trends in cross border and wholesale funding, and regulatory impact

TRANSCRIPT

TRENDS IN CROSS-BORDER AND WHOLESALE

FUNDING & REGULATORY IMPACT

Subbu Loganathan

Kramerica Consulting

AGENDA

Introduction – Funding Structures for Banks across the world Funding Patterns and Regulatory Pressures

Wholesale Funding

Cross-border bank funding

Impact of the Financial Crisis on Funding Structures

What the Crisis revealed about Wholesale Funding

What the Crisis revealed about Cross Border Funding

Regulatory Capital and Liquidity reforms and Bank Funding

Structures

Learnings

Learning 1 - Bank Funding Structures since the Financial Crisis

Learning 2 - Cross Border Funding since the Financial crisis

Q&A

INTRODUCTION TO BANK FUNDING STRUCTURES

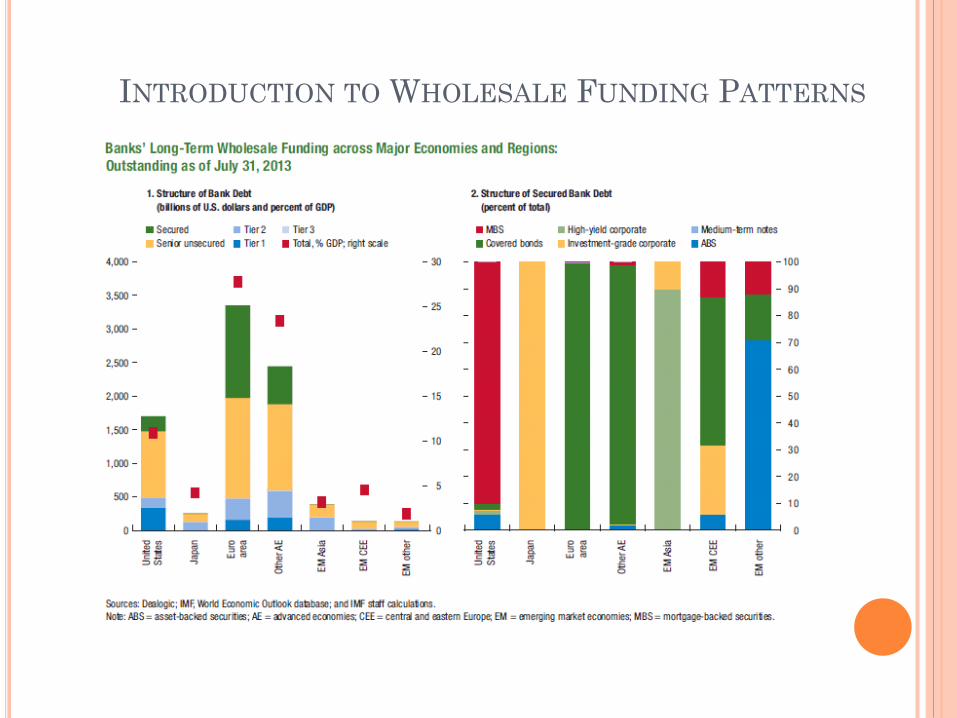

INTRODUCTION TO WHOLESALE FUNDING PATTERNS

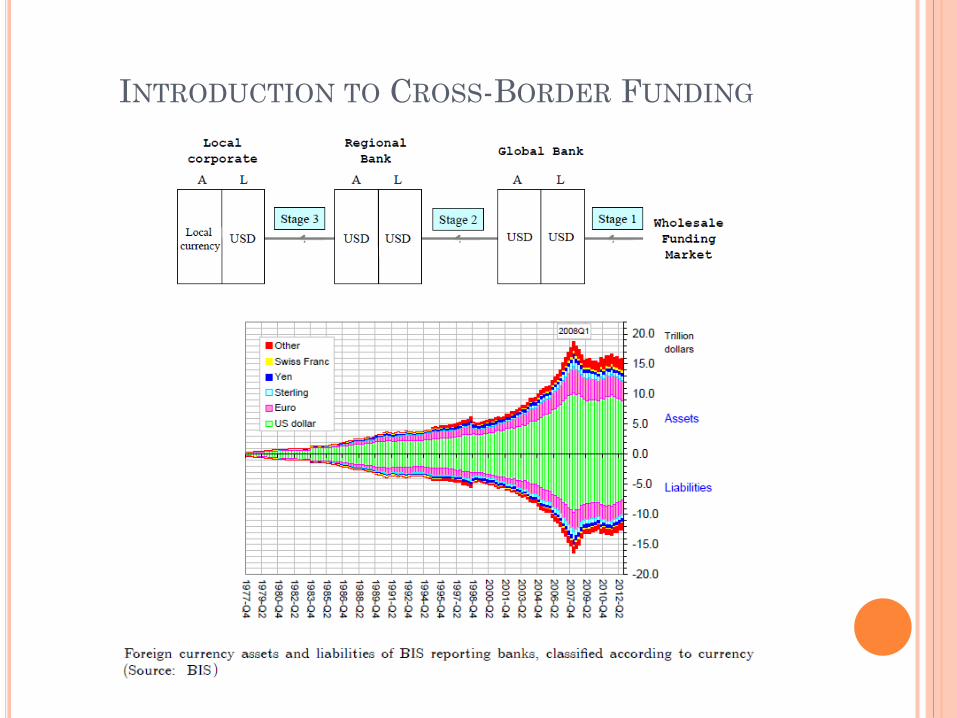

INTRODUCTION TO CROSS-BORDER FUNDING

IMPACT OF FINANCIAL CRISIS ON FUNDING

STRUCTURES

In contrast with historical systemic crises where the runs were mainly from

retail depositors, both the financial crisis that intensified with the Lehman

Brothers bankruptcy in 2008 as well as the European sovereign debt crisis as

of 2010 were largely centered on dry-ups in wholesale funding liquidity

Importantly, there has been a geographical fragmentation of liquidity in

global markets, notably around the sovereign debt crisis, unwinding partially

the financial globalisation trend of the last two decades.

The main response to combat these tensions have been central banks’ non-

standard policy actions.

The financial crisis resulted in worse Interbank access and volume for longer

