uae real estate review - q1 2015 · uae real estate review - q1 2015 ... villas and high end units...

TRANSCRIPT

Interested to know more? Please read on…

Executive Summary:

Please find below a quick snapshot of the key topics covered in this note:

Pricing trends - Sales

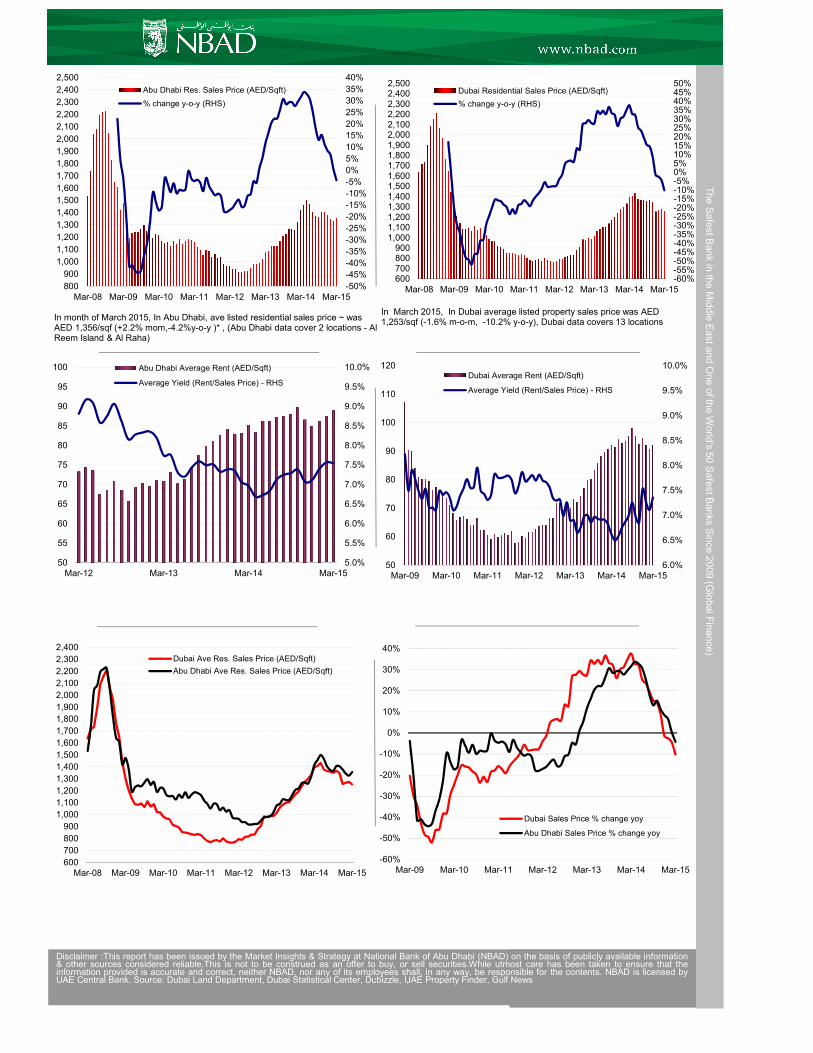

In March 2015, average listed property sales prices in Dubai declined to AED 1,253 /sqf (-1.6% m-o-m, -

10% y-o-y). Sales activity slowed down in the fourth quarter of last year. In 2014, annual average sales

prices increased 21% y-o-y, however it is expected to drop by circa 15% in 2015 based on current data.

Pricing trends - Rentals

In March 2015, average listed property rents in Dubai increased by 1.8% m-o-m, but remained stable

year on year. Average rents increased by 21% during 2014, however they are expected to decline by circa

10% y-o-y by the end of 2015.

Who’s buying Dubai residential property?

In the first quarter of 2015, UAE nationals were the largest buyers, representing 24.2% of the total value of

Dubai residential property transactions, while Indian nationals were the second largest investor group

(accounting for 14.2% of the total), and British nationals third representing 7.9%.

Supply dynamics

According to the available data, in Dubai there are currently 370,000 residential units that are already

completed. By the end of 2015 an additional 40,000 units are expected to be completed and hence the

aggregate residential unit stock is expected to reach 410,000 units. Judging by the number of cranes in

Dubai, the supply is unlikely to ease off anytime soon! Clearly this will likely keep the pressure on prices.

