ubl internship report 0f 2015

TRANSCRIPT

United Bank Limited

Bosan Road Gol Bagh Branch, Multan

A REPORT SUBMITTED TO INSTITUTE OF MANAGEMENT SCIENCES, BZU

MULTAN, IN PARTIAL FULLFILLMENT AND REQUIREMENTS FOR THE

DEGREE OF MASTER IN BUSINESS ADMINISTRATION

Submitted By

MARYAM SHABBIR

MB13- 13

Institute of Management Sciences, Multan1

2

PREFACE

In Masters of Business Administration, Internship Program is an important part to give

students an opportunity to have experience of practical field. Unless and until the students

experience the novelty of practical work, their knowledge of what they study in theoretical

courses remains incomplete. The most important point in an Internship Program is that the

student should spend their time in a true manner and with the spirit to learn practical orientation

of theoretical study framework.

This internship report is on my six weeks practical training at United Bank Limited

Bosan Road Branch, Multan. In this internship report I have tried to give details about the United

Bank Limited, working and the functions of different departments of the bank.

3

ACKNOWLEDGEMENT

All praise to ALMIGHTY ALLAH alone, the Omnipresent and the most Merciful and

compassionate. The words are bound, knowledge is limited and time is short to express His

dignity. It is one of infinite blessings of ALLAH that he best owed me with the potential and

ability to contribution towards the deep oceans of knowledge already existing. I pay hum-age to

greatest personality of the universe; HOLY PROPHET HAZARAT MUHAMMAD (PBUH)

Who is forever torch bearer and spring of guidance in every sphere of life. I am deeply indebted

and also express my gratitude to my respected teachers at BZU MULTAN for their support.

At the very outset, I am very thankful to Mr. Khalid (Branch Manager) for providing me

the opportunity to have an excellent learning experience during my internship at United Bank

Ltd Bosan road branch Multan. The person to whom I would like to give my regards is the Mam

Shaista (Customer service relationship officer) at UBL, who gave me very useful tips and

information. I might not be able to complete my internship without his cooperation and his kind

behavior. I am thankful to all my teachers of BZU Campus Multan.

I also take this opportunity to express a deep sense of gratitude to all the staff members of

UBL for their cordial support, valuable information and guidance, which helped me in

completing this task through various stages specially

Mr. Khalid Branch Manger

Mr. Yasir Operational Manger

Mam Shaista CSR officer

Mr. Samar CSR

Mr. Naeem Chief Cashier

Lastly, I thank almighty, my parents and friends for their constant encouragement without

which this internship would not be possible.

4

EXECUTIVE SUMMARY

Banking operations and services are one of the basic needs of an economy. These include

acceptance of deposits and disbursement of advances to individuals and others at higher rates.

Banks perform various fundamental factions, which are directly or indirectly contributory

towards economic and social development of countries.

The purpose of this report is to study operations and analyze performance of UBL to see

whether the bank is successful in its operational performance or not, and recommending possible

solutions for problems. For meeting the purpose both secondary and primary data have been

used.

United Bank Limited (UBL) is the second largest bank of Pakistan with assets of over Rs.

1 Trillion and a solid track record of fifty six years - in addition to the convenience of over 1320

branches serving its customers throughout the country and also at several overseas locations. In

this six weeks internship program I have learned about banking from experienced managers

running these sections.

This report contains the information and learning about UBL that I learnt during the 06

weeks internship period in United Bank limited. This report deals with History & Nature

(Business) of the UBL, its Products and Services, information about main offices and also the

review of various departments of the Bank. This report also contains Finance & Accounting

operations of the UBL, role of Financial Manager (Branch Manager), Use of Electronic Data in

core decision making and the Sources, Generation and Allocation of funds used in the banking

operations of the UBL.

Recognizing the need of Islamic banking, UBL also provided number of Islamic banking

services like Islamic Deposit Schemes and Islamic Fund Based Facilities.

5

At the end of this report, on basis of my observation during internship, financial analysis

and SWOT analysis of UBL is provided. Suggestions are also recommended as per learning from

analysis. This report will provide a better and brief learning about United Bank Limited.

6

Sr. No. Content Page No.

1 PREFACE

2 DEDICATION

3 ACKNOWLEDGEMENT

4 EXECUTIVE SUMMARY

5 1. INTRODUCTION 2

6 2. ORGANIZATIONAL STRUCTURE 15

7 3. MY LEARNING’S 23

8 4. FINANCIAL STATEMENTS, VERTICAL and TREND ANALYSIS

32

9 5. RATIO ANALYSIS 39

10 6. SWOT ANALYSIS 52

11 7. PEST ANALYSIS 55

12 8. RECOMMENDATIONS 56

13 9. ANNAXURE 62

14 10. REFERENCES 63

7

8

1. INTRODUCTION

1.1 Brief history of the organization:

About UBL:

The history of UBL can be divided into four main Phases:

Formulation

Nationalization

Privatization

UBL Today

1.1.1. FORMULATION:

In June 1957, Mr. Agha Hassan Abidi decided to open a Bank different from others, to

provide modern facilities to trade and industry and to promote thrift and habit of saving amount

common thereby stimulating the economy as a whole. Necessary formalities completed for

obtaining registration certificate from State Bank of Pakistan to perform business activities. After

passing through all these formalities on 7th November, 1959 United Bank Ltd came into

existence as a Schedule bank.

The Head office of the Bank was established in the New Jubilee Insurance House, 1.1

Chundrigar Road Karachi. It was registered as a joint stock company. The bank was incorporated

with an Authorized Capital of Rs 20,000,000 and issued and subscribed and paid up capital of

RS 10, 00,000. Saigol family owned it and Agha Hassan Abedi was its first managing Director.

1

1.1.2. NATIONALIZATION:

As a policy of nationalization fourteen commercial banks was merged into five big

banks . So consequently on 21st December 1974 Commerce Bank and Union bank was merged

with the UBL. Mr. Mushtaq Ahmed khan Yousafi took over the charge of UBL. Now, there are

six directors, a secretary and a president.

1.1.3. PRIVATIZATION OF UBL:

UBL was the largest privatization attempted by the government of Pakistan, launched in

June 2001, with 21 interested parties. It was impacted by the adverse developments of the

September 11, 2001 and was finally concluded in October 2002, which left stage only three

bidders. The consortium comprising Best way Group (BG), out of the U.K. and Abu Dhabi

Group (ADG) from the U.A.E. were finally the winners at a record price. Sale proceed was Rs

12350 million. This signaled the strong confidence reposed by these investor groups, in the

improved governance of the country, the economic potential, the banking opportunity and the

existing management of the bank.

1.1.4. UBL TODAY:

Today the bank has taken progressive steps. The United Bank Limited (UBL)

management has launched its new corporate identity and changed its 44 year-old-logo following

its privatization. UBL has started the Online Banking & Click n Remit services.

CHAIRMAN:

His Highness Shaikh Nahayan Mabarak Al Nahayan.

DEPUTY CHAIRMAN:

Sir Mohammed Anwar Pervez OBE.

PRESIDENT & CEO: Wajahat Hussain

2

BRANCHES:

1320 Online , 15 Overseas Branches.

REPRESENTATIVE OFFICES:

Tehran

Kazakhistan

China

SUBSIDIARY:

United Bank AG Zurich, Switzerland.

United National Bank Limited, UK (Joint venture with NBP).

UBL Fund Managers Limited.

ASSOCIATED COMPANIES:

Oman United Exchange Company, Muscat.

UBL Insurers Limited.

OFFSHORE BANKING UNIT:

Export Processing Zone, EPZ Branch, and Karachi, Pakistan.

HEAD OFFICE:

State Life Insurance Corp. Building #1,

I.I. Chundrigar Road, Karachi, Pakistan

P.O. Box No.: 4306

Phone: (92-21) 111-825-111

Gram: "UNITED"

Fax: (92-21) 2413492.

3

1.2 NATURE OF THE ORGANIZATION

UBL is a Banking Company, which is engaged in Commercial & Retail Banking

and related services domestically and overseas. UBL was set up in 1959 by Agha Hassan

Abedi and is today one of Pakistan's major banks in terms of deposits and advances. The

Group's principal activities are to provide commercial banking and other financial

services. The Group offers personal banking, cash management, retail loans and other

financial services. These services include deposits, savings/current bank account, vehicle

loans, personal loans, retail trade finance, global banking, lending to priority sector and

small scale sector, foreign exchange and export finance, corporate loans and equipment

loans.

In 1971 the Government of Pakistan nationalized it. In 2002, the Government of

Pakistan sold it in an open auction to a consortium of Abu Dhabi Group and Best way

Group. Since its privatization the bank has been successfully turned around and remains a

robust and strong performer in all major segments of its operations. In 2002 it merged its

operations in the UK with those belonging to National Bank of Pakistan to form United

National Bank Limited, of which it owns 55%, with National Bank of Pakistan owning

the remainder.

