transition to ifrs - valeo.com · the accounting standards (ias/ifrs)(1) published by the iasb...

TRANSCRIPT

TRANSITION TO IFRS

2

CONTENTS Pages

1 – INT R O DU CT ION 3

2 – AC C O U NTIN G POL IC I E S A D O PT ED 3

3 – F RE N C H G A A P / IFR S R E CO N C IL IAT I O N S 4

3 .1 – C hang es i n c ons o l i da te d s t oc kho l de r s ’ equ i t y be twe en Jan ua r y 1 , 2 004 a nd De ce mbe r 31 , 2004 4

3 .2 – S t a t em en t o f i n co me fo r the y ea r e nded D ec em ber 3 1 , 200 4 5

3 .3 – Ba l an ce s hee t a t De ce mbe r 31 , 2 004 8

3 .4 – D es cr i p t i o n o f IF R S re s t a t em en ts 12

3 .5 – D es cr i p t i o n o f IF R S re c l as s i f i ca t i o ns 16

3 .6 – Ma i n i mpa c ts o f IF RS r es ta te men t s on t he s ta te men t o f cas h f l o ws 18

4 – R EC O N CIL IAT ION OF Q U ART ERL Y F IG U RES AT M AR C H 31 , 20 04 19

5 – IM PACT OF ADO PT IO N OF IF R S ON F IN AN C IAL IN ST R U M ENTS AT J AN U AR Y 1 , 2005 22

5 .1 – Im pa c t on s t oc kho l de r s ’ equ i t y 22

5 .2 – Im pa c t on n e t d eb t 23

6 – ST ATUT O R Y AU D IT O RS ’ SPECIAL R EPO RT O N TH E 2004 CO N SOL IDATED F IN AN C IAL ST AT EMENT S REST AT ED IN ACCORDANCE W ITH IFRS 24

(1) Standards published from June 2003 onwards are known as International Financial Reporting Standards (IFRS). Previously-published standards continue to be known as International Accounting Standards (IAS)

3

1 – INTRODUCTION The European Union has decided to adopt the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB). Under EC regulation 1606/2002 of July 19, 2002, companies listed on a regulated stock exchange in one of the member states are required to present their consolidated financial statements for

financial years beginning on or after January 1, 2005 in conformity with IFRS. Valeo, which up to and including 2004 applied French generally accepted accounting principles (French GAAP), is subject to this requirement. As a result, Valeo is required to prepare its consolidated financial statements in conformity with IFRS with effect from the year ending December 31, 2005. Comparative figures for the year ended December 31, 2004 are also required under IFRS. In order to be able to publish these comparatives, Valeo prepared an opening balance sheet at January 1, 2004, which constitutes the starting point for the application of IFRS. The quantitative impacts of the transition to IFRS at January 1, 2004 which, in line with IFRS 1 “First-time Adoption of International Financial Reporting Standards” were recorded in equity, were disclosed in the Management Report for the year ended December 31, 2004. The next phase, which is described in this document, is the publication of reconciliations between the French GAAP financial statements and the IFRS financial statements. These reconciliations, accompanied by explanatory notes, set out the impact of the transition to IFRS on:

• changes in consolidated stockholders’ equity between January 1 and December 31, 2004;

• the income statement for the year ended December 31, 2004;

• the balance sheet at December 31, 2004. A description of the main impacts of IFRS restatements on the statement of cash flows is also provided. Given that the impact of the transition to IFRS on the financial statements for the year ended December 31, 2004 has been validated by the Audit Committee and the statutory auditors (see note 6), Valeo has decided (as announced in the 2004 Management Report) to publish this information simultaneously with figures for the first quarter of 2005 (the first set of 2005 interim results prepared under IFRS). Consequently, a reconciliation of quarterly data at March 31, 2004 is also included in this document (see note 4),

so as to show how the comparatives for the first quarter of 2004 accompanying the 2005 first-quarter figures were prepared. Finally, this document also presents the impact on Valeo’s equity and net debt of the first-time adoption as of January 1, 2005 of IAS 32 and IAS 39 on financial instruments (see note 5).

2 – ACCOUNTING POLICIES ADOPTED The accounting policies applied by Valeo in preparing its first IFRS financial statements comply with the International Financial Reporting Standards as adopted by the European Union. The accounting standards (IAS/IFRS)(1) published by the IASB (International Accounting Standards Board) as at December 31, 2004, have been approved by the European

Union, except for some parts of IAS 39, “Financial Instruments: Recognition and Measurement” which have no material impact on Valeo. Because the 2004 comparative information published with the 2005 consolidated statements must be prepared on the basis of standards applicable at December 31, 2005, Valeo may have to amend the information contained in this document to reflect changes to IFRS and the approval of such changes by the European Commission. In preparing its opening balance sheet at January 1, 2004, Valeo applied the principles relating to first-time adoption as defined in IFRS 1. The IFRSs that are in force were generally applied retrospectively, as though Valeo had always applied them. However, IFRS 1 does explicitly allow a number of exemptions to retrospective application:

• Mandatory exemptions: for example, IFRS 1 requires estimates under IFRSs at the date of transition to be consistent with estimates made at the same date under previous GAAP (i.e. it prohibits the use of hindsight to correct estimates made under previous GAAP). Also, IFRS 1 requires prospective application of hedge accounting as from the first period of application of IAS 9, “Financial Instruments: Recognition and Measurement”.

• Optional exemptions: Valeo has elected not to restate the following retrospectively:

- business combinations recognized before

January 1, 2004 (IFRS 3);

- pensions and other employee benefits (IAS 19), resulting in the resetting to zero at January 1, 2004 of cumulative actuarial gains or losses previously unrecognized under French GAAP;

- translation of the accounts of foreign entities

(IAS 21), resulting in the elimination of the cumulative translation adjustment at January 1, 2004 (with no impact on total equity);

- in addition, restatement under the first-time adoption requirements set out in IFRS 1 in relation to IFRS 2 (“Share-Based Payment”), has been limited to equity instruments granted after November 7, 2002 (date of publication of the exposure draft of IFRS 2) and not fully vested on January 1, 2005.

