turkish vat system - oecd · 2016-03-29 · •the beginning of the studies on value added tax...

TRANSCRIPT

TURKISH VAT SYSTEM

Timur CAKMAK

Head of Department

Turkish Revenue Administration

• The beginning of the studies on Value Added Tax (VAT) in Turkey goes back to 1970.

• In 1974, a draft VAT law, which was the result of studies of a technical group, was prepared. The system was inspired by the EU model.

• The 8th draft was enacted on November 2nd , 1984 and entered into force on January 1st , 1985.

• By the VAT Law, eight indirect taxes on consumption were abolished

GENERAL OVERVIEW

TURKISH VAT SYSTEM

VAT ;

• is a general consumption tax

• covers all goods and services

• is applied to all stages from producer to consumer

• is calculated on transaction value with related rate

GENERAL OVERVIEW

TURKISH VAT SYSTEM

• VAT is levied at each stage of the production

and the distribution process.

Although liability for the tax falls on the person who supplies or imports the goods or services, the real burden of VAT is borne by the final consumer.

GENERAL OVERVIEW

TURKISH VAT SYSTEM

A SYSTEM WITHOUT VAT

Purchase price of good 100 TL

Selling price of good 150 TL

The profit is 50 TL

VAT is not calculated on this

profit and the final consumer

should pay 150 TL

TURKISH VAT SYSTEM

A SYSTEM WITH VAT

Purchase price of good 100 TL

Input VAT 18 TL

Total amount 118 TL

Selling price of good 150 TL

Output VAT 27 TL

Total Received amount 177 TL

VAT paid to tax office 9 TL (50 x %18 )

Profit 50 TL

The final consumer should pay 177 TL.

TURKISH VAT SYSTEM

The Turkish tax system levies

value added tax on

the supply and the importation

of goods and services.

TURKISH VAT SYSTEM

Liability for VAT arises; When a person or entity performs

commercial

industrial

agricultural

or independent professional activities

within Turkey

and when goods or services are imported into Turkey

TURKISH VAT SYSTEM

REVENUE ADMINISTRATION

Instutional Structure- Central

Commissioner

Vice Commissioner Vice Commissioner Vice Commissioner

Department of Legal

Consultancy

Department of

Consultancy on

Press and Public

Relations Department of

Strategic

Development

Dep. of

Audit and

Management

of

Compliance

Dep. of

Revenue

Controllers

Dep. of

Human

Resources

Dep. of

Revenue

Management

I, II, III

Dep. of

Taxpayer

Services

Dep. of

EU and

Foreign

Affairs

Dep. of

Support

Services

Dep. Of

Implementation

And Data

Management

Dep. of

Collection

and

Disputed

Cases

Vice Commissioner Vice Commissioner Vice Commissioner

TURKISH VAT SYSTEM

REVENUE ADMINISTRATION Instutional Structure- Local Tax Office Directorates

Taxpayer Services

Group Directorate

LTU

Istanbul

Large Taxpayer’s

Tax Diroctorate

Audit

Group Directorate

Strategy

Group Directorate

Local

Auditors

Offices

Directorships

Directorships

Directorships

Tax Office

Directorate

Human Resources

Group Directorate

Judgement

and

Disputed

Proceedings

Group Directorate

Support

Services

Group Directorate

Tax Assessment

Committees

Legal

Advisors

TURKISH VAT SYSTEM

TAXPAYERS

VAT taxpayers are defined in the

VAT Law as those engaged in

taxable transactions, irrespective

of their legal status or nature and

their position with regard to other

taxes.

TURKISH VAT SYSTEM

TAXABLE AMOUNT

• The taxable amount of a transaction is generally the total

value of the consideration received, not including the VAT

itself.

• The VAT Law deals with the taxable amount under four

headings, namely the taxable base on supply of goods

and services, importation, international transportation and

special types of taxable amount.