The Bank is making every effort to meet the up-coming challenges through

strategic planning and making the best use of the resources at its command. A

professional team was appointed in mid 1997 to restructure the bank and to commence

rightsizing. The management is also in the process of rationalizing the branch network

and identifying and recovering its doubtful and classified portfolio. It has planned to

institute major improvements in customer services and internal systems to improve

efficiency. It also intends to launch innovative products. The bank is increasing resource

mobilization through regular deposit campaigns and accelerating the process of recovery

of outstanding advances and non-performing assets.

4

1.2.1. VISION STATEMENT:

“To be a world class bank dedicated to excellence, and to surpass the highest

expectations of our customers and all other stakeholders”.

1.2.2. MISSION STATEMENT:

Set the highest industry standard for quality across all areas of operation,

on a sustained basis;

Optimize people, processes and technology to deliver the best possible

financial solutions to our customers;

Become the most sought after investment;

Be recognized as the employer of choice.

1.2.3 Core Values:

Honesty and Integrity

Commitment and Dedication

Fairness and meritocracy

Team work and collaborative spirit

Humility and Mutual respect

Caring and socially responsible

5

1.3. NUMBER OF EMPLOYEES

1.3.1. BOARD OF DIRECTORS:

Name Designation

His Highness Shaikh Nahayan Mabarak Al Nahayan Chairman

Sir Mohammed Anwar Pervez, OBE, HPK Deputy Chairman

Mr. Atif R. Bokhari President & CEO

Mr. Omar Ziad Jaafar Al Askari Director

Mr. Zameer Mohammed Choudrey Director

Dr. Ashfaque Hasan Khan Director

Mr. Muhammad Sami Saeed

Director

Mr. Aqeel Ahmed Nasir

Company Secretary

6

1.4. PRODUCT LINES

1.4.1. DEPOSIT PRODUCTS:

UBL has taken progressive steps and has introduced innovative products and

services to provide you a variety of banking and financing services including Current and

BB Accounts.

UBL UNIFLEX ACCOUNT:

UBL has introduced a new checking account ideal for small investors, traders,

businessmen and customers from middle income group. They can now afford an amazing

7

Consumer Banking

UBL Address

UBL BusinessLi

ne

UBL CashLine

UBL Credit Cards

UBL Drive

UBL Money

Commercial Banking

Agriculture Products

Small Business Schemes

Investment and Saving Accounts

CB & Basic Banikng Accounts

UBL Business Partner (CA)

PLS UniSaver

PLS UniSaver Plus

UBL Rupee Transaction

Account (PLS Saving)

UBL UniFlex

e-Transaction (CA)

Complementry/Other Services

Insurance Certificate

UBL Net banking

UBL e-statement

rate of return plus value added benefits only available from the UBL UniFlex PLS

Savings Account.

UBL PROFIT COD:

Customer can earn a higher income on their surplus cash by investing it in UBL

Profit Certificate of Deposit. UBL Profit helps them earn extra income with their hard

earned money, while providing absolute trust and security.

PLS REGULAR TERM DEPOSITS RECEIPTS:

If customer wish to make a secured long term investment, UBL’s Term Deposit

Receipts the smart choice. UBL Term Deposit Receipts provides an attractive rate of

return. The profit is credited to the customer account every six months. Customer has the

flexibility to choose from a wide range of tenors. Customer can avail the Rollover or

Renewed option at any time before encashment. Customer can get TDR en-cashed at any

time before maturity period.

FOREIGN CURRENCY SAVINGS & FOREIGN CURRENCY TERM DEPOSITS RECEIPTS:

United Bank offers the best rates of return on Foreign Currency Deposits in the

market. Accounts can be opened in US Dollar, Pound Sterling, Euro, and Japanese Yen at

designated branches. All Pakistani nationals residing in Pakistan and outside Pakistan can

also open Foreign Currency Accounts. Resident Firms and companies including

Investment Banks can open Accounts.

8

UBL E-TRANSACTION ACCOUNT:

When it comes to electronic financial

services www.ubl.com.pk is Pakistan’s favorite Internet destination and why not! With years of

experience in innovation United Bank offers a wide spectrum of world-class of electronic

services and banking products for trailblazers like you.

1.4.2. LOANS & CARDS

UBL MONEY:

UBL Money, the Personal Installment Loan from UBL provides you with power, control,

convenience and the flexibility to manage your financial requirements and realize your dreams.

UBL Money is a fixed installment loan. It gives you access to funds starting from Rs.

50,000/- up to a maximum of Rs. 500,000/- without any collateral. UBL Money provides you the

flexibility to manage your monthly installments according to your income stream. You can select

any tenor from 1 to 5 years in a multiple of 12 months.

UBL BUSINESSLINE:

UBL Businessline is a running Finance facility that not only provides funds for growth

but also enables you to capitalize on profitable opportunities.

UBL CASHLINE:

UBL Cashline is a flexible loan that provides you cash up to Rs.500, 000 without any

9

security requirements. It empowers you to take control of your finances.

UBL Cashline is aimed to make your life easier .Whether you are a salaried individual or a

businessman.

UBL DRIVE:

UBL Drive allows you to drive away in

your own car by making a down payment of just 15% and to top that with low monthly

installments. With UBL Drive you can buy your favorite used car (up to 5 years old) at the most

affordable rates. UBL Drive is not just a car loan; it’s a financing facility that gives you Cash on

your car.

UBL ADDRESS:

UBL Address empowers you to become the proud owner of a home by offering a variety

of product and pricing options that are flexible yet affordable. So choose the best product option

and pricing to suit your needs

UBL PAYPLUS:

If you are a permanent employee of a company (Government, Semi-Government, MNC

or Local Corporate Entity/Private/Public Limited), which disburses salary through UBL, then

UBL PayPlus (loan against salary) is the right product for you. Through UBL PayPlus, you can

now easily avail a loan based on your salary level.

10

UBL CREDIT CARD:

UBL Credit Card provides the following facilities:

To share the value, excitement and benefits

Each time UBL Card members use their UBL Credit Card to purchase airline,

train or bus tickets, they are automatically covered against any sort of accident

that might befall them while traveling. The coverage amounts are:

1.4.3. AGRICULTURAL PRODUCTS

PRODUCTION LOAN:

Financing is available for Major and Minor crops across Pakistan. Main purpose of

financing is to facilitate farmers to purchase Agriculture Inputs such as Seeds, Fertilizers,

Pesticides, Sprayers, hired labor etc.

11

DEVELOPMENT LOAN:

LAND DEVELOPMENT, EQUIPMENTS AND MACHINERY:

Financing for Land Improvement, Water course improvement, Tube wells, Lift pumps,

Deep turbine pumps, Cotton pickers, Godown, Cold Storage, Harvester, Thresher, etc

TRACTOR & VEHICLE FINANCE:

To purchase Tractors, Delivery Vans, Mini Trucks, Motor Cycle and other vehicles used

for marketing Agri Products. Loan Tenure: 1 to 3 years for Motor Cycle, 1 to 7 years for Tractor,

and 1 to 5 years for other 4 wheel vehicles. Other features are:

1.4.4. OTHER SERVICES

UBL E-STATEMENT:

UBL has launched the UBL e-statement facility which makes it easier for customers to

get their statement of accounts and automated transactional debit/ credit alerts right into their

inbox. It is available for all Rupee and Foreign Currency Account holders. UBL statement

facility is:

Absolutely free of cost.

Accessible when you need it.

Security.

Automated transactional debit/ credit alerts.

12

UBL WALLET:

UBL offers ATM and Debit Card facility to all account holders at all UBL

branches anywhere in Pakistan, regardless of whether their branch is online or offline.

UBL Wallet VISA ATM & Debit Card has the entire convenience and security

account holder’s desire and the quality they deserve. This Wallet holds all the cash in

customer’s bank account. UBL Wallet VISA also gives the facility of having up to 9

supplementary cards issued against one primary card. All supplementary cardholders will

be able to conduct ATM/Debit transactions within the limits of the primary card account.

UBL WIZ:

UBL Wiz is

Pakistan’s first ever Prepaid VISA Debit Card that provides the convenience, security

and benefits of an ATM and Debit Card, locally and internationally. More than just an

ATM card, you can use your UBL Wiz everywhere VISA cards are accepted. Whether

you are using it online, paying for petrol, shopping or dining, you are accessing money

directly from your prepaid card, without having to visit the bank.

UBL NETBANKING:

UBL net banking is an

Internet Banking portal offering a simple, convenient and secure method of accessing

Using UBL net banking, the customers have access to their bank accounts 24

hours a day, 7 days a week and can keep a close eye on their account balances, print

account statements, pay bills, transfer funds, track purchases and schedule their recurring

payments at the touch of a button and much more Receive customized alerts.

