trend barometer real estate investment market - ey · pdf filemarket outlook and strategies...

TRANSCRIPT

Trend BarometerReal Estate Investment MarketSwitzerland 2016

Page 2

Overview of content

Swiss real estate transaction market, pages 4-5

Survey structure and methodology, pages 7-8

Market outlook and strategies Switzerland 2016, pages 7-29

Trend Barometer Real EstateInvestment Market Switzerland2016

Key messages Switzerland 2016, pages 31-32

Your contacts, page 33

Swiss Real Estate Transaction Market

Page 4

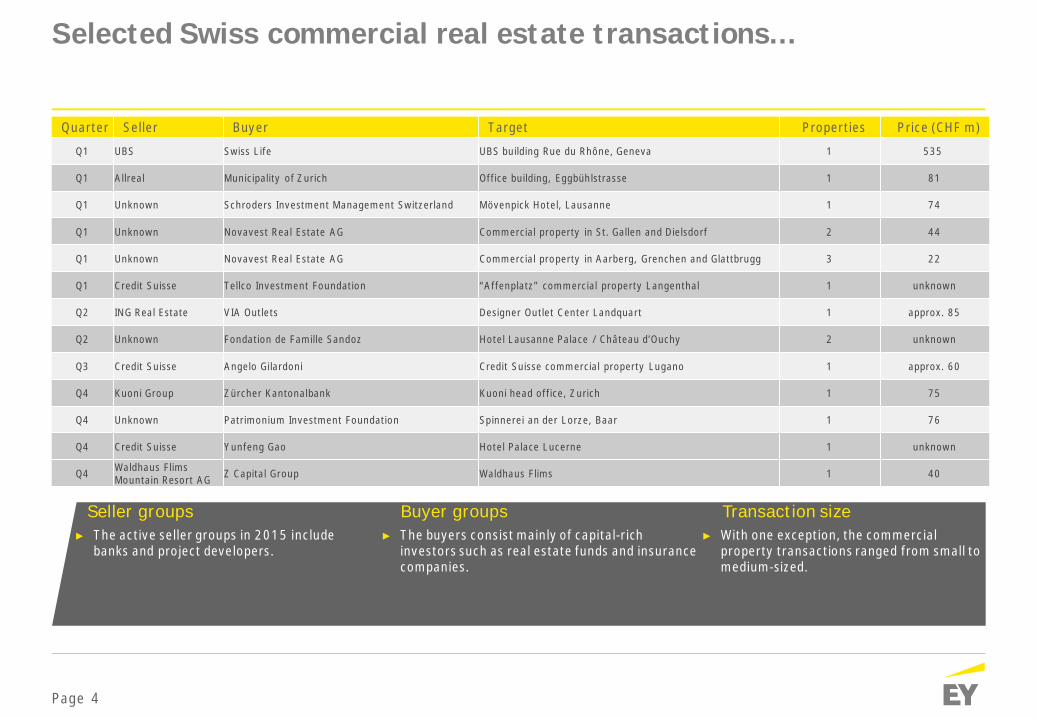

Selected Swiss commercial real estate transactions...

Quarter Seller Buyer Target Properties Price (CHF m)

Q1 UBS Swiss Life UBS building Rue du Rhône, Geneva 1 535

Q1 Allreal Municipality of Zurich Office building, Eggbühlstrasse 1 81

Q1 Unknown Schroders Investment Management Switzerland Mövenpick Hotel, Lausanne 1 74

Q1 Unknown Novavest Real Estate AG Commercial property in St. Gallen and Dielsdorf 2 44

Q1 Unknown Novavest Real Estate AG Commercial property in Aarberg, Grenchen and Glattbrugg 3 22

Q1 Credit Suisse Tellco Investment Foundation “Affenplatz” commercial property Langenthal 1 unknown

Q2 ING Real Estate VIA Outlets Designer Outlet Center Landquart 1 approx. 85

Q2 Unknown Fondation de Famille Sandoz Hotel Lausanne Palace / Château d’Ouchy 2 unknown

Q3 Credit Suisse Angelo Gilardoni Credit Suisse commercial property Lugano 1 approx. 60

Q4 Kuoni Group Zürcher Kantonalbank Kuoni head office, Zurich 1 75

Q4 Unknown Patrimonium Investment Foundation Spinnerei an der Lorze, Baar 1 76

Q4 Credit Suisse Yunfeng Gao Hotel Palace Lucerne 1 unknown

Q4 Waldhaus FlimsMountain Resort AG Z Capital Group Waldhaus Flims 1 40

Seller groups Buyer groups► The active seller groups in 2015 include

banks and project developers.

Transaction size► The buyers consist mainly of capital-rich

investors such as real estate funds and insurancecompanies.

► With one exception, the commercialproperty transactions ranged from small tomedium-sized.

Page 5

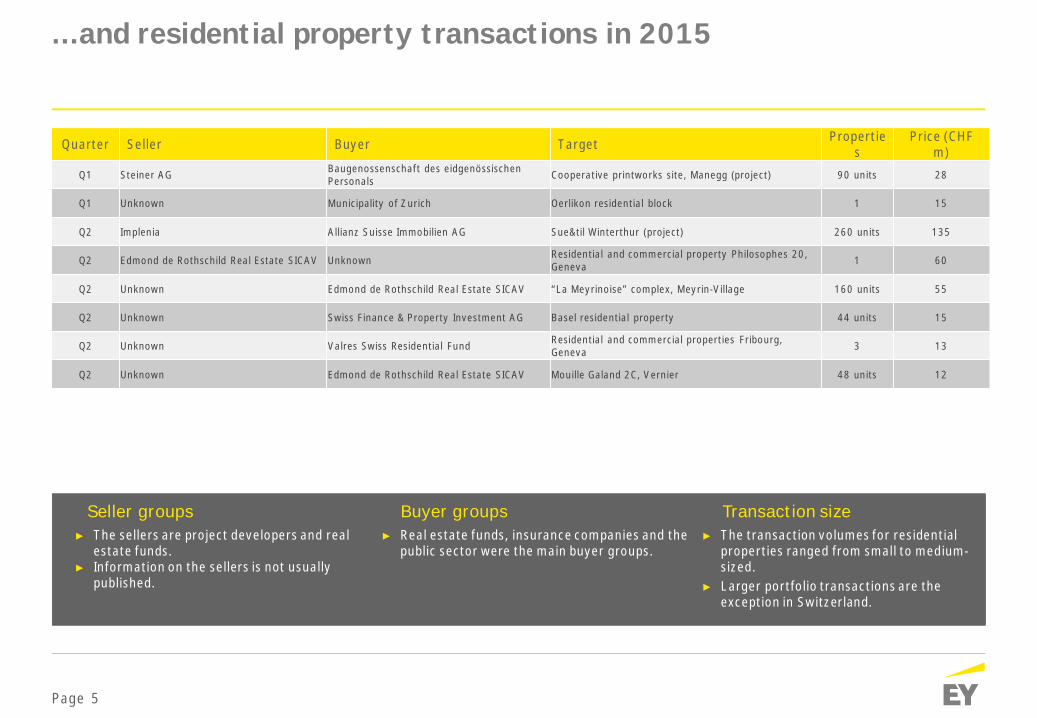

Quarter Seller Buyer Target Properties

Price (CHFm)

Q1 Steiner AG Baugenossenschaft des eidgenössischenPersonals Cooperative printworks site, Manegg (project) 90 units 28

Q1 Unknown Municipality of Zurich Oerlikon residential block 1 15

Q2 Implenia Allianz Suisse Immobilien AG Sue&til Winterthur (project) 260 units 135

Q2 Edmond de Rothschild Real Estate SICAV Unknown Residential and commercial property Philosophes 20,Geneva 1 60

Q2 Unknown Edmond de Rothschild Real Estate SICAV “La Meyrinoise” complex, Meyrin-Village 160 units 55

Q2 Unknown Swiss Finance & Property Investment AG Basel residential property 44 units 15

Q2 Unknown Valres Swiss Residential Fund Residential and commercial properties Fribourg,Geneva 3 13

Q2 Unknown Edmond de Rothschild Real Estate SICAV Mouille Galand 2C, Vernier 48 units 12

...and residential property transactions in 2015

Seller groups Buyer groups► The sellers are project developers and real

estate funds.► Information on the sellers is not usually

published.

Transaction size► Real estate funds, insurance companies and the

public sector were the main buyer groups.► The transaction volumes for residential

properties ranged from small to medium-sized.

► Larger portfolio transactions are theexception in Switzerland.

Trend Barometer Real EstateInvestment Market Switzerland 2016

Page 7

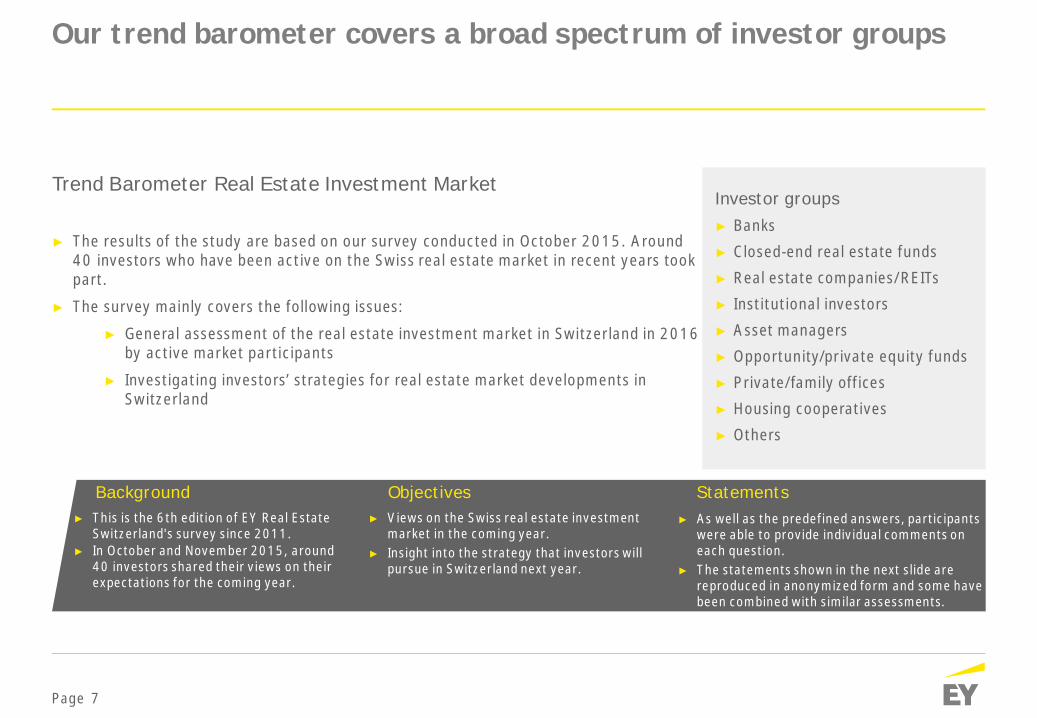

► The results of the study are based on our survey conducted in October 2015. Around40 investors who have been active on the Swiss real estate market in recent years tookpart.