Recovery since the 2008 financial crisis

After falling more than 65% since their peak prices in Q3 2008, average Dubai residential prices in March

2015 were around 40% below the peak values, having recovered significantly since the market bottomed

out. Villas and high end apartments seem to be the units of choice in the first quarter of 2015, with prices

in locations such as Arabian Ranches currently around 31.6% less than the peak values, while Jumeirah

Lake Towers pricing is around 22.5% less than peak values.

UAE Banking Sector -Factors relevant to real estate

Pre-Crisis in 2008Q3, so-called "hot money" was flowing into UAE banking system. There was excess

liquidity, annual lending growth exceeded 40% during 2007-2008. Mortgage Loan to Value ratios exceeded

95%, off plan sales and financing was the common practice. Loan to Deposit ratios were above 110%, but

are currently at around 91%.

UAE Real Estate Review - Q1 2015

Regulatory and other factors

The Dubai Government announced that they are considering clamping down on the flipping of off-plan

properties and possibly introducing extra fees and implementing new restrictions on such activity, in an

attempt to further curb speculators. Exact details weren't announced about the fee structure, but it could

possibly be a new system that would charge flippers on a sliding scale, based on how long they had held

the property. One possible method is to introduce some sort of stamp duty.

Economic Outlook

Dubai economy experienced sustainable growth in recent years. In 2014 GDP of Dubai is estimated to

have grown by 4% driven by real estate, trade, tourism and reached almost US$ 99.5 billion (25% of UAE

Nominal GDP). Highest since 2007. Business outlook remains positive. In 2015, GDP of Dubai is

estimated to grow by around 4% again mainly driven by trade, real estate & tourism.

For Abu Dhabi, average listed residential sales price declined to AED 1,355/sqf in March 2015 (2.2% mom,

-4.2% y-o-y). In 2014, annual average sales prices increased 22.5% y-o-y, and on average are expected to

drop by around 10-15% in 2015.

For Abu Dhabi, average listed residential rents declined 2% m-o-m in March, and increased slightly by 1%

y-o-y. In 2014, average annual rents increased by 13.8%, however by the end of 2015 a decline of around

5% y-o-y is expected.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information &other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, UAE Property Finder, Gulf News, Dubizzle.com

The Safest B

ank in th

e Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information& other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, Dubizzle, UAE Property Finder, Gulf News

The Safest B

ank in th

e Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

50

60

70

80

90

100

110

120

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Average Rent (AED/Sqft)

Average Yield (Rent/Sales Price) - RHS

In month of March 2015, In Abu Dhabi, ave listed residential sales price ~ was AED 1,356/sqf (+2.2% mom,-4.2%y-o-y )* , (Abu Dhabi data cover 2 locations - Al Reem Island & Al Raha)

In March 2015, In Dubai average listed property sales price was AED 1,253/sqf (-1.6% m-o-m, -10.2% y-o-y), Dubai data covers 13 locations

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Ave Res. Sales Price (AED/Sqft)

Abu Dhabi Ave Res. Sales Price (AED/Sqft)

-60%-55%-50%-45%-40%-35%-30%-25%-20%-15%-10%-5%0%5%10%15%20%25%30%35%40%45%50%

600700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,8001,9002,0002,1002,2002,3002,4002,500

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Residential Sales Price (AED/Sqft)

% change y-o-y (RHS)

-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Abu Dhabi Res. Sales Price (AED/Sqft)

% change y-o-y (RHS)

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

50

55

60

65

70

75

80

85

90

95

100

Mar-12 Mar-13 Mar-14 Mar-15

Abu Dhabi Average Rent (AED/Sqft)

Average Yield (Rent/Sales Price) - RHS

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Sales Price % change yoy

Abu Dhabi Sales Price % change yoy

Source: Dubai Land Department, RERA

Investment Value By Nationality (AED) 2014

Source: Dubai Land Department, RERA

Dubai Residential Units Available & Future Supply

Source: Jones Lang Lasalle

According to Dubai Land Department

(DLD) in 2015Q1, UAE nationals took the

lead with investments worth 24.2% of the

total up from 20.7% in 2014, Indians were

second with investments worth 14.2%

down from 16.5% in 2014. British nationals

came third with investments worth 7.9%.

