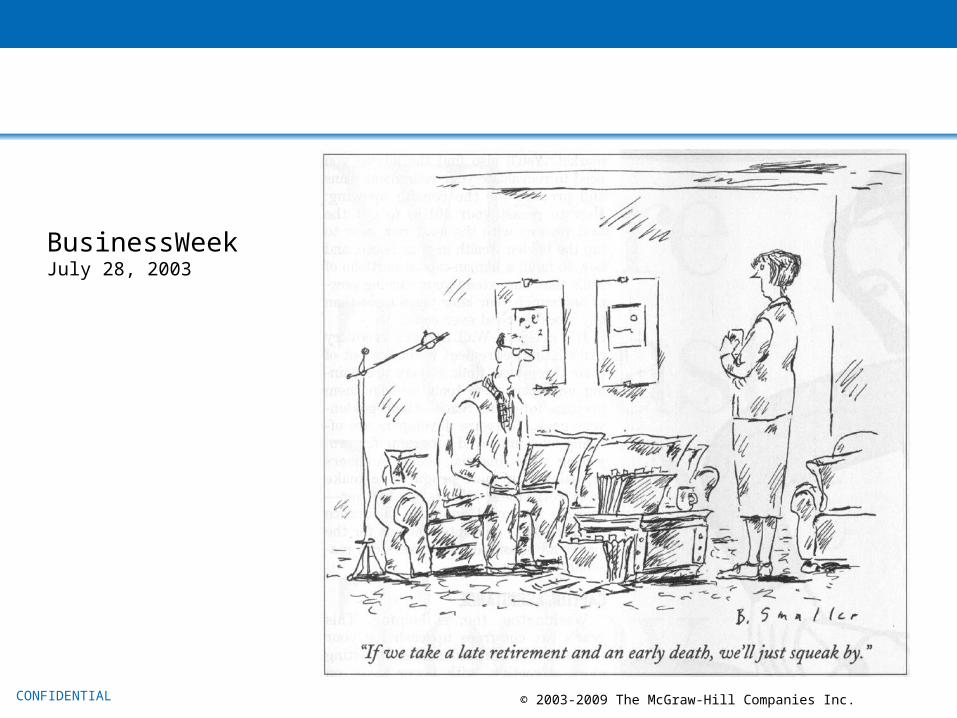

BusinessWeekJuly 28, 2003

© 2003-2009 The McGraw-Hill Companies Inc.

CONFIDENTIAL

Wall Street Journal, April 23, 2003

©2003-2009 Dow Jones & Company, Inc.

