ttr 040315e imageteil · dominated by heidelberger druck, man roland and koenig & bauer,...

TRANSCRIPT

technology and services

A N N U A L R E P O R T

2003

This division, representing 10.1 percent of revenue, operates in two distinct markets: since 1995,

technotrans has been a successful supplier of systems used in the production of optical storage

media – CDs and DVDs. More recently we have been using this expertise to make inroads into a

new area of application, microstructure technology.

M I C R O T E C H N O L O G I E S

Services designed to complement the technical divisions round off technotrans' portfolio of

activities. These services include providing customer support for the installation, maintenance

and operation of systems, and compiling technical documentation, including for manufacturers

from other sectors. Services generated 23.7 percent of revenue in 2003.

S E R V I C E S

technotrans systems and equipment control and monitor a wide range of liquid technology

processes in the offset printing environment. We have steadily been expanding the product range

over many years. The Print Division contributed 66.2 percent of revenue in the 2003 financial year.

P R I N T

REVENUEby segment

Micro Technologies…10.1%

Services…23.7%Print…66.2%

73,373

58,212

4,503

10,580

25,588

10,297

8,403

8,247

8,169

4,246

5.8

0.71

0.38

6,000

29,059

72.5

15.5

40,073

13,899

32,383

25.2

6.4

411

17,147

23.4

179

2,796

1,449

2,000,000

22.86

11.12

€'000

€'000

€'000

€'000

€'000

€'000

€'000

€'000

€'000

€'000

%

€

€

€'000

€'000

%

%

€'000

€'000

€'000

%

%

€'000

%

€'000

€'000

€'000

€

€

104,927

76,650

11,808

16,469

34,389

12,934

10,755

9,676

9,700

5,405

5.2

0.88

0.42

6,180

36,778

49.6

16.4

74,195

20,152

59,697

16.2

53.8

543

24,632

23.5

193

4,574

- 15,572

2,060,000

53.17

12.82

130,990

98,733

11,526

20,731

41,623

14,150

10,726

9,130

7,525

3,421

2.6

0.53

0.23

6,600

54,756

55.3

7.5

99,042

24,244

80,450

9.4

37.7

687

33,634

25.7

191

4,272

- 6,827

2,200,000

48.02

9.83

117,012

80,623

10,861

25,528

37,695

10,897

7,587

5,887

5,626

2,620

2.2

0.40

0.20

6,600

51,720

55.9

4.9

92,541

21,981

74,291

7.2

29.5

639

31,920

27.3

183

10,077

7,470

6,600,000

17.85

4.81

02 01 00 9903

TECHNOTRANS GROUP KEY DATA (IFRS)

* Earnings per share, dividend and historical share prices adjusted to reflect share-split1 EBIT = operating profit + foreign currency gains/losses2 EBITA = EBIT + amortisation of goodwill3 EBITDA = EBIT + amortisation of goodwill + depreciation of property, plant and equipment

and intangible assets4 capital employed = interest-bearing liabilities + equity5 ROCE = EBIT / Capital employed6 Gearing = (interest-bearing liabilities – liquidity) / equity7 Cash flow = Net cash from operating activities acc. to Cash flow Statement8 Free cash flow = Net cash from operating activities + net cash used for investments acc. to Cash flow Statement

106,737

70,631

10,774

25,332

35,929

12,685

9,084

7,522

7,377

-10,960

-10.3

-1.66

0.30

6,600

36,288

50.1

-30.2

72,391

24,318

55,305

13.3

27.5

593

29,275

27.4

180

6,491

5,394

6,600,000

12.64

3.81

Profit

Revenue

Micro Technologies

Services

Gross profit

EBITDA 3

EBITA 2

Operating Profit

Earnings before interest and tax (EBIT) 1

Net profit for the year

as % of revenue

Earnings per share (IAS) *

Dividend per share*

Balance sheet

Issued capital

Equity

Equity ratio

Return on equity

Balance sheet total

working capital

capital employed 4

ROCE 5

Gearing 6

Employees

Number of employees (yearly average)

Employee costs

as % of revenue

Revenue per employee

Cash flow

Cash flow 7

Free cash flow 8

Shares

Number of shares (at 31.12)

share price (max) *

share price (min) *

Systems supplier for liquid technology

technotrans has been concentrating

on applications for offset printing since

the early 1980s. The product range

has gradually been extended and now

comprises a wide range of systems

and equipment for controlling and moni-

toring liquid technology processes in

printing. Major printing press manufac-

turers worldwide are our key custom-

ers. They frequently equip their printing

presses ex works with technotrans

equipment. Various products in addi-

tion aimed directly at end users have

been developed in recent years; these

further automate procedures in the

printing shop or help to use resources

more efficiently.

…page 4

1 9 8 0 >

Along with the increasing mass pro-

duction of CDs, technotrans likewise

gained a foothold in this growing mar-

ket. Customers use our systems to

produce a kind of »negative« of optical

storage media, so that copies of these

can then be made. technotrans has

been the unchallenged market leader

for these electroforming systems since

2001. Once again, they are based on

a liquid technology process.

…page 10

1 9 9 5 >

The same technology as in the CD/DVD

Division is used in the manufacturing

of minute components measuring no

more than a few hundredths of a mil-

limetre. This still young area of appli-

cation is finding its way into markets

as diverse as telecommunications,

biotechnology and display technology,

and is yet to realise its potential.

…page 10

2 0 0 1 >

CD/DVD

MICROSTRUCTURETECHNOLOGY

■ Core skill of liquid technology■ Concentration on niche markets■ Systematic broadening of product range

Letter to the Shareholders…2 | Divisions…4 | R&D…18 Employees…20 | Share/Corporate Governance…22 |

Group Management Report…26 | Consolidated Financial Statements…44 | History…99

technotrans is a leading systems supplier of plant for the production of

print media and microstructures. Within these niche markets, we have been

concentrating successfully on applications based on our core skill of liquid

technology for many years now. With our 13 locations and over 600 employ-

ees, we enjoy a presence in all major markets worldwide. In close coopera-

tion with our customers, we are tapping new potential by steadily broadening

our range of products and venturing into new markets and segments. Our

strategy focuses on sustained, earnings-driven development.

technotrans is a systems supplierof high-tech plant and servicesfor the production of print mediaand microstructures.

Dear shareholders, dear business associates,

2003 was the third year in succession in which our company was confronted with

enormous challenges due to the unsatisfactory progress of those markets in which we

operate. The printing industry has been experiencing the worst crisis in its history

since 2001, and the propensity to invest in Micro Technologies likewise suffered from

the paralysis of the global economy. We can at least report that our Services Division

has fared well in this adverse climate. technotrans now generates 21 percent of its

revenue in the important North American markets; the exceptionally low value of the

dollar consequently further undermined our revenue. Our competitive position, on the

other hand, if anything improved last year as a result of a number of smaller players

going under.

Despite the difficult circumstances, we succeeded in posting an operating result of

€ 7.5 million from revenue of € 106.7 million in 2003. In view of the situation in the

CD/DVD segment, which has still failed to live up to the expectations that prompted

us to acquire the Toolex Division in 2001, we have reduced the remaining goodwill.

As a reflection of the fact that we purchased the American company Ryco, of Chicago,

when the Print sector was booming in 2000, we have likewise adjusted the acquired

goodwill to a more conservative level. In view of these measures, for the first time in

the company's history we report a loss of € 11 million, but at the same time we have

adjusted the risks in the balance sheet and have consequently already absorbed po-

tential burdens in forthcoming years in the 2003 annual accounts. We have therefore

cleared the way for an even more profitable future.