GCC nationals constituted 37.5% of the

total investment value up from 29% in

2014. Overall Arab nationals constituted

50% of total investment value - up from

40% in 2014. This is a serious jump from

previous year and demonstrates that GCC

nationals are focused more on Dubai.

Investment Value By Nationality (AED) 2015Q1

One of the possible reasons for this is the

ongoing turmoil and geopolitical unrest in

the broader Arab world which is driving

many people to have primary or secondary

homes in Dubai, especially as it is widely

regarded as a much more safe and stable

place to live, relative to many other cities in

the region

In June 2014, Dubai's Land Department

announced that "Growth in real estate

demand has been due to an improving

economy, not speculation". The

announcement came soon after the IMF

and Central Bank UAE warned that the

property market might be overheating.

According to JLL there are currently

390,000 residential units that are already

completed, by the end of 2015 the total

count is expected to surpass 410,000

units. With the pace of additional supply

seemingly relentless, there are clearly

concerns about imbalance in the supply-

demand dynamics of this market.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information &other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, Dubizzle, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

UAE24.17%

GCC exc. UAE13.33%

Non-GCC Arabs12.50%

India14.17%

UK7.88%

Pakistan5.80%

Iran2.64%

Russia2.12%

Other Non-Arabs17.39%

250

260

270

280

290

300

310

320

330

340

350

360

370

380

390

400

410

420

2009 2010 2011 2012 2013 2014 2015F

Future Supply (000)

Available (000)

UAE20.70%

GCC exc. UAE8.39%

Non-GCC Arabs10.91%

India16.47%

UK8.47%

Pakistan6.90%

Other Non-Arabs28.17%

Population growth vs Supply of residential units (Rebased to 100)

Source: Dubai Land Department, RERA, Dubai Statistical Center

Residential Rents/Price Decline 2015Q1 from peak in Q3 of 2008

Source: NBAD Real Estate Database

Lowest point in Rental/Sales Prices vs Peak in Q3 2008

Source: NBAD Real Estate Database

As we can see the supply of residential

units more than doubled since 2008, while

population increased by a more modest

50%, equivalent to circa 800,000 people.

The gap between the two lines indicates

that the supply is growing faster than the

population - however it is important to bear

in mind that people residing outside of

Dubai are also investing in such residential

units, and hence this could to some extent

mitigate an element of any potential over-

supply.

After faling more than 65%, in March 2015,

Dubai average residential prices were

around 40% less than peak values of

2008Q3. Villas and high end units were

the preferred types, prices in locations

such as Arabian Ranches are currently

around 32% less than the record values,

Jumeirah Lake Tower residential sales

price is around 22.5% less than peak

values.

The adjacent graph shows the lowest point

in rents and sales price since their peak in

Q3 2008. In some areas rents and sales

price dropped by as much as 75%. The

Dubai real estate market, after declining

for more than 40 months since its peak

values in around Sept 2008, started to

recover in May 2012, while the recovery in

Abu Dhabi started much later, in around

January 2013.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information &other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, Dubizzle, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Arabian Ranches

Dubai Land

Palm Jumeirah

JBR

JLT

Dubai M

arina

Sports City

Business Bay

International C

ity

D.T. B

urj D

ubai

The Greens

DIFC

% Change in Rent Since 2008Q3

% Change in Sales Price Since 2008Q3

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Arabian Ranches

Dubai Land

Palm Jumeirah

JBR

JLT

Dubai M

arina

Sports City

Business Bay

International C

ity

D.T. B

urj D

ubai

The Greens

DIFC

Lowest Rent Since 2008Q3 Peak

Lowest Sales Price Since 2008Q3 Peak

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

2008 2009 2010 2011 2012 2013 2014 2015F

Population Dubai Residential Supply

Dubai Residential Transactions Volume 12MSum(AED Bn)

Source : Knight Frank

Dubai Property (Comm + Res + Land) 12M Sum (AED Bn)

Source: Dubai Land Department

In March 2015, residential property

transactions, on a 12mth cumulative basis,

declined to AED36 billion (-18% yoy) but

the latest monthly data indicates that the

sales volume may be gradually picking up.

Mortgage transactions currently constitute

36% of total, up from 20% in July 2009.

