uac of nigeria plc - · pdf fileuac of nigeria cautions readers that a number of factors...

TRANSCRIPT

UAC of Nigeria PLC

Group Results Presentation – Full Year 2015

2

This presentation contains or will contain forward-looking statements which reflect management's expectations regarding the Company's future growth, results of operations, performance, business prospects and opportunities. Wherever possible, words such as "anticipate", "believe", "expects", "intend" "estimate", "project", "target", "risks", "goals" and similar terms and phrases have been used to identify the forward-looking statements. These statements reflect management's current beliefs and are based on information currently available to management. Certain material factors or assumptions have been applied in drawing the conclusions contained in the forward-looking statements. These factors or assumptions are subject to inherent risks and uncertainties surrounding future expectations generally. UAC of Nigeria cautions readers that a number of factors could cause actual results, performance or achievements to differ materially from the results discussed or implied in the forward-looking statements. These factors should be considered carefully and undue reliance should not be placed on the forward-looking statements. For additional information with respect to certain of these risks or factors, reference should be made to the Company’s disclosure materials filed from time to time with Securities & Exchange Commission in Nigeria. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Important Notice

3

2

3

2

1

Contents

Summary & outlook 3

Financial Performance review

Overview of the business in FY 2015

Larry Ettah

GMD/CEO

Abdul Bello

CFO

Larry Ettah

GMD/CEO

4

2

3

2

1

Contents

Summary & outlook 3

FINANCIAL Performance review

Overview of the business in FY 2015

Larry Ettah

GMD/CEO

Abdul Bello

CFO

Larry Ettah

GMD/CEO

Presentation Overview

“Tough operating environment in 2015 but we held our market

positions”

6

Operating Environment of 2015

GDP growth down to 3% in 2015 (6.2% 2014)

Parallel Market FX Rates - N191/1$ (2014), N266/1$ (2015)

Inflation at 9.6% (7.9% 2014)

Political uncertainty, delayed transition and stability of new Government/ Cabinet

Insecurity in the North; national petroleum product shortages

Macro-economic challenges; Government revenue falls and build-up of arrears of public servants’ wages

All led to reduced consumer purchasing power

7

Outbreak of Avian Influenza across two-thirds of the States of Nigeria led to significant

reduction in bird population & weak poultry feeds’ demand

Turmoil in the Oil & Gas Industry, volatility in Capital market and decline in general

commercial activities led to a soft Real Estate and Paints markets

8

VISION To be number one in our chosen markets, providing exceptional

value to our customers

MISSION

To grow our top-line at twice the rate of GDP growth in Nigeria at a blended EBIT profitability of 15%

OUR VALUES 1. Our Customers are our Focus 2. We act with Respect for the Individual 3. We act with Integrity in everything we do 4. Team spirit will give us good success 5. Innovation for business sustenance and value creation 6. We are Open and Communicate with our people