This future will continue to bear the hallmark of our long-standing successful strategy

of growth: the broadening of our product range with a view to boosting our content per

printing press. We had already disclosed details of one such measure in the form of

2

the scheduled takeover of Baldwin. Following the collapse of this transaction by

Baldwin, we once again find ourselves in the position of competitors in the market-

place, and will for our part concentrate on further strengthening the sound position

that technotrans enjoys among its customers. We will also undoubtedly examine

other options more closely and opt for the most promising among them.

The experience of recent years has confirmed something we have always believed:

that our company is capable of taking on exceptional challenges and overcoming

them successfully. Our employees have played a major part in this; thanks to their

remarkable dedication, creativity and inimitable feel for the right decision, they were

instrumental in enabling us to pave the way for future success last year. We are proud

and appreciative of them, and look forward to tackling the exciting tasks of the future

together with them. We know they will remain instrumental to the success of our

group.

Thank you for your interest in our Annual Report; we hope that you will continue to

follow the fortunes of technotrans. We are convinced that 2004 will be an interesting

year for all of us, not least because of the forthcoming DRUPA exhibition.

L E T T E R T O T H E S H A R E H O L D E R S 3

Wolfgang Breme, John A. Stacey, Ralph Teunissen, Heinz Harling

4

PRINTD I V I S I O N

D I V I S I O N S 5

technotrans has been honing its profile as a supplier to the printing

industry since the early 1980s, and is now a leading system partner

with an international presence. The product range with liquid technology

at its core has been systematically extended. We have deliberately

concentrated on niche markets in which we have been able to become

a leading player.

The clear strategy, our high degree of specialisation and the close, constructive coop-

eration between ourselves and the leading printing press manufacturers that often

cuts in as early as the development phase for new machinery has helped technotrans

to evolve into a leading international system supplier in the print sector.

Old economy meets high tech

The present-day printing industry stretches back to Johannes Gutenberg's invention

in around 1450 AD, and can therefore with some justification be classed as an "old

economy" activity. The market volume in 2002 totalled some 12 billion euros world-

wide, with printing presses and accessories accounting for the lion's share of this

figure. Two-thirds of all presses worldwide are German-built, with the market being

dominated by Heidelberger Druck, MAN Roland and Koenig & Bauer, followed by

Japanese manufacturers such as Komori, Ryobi and Mitsubishi, and the American

company Goss.

Some two-thirds of all printed products worldwide are produced by offset printing: busi-

ness cards, posters, newspapers, and also this Annual Report. There are many argu-

ments in favour of offset printing: among other things, its high quality and the fact that

the production process is straightforward and economical. Depending on the number of

pages and the quantity to be printed, cut sheets of paper are printed by the sheet-fed

"More technotransper printing press"

■ High-tech products for offset printing

■ Around 80 percent of revenue generated

as partner of the printing press manufacturers

■ In the wake of the economic crisis, the industry

is looking forward to the DRUPA in 2004.

6

method, or in the case of very high print runs rotary offset printing is used, with the

paper supplied from a reel.

The technology of offset printing is based on the fact that oil and water repel each

other. Zones which attract the oil-based printing ink are created on the printing plate

by photo-technical means. The other zones repel the ink, instead of which they are

wetted with a water-based dampening solution. The interplay between these two liquids

produces the printed image on the printing plate, which is then reproduced on the paper,

up to 18,000 times an hour in the case of a sheet-fed offset printing press. This is

moreover not the only area in which the old economy and high technology have formed

a rewarding symbiotic relationship.

Liquid technology everywhere on the printing press

The first devices with which technotrans became world market leader in the early 1990s

were systems for preparing this dampening solution. They mix together the solution from

water, alcohol and a variety of chemical additives, and are capable of supplying the

printing press continuously with several hundred litres of this solution per hour. Today,

all leading printing press manufacturers fit most of their presses with technotrans

equipment ex works.

In the years which followed, we systematically extended the range of products based

on liquid technology, adding for example ink roller temperature control units. The oil-

based ink reacts highly sensitively to changes in temperature. In order to stabilise the

printed results, the temperature of the ink rollers is adjusted to compensate for fluc-

tuations in the production conditions. Ink supply is another example: technotrans now

offers an extensive range of equipment and systems for the ink supply to printing

presses. These range from manual aids for smaller or older presses, through fully

automatic supply systems for cutting-edge sheet-fed offset printing presses, to supply-

ing large newspaper presses from central tanks, complete with the pumps, the compo-

nents for monitoring the levels in the tanks and for gauging ink consumption levels.

Varnish is finding increasing use in high-end printed productions. Glossy or protective

coatings refine the appearance of printed articles. technotrans' contribution: a device

that preheats the varnish so that it reaches the printing press at the correct consistency.

D I V I S I O N S 7

World market leader: dampening solution preparation from technotrans

The first technotrans products that penetrated the inner workings of printing presses

were spray dampening systems intended primarily for large newspaper presses. The

spray dampening systems technology of our American subsidiary has been installed

several thousand times over, and "microspray" permits an ultra-even coating of the

dampening solution thanks to special lamellar valves.

An ecological approach to printing that pays its way

Many technotrans devices are essential to the proper functioning of the printing press.

Others have been developed to make the printing process more efficient, for instance

by boosting the degree of automation or helping to make better use of the resources

in question. Certain technotrans products in addition combine persuasive economic

benefits with hard-and-fast ecological aspects. Such as ecoclean, a product range for

the recovery of washing agent. In order to clean the printing cylinders of the press from

ink residue among other things, solvent-based cleaning agents are used for the regular

washing processes. ecoclean enables the printer to recondition these cleaning agents

and use them again. This drastically reduces not only the consumption of cleaning

agent, but also the amount to be disposed of, as well as the cost this involves.

2004: a DRUPA year

The printing industry is dominated by German companies, so it comes as no surprise

that the biggest exhibition in the world for this industry, the DRUPA, takes place in

Düsseldorf every four years. This year's exhibits are likely to focus on new develop-

ments that boost the efficiency of printing presses, make them simpler to operate

and secure greater flexibility for the customer.

ecoclean.line saves money and preserves resources.

8

Alongside a wide range of improved and extended functions on existing systems, techno-

trans will once again be presenting an entirely new product: spinclean. This device is our

first product to target customers from the pre-press stage. spinclean has been devel-

oped for cleaning the developer fluid used in CtP plate exposure. In field tests the spin-

clean has demonstrated the ability to cut consumption of developer fluid by over 70

percent. The response from its first customers was correspondingly positive, and we

await the official market launch at this year's DRUPA with very high hopes.

Potential for the future

The printing industry has experienced its worst ever crisis in recent years, but there

have been increasing signs of a turn in the tide since the second half of 2003. We have

been doing our homework: after years of growth, occasionally of a sensational magni-

tude, we have latterly taken the opportunity to optimise our processes, cut our costs and

steadily strengthen our market position thanks in no small measure to our healthy

financial state.

Experience has shown that the printing industry worldwide expands at a similar rate

to gross domestic product. The market for system suppliers, which has an estimated

volume of almost 600 million euros in the area of our core skills, is developing with

appreciably greater dynamism. In the context of our long-term strategy, we will contin-

ue to seize the opportunities that present themselves. The present circumstances in

particular, dominated as they are by consolidation, provide a particularly favourable

opportunity to target and exploit fresh potential.

In view of the overall volume of our market and position, we are confident of returning

rapidly to our former trend of growth if the underlying economic figures move closer to

the positive zone. There is ample potential for our high tech in the old economy.

D I V I S I O N S 9

MARKET SHARE PRINTING PRESS MANUFACTURERS

MAN Roland (G)…19.7%

Koenig & Bauer (G)…16.5%

Komori (J)…10.6%

Other…12.5%

Mitsubishi (J)…5,8%

Heidelberger (G)…34.9%

technotrans has been exploring additional applications for its liquid

technologies in the field of Micro Technolgies since 1995. technotrans

systems are used for the manufacture of tools that are required in the

production of optical storage media, in other words CDs and DVDs.