13

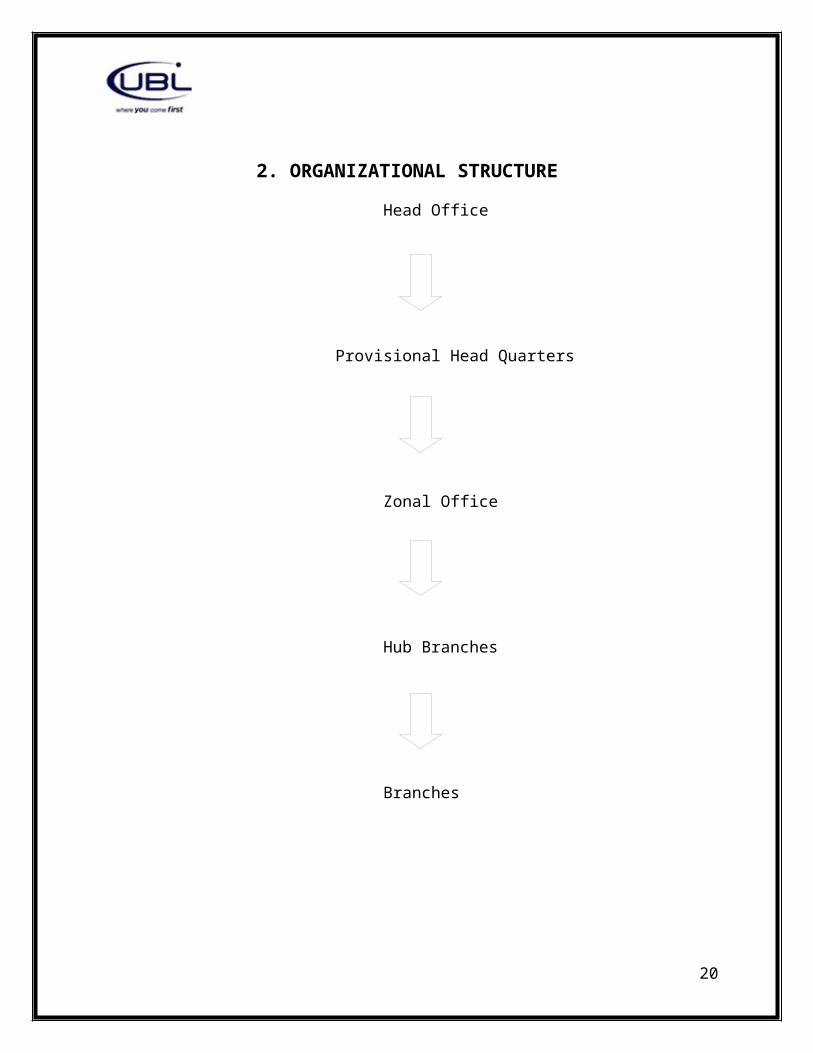

2. ORGANIZATIONAL STRUCTURE

Head Office

Provisional Head Quarters

Zonal Office

Hub Branches

Branches

2.1. Main Offices:

2.1.1. HEAD OFFICE:

The Bank's registered office and principal office is situated at State Life Building No. 1,

I. I. Chundrigar Road, Karachi.

14

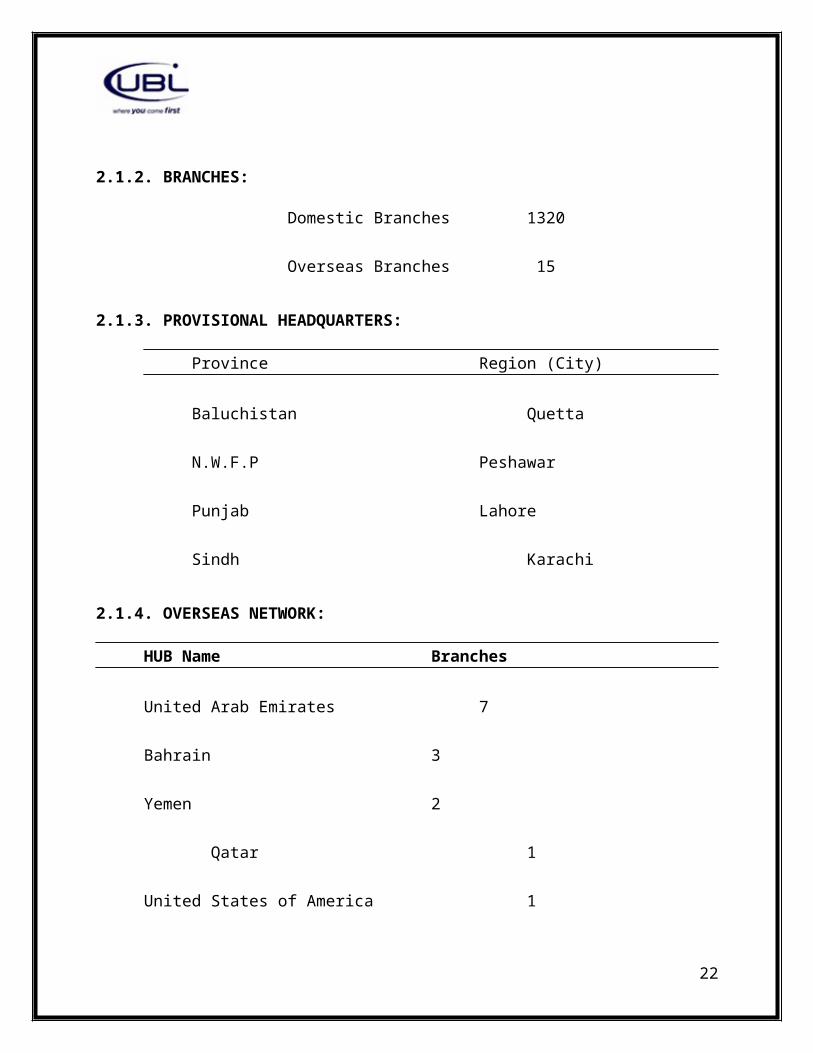

2.1.2. BRANCHES:

Domestic Branches 1320

Overseas Branches 15

2.1.3. PROVISIONAL HEADQUARTERS:

Province Region (City)

Baluchistan Quetta

N.W.F.P Peshawar

Punjab Lahore

Sindh Karachi

2.1.4. OVERSEAS NETWORK:

HUB Name Branches

United Arab Emirates 7

Bahrain 3

Yemen 2

Qatar 1

United States of America 1

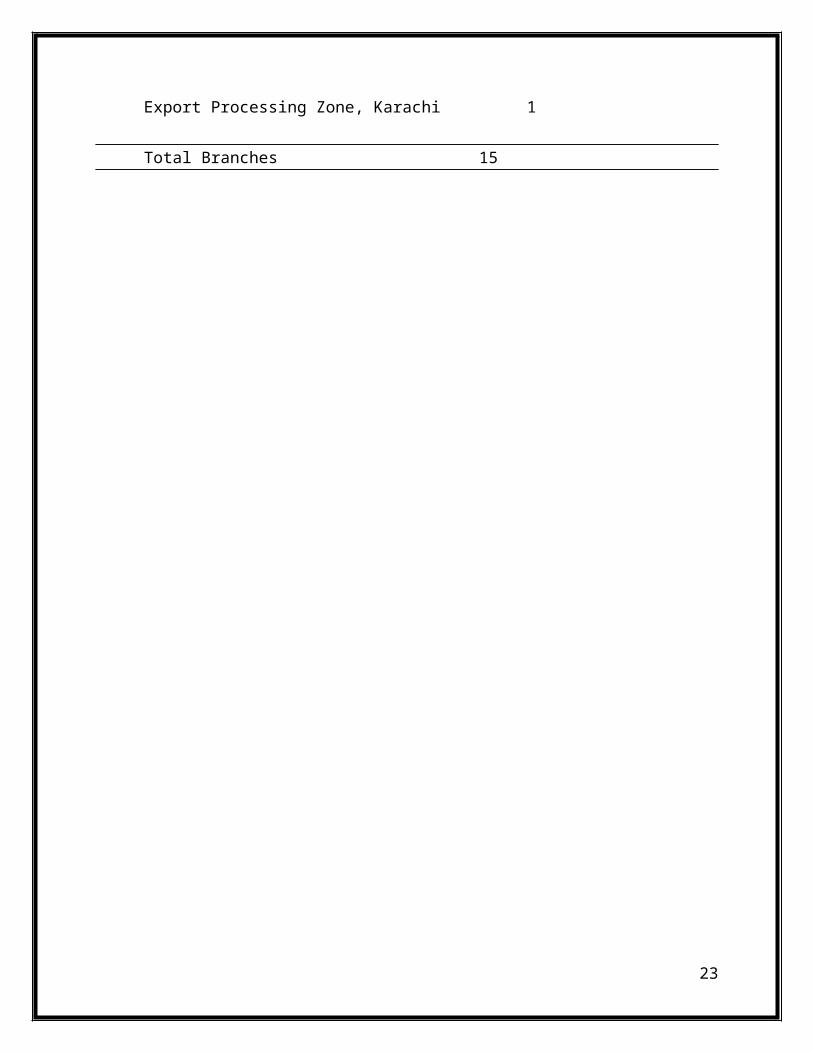

Export Processing Zone, Karachi 1

Total Branches 15

15

2.2. Departments of the UBL

2.2.1 HUMAN RESOURCE DEPARTMENT: (HR)

UBL is the place for you if you are willing to materialize all your deliverables in alignment with

the organization’s holistic vision to grow and excel. Committed and competent work force is the

primary asset in providing value addition to stakeholders of a business organization.