TURKISH VAT SYSTEM

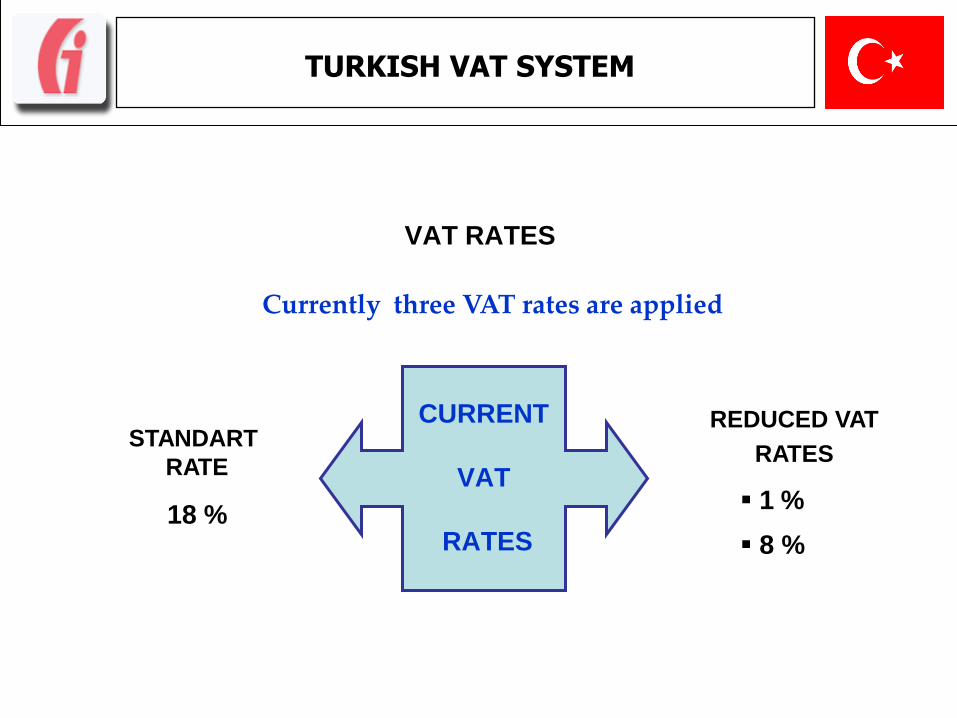

VAT RATES

• VAT rate specified on Article 28 of the Law is 10% for each of the transactions that are subject to tax

• The Council of Ministers is authorised;

To increase this rate up to 4 times, to reduce it down to 1%,

To specify different tax rates for various goods and services and

retail stage for some of the goods.

TURKISH VAT SYSTEM

VAT RATES

CURRENT

VAT

RATES

STANDART

RATE

18 %

REDUCED VAT

RATES

1 %

8 %

Currently three VAT rates are applied

TURKISH VAT SYSTEM

• The standard rate is 18%;

• Reduced rate of 1% is applied certain products such as some

agricultural goods, foodstuffs

• Reduced rate of 8% is applied certain products such as textile

products, education services

VAT RATES

TURKISH VAT SYSTEM

TYPE OF EXEMPTIONS

Full Exemptions

With right of deduction and with right of refund

– Exportation exemption

– Exemption for sea, air, and railway vehicles

– Services provided to sea and air transportation vehicles

– Petroleum explorations

– Exploring, processing, enrichment and refining activities for precious metals

TURKISH VAT SYSTEM

TYPE OF EXEMPTIONS

Partial Exemptions

Input VAT can’t be deducted and refunded, therefore the input

VAT charged on invoices is either expensed or “cost of goods”

TURKISH VAT SYSTEM

- Exemption for transitions, transferring, transformation, division transactions of enterprises

- Exemption for participation shares and sales of immovables of corporations

- Exemption for delivery of participation shares and immovables to banks as recompensation claims

