types of insurance automobile health life disability homeowners/ renters

TRANSCRIPT

Types of Insurance Automobile

Health

LifeDisability

Homeowners/Renters

What Covers This Risk?

• After losing her husband to a heart attack, a wife is left alone to care for 2 children

Life!

What Covers This Risk?

• You need a cast after breaking an ankle while roller-blading

Health!

What Covers This Risk?

• Your rented apartment is broken into and your computer is stolen

Renters!

What Covers This Risk?

• You are injured in an automobile accident and are unable to work for 2 months

Disability!

What Covers This Risk?

• Your garage was destroyed by a fire which started by a lightning bolt hitting your home

Homeowners!

What Covers This Risk?

• Sick at home from food poisoning after eating a carnival corndog

Nothing!

What Covers This Risk?

• While driving, you have brake failure. You hit a telephone pole and cause damage to the front of the car

Automobile!

What Covers This Risk?

• While driving to the mall, you are pulled over and receive a speeding ticket

Nothing!

What Covers This Risk?

• A daughter, who is financially responsible for her mother’s nursing home bills, dies from an undetected heart defect

Life!

What Covers This Risk?

• A doctor diagnoses a child with tonsillitis during a visit to a clinic

Health!

Applying

• What would result if you had an automobile accident and did not have automobile insurance?

Automobile Insurance: The Basics

Automobile Insurance: The Basics

What is the likelihood you will be in an What is the likelihood you will be in an automobile accident?automobile accident?

There are more than 12 million motor vehicle accidents There are more than 12 million motor vehicle accidents annuallyannually

The typical driver will have a near automobile accident one or The typical driver will have a near automobile accident one or two times per monthtwo times per month

The typical driver will be in a collision of some type on average The typical driver will be in a collision of some type on average of every 6 yearsof every 6 years

Crashes are the leading cause of death for ages 3-33Crashes are the leading cause of death for ages 3-33

Automobile Insurance: The Basics

Even a minor accident can result in thousands of Even a minor accident can result in thousands of dollars in damagesdollars in damages

•Damage to your carDamage to your car

•Damage to other cars involvedDamage to other cars involved

•Medical BillsMedical Bills

•Lost wagesLost wages

•Pain and sufferingPain and suffering

•ProsecutionProsecution

•Legal FeesLegal Fees

•FinesFines

Automobile Insurance: The Basics

If you are in an accident how do If you are in an accident how do you pay for it?you pay for it?

Bank Account?Bank Account?

Parents?Parents?

Rich Uncle?Rich Uncle?

Best Friend?Best Friend?

Insurance?Insurance?

Automobile Insurance: The Basics

What is Automobile Insurance?What is Automobile Insurance?

An auto insurance policy is a contract between you An auto insurance policy is a contract between you and an insurance company. and an insurance company.

You pay a premium, and in exchange, the insurance You pay a premium, and in exchange, the insurance company promises to pay for specific car-related company promises to pay for specific car-related financial losses during the term of the policy. financial losses during the term of the policy.

Why do I need auto insurance

• It’s the law!It’s the law!

• There are risks you can’t afford to takeThere are risks you can’t afford to take • What happens if…What happens if…

– You’re involved in a crash that causes property You’re involved in a crash that causes property damage?damage?

– You hurt yourself or someone else?You hurt yourself or someone else?– Your car is damaged when you’re not driving it? Your car is damaged when you’re not driving it?

(by weather, vandalism or a hit-and-run)(by weather, vandalism or a hit-and-run)– Your car is stolen?Your car is stolen?– Your car breaks down and needs to be towed?Your car breaks down and needs to be towed?

Automobile Insurance: The Basics

Are you a risk to the insurance Are you a risk to the insurance company?company?

To keep premiums as low as possible to the insured, To keep premiums as low as possible to the insured, a screening process is completed before an a screening process is completed before an insurance contract is completedinsurance contract is completed

Automobile Insurance: The Basics

What is the insurance company What is the insurance company looking for?looking for?