► The survey mainly covers the following issues:

► General assessment of the real estate investment market in Switzerland in 2016by active market participants

► Investigating investors’ strategies for real estate market developments inSwitzerland

Trend Barometer Real Estate Investment MarketInvestor groups► Banks

► Closed-end real estate funds

► Real estate companies/REITs

► Institutional investors

► Asset managers

► Opportunity/private equity funds

► Private/family offices

► Housing cooperatives

► Others

► This is the 6th edition of EY Real EstateSwitzerland's survey since 2011.

► In October and November 2015, around40 investors shared their views on theirexpectations for the coming year.

Background Objectives► As well as the predefined answers, participants

were able to provide individual comments oneach question.

► The statements shown in the next slide arereproduced in anonymized form and some havebeen combined with similar assessments.

Statements► Views on the Swiss real estate investment

market in the coming year.► Insight into the strategy that investors will

pursue in Switzerland next year.

Our trend barometer covers a broad spectrum of investor groups

Page 8

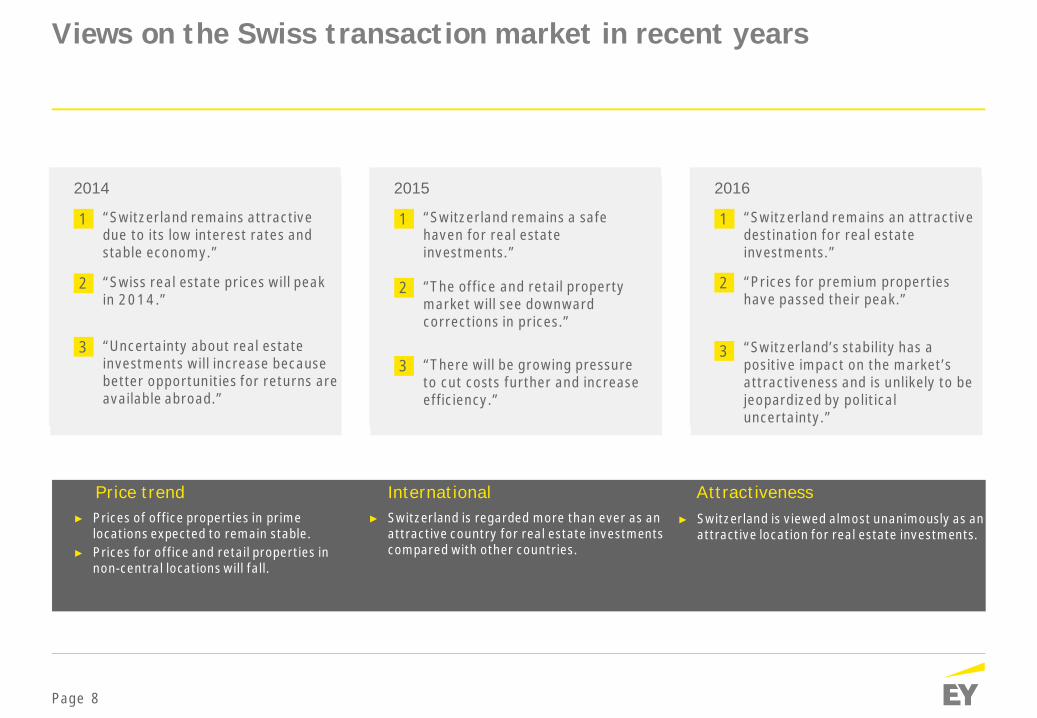

Views on the Swiss transaction market in recent years

► Prices of office properties in primelocations expected to remain stable.

► Prices for office and retail properties innon-central locations will fall.

Price trend International► Switzerland is viewed almost unanimously as an

attractive location for real estate investments.

Attractiveness► Switzerland is regarded more than ever as an

attractive country for real estate investmentscompared with other countries.

2015

“Switzerland remains a safehaven for real estateinvestments.”

1

3 “There will be growing pressureto cut costs further and increaseefficiency.”

2 “The office and retail propertymarket will see downwardcorrections in prices.”

2016

“Switzerland remains an attractivedestination for real estateinvestments.”

1

3 “Switzerland’s stability has apositive impact on the market’sattractiveness and is unlikely to bejeopardized by politicaluncertainty.”

2 “Prices for premium propertieshave passed their peak.”

2014

“Switzerland remains attractivedue to its low interest rates andstable economy.”

1

3 “Uncertainty about real estateinvestments will increase becausebetter opportunities for returns areavailable abroad.”

2 “Swiss real estate prices will peakin 2014.”

Page 9

Switzerland’s attractiveness as a location for real estate investments

Wording of the question: “In absolute terms, how do you rate Switzerland’s attractiveness as a location for real estate investments in 2016?”

91% of respondents rate Switzerland as an attractive or veryattractive investment location...

Key messages► The vast majority of respondents

(91%) continue to view Switzerlandas an attractive or very attractivelocation for real estate investmentsin 2016.

► The market is considered to beslightly less attractive than in theprevious year (2015: 97% consideredSwitzerland attractive or veryattractive).

Messages► “Property prices have reached a level that no longer provides an appropriate reward for the long term risks of real estate investments.”

(Pension fund)► “Given the very high price levels in most cases and generally falling rents the real estate investment market in Switzerland no longer offers

attractive yields even for investors with a long-term horizon.” (“Other” investor)► “Switzerland continues to deliver stable cash flow yields. However, its performance in terms of capital gains is much weaker.” (Insurer)

24 %

67 %

9 %

very attractive attractive less attractive

Page 10

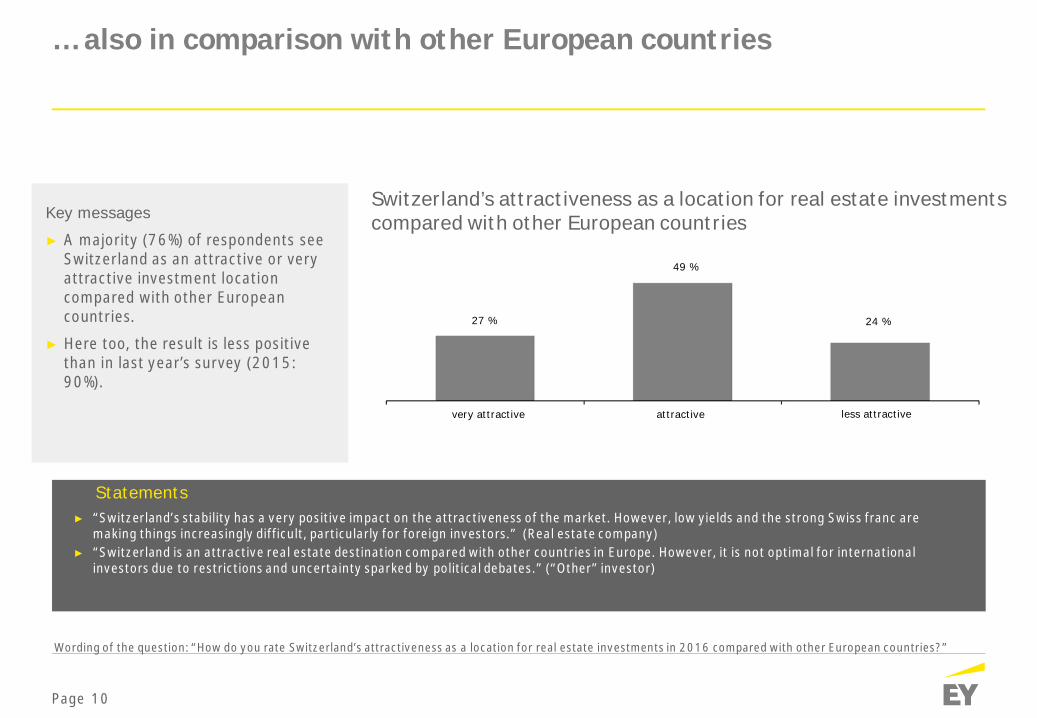

Wording of the question: “How do you rate Switzerland’s attractiveness as a location for real estate investments in 2016 compared with other European countries?”

… also in comparison with other European countries

Switzerland’s attractiveness as a location for real estate investmentscompared with other European countriesKey messages

► A majority (76%) of respondents seeSwitzerland as an attractive or veryattractive investment locationcompared with other Europeancountries.

► Here too, the result is less positivethan in last year’s survey (2015:90%).

