trends and strategies for outbound real estate investments · trends and strategies for outbound...

TRANSCRIPT

Trends and Strategies for Outbound Real Estate Investments Presented by

Dr Henry Chin

Head of Research, Asia Pacific

CBRE

2 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

What are investors thinking?

Continue to commit more capital into real estate

Increase risk appetite, but prefer to stay at domestic markets

CRE is perceived to be overpriced by investors

Where are investors going?

Strong growth in global investment activities

Less inflow but more outflow from Asia Pacific

Increasing RE allocation from Asian institutional investors

How will investors allocate their capitals globally?

Progress of institutionalization of real estate investments and industries

Multiple options to deploy capitals

Various investment themes globally based on risk-return profiles

KEY MESSAGES

WHAT ARE INVESTORS THINKING? Key Findings from Investor Intentions Survey

4 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

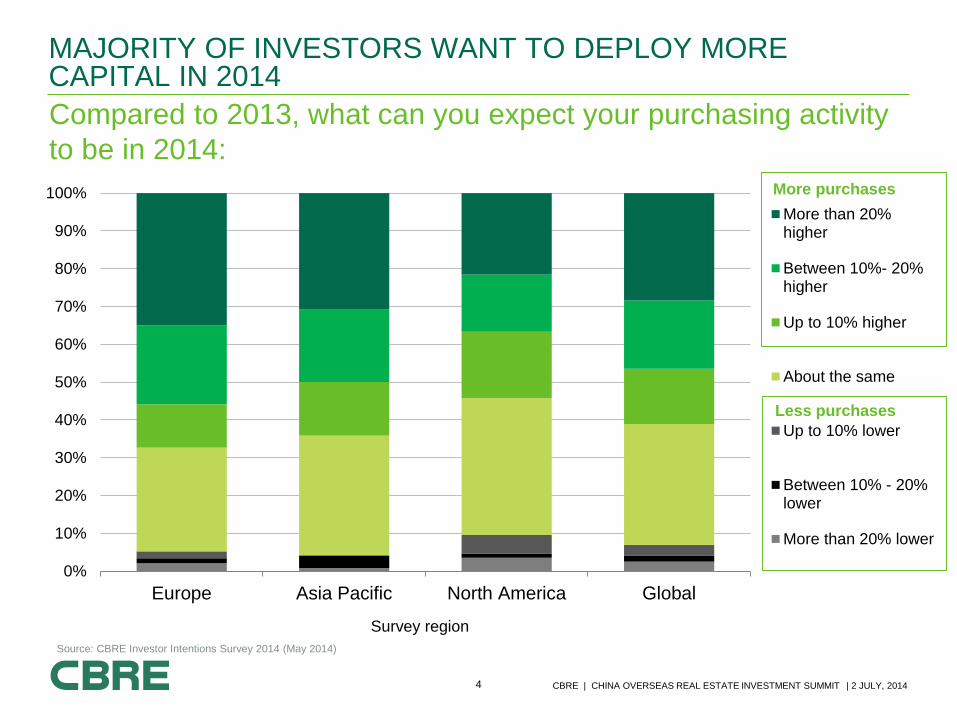

Compared to 2013, what can you expect your purchasing activity

to be in 2014:

MAJORITY OF INVESTORS WANT TO DEPLOY MORE CAPITAL IN 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Europe Asia Pacific North America Global

Survey region

More than 20%higher

Between 10%- 20%higher

Up to 10% higher

About the same

Up to 10% lower

Between 10% - 20%lower

More than 20% lower

Source: CBRE Investor Intentions Survey 2014 (May 2014)

More purchases

Less purchases

5 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

AND PREFER GLOBAL MAJOR CITIES

30% 14%

9%

London Madrid Berlin Munich Paris

6% 6%

Sydney Tokyo Shanghai Melbourne Jakarta

18% 17%

11% 8%

6%

Source: CBRE Investor Intentions Survey 2014 (May 2014)

Asia Pacific

Europe

North America 8.5%

SF LA SEA NYC HOU

7% 5.5% 5% 5%

6 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

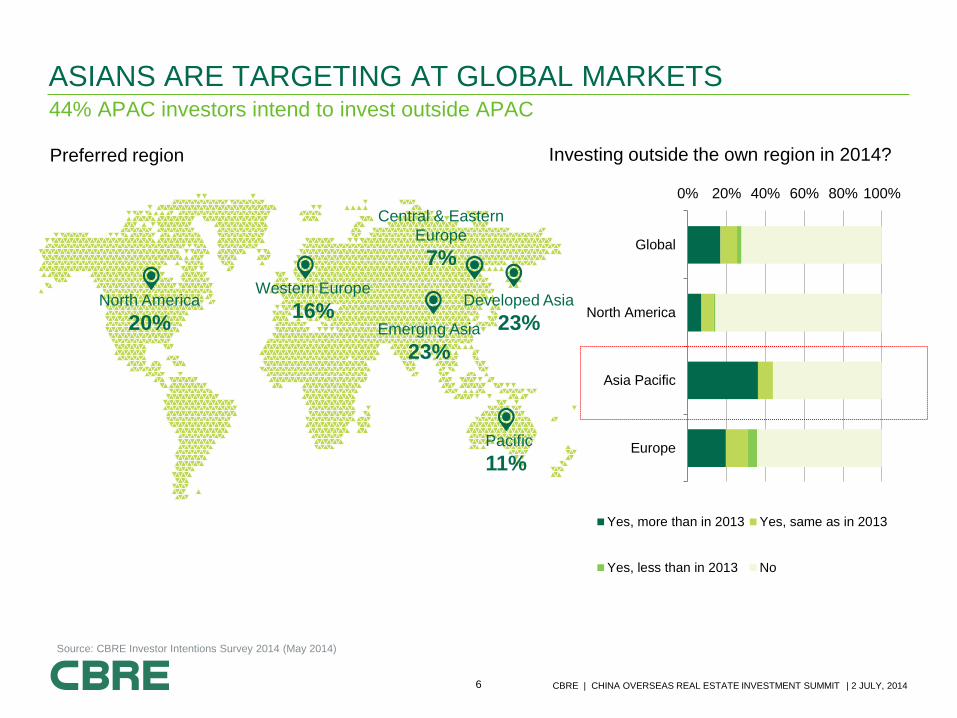

44% APAC investors intend to invest outside APAC

ASIANS ARE TARGETING AT GLOBAL MARKETS

Pacific

11%

Western Europe

16% North America

20% Developed Asia

23% Emerging Asia

23%

Central & Eastern

Europe

7%

0% 20% 40% 60% 80% 100%

Europe

Asia Pacific

North America

Global

Yes, more than in 2013 Yes, same as in 2013

Yes, less than in 2013 No

Investing outside the own region in 2014? Preferred region

Source: CBRE Investor Intentions Survey 2014 (May 2014)