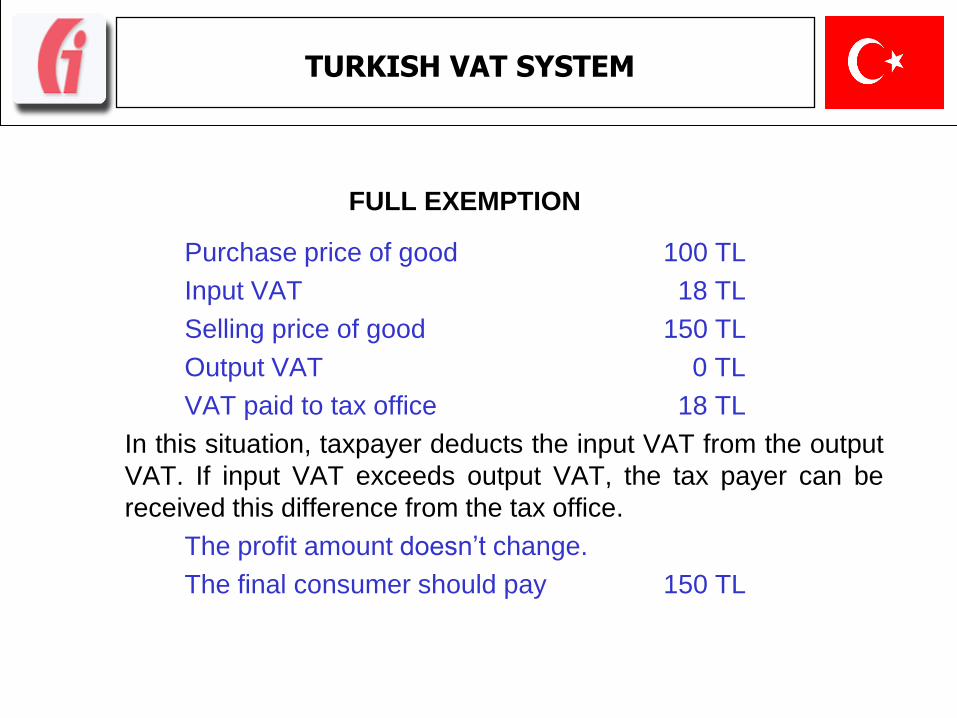

FULL EXEMPTION Purchase price of good 100 TL

Input VAT 18 TL

Selling price of good 150 TL

Output VAT 0 TL

VAT paid to tax office 18 TL

In this situation, taxpayer deducts the input VAT from the output

VAT. If input VAT exceeds output VAT, the tax payer can be

received this difference from the tax office.

The profit amount doesn’t change.

The final consumer should pay 150 TL

TURKISH VAT SYSTEM

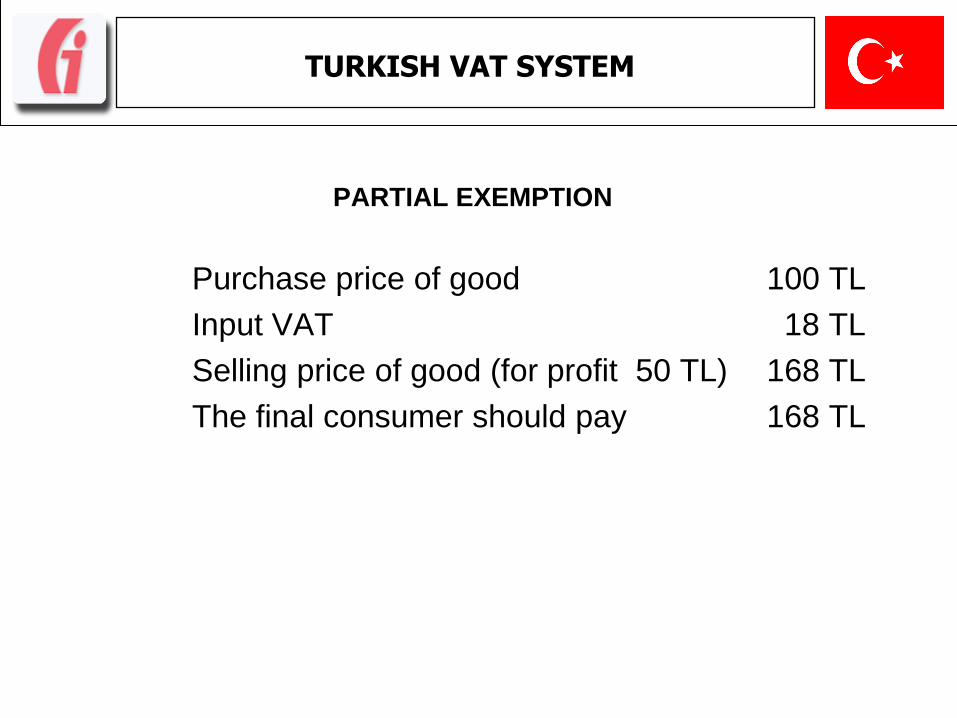

PARTIAL EXEMPTION

Purchase price of good 100 TL

Input VAT 18 TL

Selling price of good (for profit 50 TL) 168 TL

The final consumer should pay 168 TL

TURKISH VAT SYSTEM

DEDUCTION MECHANISM

• VAT is initially computed by applying the appropriate rate of taxation to the taxable amount for goods and services supplied by the taxable person during a taxable period.

• This amount is then reduced by a credit for VAT previously paid on importation and on goods and on services supplied to taxable person.

• VAT represented on invoices or similar documents made out for supplies and services conducted for themselves.

• VAT paid for imported goods and services.

TURKISH VAT SYSTEM

Taxable persons record VAT seen on the invoices or other

relevant documents as input VAT their accounting entries and

deduct input VAT from VAT collections (output VAT) from

supply of goods or services monthly basis.

DEDUCTION MECHANISM

TURKISH VAT SYSTEM

TAX REFUND

• If the sum of the deducted tax exceeds the sum of the

calculated VAT, the difference is “transferred to next

taxation period” and is not refunded.

• Refund is only possible for some transactions that are

stated in the Law and related legislation.