HR Division is responsible for attracting, selecting and recruiting the right people from

the market. UBL is proud of its highly professional, transparent and objective approach in its

recruitment and selection processes. After applying the eligibility criteria, which depends on the

Job grade, a series of selection procedures are applied before hiring employees. Normally the

candidates go through the process of test, group discussion and interview. The Interview is

conducted by a team of internal as well as external professionals of the related area.

Sophisticated recruitment and selection tools like oracle based data management system; online

application and behavioral based interviewing techniques have been introduced.

Consolidation of Bank's budgets, its monitoring and constant review of various financial

indicators. Finance Division works as the back bone for all Banks’ operations.

The Division, which reports directly to the President and Chief Executive of the Bank, has been instrumental in preparation of Bank's business plans and future strategies.

2.2.2 INFORMATION TECHNOLOGY DEPARTMENT:

Operations of UBL have been significantly streamlined post-privatization, however

further plans for improving operational efficiency are under-way. Currently the bank is using

data software called SYMBOL for all its transactions record. This software is utilizing Oracle

Financials at the back end. As all daily banking transactions are stored at the respective branches,

consolidation at the head office takes place at day end.

Information Technology Department is related with all computer activities like to manage

the Central Data Base (CDB) which is placed in Head Office of UBL Karachi in all the daily

transactions in all the branches of the country are up-dated on daily basis. This Department also

makes the web site new news to web site

16

2.2.3 AUDIT DEPARTMENT:

The responsibility of this department is to audit and inspect the operations of the

branches. Either the operations are Regulated by the branches in a right way or not. The Board

Audit Committee (BAC) comprising three members meets every quarter and is responsible,

among other things, for ensuring the effectiveness of the internal audit function and systems for

monitoring compliance.

Internal audit procedures include routine branch and business function audit as well as

special surprise audits. There is also a dedicated compliance division mainly to follow up on the

recommendations advised by the audit team. The deliberations of BAC however reflect concern

regarding the overall control environment. The audit and inspection department has been

highlighting issues with regard to operational control weaknesses at the branch level.

2.2.4 CASH DEPARTMENT :

This is sensitive department of the branch. No other person is allowed to enter in the

premises of cash department. As obvious from name that this department deals in cash deposits

and payments. Cash department is performing its functions/duties manually. For payments and

receipts, it has to maintain certain sheets, books of accounts and various ledgers

17

3. MY LEARNINGS

Standing in the IMS dept. of Bzu, I heard the good news of me having a six week

opportunity to interact with a world class bank. All these six weeks were full of events, full of

learning and most importantly full of professional working. Here 'professional' regards in all

from clerical to managerial work. In these six weeks period, the best thing to me was the

authority and dependency of customers upon me, when they come with a hope that I'm there to

guide them. Knowing all is not learning, the real learning is to convey right. I tried to learn real,

see real UBL, and tried to comprehend the difference between what we look from outside and

what is going on inside.

UBL is full of experienced and professional traditional bankers. As it perfectly suit the

environment we are operating in, you attitude has helped UBL in capturing masses. In the private

sector, no doubt its a fast growing bank, but here's something that's still unrealistic to the policy

makers. The line of unsatisfied customers is increasing, not because we are not serving well, it's

because customers are not understanding the YOU attitude right. Every customer wants to make

sure his work is done at the first convenience, but they are not concerned about the responsibility

with which every employee is working. Back to my real learning’s in my six week internship, I

worked in customer service relationship (CRO) department, as well as in Clearing

department. Because of some work load, I was unable to learn much about other cash and

accounting department. Here is my countdown learning of six weeks.

CLEARING DEPARTMENT:

My initial days at clearing department was the liveliest experience of my internship. Though

physically I was there just to assist the customer service officer, but it turned Out to be much

more for me. That is when I first actually imitated as a presenter of UBL to customers, when to

many people, I'm their hope. Working at Customer Service Department, I did counter with

different types of Customer and filled the deposits slips under the supervision of the officer. It’s

always very important to understand the needs of your customer.

18

.

3.1 Clearing of Cheques:

3.2.1 Outward Clearing:

My experience at Bosan road branch started from the clearing department. Right in the

morning cheques collected from the drop box simply flood over my table. According to all I

learnt through listening, viewing and questioning is summarized below.

3.2.2 Documentation of Consumer Cheques:

All the cheques collected are first categorized into

Credit Cards

Auto Loans

Personal Loans

Cash Line

Verified cheques are then validated before being documented into the drop

box collection sheet for our daily drop box collections record. To anticipate the approval

of cheques, we need to validate some important specifications of all the cheques. They

are:

Date: Cheque should not be post dated or out of date.

Figures: Amount in words and figures should match.

Signature: Drawers signature must be clear.

Intercity: Cheques must not be of other cities. Intercity clearing cheques

for consumer departments are not entertained

Payee’s Name: Payee’s name should be written, and endorsement should

be as per the beneficiary of the cheque.

There should be no over writing in everything penned.

19

All the filtered cheques are then entered into the collection sheet in which

following information is entered.

Cheque No.

Name of bank

Name of Customer

Amount

Document No.

All the documented consumer cheques are then posted into the system. Which I can not

learn due to there security reasons.

3.2.3 Cleared Cheques:

Now the next day when clearing is confirmed by NIFT, respected accounts are debited.

We go into the banking option and in transfer, we debit all the respected accounts. Same is the

case with intercity and OBC cheques.

In documentation, debit and credit vouchers are made, which show total amount of

clearing as per day.

3.2.4 Returned Cheques:

All the cheques which are returned, due to any reason, are then reversed. They are

debited back in the clearing schedule. All the returned cheques are documented in the cheque

return registers and all the account holders of returned cheques are charged with service penalty.

*All the vouchers are signed by the designated officer and all the entries over 50,000 are

supervised.

20

3.2 Remittances Department:

After having experience in clearing department I moved to Remittances department where I

learned that how the transfer of money from one branch to another branch takes place. In this

department I perform following duties.

Cashier’s Cheque

Demand Draft

Security deposits Receipts

Telegraph Transfer

Pay Order

Before going in details I want to explain one thing that comes in mind while performing

remittance activities that is

Suppose if a person has account in UBL Rawalpindi and that person is resident of Multan. How

he/she will deposit money in its account from UBL Multan Branch. I observed this thing and

found that what the procedure to deposit money in his account is. He/she will take online form,

fill it with care and submit in cash management division. Then it will be transfer by cashiers at

the end of the day.

I found it necessary to explain this problem, because I personally handled such type of issues in

branch. Some customers directly filled the deposit slips to deposit it directly in the account but it

is not possible to deposit money directly in another branch account of same bank. Another reason

of explaining it is that first of all I myself was not sure about that what we should do if such type

of transfer is takes place, and it belongs to remittance activities. Now, all other activities that was

learned and handled by me in remittance department are given with detail below.

3.2.1 Cashier’s Cheque (CC) /Corporate Bankers Cheque – CBC

Cashier’s Cheque is a negotiable instrument, which is drawn by one branch to another branch of

the same bank. In case of agency arrangements Cashier’s Cheque can also be issued by one

branch of the bank payable to other branch of the payee bank e.g. CC issued by UBL payable by

UBL.

21

If a person wants to make payment from one city to another city then he/she can make payment

through Cashier’s Cheque. Bank charges a commission for performing this kind of service

according to bank rate schedule, which is revised after six months.

3.2.2 Demand Draft:

DDs are always a secure way of paying remittances in other cities. Both account holders

and walk in customers can avail the facility of DDs. Charges tend to differ for both customers

but the advantage tend to be same. DDs are made in the favor of beneficiary and remitter either

pays in cash or through cheque.

When DDs are issued, head office account is debited and remitters account is credited, on presentation, head office account is credited and beneficiary’s account is debited

3.2.3 Security Deposit Receipts (SDR)

Security deposit Receipts are your safe way of making payments. Not only it’s free of cost for

A/C holders, it also offers you the best liquidity solution as the cash continues to be with you

until and unless your deal gets final and you pay off. In case of cancellation, it's also free of cost

for A/C holders and their amount is returned to their normal account balance.

3.2.4 Telegraph Transfer (TT)

It is just a shape of Cashier’s Cheque. The difference is that it is not drawn on the specified

branch. It can be drawn on any branch of the same bank. The paying bank has to verify the

signatures and after verification payment is made.

3.2.5 Pay order (PO)

Pay-to-order instruments are negotiable checks or drafts that are generally written as "pay to X or order."Payment order is an international banking term that refers to a directive to a bank or other financial institution from a bank account holder instructing the bank to make a payment or series of payments to a third party. These are the Instructions to transfer funds sent via paper and/or electronic means". A form is filled up for pay order when money move within the city the party made pay order. Pay order is issued and played by the same branch

22

.

