tri-state regional workforce alliance, economic report, 2016 update

TRANSCRIPT

0

REGIONAL

ECONOMIC

REPORT, 2016

UPDATE An assessment of the Tri-State Region’s economic and demographic

identity

ABSTRACT This report examines the

demographic, economic, and

industrial profile of the Tri-State

Region. Analyses showed that

educational attainment, income

levels, and unemployment rates have

all improved in the region since

2009. However, educational

attainment and household income

remain relatively low, while poverty

rates remain high. Stakeholders

should be proactive in addressing

these issues and put forth initiatives

at the intersections of social policy

and economic development. The

special focus of this report is the

health services sector. Analysis

reveals that it is becoming an

increasingly important part of the

region’s economic identity for which

policymakers should create

workforce development and industrial recruitment initiatives.

Lucas Stewart B.S. Candidate, Economics

1

A. Introduction The Tri-State Regional Workforce Alliance, Inc. (TSRWA), established in March 2009

as a nonprofit organization, serves a 26 county region spanning Alabama, Georgia and

Tennessee.i Overall, the TSRWA serves to collaboratively advance the region’s economic

competitiveness and develop workforce talent. Recently, the TSRWA created a web-based toolii

aimed at promoting the data-driven formation of regionally focused, sector-oriented labor market

strategies. The current report serves to supplement their work and focuses on assessing the

region’s demographic and economic identity.

The first section provides historical comparisons of key labor market statistics, and gives

an overview of current labor market conditions, making use of data underlying the TSRWA’s

previously developed web tool. Next, the region’s industrial sector is assessed. The discussion

begins with historical comparisons, and then shifts to analyze current leading industrial sectors

for the area, with a special focus on the healthcare sector. The report concludes with synthesized

findings from data analyses and recommendations aimed at aiding the region in maintaining its

economic competitiveness in both the short- and long-term.

B. Regional Demographic and Economic Assessment

1. Population

Between 2009 and 2014, the Tri-State Region experienced population growth of 3.1%. In

comparison, the respective states with counties in the region saw the following population

growth rates: Alabama (1.3%), Georgia (3.0%), and Tennessee (2.3%). Population growth in the

area also surpassed nationwide population growth of 2.4% for the period.

2

2. Age

Age Group 2009 2014 Percentage Change

Under 15 19.8% 18.8% -5.4%

15 to 19 6.4% 6.5% 1.6%

20 to 34 19.7% 18.2% -7.5%

35 to 54 27.9% 27.2% -2.8%

55 to 64 11.9% 12.6% 6.5%

65 and over 14.3% 15.8% 10.2%

Table 1. Tri-State Region’s Age Distribution, 2009 vs. 2014

An important aspect of the population related to economic growth and development is

age distribution. Table 1 shows that, overall, the region experienced growth in its population

aged 55 years old and older, while the relative portion represented by younger residents either

declined or remained essentially the same from 2009 to 2014. The relative portion of the total

population represented by those in the working-age population (15 to 64 years old) declined by

2.1%, while the representation of the (approximated) prime working-age population (20 to 54

years old) decreased by 4.7%, between 2009 and 2014. Current statistics indicate that the

working-age population (15 to 64 years old) represents 64.0% of the total population, which is

comparatively lower than the same populations’ representation in the following geographical

units: AL (66.3%), GA (67.6%), TN (66.6%), and US (66.8%).

Changes in the population’s age structure have important implications for the region’s

economy. As more individuals move into retirement, policymakers need to ensure that the future

workforce is able to meet the demands of employers – particularly of those operating in

advanced, highly-competitive industries.

3

According to a recent report from the Brookings Institution, advanced industrial sectors

operating within the Tri-State Region are growing in importance.iii,iv From 2010 to 2013,

advanced industries experienced employment growth of 6.4% in the Chattanooga, TN-GA

metropolitan statistical area (MSAv). In addition, output from this sector grew by 8.0% in the

area for the same period. These percentage changes were the 9th largest and 6th largest in the

nation, respectively. Advanced sectors of importance include: (1) Architectural, Engineering, and

Related Services, (2) Management, Scientific, and Technical Consulting Services, and (3) Motor

Vehicle Parts Manufacturing. Each of these industries experienced more than 10.0% growth in

employment between 2010 and 2013.

Workforce development initiatives should be established that focus on employers’ needs

in these sectors for entry-level positions. In addition, on-the-job training and continuing

education offerings should be made available to mid-level career professionals who will be

replacing higher-skilled persons entering retirement. Such measures would improve the

economic competitiveness and viability of the region by increasing labor mobility and attracting

new, more demanding employers to the area.