Given the delay by the European Union in approving IAS 32 and IAS 39 on financial instruments in 2004, Valeo has elected to apply these standards only with effect from January 1, 2005, with the resulting impact recorded in equity at said date.

4

3 – FRENCH GAAP/IFRS RECONCILIATIONS

3.1 – Changes in consolidated stockholders’ equity between January 1 and December 31, 2004

The table below shows a reconciliation of movements in consolidated stockholders’ equity under French GAAP and under IFRS:

( million) Notes Jan. 1, 2004

Dividend paid

Equalization tax

Share issue

Other movements

Translation adjustment

2004 net income

Dec. 31, 2004

Stockholders’ equity – French GAAP 2,112 (94) (101) 33 (297) 10 181 1,844

Pensions and other employee benefits 3.4.1 (245) - - - 245 - - -

Development expenditure 3.4.2 148 - - - (1) - 29 176

Specific tooling 3.4.3 (53) - - - (2) - 3 (52)

Consolidation methods 3.4.4 (35) 2 - - 2 - (27) (58)

Currency translation 3.4.5 (25) - - - 2 (5) - (28)

Impairment of assets 3.4.6 (19) - - - (1) - 74 54

Business combinations 3.4.7 (16) - - - (8) - - (24)

Share-based payment 3.4.8 - - - - 5 - (7) (2)

Other adjustments 3.4.9 (14) - - - 2 - (2) (14)

Deferred taxes 3.4.10 (3) - - - (4) - (2) (9)

Stockholders’ equity – IFRS 1,850 (92) (101) 33 (57) 5 249 1,887

Minority interests 97 (7) - - (38) (3) 8 57

Total excluding minority interests 1,753 (85) (101) 33 (19) 8 241 1,830

5

3.2 – 2004 statement of income Adjustments to the statement of income arising from first-time adoption of IFRS have been split into two categories, each described in a separate set of explanatory notes:

• restatements, which have an impact on consolidated net income; • reclassifications, which only impact the way in which items are classified within the statement of income.

( mill ion) 2004

French GAAP

IFRS

restatements

IFRS

reclassifications

Total IFRS

impact

2004

IFRS

Notes 3.4 3.5

NET SALES 9,439 (197) (13) (210) 9,229

Other operating revenues (1) - 15 49 64 64

TOTAL OPERATING REVENUES 9,439 (182) 36 (146) 9,293

Cost of sales (7,771) 154 (14) 140 (7,631)

GROSS MARGIN (2) 1,668 (43) (27) (70) 1,598

% of net sales 17.7% 17.3%

Research & development expenditure (584) 24 (43) (19) (603)

Selling expenses (187) 2 (1) 1 (186)

Administrative expenses (439) 2 (7) (5) (444)

Other income and expenses (1) - (18) (78) (96) (96)

OPERATING INCOME 458 (18) (107) (125) 333

% of total operating revenues 4.9% 3.6%

Net financial expense (3) (31) - 31 31 -

Cost of net debt (1) - (1) (32) (33) (33)

Other financial income and expense (1) - 1 (40) (39) (39)

Other income/expense – net (3) (148) - 148 148 -

INCOME BEFORE INCOME TAXES 279 (18) - (18) 261

Income taxes (15) (2) - (2) (17)

NET INCOME FROM CONSOLIDATED COMPANIES 264 (20) - (20) 244

Equity in net earnings of associated companies 7 (2) - (2) 5

Amortization of goodwill (3) (90) 90 - 90 -

NET INCOME BEFORE MINORITY INTERESTS 181 68 - 68 249

% of total operating revenues 1.9% - - - 2.7%

Minority interests (31) 23 - 23 (8)

NET INCOME 150 91 - 91 241

% of total operating revenues 1.6% 2.6%

Basic earnings per share (in ) 3.4.11 1.83 2.93

Diluted earnings per share (in ) 3.4.11 1.82 2.93

(1) New line in the IFRS statement of income

(2) Gross Margin is the difference between Net sales and Cost of sales, and does not include Other operating revenues (3) Line no longer included in the IFRS statement of income

6

3.2.1 – Details of restatements to the statement of income

( mill ion) Development

expenditure

Specific

tooling

Consolidation

methods

Impairment of

assets

Share-based

payment

Other

restatements

Deferred

taxes

Total IFRS

restatements

Notes 3.4.2 3.4.3 3.4.4 3.4.6 3.4.8 3.4.9 3.4.10

NET SALES (2) 1 (199) - - 3 - (197)

Other operating revenues (1) 15 - - - - - - 15

TOTAL OPERATING REVENUES 13 1 (199) - - 3 - (182)

Cost of sales - 2 155 (1) (2) - - 154

GROSS MARGIN (2) (2) 3 (44) (1) (2) 3 - (43)

Research & development expenditure 16 - 10 - (1) (1) - 24

Selling expenses - - 2 - - - - 2

Administrative expenses - - 7 - (4) (1) - 2

Other income and expenses (1) - - - (15) - (3) - (18)

OPERATING INCOME 29 3 (25) (16) (7) (2) - (18)

Net financial expense (3) - - - - - - - -

Cost of net debt (1) - - - - - (1) - (1)

Other financial income and expense (1) - - - - - 1 - 1

Other income/expenses – net (3) - - - - - - - -

INCOME BEFORE INCOME TAXES 29 3 (25) (16) (7) (2) - (18)

Income taxes - - - - - - (2) (2)

NET INCOME FROM CONSOLIDATED COMPANIES

29 3 (25) (16) (7) (2) (2) (20)

Equity in net earnings of associated

companies - - (2) - - - - (2)