4. FINANCIAL STATEMENTS, VERTICAL AND TREND ANALYSIS

23

4.1 Vertical and Trend Analysis

24

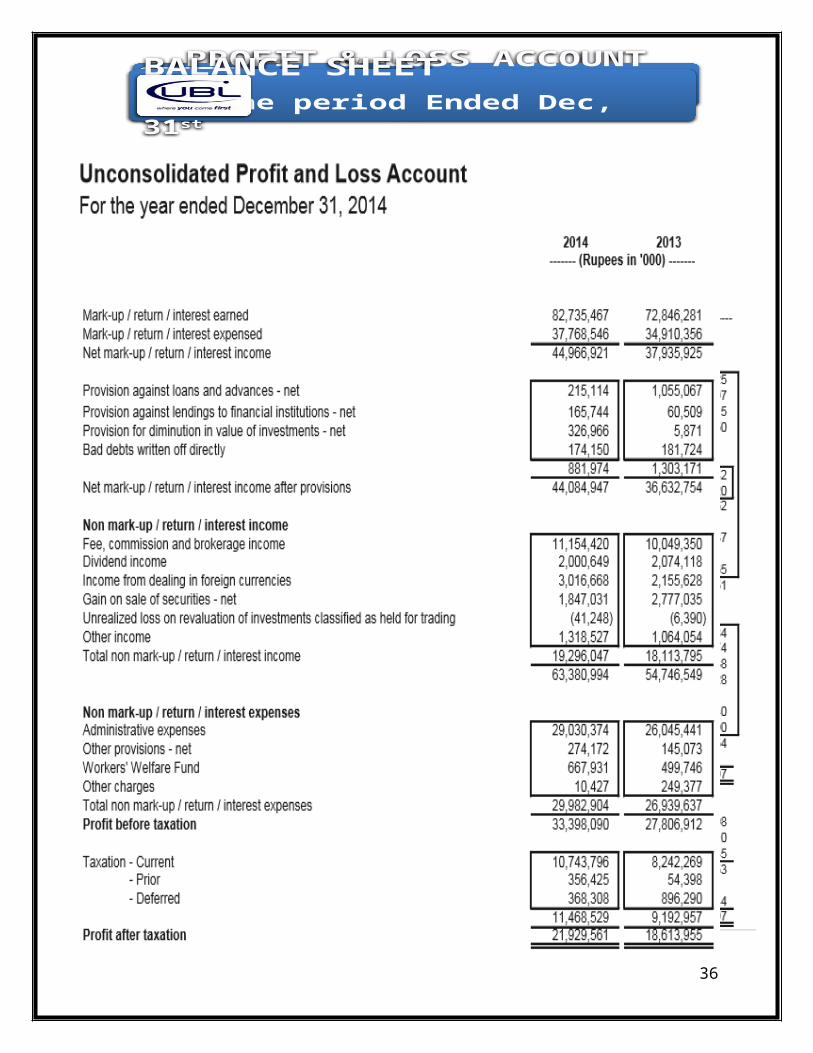

PRO FIT & LO SS A CCO U N TFor the period Ended D ec, 31 st

BALANCE SHEETFor the period Ended Dec, 31 st

Assets 2014 %

2013%

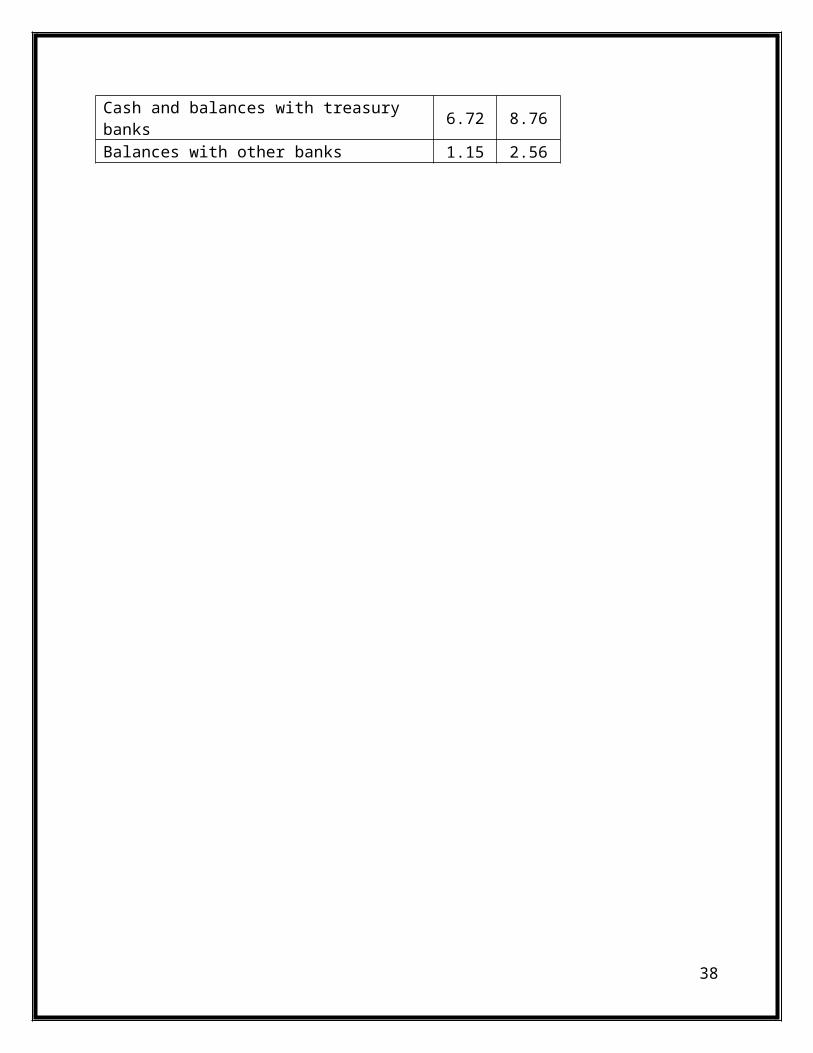

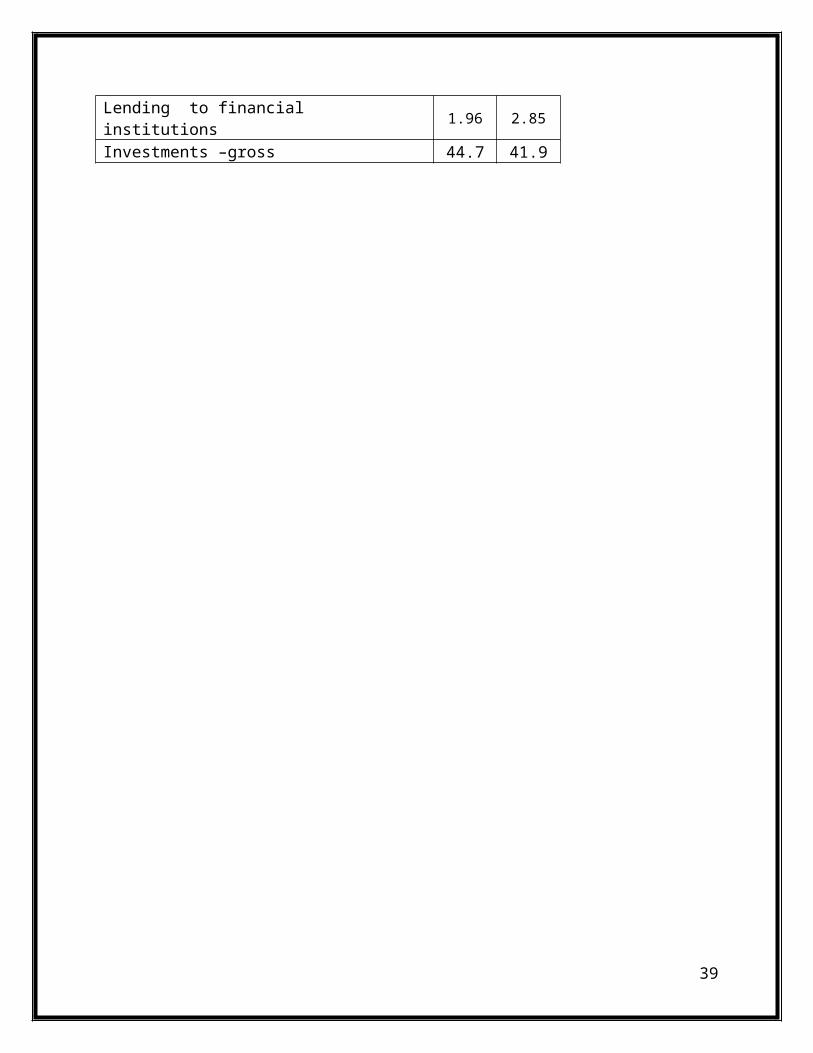

