translational valley of death - milken institute · translational valley of death *includes $21b/yr...

TRANSCRIPT

Translational valley of death

*Includes $21B/yr from NIH academic grants (2011) and $1.3B/yr from medical research foundations (2009). **Includes $584M/yr from NIH SBIR (2011), $400M/yr from angel investors (2011), and $6B from VCs (2011). SOURCES: RESEARCH!AMERICA, NATIONAL INSTITUTES OF HEALTH, CB INSIGHTS, NATIONAL VENTURE CAPITAL ASSOCIATION, CENTER FOR VENTURE RESEARCH.

What problem are we trying to solve?

Insufficient capital applied to scientific development

Crossing the “valley of death” in translational medicine

Large inventory of unfunded biomedical assets

Bias to invest in incremental versus revolutionary innovation

Impatient capital, aversion to future-financing risk

Inefficient capital deployment

Limited investment opportunities for institutional investors

Lack of new cures/solutions to some major social priorities

2012 by Fernandez, Stein, and Lo, All Rights Reserved

Israel's life sciences industry Sectors & growth

Source: IATI data base 2013 ; ISTIP report, Caesarea forum, 2013

Medical Devices

60%

AGBiotech 2%

Health IT 8%

Service 1%

Other 1%

Biotechnology 18%

Pharmaceuticals 11%

A decade of growth 30% of Life Sciences companies operating in Israel were established in the last 5 years 39% of companies are generating revenue, majority are Medical Device ~ 200 therapeutics in clinical stages

Impact reflecting the potential

Product (Company) Indication Sales 2012

(M$)

Academic

Institute

Humira (AbbVie/Eisai) RA 9,380 WIS

Enbrel (Amgen) RA 8,370 WIS

Copaxone (Teva) MS 3,996 WIS

Rebif (Merck Serono) MS 2,400 WIS

Erbitux (BMS & Eli Lilly) CRC 1,800 WIS

Avonex (Biogen) MS 1,570 WIS

Exelon (Novartis) AD 1,000 HUJI

Doxil* (J&J) Cancer 500 HUJI

Azilect (Teva) Parkinson 330 Technion

Total 29,346

Developed in Israel 6,726

Medical Device

Developed & Produced in Israel

2012 sales: $3,485M

Invented in Israel Bio-Pharma Blockbusters

“ISRAEL INSIDE”

$24.6 billion of the 2012 global biotech industry's turnover of $120 billion is based on products originated in Israeli research

Israeli products account for 1% of the $350 billion global medical devices turnover

Globes 2013, Ruth Alon, general partner, Pitango VC

World Leadership in # of Granted Patents per Capita

Rapid growth in Life sciences R&D Companies

Global Success and Positioning ; Blockbuster Products in the Market (Copaxon, Rrbif, Erbitux, Doxil, Azilect, Exelon)

Strategic partnership with leading global companies: Merck KGA, Medtronic, Abbot, Boston Scientific, J&J, GE, Roche, St. Jude, Covidient, Takeda, Sanofi, Genentech

The industry drivers

High level and productive Academia – Basic & Applied

Strong Entrepreneurial spirit – serial entrepreneurs

Technology convergence and interdisciplinary

Human Capital – available, high level and qualified

World Largest VC availability per capita, investing 26% in Life Sciences

Government incentives – leverage the private sector in a risk related proportion (28% of budget for Life Sciences)

The Industry hurdles – Sustainable LS industry

However…. Fragmented Industry, Insufficient capital, lack of Business models and managerial expertise, 80% of companies has less than 25 employees, Limited Industrial Development, Early exit business strategy

Financial Infrastructure - Life Sciences $2220M Fund - JV Israeli government and private sector

(PPP). In addition to OCS grants, and syndicates

Strategic Partners - Global Pharma investment in seed companies (directly & via Incubator) ; Global