Amortization of goodwill (3) - - - 90 - - - 90

NET INCOME BEFORE MINORITY

INTERESTS 29 3 (27) 74 (7) (2) (2) 68

Minority interests - - 27 - - (1) (3) 23

NET INCOME 29 3 - 74 (7) (3) (5) 91

(1) New line in the IFRS statement of income

( 2 ) Gross Margin is the difference between Net sales and Cost of sales, and does not include Other operating revenues

(3) Line no longer included in the IFRS statement of income

7

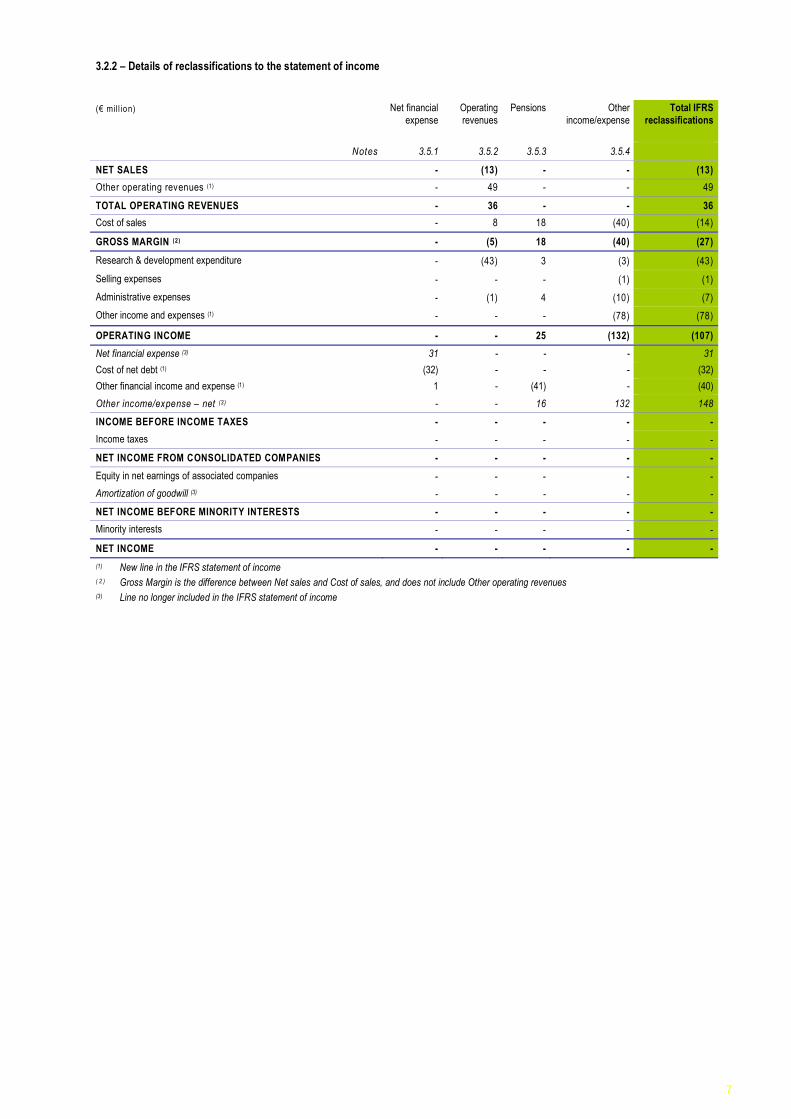

3.2.2 – Details of reclassifications to the statement of income

( mill ion) Net financial

expense

Operating

revenues

Pensions Other

income/expense

Total IFRS

reclassifications

Notes 3.5.1 3.5.2 3.5.3 3.5.4

NET SALES - (13) - - (13)

Other operating revenues (1) - 49 - - 49

TOTAL OPERATING REVENUES - 36 - - 36

Cost of sales - 8 18 (40) (14)

GROSS MARGIN (2) - (5) 18 (40) (27)

Research & development expenditure - (43) 3 (3) (43)

Selling expenses - - - (1) (1)

Administrative expenses - (1) 4 (10) (7)

Other income and expenses (1) - - - (78) (78)

OPERATING INCOME - - 25 (132) (107)

Net financial expense (3) 31 - - - 31

Cost of net debt (1) (32) - - - (32)

Other financial income and expense (1) 1 - (41) - (40)

Other income/expense – net (3) - - 16 132 148

INCOME BEFORE INCOME TAXES - - - - -

Income taxes - - - - -

NET INCOME FROM CONSOLIDATED COMPANIES - - - - -

Equity in net earnings of associated companies - - - - -

Amortization of goodwill (3) - - - - -

NET INCOME BEFORE MINORITY INTERESTS - - - - -

Minority interests - - - - -

NET INCOME - - - - -

(1) New line in the IFRS statement of income

( 2 ) Gross Margin is the difference between Net sales and Cost of sales, and does not include Other operating revenues