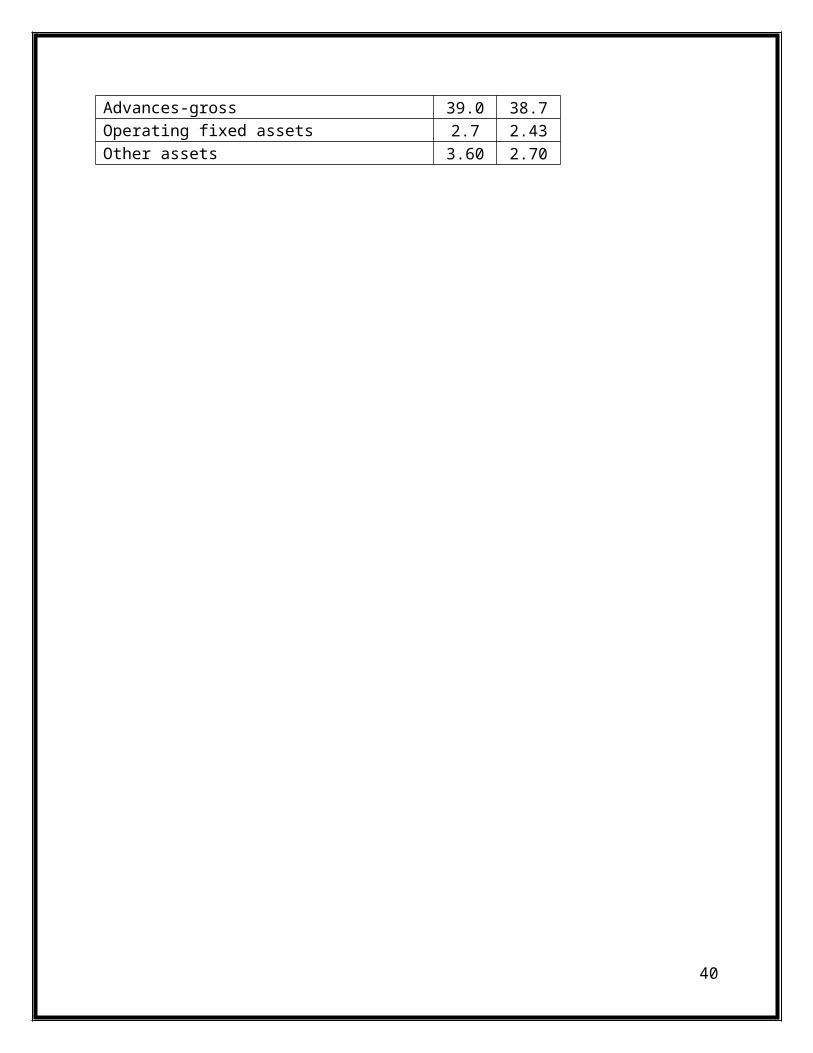

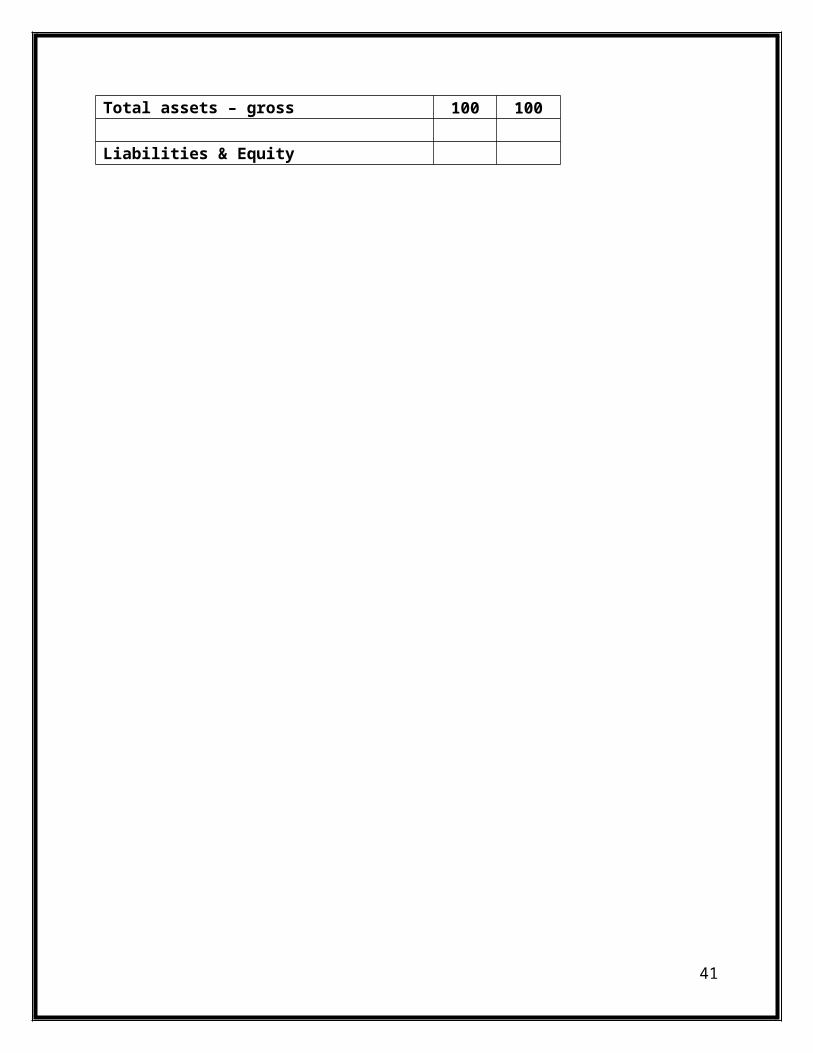

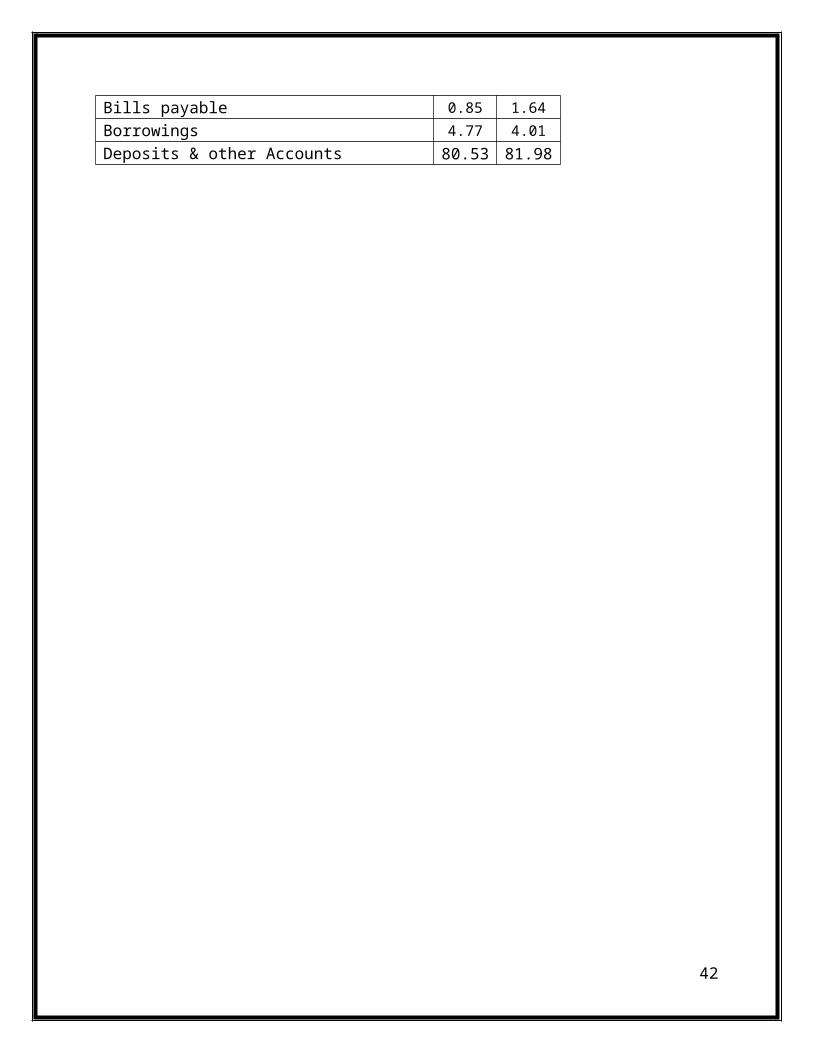

Cash and balances with treasury banks 6.72 8.76Balances with other banks 1.15 2.56Lending to financial institutions 1.96 2.85Investments –gross 44.7 41.9Advances-gross 39.0 38.7Operating fixed assets 2.7 2.43Other assets 3.60 2.70Total assets – gross 100 100