These systems have recently also been used in the volume production

of minute components measuring just a few hundredths of a millimetre.

D I V I S I O N S10

D I V I S I O N

11

MICRO TECHNOLOGIES

Taking its core skill of liquid technology as its starting point, technotrans has been

developing the systems required in the manufacture of optical storage media, meaning

initially CDs (compact discs) and then DVDs (digital versatile discs), since 1995. We

have been the world leader in this market since 2001.

The "masters" for more than half of all these silver discs worldwide are made on technotrans systems

In order to make CDs and DVDs out of plastic, the digital data first needs to be pre-

pared in the form of a tool for the injection moulding process. To this end, the data is

burned into a varnish coating with the aid of a laser beam. The burned areas are then

rinsed and the structure that is left behind is coated with a wafer-thin layer of metal.

A solid nickel disc is then produced on this surface in a technotrans system by means

of an electrodepositing process – a liquid technology process.

"Our smallest worker is the nickelmolecule"

■ World market leader for systems for the production of CDs and DVDs

■ Strategic line: venturing into new markets with familiar technology

■ Microstructure technology with potential for the future

12

This master disc constitutes the basis of the subsequent replication process, where

polycarbonate is pressed onto the nickel disc up to 150,000 times, at a pressure run-

ning into tonnes. The result is a very familiar object: CDs containing everything from

music to computer programs, and DVDs with films or music concerts.

Market with big aspirations: microstructure technology

There is already a wide range of additional applications for this technology. Minute

components are used for example in sensors, in glass fibre technology and in biotech-

nology. These components, which are often just a few hundredths of a millimetre in

size, are produced using the same technology as optical storage media. We are suc-

cessfully venturing into these new markets of microstructure technology.

In 2003, for example, a system that is to be used for the production of displays was

shipped to Taiwan. A special plastic disc to which tiny lenses are applied using the

technotrans plant ensures that the displays are illuminated more evenly and efficiently.

technotrans systems on which work is already being performed on potential series pro-

ducts of the future are in use at several research and development centres worldwide.

The Micro Technologies Division still accounts for 10 percent of technotrans revenue,

but there is immense potential for these innovative applications. This is why we have

invested extensively in this expertise over the past two years, and gathered experience

in this innovative area. We have identified numerous products as a result, and are

collaborating on their realisation. It is entirely possible that one or more of these will

achieve a breakthrough and create a new market. It is equally possible that we will

need a little more time and patience before this breakthrough materialises.

D I V I S I O N S 13

The moulds used in the manufacturing of microstructure components are produced on technotrans systems.

technotrans' two technical divisions are complemented by services

through which we support the customer for instance with the install-

ation or operation of systems, or provide assistance in the event of

hitches. Our technicians also serve as our "finger on the pulse" of

the market, enabling us to steadily improve in our efforts to meet

the customer's needs.

D I V I S I O N S14

15

D I V I S I O NSERVICES

technotrans equipment is used for governing applications that are frequently of critical

importance to the customer, as a result of which maintaining its availability is general-

ly a top priority. technotrans has consequently developed a comprehensive range of

services to provide our customers with the best possible support, in line with their

individual preferences.

This support often starts as early on as the installation and training processes, be-

cause expert users not only achieve better results in their everyday use of our equip-

ment; they are also more satisfied customers.

Rapid response for emergencies

If an operating fault should nevertheless occur, a carefully coordinated chain of mea-

sures cuts in, like interlocking gearwheels, to come swiftly to the customer's aid. The

international hotline makes an initial attempt to narrow down the source of the prob-

lem and produce interim solutions. Sophisticated logistics ensure that the necessary

spare parts are shipped as swiftly as possible to the customer, who, thanks to the

modular design of our equipment, will then often be able to exchange the relevant part

themselves. If it is nevertheless necessary to call out a member of our service team,

aid can be summoned straight away.

"Services when andwhere the customerneeds them"

■ Comprehensive support for customer-critical applications

■ Services to enhance customer satisfaction

■ Technical documentation offering own software solution

16

And many emergencies can be avoided by preventive maintenance, which we are also

able to provide via the Internet. Our experience has shown that many faults can be

anticipated from the operating data, with the result that regular operations can be

maintained with minimal effort.

Technical documentation for high-tech products

technotrans has also been offering a technical documentation service for some time.

This term includes such documents as installation, maintenance, operating and ser-

vice manuals, whether available in printed form, on CD-ROM or on the Internet. As an

international system supplier, we very early on developed these activities into a core

skill of our group and also offer other manufacturers a documentation service for their

technical systems and equipment in whatever language it is required.

We have now even developed our own software solution, which we are marketing with

notable success. As well as providing efficient translation management, this tool for

example makes it easier for the customer to update documentation efficiently. If a com-

ponent or assembly has been modified, the program knows at the press of a button

which passages in the documentation are affected by this change. We believe that

documentation is a core skill of technotrans, and do our utmost to investigate and

find every opportunity for producing it even faster and more efficiently.

The operating status of numerous devices can alreadybe monitored over the Internet, and emergencies thuspre-empted.

D I V I S I O N S 17

"R&D constitutes the basis for our strategy"

■ R&D target is to set new standards

■ In 2003 we invested € 3.6 million on R&D

18

As a technology company, technotrans naturally attaches considerable importance to

research and development. This field of activity in effect serves as the basis of our

strategy: we aim to expand or grow in new markets with our established technology, by

implementing new technology in established markets.

Automatic ink supply ink.line replaces the spatula

Our development activities – free from the pressure of day-to-day business yet never

very far from the customer – focus on very specific projects, the results of which play

a part in continuing to boost the technotrans content per printing press. A typical ex-

ample: ever since the invention of offset printing, printers have had to stand next to

their sheet-fed machines and dispense printing ink into the ink duct manually. A tedious

chore that is now superfluous, because we have replaced the need for a spatula with

the automatic ink supply system. The sensor-controlled ink.line system dispenses the

ink from cartridges to precisely the ink duct where it is needed. The printer can now

concentrate instead on the core task, which is the real key to creating "value added".

Over 6,000 systems have been installed worldwide since DRUPA 2000, when ink.line

marked its debut.

R&D with environmental benefit: spinclean

Greater automation, the desire to boost efficiency or simply the ambition to use

resources more effectively: the motives of our engineers are as diverse as the pro-

ducts that they develop. At this year's DRUPA, we will be unveiling the spinclean, for

example: a device that continually cleans the developer fluid that is used in the pro-

duction of printing plates. Initial field tests have revealed that at least 70 percent of

R E S E A R C H & D E V E L O P M E N T 19

R&D EXPENSES in million €

3.7 3.3 3.4 2.3 3.0

9999 0000 0011 0022 0033

% of sales

the developer fluid can be recovered in this way. This is a technology that rapidly pays

its way and protects the environment, because it also reduces the amount of chemi-

cals that need to be disposed of.

Development of new standards through listening to the market

In addition to developing new technologies and products, the aim of development is to

throw established ideas open to question. Part of this involves listening to the market

and identifying potential trends in customers' everyday practices. By adopting this

approach, we have succeeded in developing an array of new filtration systems, includ-

ing the adoption of separator technology in dampening solution supply devices. And as

so often in the past, we are convinced that this pioneering technology again will estab-

lish a new benchmark in the market.

We have also embarked on a quest to establish the standard in the domain of

microstructure technology. Over the past two years we have invested considerably in

the development of series-production devices that can be used to manufacture minute

components. Here too, we believe that standard technology will be used when industrial-

scale production gets off the ground. It is our aim to cement this market lead now.

We invested around € 3.6 million on development activities last year, thus making a

significant contribution towards consolidating and building on our position as a tech-

nology group in every market segment. To complement our activities, we are conduct-

ing cross-company research projects and collaborating with other research institutes.