(3) Line no longer included in the IFRS statement of income

8

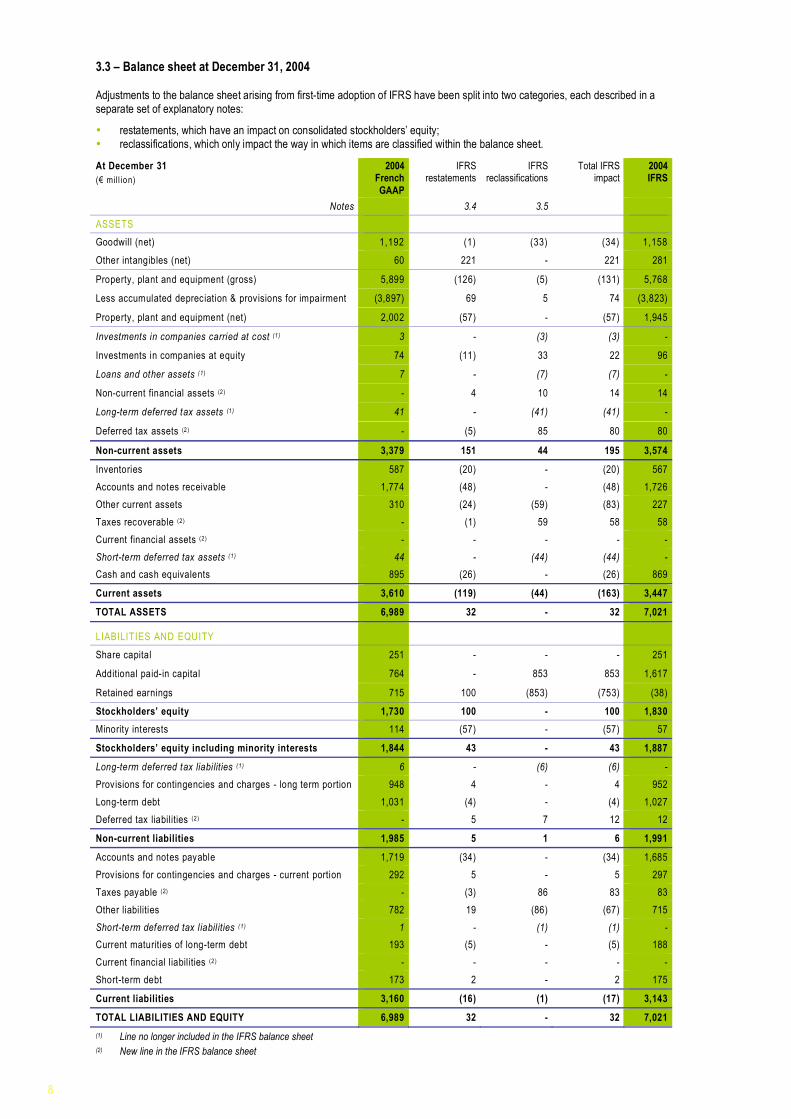

3.3 – Balance sheet at December 31, 2004 Adjustments to the balance sheet arising from first-time adoption of IFRS have been split into two categories, each described in a separate set of explanatory notes:

• restatements, which have an impact on consolidated stockholders’ equity; • reclassifications, which only impact the way in which items are classified within the balance sheet.

At December 31

( mill ion)

2004 French

GAAP

IFRS restatements

IFRS reclassifications

Total IFRS impact

2004 IFRS

Notes 3.4 3.5

ASSETS

Goodwill (net) 1,192 (1) (33) (34) 1,158

Other intangibles (net) 60 221 - 221 281

Property, plant and equipment (gross) 5,899 (126) (5) (131) 5,768

Less accumulated depreciation & provisions for impairment (3,897) 69 5 74 (3,823)

Property, plant and equipment (net) 2,002 (57) - (57) 1,945

Investments in companies carried at cost (1) 3 - (3) (3) -

Investments in companies at equity 74 (11) 33 22 96

Loans and other assets (1) 7 - (7) (7) -

Non-current financial assets (2) - 4 10 14 14

Long-term deferred tax assets (1) 41 - (41) (41) -

Deferred tax assets (2) - (5) 85 80 80

Non-current assets 3,379 151 44 195 3,574

Inventories 587 (20) - (20) 567

Accounts and notes receivable 1,774 (48) - (48) 1,726

Other current assets 310 (24) (59) (83) 227

Taxes recoverable (2) - (1) 59 58 58

Current financial assets (2) - - - - -

Short-term deferred tax assets (1) 44 - (44) (44) -

Cash and cash equivalents 895 (26) - (26) 869

Current assets 3,610 (119) (44) (163) 3,447

TOTAL ASSETS 6,989 32 - 32 7,021

LIABILITIES AND EQUITY

Share capital 251 - - - 251

Additional paid-in capital 764 - 853 853 1,617

Retained earnings 715 100 (853) (753) (38)

Stockholders’ equity 1,730 100 - 100 1,830

Minority interests 114 (57) - (57) 57

Stockholders’ equity including minority interests 1,844 43 - 43 1,887

Long-term deferred tax liabilities (1) 6 - (6) (6) -

Provisions for contingencies and charges - long term portion 948 4 - 4 952

Long-term debt 1,031 (4) - (4) 1,027

Deferred tax liabilities (2) - 5 7 12 12

Non-current liabilities 1,985 5 1 6 1,991

Accounts and notes payable 1,719 (34) - (34) 1,685

Provisions for contingencies and charges - current portion 292 5 - 5 297

Taxes payable (2) - (3) 86 83 83

Other liabilities 782 19 (86) (67) 715

Short-term deferred tax liabilities (1) 1 - (1) (1) -

Current maturities of long-term debt 193 (5) - (5) 188

Current financial l iabilities (2) - - - - -

Short-term debt 173 2 - 2 175

Current liabilities 3,160 (16) (1) (17) 3,143

TOTAL LIABILITIES AND EQUITY 6,989 32 - 32 7,021

(1) Line no longer included in the IFRS balance sheet (2) New line in the IFRS balance sheet

9

3.3.1 – Details of restatements to the balance sheet

At December 31

( mill ion)

Development

expenditure

Specific

tooling

Consolidation

methods

Currency

translation

Impairment

of assets

Sub-total IFRS

Restatements

Notes 3.4.2 3.4.3 3.4.4 3.4.5 3.4.6

ASSETS

Goodwill (net) (5) - - (27) 56 24

Other intangibles (net) 223 - (2) - - 221

Property, plant and equipment (gross) - (37) (105) (12) - (154)

Less accumulated depreciation & provisions for impairment - 15 63 11 (2) 87

Property, plant and equipment (net) - (22) (42) (1) (2) (67)

Investments in companies carried at cost (1) - - - - - -

Investments in companies at equity - - (10) - - (10)