4

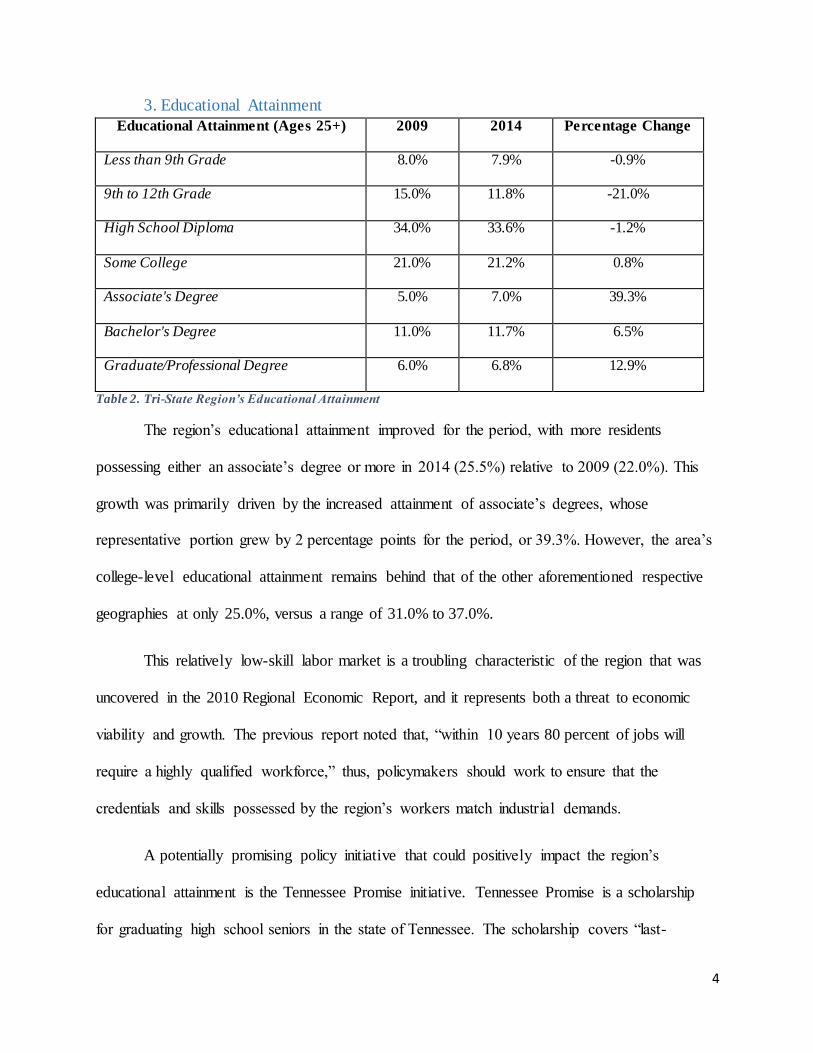

3. Educational Attainment

Educational Attainment (Ages 25+) 2009 2014 Percentage Change

Less than 9th Grade 8.0% 7.9% -0.9%

9th to 12th Grade 15.0% 11.8% -21.0%

High School Diploma 34.0% 33.6% -1.2%

Some College 21.0% 21.2% 0.8%

Associate's Degree 5.0% 7.0% 39.3%

Bachelor's Degree 11.0% 11.7% 6.5%

Graduate/Professional Degree 6.0% 6.8% 12.9%

Table 2. Tri-State Region’s Educational Attainment

The region’s educational attainment improved for the period, with more residents

possessing either an associate’s degree or more in 2014 (25.5%) relative to 2009 (22.0%). This

growth was primarily driven by the increased attainment of associate’s degrees, whose

representative portion grew by 2 percentage points for the period, or 39.3%. However, the area’s

college-level educational attainment remains behind that of the other aforementioned respective

geographies at only 25.0%, versus a range of 31.0% to 37.0%.

This relatively low-skill labor market is a troubling characteristic of the region that was

uncovered in the 2010 Regional Economic Report, and it represents both a threat to economic

viability and growth. The previous report noted that, “within 10 years 80 percent of jobs will

require a highly qualified workforce,” thus, policymakers should work to ensure that the

credentials and skills possessed by the region’s workers match industrial demands.

A potentially promising policy initiative that could positively impact the region’s

educational attainment is the Tennessee Promise initiative. Tennessee Promise is a scholarship

for graduating high school seniors in the state of Tennessee. The scholarship covers “last-

5

dollarvi” tuition and fees for two years at state community colleges, colleges of applied

technology, or other eligible schools that offer associate's degrees.

Currently there are 122 community and technical colleges in AL, GA, NC, and TN

(IPEDS, 2015). The first year of Tennessee Promise led to 24.7% and 20.0% increases in first-

time freshmen enrollment at Tennessee community colleges and colleges of applied technology,

respectively (THEC, 2016). The potential benefits of this policy are sizable, and surrounding

geographies (e.g., the entirety of the Tri-State Region) could gain from the policies positive

externalities such as higher wages, lower unemployment, and increased tax revenues.

4. Race and Ethnicity

Race & Ethnicity Classificationvii 2009 2014 Percentage Change

White 84.5% 87.1% 3.1%

Black/African American 7.5% 7.6% 2.2%

American Indian/Alaskan Native 0.4% 0.4% 12.3%

Asian 0.8% 1.0% 14.0%

Native Hawaiian/Pacific Islander 0.0% 0.0% -0.9%

Two or More Races 1.1% 1.8% 62.8%

Table 3. Tri-State Region’s Racial and Ethnic Distribution

As of 2014, the racial and ethnic distribution of the region’s population was

predominantly white, at 87.1%. Black/African American persons represented 7.6% of the total,

while the remaining racial and ethnic classifications amounted to less than 2%. This distribution

is essentially unchanged from 2009, however, we expect the area’s population to become

increasingly diverse over time.