► “Switzerland’s stability has a very positive impact on the attractiveness of the market. However, low yields and the strong Swiss franc aremaking things increasingly difficult, particularly for foreign investors.” (Real estate company)

► “Switzerland is an attractive real estate destination compared with other countries in Europe. However, it is not optimal for internationalinvestors due to restrictions and uncertainty sparked by political debates.” (“Other” investor)

Statements

27 %

49 %

24 %

very attractive attractive less attractive

Page 11

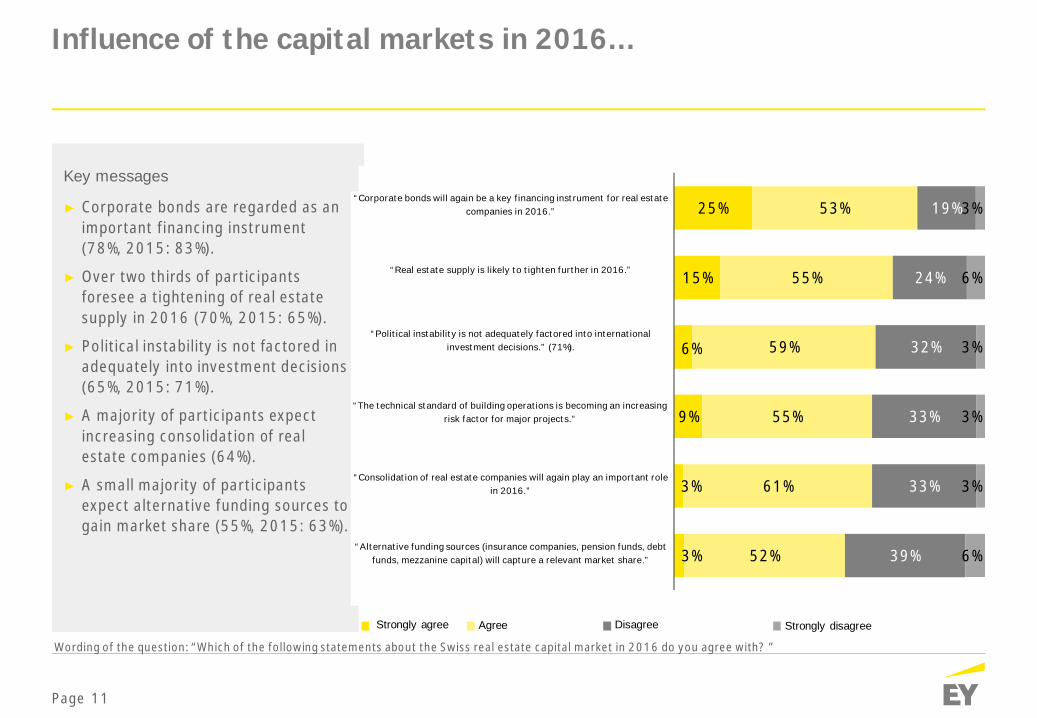

Influence of the capital markets in 2016...

Wording of the question: “Which of the following statements about the Swiss real estate capital market in 2016 do you agree with? ”

25%

15%

6%

9%

3%

3%

53%

55%

59%

55%

61%

52%

19%

24%

32%

33%

33%

39%

3%

6%

3%

3%

3%

6%

"Unternehmensanleihen sind auch 2016 ein wichtigesFinanzierungsinstrument für Immobiliengesellschaften."

"2016 ist mit einer weiteren Verknappung desImmobilienangebots zu rechnen."

"Politische Instabilitäten werden bei internationalenInvestitionsentscheidungen nicht hinreichend eingepreist."

"Die technische Inbetriebnahme von Bauleistungen wird einzunehmender Risikofaktor bei Grossprojekten."

"Auch im Jahr 2016 werden Konsolidierungen vonImmobiliengesellschaften eine wesentliche Rolle spielen."

"Alternative Finanzierungsquellen (Versicherungen,Pensionskassen, Debt Funds, Mezzanine-Kapital) erobern einenrelevanten Marktanteil."

Statements

Strongly agree Agree Disagree Strongly disagree

Key messages

► Corporate bonds are regarded as animportant financing instrument(78%, 2015: 83%).

► Over two thirds of participantsforesee a tightening of real estatesupply in 2016 (70%, 2015: 65%).

► Political instability is not factored inadequately into investment decisions(65%, 2015: 71%).

► A majority of participants expectincreasing consolidation of realestate companies (64%).

► A small majority of participantsexpect alternative funding sources togain market share (55%, 2015: 63%).

“Corporate bonds will again be a key financing instrument for real estatecompanies in 2016.”

“Real estate supply is likely to tighten further in 2016.”

“Political instability is not adequately factored into internationalinvestment decisions.” (71%).

“The technical standard of building operations is becoming an increasingrisk factor for major projects.”

“Consolidation of real estate companies will again play an important rolein 2016.”

“Alternative funding sources (insurance companies, pension funds, debtfunds, mezzanine capital) will capture a relevant market share.”

Page 12

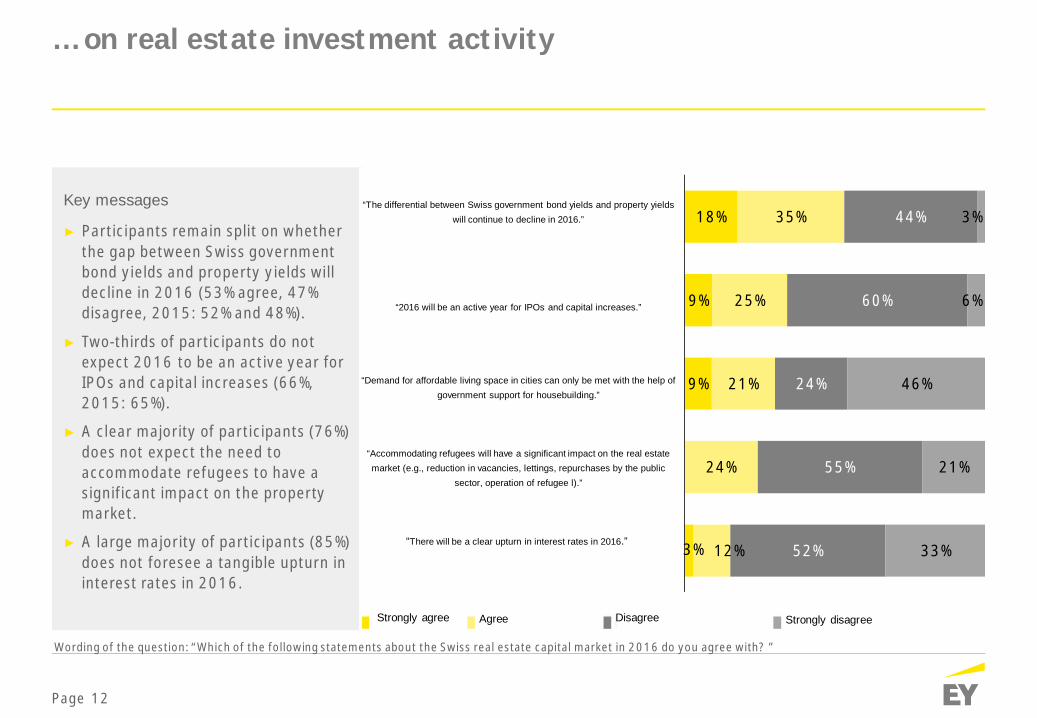

… on real estate investment activity

Wording of the question: “Which of the following statements about the Swiss real estate capital market in 2016 do you agree with? ”

18%

9%

9%

3%

35%

25%

21%

24%

12%

44%

60%

24%

55%

52%

3%

6%

46%

21%

33%

"Der Renditeabstand zwischen der Verzinsung vonSchweizer Staatsanleihen und Immobilienrenditen

nimmt 2016 weiter ab."

"2016 wird ein aktives Jahr für Börsengänge undKapitalerhöhungen."

"Die Nachfrage nach bezahlbarem Wohnraum inBallungsgebieten ist nur durch staatliche Förderung

zu decken."

"Die Unterbringung von Flüchtlingen hatwesentliche Auswirkungen auf die

Immobilienwirtschaft (z.B. Leerstandsabbau,Vermietung, Rückkauf durch öffentliche Hand,

Betreiben von Flüchtlingsheimen)."

"Im Jahr 2016 kommt eine spürbare Zinswende."

“The differential between Swiss government bond yields and property yieldswill continue to decline in 2016.”

“2016 will be an active year for IPOs and capital increases.”

“Demand for affordable living space in cities can only be met with the help ofgovernment support for housebuilding.”

“Accommodating refugees will have a significant impact on the real estatemarket (e.g., reduction in vacancies, lettings, repurchases by the public

sector, operation of refugee l).”

“There will be a clear upturn in interest rates in 2016.”

Strongly agree Agree Disagree Strongly disagree

Key messages

► Participants remain split on whetherthe gap between Swiss governmentbond yields and property yields willdecline in 2016 (53% agree, 47%disagree, 2015: 52% and 48%).

► Two-thirds of participants do notexpect 2016 to be an active year forIPOs and capital increases (66%,2015: 65%).

► A clear majority of participants (76%)does not expect the need toaccommodate refugees to have asignificant impact on the propertymarket.

► A large majority of participants (85%)does not foresee a tangible upturn ininterest rates in 2016.

Page 13

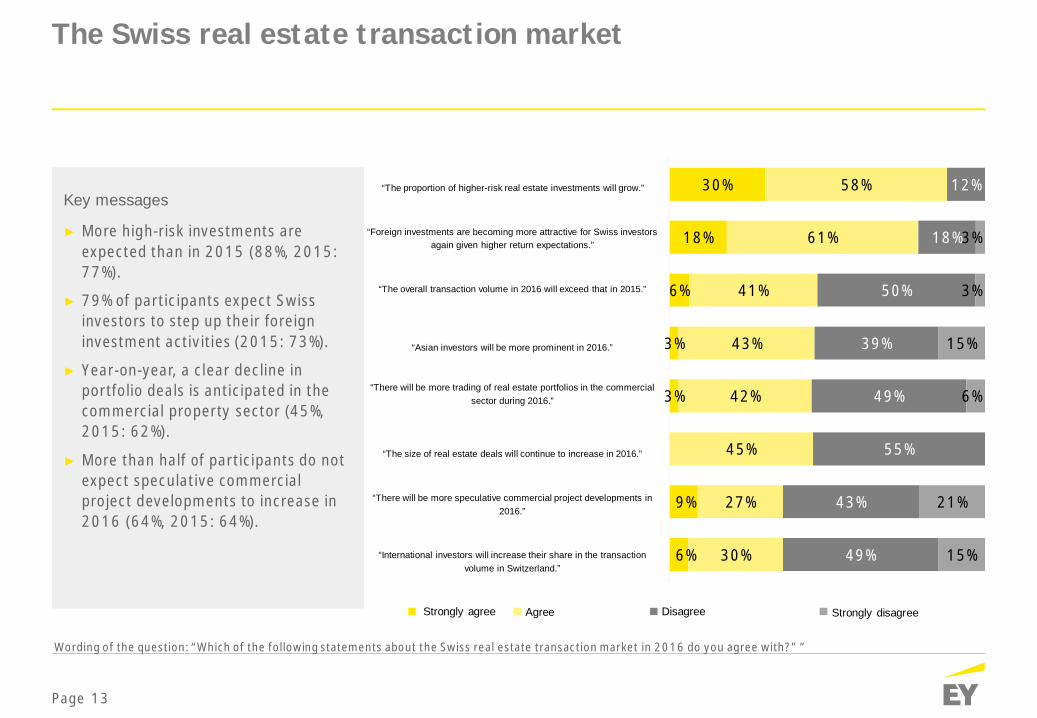

The Swiss real estate transaction market

Wording of the question: “Which of the following statements about the Swiss real estate transaction market in 2016 do you agree with?” ”

30%

18%

6%

3%

3%

9%

6%

58%

61%

41%

43%

42%

45%

27%

30%

12%

18%

50%

39%

49%

55%

43%

49%

3%

3%

15%

6%

21%

15%

"Der Anteil an risikoreicherer Immobilieninvestments wirdsteigen."