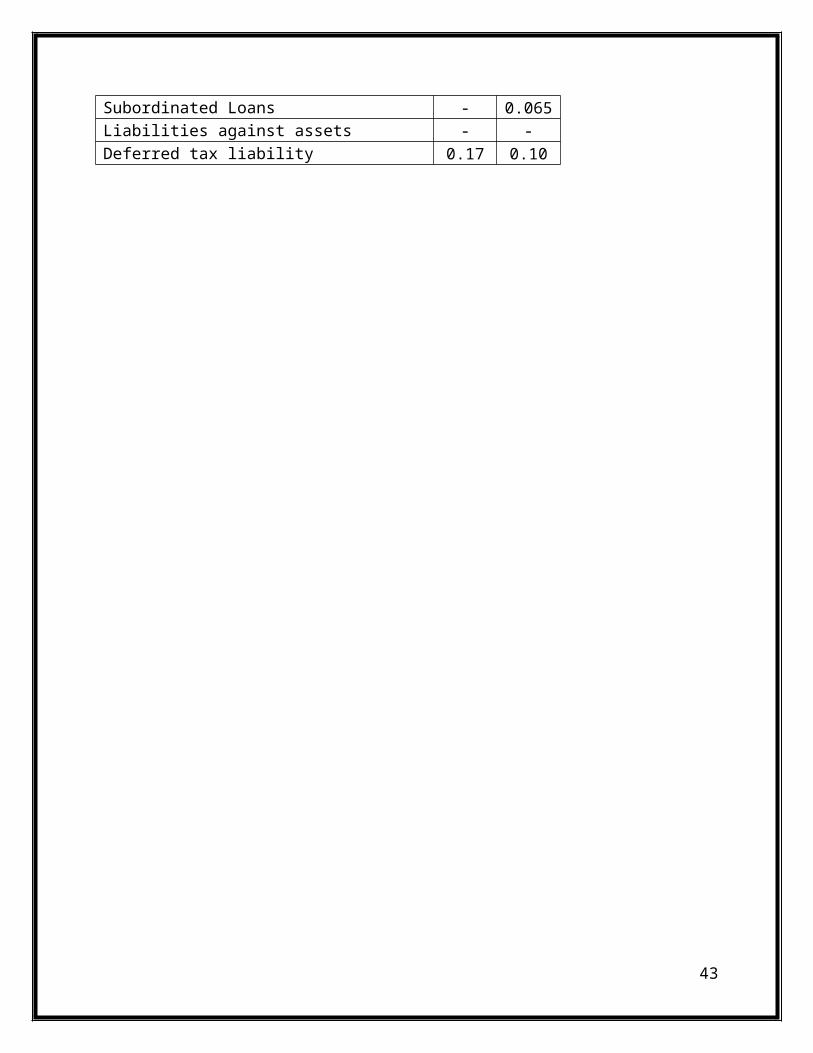

Liabilities & EquityBills payable 0.85 1.64Borrowings 4.77 4.01Deposits & other Accounts 80.53 81.98Subordinated Loans - 0.065Liabilities against assets - -Deferred tax liability 0.17 0.10Other liabilities 2.36 2.18EquityShare capital 1.10 1.21Reserves 3.07 3.33Unappropriated profit 4.33 4.22Surplus on revaluation of assets 2.78 1.22Total liabilities & equity 100.0 100.0

25

BALANCE SHEETVertical Analysis

26

BALANCE SHEETTrend Analysis

Profit & Loss AccountsVertical Analysis

Assets 2014 %

2013%

Cash and balances with treasury banks 84.3 100Balances with other banks 49.8 100Lending to financial institutions 75.8 100Investments-gross 117.3 100Advances-gross 111.1 100Operating fixed assets 123.1 100Other assets 146.6 100Total assets – gross 110.0 100.0

Liabilities & EquityBills payable 57.5 100Borrowings 130.7 100Deposits & other Accounts 108.1 100Subordinated Loans - 100Liabilities against assets - 100Deferred tax liability 174.6 100Other liabilities 119.2 100Total Liabilities 105.5 100Net Assets 124.3 100EquityShare capital 100 100Reserves 101.3 100Unappropriated profit 113.0 100Surplus on revaluation of assets 106.8 100Total liabilities & equity 100.0 100.0

Profitability 2013%

2012%

Markup/return/interest earned 80.09 81.10

Markup/return/interest expensed 48.25 48.04

Net Markup/Interest income 32 33

Fee, commision, brokerage and exchange income 13.42 11.06

Capital gain & dividend income 5.33 3.45

Other income 1.17 4.39

Noninterest income 20 19

Gross income 52 52

Administrative expenses and other charges 36.93 33.41

Profit before provisions 15 19

Donations 0.11 0.05

Provisions 2.00 6.18

Profit before taxation 13 12

Taxtation 12.71 12.32

Profit after taxation 26 25

Total Income 100 100

Total Expense 100 100

27

Profit & Loss AccountsTrend Analysis

Profitability 2014%

2013%

Markup/return/interest earned -0.9 4.3

Markup/return/interest expensed -0.1 12.6

Net Markup/Interest income -1.6 -2.2

Fee, commission, brokerage and exchange income 21.7 11.1

Capital gain & dividend income 54.7 148.3

Other income -73.2 63.6

Noninterest income 5.7 34.7

Gross income 0.6 6.8

Administrative expenses and other charges 9.9 19.4

Profit before provisions -6.5 -1.3

Donations 120.0 -35.2

Provisions -67.8 -40.2

Profit before taxation 3.6 10.8

Taxation 2.6 2.7

Profit after taxation 4.0 15.4

Total Income 0.4 9.0

Total Expense -0.6 7.5

5. RATIO ANALYSISRatio analysis is very helpful to the management of the organization as well as for the

investors and creditors. Investors keep an eye on the bank’s financial statement and make

28

decisions whether to invest funds in that bank or not. Similarly a creditor also analysis the financial statements and makes decisions whether to grant loan or not.

5.1. Liquidity Ratios:

Liquidity ratios means to measure short term solvency of the company. Ability of the company to pay off its short term debt. Following ratios are calculated in order to measure the short term solvency of the company

5.1.1Current Ratio:

Current Assets: Cash and balances with treasury and other banks + lending to financial institutions + Investment + Advances

Current Liabilities: Deposits & other Accounts + Borrowings from financial institutions + Sub-ordinate loans + Bills Payable

YEARS 2014 2013 2012 FORMULA

Current Ratio 1.12 1.13 1.14 Current Assets / Current Liabilities

Asset Turnover 0.04 0.03 0.04 Markup Revenue / Total Assets

Debt to Asset 1.13 1.12 1.01 Total Debt / Total Assets

Debt to Equity 11.2 9.99 10.2 Total Equity / Total Assets

Coverage Ratio 0.8 0.79 0.76 EBIT / Interest Expense

Gross Profit ratio 26.5% 25.5% 15.4% Gross Profit / Revenue * 100

Net Profit Margin 14.7% 6.0% 6.8% Net Profit / Revenue * 100

Return On Asset 2.1% 2.0% 2.1% Net Profit / Total Assets * 100

Return On Equity 23.9% 22.3% 23.8% Net Profit / Total Equity * 100

Advances to Deposit Ratio 48.5% 47% 40.2% Advances / Deposits * 100

Investment to Deposit 55% 51.% 45% Investment / Deposits * 100

Cash Ratio 9.1% 12.9% 13.9% Cash / Current Liabilities * 100

Calculations:

29

Investment to deposits: Investment/deposits

In 2013 423777250/827847738*100=51%

In 2014 497334002/895083053*100=55%

Advances to deposits: Advances/deposits

In 2013 390813462/827847738*100=47%

In 2014 434264050/895083053*100=48.5%

Gross Profit ratio: Gross Profit / Revenue*100

1n 2013 18613955/72846281=25.5%

1n 2014 21929561/82735467=26.5%

5.2 Activity Ratio

Activity ratios measure a firm’s ability to convert different accounts within their balance sheets into cash or sales -inflows or outflows.

Total Assets Turnover The total asset turnover indicates the efficiency with which the firm uses its assets to generate revenues.

Interpretation:

Turnover means how many times we make the revenues during the year as compare to our total assets. This trend of increasing ratio in 2014 means the more efficiently its assets have been used.

5.3 Debt Ratio:

The debt ratio measures the proportion of total assets financed by the firm’s creditors.

Interpretation:

Debt to asset ratio means higher ratio in 2014 the greater the bank’s degree of indebtedness.

5.3.1 Coverage Ratio

The firm’s ability to make contractual interest payments. The higher the ratio , the better able the firm is to fulfill its interest obligations.

30

5.4 Profitability Ratio:

Profitability ratios measure the earning ability of the firm. Following ratios are calculated:

Net Profit Margin Return on Assets Return on Total Equity Gross Profit Margin

Total Revenue = Markup/Return/interest earned

5.4.1 Gross Profit Margin

Interpretation:

Gross profit margin on year to year basis is increasing. It also shows that United Bank also expending his business that’s why its gross income is increases.

5.4.2 Net profit Margin:

Interpretation:

Net Profit margin in the Year 2013 is 25% and 2014 is 26.5% respectively which shows increase in Net Profit margin in this year. Net Profit Margin is to a reasonable extent i.e. return on sales after payment of tax.