Some vehicles, and some drivers, carry more risk Some vehicles, and some drivers, carry more risk than othersthan others

•Low risks will be charged a lower premiumLow risks will be charged a lower premium

•High risks will be charged a higher premiumHigh risks will be charged a higher premium

Automobile Insurance: The Basics

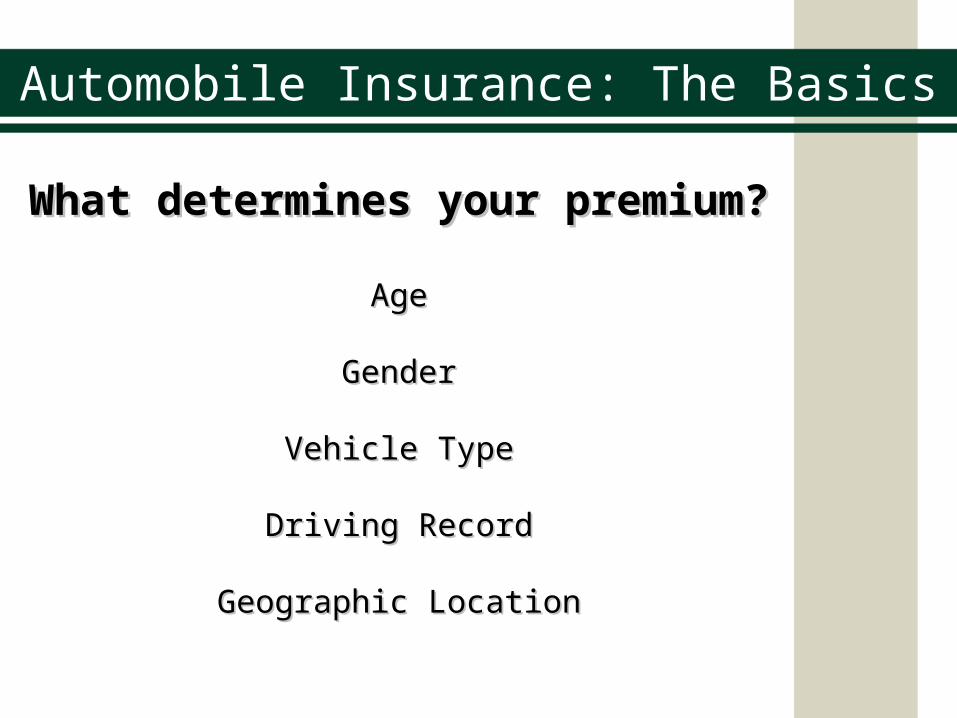

What determines your premium?What determines your premium?

AgeAge

GenderGender

Vehicle TypeVehicle Type

Driving RecordDriving Record

Geographic LocationGeographic Location

Types of Automobile Insurance Coverages

Three QuestionsThree Questions

1.1. What are third-party coverages?What are third-party coverages?

2.2. What are first-party injury What are first-party injury coverages?coverages?

3.3. What are first-party property What are first-party property coverages?coverages?

What are third-party coverages?What are third-party coverages?

Bodily Injury LiabilityBodily Injury Liability

People costs (medical expenses, lost wages, People costs (medical expenses, lost wages, pain and suffering)pain and suffering)

Property Damage LiabilityProperty Damage Liability

Things (other cars and property)Things (other cars and property)

Both are types of coverage required by law in Both are types of coverage required by law in most statesmost states

Types of Automobile Insurance Coverages

What are first-party injury coverages?What are first-party injury coverages?

Medical Payments (MedPay)Medical Payments (MedPay)

Covers medical and funeral expenses resulting from Covers medical and funeral expenses resulting from accidents with your vehicleaccidents with your vehicle

Personal Injury Protection (PIP)Personal Injury Protection (PIP)

Extends MedPay to include lost wagesExtends MedPay to include lost wages

Uninsured MotoristsUninsured Motorists

Covers expenses if the at fault driver does not have Covers expenses if the at fault driver does not have coveragecoverage

Underinsured MotoristsUnderinsured Motorists

Covers expenses when the at fault driver does not have Covers expenses when the at fault driver does not have enough coverageenough coverage

Types of Automobile Insurance Coverages

What are first-party property coverages?What are first-party property coverages?