7 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

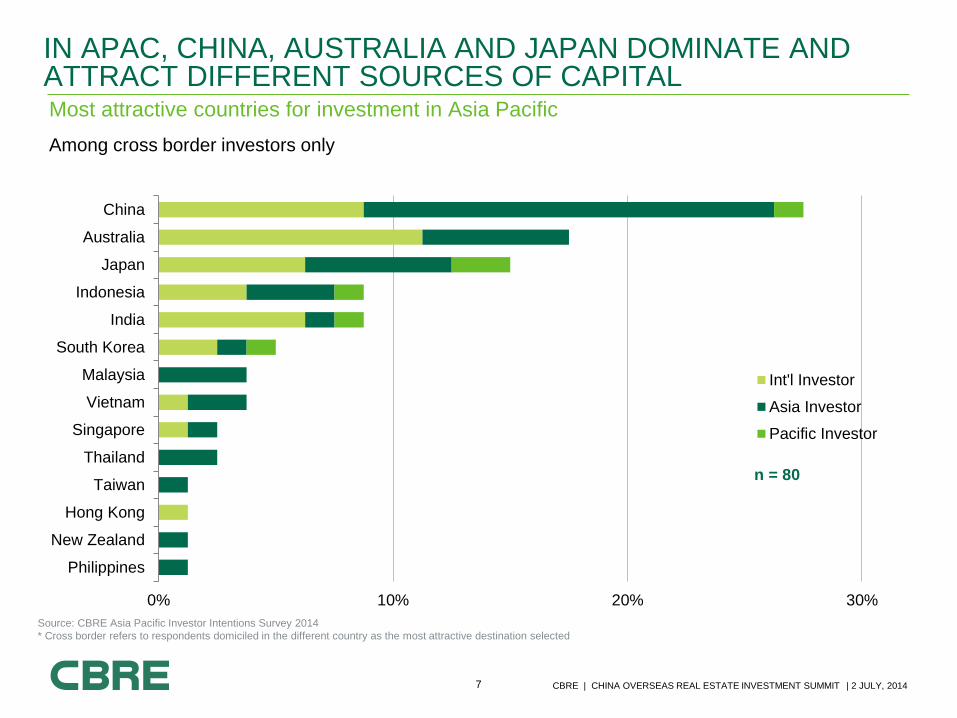

Most attractive countries for investment in Asia Pacific

Among cross border investors only

IN APAC, CHINA, AUSTRALIA AND JAPAN DOMINATE AND ATTRACT DIFFERENT SOURCES OF CAPITAL

Source: CBRE Asia Pacific Investor Intentions Survey 2014

* Cross border refers to respondents domiciled in the different country as the most attractive destination selected

0% 10% 20% 30%

Philippines

New Zealand

Hong Kong

Taiwan

Thailand

Singapore

Vietnam

Malaysia

South Korea

India

Indonesia

Japan

Australia

China

Int'l Investor

Asia Investor

Pacific Investor

n = 80

8 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Prime or coreassets

Goodsecondary

Opportunistic /value-added

Distressedassets

STRONGER APPETITE FOR RISKIER ASSETS Count of Final Size (mn USD)

Primary Strategy Total

Core 7

Core-Plus 13

Debt 23

Distressed 15

Fund of Funds 9

Opportunistic 45

Secondaries

Value Added 45

Grand Total 157

Sum of Final Size (mn

USD)

Primary Strategy Total

Core

1,839

Core-Plus

2,214

Debt

12,237

Distressed

12,701

Fund of Funds

1,076

Opportunistic

34,698

Secondaries

Value Added

17,534

Grand Total

82,298

Source: CBRE Asia Pacific Investor Intentions Survey 2014

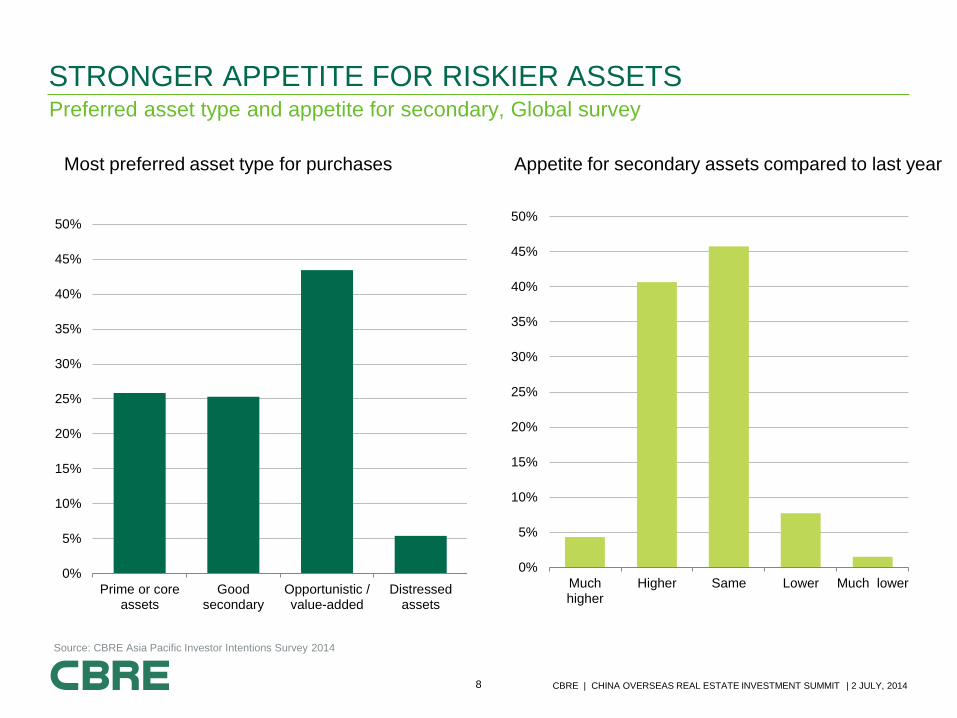

Most preferred asset type for purchases Appetite for secondary assets compared to last year

Preferred asset type and appetite for secondary, Global survey

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Muchhigher

Higher Same Lower Much lower

9 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

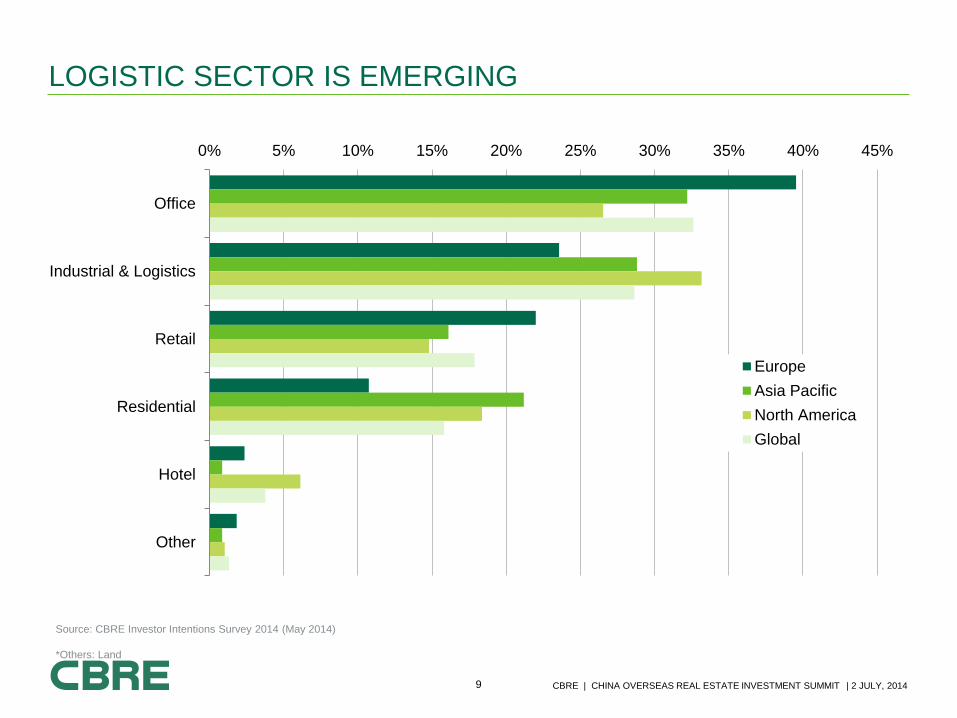

LOGISTIC SECTOR IS EMERGING

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Office

Industrial & Logistics

Retail

Residential

Hotel

Other

Europe

Asia Pacific

North America

Global

Source: CBRE Investor Intentions Survey 2014 (May 2014)