A sound investment in the future of technotrans.

5.0 3.1 2.6 2.0 2.8

technotrans is a young company which offers its employees a distinctly international

working context, for all the provincial location of its headquarters in Sassenberg, in

the Münster region. The corporate philosophy of "Think-Learn-Act", in which aspects

such as customer orientation and open communication play as central a role as re-

sponsiveness and the challenge to question established concepts, is acted out direct-

ly in the day-to-day working environment. This means flat hierarchies, short decision-

making routes and ample space for creativity.

technotrans' employees are likewise young, with an average age of 36. More than

one-fifth of them have an academic education, including a large number of graduates

in various engineering disciplines. They particularly appreciate the freedom that techno-

trans gives them to attain their objectives. A system of remuneration that closely re-

flects personal performance and a group-wide stock options scheme ensure that all

employees are able to share directly in the company's success.

This climate that is characterised by trust and a genuine team spirit has also made

it possible to overcome successfully the economic challenges of the past few years.

From a shorter working week to wage concessions and short-time, no measure was

left unexplored as a means of steering the company through the industry-wide crisis.

The cooperative attitude of the Works Council deserves particular mention in this

specific connection. Thanks to these measures, job losses since 2001 have been

"Ample latitude for our employees"

■ Promoting frank exchanges and entrepreneurial thinking through

the corporate philosophy of "Think – Learn – Act"

■ Prominence of training and advancement at the company

■ Sense of solidarity even in difficult times

20

kept just a little above 100. This trend was moreover reversed in the latter months of

2003, and for the first time in a long while production capacity was increased. There

were 596 employees at technotrans at the end of the year.

Learning is an elementary pillar of technotrans' corporate culture, and training and ad-

vancement consequently enjoy a prominent status at the company. Each year, school-

leavers embark on apprenticeships in various vocations at our company. In view of

the chronic shortage of apprenticeships in Germany, we have in addition decided to

increase significantly the number of apprentices taken on by technotrans in the cur-

rent year. The company moreover offers its employees a wide range of opportunities

for acquiring additional specialist and personal qualifications. These include English

courses, special management development schemes and product training courses,

and even back training and give-up-smoking courses.

As a listed company, technotrans very early on started to help its employees to save

for the longer term. In recent years, a portion of the voluntary Christmas bonus has

regularly been paid to employees in the form of shares. Over the years, outside ex-

perts have helped us to develop an extensive range of individual savings products now

comprising three alternative forms of pension fund, a direct insurance policy, two ver-

sions of a second top-up pension and capital formation contributions. In-depth infor-

mation events and individual advisory sessions were arranged to enable every em-

ployee to choose which savings scheme best suited their needs.

E M P L O Y E E S 21

EMPLOYEES ACCORDING TO QUALIFICATION

Graduates…21%

Trainees…4%

Technical…22%

Other…9%Specialist trades…44%

NUMBER OF TECHNOTRANS EMPLOYEES

439 580 698 621 596

9999 0000 0011 0022 0033

Germany

outside Germany

technotrans AG has been a listed company since March 1998. Both we and our

shareholders have been subjected to a roller-coaster experience on the Neuer Markt

in recent years, with technotrans shares experiencing almost every conceivable turn of

fortune: from an inconspicuous security to a high flyer that for a long time flourished

independently of market trends, it was included in the Nemax 50 index in mid-2002

before finally plummeting irrationally and over the odds.

The shares started 2003 on 4.89 euros. The switch to Deutsche Börse's Prime

Standard and the abolition of the Nemax 50 blue-chip index finally put an end to the

fundamentally incomprehensible nosedive in the share price. The tide turned in mid-

March 2003, after our shares had hit an all-time low of 3.81 euros. By way of compar-

ison, the issue price in 1998 was 11.23 euros. This exaggeratedly depressed price

was corrected as the year went on, with the shares closing on 11.65 euros at the

end of December. This represents an increase of over 200 percent compared to the

record low. Alongside the fact that the shares were fundamentally undervalued, this

price appreciation was attributable to the brighter prospects for the economy in gen-

eral and the markets in which technotrans is active.

"technotrans sharesback on track"

■ Switch to the Prime Standard

■ Considerable investor confidence in our business model

■ Open dialogue with the capital market

22

STOCK EXCHANGES: FRANKFURT, XETRA ISIN DE0007449001

SHAREHOLDER STRUCTURE as of 31.12.2003

Free Float…87.5%

WestKB…5.45%

Management…7.05%

S H A R E / C O R P O R A T E G O V E R N A N C E 23

Year-high

Year-low

Year-end

Earnings per share

Cash flow per share

Dividend per share

* Dividend proposal

0203

KEY DATA

12.64

3.81

11.65

-1.66

1.02

0.30*

17.85

4.81

4.89

0.40

1.53

0.20

€

€

€

€

€

€

TECHNOTRANS SHARE MOVEMENT

175%

02.01.2003 = 5.08 €

250% 18.02.2004 = 13.90 €

TecDax

technotrans

We have naturally maintained a dialogue with the capital market throughout these

times, regularly staged roadshows in Germany and internationally, and were again able

to welcome over 30 analysts to our annual conference. Following this difficult year, we

can even take some pride in the fact that our investor base remains virtually unchanged.

The basis for this stability – an understanding of the company and its business model

as well as confidence in the management – is something we detected in many of the

discussions we held. This is the best motivation for us to continue along our chosen

path of partnership-driven success on the capital market.

Our objective is maximum transparency, as for example explicitly stated in the Investor

Relations section of our website. With a view to informing all capital market players

simultaneously, we offer an opportunity to register for the email subscription feature.

This enables us to supply interested parties automatically with all current news items

that are of relevance for the ongoing development of the company. We naturally regis-

tered a record number of visits following the disclosure of our plans to acquire Baldwin

in December 2003. We set up a special area providing information on all questions

concerning this topic.

Corporate governance

Most of the principles of corporate governance laid out in the recommendations have

been standard practice at technotrans for many years. The May 2003 version of the

German Corporate Governance Code incorporated further extensive additions, and

while many aspects of the Code reflect the current legal position, a great many of the

specifications are also aimed at companies and circumstances that are not wholly

applicable in the case of technotrans. For this reason, the 2003 Declaration of Com-

pliance by the Board of Management and Supervisory Board contained more qualifica-

tions than in the previous year.

The departures from the Corporate Governance Code relate on the one hand to aspects

that are not yet common practice at technotrans but which are to be taken into account

in the future. These include this corporate governance report in the Annual Report, and

the explanation of departures from the requirements, as well as the announcement of

the basic principles of the remuneration system for the Board of Management on the

Internet and the corresponding notes in the Annual Report, and notification of the Share-

holders' Meeting of the basic principles and changes. We in addition report shareholders'

equity in investments for the first time on page 52 of this Annual Report.

24

Interested parties will find the full current wording of the Declaration of Compliance

in the Investor Relations area of our website. www.technotrans.de

S H A R E / C O R P O R A T E G O V E R N A N C E 25

On the other hand, as mentioned above, various aspects of the Code relate to prac-

tices that are not relevant to technotrans, as a result of which we have decided not to

adopt the Code's specifications on certain matters. These include the requirement of

an excess for D&O insurance cover. The current policies do not envisage an excess,

nor do we perceive any need to take out new policies at the current time. A cap on

gains from our stock options scheme is likewise not envisaged. We provide detailed

information on the scheme on pages 69-70. In view of its special form and demanding

objectives, it serves as an appropriate means of motivating virtually all employees

within the company, and a cap specifically for members of the Board of Management

is neither envisaged nor particularly advisable in this instance.