Net Profit = profit after taxation

5.4.3 Return on total Assets

Interpretation:

As for as Return on total Assets is concerned, in the year 2012 it is 2.0%, and in the year 2014 is 2.1% which depicts that return on total assets is much Higher as compare to last year.

5.4.5 Return on Total Equity:

Interpretation:

Return on Equity mean’s how much earn on Equity in the year 2013 is 22.3%, and in the year 2014 is 22.9% which shows an increasing trend this year.

31

32

Return on Assets

GRAPHICAL REPRESENTATIONS OF RATIOS:

Current Ratio

Asset Turnover Ratio

Debt to Assest Ratio

0 0.2 0.4 0.6 0.8 1 1.2

2014 2013 2012

Debt to Equity

Gross Profit

Net profit Margin

Cash Ratio

0 2 4 6 8 10 12 14 16 18 20

2014 2013 2012

33

Advances To Deposite

Investment to Deposite

0 10 20 30 40 50 60

2014 2013 2012

NOTE:

All the ratios are calculated on the basis of data published in United Bank annual reports 2012 to 2014. Balance sheet, profit & loss account (Income statement) are taken as it is as published in annual reports. All the amounts of these statements are taken into Millions. Errors and omissions can be omitted.

34

6. SWOT ANALYSIS:SWOT is useful tool for providing a framework for analysis of an organization. SWOT

stands for Strengths, Weaknesses, Opportunities and Threats. It is a common approach to make

assessments in terms of internal and external environment of the organization, and to formulate

strategies analyzing its internal strengths and weaknesses, external opportunities and threats,

coming up is the SWOT analysis for the UBL.

6.1 STRENGTHS:

It has a well-knitted and adequately equipped branch networking system that efficiently

covers both the domestic and international markets.

It is involved in both corporate and retail banking.

Advances investment of the bank shows a constant growth pattern.

The bank is owned by parties of financial repute and credit worthiness like, SBP, Best

Way group and Abu Dubai group. Others are GOP, NBP Trustee Department, State Life

Insurance Corporation etc.

UBL is actively participating in international markets and has recently introduced credit

cards in UAE, Bahrain, and Qatar, being backed up by 24 hours call center out of UAE.

The bank is run by highly professional recruited from and trained by foreign banks like

City Bank.

35

6.2 WEAKNESSES:

Due to risks such as political, economic and legal etc the bank has suffered losses the

main reason was that of piling up of large amount of unrecoverable loans and debts

which have adversely affected the image of the UBL.

Accumulated losses pushed the bank to cut down its promotional activities in order to

reduce expenses for last few years.

During the nationalization life span of the bank political lords used influence in bank

business and selection of employee at each level and thus adversely affected the bank’s

efficiency and effectiveness.

Promotions are carried out on annual basis ignoring the importance of capabilities and

performance outputs.

The bank has large number of employees who are simple graduates with no banking

knowledge.

Unsatisfactory working conditions. Employees don’t promotion for many years

HRM is not much effective and active in the bank. Every branch must have

one HR counter

6.3 OPPORTUNITIES:

Growing policies of the GOP on business and economic sectors provide UBL an

opportunity to efficiently meet with the business people requirements of instant cash

facilities e.g. the government intentions of developing housing and agriculture sectors.

The efficiency of stock market and sound exchange reserve level is providing a good

opportunity for effective investment decisions.

36

Foreign remittances are another area as present worldwide control systems over transfer

of currencies through illegal channels has facilitated the area for the banks.

Reconstruction of Afghanistan is a golden opportunity where the bank can effectively

participate.

37

There is a large pool of unemployed MBAs who can be hired to achieve professionalism

on its organizational culture.

Outsourcing of promotional companies or use of available excellent promotional

facilities.

Entering new market segments.

Increase the product range to meet the broader range of customers’ needs.

6.4 THREATS:

Increase in competition due to increasing number of foreign and domestic private banks

offering highly specialized and attractive services.

Growing global technological advancements and adaptation of modern style of

management in banking sectors.

Extensive promotion campaigns run by competitors.

Unemployment, lower level of income and prices like problems in the motherland

coupled with low rate of industrialization, geo political adverse conditions, religious

factor, lack of consistency in policies due to political instability are some of the other

major threats.

This SWOT analysis is a mirror image of the bank’s present conditions. Some efforts are

made and others are still required to be made in order to improve the situation. The

management can develop elaborate strategic plans for capitalizing the available

opportunities. The bank should maintain principal of professional management and adhere to

sound and sophisticated banking rules and regulations so that confidence and trust of the

public in the institutions could be re earned.

38

7. PEST ANALYSIS

7.1 POLITICAL

Pakistan despite all international and public perceptions, today is a functioning

democracy and gradually there is a change in complexion and composition of legislatures

with more educated people and women (27% of National Assembly and17% of Senate)

entering into politics Similarly it helps in designing best strategies to implement that

could support the revival of bank industry. Like in the era of nationalization banks had to

suffer as other industries that’s why that impact is still found in the performance of this

industry.

7.2 ECONOMICAL

Although banking sector development is important at the early stage of economic

growth, general liberalization presuming a homogeneous bank role may not necessarily

promote growth. The estimated cost structure indicates that state-owned commercial

banks are large enough, while development financial institutions and private banks can

expect to obtain cost-saving advantages by expanding their operations. Since scope

economies are significant, portfolio diversification generally increases bank profits. In

addition, privatized banks are the most efficient, followed by foreign and

private banks. Public banks are the least efficient.

7.3 SOCIAL

Banks always helped people in improvement of living condition of poor people in

various forms like giving loans to poor for starting business or directly providing them

the instruments that could enhance their living conditions. Similarly UBL always tried

to provide the needy people loans on soft terms and helped also to decrease

unemployment by providing job opportunities.

39

7.4 TECHNOLOGY

The Banking sector in Pakistan has experienced a rapid transformation. Just about

a decade back this sector was limited to the Sarkari (nationalized) and co-operative

banks. Then

came the multi-national banks, but these were confined to serving an elite few. One could regard

the past as the medieval ages in the banking industry, wherein every branch of the same bank

acted as an independent information and multi-channel banking (ATMs, Net banking, Tele-

banking, etc) was almost non-existent. Today banks have to look much beyond just providing a

multi-channel service platform for its customers.

8. RECOMMENDATIONSRecommendations are considered to be the most important part of an internship

report, without which no report is considered complete and meaningful. This part of the

report is based on the previous sections i.e. review and analysis. Moreover, for bringing

suggestions, discussions have been conducted with the staff of UBL officers, who not

only provided the basis for recommendations but also pointed out some areas, where the

change for the development is utmost important. Realizing the importance of this section,

efforts have been made to give feasible recommendations, which are categorized under

the following headings.

Adopt Pro-Active Approach

UBL management should adopt proactive to survive in this sector. What I have observed is that

UBL management is having reactive approach means that they react to the situation that their

competitors have created. UBL should try for new innovative ideas rather than moving on the

same track that their competitive are doing.

Basis for Promotion:

A sizeable portion of the officers of UBL, are promoted in without test and interviews

to officers.. The promotion policy must be too tight and transparent that no one may have

40

the chance to be promoted on criteria other than the required qualification, experience

and performance. As for the present excess staff, those not found up to the required

criteria, may be given GHS etc .

Needs of change in Recruitment Policy:

It is important to say that the external level market is full of the required talent like

MBA, M. Com etc,. But on the country only graduation with simple subjects is still the

requisite qualification for officer’s cadre, which has already worked amply in the

devastation of UBL. Therefore the recruitment qualification to the officer’s framework

should be enhanced for simple graduation, to professionally qualify preferably Masters in

their respective fields.

Customers Orientation:

Every entrepreneur if concerned about the success of his business has to

understand, recognize, carefully and appropriately that his customer is “The King” of the

business system and the original spring of the business revenue. UBL should recognize

its customers as the

mainstream of the bank’s revenue. They need to be provided the deserved respect, quality and in

time service and to be politely dealt with.

Proper Documentation:

Loans become irrecoverable through court of law in case of default when the bank

fails to prove their claims against the delinquent borrower. If documents are obtained

properly as per terms of the loan it is not difficult for the counsel of the bank to get

decree against the defaulter. For proper and valid documentation the following aspects

must be kept in mind.

I. The bank should confirm that standard loan documentation is in place for each credit

facility prior to disbursement. If the documents required are different from the bank’s

standard approved format, arrangement for vetting of the legal counsel.

II. Bank should ensure that the documentation are correct, complete and correspond with the

approved facilities. Also to ensure that blank spaces are filled, documents are dated,

41

signed and stamped, the signer is authorized to execute such documents and signatures

are verified.

III. Maintaining computerized record of documentation.

IV. Division of documentation on the basis of sector, to which loan is given.

42

43

44

10. REFERENCES

Annual Report of the United Bank, limited 2012.

Annual Report of the United Bank, limited 2013.

Annual Report of the United Bank, limited 2014.

James C. Van Horne, 2000. Financial Management. www.ubl.com.pk

45