This clearly indicates that investors have

access to loans, market sentiment is

improving, and banks are indeed lending.

However, it is still noteworthy that despite

this change, circa 64% of all residential

transations are still on a cash basis (i.e.

close to two thirds of the total value of

residential transactions are done with cash

and without any mortgage involved).

Property sales volumes had been

increasing from 2011 to Q1 2014, when

they peaked and sales activity showed

signs of slowing down in last quarter of

2014. Most recent monthly data from

2015Q1 indicates there may be a slight

revival in activity.

The Dubai Real Estate Investor Law

(Tanweer) aims to minimize legal disputes

and protect investors' rights. DLD also

increased the transaction tax on real estate

from 2% to 4% and this shows the

government's intention to reduce the

amount of speculative activity. The market

still has some degree of speculation in it,

but the Real Estate Regulatory Authority

and the UAE Central Bank have been

implementing counter measures which

have led to the regulatory environment

being much better than the 2008 period.

The new regulations require that

developers deposit between 30% and 40%

of the total construction costs in escrow

account before any pre-sales. In addition,

developers are required to have 100%

ownership of their land. These measures

are designed to protect the investors and

generate greater confidence and comfort

among those looking to invest in this

market. Additional details of the

regulations imposed are shown at the back

of this report.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information& other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Cenler, Dubizzle, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

40

45

50

55

60

Jul-09 Dec-10 May-12 Oct-13 Mar-15

Residential Mortgage Sales Volume (12M Sum)

Residential Cash Sales Volume (12M Sum)

% change y-o-y (RHS)

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0

20

40

60

80

100

120

140

160

180

200

220

240

260

M-04 M-05 M-06 M-07 M-08 M-09 M-10 M-11 M-12 M-13 M-14 M-15

Property Mortgage Volume (12M Sum)

Property Cash Sales Volume (12M Sum)

% change y-o-y (RHS)

Dubai Population Pyramid By Gender 2013

Source: Dubai Statistical Center (DSC)

Dubai Population By Nationality

Source: Dubai Statistical Center (DSC), National Bureau of Statistics (NBS)