TURKISH VAT SYSTEM

• Transactions entitling refund right;

– Transactions that are in the scope of full exemptions,

– Transactions that are subject to reduced rate,

– Transactions that are in the scope of partial reverse charge application,

– Transactions prescribed in international agreements,

– Transactions for which excess and unnecessary tax is paid.

TAX REFUND

TURKISH VAT SYSTEM

ACCELARATED VAT REFUND SYSTEM

• Taxpayers who fulfill the certain conditions are given Accelerated

VAT Refund Certificate.

• Request in cash and/or on account submitted by taxpayers with

AVRC certificate is fulfilled without the request of any guarantee,

inspection report or Sworn Fiscal Consultant full certification

report.

TURKISH VAT SYSTEM

• Difficulty in voluntary compliance

• False or misleading invoices

• Lack of auditing

TURKISH VAT SYSTEM

PROBLEMS

TAXABLE PERIOD AND SUBMISSION OF VAT RETURNS

• The Ministry of Finance has established monthly taxable periods for all taxable persons under the normal VAT regime as of 01.10.1985.

• Taxable persons shall submit their returns to the local tax office within 24 days following the end of each taxable period.

TURKISH VAT SYSTEM

ELECTRONIC RETURN

The taxable persons of Personal Income Tax and Corporation Tax who

have commercial, agricultural and professional activities, are obliged to

send their VAT Returns via internet since October of 2007

TURKISH VAT SYSTEM

VAT payments are made 2 days after submission of VAT returns to tax offices or banks.

PAYMENT

TURKISH VAT SYSTEM

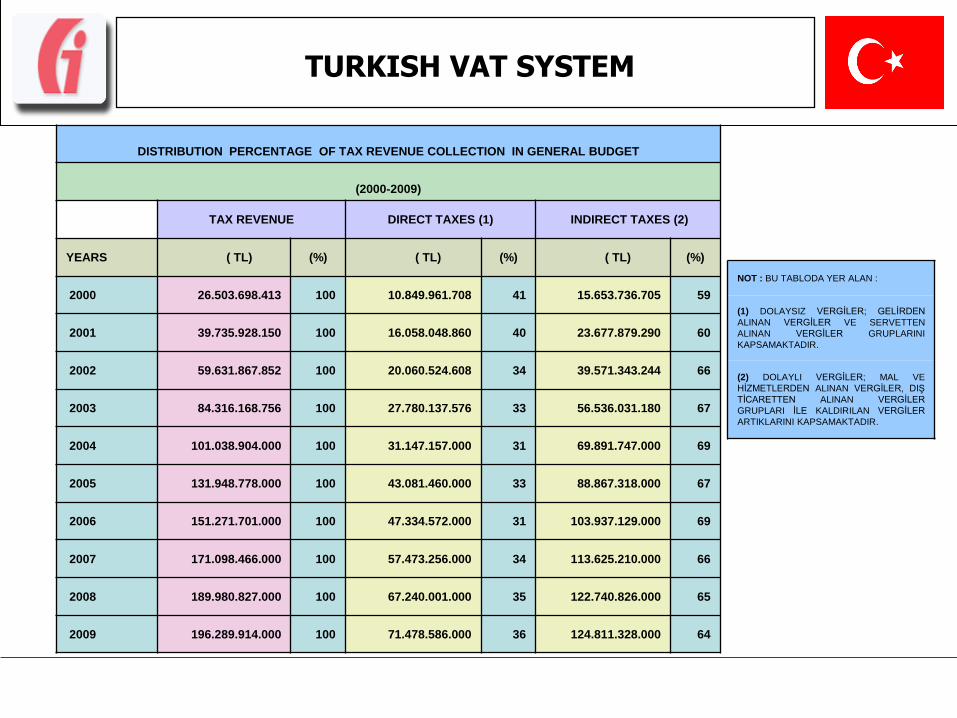

DISTRIBUTION PERCENTAGE OF TAX REVENUE COLLECTION IN GENERAL BUDGET

(2000-2009)

TAX REVENUE DIRECT TAXES (1) INDIRECT TAXES (2)

YEARS ( TL) (%) ( TL) (%) ( TL) (%)

2000 26.503.698.413 100 10.849.961.708 41 15.653.736.705 59

2001 39.735.928.150 100 16.058.048.860 40 23.677.879.290 60

2002 59.631.867.852 100 20.060.524.608 34 39.571.343.244 66

2003 84.316.168.756 100 27.780.137.576 33 56.536.031.180 67

2004 101.038.904.000 100 31.147.157.000 31 69.891.747.000 69

2005 131.948.778.000 100 43.081.460.000 33 88.867.318.000 67

2006 151.271.701.000 100 47.334.572.000 31 103.937.129.000 69

2007 171.098.466.000 100 57.473.256.000 34 113.625.210.000 66

2008 189.980.827.000 100 67.240.001.000 35 122.740.826.000 65

2009 196.289.914.000 100 71.478.586.000 36 124.811.328.000 64

NOT : BU TABLODA YER ALAN :

(1) DOLAYSIZ VERGİLER; GELİRDEN

ALINAN VERGİLER VE SERVETTEN

ALINAN VERGİLER GRUPLARINI

KAPSAMAKTADIR.