6

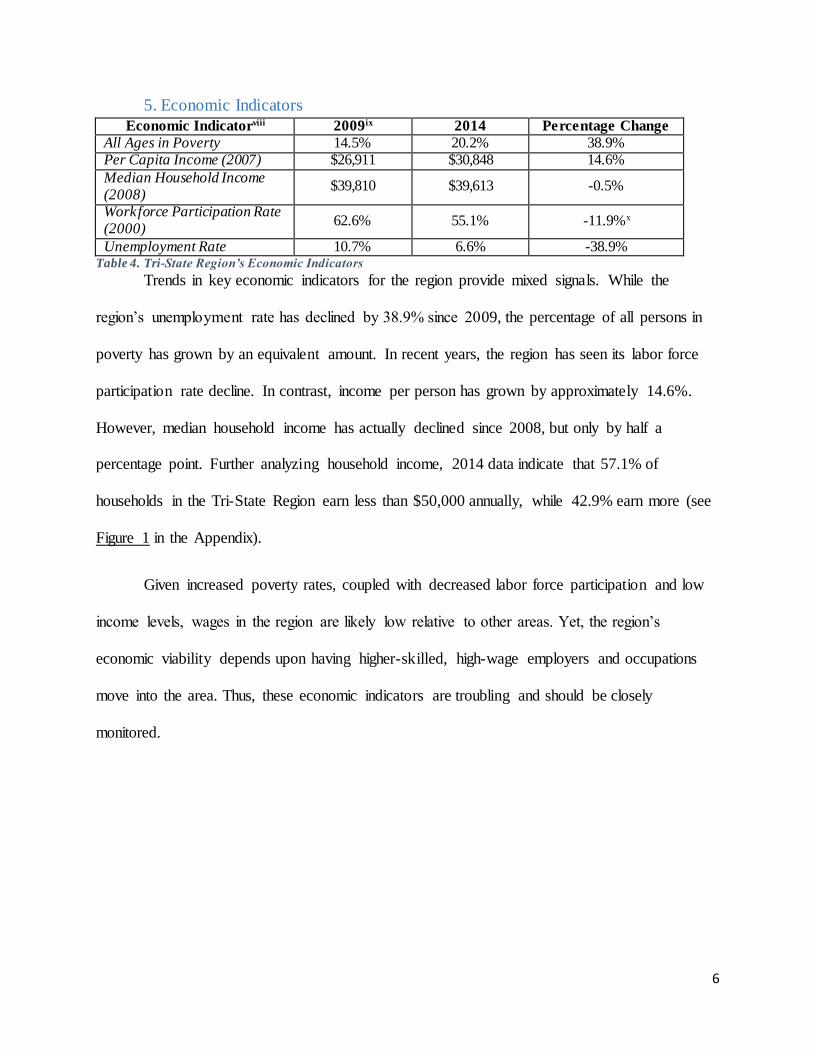

5. Economic Indicators

Economic Indicatorviii 2009ix 2014 Percentage Change

All Ages in Poverty 14.5% 20.2% 38.9% Per Capita Income (2007) $26,911 $30,848 14.6%

Median Household Income (2008)

$39,810 $39,613 -0.5%

Workforce Participation Rate (2000)

62.6% 55.1% -11.9%x

Unemployment Rate 10.7% 6.6% -38.9% Table 4. Tri-State Region’s Economic Indicators

Trends in key economic indicators for the region provide mixed signals. While the

region’s unemployment rate has declined by 38.9% since 2009, the percentage of all persons in

poverty has grown by an equivalent amount. In recent years, the region has seen its labor force

participation rate decline. In contrast, income per person has grown by approximately 14.6%.

However, median household income has actually declined since 2008, but only by half a

percentage point. Further analyzing household income, 2014 data indicate that 57.1% of

households in the Tri-State Region earn less than $50,000 annually, while 42.9% earn more (see

Figure 1 in the Appendix).

Given increased poverty rates, coupled with decreased labor force participation and low

income levels, wages in the region are likely low relative to other areas. Yet, the region’s

economic viability depends upon having higher-skilled, high-wage employers and occupations

move into the area. Thus, these economic indicators are troubling and should be closely

monitored.