CONFIDENTIAL

Mother-in-Law

CONFIDENTIAL

CONFIDENTIAL

Return onInvestmentReturn on

InvestmentReliabilityof IncomeReliabilityof Income

Consumer Change of Focus

Accumulation Phase

Distribution Phase

CONFIDENTIAL

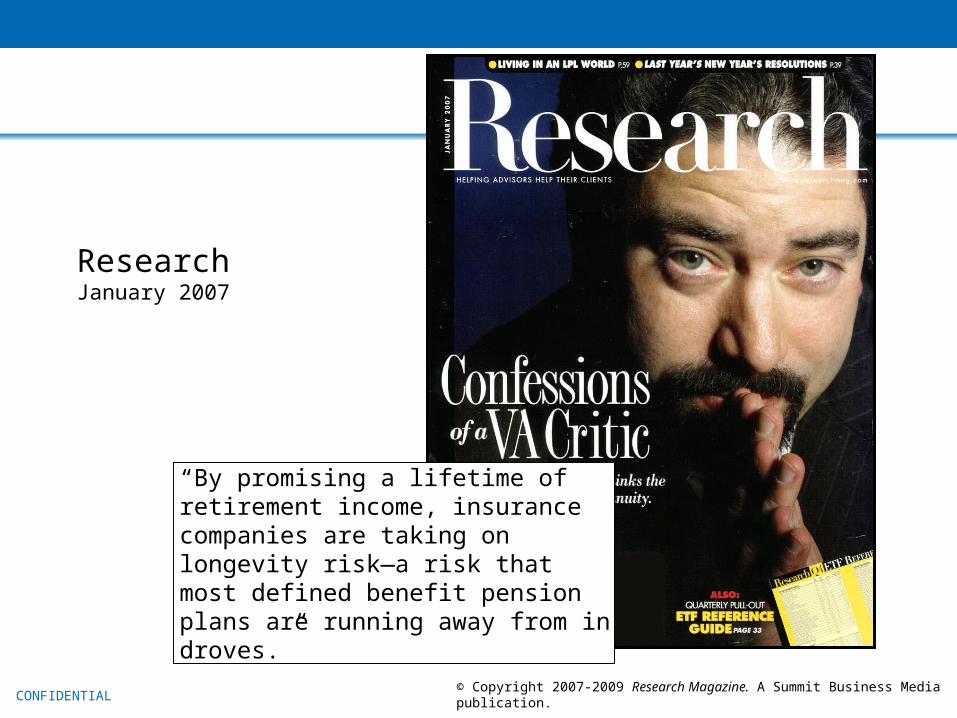

ResearchJanuary 2007

“By promising a lifetime of retirement income, insurance companies are taking on longevity risk—a risk that most defined benefit pension plans are running away from in droves.”

© Copyright 2007-2009 Research Magazine. A Summit Business Media publication.

CONFIDENTIAL

The Importance of LongevityTraditional Retirement Calculation: Monthly Income

PortfoliosConservative Aggressive

1. Retirement Start Age: 65 Years 2. Retirement Length: 15 Years3. Retirement Assets: $1 mil 4. Simulated Success Rate: 90%5. Inflated by 3% each year, year 2+

Stocks5%

Bonds25%

ShortTermBond70%

Stocks15%

Bonds35%

ShortTermBond50%

Stocks25%

Bonds40%

ShortTermBond35%

Stocks40%

Bonds40%

ShortTermBond20%

Stocks60%

Bonds30%

ShortTermBond10%

Stocks80%

Bonds20%

ShortTermBond0%

Stocks100%

Bonds0%

ShortTermBond0%

Source: Mathew Greenwald & Associates Inc., 2007. Chart reflects initial monthly income, inflated by 3% annually each year. Figures, calculations, and graphs are for illustrative purposes only. They are based on hypothetical rates of return and do not represent investment in any specific product. Assumed Portfolios are from T. Rowe Price Retirement Calculator which can be found at http://www3.troweprice.com/ric/RIC, and assume the use of Large Cap, Small Cap and International stocks; Investment-Grade, High Yield, International, and short term Bonds. They may not be used to predict or project investment performance. Unless noted, charges and expenses that would be associated with an actual investment are not reflected.

$5,800 $5,900 $5,800 $5,700 $5,500$5,300

$6,000

Stocks

Bonds

CONFIDENTIAL

The Importance of LongevityTraditional Retirement Calculation: Monthly Income

PortfoliosConservative Aggressive

Source: Mathew Greenwald & Associates Inc., 2007. Chart reflects initial monthly income, inflated by 3% annually each year. Figures, calculations, and graphs are for illustrative purposes only. They are based on hypothetical rates of return and do not represent investment in any specific product. Assumed Portfolios are from T. Rowe Price Retirement Calculator which can be found at http://www3.troweprice.com/ric/RIC, and assume the use of Large Cap, Small Cap and International stocks; Investment-Grade, High Yield, International, and short term Bonds. They may not be used to predict or project investment performance. Unless noted, charges and expenses that would be associated with an actual investment are not reflected.