"Für Schweizer Anleger werden Investitionen im Auslandwegen höherer Renditeerwartungen wieder interessanter."

"Insgesamt wird das Transaktionsvolumen im Jahr 2016über dem Niveau von 2015 liegen."

"Asiatische Investoren werden 2016 vermehrt inErscheinung treten."

"Im Gewerbebereich werden im Jahr 2016Immobilienportfolios vermehrt gehandelt."

"Die Grösse der Immobiliendeals wird im Jahr 2016 weiterzunehmen."

"Spekulative gewerbliche Projektentwicklungen werden imJahr 2016 zunehmen."

"Internationale Investoren werden ihren Anteil amTransaktionsvolumen in Schweiz vergrössern."

“The proportion of higher-risk real estate investments will grow.”

“Foreign investments are becoming more attractive for Swiss investorsagain given higher return expectations.”

“The overall transaction volume in 2016 will exceed that in 2015.”

“Asian investors will be more prominent in 2016.”

“There will be more trading of real estate portfolios in the commercialsector during 2016.”

“The size of real estate deals will continue to increase in 2016.”

“There will be more speculative commercial project developments in2016.”

“International investors will increase their share in the transactionvolume in Switzerland.”

Key messages

► More high-risk investments areexpected than in 2015 (88%, 2015:77%).

► 79% of participants expect Swissinvestors to step up their foreigninvestment activities (2015: 73%).

► Year-on-year, a clear decline inportfolio deals is anticipated in thecommercial property sector (45%,2015: 62%).

► More than half of participants do notexpect speculative commercialproject developments to increase in2016 (64%, 2015: 64%).

Strongly agree Agree Disagree Strongly disagree

Page 14

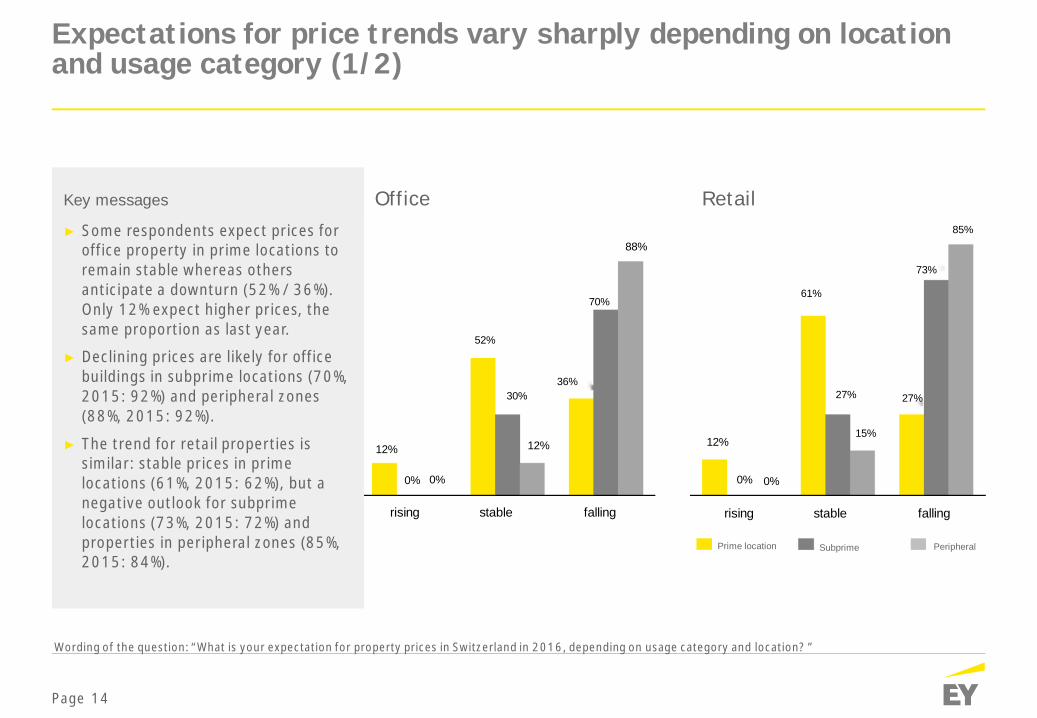

Expectations for price trends vary sharply depending on locationand usage category (1/2)

Wording of the question: “What is your expectation for property prices in Switzerland in 2016, depending on usage category and location? ”

Office Retail

SubprimePrime location Peripheral

Key messages

► Some respondents expect prices foroffice property in prime locations toremain stable whereas othersanticipate a downturn (52% / 36%).Only 12% expect higher prices, thesame proportion as last year.

► Declining prices are likely for officebuildings in subprime locations (70%,2015: 92%) and peripheral zones(88%, 2015: 92%).

► The trend for retail properties issimilar: stable prices in primelocations (61%, 2015: 62%), but anegative outlook for subprimelocations (73%, 2015: 72%) andproperties in peripheral zones (85%,2015: 84%).

12%

0%

52%

30%

12%

36%

70%

88%

rising stable falling

12%

0% 0%

61%

27%

15%

27%

73%

rising stable falling

Prime location Subprime Peripheral

85%

0%

Page 15

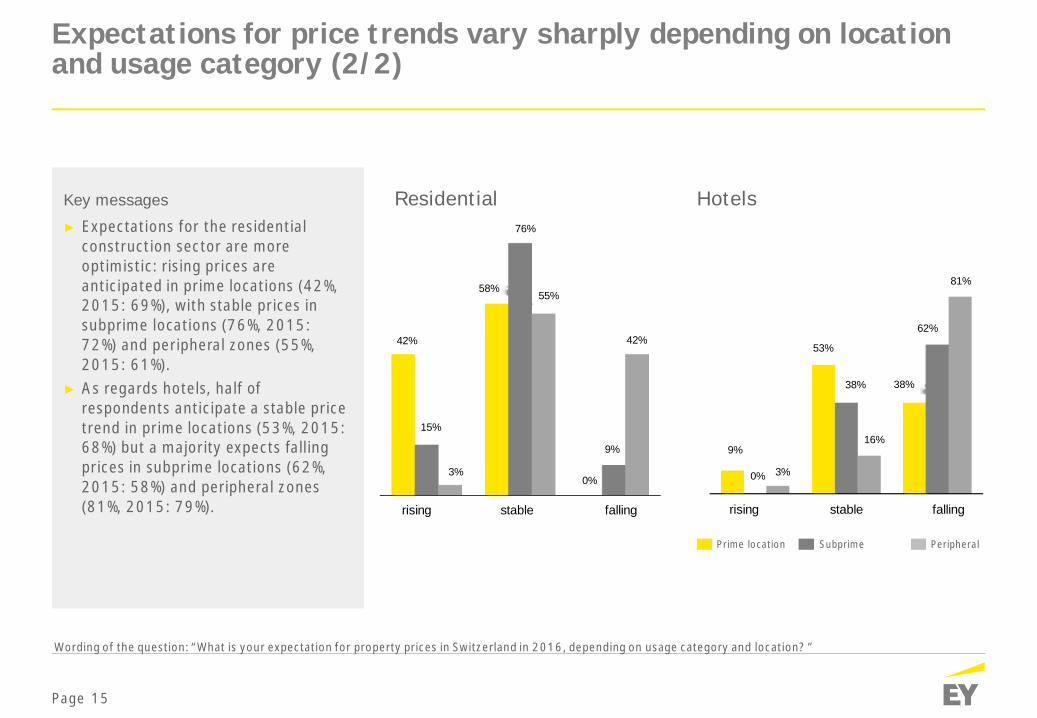

Expectations for price trends vary sharply depending on locationand usage category (2/2)

Wording of the question: “What is your expectation for property prices in Switzerland in 2016, depending on usage category and location? ”

ResidentialKey messages

► Expectations for the residentialconstruction sector are moreoptimistic: rising prices areanticipated in prime locations (42%,2015: 69%), with stable prices insubprime locations (76%, 2015:72%) and peripheral zones (55%,2015: 61%).

► As regards hotels, half ofrespondents anticipate a stable pricetrend in prime locations (53%, 2015:68%) but a majority expects fallingprices in subprime locations (62%,2015: 58%) and peripheral zones(81%, 2015: 79%).

Hotels

SubprimePrime location Peripheral

42%

15%

3%

58%

76%

55%

0%

9%

42%

rising stable falling rising stable falling

9%

0% 3%

53%

38%

16%

38%

62%

81%

Page 16

30%

27%

22%

22%

21%

15%

15%

12%

6%

3%

55%

49%

53%

38%

55%

52%

46%

33%

33%

52%

15%

24%

25%

40%

24%

33%

39%

55%

61%

45%

Opportunity-/PE-Fonds

Sonstige internationale Fonds

Immobilien-AGs/REITs

Versicherungen/Pensionsfonds

Banken

Corporates (Non-Property)

Offene Fonds

Wohnungsgesellschaften

Öffentliche Hand

Geschlossene Fonds

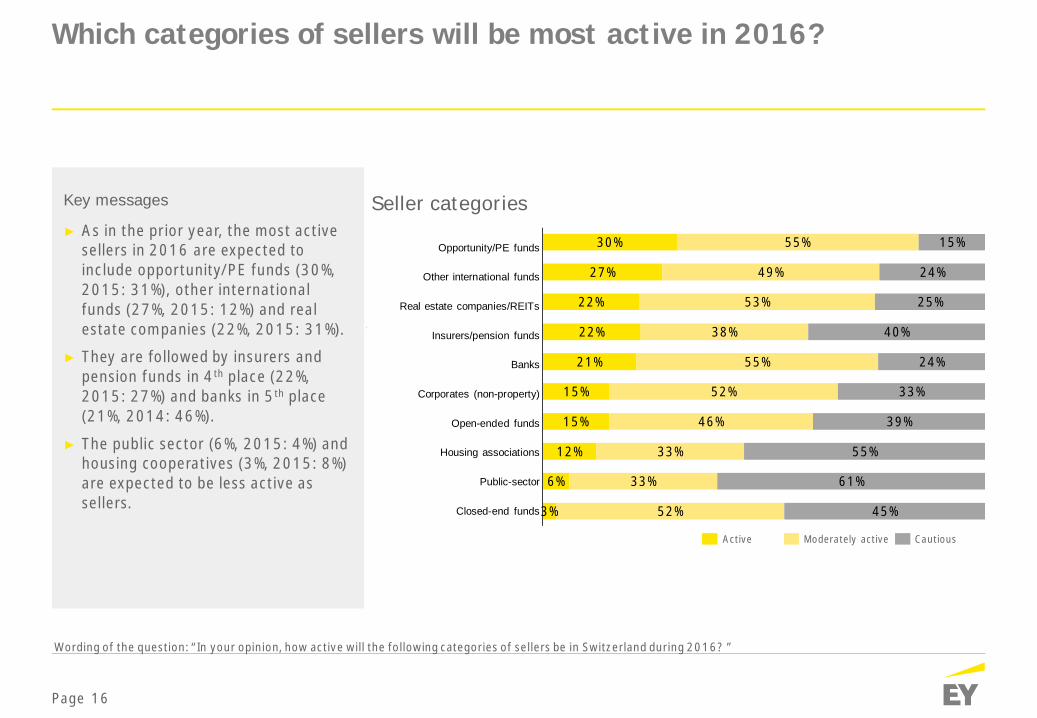

Which categories of sellers will be most active in 2016?