(2) DOLAYLI VERGİLER; MAL VE

HİZMETLERDEN ALINAN VERGİLER, DIŞ

TİCARETTEN ALINAN VERGİLER

GRUPLARI İLE KALDIRILAN VERGİLER

ARTIKLARINI KAPSAMAKTADIR.

TURKISH VAT SYSTEM

THE SHARE OF VAT IN GENERAL BUDGET REVENUE

(1988 - 2009) (1000 TL.)

YEARS COLLECTION OF TAX REVENUES

TOTAL AMOUNT OF VAT COLLECTION

(INWARD + İMPORT)

SHARE OF VAT IN TAX REVENUES

(%)

1988 14.232 4.177 29,3

1989 25.550 6.461 25,3

1990 45.399 12.371 27,2

1991 78.643 22.832 29,0

1992 141.602 42.088 29,7

1993 264.273 81.877 31,0

1994 534.888 176.742 33,0

1994 587.760 176.742 30,1

1995 1.084.350 354.980 32,7

1996 2.244.094 743.026 33,1

1997 4.745.484 1.561.562 32,9

1998 9.228.596 2.725.083 29,5

1999 14.802.280 4.164.334 28,1

2000 26.503.698 8.379.554 31,6

2001 39.735.928 12.438.860 31,3

2002 59.631.868 20.400.201 34,2

2003 84.316.169 27.031.099 32,1

2004 101.038.904 34.325.208 34,0

2005 119.250.807 38.280.429 32,1

2006 151.271.701 50.723.560 33,5

2007 171.098.466 55.461.123 32,4

2008 189.980.827 60.066.230 31,6

2009 196.289.914 60.166.409 30,7

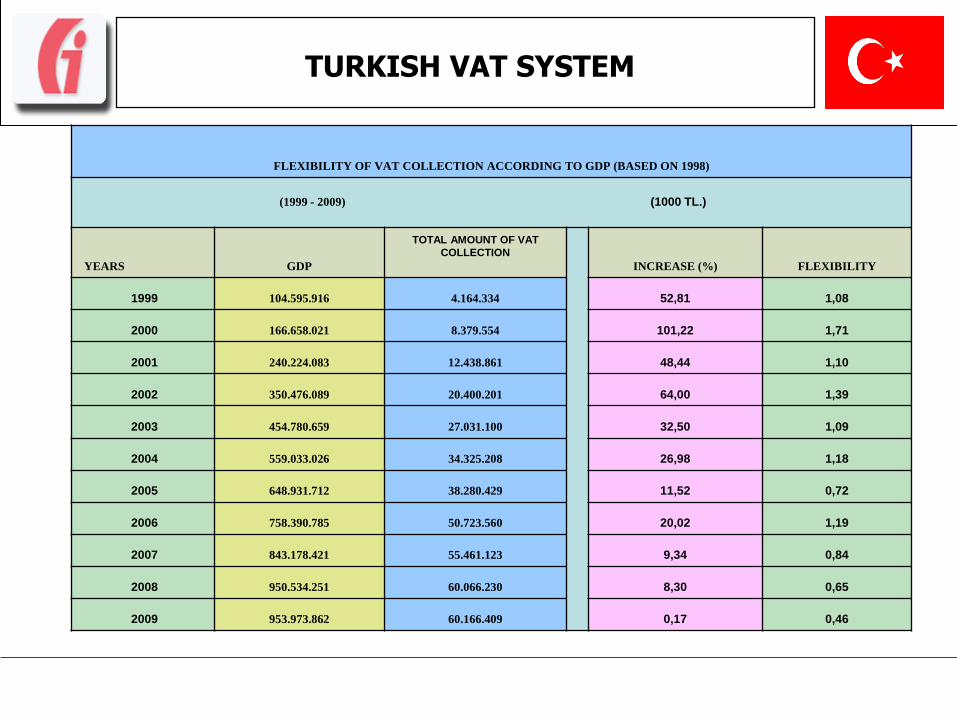

TURKISH VAT SYSTEM

FLEXIBILITY OF VAT COLLECTION ACCORDING TO GDP (BASED ON 1998)

(1999 - 2009) (1000 TL.)