Source: NBAD Real Estate Database

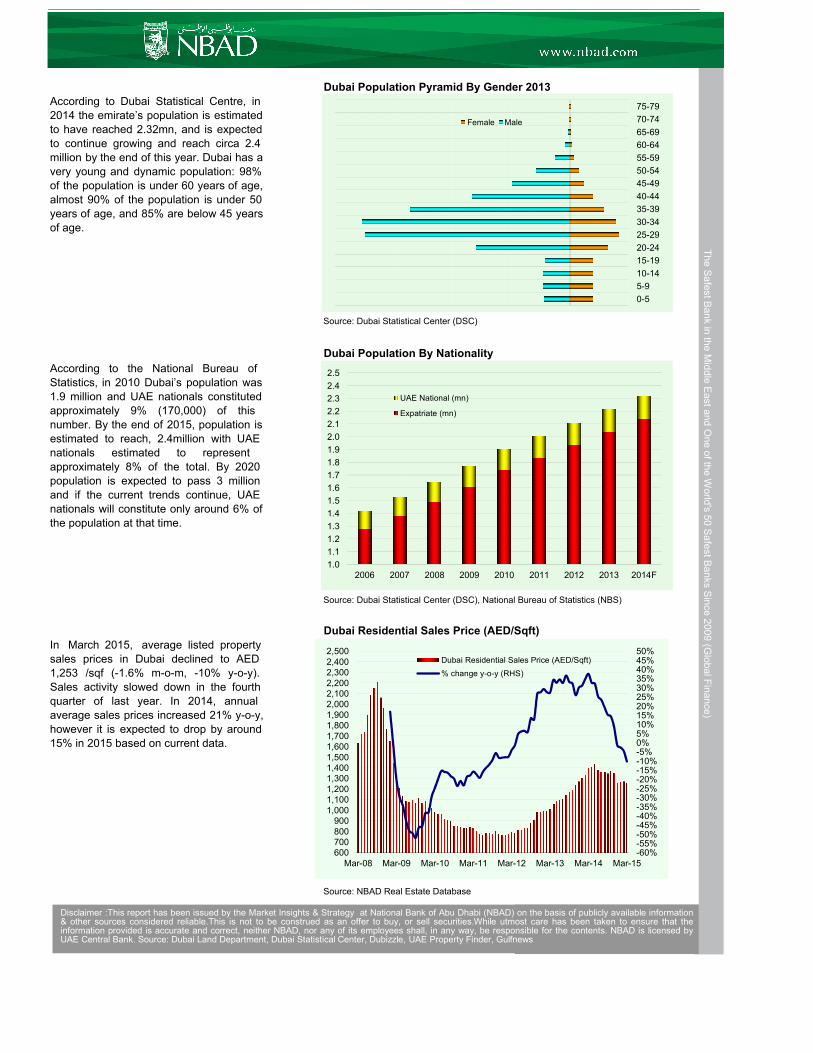

In March 2015, average listed property

sales prices in Dubai declined to AED

1,253 /sqf (-1.6% m-o-m, -10% y-o-y).

Sales activity slowed down in the fourth

quarter of last year. In 2014, annual

average sales prices increased 21% y-o-y,

however it is expected to drop by around

15% in 2015 based on current data.

According to the National Bureau of

Statistics, in 2010 Dubai’s population was

1.9 million and UAE nationals constituted

approximately 9% (170,000) of this

number. By the end of 2015, population is

estimated to reach, 2.4million with UAE

nationals estimated to represent

approximately 8% of the total. By 2020

population is expected to pass 3 million

and if the current trends continue, UAE

nationals will constitute only around 6% of

the population at that time.

Dubai Residential Sales Price (AED/Sqft)

According to Dubai Statistical Centre, in

2014 the emirate’s population is estimated

to have reached 2.32mn, and is expected

to continue growing and reach circa 2.4

million by the end of this year. Dubai has a

very young and dynamic population: 98%

of the population is under 60 years of age,

almost 90% of the population is under 50

years of age, and 85% are below 45 years

of age.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information& other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, Dubizzle, UAE Property Finder, Gulfnews

TTTTThe Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

0-5

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

Female Male

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2006 2007 2008 2009 2010 2011 2012 2013 2014F

UAE National (mn)

Expatriate (mn)

-60%-55%-50%-45%-40%-35%-30%-25%-20%-15%-10%-5%0%5%10%15%20%25%30%35%40%45%50%

600700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,8001,9002,0002,1002,2002,3002,4002,500

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Residential Sales Price (AED/Sqft)

% change y-o-y (RHS)

Dubai Residential Rent (AED/Sqft)

Source: NBAD Real Estate Database

Abu Dhabi Residential Sales Price (AED/Sqft)