Loans and other assets (1) - - - - - -

Non-current financial assets (2) - - 4 - - 4

Long-term deferred tax assets (1) - - - - - -

Deferred tax assets (2) - - - - - -

Non-current assets 218 (22) (50) (28) 54 172

Inventories - (8) (13) - - (21)

Accounts and notes receivable - (1) (46) - - (47)

Other current assets (1) (15) (7) - - (23)

Taxes recoverable (2) - - (1) - - (1)

Current financial assets (2) - - - - - -

Short-term deferred tax assets (1) - - - - - -

Cash and cash equivalents - - (26) - - (26)

Current assets (1) (24) (93) - - (118)

TOTAL ASSETS 217 (46) (143) (28) 54 54

LIABILITIES AND EQUITY

Share capital - - - - - -

Additional paid-in capital - - - - - -

Retained earnings 176 (52) - (28) 54 150

Stockholders’ equity 176 (52) - (28) 54 150

Minority interests - - (58) - - (58)

Stockholders’ equity including minority interests 176 (52) (58) (28) 54 92

Long-term deferred tax liabilities (1) - - - - - -

Provisions for contingencies and charges - long term portion - 2 (6) - - (4)

Long-term debt - - (8) - - (8)

Deferred tax liabilities (2) - - - - - -

Non-current liabilities - 2 (14) - - (12)

Accounts and notes payable (1) 5 (39) - - (35)

Provisions for contingencies and charges - current portion - 10 (7) - - 3

Taxes payable (2) - - (2) - - (2)

Other liabilities 42 (11) (15) - - 16

Short-term deferred tax liabilities (1) - - - - - -

Current maturities of long-term debt - - (10) - - (10)

Current financial l iabilities (2) - - - - - -

Short-term debt - - 2 - - 2

Current liabilities 41 4 (71) - - (26)

TOTAL LIABILITIES AND EQUITY 217 (46) (143) (28) 54 54

(1) Line no longer included in the IFRS balance sheet

(2) New line in the IFRS balance sheet.

10

At December 31

( mill ion)

Sub-total IFRS

Restatements

Business

combinations

Share-based

payment

Other

restatements

Deferred

taxes

Total IFRS

Restatements

Notes 3.4.7 3.4.8 3.4.9 3.4.10

ASSETS

Goodwill (net) 24 (24) - (1) - (1)

Other intangibles (net) 221 - - - - 221

Property, plant and equipment (gross) (154) - - 28 - (126)

Less accumulated depreciation & provisions for impairment 87 - - (18) - 69

Property, plant and equipment (net) (67) - - 10 - (57)

Investments in companies carried at cost (1) - - - - - -

Investments in companies at equity (10) - - (1) - (11)

Loans and other assets (1) - - - - - -

Non-current financial assets (2) 4 - - - - 4

Long-term deferred tax assets (1) - - - - - -

Deferred tax assets (2) - - - - (5) (5)

Non-current assets 172 (24) - 8 (5) 151

Inventories (21) - - 1 - (20)

Accounts and notes receivable (47) - - (1) - (48)

Other current assets (23) - - (1) - (24)

Taxes recoverable (2) (1) - - - - (1)

Current financial assets (2) - - - - - -

Short-term deferred tax assets (1) - - - - - -

Cash and cash equivalents (26) - - - - (26)

Current assets (118) - - (1) - (119)

TOTAL ASSETS 54 (24) - 7 (5) 32

LIABILITIES AND EQUITY

Share capital - - - - - -

Additional paid-in capital - - - - - -

Retained earnings 150 (24) (2) (15) (9) 100

Stockholders’ equity 150 (24) (2) (15) (9) 100

Minority interests (58) - - 1 - (57)

Stockholders’ equity including minority interests 92 (24) (2) (14) (9) 43

Long-term deferred tax liabilities (1) - - - - - -

Provisions for contingencies and charges - long term portion (4) - - 8 - 4

Long-term debt (8) - - 4 - (4)

Deferred tax liabilities (2) - - - 1 4 5

Non-current liabilities (12) - - 13 4 5

Accounts and notes payable (35) - - 1 - (34)

Provisions for contingencies and charges - current portion 3 - - 2 - 5

Taxes payable (2) (2) - - (1) - (3)

Other liabilities 16 - 2 1 - 19

Short-term deferred tax liabilities (1) - - - - - -

Current maturities of long-term debt (10) - - 5 - (5)

Current financial l iabilities (2) - - - - - -

Short-term debt 2 - - - - 2

Current liabilities (26) - 2 8 - (16)

TOTAL LIABILITIES AND EQUITY 54 (24) - 7 (5) 32

(1) Line no longer included in the IFRS balance sheet (2) New line in the IFRS balance sheet

11

3.3.2 – Details of reclassifications to the balance sheet

At December 31

( mill ion)

Income taxes

Financial assets & liabilities

Business combinations

Other reclassifications

Total IFRS Reclassifications

Notes 3.5.6 3.5.7 3.5.8 3.4.9

ASSETS

Goodwill (net) - - (33) - (33)

Other intangibles (net) - - - - -

Property, plant and equipment (gross) - - - (5) (5)

Less accumulated depreciation & provisions for impairment - - - 5 5

Property, plant and equipment (net) - - - - -

Investments in companies carried at cost (1) - (3) - - (3)

Investments in companies at equity - - 33 - 33

Loans and other assets (1) - (7) - - (7)

Non-current financial assets (2) - 10 - - 10

Long-term deferred tax assets (1) (41) - - - (41)

Deferred tax assets (2) 85 - - - 85

Non-current assets 44 - - - 44

Inventories - - - - -

Accounts and notes receivable - - - - -

Other current assets (59) - - - (59)

Taxes recoverable (2) 59 - - - 59

Current financial assets (2) - - - - -

Short-term deferred tax assets (1) (44) - - - (44)