$3,600 $3,700 $3,800 $3,800 $3,700 $3,600$3,800

Stocks

Bonds

1. Retirement Start Age: 65 Years 2. Retirement Length: 25 Years3. Retirement Assets: $1 mil 4. Simulated Success Rate: 90%5. Inflated by 3% each year, year 2+

CONFIDENTIAL

Will Sequence of Returns Matter?Drowning in Two Inches of Water

17%

-22%27%

8%

Source: Moshe Milevsky, Ph.D.; IFID

Average Return

$1 milNest Egg

$3,800Monthly

Withdrawal

+3% Inflation

CONFIDENTIAL

Will Sequence of Returns Matter?1

Drowning in Two Inches of Water

1.) Source: Moshe Milevsky, Ph.D.; IFID. 2.) Assumptions: Hypothetical return of 17%, 27% and -22% in 3 year cycle for life of investment. Hypothetical investment management fee of 2.05% (0.8% fund company management fee and 1.25% WRAP fee. 3. Assumptions: Hypothetical return of 17%, -22 and -27% in 3 year cycle for life of investment. Hypothetical investment management fee of 2.05% (0.8% fund company management fee and 1.25% WRAP fee.) Figures, calculations, and graphs are for illustrative purposes only. They are based on hypothetical rates of return and do not represent investment in any specific product. They may not be used to predict or project investment performance. Unless noted, charges and expenses that would be associated with an actual investment are not reflected.

$1 milNest Egg

$3,800Monthly Withdrawal

+ 3% Inflation

+17%

-22%+27%

8%AverageReturn

+17%

-22%+27%

8%AverageReturn

Age at Ruin: 2

90Age at Ruin: 3

86

CONFIDENTIAL

Will Sequence of Returns Matter?The Implications of Timing = Less In Future

PortfoliosConservative Aggressive

Assumptions: Hypothetical return of 17%, -22% and -27% in 3 year cycle for life of investment. Hypothetical investment management fee of 2.05% (0.8% fund company management fee and 1.25% WRAP fee.) Initial income inflated by 3% annually (per prior slides), Figures, calculations, and graphs are for illustrative purposes only. They are based on hypothetical rates of return and do not represent investment in any specific product. They may not be used to predict or project investment performance. Unless noted, charges and expenses that would be associated with an actual investment are not reflected.

$3,600 $3,700 3,800 $3,800 $3,700 $3,600

Year 1 $3,800

Yr 2+$3,325

+17%

-20%+27%

8.00%Avg. ROR

-22%1. Retirement Start: Age 65 2. Retirement Length: 25 Years3. Retirement Assets: $1 mil 4. Simulated Success Rate: 90%5. Inflated by 3% each year, year 2+

CONFIDENTIAL ©2009 Dow Jones & Company, Inc.

“Give yourself a pay cut by withdrawing a little less today and continuing to take out less over the next several years.”

“If your portfolio took a 30% loss, the news is much more grim: You’d have a 79% chance of running out of money prematurely if you continued a traditional withdrawal strategy.”