7

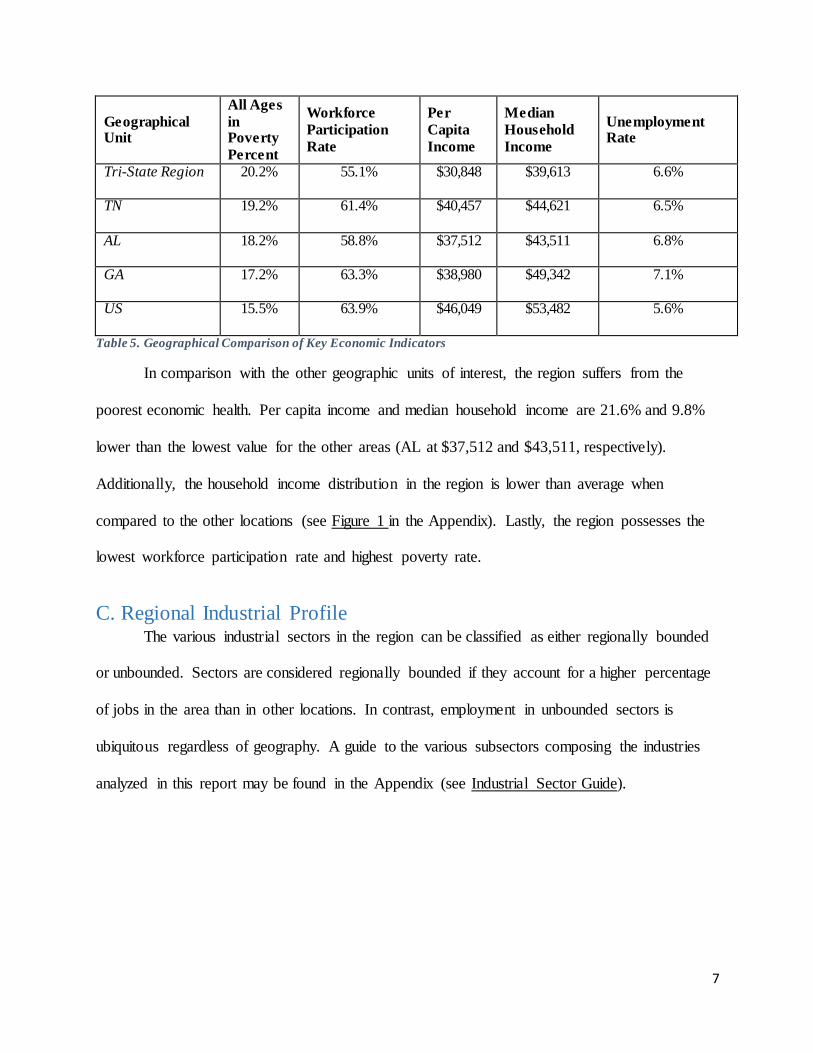

Geographical Unit

All Ages

in Poverty

Percent

Workforce

Participation

Rate

Per

Capita

Income

Median

Household

Income

Unemployment Rate

Tri-State Region 20.2% 55.1% $30,848 $39,613 6.6%

TN 19.2% 61.4% $40,457 $44,621 6.5%

AL 18.2% 58.8% $37,512 $43,511 6.8%

GA 17.2% 63.3% $38,980 $49,342 7.1%

US 15.5% 63.9% $46,049 $53,482 5.6%

Table 5. Geographical Comparison of Key Economic Indicators

In comparison with the other geographic units of interest, the region suffers from the

poorest economic health. Per capita income and median household income are 21.6% and 9.8%

lower than the lowest value for the other areas (AL at $37,512 and $43,511, respectively).

Additionally, the household income distribution in the region is lower than average when

compared to the other locations (see Figure 1 in the Appendix). Lastly, the region possesses the

lowest workforce participation rate and highest poverty rate.

C. Regional Industrial Profile The various industrial sectors in the region can be classified as either regionally bounded

or unbounded. Sectors are considered regionally bounded if they account for a higher percentage

of jobs in the area than in other locations. In contrast, employment in unbounded sectors is

ubiquitous regardless of geography. A guide to the various subsectors composing the industries

analyzed in this report may be found in the Appendix (see Industrial Sector Guide).

8

1. Regionally Bounded Industrial Sectors

Regionally Bounded Industrial Sector

Percentage of

Total Jobs

(2009)

Percentage of

Total Jobs

(2014)

Percentage Change

Transportation Product and Delivery

8.1% 9.1% 12.3%

Fabric Product Manufacturing 5.8% 6.9% 20.6% Specialized Economies 4.1% 5.9% 44.1%

Table 6. Percentage of Total Jobs Accounted for by Regionally Bounded Industrial Sectors, 2009 vs. 2014

In 2009, the rank order – in terms of the percent of total jobs accounted for – of the

sectors that form the region’s economic fingerprint were: (1) transportation product and delivery

(8.1%), (2) fabric product manufacturing (5.8%), and (3) specialized economies (4.1%). While

that same rank order held for 2014, the rank order of percentage growth in representation of total

jobs was opposite. However, the changes in terms of percentage points were relatively small (see

Table 6). Relative to other geographies, the percent of total jobs represented by either the fabric

product manufacturing or specialized economies sectors is greater in the Tri-State Region,

however, transportation product and delivery occupations have less of a presence in the region

relative to both AL and TN (see Table 8 in the Appendix).

As of 2014, based on metropolitan statistical area (MSA) and county-level occupational

employment data, jobs in the transportation product and delivery sector were most heavily

concentrated in southeastern TN, Cherokee County, NC, and DeKalb County, AL, while fabric

product manufacturing positions were most prevalent in Bartow, Gilmer and Gordon County,

GA, as well as the Dalton, GA MSA. Occupations in the specialized economies sector were

focused in Cherokee and Graham County, NC (see Tables 11 - 14 in the Appendix). It is

important for policymakers/stakeholders to keep these occupational employment concentrations

in mind for purposes of workforce development and attracting new employers to the region.

9

2. Regionally Unbounded Industrial Sectors

Sector Pct of Total

Jobs (2009)

Pct of Total

Jobs (2014) Percentage Change

Extractive Industries 2.6% 0.2% -91.6%

Construction 7.5% 4.1% -45.5%

Finance, Information and

Real Estate (FIRE) 9.0% 6.6% -26.2%

Professional and Business

Services 10.5% 10.4% -1.5%

Other Services 21.6% 21.9% 1.8%

Health Services 8.3% 11.1% 33.5%

Leisure and Hospitality 7.5% 11.2% 50.3%

Table 7. Percentage of Total Jobs Accounted for by Regionally Unbounded Industrial Sectors, 2009 vs. 2014

Excluding “other services” – 2009 data from the TSRWA show that professional and

business services (10.5%), finance, information and real estate (FIRE) (9.0%), and health

services (8.3%) were the leading regionally unbounded sectors in terms of percentage of total

jobs. Extractive industries had the smallest sectoral representation at only 2.6%. Between 2009

and 2014, leisure and hospitality and health services experienced the greatest growth, with each

increasing by more than 33.0%. Over the same period, construction and FIRE underwent the

largest percentage point declines (3.4 and 2.4 percentage points, respectively), while extractive

industries felt the most sizable percentage decrease. These results are not surprising given the

dampened economic activity in these sectors resulting from the Great Recession of 2007 –

2009.xi

For 2014, again excluding “other services,” leisure and hospitality, health services, and

professional and business services represented the largest sectors at 11.2%, 11.1%, and 10.4% of

10

total jobs, respectively. The remaining regionally unbounded sectors accounted for less than

7.0% of total jobs, with extractive industries only amounting to 0.2%.