Wording of the question: “In your opinion, how active will the following categories of sellers be in Switzerland during 2016? ”

Seller categories

Active Moderately active Cautious

Key messages

► As in the prior year, the most activesellers in 2016 are expected toinclude opportunity/PE funds (30%,2015: 31%), other internationalfunds (27%, 2015: 12%) and realestate companies (22%, 2015: 31%).

► They are followed by insurers andpension funds in 4th place (22%,2015: 27%) and banks in 5th place(21%, 2014: 46%).

► The public sector (6%, 2015: 4%) andhousing cooperatives (3%, 2015: 8%)are expected to be less active assellers.

Opportunity/PE funds

Other international funds

Real estate companies/REITs

Insurers/pension funds

Banks

Corporates (non-property)

Open-ended funds

Housing associations

Public-sector

Closed-end funds

Page 17

73%

55%

44%

43%

36%

30%

24%

24%

21%

15%

9%

27%

30%

31%

39%

55%

37%

58%

40%

46%

52%

52%

15%

25%

18%

9%

33%

18%

36%

33%

33%

39%

Versicherungen/Pensionsfonds

Privat/Family Offices

Immobilien-AGs/REITs

Wohnungsgesellschaften

Offene Fonds

Opportunity-/PE-Fonds

Geschlossene Fonds

Sonstige internationale Fonds

Banken

Staatsfonds

Öffentliche Hand

Insurers/pension funds

Private/family offices

Real estate companies/REITs

Housing associations

Open-ended funds

Opportunity/PE funds

Closed-end funds

Other international funds

Banks

Sovereign wealth funds

Public sector

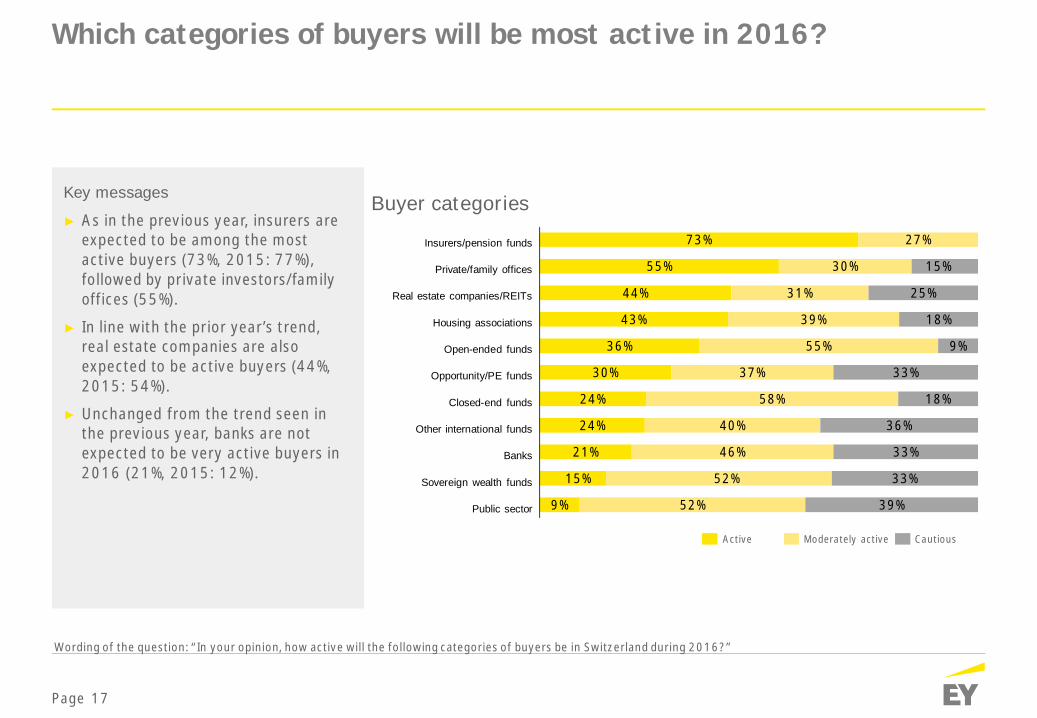

Which categories of buyers will be most active in 2016?

Wording of the question: “In your opinion, how active will the following categories of buyers be in Switzerland during 2016?”

Buyer categories

Active Moderately active Cautious

Key messages

► As in the previous year, insurers areexpected to be among the mostactive buyers (73%, 2015: 77%),followed by private investors/familyoffices (55%).

► In line with the prior year’s trend,real estate companies are alsoexpected to be active buyers (44%,2015: 54%).

► Unchanged from the trend seen inthe previous year, banks are notexpected to be very active buyers in2016 (21%, 2015: 12%).

Page 18

67%

9%

3%

6%

33%

40%

30%

15%

30%

55%

55%

21%

12%

24%

Abweichende Kaufpreisvorstellungen zwischenKäufer und Verkäufer

Höhe des erforderlichen Eigenkapitals

Mangelnde Verfügbarkeit von nachrangigenKreditfinanzierungen (Junior)

Verfügbarkeit von erstrangigenKreditfinanzierungen (Senior)

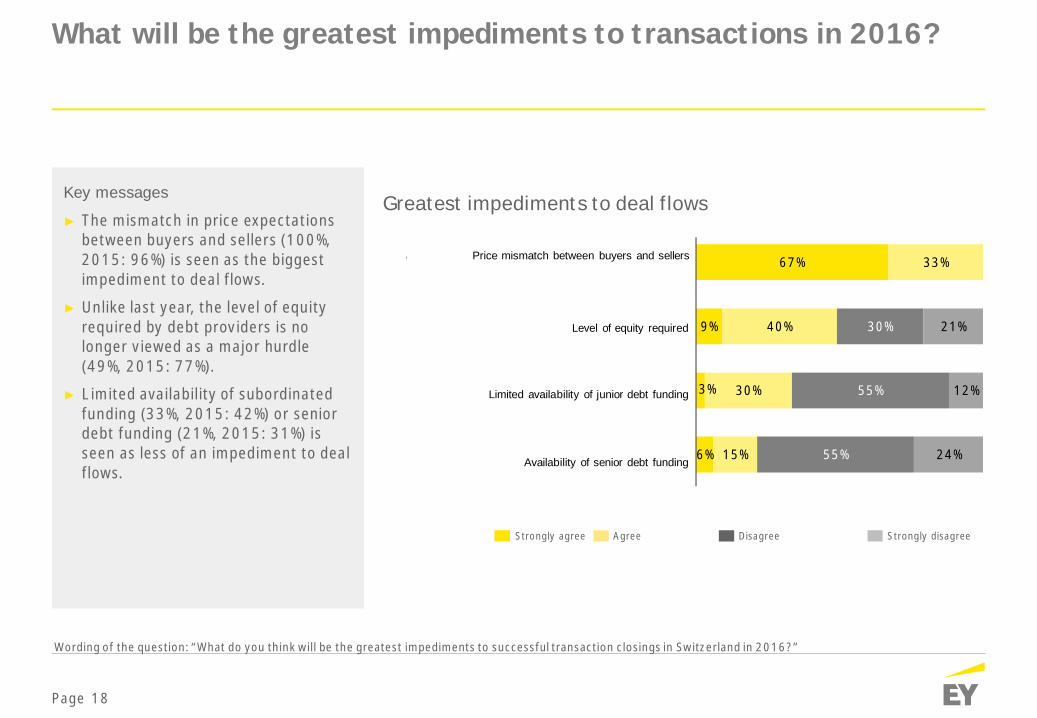

What will be the greatest impediments to transactions in 2016?

Wording of the question: “What do you think will be the greatest impediments to successful transaction closings in Switzerland in 2016?”

Greatest impediments to deal flows

Strongly agree Agree Disagree Strongly disagree

Key messages

► The mismatch in price expectationsbetween buyers and sellers (100%,2015: 96%) is seen as the biggestimpediment to deal flows.

► Unlike last year, the level of equityrequired by debt providers is nolonger viewed as a major hurdle(49%, 2015: 77%).

► Limited availability of subordinatedfunding (33%, 2015: 42%) or seniordebt funding (21%, 2015: 31%) isseen as less of an impediment to dealflows.