DESIRED OUTCOME Adding value to the lives of our stakeholders

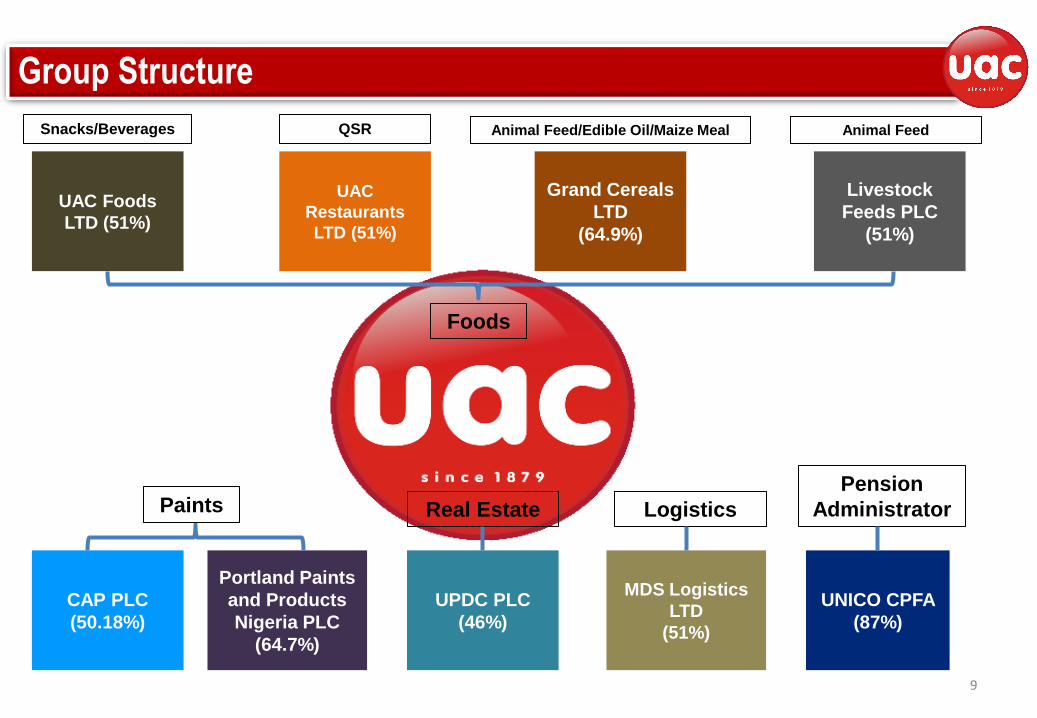

Group Structure

9

UAC Foods

LTD (51%)

UAC

Restaurants

LTD (51%)

Livestock

Feeds PLC

(51%)

CAP PLC

(50.18%)

MDS Logistics

LTD

(51%)

UPDC PLC

(46%)

Portland Paints

and Products

Nigeria PLC

(64.7%)

UNICO CPFA

(87%)

Grand Cereals

LTD

(64.9%)