After carefully weighing up the public interest against the interests of the members of

the Board of Management and Supervisory Board, we have moreover decided to pub-

lish details of their remuneration, broken down according to fixed and variable compo-

nents, but not individually for each member of these corporate bodies. We believe that

the knowledge gained by the public by the latter measure would encroach unreason-

ably on the private sphere of these members.

Group Management Report

26

General economic situation2003 was another year in which worldwide growth predictions failed to materialise.

The weak start to the year could not be made good in the second half, with the result

that the growth originally expected did not in the end take shape.

The underlying economic figures improved in the course of the year: the war in Iraq

was over relatively quickly, and a marked recovery on stock markets foreshadowed the

impending economic recovery. This trend was underpinned by the stabilisation of the

price of oil and comparatively very low interest rates.

Extreme fluctuations on foreign exchange markets, in particular the dramatic apprecia-

tion of the euro against the US dollar, were unable to stop the positive development in

the second half of 2003. In some quarters, the strengthening of the euro was regard-

ed as a sign of new confidence in the single currency.

The US economy made unexpectedly good progress, with domestic product growing by

3.0 percent, and the business confidence index for the eurozone has likewise been

pointing to growth since July. Germany put in a below-par performance with a year of

economic stagnation. The situation on the labour market remained difficult.

Situation in our branchThe printing industry, as the core market of technotrans' Print segment – it accounts

for two-thirds of the company's revenue – experienced a third year of crisis. The

German printing press manufacturers Heidelberger Druckmaschinen AG, MAN Roland

AG and Koenig & Bauer AG – which between them supply two out of three of all print-

ing presses worldwide – reported a sharp drop in orders, which in some categories

were down by more than 30 percent. As a consequence they were obliged to focus on

restructuring measures last year.

This Management Report

as well as the following

sections of the Annual

Report up to page 98

are a translation of the

German original. In the

case of doubt, the

German original takes

precedence.

G R O U P M A N A G E M E N T R E P O R T 27

Advertising spending is to some extent the driving force behind the printing industry.

Spending from this source was decidedly weak at the start of the year, though the

positive signs increased significantly in number in the second half. According to recent

research findings, advertising spending in Germany in 2003 rose by 3.3 percent to its

highest level since 2000. The volume for daily newspapers showed positive progress,

growing by more than 10 percent to € 4.1 billion (by comparison: Internet € 265 mil-

lion, +3.7 percent).

The second technology segment of technotrans, the Micro Technologies Division,

depends on the one hand on the market for systems for the production of optical stor-

age media, and on the other hand on microstructure production facilities. The number

of CDs and DVDs being produced continues to grow worldwide (at varying rates,

depending on format), but the installed capacity of electroforming systems is largely

sufficient to cover this demand. Investment spending in new equipment in the first

instance represents replacement investment. The field of microstructure technology is

rated by experts as a vigorously growing, innovative market that spans a wide range of

branches of industry. The potential for the manufacturing technology of these new

applications is thought to be vast, but cannot yet be clearly demarcated.

Revenue and earnings

Revenue growth delayed until second half

As a result of the protracted crisis in the printing industry, revenues in the first half of

the year were ultimately much lower than had been expected at the start of the year.

Compared with the rest of the world, the markets in the US, Europe and particularly

Germany were manifestly weak. The recovery in the second half of the year brought

the desired turn of fortunes. Revenue rose for the first time in two years in the third

and fourth quarters, in the latter case by more than 9 percent. This was nevertheless

insufficient to achieve the original revenue target for 2003 of € 115-120 million.

Revenue fell short of expectations by around € 10 million, at € 106.7 million (previ-

ous year: € 117.0 million, -8.8 percent).

28

In view of the question marks over an economic recovery in our main markets, we

resolved very early on to take appropriate measures to tackle the continuing fall in

demand. By winding up our production plant in Colchester, England, and transferring

operations to Sassenberg, Germany, in the first half of 2003 we were able to make

better use of existing capacity and optimise our cost structures.

Gross profit target achieved

Despite an almost 9 percent fall in revenue, technotrans succeeded in achieving its

earnings targets for its operations. This demonstrates that we have adapted flexibly to

fluctuating demand at a time of economic slackness, and have successfully shored up

our profitability through focused cost management. Although gross profit of € 35.9

million did not match the previous year's figure (-4.7 percent), the gross margin rose

from 32.2 percent to 33.7 percent.

Operating profit up 28 percent

The operating profit was up 27.8 percent on the previous year (€ 5.9 million) to slight-

ly more than € 7.5 million. With an operating margin of 7 percent as against 5 per-

cent in the previous year, we are able to report a significant improvement in this area,

too. Administrative costs were inflated in particular by consultancy costs of more than

€ 1.6 million for the planned takeover of the American company Baldwin Technology, Inc.

A letter of intent had been made public by both companies on December 12, 2003,

but Baldwin terminated negotiations at the end of January 2004. On the other hand,

SALES by region

other Europe…27%

USA…21%

Asia…10%

other…2%Germany…40%

SALES by segment in € million

73.4 104.9 131.0 117.0 106.7

9999 0000 0011 0022 0033

ServicesMicro Technologies

G R O U P M A N A G E M E N T R E P O R T 29

this expense was partly offset by the excess of proceeds over book value from the

sale of the production building in Colchester. Research and development costs rose

as expected from € 2.3 million to € 3 million in the run-up to this year's DRUPA. The

prior-year result was diminished by the creation of a provision of € 3.3 million for the

patent dispute with Baldwin.

Currency effects have minimal influence

Interest expense was reduced by 23.5 to just over € 1 million in 2003 thanks to the

reduction in long-term borrowings (by € 3.1 million). The influence of currency effects

was again minimal in 2003; technotrans benefits on the one hand from the fact that

the bulk of its revenue is billed in euros, and on the other hand from the fact that its

own production companies in America supply the same currency zone and that foreign

exchange losses from the financing of foreign entities (subsidiaries) are "parked" with-

in equity, with no effect on income, according to IAS.

Impairment of goodwill

In addition to regular goodwill amortisation (€ 1.7 million in 2003), a need for impair-

ment of goodwill and intangible assets in the Print and Micro Technologies segments

was ascertained in the year under review. technotrans had purchased the American

company Ryco Graphic Manufacturing, Inc., Chicago, in 2000, when the industry was

at its peak, at a price of € 18.6 million; a goodwill amount of € 15.4 million had to

be capitalised at the time. This goodwill constitutes part of the "Print" unit. The value

in use of the "Print" unit undercut its carrying amount by € 8.6 million, with the result

that the goodwills for this unit were reduced by the same amount.

The situation at the end of 2003 for the goodwill and intangible assets from the acqui-

sition of a Toolex division in 2001, which became part of the Micro Technologies seg-

ment, was similar. In this case, the remaining goodwill was reduced by € 2.8 million

and patents and expertise with a value of € 0.8 million written down.