*Others: Land

10 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

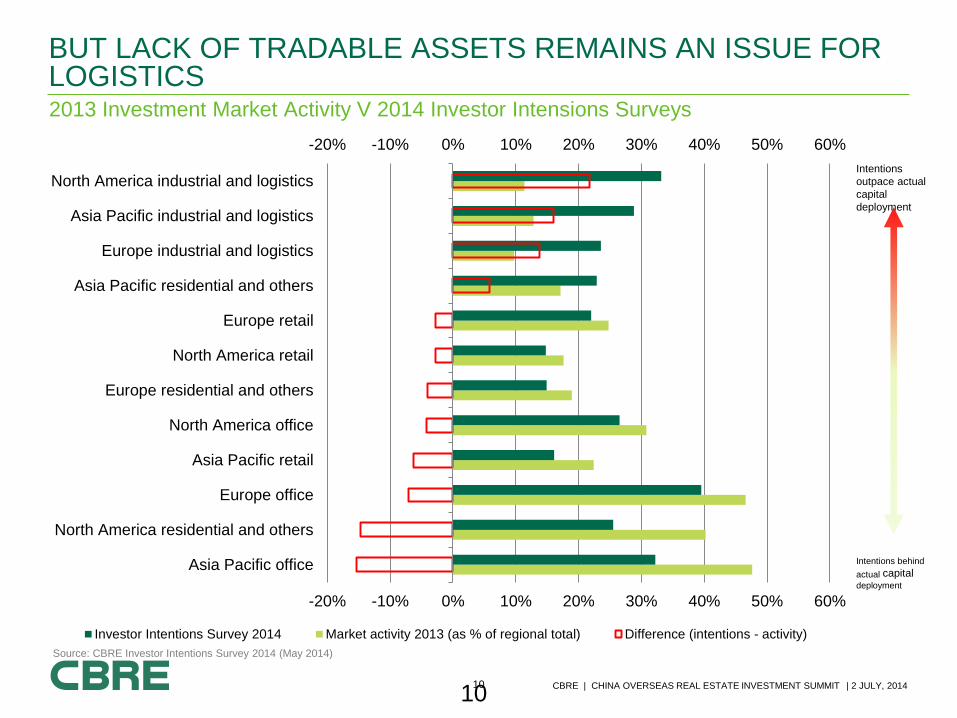

BUT LACK OF TRADABLE ASSETS REMAINS AN ISSUE FOR LOGISTICS

-20% -10% 0% 10% 20% 30% 40% 50% 60%

-20% -10% 0% 10% 20% 30% 40% 50% 60%

Asia Pacific office

North America residential and others

Europe office

Asia Pacific retail

North America office

Europe residential and others

North America retail

Europe retail

Asia Pacific residential and others

Europe industrial and logistics

Asia Pacific industrial and logistics

North America industrial and logistics

Investor Intentions Survey 2014 Market activity 2013 (as % of regional total) Difference (intentions - activity)

10

2013 Investment Market Activity V 2014 Investor Intensions Surveys

Intentions

outpace actual

capital

deployment

Intentions behind actual capital deployment

Source: CBRE Investor Intentions Survey 2014 (May 2014)

11 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

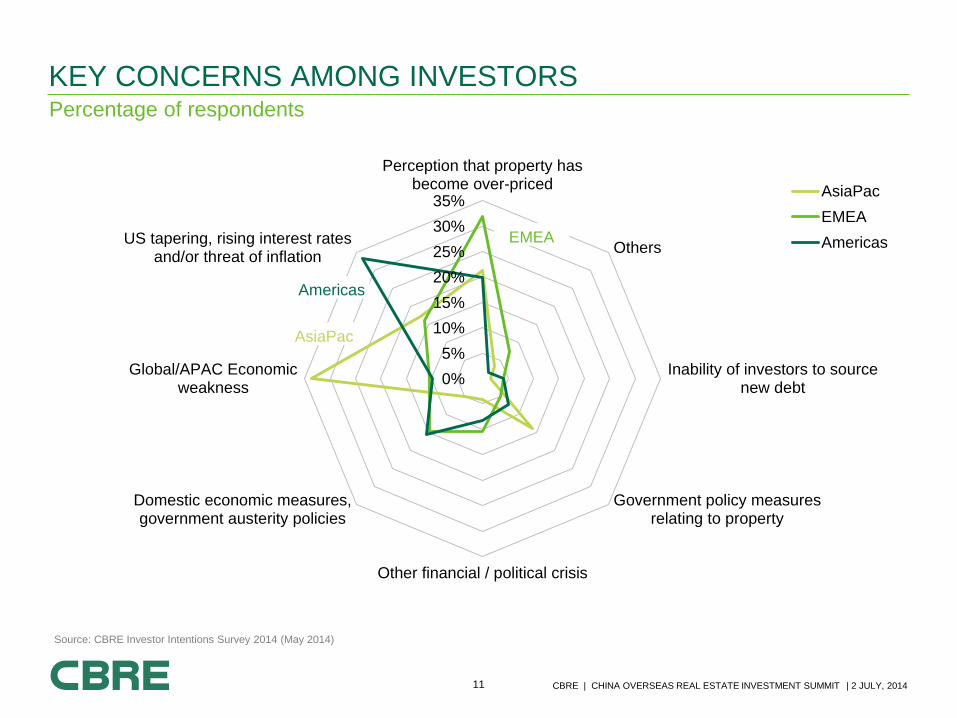

Percentage of respondents

KEY CONCERNS AMONG INVESTORS

0%

5%

10%

15%

20%

25%

30%

35%

Perception that property hasbecome over-priced

US tapering, rising interest ratesand/or threat of inflation

Global/APAC Economicweakness

Domestic economic measures,government austerity policies

Other financial / political crisis

Government policy measuresrelating to property

Inability of investors to sourcenew debt

Others

AsiaPac

EMEA

AmericasEMEA

Americas

Source: CBRE Investor Intentions Survey 2014 (May 2014)

AsiaPac

12 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

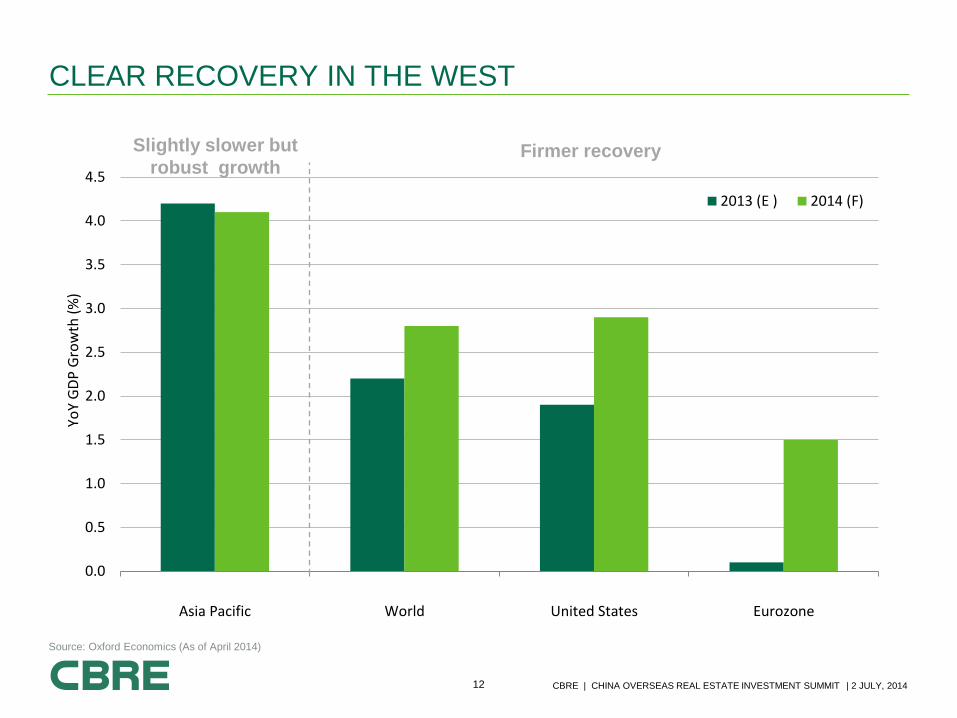

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Asia Pacific World United States Eurozone

2013 (E ) 2014 (F)

YoY

GD

P G

row

th (

%)

CLEAR RECOVERY IN THE WEST

Source: Oxford Economics (As of April 2014)