Price mismatch between buyers and sellers

Level of equity required

Limited availability of junior debt funding

Availability of senior debt funding

Page 19

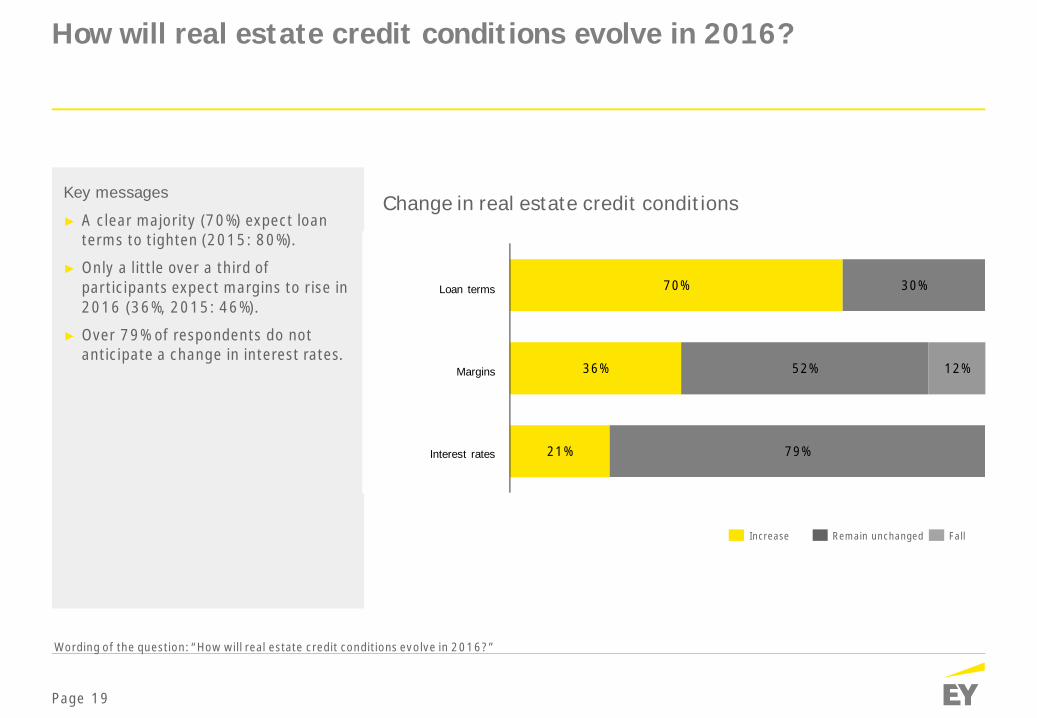

How will real estate credit conditions evolve in 2016?

Wording of the question: “How will real estate credit conditions evolve in 2016?”

Change in real estate credit conditions

Interest rates

LTV

Margin

Loan term

Increase Remain unchanged Fall

70%

36%

21%

30%

52%

79%

12%

Kreditanforderungen

Marge

Zins

Key messages

► A clear majority (70%) expect loanterms to tighten (2015: 80%).

► Only a little over a third ofparticipants expect margins to rise in2016 (36%, 2015: 46%).

► Over 79% of respondents do notanticipate a change in interest rates.

Loan terms

Margins

Interest rates

Page 20

18%

16%

9%

3%

58%

59%

46%

39%

36%

36%

18%

22%

39%

55%

61%

52%

6%

3%

6%

3%

3%

12%

Consensual restructuring

Extension of repayment period

Changing asset managers

Sale of loans

Debt-for-equity swaps

Repossessions

Banks’ approach to non-performing loans

Wording of the question: “What in your view will be the main ways banks in Switzerland deal with non-performing loans in 2016?”

Approaches to dealing with non-performing loans

Strongly agree Agree Disagree Strongly disagree

Key messages

► As in the prior year, consensualrestructuring deals (76%, 2015:88%) and prolongation of therepayment period (75%, 2015: 65%)are seen as the best approaches todealing with non-performing loans.

► Only a little over a third ofparticipants expect banks to dealwith non-performing loans throughrepossessions (36%, 2015: 31%).

Page 21

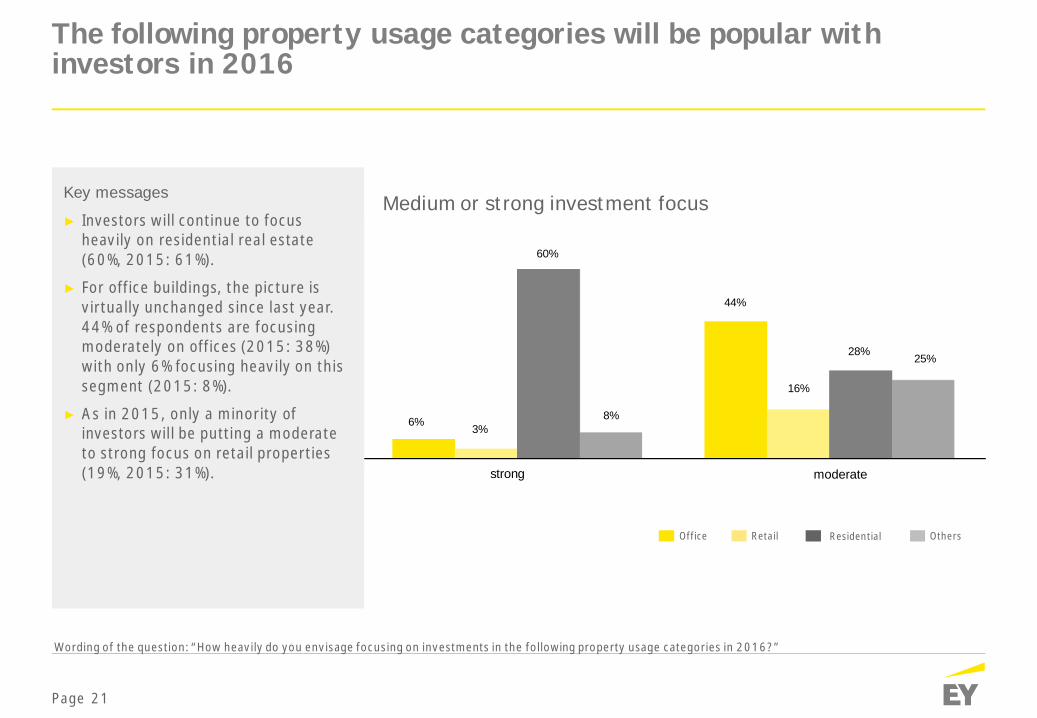

The following property usage categories will be popular withinvestors in 2016

Wording of the question: “How heavily do you envisage focusing on investments in the following property usage categories in 2016?”

Medium or strong investment focus

Retail Residential OthersOffice

Key messages

► Investors will continue to focusheavily on residential real estate(60%, 2015: 61%).

► For office buildings, the picture isvirtually unchanged since last year.44% of respondents are focusingmoderately on offices (2015: 38%)with only 6% focusing heavily on thissegment (2015: 8%).

► As in 2015, only a minority ofinvestors will be putting a moderateto strong focus on retail properties(19%, 2015: 31%).

6% 3%

60%

8%

44%

16%

28% 25%

strong moderate

Page 22

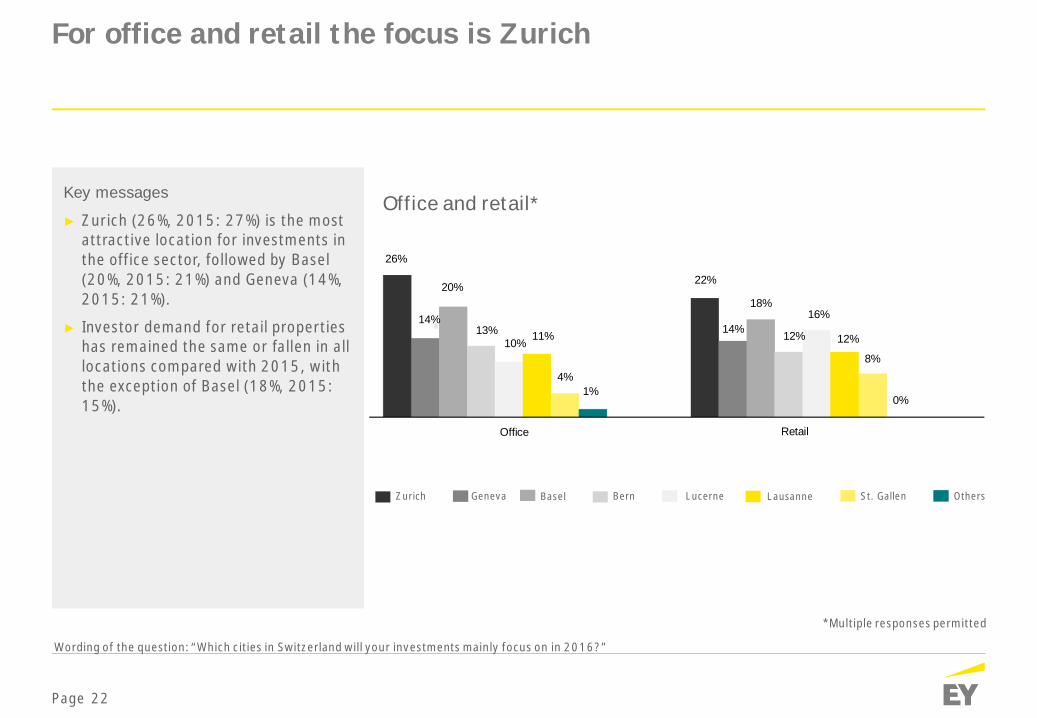

For office and retail the focus is Zurich

Wording of the question: “Which cities in Switzerland will your investments mainly focus on in 2016?”

Office and retail*

*Multiple responses permitted

Key messages

► Zurich (26%, 2015: 27%) is the mostattractive location for investments inthe office sector, followed by Basel(20%, 2015: 21%) and Geneva (14%,2015: 21%).

► Investor demand for retail propertieshas remained the same or fallen in alllocations compared with 2015, withthe exception of Basel (18%, 2015:15%).