Source: NBAD Real Estate Database

Abu Dhabi Residential Rent (AED/Sqft) vs Yield

Source: NBAD Real Estate Database

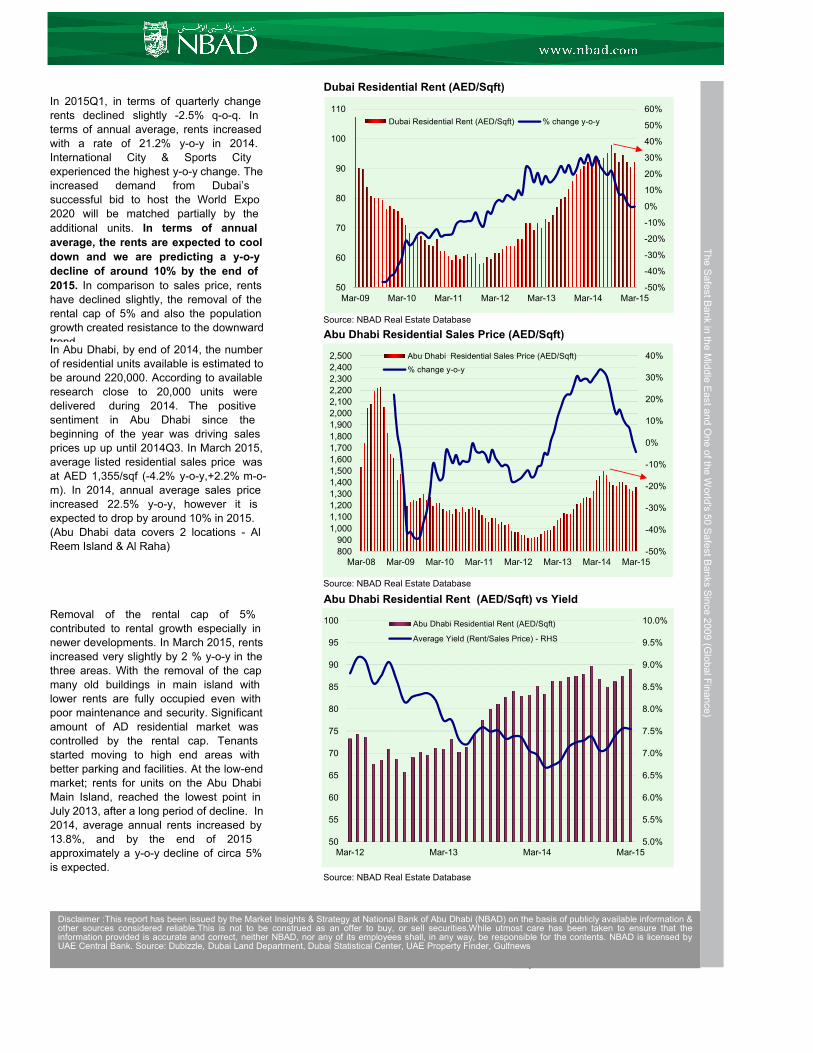

In Abu Dhabi, by end of 2014, the number

of residential units available is estimated to

be around 220,000. According to available

research close to 20,000 units were

delivered during 2014. The positive

sentiment in Abu Dhabi since the

beginning of the year was driving sales

prices up up until 2014Q3. In March 2015,

average listed residential sales price was

at AED 1,355/sqf (-4.2% y-o-y,+2.2% m-o-

m). In 2014, annual average sales price

increased 22.5% y-o-y, however it is

expected to drop by around 10% in 2015.

(Abu Dhabi data covers 2 locations - Al

Reem Island & Al Raha)

Removal of the rental cap of 5%

contributed to rental growth especially in

newer developments. In March 2015, rents

increased very slightly by 2 % y-o-y in the

three areas. With the removal of the cap

many old buildings in main island with

lower rents are fully occupied even with

poor maintenance and security. Significant

amount of AD residential market was

controlled by the rental cap. Tenants

started moving to high end areas with

better parking and facilities. At the low-end

market; rents for units on the Abu Dhabi

Main Island, reached the lowest point in

July 2013, after a long period of decline. In

2014, average annual rents increased by

13.8%, and by the end of 2015

approximately a y-o-y decline of circa 5%

is expected.

In 2015Q1, in terms of quarterly change

rents declined slightly -2.5% q-o-q. In

terms of annual average, rents increased

with a rate of 21.2% y-o-y in 2014.

International City & Sports City

experienced the highest y-o-y change. The

increased demand from Dubai’s

successful bid to host the World Expo

2020 will be matched partially by the

additional units. In terms of annual

average, the rents are expected to cool

down and we are predicting a y-o-y

decline of around 10% by the end of

2015. In comparison to sales price, rents

have declined slightly, the removal of the

rental cap of 5% and also the population

growth created resistance to the downward

trend.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information &other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubizzle, Dubai Land Department, Dubai Statistical Center, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

T

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Abu Dhabi Residential Sales Price (AED/Sqft)

% change y-o-y

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

50

55

60

65

70

75

80

85

90

95

100

Mar-12 Mar-13 Mar-14 Mar-15

Abu Dhabi Residential Rent (AED/Sqft)

Average Yield (Rent/Sales Price) - RHS

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

50

60

70

80

90

100

110

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Dubai Residential Rent (AED/Sqft) % change y-o-y

TTTTTTT

Alp Eke

Senior Economist

Market Insights & Strategy

Global Markets, NBAD

P O Box 4, Abu Dhabi, UAE

Tel: +971 2 6110157

12th May 2015

Certificates of Deposit (AED Billion)

Source: Central Bank of UAE (CBUAE)

Certificates issued by the Central Bank

and sold only to banks to absorb excess

liquidity and are also used as an indicator

to determine domestic interest rates. Pre-

Crisis in 2008Q3, hot money was flowing

into UAE banking system, and annual

lending growth exceeded 25% during 2007-

2008. Mortgage Loan to Value ratios

exceeded 95%, off plan sales and

financing was commonplace. Loan to

Deposit (LTD) ratio was above 110%.