Slightly slower but

robust growth Firmer recovery

13 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

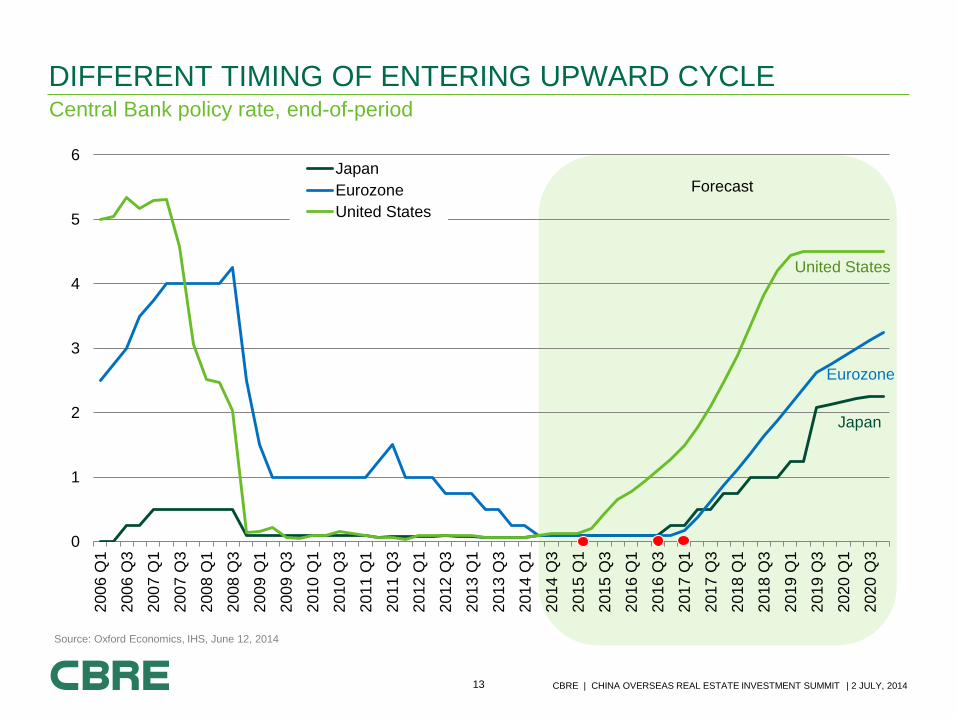

Central Bank policy rate, end-of-period

DIFFERENT TIMING OF ENTERING UPWARD CYCLE

0

1

2

3

4

5

6

200

6 Q

1

200

6 Q

3

200

7 Q

1

200

7 Q

3

200

8 Q

1

200

8 Q

3

200

9 Q

1

200

9 Q

3

201

0 Q

1

201

0 Q

3

201

1 Q

1

201

1 Q

3

201

2 Q

1

201

2 Q

3

201

3 Q

1

201

3 Q

3

201

4 Q

1

201

4 Q

3

201

5 Q

1

201

5 Q

3

201

6 Q

1

201

6 Q

3

201

7 Q

1

201

7 Q

3

201

8 Q

1

201

8 Q

3

201

9 Q

1

201

9 Q

3

202

0 Q

1

202

0 Q

3

Japan

Eurozone

United States

Forecast

Japan

Eurozone

United States

Source: Oxford Economics, IHS, June 12, 2014

CAPITAL FLOW Where are investors going?

15 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

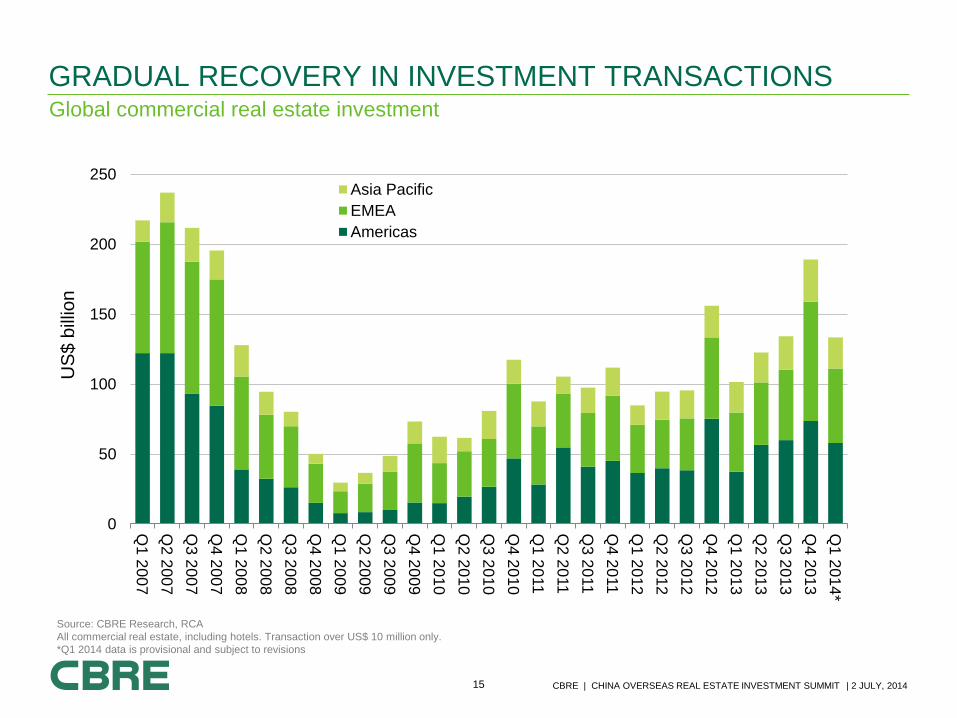

Global commercial real estate investment

GRADUAL RECOVERY IN INVESTMENT TRANSACTIONS

0

50

100

150

200

250

Q1

20

07

Q2

20

07

Q3

20

07

Q4

20

07

Q1

20

08

Q2

20

08

Q3

20

08

Q4

20

08

Q1

20

09

Q2

20

09

Q3

20

09

Q4

20

09

Q1

20

10

Q2

20

10

Q3

20

10

Q4

20

10

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

11

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

12

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

13

Q1

20

14

*

Asia Pacific

EMEA

Americas

US

$ b

illio

n

Source: CBRE Research, RCA

All commercial real estate, including hotels. Transaction over US$ 10 million only.

*Q1 2014 data is provisional and subject to revisions

16 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

Top 10 Global Investment Markets*, 2013

GATEWAYS CITIES DOMINATE

-

5

10

15

20

25

30

35

40

45

50

London New York Paris (IDF) Tokyo HongKong

Singapore Sydney Shanghai Houston Chicago

US

$ b

illio

n

Europe

North America

Asia Pacific

Source: CBRE Research, RCA

All commercial real estate, including hotels. Transaction over US$ 10 million only.