ComprehensiveComprehensive

Compensates you for physical damage to your car, Compensates you for physical damage to your car, including theft, vandalism, natural disastersincluding theft, vandalism, natural disasters

CollisionCollision

Pays for damage to your vehicle in case of Pays for damage to your vehicle in case of collisioncollision

Both Coverages require you to pay a deductibleBoth Coverages require you to pay a deductible

Types of Automobile Insurance Coverages

What is a Deductible?

This is the amount per accident that you pay out This is the amount per accident that you pay out of pocket before insurance starts to payof pocket before insurance starts to pay

Common deductible amounts are usually $250, Common deductible amounts are usually $250, $500, and $1000$500, and $1000

The higher the deductible amount you pay the The higher the deductible amount you pay the lower your premiums arelower your premiums are

Automobile Insurance: The Policy

A common mistake when shopping for automobile A common mistake when shopping for automobile insurance is looking only at the price between two insurance is looking only at the price between two policiespolicies

Policies differ from policy to policy and company to Policies differ from policy to policy and company to companycompany

5 parts to an insurance policy:5 parts to an insurance policy: DeclarationsDeclarations

CoveragesCoverages

ExclusionsExclusions

ConditionsConditions

DefinitionsDefinitions

Declarations

Lists important personal policy information Lists important personal policy information and is unique to each individual insuredand is unique to each individual insured

Contains personal information:Contains personal information:

namename

addressaddress

vehicle make and modelvehicle make and model

vehicle identification numbervehicle identification number

types of coveragestypes of coverages

policy limitspolicy limits

deductible amountsdeductible amounts

Coverage Parts/Insuring Agreement

Outlines the coverage options and coverage Outlines the coverage options and coverage limits purchasedlimits purchased

In short, what your insurance company In short, what your insurance company promises to provide in return for your promises to provide in return for your payment, based on the coverages and payment, based on the coverages and coverage limits selectedcoverage limits selected

Exclusions

Details what is Details what is notnot covered by the policy covered by the policy

Examples:Examples:

Intentional damage to your own vehicleIntentional damage to your own vehicle

Damages caused while vehicle is used as a delivery Damages caused while vehicle is used as a delivery vehiclevehicle

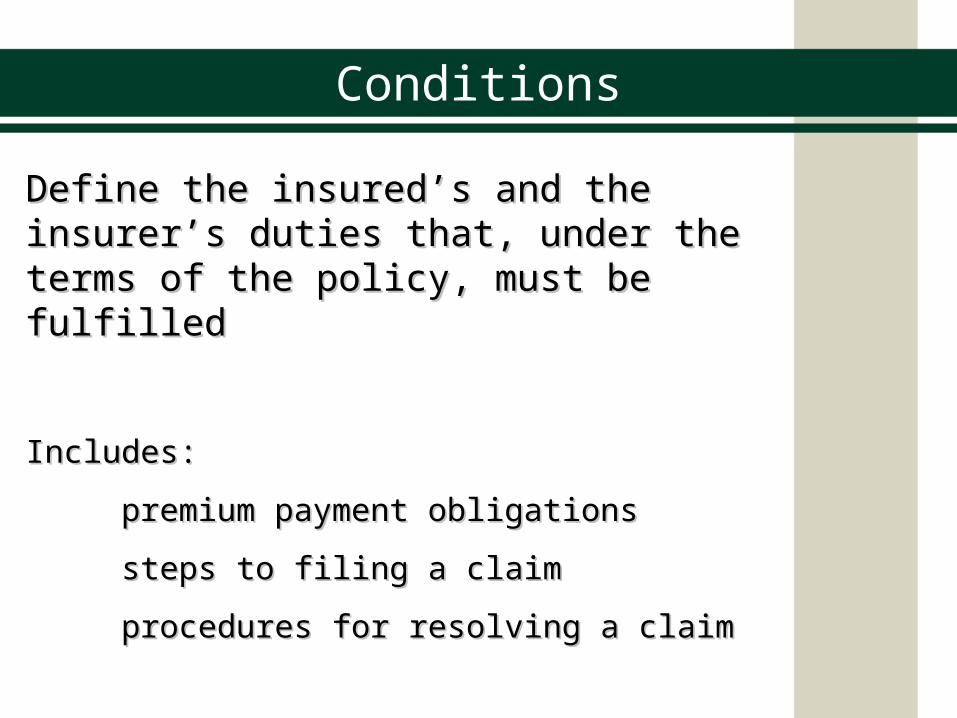

Conditions

Define the insured’s and the insurer’s duties Define the insured’s and the insurer’s duties that, under the terms of the policy, must be that, under the terms of the policy, must be fulfilledfulfilled