BioMed R&D centers

R&D Infrastructures - LS and Stem cell service R&D ; Tissue Bank

New Funding rout for applied and translational research in the academia

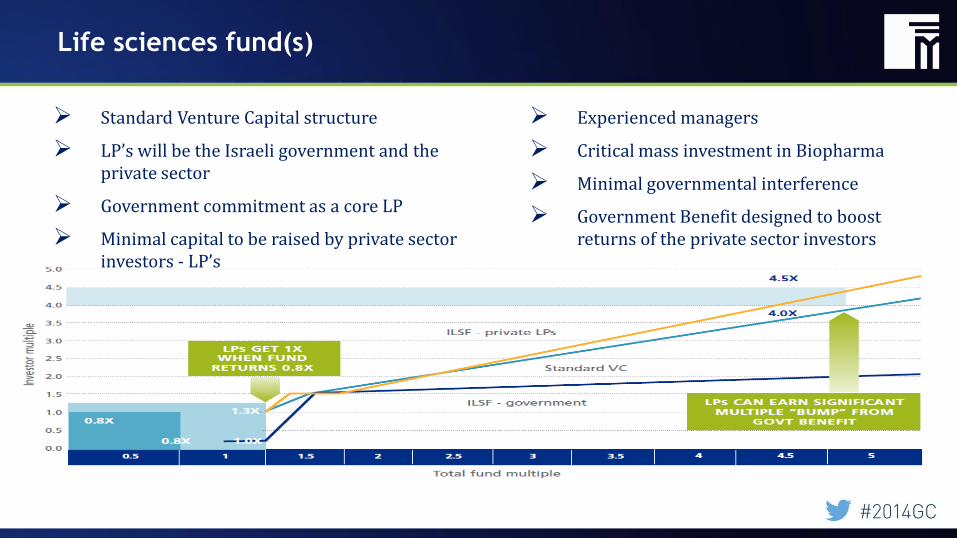

Life sciences fund(s)

Standard Venture Capital structure

LP’s will be the Israeli government and the private sector

Government commitment as a core LP

Minimal capital to be raised by private sector investors - LP’s

Experienced managers

Critical mass investment in Biopharma

Minimal governmental interference

Government Benefit designed to boost returns of the private sector investors

Changing healthcare landscape

Open innovation and collaboration increases probability of success

Deeper understanding of disease biology and new drug targets

No one company can work in isolation across all points in value chain

Closer interaction between academia, industry and government

Productive and capital efficient model to expedite innovation

Sharing or “No Rights” of intellectual property is increasingly common

Integrative approach to deliver “outcomes-based” medicines

Shift from pharmaceutical provider to healthcare solutions provider Innovation + integration will deliver superior therapeutic solutions

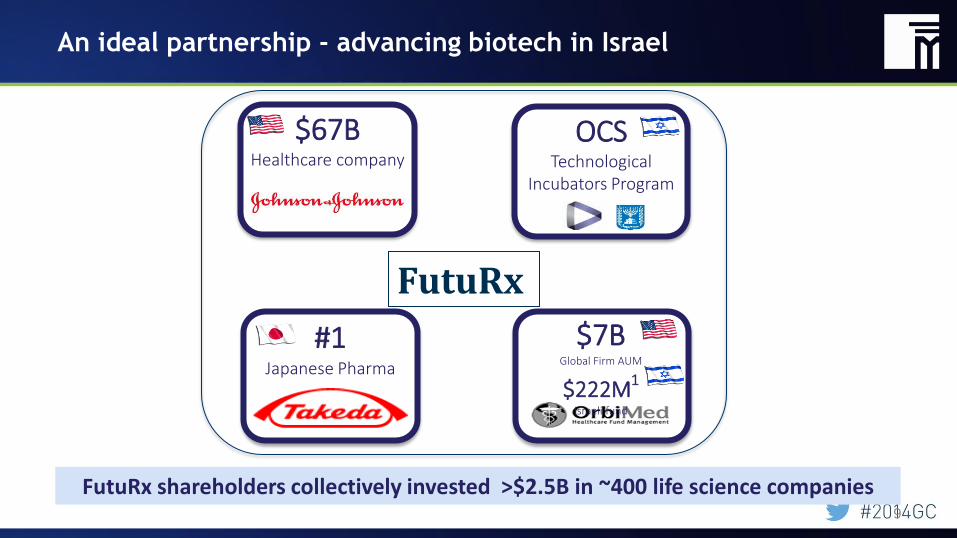

FutuRx is positioned to transform this challenge into an opportunity

$7B Global Firm AUM

$222M1 Israeli fund

#1 Japanese Pharma

$67B Healthcare company

An ideal partnership - advancing biotech in Israel

9

OCS Technological

Incubators Program

FutuRx shareholders collectively invested >$2.5B in ~400 life science companies

FutuRx

Sustainable Life Sciences Industry

NEXT

PPPP Bio-Fund ?!

Public Private Philanthropy Partnership

P4

ROGER STEIN

12

Can Financial Engineering Cure Cancer? David E. Fagnan, Jose-Maria Fernandez, Austin A. Gromatzky, Roger M. Stein and Andrew W. Lo (please see references for author affiliations)

13

DISCLAIMER

The views expressed here are my own and do not

represent the views of current or former employers

or any of their affiliates. Accordingly, these companies

and their affiliates expressly disclaim all responsibility

for the content and information contained herein.

A bit of stylized graphical “notation”...