17 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

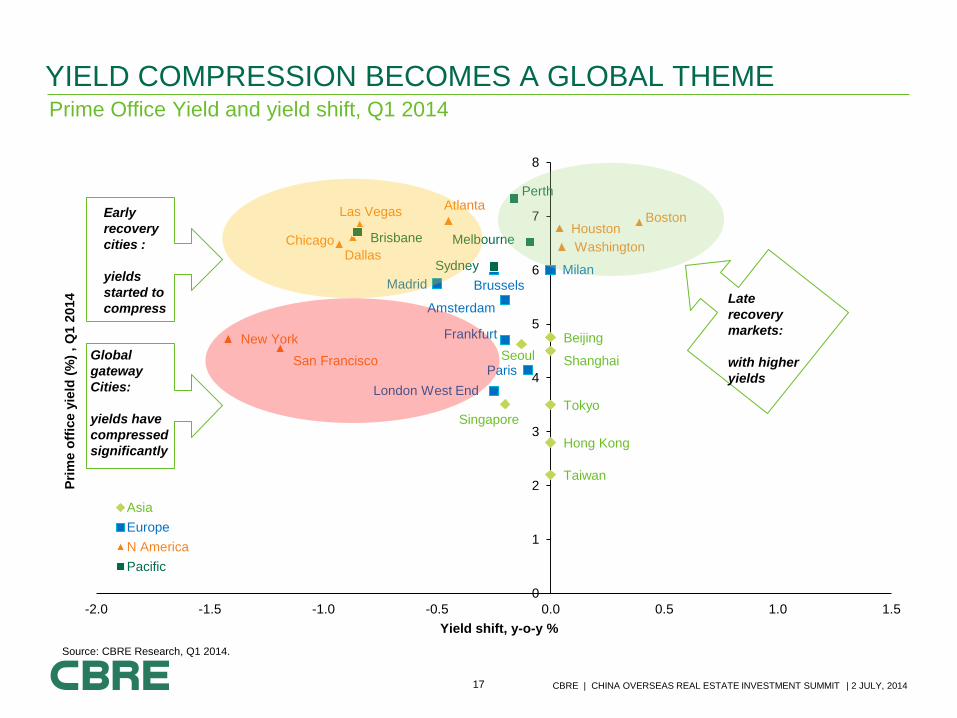

Beijing

Seoul Shanghai

Singapore Tokyo

Hong Kong

Taiwan

Madrid

Frankfurt

Paris

London West End

Brussels

Amsterdam

Milan

Chicago Washington

New York

San Francisco

Houston

Dallas

Atlanta Boston Las Vegas

Brisbane

Perth

Melbourne

Sydney

0

1

2

3

4

5

6

7

8

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Pri

me o

ffic

e y

ield

(%

) , Q

1 2

014

Yield shift, y-o-y %

Asia

Europe

N America

Pacific

Global

gateway

Cities:

yields have

compressed

significantly

Early

recovery

cities :

yields

started to

compress

YIELD COMPRESSION BECOMES A GLOBAL THEME Prime Office Yield and yield shift, Q1 2014

Source: CBRE Research, Q1 2014.

Late

recovery

markets:

with higher

yields

18 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

0%

2%

4%

6%

8%

10%

12%

0%

1%

2%

3%

4%

5%

6%

Apr-

03

Oct-

03

Apr-

04

Oct-

04

Apr-

05

Oct-

05

Apr-

06

Oct-

06

Apr-

07

Oct-

07

Apr-

08

Oct-

08

Apr-

09

Oct-

09

Apr-

10

Oct-

10

Apr-

11

Oct-

11

Apr-

12

Oct-

12

Apr-

13

Oct-

13

Apr-

14

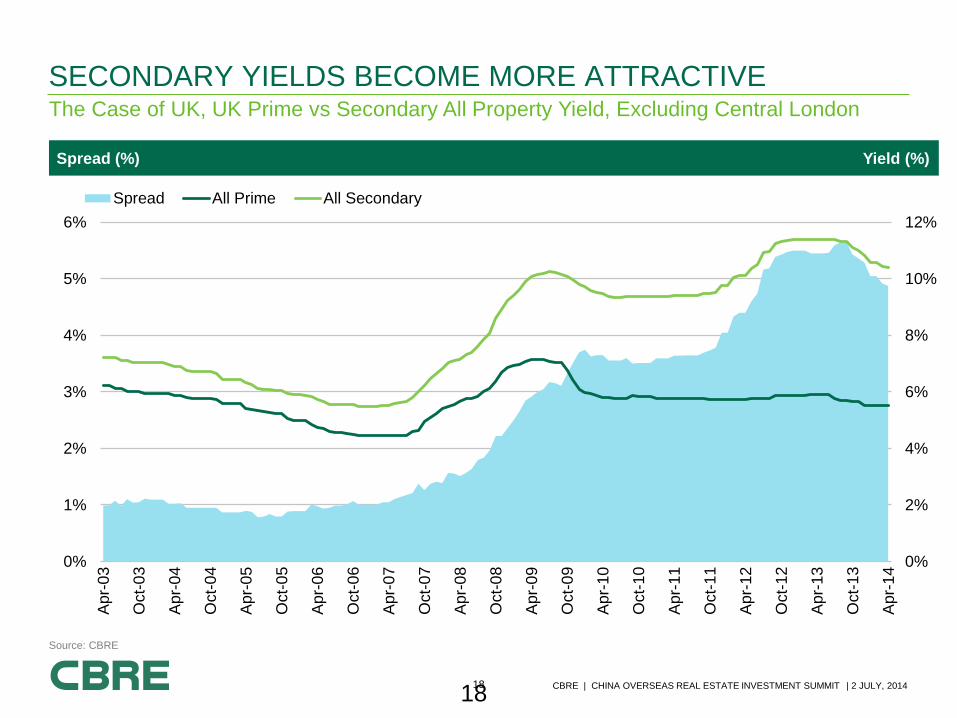

Spread All Prime All Secondary

18

SECONDARY YIELDS BECOME MORE ATTRACTIVE

Spread (%) Yield (%)

Source: CBRE

The Case of UK, UK Prime vs Secondary All Property Yield, Excluding Central London

19 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

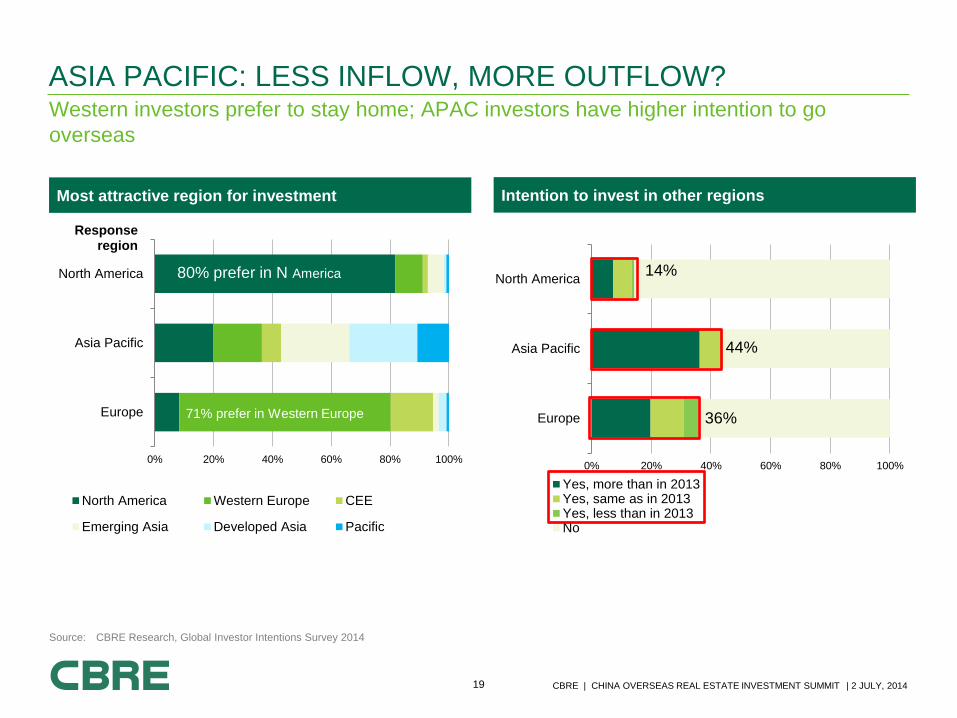

Western investors prefer to stay home; APAC investors have higher intention to go

overseas

ASIA PACIFIC: LESS INFLOW, MORE OUTFLOW?