Banking sector liquidity has improved

significantly. It is reflected in the net LTD

ratio decline. In June 2014 the LTD ratio

reached lowest point at 87%. Currently in

February 2014, LTD ratio is at around 91%.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information &other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that the informationprovided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed by UAE CentralBank. Source: Dubizzle, Dubai Land Department, Dubai Statistical Center, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)

TTTT

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

0102030405060708090100110120130140150160170180190200210220

Dec-14Sep-12Jun-10Mar-08Dec-05

Certicates Deposit (AED Billion)

% change yoy (LHS)

2002

2. Law 14: Mortgage Registration. Protects banks and financial institutions by registering mortgages on

real estate and enforcement of rights in case of default

20061. Law 7: Real Property Registration. Allows foreigners to own real estate in designated areas

A developer can offer units off plan when 20% of construction has been done or the developer has deposited 20% of

project value with RERA in an ESCROW account

All projects have to registered with RERA. Only RERA registered developer can launch a project.

2013

1. Investor Protection Law (TANWEER): Not yet released. Allows investors to get full refund in case of

developer failure to deliver/complete property in specified time frame or alters specifications of flats without

permission. Allows for compensation for breach of any warranty in contract or misrepresentation by the

developer or broker.

RERA Regulations That Protect Investor Interest

2008

2. Law 8: Escrow Law. This law ensures off plan sales reveue to be used only for the project it is collected

1. Real Estate Regulatory Authority (RERA) formed. RERA becomes the regulatory institution for real

estate market.

2. In July 2013, Government of Dubai announced establishment of a special legal committee to settle the

disputes between the property developers and investors over the cancellation of projects. The decisions of

this legal committee can not be challenged by any Dubai Court

1. Amendments to Law 13 of 2008: Developer can keep full amount paid and claim remaining purchasing

price if at least 80% of the project is completed. Developer can revoke the contract and keep up to 40% of

the purchase price if at least 60% of the project is completed. Developer can revoke the contract and keep

up to 25% of the purchase price if construction started but didn't reach 60%.Developer can revoke the

contract and keep up to 30% of amount paid if construction has not started for reasons beyond control.

1. Law 27: Jointly owned properties (Strata Law). Strata law benefits buyers bringing transparency and

fairness on issues such as service charges, contracts with service providers and the use of common areas

and facilities.

2. Decree 4: Ownership of Land granted for industrial and commercial purposes. The decree allows

holders of commercial granted lands to convert them into freehold payment of fees and market prices

enabling them to use land to raise capital or sell it in open market.

2007

Property market opens up for foreigners

2010

Time Line of Dubai Real Estate Regulation

2009

1. Law 13: Interim Real Estate Registry. Developers can't sell units off plan unless they take possession of

land. All real estate units to be recorded in interim Real Estate Register. In case of default by the investor,

developer must refund money after a deduction not exceeeding 30% of money paid by the investor.

3. In October 2013, Central Bank issued new rules governing bank lending. The new rules will limit home

loans for expatriates to 75% of property's value for investments less then AED5million and 80% for UAE

nationals. For second property expatriates will be allowed 60% of property value and 65% for UAE

nationals.Loans will be limited to maximum of 25 years.Maximum age for last repayment is 65 years for

expatriates and 70 for UAE nationals.

4. In October 2013, Dubai Land Department as real estate regulatory authority in order to prevent

excessive amount of speculation it would double the transfer fee on each sale to 4% of property's value.

Disclaimer :This report has been issued by the Market Insights & Strategy at National Bank of Abu Dhabi (NBAD) on the basis of publicly available information& other sources considered reliable.This is not to be construed as an offer to buy, or sell securities.While utmost care has been taken to ensure that theinformation provided is accurate and correct, neither NBAD, nor any of its employees shall, in any way, be responsible for the contents. NBAD is licensed byUAE Central Bank. Source: Dubai Land Department, Dubai Statistical Center, Dubizzle, UAE Property Finder, Gulfnews

The Safest B

ank in the Middle East and One of th

e W

orld's 50 Safest B

anks Since 2009 (G

lobal Finance)