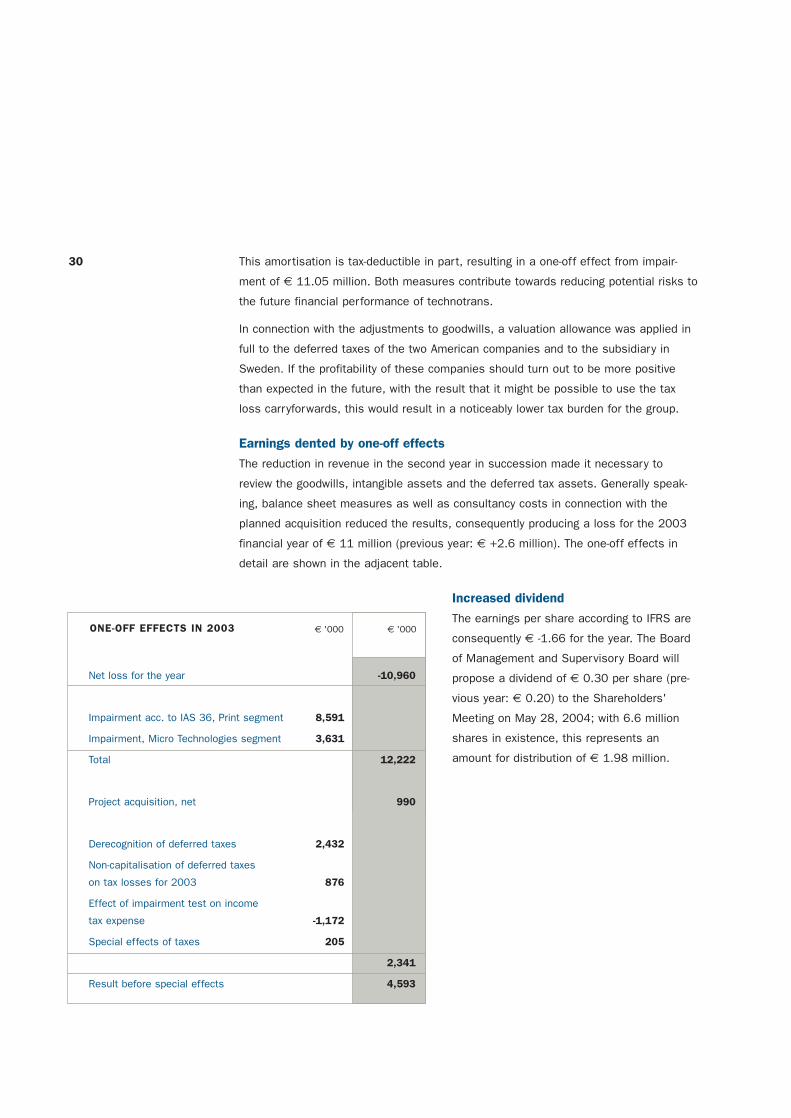

30 This amortisation is tax-deductible in part, resulting in a one-off effect from impair-

ment of € 11.05 million. Both measures contribute towards reducing potential risks to

the future financial performance of technotrans.

In connection with the adjustments to goodwills, a valuation allowance was applied in

full to the deferred taxes of the two American companies and to the subsidiary in

Sweden. If the profitability of these companies should turn out to be more positive

than expected in the future, with the result that it might be possible to use the tax

loss carryforwards, this would result in a noticeably lower tax burden for the group.

Earnings dented by one-off effects

The reduction in revenue in the second year in succession made it necessary to

review the goodwills, intangible assets and the deferred tax assets. Generally speak-

ing, balance sheet measures as well as consultancy costs in connection with the

planned acquisition reduced the results, consequently producing a loss for the 2003

financial year of € 11 million (previous year: € +2.6 million). The one-off effects in

detail are shown in the adjacent table.

Increased dividend

The earnings per share according to IFRS are

consequently € -1.66 for the year. The Board

of Management and Supervisory Board will

propose a dividend of € 0.30 per share (pre-

vious year: € 0.20) to the Shareholders'

Meeting on May 28, 2004; with 6.6 million

shares in existence, this represents an

amount for distribution of € 1.98 million.

ONE-OFF EFFECTS IN 2003 € '000€ '000

Net loss for the year

Impairment acc. to IAS 36, Print segment

Impairment, Micro Technologies segment

Total

Project acquisition, net

Derecognition of deferred taxes

Non-capitalisation of deferred taxes

on tax losses for 2003

Effect of impairment test on income

tax expense

Special effects of taxes

Result before special effects

-10,960

12,222

990

2,341

4,593

8,591

3,631

2,432

876

-1,172

205

G R O U P M A N A G E M E N T R E P O R T 31

Print segmentThe level of demand continued to fall in 2003 due to the crisis in the printing industry,

reaching the nadir mid-way through the year. The second half of the year, by contrast,

showed a marked improvement. Revenue for the Print segment amounted to € 70.6

million for the year as a whole. Although this figure was € 10 million or 12.4 percent

down on 2002, the decrease in 2002 had been in the order of € 18 million. The rev-

enue shortfall – particularly in the first half of the year – was nevertheless higher than

initially planned, not least because of exchange-rate effects. Print still accounted for

two-thirds of revenue in 2003.

As a result, structures were once again adjusted, including the closing-down of produc-

tion operations in Colchester and their transfer to Sassenberg. Even at this revenue

level, we thus succeeded in posting a positive operating result. The segment reported

earnings of € 1.8 million (previous year: € 0.6 million) at the end of the year. A sum

of slightly more than € 1.6 million in consultancy costs for the intended acquisition

constituted a charge for which it was not possible to budget. Without these costs, the

rate of return for the segment would have been 4.9 percent, not 2.6 percent, and

therefore on a par with the prior-year operating result in spite of the lower revenue.

SALES by segment

Micro Technologies…10.1%

Services…23.7%Print…66.2%

OPERATING PROFIT in € million

8.25 9.68 9.13 5.89 7.52

9999 0000 0011 0022 0033

32 Micro Technologies segmentRevenue for the Micro Technologies segment, which brackets together the areas

CD/DVD and microstructure technology, totalled € 10.8 million in 2003, thus once

again matching the prior-year level. This is all the more gratifying considering that

demand from the CD/DVD sector remained flat for the third year in succession, as

well as the fact that the market witnessed considerable competition, with the strength

of the euro against the US dollar presenting us with an added hurdle. The revenue

contribution of microstructure technology activities was welcome, though the growth

rates, starting from a very low base level, are not yet sufficient to outweigh the eas-

ing-off of demand from the CD/DVD sector, let alone emulate the past growth rates

of this segment.

The result for the segment continues to be diminished by the cost of developing the

future growth area of microstructure technology, totalling € 641,000 compared with

€ 819,000 in the previous year. In addition to a substantial improvement in profitability

at the end of the year, one-off effects amounting to € 600,000 at group level and

associated among other things with the valuation allowances on goodwill in the annual

financial statements were the reason why we were able to post a positive result at

year-end. Depreciation for the segment will be € 300,000 lower from 2004. This,

together with various internal measures, should help to provide sustained revenue.

Services segmentFollowing a surge in growth in 2002 (+23.1 percent), revenue for the Services seg-

ment of € 25.3 million was maintained at the previous year's level (€ 25.5 million).

Its proportion of total revenue rose from 21.8 percent to 23.7 percent. Due to the pre-

vailing economic situation, the emphasis for installations shifted more towards mainte-

nance and spare parts, as expected. The Technical Documentation business area like-

wise posted positive progress. In this area, more than half of external revenue for 2003

was generated through our self-developed software doculab.

The Services segment remains a dependable source of earnings for the group in these

difficult times. The result for the segment of € 4.8 million represents 63.5 percent of

consolidated operating earnings. Services which yield above-average profitability, such

as the sale of software licences, helped to boost the margin to a satisfying 18.9 per-

cent for the year under review (previous year: 15.9 percent). Since the fourth quarter,

however, it has become evident that the temporary need to provide more intensive sup-

port for new products appearing on the market, as is the case before the DRUPA indus-

try exhibition, is having an adverse effect on the result.

G R O U P M A N A G E M E N T R E P O R T 33

BALANCE SHEET STRUCTURE GROUP in € million

Cash…8.8 21.8…Short-term debt

14.3…Long-term debt

36.3…Equity

Receivables and prepaid expenses…19.2

Inventories…18.2

Non-current assets…26.2

72.4 72.4

Assets Liabilities

Balance sheet structureThe balance sheet total at December 31, 2003 was € 72.4 million (previous year:

€ 92.5 million). Allowances for goodwill made at the end of the year were the main

reason for this fall. They had become necessary in order to bring the balance sheet

values in line with the discounted cash flows over the remainder of the amortisation

period. Goodwill was consequently reduced by amortisation and impairment as well as

by exchange-rate losses of € 2.3 million booked with no effect on income, from € 19.8

million in the previous year to € 4.5 million (-77.5 percent). In this connection, the level

of deferred tax assets was likewise reduced from € 4.4 million at the end of 2002 to

€ 1.1 million at December 31, 2003. This measure will reduce potential future balance-

sheet risks.