Most attractive region for investment Intention to invest in other regions

• This chart is embedded

and can be edited

when required

STEPS

1. To edit elements

within the chart

select the element

and the ‘Chart Tools’

tabs will become

available in your

ribbon (alternatively

select the element

and right-click,

‘Format …’)

2. Apply required

changes

3. To edit data, select

the chart and right-

click. Select ‘Edit

Data’ – an Excel

window containing

the chart data will

open

Source: CBRE Research, Global Investor Intentions Survey 2014

0% 20% 40% 60% 80% 100%

Europe

Asia Pacific

North America

Response region

North America Western Europe CEE

Emerging Asia Developed Asia Pacific

0% 20% 40% 60% 80% 100%

Europe

Asia Pacific

North America

Yes, more than in 2013Yes, same as in 2013Yes, less than in 2013No

80% prefer in N America

71% prefer in Western Europe

14%

44%

36%

20 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

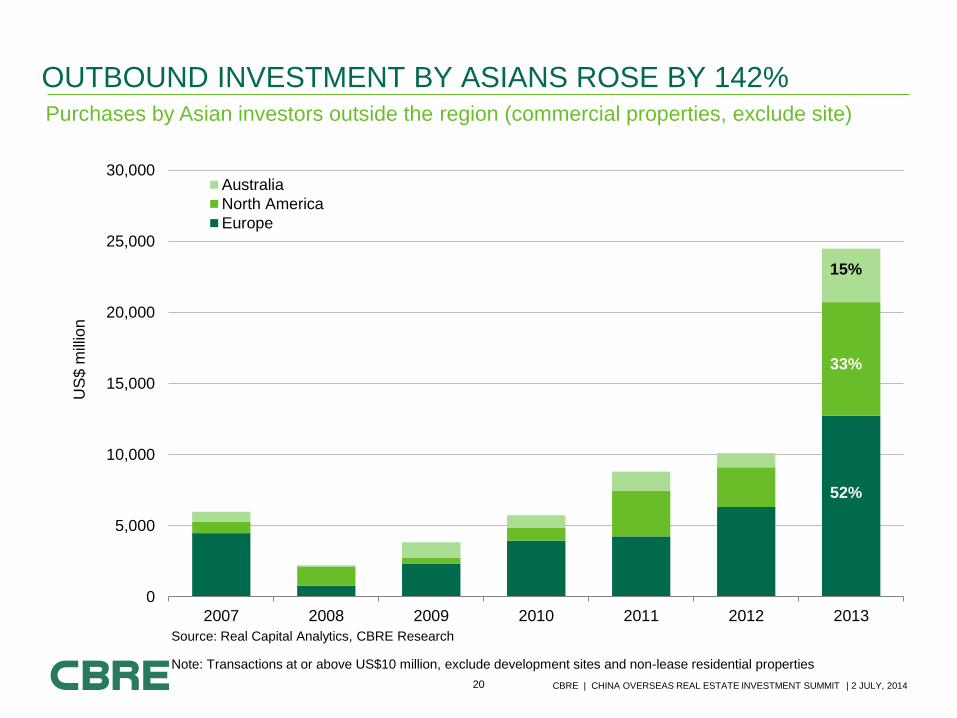

OUTBOUND INVESTMENT BY ASIANS ROSE BY 142%

0

5,000

10,000

15,000

20,000

25,000

30,000

2007 2008 2009 2010 2011 2012 2013

US

$ m

illio

n

Australia

North America

Europe

Source: Real Capital Analytics, CBRE Research

Note: Transactions at or above US$10 million, exclude development sites and non-lease residential properties

Purchases by Asian investors outside the region (commercial properties, exclude site)

52%

33%

15%

21 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

…GROWTH WAS LED BY CHINESE AND SINGAPOREAN

0

5,000

10,000

15,000

20,000

25,000

30,000

2007 2008 2009 2010 2011 2012 2013

US

$ m

illio

n

Rest of Asia

Hong Kong

Japan

Malaysia

South Korea

China

Singapore

Source: Real Capital Analytics, CBRE Research

Note: Transactions at or above US$10 million, exclude development sites and non-lease residential properties

Purchases by Asian investors outside the region (commercial properties, exclude site)

22 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

.. FOCUS ON GATEWAY CITIES AND TROPHY ASSETS

US$10m and above, office, retail, industrial and mixed use properties Only

Source: RCA, CBRE Research

- 2,000 4,000 6,000 8,000 10,000 12,000

London

New York

Sydney

Singapore

Shanghai

Melbourne

Guangzhou

Hawaii

Beijing

Hong Kong

Paris

Houston

Los Angeles

Jakarta

UK Nationwide

US$ millions

Asian’s Top cross-border destinations, 2013

Europe

North America

Asia Pacific

23 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

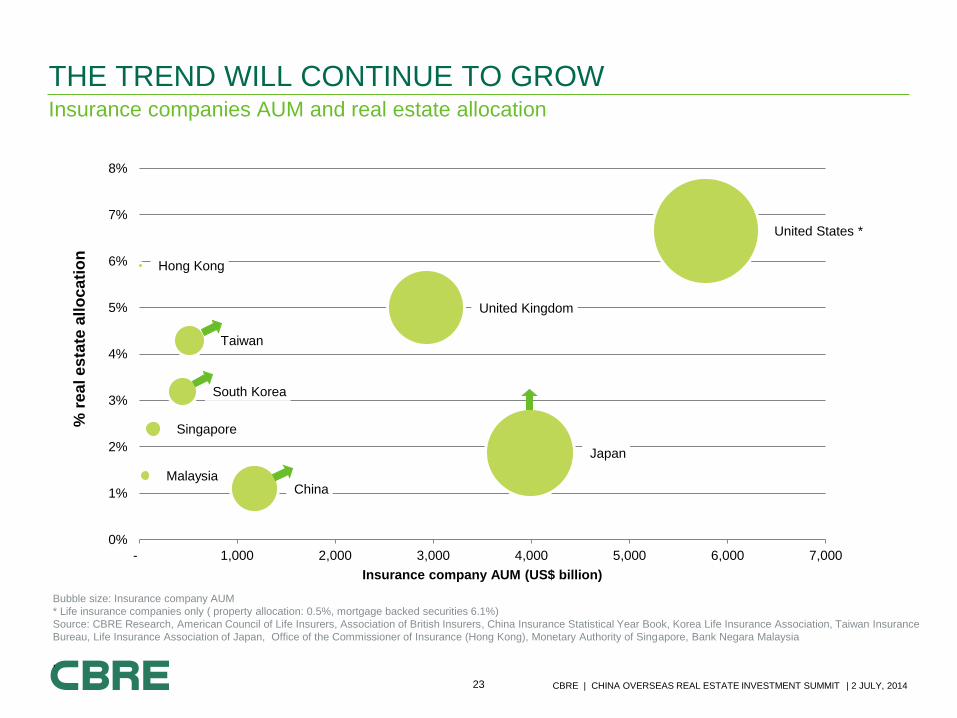

Insurance companies AUM and real estate allocation

THE TREND WILL CONTINUE TO GROW

United States *

Hong Kong

United Kingdom

Taiwan

South Korea

Singapore

Japan

Malaysia China

0%

1%

2%

3%

4%

5%

6%

7%

8%

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

% r

ea

l e

sta

te a

llo

ca

tio

n

Insurance company AUM (US$ billion)

Bubble size: Insurance company AUM

* Life insurance companies only ( property allocation: 0.5%, mortgage backed securities 6.1%)

Source: CBRE Research, American Council of Life Insurers, Association of British Insurers, China Insurance Statistical Year Book, Korea Life Insurance Association, Taiwan Insurance

Bureau, Life Insurance Association of Japan, Office of the Commissioner of Insurance (Hong Kong), Monetary Authority of Singapore, Bank Negara Malaysia

,

INVESTMENT STRATEGY How will investors allocate their capitals globally?