Includes:Includes:

premium payment obligationspremium payment obligations

steps to filing a claimsteps to filing a claim

procedures for resolving a claimprocedures for resolving a claim

Definitions

Explains specific terms used throughout the Explains specific terms used throughout the policypolicy

Examples:Examples:

““You” or “Your” refers to the “Named Insured”You” or “Your” refers to the “Named Insured”

““We” or “Us” or “Our” refers to the insurance We” or “Us” or “Our” refers to the insurance companycompany

““Family Member” refers to a resident of your Family Member” refers to a resident of your

householdhousehold

Automobile Insurance: Accidents

Chances are even if you are never in an Chances are even if you are never in an accident you will witness oneaccident you will witness one

What should you do if you are involved What should you do if you are involved in an accident?in an accident?

Steps to take after an accident

•Help anyone who is injuredHelp anyone who is injured

•You have an ethical and legal responsibilityYou have an ethical and legal responsibility

•Notify the policeNotify the police

•Prevent further accidentsPrevent further accidents

•Protect the accident sceneProtect the accident scene

•Record informationRecord information

•Exchange information with the parties involvedExchange information with the parties involved

•Take note of time, location, weather, and road Take note of time, location, weather, and road conditionsconditions

It is important that the accident is reported It is important that the accident is reported promptly to the insurance agent or companypromptly to the insurance agent or company

The policy will guide the insured on the The policy will guide the insured on the correct steps to take to report the claimcorrect steps to take to report the claim

The company will guide the insured through The company will guide the insured through the processthe process

Filing a Claim

When you are liable for an accidentWhen you are liable for an accident

•The insurance company covers the loss up to the The insurance company covers the loss up to the policy limitspolicy limits

•Your insurer represents you if you are suedYour insurer represents you if you are sued

•Your insurer has the right to settle any legal action Your insurer has the right to settle any legal action without your permissionwithout your permission

•Your premium may riseYour premium may rise

•Insurer has the right to cancel your policyInsurer has the right to cancel your policy

•If the losses exceed the policy provisions, the If the losses exceed the policy provisions, the insured is responsible to cover the excessinsured is responsible to cover the excess

Filing a Claim

Automobile Insurance: The Basics

What can you do to reduce risk and What can you do to reduce risk and lower premiums?lower premiums?

Use your seatbeltUse your seatbelt

Observe Speed LimitsObserve Speed Limits

Know your own limitsKnow your own limits

Concentrate on drivingConcentrate on driving

Be PatientBe Patient

Don’t Drink and DriveDon’t Drink and Drive

Get good gradesGet good grades

Analyzing

• Can you identify the different parts of automobile insurance coverage?

Situation 1

• Jose was driving to Streamwood High School. As he was turning into school he was rear-ended by Robert. Jose’s head hit the steering wheel and he was transported directly to the hospital by ambulance. Robert failed to pay his insurance premium for several months and his policy was cancelled. What type of automobile insurance coverage(s) is needed in this situation?

Situation 2

• Kathy was leaving Hotdog.com when she backed into Mr. Durbach’s Ferrari. Only the automobiles suffered physical damage. What type of automobile coverage(s) is needed in this situation?

Situations 3

• Matthew went fishing at The Fox River. While his car was unattended, someone stole Matthew’s hubcaps. What type of coverage(s) is needed?

Situation 4

• Gabby has an “old junker” worth $300. As she left Saturday School she hit the Sabre Rock. What type of coverage(s) is needed?

Situation 5

• Angelina, Sam and Miguel were driving to Carmelita’s for dinner. Angelina was talking on her cell phone and totaled her car. Both passengers were not seriously injured but did require medical attention. What type of coverage(s) is needed?

Situation 6

• Russell swerved to avoid hitting a cat and struck a tree. What type of coverage(s) is needed?