Paints Logistics

Pension

Administrator

Snacks/Beverages QSR Animal Feed/Edible Oil/Maize Meal Animal Feed

Foods

Real Estate

10

11

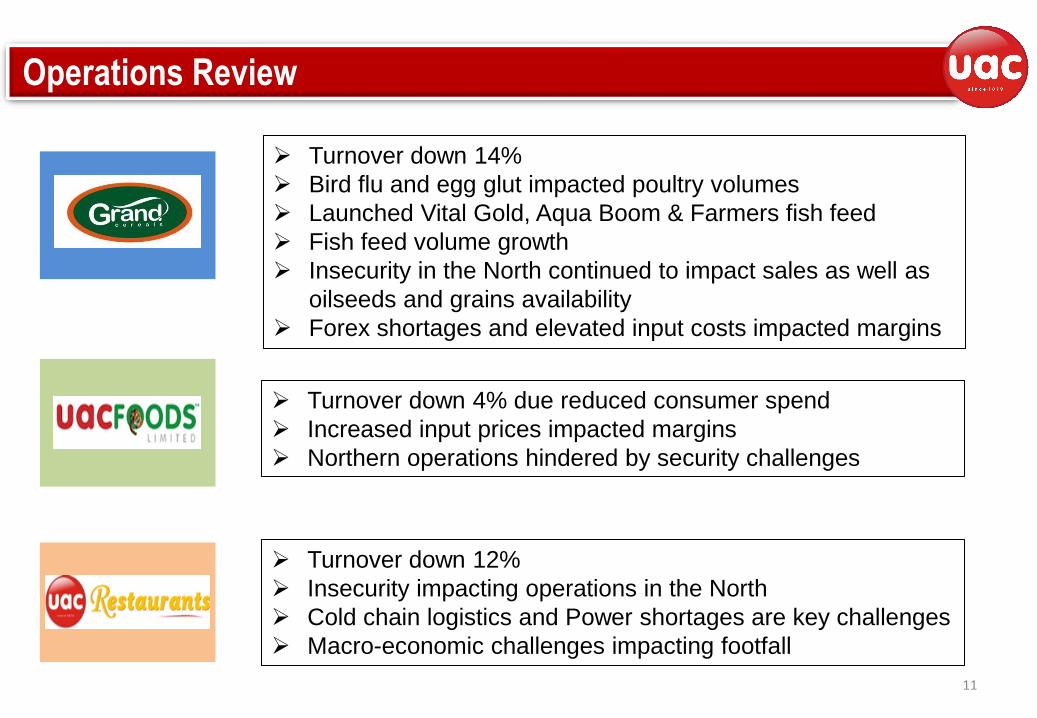

Operations Review

Turnover down 14%

Bird flu and egg glut impacted poultry volumes

Launched Vital Gold, Aqua Boom & Farmers fish feed

Fish feed volume growth

Insecurity in the North continued to impact sales as well as

oilseeds and grains availability

Forex shortages and elevated input costs impacted margins

Turnover down 4% due reduced consumer spend

Increased input prices impacted margins

Northern operations hindered by security challenges

Turnover down 12%

Insecurity impacting operations in the North

Cold chain logistics and Power shortages are key challenges

Macro-economic challenges impacting footfall

12

Operations Review

Turnover up 13% on the back of new Ikeja mill & introduction of

Aquamax Fish feed

Rationalised Benin-City factory; toll milling from Grand Cereals’

Onitsha plant

Rising input costs and grains and oilseeds shortages

Egg glut & later ‘Bird Flu’ outbreak impacted volumes

Turnover up 1%

Launched Dulux TV Commercial

High cost of input materials impacted margins

Decline in consumer spend impacted volumes

Delayed forex allocations

Turnover down 23%

Restructured Sales model & impaired debts and inventory

associated with old model and exit from Sanitary wares

Operating environment – Oil & Gas, Construction impacted

volumes

13

Operations Review

Turnover down 56%

Property market remains soft

Rising interest rates impacting margins Festival Mall opened for business

Turnover up 1%

Increased client base but overall client volume decline

Major fire at Abuja Pharmaceutical warehouse; quickly

rebuilt and trading

Warehouse expansion/modernization at Abuja, Sokoto

and Acme locations

Portfolio optimisation of service offerings to clients

Performance of Key Subsidiaries

Grand Cereals (N’Million)

UAC Restaurants (N’Million) UAC Foods (N’Million)

14

Livestock Feeds (N’Million)

1,221

108

1,078

-134 Turnover PBT

2014 2015

35,813

2,925

30,620

2,041

Turnover PBT

2014 2015 7,914

361

8,963

280

Turnover PBT

2014 2015

15,143

1,463

14,550

1,434

Turnover PBT

2014 2015

Performance of Key Subsidiaries

UPDC (N’Million)

Portland Paints (N’Million) CAP (N’Million)

15

MDS (N’Million)