The rank order of and percentage changes in the proportion of total jobs represented by

the various regionally unbounded industrial sectors should be closely monitored by

policymakers, employers and employees alike. Sectors with a low employment presence and/or

experiencing declines in employment pose issues for employers, workers, and policymakers.

Persons affiliated with these sectors, including policymakers, must innovate in order to survive

(and hopefully thrive) in a dynamic economy. Alternatively, sectors with a high employment

presence and/or growth sectors represent both the strengths and opportunities possessed by the

Tri-State Region; policy initiatives can be targeted at these sectors to improve the area’s

economic competitiveness.

3. Health Services

The health services sector is already an integral part of the Tri-State Region’s economy: it

represents 11.1% of total jobs in the region, and it has experienced job growth of nearly 3

percentage points since 2009 (see Table 7 above). This sectors’ significance will only continue

growing: the Bureau of Labor Statistics (BLS) estimates that health services jobs will account for

more than one-third of US projected job growth from 2014 to 2024 (BLS, Current Employment

Statistics (CES)).

The health services sector is comprised of the following subsectors: (1) ambulatory

healthcare services, (2) hospitals, (3) nursing and residential care facilities, and (4) social

assistance. The services in this sector are delivered by trained and credential professiona ls, and

typical occupations include home health aides, licensed practical and license vocational nurses

(LPN and LVN), and medical and health services managers. Additionally, the field comprises

11

higher level practitioners such as nurse practitioners, general physicians, dentists, optometrists,

etc.

The sector possesses positive economic characteristics. According to preliminary May

2016 estimates from the BLS, the average hourly earnings of all employees in the health services

sector is $25.93, or $51,860 annually, while the national unemployment rate for all persons

employed in this sector stands at only 2.9% (BLS, CES). Additionally, a sizable portion of jobs

in health services require only an associate’s degree or postsecondary vocational award,

including LPNs and LVNs, occupational and physical therapy assistants, diagnostic medical

sonographers and dental hygienists. These occupations are expected to experience employment.

Also, national employment projections indicate that nurse practitioners, physical therapists and

optometrists will all see their occupations grow by 27.0% or greater between 2014 and 2024

(BLS, Employment Projections).

Overall, the health services sector is becoming increasingly relevant to the region’s

economy, thus, efforts should be made to ensure that educational credentials and job skills

possessed by the area’s workforce match industry standards in order to optimize employment in

and the economic impact of this sector. Additionally, health services, coupled with other growth

sectors, provides policymakers with the opportunity to forge a “new economy” for the Tri-State

Region, solidifying overall economic viability and sustainability through collaboration with

those currently operating in the sectors constituting the region’s economic identity.

Some important factors pertaining to the health services sector for

policymakers/stakeholders to bear in mind are: (1) aging population and (2) the Patient

Protection and Affordable Care Act (PPACA, aka, ACA). As residents in the Tri-State Region

continue aging, the health services sector should continue growing due to increased demand for

12

health-related treatment/procedures. Thus, an area of focus for workforce development may be

geriatric care, particularly home health aides.

While the impacts of an aging/retiring population are relatively straightforward as they

pertain to healthcare, those posed by the passage and implementation of the ACA are more

uncertain. With a greater portion of the population insured, one could reasonably assume that

demand for the services of healthcare workers/providers will increase. However, the magnitude

and composition of such a demand effect may be altered by other factors. If states choose to

expand Medicaid, this may further increase demand for health services by expanding coverage.xii

In addition, factors outside of the legislation such as regional income levels may contribute to

demand for healthcare. Lastly, some insurers have dropped out of the Marketplace exchanges

after experiencing losses – this could lead to higher premiums and dampened demand through

limited coverage options.

D. Conclusion and Recommendations Between 2009 and 2014, the Tri-State Region saw improvements in educational

attainment, per capita income levels and the unemployment rate. Promising initiatives such as

Tennessee’s Labor Education Alignment Program (LEAP) are aiding in this progress by aligning

the skills and credentials of postsecondary graduates with industry demands.

In addition, the health services sector is growing in importance for the region’s economy.

Given the strong wage characteristics and employment projections possessed by occupations in

this sector, policymakers should integrate this sector into economic development policies both

now and in the future. Furthermore, the changing US healthcare landscape should be attentively

tracked to ensure that current and future policies are adjusted accordingly.

13

However, other changes during the period highlight present and emerging challenges that

will require intervention efforts from stakeholders. These are elaborated upon below:

1. Aging population: As the region’s population continues aging, age composition should

be closely monitored by policymakers as the size of the prime working age population

(25 to 54 years old) plays a significant role in economic growth.