Wall Street Journal October 14, 2008

CONFIDENTIAL

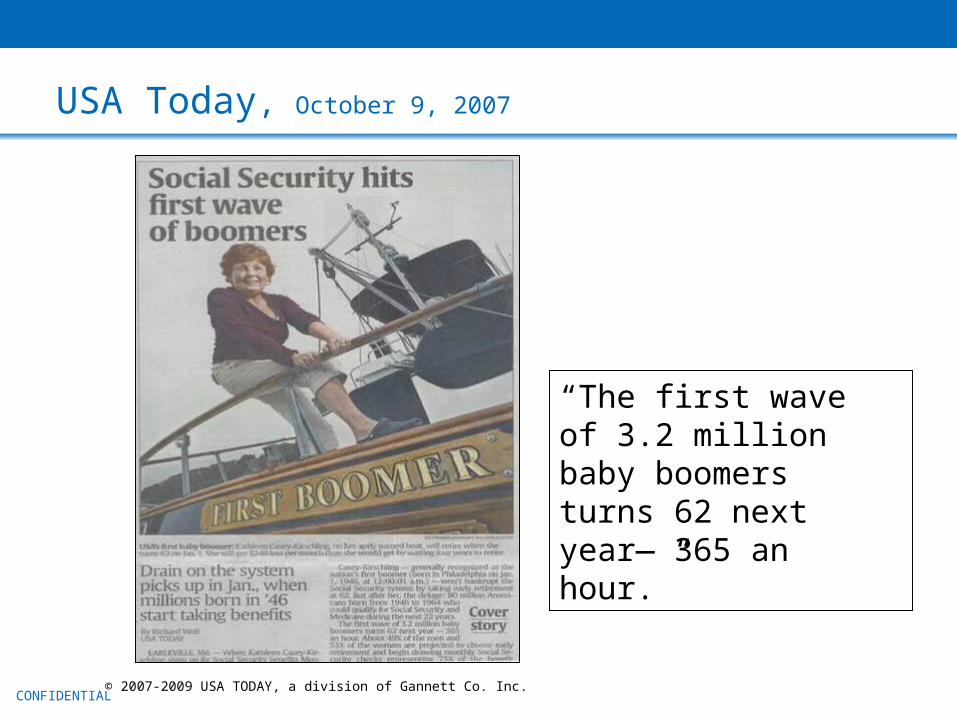

USA Today, October 9, 2007

“The first wave of 3.2 million baby boomers turns 62 next year— 365 an hour.”

© 2007-2009 USA TODAY, a division of Gannett Co. Inc.

CONFIDENTIAL

A Life of

Significance

CONFIDENTIAL

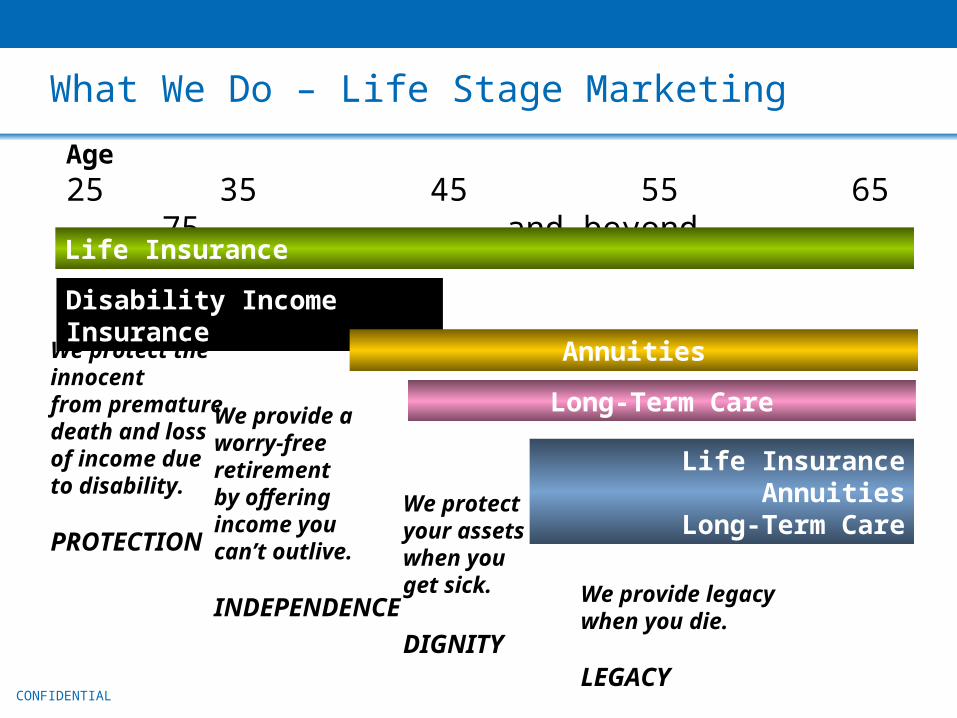

Age25 35 45 55 65 75 … and beyond

Life Insurance

Disability Income Insurance

Annuities

Long-Term Care

Life InsuranceAnnuities

Long-Term Care

We provide legacy when you die.

LEGACY

We protect the innocentfrom prematuredeath and loss of income dueto disability.

PROTECTION

We provide aworry-freeretirementby offeringincome youcan’t outlive.

INDEPENDENCE

We protect your assets when you get sick.

DIGNITY

What We Do – Life Stage Marketing

CONFIDENTIAL

YOU’RE A HERO

CONFIDENTIAL

Living a Life of Significance

CONFIDENTIAL

CONFIDENTIAL

MDRT Excerpt

CONFIDENTIAL

CONFIDENTIAL

Life of Significance

CONFIDENTIAL