terms funding as compared to overnight maturities

The cross-border funding effects were quantitatively stronger in the

sovereign debt crisis for banks headquartered in peripheral countries.

WHAT THE CRISIS REVEALED ABOUT WHOLESALE

FUNDING

Funding at short maturities instead of longer maturities. Resulting in

collective withdrawals during the credit and liquidity crunch

Wholesale funding on a secured basis Resulting in a freeze of repo

funding markets (“a run on repo”) due to concerns on quality of collateral.

More interconnected financial system due to both bank and nonbank

institutions providing liquidity to each other resulting in collapse of

interbank markets due to hoarding of liquidity during the crisis.

Complex interactions between bank assets and liabilities Resulting in

asset fire sales to generate liquidity during a funding freeze.

Variations in value of collateral and margin requested and other funding

market conditions Resulting in major changes to bank leverage and credit

processes.

WHAT THE CRISIS REVEALED ABOUT CROSS BORDER

FUNDING

Financial fragmentation and deleveraging have impacted cross border

funding patterns.

There was a significant decline in foreigners’ investments in bank-issued debt

securities located in the stressed euro area countries of Ireland, Italy, Portugal

and Spain, while the banks in core euro area countries experienced the exact

opposite.

The changes were smaller in non-euro area advanced economies.

In the euro area, foreign investors can be differentiated between core and

stressed economies, reflecting financial segmentation and and ongoing

bank deleveraging.