25 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

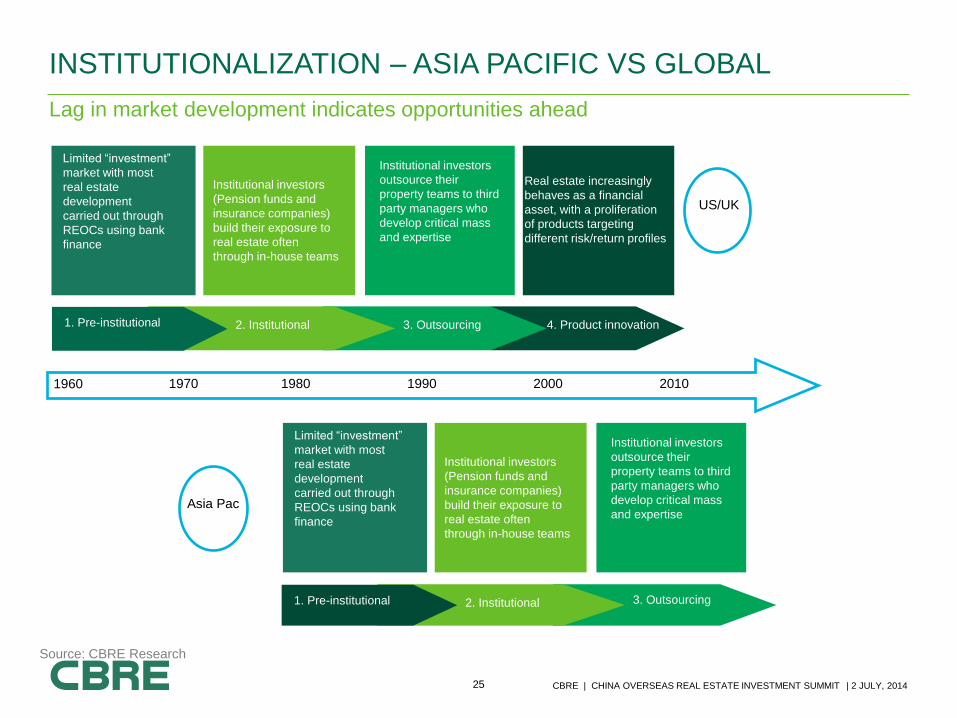

INSTITUTIONALIZATION – ASIA PACIFIC VS GLOBAL

Source: CBRE Research

Limited “investment”

market with most

real estate

development

carried out through

REOCs using bank

finance

Institutional investors

(Pension funds and

insurance companies)

build their exposure to

real estate often

through in-house teams

Institutional investors

outsource their

property teams to third

party managers who

develop critical mass

and expertise

Real estate increasingly

behaves as a financial

asset, with a proliferation

of products targeting

different risk/return profiles

1. Pre-institutional 2. Institutional 3. Outsourcing 4. Product innovation

1960 1970 1980 1990 2000 2010

US/UK

Asia Pac

Limited “investment”

market with most

real estate

development

carried out through

REOCs using bank

finance

Institutional investors

(Pension funds and

insurance companies)

build their exposure to

real estate often

through in-house teams

Institutional investors

outsource their

property teams to third

party managers who

develop critical mass

and expertise

1. Pre-institutional 2. Institutional 3. Outsourcing

Lag in market development indicates opportunities ahead

26 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

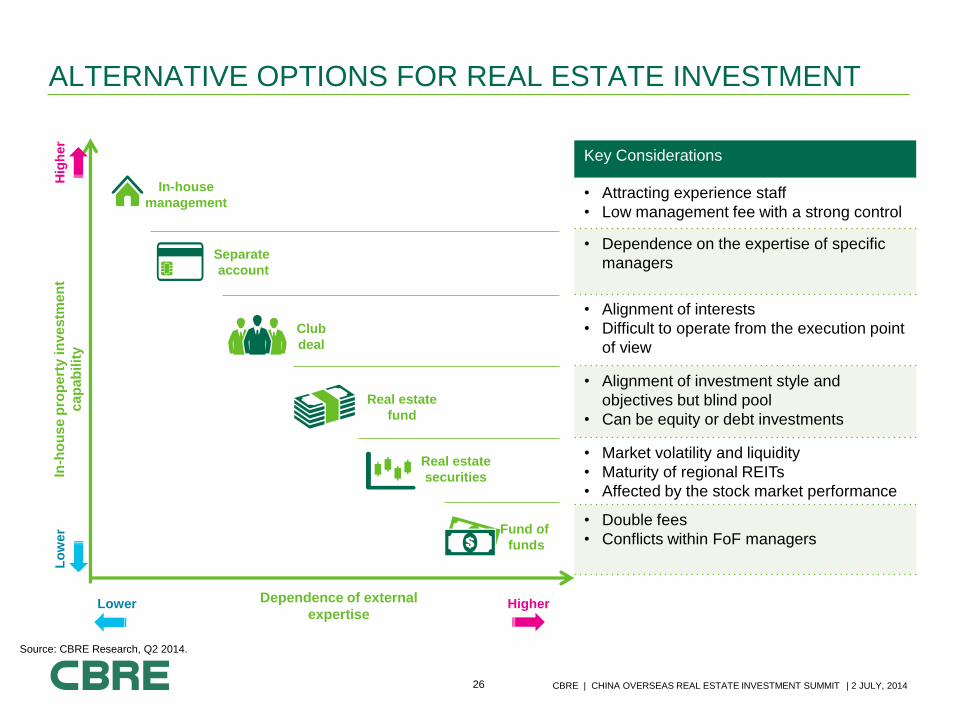

ALTERNATIVE OPTIONS FOR REAL ESTATE INVESTMENT

In-house

management

In-h

ou

se

pro

pe

rty i

nve

stm

en

t

ca

pa

bilit

y

Dependence of external

expertise

Separate

account

Club

deal

Real estate

fund

Real estate

securities

Fund of

funds

Source: CBRE Research, Q2 2014.

Lower Higher

Lo

wer

Hig

her

Key Considerations

• Attracting experience staff

• Low management fee with a strong control

• Dependence on the expertise of specific

managers

• Alignment of interests

• Difficult to operate from the execution point

of view

• Alignment of investment style and

objectives but blind pool

• Can be equity or debt investments

• Market volatility and liquidity

• Maturity of regional REITs

• Affected by the stock market performance

• Double fees

• Conflicts within FoF managers

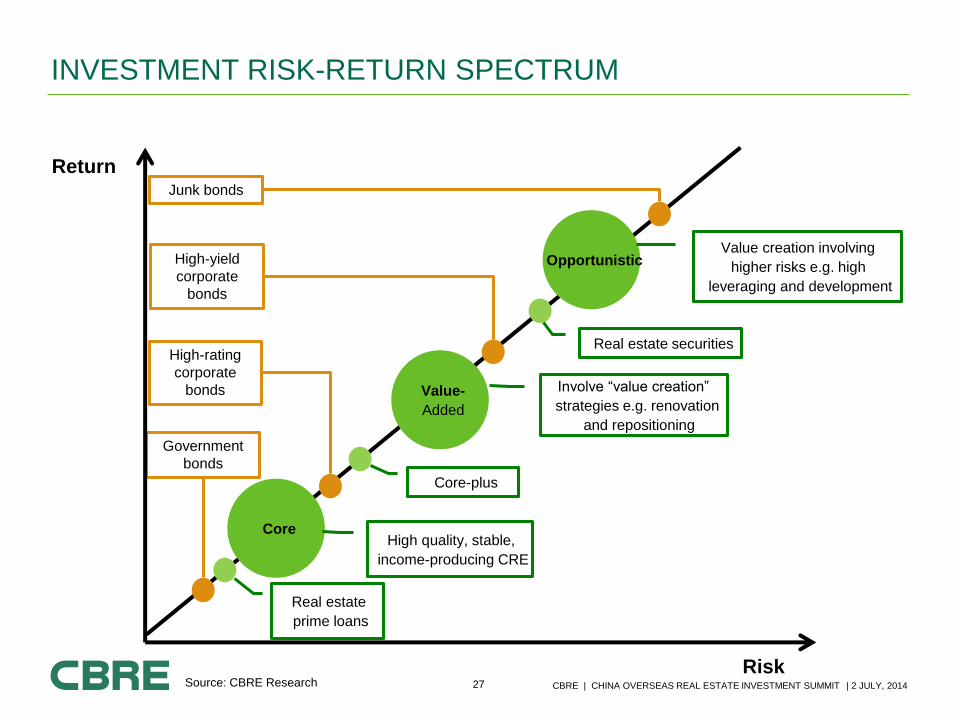

27 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014 Source: CBRE Research