2,798

105

2,168

-332 Turnover PBT

2014 2015

11,701

3,541

5,121

56

Turnover PBT

2014 2015 4,836

1,501

4,860

1,026

Turnover PBT

2014 2015

6,988

2,442

7,057

2,572

Turnover PBT

2014 2015

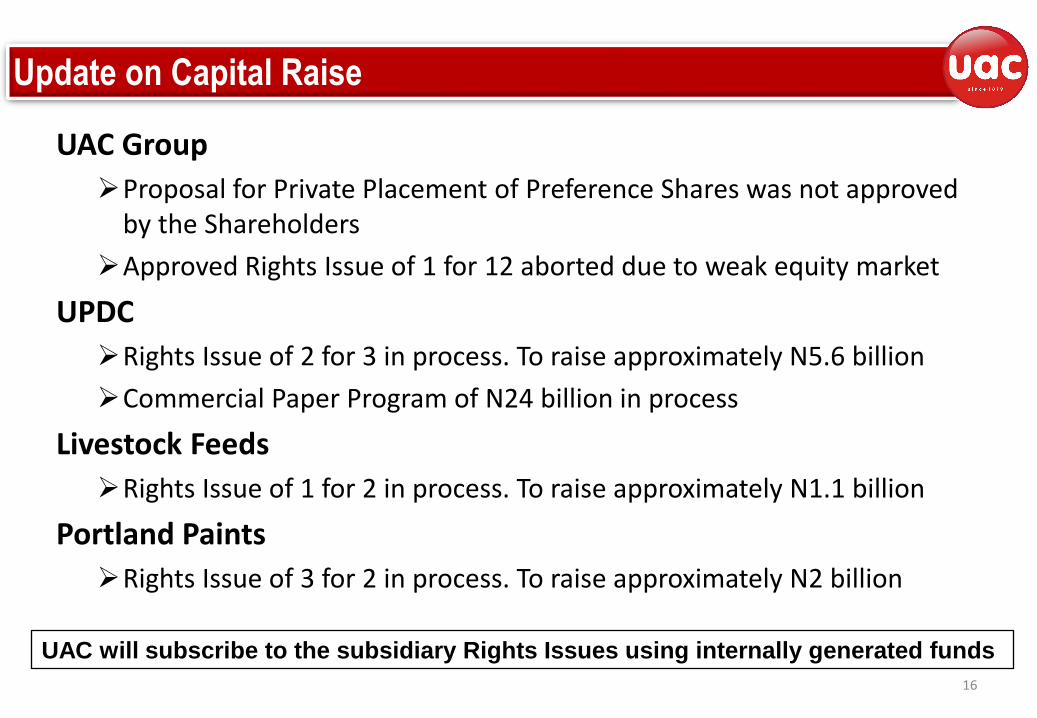

UAC Group

Proposal for Private Placement of Preference Shares was not approved by the Shareholders

Approved Rights Issue of 1 for 12 aborted due to weak equity market

UPDC

Rights Issue of 2 for 3 in process. To raise approximately N5.6 billion

Commercial Paper Program of N24 billion in process

Livestock Feeds

Rights Issue of 1 for 2 in process. To raise approximately N1.1 billion

Portland Paints

Rights Issue of 3 for 2 in process. To raise approximately N2 billion

16

UAC will subscribe to the subsidiary Rights Issues using internally generated funds

Update on Capital Raise

17

18

2

3

2

1

Outline

Summary & outlook 3

FINANCIAL Performance review

Overview of the business in 1h 2015

Larry Ettah

GMD/CEO

Abdul Bello

CFO

Larry Ettah

GMD/CEO

19

Poor quality photo!

20

Key Performance Highlights

Financial

Performance

Financial

Position

Performance

Ratios

2015 2014 2015 2014

Turnover 73,145 85,654 821 929

Gross Profit 16,565 19,183 821 929

EBIT 7,607 12,394 2,684 3,941

PBT 7,944 14,097 4,162 5,341

2015 2014 2015 2014

Cash (N'm) 9,183 7,957 3,431 2,855

Borrowings (N'm) 25,649 28,295 - -

Total Assets (N'm) 128,655 130,361 27,572 26,474

Total Liabilities (N'm) 54,513 55,283 5,987 5,031

Net Assets (N'm) 74,142 75,078 21,585 21,443

2015 2014 2015 2014

Gross Margin 23% 22% 100% 100%

EBIT Margin 10% 14% 327% 424%

PBT Margin 11% 16% 507% 575%

ROE 7% 15% 16% 20%

Gearing 0.35x 0.38x - -

Group Company

21

Statement of Profit or Loss

Revenue decline largely on account

of drop in sales in UPDC (N6.2

billion) and Grand Cereals (N5.7

billion)