© 2013 by Fagnan, Fernandez, Stein, and Lo All Rights Reserved

MIT LFE

Phase II

WD/Sold

Phase III

WD/Sold

Approved

WD/Sold

WD/Sold

Phase I

We can characterize the approval process compactly using

transition probabilities

15

© 2013 by Fagnan, Fernandez, Stein, and Lo All Rights Reserved MIT LFE

Describe the probability of moving from one state to another over a fixed period of time

Derived from historical data, expert judgement or a mixture of both

Simulating a drug state evolution (e.g., currently in Phase II)

16

© 2013 by Fagnan, Fernandez, Stein, and Lo All Rights Reserved

MIT LFE

Phase II Phase III

NDA WithdrawalSemester=12 Semester=13

Simulating a drug state evolution (e.g., currently in Phase II

Phase III)

17

© 2013 by Fagnan, Fernandez, Stein, and Lo All Rights Reserved

MIT LFE

Semester=13 Semester=14

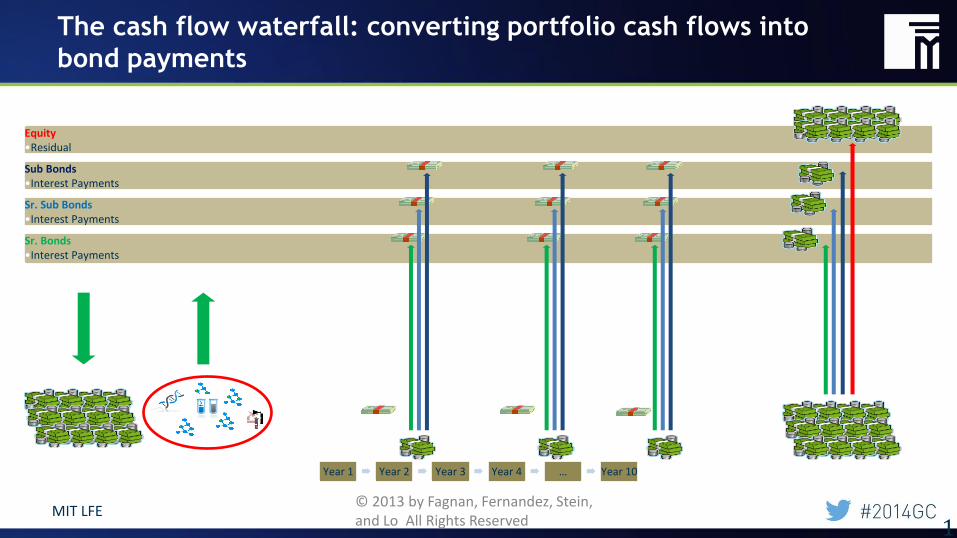

Create a “megafund” to finance drug trials

The cash flow waterfall: converting portfolio cash flows into

bond payments

19

© 2013 by Fagnan, Fernandez, Stein, and Lo All Rights Reserved

MIT LFE

Year 1 Year 2 Year 3 Year 4 … Year 10

Equity •Residual

Sub Bonds •Interest Payments

Sr. Sub Bonds •Interest Payments

Sr. Bonds •Interest Payments

Results, assumptions and source code are all freely available

20

Fernandez, JM, Stein, RM and Lo, AW (2012), “Commercializing biomedical research through securitization techniques”, Nature Biotech. Fagnan, D., Fernandez, JM, Stein, RM and Lo, AW (2013), “Can Financial Engineering Cure Cancer?”, American Economic Review. Fagnan, D., Gromatzky, AA, Fernandez, J-M, Stein, RM., Lo, AW. Financing drug discovery for orphan diseases Drug Discovery Today.

www.CancerRx.mit.edu

HAIM BITTERMAN

The changing paradigm of healthcare systems

Increasing costs threaten healthcare systems

Scientific and technological breakthroughs augment healthcare sustainability:

Advancement in informatics, diagnostics & personalized medicine lead to more efficient data-driven decision making and novel

intervention models

Emphasis on prevention of chronic medical conditions

Profound change in the traditional doctor-patient relationship (e.g. task shifts, team work, continuity of care, tele-care)

Proliferation of new financial and operational models

More then ever before, the sustainability (quality, safety and costs) of healthcare systems depends on an

effective innovation environment

The healthcare system as a catalyst for innovation

Traditional Model –

linear innovation process (Research – Development - Market) –

Healthcare system as a receptor of innovation.

Alternative Model –

Healthcare system as a catalyst for innovation.

Clalit Health Services:

52% Market Share (>4M members)

Ethnic and socio-economic diversity

Overrepresentation of chronic diseases (75% of diabetics)

2000 community clinics, 30% of general hospital beds, 40K employees

Electronic information (a single uniform EMR) since the 1990’s

Experience in predictive modelling, data-driven decision making, and

implementation of novel interventions in a “real life” environment.

Partner with us in our current initiatives

Our strategic goal is to position

as a leading

innovation center

To utilize 4.2M patients,

40K employees, unique data

infrastructure & culture

to boost healthcare Innovation

For more info: [email protected] [email protected]