Core

Value-

Added

Opportunistic

High quality, stable,

income-producing CRE

Value creation involving

higher risks e.g. high

leveraging and development

Involve “value creation”

strategies e.g. renovation

and repositioning

Government

bonds

High-rating

corporate

bonds

High-yield

corporate

bonds

Junk bonds

Real estate

prime loans

Core-plus

Real estate securities

INVESTMENT RISK-RETURN SPECTRUM

Risk

Return

28 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

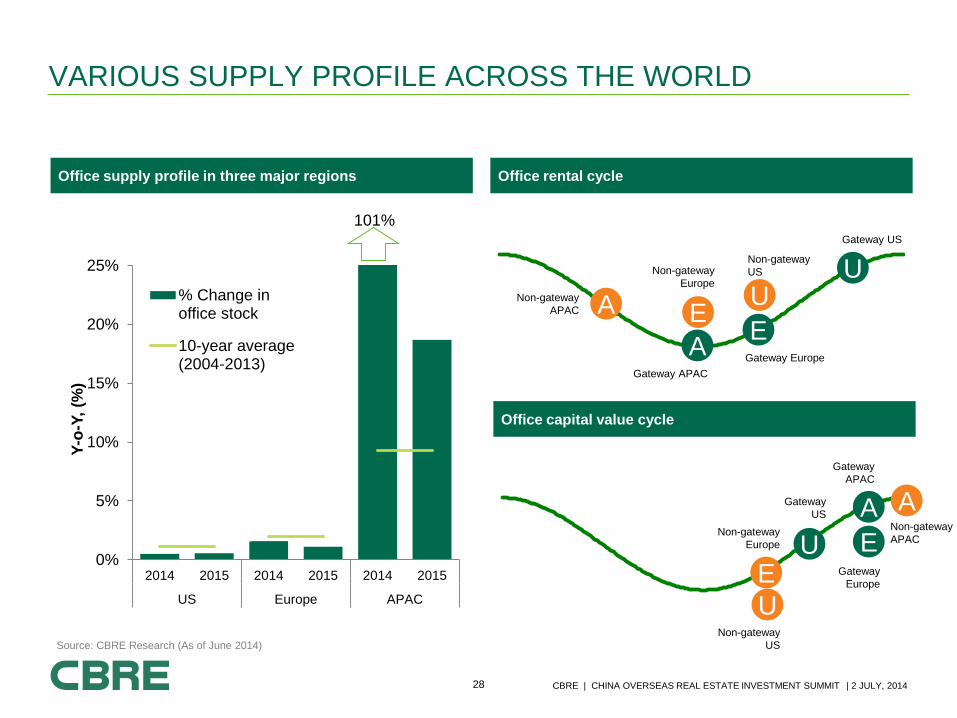

0%

5%

10%

15%

20%

25%

2014 2015 2014 2015 2014 2015

US Europe APAC

Y-o

-Y,

(%)

% Change inoffice stock

10-year average(2004-2013)

VARIOUS SUPPLY PROFILE ACROSS THE WORLD

Source: CBRE Research (As of June 2014)

A E

Office supply profile in three major regions Office rental cycle

U U

E A Non-gateway

APAC

Non-gateway

Europe

Gateway APAC

Gateway US

Gateway Europe

Non-gateway

US

A

E

Office capital value cycle

U

U

E

A Non-gateway

APAC Non-gateway

Europe

Gateway

APAC

Gateway

US

Gateway

Europe

Non-gateway

US

101%

29 CBRE | CHINA OVERSEAS REAL ESTATE INVESTMENT SUMMIT | 2 JULY, 2014

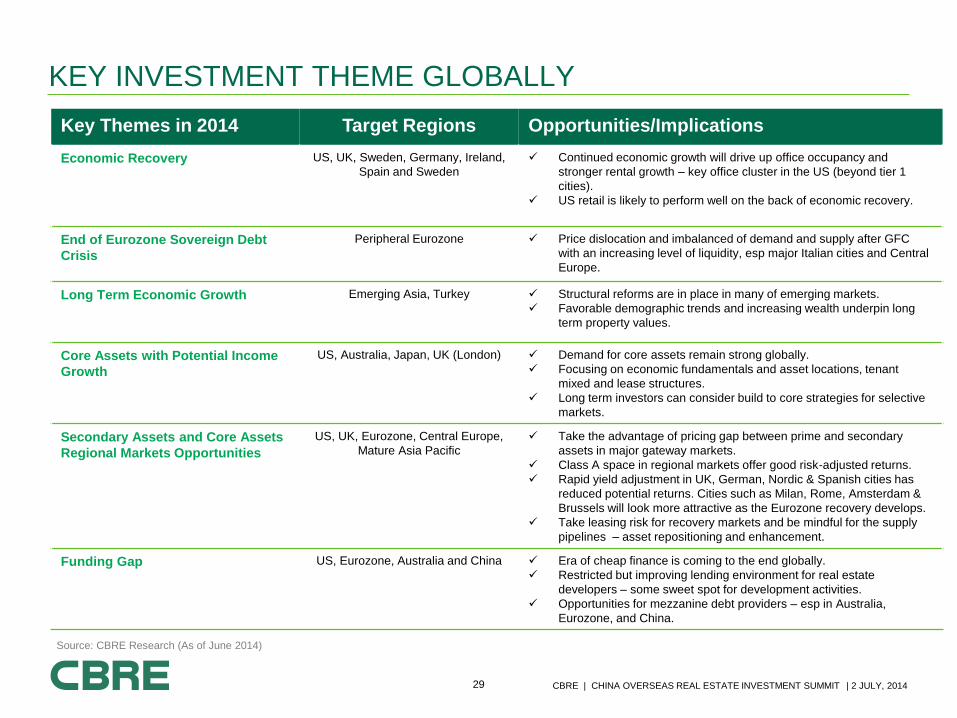

KEY INVESTMENT THEME GLOBALLY

Key Themes in 2014 Target Regions Opportunities/Implications

Economic Recovery US, UK, Sweden, Germany, Ireland,

Spain and Sweden

Continued economic growth will drive up office occupancy and

stronger rental growth – key office cluster in the US (beyond tier 1

cities).

US retail is likely to perform well on the back of economic recovery.

End of Eurozone Sovereign Debt

Crisis

Peripheral Eurozone Price dislocation and imbalanced of demand and supply after GFC

with an increasing level of liquidity, esp major Italian cities and Central

Europe.

Long Term Economic Growth Emerging Asia, Turkey Structural reforms are in place in many of emerging markets.

Favorable demographic trends and increasing wealth underpin long

term property values.

Core Assets with Potential Income

Growth

US, Australia, Japan, UK (London) Demand for core assets remain strong globally.

Focusing on economic fundamentals and asset locations, tenant

mixed and lease structures.

Long term investors can consider build to core strategies for selective

markets.

Secondary Assets and Core Assets

Regional Markets Opportunities

US, UK, Eurozone, Central Europe,

Mature Asia Pacific

Take the advantage of pricing gap between prime and secondary

assets in major gateway markets.

Class A space in regional markets offer good risk-adjusted returns.

Rapid yield adjustment in UK, German, Nordic & Spanish cities has

reduced potential returns. Cities such as Milan, Rome, Amsterdam &

Brussels will look more attractive as the Eurozone recovery develops.

Take leasing risk for recovery markets and be mindful for the supply

pipelines – asset repositioning and enhancement.

Funding Gap US, Eurozone, Australia and China Era of cheap finance is coming to the end globally.

Restricted but improving lending environment for real estate

developers – some sweet spot for development activities.

Opportunities for mezzanine debt providers – esp in Australia,

Eurozone, and China.

Source: CBRE Research (As of June 2014)

Thank you