2. Educational attainment: While college-level (postsecondary vocational award or

associate’s degree and beyond) educational attainment improved over the past five years,

the region continues to lag behind surrounding geographies. Policymakers should

continue improving educational and job-skill development interventions to mitigate the

present low-skill labor market and ensure that the area’s workforce maintains pace with

industry standards.

3. Poverty: Low-income/high-poverty levels are economic issues for the region.

Stakeholders should collaborate to establish innovative policies focused on reducing

these problems: investments in workforce development and new employer recruitment

offer two potentially useful policy levers.

Based on the above challenges, we recommend that policymakers in the area collaborate to

undertake further research focused on alleviating multidimensional poverty in the Tri-State

Region. Components of multidimensional poverty include: (1) low income, (2) low educational

attainment, (3) geographical disparities of income and educational attainment, (4) lack of health

insurance, and (5) unemployment.xiii By analyzing these facets and forming policies to mitigate

their effects, policymakers can improve the performance of the region’s economy. Such efforts

will require significant collaboration and outreach beyond the scope of previous work, but the

14

central outcome of a more productive, positive workforce warrants the undertaking of such a

project.

15

E. Appendix

Figure 1. Geographical Comparison of Household Income Distributions, 2014

*Note: The two highest household income ranges ($150,000 to $199,999 and $200,000 or more)

each represent 5.0% or less of the respective geographies household income distributions. Thus, data labels are not presented.

Geographical

Unit

Percentage of Total Jobs

Transportation Product and

Delivery

Fabric Product

Manufacturing

Specialized

Economies

Tri-State Region 9.1% 6.9% 5.9%

US 6.7% 0.3% 3.8%

AL 10.6% 0.9% 5.0%

GA 7.3% 1.4% 3.9%

NC 5.5% 1.3% 5.7%

TN 10.6% 0.4% 4.8%

Table 8. Geographical Comparison of Regionally Bounded Sectoral Concentration, 2014

8.7%

8.2%

8.7%

9.9%

7.2%

8.5%

6.4%

6.3%

5.6%

7.0%

5.3%

7.0%

12.8%

11.9%

11.3%

12.9%

10.7%

13.7%

11.9%

11.8%

10.8%

11.4%

10.2%

12.4%

14.9%

14.9%

14.0%

14.4%

13.5%

15.3%

18.1%

18.1%

18.0%

17.2%

17.8%

18.3%

10.9%

11.4%

11.5%

10.8%

12.2%

10.7%

10.0%

10.6%

11.6%

10.3%

13.0%

9.2%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0%

TN

NC

GA

AL

US

Tri-State Region

Less than $10,000 $10,000 to $14,999 $15,000 to $24,999 $25,000 to $34,999

$35,000 to $49,999 $50,000 to $74,999 $75,000 to $99,999 $100,000 to $149,999

$150,000 to $199,999 $200,000 or more

16

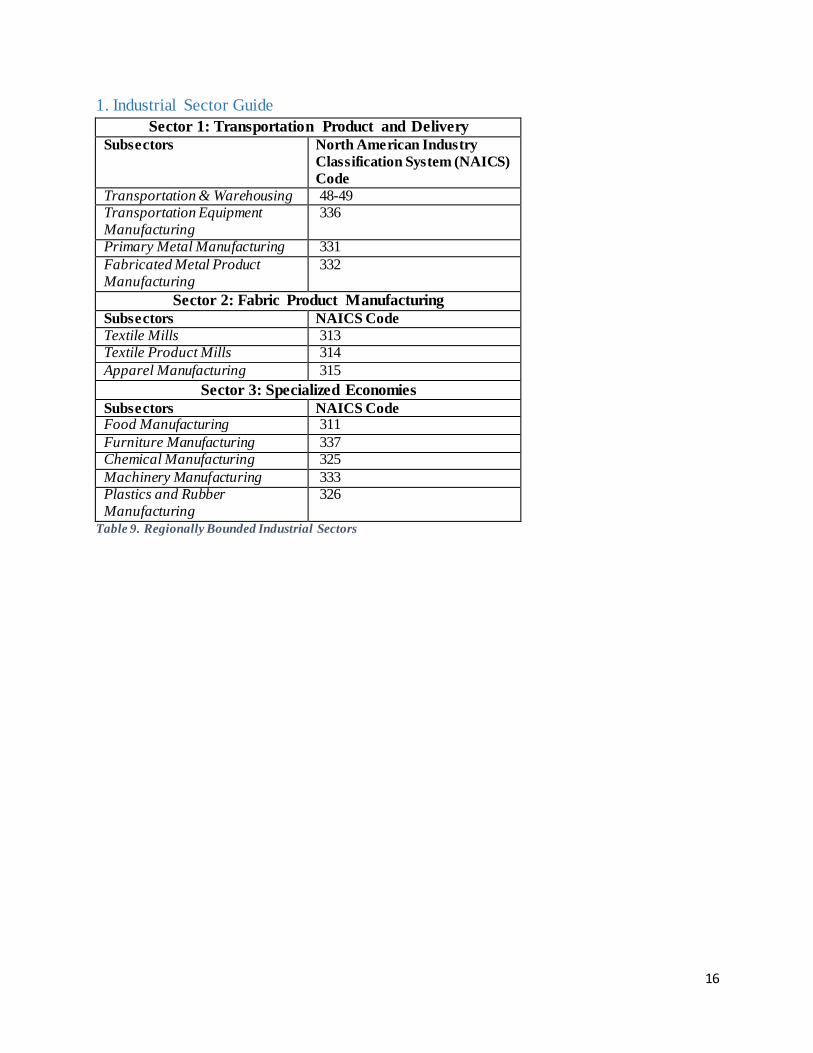

1. Industrial Sector Guide

Sector 1: Transportation Product and Delivery

Subsectors North American Industry

Classification System (NAICS)