Cash and cash equivalents - - - -

Current assets (44) - - - (44)

TOTAL ASSETS - - - - -

LIABILITIES AND EQUITY

Share capital - - - - -

Additional paid-in capital - - 853 - 853

Retained earnings - - (853) - (853)

Stockholders’ equity - - - - -

Minority interests - - - - -

Stockholders’ equity including minority interests - - - - -

Long-term deferred tax liabilities (1) (6) - - - (6)

Provisions for contingencies and charges - long term portion - - - - -

Long-term debt - - - - -

Deferred tax liabilities (2) 7 - - - 7

Non-current liabilities 1 - - - 1

Accounts and notes payable - - - - -

Provisions for contingencies and charges - current portion - - - - -

Taxes payable (2) 86 - - - 86

Other liabilities (86) - - - (86)

Short-term deferred tax liabilities (1) (1) - - - (1)

Current maturities of long-term debt - - - - -

Current financial l iabilities (2) - - - - -

Short-term debt - - - - -

Current liabilities (1) - - - (1)

TOTAL LIABILITIES AND EQUITY - - - - -

(1) Line no longer included in the IFRS balance sheet (2) New line in the IFRS balance sheet

12

3.4 - Description of IFRS restatements 3.4.1 – Pensions and other employee benefits

Valeo’s obligations in respect of pensions and other employee benefits falling within the scope of IAS 19 consist of: • post-employment benefits, including statutory retirement

benefits, supplementary pension benefits and coverage of some medical costs for retirees and early retirees;

• other long-term benefits payable during employment, mainly long-service bonuses.

These benefits fall into two categories: • defined contribution plans: the employer pays fixed

contributions on a regular basis and has no legal or constructive obligation to pay further contributions;

• defined benefit plans: the employer guarantees a future level of benefits. Valeo measured its obligation in respect of defined benefit plans in accordance with IAS 19, and provided for this obligation in full at January 1, 2004.

The impact of 245 million on opening equity includes:

• mainly, the resetting at zero (in accordance with IFRS 1 on first-time adoption) of the actuarial gains and losses recognized at December 31, 2003 under French GAAP. These gains and losses usually arise from changes in actuarial assumptions or from experience adjustments

(the effects of differences between previous assumptions and what has actually occurred);

• secondarily, the effect of changing the method used to measure certain obligations, due to the fact that IAS 19 allows only one measurement method (projected unit credit method based on final salary);

• and finally, the redefinition of some actuarial assumptions

that are determined more precisely under IFRS – for example, discount rates must be determined by reference to market yields on high quality corporate bonds over a term consistent with that of the obligation measured.

In the 2004 French GAAP consolidated financial statements, Valeo applied Recommendation no. 2003-R.01 of the French

National Accounting Board (CNC) which recommends that from January 1, 2004, all obligations in respect of pensions and other employee benefits should be provided for using the same methods as prescribed under IAS 19. The impact of the first-time application of Recommendation no. 2003-R.01 (primarily the resetting to zero of previously unrecognized actuarial gains and losses) was recorded in opening equity net of deferred taxes, in accordance with the required treatment of changes in accounting method. Consequently, the French GAAP financial statements and the IFRS financial statements show the same amounts for (i) the net expense relating to pensions and other employee benefits arising in the year ended December 31, 2004, and (ii) the provision in the balance sheet at that date.

Valeo is applying the corridor method to post-employment benefits prospectively from January 1, 2004. Under this method, only the portion of new actuarial gains and losses arising after the transition date exceeding the greater of (i) 10% of the present value of the obligation or (ii) 10% of the fair value of plan assets at the balance sheet date is recognized and amortized over the average remaining working lives of the

employees. In the case of long-term benefits payable during employment, actuarial gains and losses are recognized in full at each balance sheet date. 3.4.2 – Development expenditure In accordance with French GAAP as applied by Valeo up to and including 2004, research and development expenditure was expensed as incurred. Under IAS 38, research costs are expensed as incurred, and development expenditure must be capitalized if the enterprise can demonstrate: • that it has the intention, and the technical and financial

resources to complete the development;

• that it is probable that the future economic benefits attributable to the development expenditure will flow to the enterprise;

• and that the cost of the intangible asset represented by the development expenditure can be measured reliably.

Based on these criteria, Valeo is now capitalizing development expenditure incurred between (i) the date of receipt of the nomination letter from the customer (which demonstrates that Valeo has been chosen as supplier for volume production, and hence the existence of a market) and (ii) the start of volume production. This development expenditure is then amortized over a maximum period of 4 years from the start of volume production. Customer contributions to Valeo’s development expenditure (which under French GAAP were recognized in the statement of income when billed) are taken to income on a straight line basis over a maximum of 4 years under IFRS, irrespective of the billing frequency. In accordance with IFRS 1, Valeo retrospectively capitalized development expenditure and deferred customer contributions

for all projects with a residual value other than zero at January 1, 2004. However, the average level of development expenditure capitalized and of customer contributions deferred was limited by the unavailability of some historical data for the period subject to retrospective restatement (1998 to 2003).

13

The impact on the 2004 financial statements of restating development expenditure breaks down as follows:

Impact on balance sheets at January 1 and December 31, 2004

( million)

January 1, 2004 December 31, 2004

Development expenditure on projects in volume production

• gross carrying amount 127 227

• amortization and provisions for impairment in value (50) (95)

• net carrying amount 77 132

Projects in development phase (1) 104 90

Total capitalized development expenditure (net carrying amount) 181 222

Deferral of customer contributions (30) (41)

Restatement of goodwill (2) (3) (5)

Total impact on equity 148 176

(1) Net carrying amount after any impairment in value (2) Corresponds to the carrying amount (at the transition date) of development expenditure acquired in a business combination but not capitalized under

French GAAP. In accordance with IFRS 1, these costs have been capitalized and goodwill adjusted accordingly.