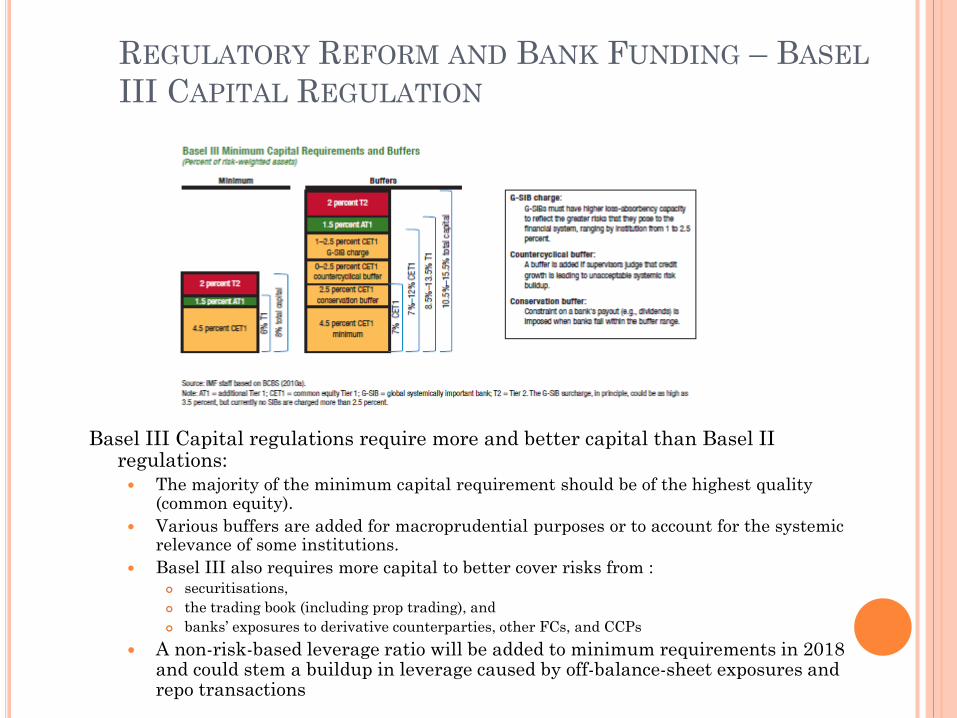

REGULATORY REFORM AND BANK FUNDING – BASEL

III CAPITAL REGULATION

Basel III Capital regulations require more and better capital than Basel II regulations:

The majority of the minimum capital requirement should be of the highest quality (common equity).

Various buffers are added for macroprudential purposes or to account for the systemic relevance of some institutions.

Basel III also requires more capital to better cover risks from : securitisations,

the trading book (including prop trading), and

banks’ exposures to derivative counterparties, other FCs, and CCPs

A non-risk-based leverage ratio will be added to minimum requirements in 2018 and could stem a buildup in leverage caused by off-balance-sheet exposures and repo transactions

REGULATORY REFORM AND BANK FUNDING – BASEL

III LIQUIDITY REGULATION

25.0min

1

30%75max

OutflowCash

InflowsOutflow

LA

T

LCR

Objective :

Liquidity even under very severe liquidity

stress over 30 days w/o govt & Central Bank

assistance

Minimum requirements

NSFR

Objective :

Reduce maturity mismatch between funding

and assets

Assets > 1 y funded by liabilities > 1y

1RSF

ASF

IMPACT OF REGULATORY REFORM ON BANK FUNDING

STRUCTURES

Basel III Capital regulations and OTC Derivatives reforms will enhance

safety of markets but will encumber more assets.

Some changes to funding structures (including more equity) combined

with reallocation of losses upon bank failure among different debt holders

can produce disproportionate changes of funding costs that are not easily

anticipated.

Basel III Liquidity Regulations aim for longer and more stable funding :

Some aspects of the liquidity regulations could encourage covered bond

issuance and increase asset encumbrance (as covered bonds qualify as

part of HQLA)

LEARNING 1 : BANK FUNDING STRUCTURES SINCE THE

FINANCIAL CRISIS

Since the crisis began, banks around the world have :

raised their capital adequacy ratios,

reduced wholesale funding,

and in some cases raised more deposits,

all of which have improved their stability.

However, distressed banks funding structures have not similarly

improved and they remain vulnerable.

The global financial crisis caused substantial stress in wholesale funding

markets, forcing banks to adjust their funding models.

Trends across global bank funding structures:

Europe – not out of the woods yet

US – Reduced secured funding

Asia and other – slightly increased wholesale funding, but still less than US or Europe

LEARNING 2 : CROSS BORDER BANK FUNDING SINCE

THE FINANCIAL CRISIS

Cross-border banking brings important benefits, but also exacerbates stresses, as

the global financial crisis revealed very clearly.

Financial integration in general, and cross-border banking in particular,

accelerated the transmission of the crisis from its origins in US housing markets

to wholesale financial markets across the world.

Euro Region :

The financial crisis has induced many banks to focus on core activities and

markets, with less emphasis on cross-border expansion.

However, some strong, large banks have expanded overseas during the

crisis, using capital raised by domestic disposals in order to acquire foreign

targets at attractive prices.

Western Europe experienced the largest reduction in cross-border flows,

however these flows have not recovered as rapidly, unlike in other regions of

the world.

The impact on Central and Eastern European countries was modest and

probably mitigated by the presence of foreign banks.

Outside Euro area –

Though the financial crisis impacted almost all global economies and banking,

the cross-border funding activities for advanced economies and banks outside

the euro zone has rebounded and remained fairly stable since 2012.