Improved liquidity

The increase in current assets is attributable almost exclusively to a renewed improve-

ment in liquidity. Compared with € 7.3 million at the end of 2002, cash now totalled

€ 8.8 million (+20.1 percent). Inventories remained almost unchanged (€ 18.2 mil-

lion as against € 17.9 million).

In line with the changes on the assets side, the principal changes to equity and

liabilities relate to the item equity. This fell by € 15.4 million, from € 51.7 million to

€ 36.3 million, in particular as a result of the accumulated loss (€ 11.0 million), the

distribution of dividend for 2002 (€ 1.3 million) and exchange-rate losses not affect-

ing income (€ 2.9 million).

34 Long-term borrowings were again reduced in 2003 (-3.3 million, -21.5 percent). The

main changes within short-term borrowings related to the typical decrease in advances

received as a reflection of the order mix (€ -0.7 million) and a slight increase in pro-

visions (€ 9.0 million compared with € 8.4 million).

Sound balance sheet indicators

The main balance sheet indicators remain virtually unaffected by these changes, or

have improved significantly as a result (prior-year figures in brackets): the equity ratio

remains satisfactory at 50.1 percent (55.9 percent), the capital employed (as the sum

of interest-bearing liabilities and equity) fell to € 55.3 million (€ 74.4 million), the

return on capital employed (ROCE; operating profit + currency result as a ratio of capi-

tal employed) rose to 13.3 percent (7.6 percent).

Investment and finance€ 3.1 million (previous year: € 2.8 million) were invested in intangible assets and

property, plant and equipment in the past year. Investment was consequently lower

than depreciation (€ 5.3 million). This investment in the first instance took the form of

spending on extensions to the IT infrastructures and replacement investment, for

example for service vehicles. As a company with low manufacturing penetration, no

maintenance investment in plant and machinery was necessary, nor was any expan-

sion to capacity required in the light of the prevailing economic situation in 2003.

Investment was financed from cash flow; cash flow from operating activities amounted

to € 6.5 million (previous year: € 10.1 million). Although the free cash flow of € 5.4

million was unable to match the previous year's high level (€ 7.5 million), this figure

was positive for the second year in succession. On the other hand, we easily achieved

our aim of posting a positive free cash flow of at least the same magnitude as the tar-

geted earnings.

Procurement and productiontechnotrans develops, manufactures and sells equipment and systems for the printing

industry (Print segment) and electroforming systems for the manufacturing of

microstructures (Micro Technologies segment). The development of these systems and

the assembly of their components are among technotrans' core skills, whereas the

manufacturing of the components is outsourced to specialist suppliers. Our manufac-

turing penetration is thus exceptionally low.

INVESTMENT in € million CASH FLOW from operating activitiesin € million

2.8 4.6 4.3 10.1 6.5

9999 0000 0011 0022 0033

9999 0000 0011 0022 0033

G R O U P M A N A G E M E N T R E P O R T 35

Specialised locations worldwide

technotrans had five production locations worldwide at the end of 2003; the largest of

these locations act as centres of expertise for a particular technology. The production

companies use the group's entire network of 13 locations worldwide for their distribu-

tion and service activities. In Germany, various ancillary units for the printing industry

and systems for the Micro Technologies sector are manufactured at Sassenberg,

whereas the Stadtbergen plant, near Augsburg, has specialised in ink supply equip-

ment. Chicago is the production centre for spray dampening systems. Specific ancil-

lary units for the American offset printing market are made in Corona, near Los

Angeles. Beijing is our smallest production operation; it predominantly supplies pre-

assembled components for other production sites.

Ample capacity for handling an economic recovery

The question of production capacity utilisation has become more pertinent in the cur-

rent economic climate. With its very low manufacturing penetration technotrans is

demonstrably able to respond very flexibly to fluctuating demand. Capacity utilisation

in the traditional sense therefore refers exclusively to the floor space at the production

plants and the employees who work there. The company has no machinery or plant

that would cause a bottleneck when demand is running at a high level nor the corre-

sponding depreciation which diminishes profitability when demand is low. The existing

production area provides ample reserves for improved capacity utilisation when

demand recovers.

Investments – Other assetsInvestments – Property, plant and equipmentDepreciation

20

10

36 Suppliers tightly integrated

In view of the company's spread over five production sites and the low manufacturing

penetration, procurement management has become increasingly important. The aim is

to pool demand rationally for all manufacturing group companies worldwide, to inte-

grate suppliers closely into the production procedures and to develop joint strategies

for coping with fluctuating demand. We of course have sufficiently close ties with most

of our long-standing suppliers that any difficulties at those suppliers would become

evident well in advance, allowing us to arrange suitable alternatives.

Personnel and welfareThe number of employees within the technotrans Group again eased off in 2003. At

December 31, 2003 there were 596 (previous year 621) employees, a decrease of

4 percent. Whereas the workforce was trimmed in the first half of the year due to the

fall in demand, capacity was once again built up in the second half. The revenue per

employee (based on the average employee total for the year) has not changed sub-

stantially from the previous year, and was € 180 thousand (€ 183 thousand) for the

year under review.

In order to adapt to fluctuations in demand, priority measures implemented in 2003

involved the introduction of more flexible working hours and the postponement of the

collectively negotiated pay increase (at Sassenberg).

Personnel costs fell to € 29.3 million (previous year: € 31.9 million); this item as a

proportion of revenue remained almost unchanged at 27.4 percent (2002: 27.3 per-

cent).

Last year the employees once again received shares as a form of voluntary Christmas

bonus, with a two-year holding period. Six years on from the initial public offering, over

90 percent of all employees own shares in the company. The third tranche of stock

options was moreover issued after the Shareholders' Meeting in May 2003. These

stock options provide every employee with an opportunity to purchase shares at a

predetermined price after a waiting period of no less than two years, provided the per-

formance targets have been met. Further details of the stock options scheme are pro-

vided in the Notes, under Equity.

G R O U P M A N A G E M E N T R E P O R T 37

EMPLOYEES by segment

MicroTechnologies…8%

Services…26%Print…6%

Risk reportAs a worldwide technology and services group, technotrans is naturally exposed to a

large number of risks. We analyse and approach these on the basis of our principle of

dealing with potential risks responsibly.

Our risk management system is fundamentally aimed at assuring a uniform aware-

ness of risks among all employees, and forms an integral part of our business opera-

tions. To this end, potential risks in the various functional areas are systematically

identified and assessed. Where risks exceed defined thresholds of significance, they

are observed continually and corresponding measures initiated. The management is

informed promptly of potential risks and of the measures that have been taken.

Recent years have demonstrated that periods of economic slackness constitute a sig-

nificant risk for many companies, including in the printing industry. The current invest-

ment reticence among end customers, in other words printers, is being further exag-

gerated by the fact that DRUPA 2004 is looming large. On top of this, the structure of

the printing press industry resembles an oligopoly, dominated as it is by a small num-

ber of manufacturers. It is therefore only logical that technotrans generates over 60

percent of consolidated revenue in the Print segment from the world's five largest

printing press manufacturers. It would not be possible to compensate in the short

term for the unexpected loss of one such customer, and indeed would be difficult to

38 do so in the medium term. We are tackling economic and industry risks by constantly

analysing the market situation, exploiting scope for rationalisation, steadily expanding

our range of customer-focused services and extending both the depth and breadth of

our product range.