Impact on the statement of income

( million)

2004

Total research and development expenditure – French GAAP (584)

Capitalization of development expenditure incurred in 2004 94

Amortization and impairment of capitalized expenditure (53)

Sub-total: development expenditure 41

Elimination of customer contributions received in 2004 (25)

Portion of deferred customer contribut ions released to income in 2004 13

Sub-total: customer contributions (12)

Total of “Development expenditure” restatement column (see note 3.2.1) 29

Impact of reclassification of deferred customer contributions to “Other operat ing revenues" (13)

Other restatements (1) 8

Other reclassifications (2) (43)

Total research and development expenditure – IFRS (603)

(1) Relates mainly to changes in consolidation methods (see note 3.4.4). (2) Relates mainly to sales of studies and prototypes (see note 3.5.2).

The positive effect on the 2004 IFRS statement of income arises because the amounts capitalized during the year exceed the amortization charged against the development expenditure capitalized in the balance sheet at January 1, 2004. This is due largely to partial unavailability of historical data, as described above. However, the improvement in net income is reduced by a symmetrical counter-effect from the deferral of customer contributions.

Assuming that development expenditure and customer contributions remain stable, this positive effect is likely to diminish in future years as the level of capitalized development expenditure in the balance sheet rises.

14

3.4.3 – Specific tooling Specific tooling is a complex issue, posing numerous practical difficulties, particularly concerning:

• identifying the owner (automaker or supplier);

• how the automaker’s contribution is billed:

- separate;

- included in the price of volume produced parts in the form of explicit amortization (either with or without a guarantee), or

- taken into account in the sales price without any

separation of the portion relating to specific tooling.

Valeo therefore carried out an economic analysis of contractual relations with automakers to determine which party has control over the future economic benefits and risks relating to specific tooling over its estimated useful life. Based on this analysis, Valeo defined two alternative accounting treatments for specific tooling that comply with IFRS:

• if Valeo has control over the future economic benefits and risks relating to specific tooling, the tooling is capitalized (in accordance with IAS 16) and amortized over a period not exceeding 4 years, with the automaker’s contribution deferred and released to income over the same period.

• if the automaker has control over the future economic benefits and risks, tooling is recorded as inventory (in accordance with IAS 2) until the sale of the tooling to the automaker is recognized. Any resulting loss on the tooling contract (corresponding to the difference between the automaker’s contribution and the cost of the tooling) is provided as soon as the loss is known

The impact of the specific tooling restatement breaks down as follows:

Impact on equity

( million)

January 1, 2004 December 31, 2004

Derecognition of tooling where risks and benefits have been transferred (19) (22)

Provision for losses on future sales of tooling (34) (30)

Total (53) (52)

3.4.4 – Consolidation methods Under French GAAP, Valeo used the full consolidation method for entities in which it held an equal share of voting rights, where the Group exercised de facto control over operational management of the entity. Under IAS 27, control is determined solely by reference to the contractual arrangements governing the running of the entity. This means that where joint control is legally established under a contractual arrangement, such entities will now be accounted for using the proportionate consolidation method. Under this method, the balance sheets and statements of income of jointly-controlled entities will now be included in the consolidated financial statements only in proportion to Valeo’s control in the entity concerned. This change in method results in:

• a reduction of 35 million in consolidated stockholders’ equity at January 1, 2004;

• a reduction of 199 million in net sales and of 25 million in operating income in 2004.

This restatement, which has the effect of eliminating minority interests in these entities, has no impact on net income.

3.4.5 – Currency translation Under IAS 21, goodwill arising on the acquisition of a foreign company must be treated as an asset of that company, and hence must be expressed in the functional currency of the acquired company. This treatment is the same as that currently applied by Valeo under French GAAP except in the case of sub-groups, where no goodwill allocation had been made at individual subsidiary level. This allocation has now been made, resulting in a reduction of 21 million in stockholders’ equity at January 1, 2004. Valeo has also changed the reporting currency for certain of its entities. This is necessary because under IAS 21, the reporting currency must be the same as the functional currency, defined as the currency of the economic environment in which the main cash inflows and outflows occur. The impact on stockholders’ equity at January 1, 2004 is 4 million.

15

3.4.6 – Impairment of assets Under French GAAP, Valeo amortized goodwill using the straight line method over a period determined on a case-by-case basis not exceeding twenty years. If indications of other-than-temporary impairment were identified, a review was conducted which could result in an exceptional write-down of goodwill. Under IFRS 3, it is no longer possible to amortize goodwill. Instead, impairment tests must be performed on a systematic basis in accordance with the revised IAS 36. Discontinuation of goodwill amortization had a favorable impact of 90 million on 2004 net income. Valeo subjected all its goodwill to systematic impairment tests using the discounted cash flow method. The discount rate used (based on the weighted average cost of capital) was 8.0% after tax for 2004. These tests resulted in the recognition of impairment losses of 18 million in the opening balance sheet and 15 million in 2004, representing around 1% of the net carrying amount of goodwill as reported in the French GAAP

balance sheets at December 31, 2003 and 2004 respectively. Impairment tests were also conducted for property, plant and equipment where there was an indication of impairment based on the operational split of Valeo into Cash Generating Units (CGUs) as defined in IAS 36. However, this exercise did not reveal any material impact ( 1 million on stockholders’ equity at January 1, 2004 and on net income for the year ended December 31, 2004). 3.4.7 – Business combinations Valeo acquired a controlling interest in Zexel on December 1, 2003. In the 2003 financial statements, Valeo provisionally determined the fair value of the assets and liabilities acquired. The final fair value determination carried out for the 2004 French GAAP financial statements (within the standard time period allowed under French GAAP) was also used in the IFRS opening balance sheet, so that a final valuation of goodwill would be used at the date of transition to IFRS rather than a provisional valuation. The impact on consolidated stockholders’ equity (including minority interests) at January 1, 2004 was 16 million. No goodwill was recognized on buyouts of minority interests in companies already under Valeo’s exclusive control, on the basis that these are treated as capital transactions. As a result, the difference between the acquisition cost of the shares and the share of net assets acquired was recognized in equity for all acquisitions during 2004 of additional interests in companies already accounted for by Valeo using the full consolidation method. This accounting treatment resulted in a reduction of

24 million in IFRS stockholders’ equity at December 31, 2004.