Zurich LausanneGeneva St. GallenBasel Bern Lucerne Others

26%

14%

20%

13%10% 11%

4%1%

22%

14%

18%

12%

16%

12%

8%

0%

Office Retail

Page 23

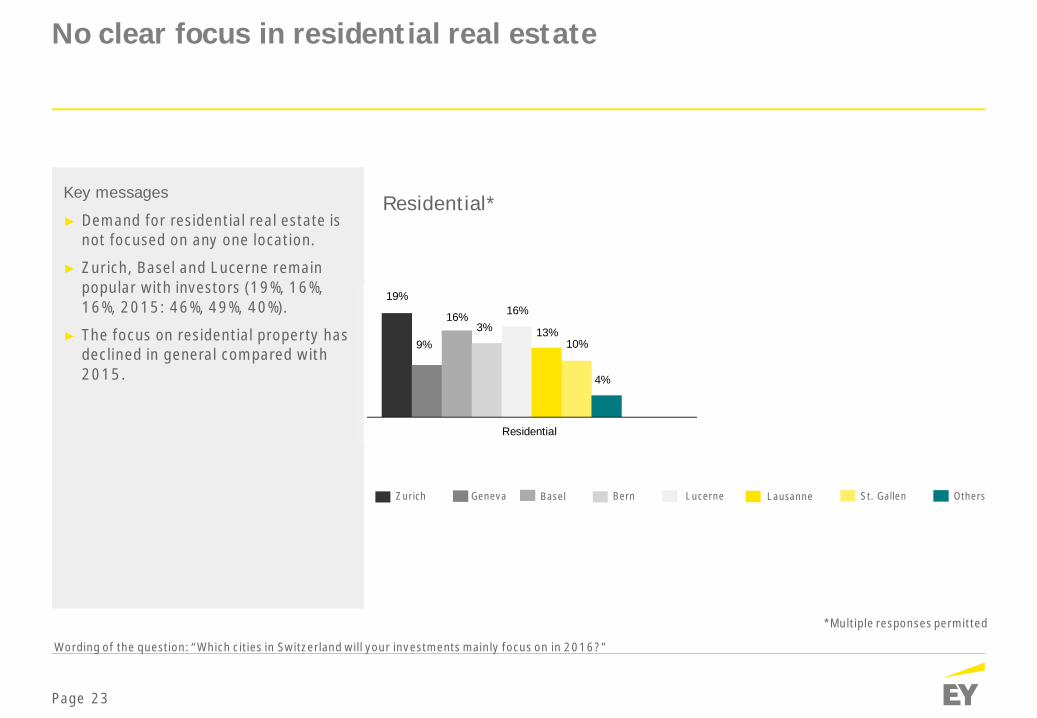

No clear focus in residential real estate

Wording of the question: “Which cities in Switzerland will your investments mainly focus on in 2016?”

Residential*

*Multiple responses permitted

Key messages

► Demand for residential real estate isnot focused on any one location.

► Zurich, Basel and Lucerne remainpopular with investors (19%, 16%,16%, 2015: 46%, 49%, 40%).

► The focus on residential property hasdeclined in general compared with2015.

Zurich LausanneGeneva St. GallenBasel Bern Lucerne Others

19%

9%

16%3%

16%

13%10%

4%

Residential

Page 24

Most attractive exit options for real estate investments in 2016

Wording of the question: “Which exit strategies do you envisage in 2016?”

Potential exit strategies*

*Multiple responses permitted

Key messages

► Most respondents (77%) do notenvisage an exit; if at all, a directsale as a single asset appears to bethe preferred option in 2016 (37%).

► Strategies such as direct sales ofportfolios (13%) and special funds(3%) will be less significant exitoptions.

37%

13%

3%

10%

3% 0%

77%

Direct sale —single asset

Direct sale —portfolio

Special funds Real estatecomps./REITs

(IPOs)

Mutual fund Closed-endfunds

No exit

Page 25

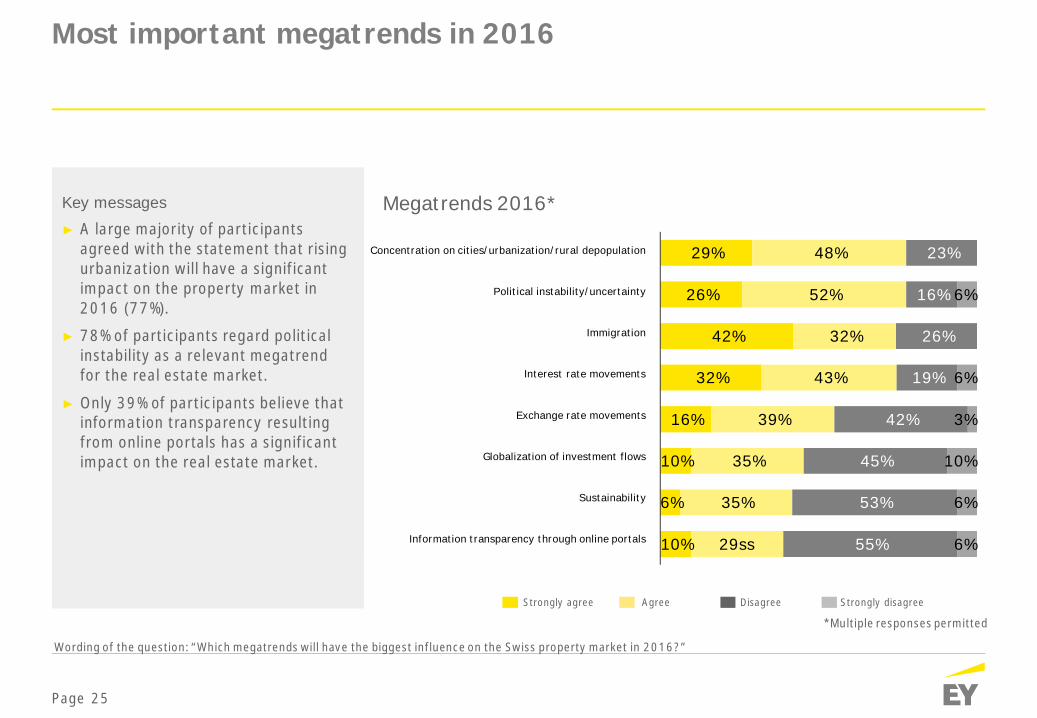

Key messages

► A large majority of participantsagreed with the statement that risingurbanization will have a significantimpact on the property market in2016 (77%).

► 78% of participants regard politicalinstability as a relevant megatrendfor the real estate market.

► Only 39% of participants believe thatinformation transparency resultingfrom online portals has a significantimpact on the real estate market.

Most important megatrends in 2016

Wording of the question: “Which megatrends will have the biggest influence on the Swiss property market in 2016?”

Megatrends 2016*

*Multiple responses permitted

29%

26%

42%

32%

16%

10%

6%

10%

48%

52%

32%

43%

39%

35%

35%

29ss

23%

16%

26%

19%

42%

45%

53%

55%

6%

6%

3%

10%

6%

6%

Konzentration auf Grossstädte/Urbanisierung/Landflucht

Politische Instabilitäten/Unsicherheiten

Zuwanderung

Zinsentwicklung

Wechselkursentwicklung

Globalisierung der Investitionsströme

Nachhaltigkeit

Informationstransparenz durch Onlineportale

Concentration on cities/urbanization/rural depopulation

Political instability/uncertainty

Immigration

Interest rate movements

Exchange rate movements

Globalization of investment flows

Sustainability

Information transparency through online portals

Strongly agree Agree Disagree Strongly disagree

Page 26

12%

88%

24%

40%

24%

12%

49%

45%

6%

Wording of the question: “What will be the leading trends in the residential category in 2016?”

“Prices forcondominiums

have reached their peakfor the time being.”

“Government regulationof rents is a good idea.”

94% 0%

64%

Strongly agree Agree Disagree Strongly disagree

Residential trends:

“The regulation ofimmigration is havingan adverse impact on

rental increases”

12%

52%

30%

6%

“Furnished apartments(e.g., micro and student

apartments) areemerging as an attractive

investment product.”

64%

Page 27

76%

24%

67%

33%

30%

52%

18%27%

61%

12%

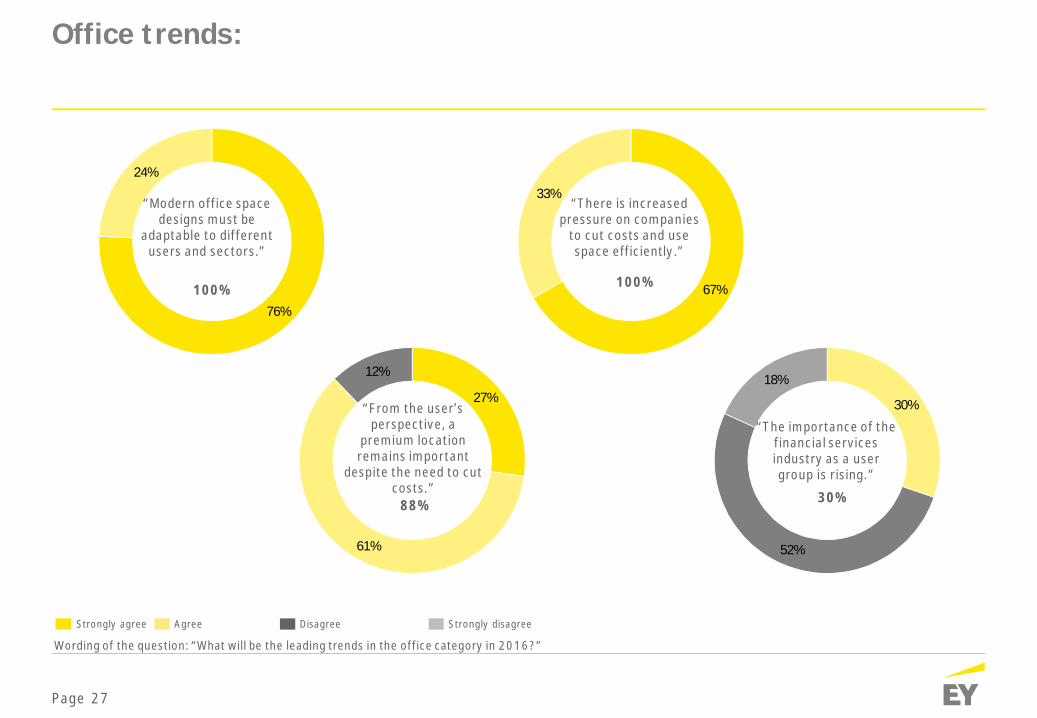

Wording of the question: “What will be the leading trends in the office category in 2016?”

“There is increasedpressure on companies

to cut costs and usespace efficiently.”

100%

“From the user’sperspective, a

premium locationremains important

despite the need to cutcosts.”

88%

“Modern office spacedesigns must be

adaptable to differentusers and sectors.”

100%

“The importance of thefinancial servicesindustry as a usergroup is rising.”