YEARS GDP

TOTAL AMOUNT OF VAT

COLLECTION

INCREASE (%) FLEXIBILITY

1999 104.595.916 4.164.334 52,81 1,08

2000 166.658.021 8.379.554 101,22 1,71

2001 240.224.083 12.438.861 48,44 1,10

2002 350.476.089 20.400.201 64,00 1,39

2003 454.780.659 27.031.100 32,50 1,09

2004 559.033.026 34.325.208 26,98 1,18

2005 648.931.712 38.280.429 11,52 0,72

2006 758.390.785 50.723.560 20,02 1,19

2007 843.178.421 55.461.123 9,34 0,84

2008 950.534.251 60.066.230 8,30 0,65

2009 953.973.862 60.166.409 0,17 0,46

TURKISH VAT SYSTEM

• VAT was introduced by the Directive 77/388/EEC, 17 May

1977 (6th Directive)

• From 1st January 2008 a new directive 2006/112/EC

• Each Member State's national VAT legislation must comply

with the provisions of EU VAT law as set out in Directive

2006/112/EC

• Now EU have 27 Countries

EU VAT SYSTEM

• Before the abolition of the customs control inside the European

Union (1993), the customs officer controlled the physical

transport from one country to another

• Since 1.1.1993, there is no check of the goods transported

from one member state to another

EU VAT SYSTEM

• Intra-community supplies/acquisitions = All the transactions

inside the Community

• Exports/Imports = All the transactions for or from the

countries outside the Community. They can’t use these

terms for transactions inside Community

• The customer is registered for VAT in another Member

State and has supplied his VAT number to the supplier

• The goods are dispatched or transported by the customer

or the supplier or by a person acting on their behalf from

member state of the supplier to another member state

EU VAT SYSTEM

OECD ANKARA

MULTILATERAL

TAX CENTER

The OECD Ankara Multilateral Tax Center has been established in 1993 based on a Memorandum of Understanding between the OECD and the Republic of Turkey. Other OECD Multilateral Tax Centers : Budapest Seoul Vienna Mexico

LEGAL BASIS

BUDGET

In general, costs of the OECD Multilateral Tax

Centers are being covered by the total budget composed of voluntary cash and in-kind contributions of the OECD member countries.

The expenditures of the OECD Ankara Multilateral Tax Center are also being covered both by cash and in-kind contribution of the Turkish Revenue Administration.

EVENTS

3869 mid and high-level tax officials

42 countries from 1993 to date

Experienced experts and high level officials from OECD Secretariat and member countries Senior officials from the Turkish Revenue Administration have also been contributing as lecturer in events held in Ankara and in other OECD Centers.

Events held in Ankara Multilateral Tax Center are mostly related to International Taxation System and current tax topics.

Generally all events include case studies and workshops where participants from different countries have the opportunity to present their practices.

EVENTS (Cont’d)

EVENTS (Cont’d)

Encourage non-OECD economies to adopt taxation practices which promote economic growth through the development of international trade and investment.

Aim to associate non-OECD economies with international best practice in taxation and provide a forum for multilateral dialogue between the OECD and non-OECD economies.