Code

Transportation & Warehousing 48-49 Transportation Equipment Manufacturing

336

Primary Metal Manufacturing 331

Fabricated Metal Product Manufacturing

332

Sector 2: Fabric Product Manufacturing

Subsectors NAICS Code

Textile Mills 313 Textile Product Mills 314

Apparel Manufacturing 315

Sector 3: Specialized Economies

Subsectors NAICS Code Food Manufacturing 311

Furniture Manufacturing 337 Chemical Manufacturing 325

Machinery Manufacturing 333 Plastics and Rubber Manufacturing

326

Table 9. Regionally Bounded Industrial Sectors

17

Sector A: Construction

Subsector NAICS Code Construction 23

Sector B: Leisure and Hospitality

Subsector NAICS Code Arts, Entertainment, and Recreation

71

Accommodation and Food Services

72

Sector C: Health Services

Subsector NAICS Code

Healthcare and Social Assistance 62

Sector D: Professional and Business Services

Subsector NAICS Code

Professional, Scientific, and Technical Services

54

Management of Companies and Enterprises

55

Administrative and Support and Waste Management and Remediation Services

56

Sector E: Finance, Information and Real Estate (FIRE)

Subsector NAICS Code

Finance and Insurance 52 Information 51

Real Estate and Rental and Leasing

53

Sector F: Extractive Industries (Natural Resources and

Mining)

Subsector NAICS Code

Agriculture, Forestry, Fishing and Hunting

11

Mining Quarrying, and Oil and Gas Extraction

21

Sector G: Other Services

Subsector NAICS Code Utilities 22

Wholesale Trade 42 Retail Trade 44 – 45

Educational Services 61

Other Services, Except Public Administration

81

Table 10. Regionally Unbounded Industrial Sectors

18

2. Occupational Employment Presence Classifications

Classification Percentage Range Cell Color

High >10%

Moderate 5-10%

Low <5%

Table 11. Presence Classification Guide

*Definition: Presence classifications are based on the percentage of total jobs accounted for by

the respective industrial sectors in the respective areas analyzed.

*Note: For Tables 12 – 14 below, some locations and their corresponding values are not reported

as the US Census Bureau’s County Business Patterns (CBP) does not provide small data values

due to privacy concerns.

*Caveat: The metropolitan statistical areas (MSAs) reported in the following presence

classification tables include counties outside of the Tri-State Region. Thus, statistics for the

respective MSAs may not be entirely representative of the Tri-State Region’s counties contained

within.

State Geography Jobs Percentage of Total Jobs

TN Van Buren 171 42.8%

TN Monroe 3,186 28.3%

NC Cherokee 1,479 23.6%

AL DeKalb 3,330 19.0%

TN Mcminn 2,166 14.6%

TN Blount 5,478 14.6%

TN Loudon 1,684 14.4%

TN-GA Chattanooga, TN-GA MSA 20,978 11.0%

GA Rome, GA MSA 2,443 7.6%

TN Rhea 581 7.3%

GA Bartow 1,887 6.8%

TN Cleveland, TN MSA 2,385 6.2%

AL Jackson 548 4.3%

GA Gordon 325 1.8%

GA Chatooga 48 1.0%

TN Meigs 13 0.9%

GA Pickens 39 0.7%

GA Dalton, GA MSA 180 0.3%

GA Gilmer 19 0.3%

GA Fannin 13 0.3%

NC Graham 4 0.3%

Table 12. Transportation Product and Delivery – Presence Classifications, 2014

19

State Geography Jobs Percentage of Total Jobs GA Gordon 5,928 32.7%

GA Dalton, GA MSA 17,461 30.6% GA Gilmer 810 13.4%

GA Bartow 3,379 12.1% AL DeKalb 1,666 9.5%

NC Graham 62 4.1% TN Monroe 445 4.0%

GA Rome, GA MSA 1,260 3.9% TN Mcminn 290 2.0%

GA Fannin 73 1.6%

TN Cleveland, TN MSA 609 1.6% TN-GA Chattanooga, TN-GA MSA 2,719 1.4%

AL Jackson 158 1.3% TN Loudon 31 0.3%

NC Cherokee 16 0.3% Table 13. Fabric Product Manufacturing – Presence Classifications, 2014