Other gains – Reduction in gains on

fair valuation of UPDC properties

Other losses – Impairment of

Assets in UPDC Hotels and decline

in property valuation at Holdco

Share of Profit in Associate – REIT

measurement period; 19 months in

2014 vs 12 months in 2015

Taxation relatively up on account of

back duty taxes post-restructuring

Comments 2015 2014 2015 2014

N'M N'M N'M N'M

Continuing Operations

Revenue 73,145 85,654 821 929

Cost of sales (56,580) (66,472) - - - -

Gross profit 16,565 19,183 821 929

Dividend income - - 3,216 3,534

Selling and distribution expenses (3,319) (3,629) - -

Administrative expenses (6,882) (6,551) (1,515) (1,479)

Other gains 1,959 3,464 343 1,028

Other losses (716) (73) (181) (71)

Operating profit 7,607 12,394 2,684 3,941 - -

Net finance (cost) / income (1,451) (1,276) 1,478 1,400

Share of profit of equity accounted associate 1,787 2,979 - - - -

Profit before taxation 7,943 14,097 4,162 5,341

Taxation (2,797) (3,366) (659) (1,028)

Profit from continuing operations 5,147 10,730 3,503 4,313

Profit from discontinued Operations 38 214 - -

Profit for the year 5,185 10,944 3,503 4,313 - -

Profit attributable to Parent 2,997 6,536 3,503 4,313

Profit attributable to NCI 2,188 4,409 - -

Group Company

22

Statement of Financial Position

2015 2014 2015 2014

N'M N'M N'M N'M

PPE 35,439 36,613 858 852

Investment property 20,035 19,924 2,985 3,199

Investments in associates 21,208 19,101 - -

Investments in subsidiaries - - 11,641 11,641

Trade and other receivables 14,594 15,950 8,572 7,815

Cash and short-term deposits 9,183 7,957 3,431 2,855

Other Assets 28,195 30,816 85 113 Total Assets 128,655 130,361 27,572 26,474

Long-term borrowings 8,126 7,737 - -

Short-term borrowings 17,523 20,558 - -

Trade and other payables 14,941 13,961 629 908

Other liabilities 13,923 13,026 5,358 4,123 Total Liabilities 54,513 55,283 5,987 5,031

Equity - Parent 44,588 44,968 21,585 21,443

NCI 29,554 30,110 - -

Total Equity 74,142 75,078 21,585 21,443

Total Equity & Liabilities 128,655 130,361 27,572 26,474

Group Company

Group Trend Analysis Operating Profit (N’M) Turnover (N’M)

23

Turnover trend in 2015 reflects the challenge of the environment and the

consumer

59,638

69,632

78,714 85,654

73,145

2011 2012 2013 2014 2015

7,715

11,526

15,192

12,394

7,607

2011 2012 2013 2014 2015

Group Trend Analysis DPS (Kobo) EPS (Kobo)