1993-2010

NUMBER OF PARTICIPANTS

Albania 560

Armenia 141

Azerbaijan 339

Bangladesh 10

Belarus 140

Bosnia 13

Bulgaria 15

Cambodia 7

China 122

Croatia 3

Czech Rep. 13

Egypt 55

Estonia 14

Georgia 383

Hungary 10

India 12

Indonesia 17

Kazakhstan 156

Kosovo 65

Kyrgyzstan 108

Latvia 27

Lithuania 22

Macedonia 9

Mongolia 383

Moldova 219

Montenegro 3

Morocco 71

Pakistan 41

Poland 39

Romania 63

Russian Fed. 317

Saudi Arabia 14

Sierra Leone 3

Slovak Rep. 8

Slovenia 20

South Afr. Rep. 4

Tajikistan 82

Turkmenistan 138

Ukraine 102

United Kingdom 1

Uzbekistan 115

Vietnam 5

TOTAL 3869

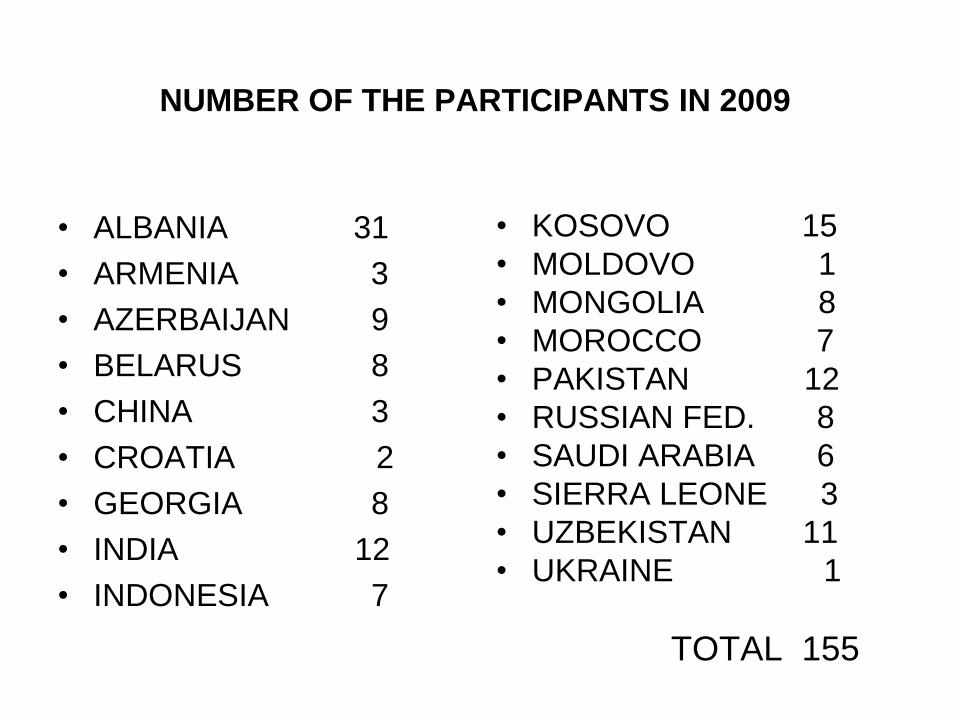

NUMBER OF THE PARTICIPANTS IN 2009

• ALBANIA 31

• ARMENIA 3

• AZERBAIJAN 9

• BELARUS 8

• CHINA 3

• CROATIA 2

• GEORGIA 8

• INDIA 12

• INDONESIA 7

• KOSOVO 15

• MOLDOVO 1

• MONGOLIA 8

• MOROCCO 7

• PAKISTAN 12

• RUSSIAN FED. 8

• SAUDI ARABIA 6

• SIERRA LEONE 3

• UZBEKISTAN 11

• UKRAINE 1

TOTAL 155

TOPICS OF THE EVENTS HELD IN OECD ANKARA MTC

Transfer Pricing

Tax Incentives

Tax Policy-Modeling

International Tax Avoidance and Evasion

Auditing Multinational Enterprises

Tax Treaty Issues

Application of Tax Treaties

Auditing Small and Medium Enterprises

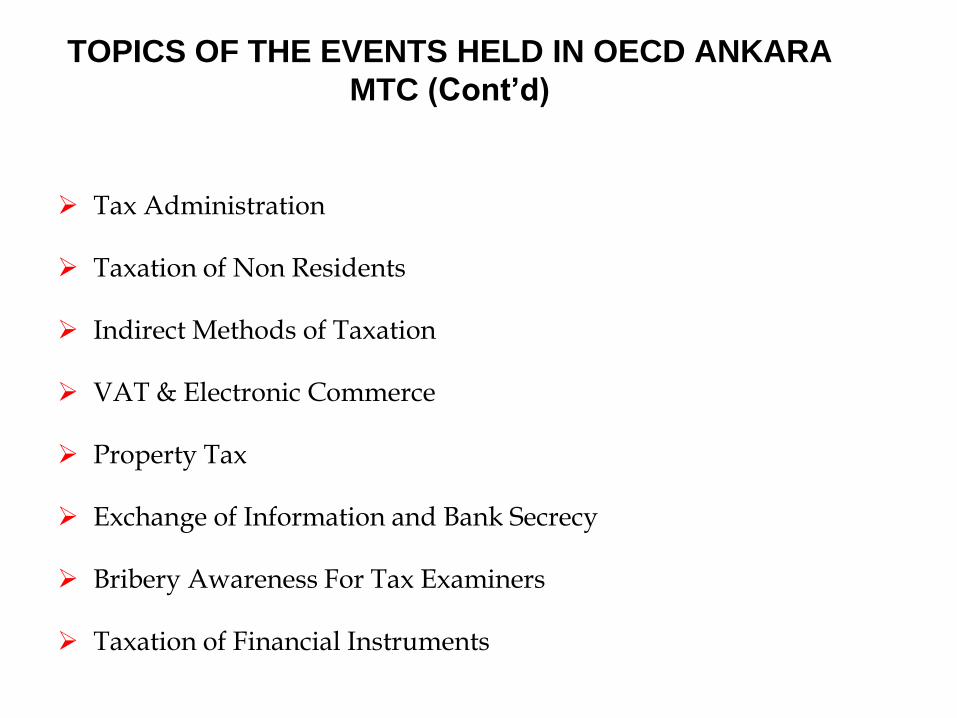

TOPICS OF THE EVENTS HELD IN OECD ANKARA

MTC (Cont’d)