Every company has to use certain assumptions about how markets will develop as the

basis for its plans. The failure of anticipated figures to materialise can have an unsched-

uled impact on the company's development, which must then be assessed as part of

the risk management process and countermeasures then taken as appropriate.

The Micro Technologies segment is likewise exhibiting a protracted reluctance to invest.

Surplus capacity in the market is hindering demand. The market for microstructure appli-

cations is still young and expanding, and we believe it still harbours immense potential

for our equipment lines. The risks stem from the uncertainty as to how a young market

will develop.

As a company with international activities, technotrans has to contend with a large

number of legal constraints. There exists a particular risk in connection with the patent

dispute with a competitor that has been dragging on for several years. technotrans was

defeated in this lawsuit at the second instance. The ruling at the second instance of

November 14, 2002 paves the way for a claim for compensation, the level of which

may have to be determined in further legal proceedings. To minimise the risk, a provi-

sion totalling € 3 million was created, reflecting the value of the matter in dispute of

€ 2.5 million at the second instance as well as further legal expenses. technotrans

has filed a complaint against the non-admission of an appeal with the Federal Supreme

Court and lodged a revocation action against the enforced patent of its competitor with

the Federal Patents Court. There are no other legal proceedings of any significance. In

order to counteract potential risks from the wide range of tax, environmental, competi-

tion and other regulations and laws, we strictly adhere to laws and regulations and

obtain comprehensive advice both from our own employees and, in certain cases, from

established experts. As well as taking out an appropriate and economically justifiable

level of insurance cover, the company takes its own precautionary measures to guard

against the risk of elementary losses such as fire and loss of production.

In the light of volatile financial markets, the increasingly international scale of busi-

ness operations harbours risks in particular as a result of exchange rate movements.

Risks to business operations can largely be eliminated by natural hedging, which

means that the currencies in which purchases and sales are conducted are system-

atically harmonised. Group-wide finance management reduces further risks by hedging

substantial transactions. We aim to compensate for competitive disadvantages as a

result of exchange rate factors by implementing technological measures.

G R O U P M A N A G E M E N T R E P O R T 39

The adverse overall economic situation has prompted a rise in bankruptcies among

end customers and a deterioration in payment habits. We counteract this through a

stringent approach to the management of receivables and creditworthiness. Appropriate

specifications are applied as a means of reducing the credit risk by basing the provi-

sion of sales and services on the prevailing risk.

As a system supplier, the development of pioneering technologies is a key success

factor for us. Close cooperation with our customers right from the initial product idea,

through the development of the specific systems, to the drafting of concepts for

improvements, enables us to minimise potential risks at an early stage. We have also

established partnerships with research bodies, assuring the transfer of knowledge on

new potential applications. Both highly qualified and experienced employees safeguard

the necessary expertise for technotrans in this area.

This presentation of the applicable risks by no means constitutes an exhaustive sum-

mary – aspects of IT security, the valuations of inventories and technological substitu-

tion risks are also constantly monitored, for example. However, it is clear on the whole

that the level of exposure is limited by our adopting a responsible approach to identi-

fied and analysed risks, and that the only serious threat to technotrans is in the sum

of a large number of individual risks We have currently identified no risks which could

endanger the company's survival.

Research and developmentOur research and development activities make a significant contribution towards consol-

idating and building on our position in every market segment as an efficient, internation-

ally active technology group. Innovative capability is a decisive competitive advantage.

To complement this, pioneering technology trends are investigated and shaped at an

early stage through cross-company research projects and in collaboration with other

research institutes.

40 Pre-DRUPA year sees rise in spending

A total of € 3.6 million (previous year: € 3.3 million) was spent on research and devel-

opment in 2003. Of this amount, € 0.6 million was to be capitalised in accordance with

IFRS criteria (previous year: € 1.1 million). This total amount is spread between the Print

and Micro Technologies segments.

Activities for the Print segment focused on innovations that will be on show for the first

time at this year's DRUPA, the largest industry exhibition. Developments include an auto-

mated cartridge changer for the ink.line ink supply system. This reduces manual inter-

vention by the printer and responds to calls for a greater degree of automation.

We are also presenting our first product for the pre-press area: the spinclean is a de-

vice for cleaning the developer fluid used in printing plate exposure. Use of the spinclean

reduces the high costs arising from replacing and disposing of the developer fluid by

more than 70 percent. This is an outstanding example of how ecology and economics

can enter into a successful alliance.

In the Micro Technologies segment, the projects of the past year – above all the large-

area electroplating system "microform.400" – were largely completed. As well as this

large-format system, a system for smaller formats has been developed and well received

by the market.

Environmental protectionEnvironmental protection is regarded as a high priority at technotrans, even though

no immediate hazards to either the employees or the environment are created by the

company's activities of assembling plant and equipment. There is nevertheless a spe-

cial team by the name of technosafe, which has the purpose of identifying and elimi-

nating hazards.

The company's everyday operations also include a whole range of activities focusing

for example on reducing the amount of packaging, minimising the consumption of

water, electricity and gas, and making increased use of returnable packaging and

interchangeable containers as part of an ongoing process of optimisation.

A detailed survey of the situation at the largest production plant at Sassenberg car-

ried out in 2001, in line with the requirements of DIN EN ISO 14001 standard, con-

firmed our belief that technotrans has an efficient environmental protection system,

and there was consequently no immediate need for a further-reaching environmental

audit.

G R O U P M A N A G E M E N T R E P O R T 41

A whole array of our products also help to preserve natural resources. There is for

example ecoclean, the washing agent recovery system for the printing process. As

well as cutting the amount of solvent that the printer has to buy by around 90 percent,

it reduces the amount of toxic waste to be disposed of. We are conscious of our re-

sponsibility for our products and for the markets in which we operate. Our sales and

service employees actively endorse these principles in their dealings with customers,

and espouse the cause of protecting the environment.

Supplementary reportAfter the end of the financial year, Baldwin Technology Company, Inc., of Shelton,

Connecticut, USA, informed us on January 30, 2004 that it no longer wished to pur-

sue the negotiations on a potential merger of the two companies.

OutlookThe average growth rate forecasts for various national economies in the current finan-

cial year are 6 percent (Asia), 3 percent (USA), 1.8 percent (eurozone) and 1.5 to 2

percent (Germany). Global stimuli are being provided by Japan, Argentina and Brazil,

which appear to have pulled through the crisis. The semiconductor industry, which

kicked off the calamitous global downturn as a sector at the vanguard of the econom-

ic cycle, started 2004 just 14 percentage points down on the record highs of 2000.

Thanks to improved worldwide and internal basic data, a change for the better appears

to be more probable. Adjustment measures within the industry are likewise bearing

fruit: companies' profits have latterly risen by 15 percent and it is expected that

investment will pick up as a result.

Foreign exchange markets are one potential risk to global growth. The appreciation of

the euro has meant that percentage price increases for goods run into double digits,

with the result that although exports within the euro zone have gone up, sales to the

USA have fallen.

42 Germany anticipates growth

The experts expect that Germany will benefit in full from the economic recovery.

The IFO business confidence index has latterly returned to the level of late 2000 and

many early indicators lend substance to this confidence. Uncertainty as to forthcoming

reforms continues to cloud the horizon, with the result that the consumer sector is

still failing to deliver any impetus. Growth rates of 2.5 percent are expected for the

mechanical engineering sector in 2004; the priority remains to invest in rationalisation

measures rather than in additional capacity. This will consequently not ease the situa-

tion on the labour market in the short term.

As the printing industry lags behind in the economic cycle, it generally reflects trends

somewhat later. Experience has shown that an economic recovery generally goes hand

in hand with a rise in advertising spending, which provides printers with a reason to