24

160 175 175

100

2012 2013 2014 2015

257

291

340

156

2012 2013 2014 2015

Dividend cut bolsters our capital position

Group Trend Analysis ROE Gearing/Current Ratio

25

12%

14% 15%

7%

2012 2013 2014 2015

1.22 1.16

1.25 1.19

0.50

0.36 0.38 0.35

2012 2013 2014 2015

Current Ratio Gearing

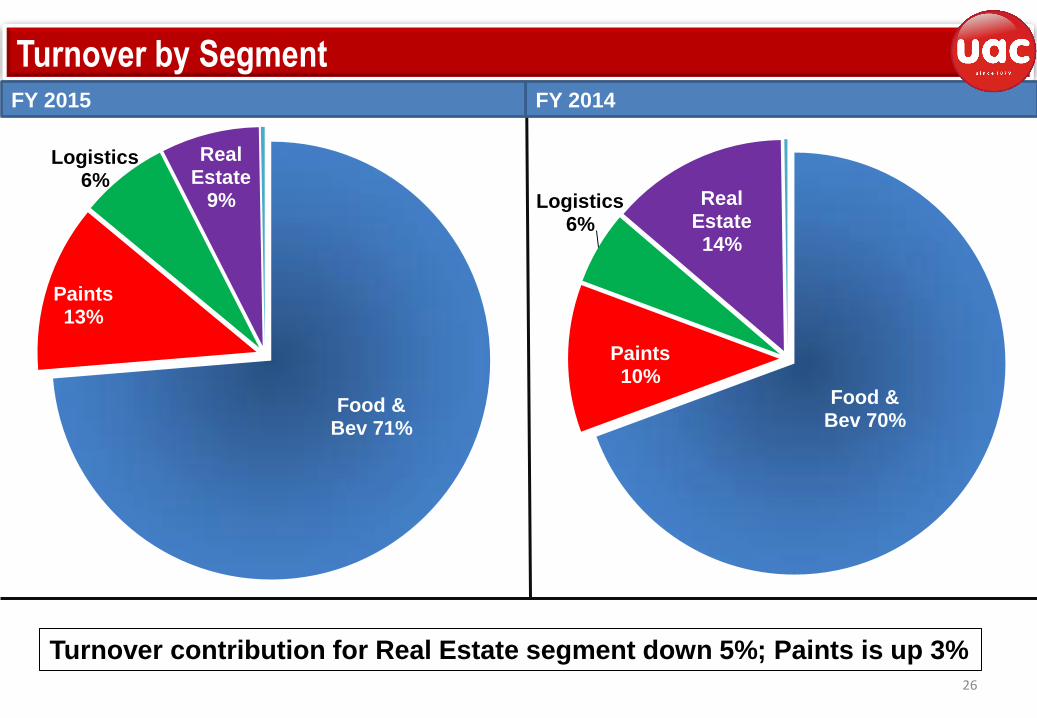

Turnover by Segment FY 2014 FY 2015

26

Turnover contribution for Real Estate segment down 5%; Paints is up 3%

Food & Bev 70%

Paints 10%

Logistics 6%

Real Estate 14%

Food & Bev 71%

Paints 13%

Logistics 6%

Real Estate

9%

PBT by Segment FY 2014 FY 2015

27

Paints contribution to PBT was 34%; Foods is up 11%, both on

account of decline in UPDC

Food & Bev 39%

Paints 20%

Logistics 12%

Real Estate 28%

Others 1%

Food & Bev 50%

Paints 34%

Logistics 14%

Others

2%

Segment Analysis Gross Margins Turnover (N’M)

28

60,091

11,701

4,836

9,786

55,212

5,121 4,860

9,225

Foods Real Estate Logistics Paints

17% 16%

36%

50%

16%

36%

29%

49%

Foods Real Estate Logistics Paints

Segment Analysis PBT Margins

29

8%

30% 31%

28%

6%

1%

21%

25%

Foods Real Estate Logistics Paints

30

31

2

3

2

1

Outline

Summary & outlook 3

FINANCIAL Performance review

Overview of the business in FY 2015

Larry Ettah

GMD/CEO

Abdul Bello

CFO

Larry Ettah

GMD/CEO

Outlook FY 2016

Planned Government spend will be inflationary but same should improve purchasing power of consumers

Forex shortages and Government focus on Agriculture should be supportive of our animal feed businesses

Government focus on Housing development should be supportive of our Real estate and Paints businesses

Planned reintroduction and passage of Petroleum Industry Bill should be supportive of our marine coatings segment of the Paints business

Forex shortages and exchange rate volatility will persist leading to input material shortages and rising input prices

We will achieve growth through strong execution of our strategic thrusts

32

33

1

2

3

Innovation

Talent

Management

Strategic

Fast-track innovation in manufacturing units

Introduce new products in key categories

Resource

Optimisation

4

Resourcing & Human Capacity building

Asset and yield optimisation

Drive for greater efficiency especially in supply chain

Cost optimisation

SAP ERP Benefit Realisation

Restructure financing of UPDC, Livestock Feeds & Portland Paints

Pursue greater integration of Livestock & Portland

Route to market redefinition

Our 2016 Priorities