State Geography Jobs Percentage of Total Jobs NC Cherokee 3,523 56.3%

NC Graham 359 23.6% TN Mcminn 1,403 9.5%

TN Loudon 1,101 9.4% GA Gordon 1,632 9.0%

GA Bartow 2,390 8.6% GA Rome, GA MSA 2,002 6.2%

TN-GA Chattanooga, TN-GA MSA 11,581 6.1% TN Cleveland, TN MSA 2,177 5.7%

AL Jackson 548 4.3% GA Dalton, GA MSA 2,363 4.1%

AL DeKalb 496 2.8% TN Grundy 33 2.4%

TN Monroe 229 2.0% GA Fannin 66 1.5%

GA Gilmer 66 1.1%

TN Blount 380 1.0% GA Pickens 52 0.9%

Table 14. Specialized Economies – Presence Classifications, 2014

20

3. Data Sources

1. Population Estimates – US Census Bureau, 2010 – 2014 American Community Survey

(ACS) 5-Year Estimates1

2. Educational Attainment – same as above

a. Number of Community and Technical Colleges – U.S. Department of

Education. Institute of Education Sciences, National Center for Education

Statistics. Integrated Postsecondary Education Data System (IPEDS), Final

Release Data, 2014-20152

b. Tennessee Promise Year 1 Performance – Tennessee Higher Education

Commission (THEC)3

3. Racial and Ethnic Distribution – same as above

4. Economic Indicators

a. All Ages in Poverty – Small Area Income and Poverty Estimates (SAIPE), State

and County Estimates for 20144

b. Per Capita Income – US Department of Commerce, Bureau of Economic

Analysis (BEA), Regional Data: Local Area Personal Income and Employment5

c. Median Household Income – 2014 ACS 5-Year Estimates

d. Workforce Participation Rate

i. National Estimates – US Department of Labor (DOL), Bureau of Labor

Statistics (BLS), Current Population Survey (CPS)6

ii. State and County Estimates – US DOL, BLS, Local Area Unemployment

Statistics (LAUS)7

e. Unemployment Rate

i. National Estimates – same as above

ii. State and County Estimates – same as above

5. Regional Industrial Profile

a. National, State and County Estimates – US DOL, BLS, Quarterly Census of

Employment & Wages (QCEW)8

b. Metropolitan Statistical Area (MSA) Estimates – US DOL, BLS, Occupational

Employment Statistics (OES)9

Notes:

1. All data from this source was collected using the US Census Bureau’s American

FactFinder tool, found here: http://factfinder.census.gov/faces/nav/jsf/pages/index.xhtml.

2. Institutional data was collected using the following tool (URL -

https://nces.ed.gov/ipeds/datacenter/InstitutionByGroup.aspx)

3. Infographic with information related to Tennessee Promise may be found here (URL -

https://www.tn.gov/thec/article/tn-promise-year-1-infographic)

4. Data was assembled using the Interactive SAIPE Data and Mapping Tool (URL -

https://www.census.gov/did/www/saipe/data/interactive/saipe.html)

5. Data was gathered using the BEA’s Interactive Data Application (URL -

http://www.bea.gov/itable/)

21

6. CPS Labor Force Statistics were collected using the one-screen data search here:

http://www.bls.gov/cps/#data

7. LAUS data were assembled using the multi-screen data search here:

http://www.bls.gov/data/#unemployment; also, as LAUS does not contain population

estimates, 2014 ACS 5-Year Estimates were used for the adult population denominator of

the workforce participation rate formula.

8. QCEW statistics were gathered using the multi-screen data search here:

www.bls.gov/data/#employment.

9. OES data were gathered from the following web page:

http://www.bls.gov/oes/tables.htm.

i The 2010 Regional Sector-Based Analysis and Report from Tri-State Regional Workforce Alliance, Inc. indicated

that a 30-county region, including 2 counties (Cherokee and Graham) in North Carolina, formed the economic

identity and geographic scope of the Tri-State Region. Thus, estimates for these 2 counties may be present in the

current report. ii The web-based tool may be found here: http://www.nsparc.msstate.edu/sites/Tri-State-Website/. iii The referenced report is titled America’s Advanced Industries: What They Are, Where They Are, and Why They

Matter. The report, along with useful interactive data tools, may be found here -

https://www.brookings.edu/research/americas -advanced-industries-what-they-are-where-they-are-and-why-they-

matter/. iv Quoting directly from the Brookings’ report, the authors identified advanced industries using the following

criteria: (1) “An industry’s R&D spending per worker must fall in the 80th percentile of industries or higher,

exceeding $450 per worker,” and (2) “The share of workers in an industry whose occupations require a high degree

of STEM knowledge must also be above the national average, or 21 percent of all workers.” v In laymen’s terms, a metropolitan statistical area (MSA) is a geographical region possessing a re latively high core

population density with close economic connections in the area. For a more precise, detailed definition, see the

following: http://www.census.gov/population/metro/about/. vi Last-dollar scholarships cover the gap between the direct cost of enrollment (tuition and fees) and aid from federal,

state, and institutional grants (Carruthers & Fox, 2015). vii According to the US Census Bureau, persons who identify their origin as Hispanic, Latino, or Spanish may be of

any race. Thus, related statistics are not exclusively reported for these persons. For additional information, please

consult the following: http://www.census.gov/population/hispanic/about/faq.html. viii Per capita income is in current dollars (not adjusted for inflation). Household income is inflation adjusted (USD

2014). Unemployment rates are not seasonally adjusted and pertain to persons 16 years and o ver. ix Statistics presented here represent the most recent data reported on the TSRWA web page under Basic Economic

Indicators and Demographics. A parenthetical reference for the year data was collected for the respective statistics

not collected in 2009 is provided. x The workforce participation rate percentage change should be interpreted with caution as the US economy was

thriving in 2000 relative to later years, and the impacts of the Great Recession are likely still present in recent data. xi Periods of economic recession are defined by the National Bureau of Economic Research (NBER) and can be

found here: http://www.nber.org/cycles.html. xii States have the option to expand Medicaid; however, none of the states comprising the Tri-State Region have

chosen to enact this measure. xiii These dimensions come from an April 2016 report from the Brookings Institution titled Five Evils:

Multidimensional Poverty and Race in America by Richard Reeves, Edward Rodrigue, and Elizabeth Kneebone.