Tax Administration

Taxation of Non Residents

Indirect Methods of Taxation

VAT & Electronic Commerce

Property Tax

Exchange of Information and Bank Secrecy

Bribery Awareness For Tax Examiners

Taxation of Financial Instruments

BILATERAL SEMINARS

Due to the protocol between the Turkish Ministry of Finance Revenue Administration and the Turkish International Cooperation Agency (TICA), Revenue Administration arranges seminars up to demand of the transition economies.

Sharing experience with the officials of the participant country on

tax matters

Providing legislative infrastructure

Developing the cooperation on taxation system

CERTAIN TOPICS OF THE SEMINARS

• Tax Procedure Law, Personal-Corporate Income Tax, VAT, Special

Consumption Tax

• Tax Audit

• Electronic Declaration, Risk Analysis and Automation System

• Tax Exemptions

• Tax Collection and Administration of Tax

• The System of Documentation, Cash Register Application, Registry

and Conveyance of Taxpayer

• Restructuring Process of Revenue Administration

COUNTRIES INVOLVED IN THE SEMINARS IN

A BILATERAL BASIS (2005-2010)

• Azerbaijan

• Bangladesh

• Bosnia Herzegovina

• China

• Kosovo

• Kyrgyzstan

• Mongolia

• Morocco

• Pakistan

• Tajikistan

• Turkmenistan

• Uzbekistan

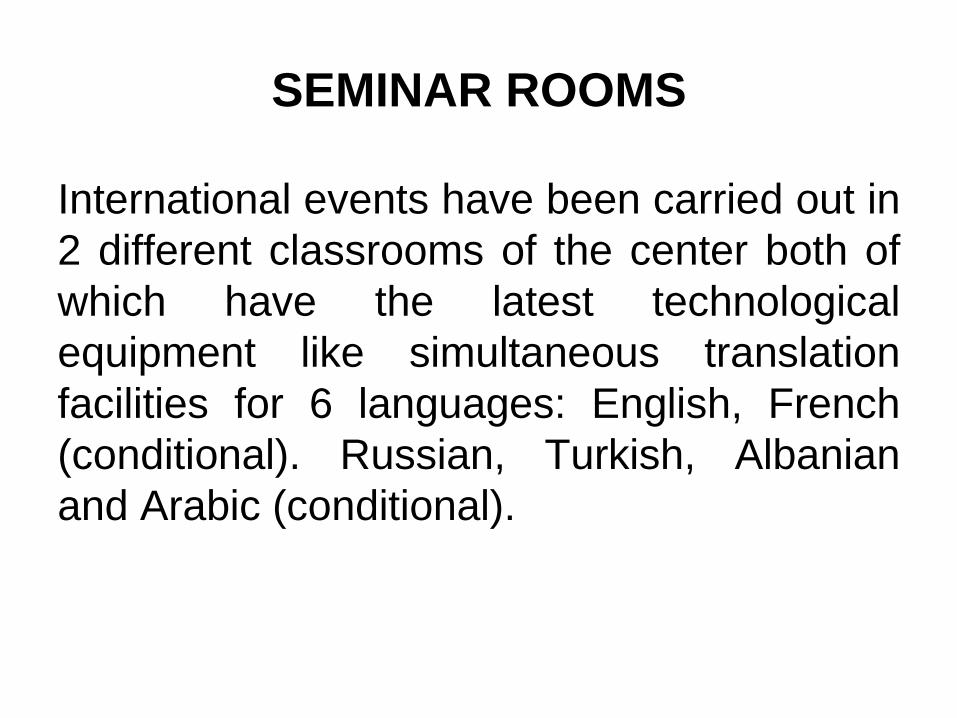

SEMINAR ROOMS

International events have been carried out in

2 different classrooms of the center both of

which have the latest technological

equipment like simultaneous translation

facilities for 6 languages: English, French

(conditional). Russian, Turkish, Albanian

and Arabic (conditional).

OVERLOOK ON MENA PROJECT AND

OECD ANKARA MTC

Republic of Turkey and OECD have signed a

Memorandum of Understanding in order to establish

OECD Ankara MTC, for a period of five years in 1993,

which can be extended for five-year-periods. A

provision adopted at the last extension in 2008 allows

the technical facilities of the OECD-Ankara Multilateral

Tax Centre to be utilised for MENA project.

Turkey’s annual in cash contribution to the MENA

project is € 75.000.

THANK YOU