30%

Office trends:

Strongly agree Agree Disagree Strongly disagree

Page 28

3%

29%

58%

10%23%

45%

19%

13%

16%

65%

19%

63%

31%

6%

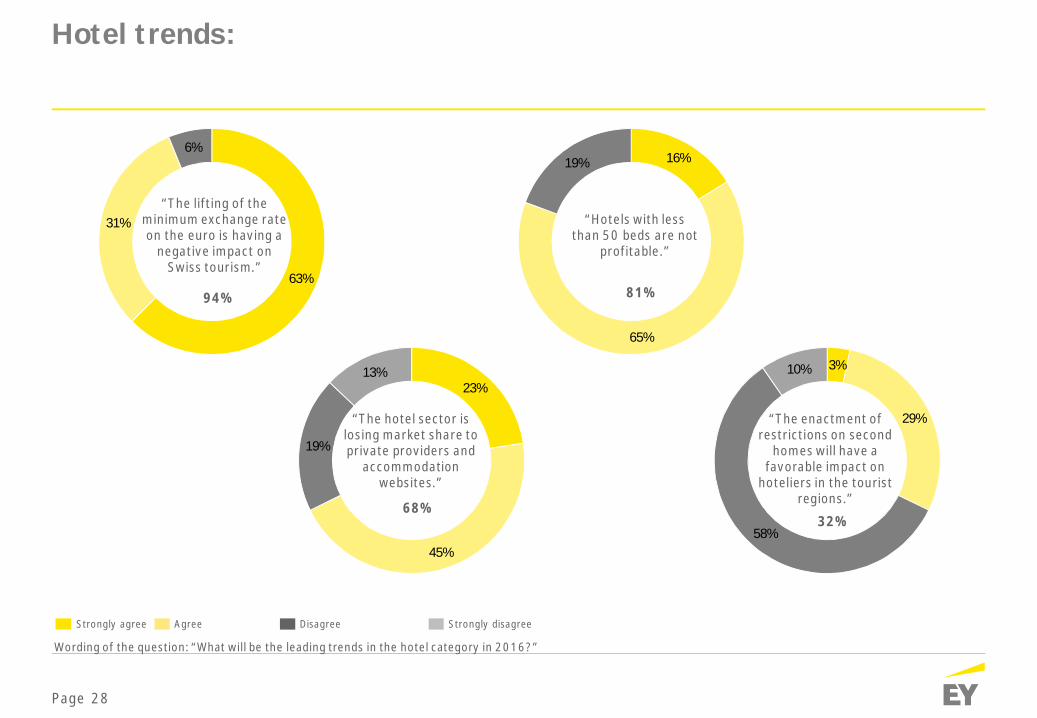

Wording of the question: “What will be the leading trends in the hotel category in 2016?”

“The lifting of theminimum exchange rateon the euro is having a

negative impact onSwiss tourism.”

94%

“The hotel sector islosing market share toprivate providers and

accommodationwebsites.”

68%

“Hotels with lessthan 50 beds are not

profitable.”

81%

“The enactment ofrestrictions on second

homes will have afavorable impact on

hoteliers in the touristregions.”

32%

Strongly agree Agree Disagree Strongly disagree

Hotel trends:

Page 29

“Temporary retailspace (pop-up shops)are becoming a more

attractiveproposition.”

9%

33%

49%

9%

36%

40%

18%

6%

64%

30%

6%

38%

49%

13%

Wording of the question: “What will be the leading trends in the retail category in 2016?”

“Online retailingremains a major

concern for traditionalbricks-and-mortar

retailing.”

94%

“The lifting of theminimum exchangerate on the euro ishaving a negativeimpact on buying

behavior inSwitzerland.”

76%

“Bricks-and-mortarretailing will be even

more focused onprime locations in

future.”

87%

“There is no future fordiscounters with low

sales square footage.”

42%

Retail trends:

Strongly agree Agree Disagree Strongly disagree

27%

55%

18%

82%

Key messagesSwitzerland 2016

Page 31

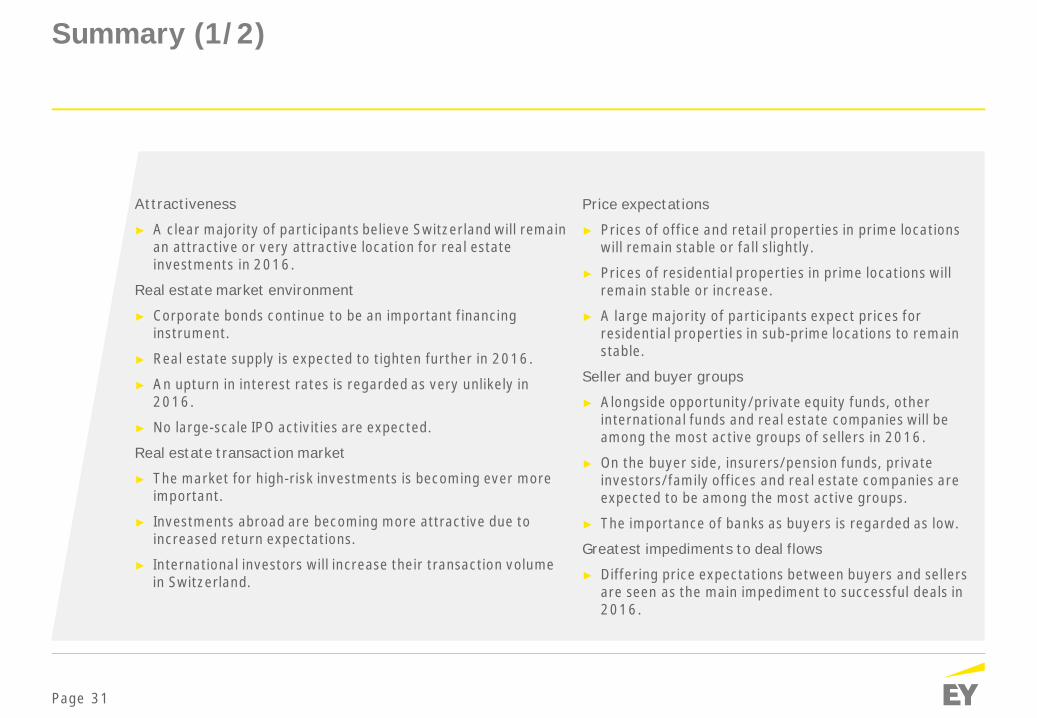

Attractiveness

► A clear majority of participants believe Switzerland will remainan attractive or very attractive location for real estateinvestments in 2016.

Real estate market environment

► Corporate bonds continue to be an important financinginstrument.

► Real estate supply is expected to tighten further in 2016.

► An upturn in interest rates is regarded as very unlikely in2016.

► No large-scale IPO activities are expected.

Real estate transaction market

► The market for high-risk investments is becoming ever moreimportant.

► Investments abroad are becoming more attractive due toincreased return expectations.

► International investors will increase their transaction volumein Switzerland.

Price expectations

► Prices of office and retail properties in prime locationswill remain stable or fall slightly.

► Prices of residential properties in prime locations willremain stable or increase.

► A large majority of participants expect prices forresidential properties in sub-prime locations to remainstable.

Seller and buyer groups

► Alongside opportunity/private equity funds, otherinternational funds and real estate companies will beamong the most active groups of sellers in 2016.

► On the buyer side, insurers/pension funds, privateinvestors/family offices and real estate companies areexpected to be among the most active groups.

► The importance of banks as buyers is regarded as low.

Greatest impediments to deal flows

► Differing price expectations between buyers and sellersare seen as the main impediment to successful deals in2016.

Summary (1/2)

Page 32

Real estate loan terms

► Real estate loan terms are expected to tighten.

► The interest rate level is likely to remain constant.

Banks’ approach to non-performing loans

► Consensual restructuring deals and prolongation of therepayment period are the most likely approach.

► It is highly unlikely that repossessions will become morefrequent.

Investment focus by usage category

► The spotlight will be on residential real estate in 2016.

► Demand for office properties will be moderate to low,depending on their location.

► Only a minority of participants stated that they would put theirinvestment focus on retail properties in 2016.

Preferred investment locations► Zurich, Basel and Geneva are popular destinations for

investments in office properties.► Demand for residential properties is highest in Zurich, Basel

and Lucerne.

Exit strategies► A majority of respondents consider that an exit in 2016 is

unattractive in general.► If at all, the direct sale of a single asset will be the most

significant exit strategy in 2016.

Top trends

► The participants agreed that urbanization and ruralpopulation flight will have a significant impact on theSwiss property market.

► Political instability and uncertainty are also regarded as arelevant megatrend.

► Regulation of immigration is seen as having a detrimentalimpact on rental increases.

► Government regulation of rents is not regarded as a goodidea.

► The pressure on companies to cut costs and use spaceefficiently will increase further.

Summary (2/2)

Page 33

Your contacts

Rolf BachExecutive Director

Ernst & Young AGMaagplatz 1P.O. BoxCH-8010 ZurichPhone +41 58 286 38 [email protected]

Natalie GischlerManager

Ernst & Young AGMaagplatz 1P.O. BoxCH-8010 ZurichPhone +41 58 286 86 [email protected]

Daniel Zaugg MRICSPartner

Ernst & Young AGMaagplatz 1P.O. BoxCH-8010 ZurichPhone +41 58 286 46 [email protected]

EY | Assurance | Tax | Transactions | Advisory

About the global EY organization

The global EY organization is a leader in assurance, tax, transaction, legaland advisory services. We leverage our experience, knowledge and servicesto help build trust and confidence in the financial markets and in economiesall over the world. We are ideally equipped for this task – with well trainedemployees, strong teams, excellent services and outstanding client relations.Our global mission is to drive progress and make a difference by building abetter working world – for our people, for our clients and for ourcommunities.

The global EY organization refers to all member firms of Ernst & Young GlobalLimited (EYG). Each EYG member firm is a separate legal entity and has noliability for another such entity’s acts or omissions. Ernst & Young GlobalLimited, a UK company limited by guarantee, does not provide services toclients. For more information, please visit www.ey.com.

EY’s organization is represented in Switzerland by Ernst & Young Ltd, Basel,with ten offices across Switzerland, and in Liechtenstein by Ernst & YoungAG, Vaduz. In this publication, «EY» and «we» refer to Ernst & Young Ltd,Basel, a member firm of Ernst & Young Global Limited.

© 2016Ernst & Young LtdAll Rights Reserved.

This publication contains information in summary form and is therefore intended for generalguidance only. Although prepared with utmost care this publication is not intended to be asubstitute for detailed research or professional advice. Therefore, by reading this publication, youagree that no liability for correctness, completeness and/or currentness will be assumed. It is solelythe responsibility of the readers to decide whether and in what form the information made availableis relevant for their purposes. Neither Ernst & Young Ltd nor any other member of the global EYorganization accepts any responsibility. On any specific matter, reference should be made to theappropriate advisor.

www.ey.com/ch