3.4.8 – Share-based payment

Valeo has granted its employees stock subscription options

and stock purchase options. Under French GAAP, no expense is recognized in connection with the granting of stock options. On exercise of stock subscription options, Valeo issues new shares via a capital increase. On exercise of stock purchase options, Valeo sells to the employees shares previously acquired by the Group. Only the gain or loss arising on the sale of these shares is recognized in the financial statements.

In 2004, Valeo implemented an international employee stock ownership program, which resulted in a capital increase of

33 million but had no impact on net income under French GAAP.

By contrast, IFRS 2, “Share-Based Payment”, requires that an expense be recognized equal to the fair value of the services rendered by the employees in return for the equity instruments granted to them.

In the case of stock subscription and stock purchase options,

this employee compensation expense (which Valeo measures at the grant date using the Black-Scholes-Merton model) is deferred and charged to income over the vesting period of the rights. Under the first-time adoption requirements set out in IFRS 1 in relation to IFRS 2, only plans granted after November 7, 2002 and not fully vested at January 1, 2005 are required to be restated. IFRS 2 has no impact on stockholders' equity at January 1 and December 31, 2004, because the contra entry for this employee compensation expense is an increase in consolidated reserves (retained earnings). For the year ended December 31, 2004, IFRS 2 gives rise to an expense of 5 million.

The employee stock ownership program, under which all the rights had vested at December 31 2004, does not require the recognition of an expense (in accordance with the transitional provisions of IFRS 2) where transactions with employees were settled by the issuance of shares. However, in the case of transactions settled in cash in the form of share appreciation rights (SARs) outstanding at January 1, 2005, an expense of

2 million has been recognized based on the fair value of the instrument as of December 31, 2004.

3.4.9 – Other adjustments This heading covers a number of divergences from Valeo’s previous accounting practices giving rise to restatements or reclassifications that are individually immaterial.

16

3.4.10 – Deferred taxes

This heading shows the tax impact of the IFRS restatements described above. The impact is immaterial, because the IFRS restatements relate mainly to countries where the amount of deferred tax assets recognized is already capped.

3.4.11 – Earnings per share

Under French GAAP, basic earnings per share was calculated by dividing net income for the year by the weighted average number of shares outstanding during the year. Diluted earnings per share was calculated by including instruments giving deferred access to Valeo’s capital (stock subscription options and convertible bonds), taking account of the probability of exercise or conversion in light of the market price (the average Valeo share price for the year). When funds are received on the exercise of these rights (such as on the subscription of shares), they are deemed to be allocated in priority to the purchase of shares at market price. This calculation method – know as the treasury stock method – serves to determine the “unpurchased” shares to be added to the shares of common stock outstanding for the purpose of computing the dilution. When funds are received at the date of issue of dilutive instruments (such as for convertible bonds), net income is adjusted for the net of tax interest savings which would result from the conversion of the bonds into shares. IAS 33 does not give rise to any significant divergences from the treatment currently used by Valeo. From January 1, 2005, the date of first application of IAS 32 (see note 5), treasury shares will however have to be deducted from the weighted

average number of shares outstanding used in the calculation of basic and diluted earnings per share.

3.5 – Description of IFRS reclassifications

3.5.1 – General presentation of the statement of income

Under IAS 1, the statement of income may be presented either by nature or by function. To retain the required level of clarity for assessing performance and to ensure comparability with the main players in the auto parts sector, Valeo has decided to continue presenting its statement of income by function, as it did under French GAAP.

However, the French GAAP item “Net financial expense” is now split into:

• “Cost of net debt”, representing interest expense on long-

term debt and short-term loans, less mainly financial income from the investment of surplus cash.

• “Other financial income and expense”, which includes:

- the effect of unwinding of discount on provisions (in

particular for pension obligations, see note 3.5.3);

- income statement impacts of non-current financial

assets (dividends, provisions for impairment, gains and losses on disposal);

- changes in fair value of financial instruments that

do not qualify for hedge accounting (see note 5.1.3);

- the ineffective portion of hedging relationships (see

note 5.1.3);

- realized foreign exchange gains and losses.

In addition, two lines included in the French GAAP statement of

income no longer appear in the IFRS format:

• other income/expense – net (see note 3.5.4);

• amortization of goodwill (see note 3.4.6).

3.5.2 – Operating revenues

In Valeo’s French GAAP financial statements, net sales consisted of revenues from sales of goods to third parties in the ordinary course of business (mainly sales of finished goods, plus tooling and prototypes). Other revenues generated in the ordinary course of business but not strictly qualifying as sales were usually netted against the relevant cost by function in the statement of income. For example, client contributions towards the cost of manufacturing tooling (ownership of which is retained by Valeo) or towards development costs were netted off the relevant expense item (respectively, cost of sales and research & development expenditure).

Under IFRS, netting of income and expense is disallowed except in some special cases (IAS 1). Valeo has therefore adopted the concept of “Total operating revenues”, in line with IAS 18. This concept is broader than that of net sales, because it includes not just sales of goods but also sales of services and various types of royalty and license income. The “Total operating revenues” line is sub-divided into two categories:

• net sales, which primarily includes sales of finished goods

and also includes all tooling revenues (with the related costs included in cost of sales);

• other operating revenues, consisting of all revenues for which the associated costs are recorded below the gross margin line. This mainly comprises sales of prototypes and contributions to development costs.

In light of this new revenue presentation, Valeo has reviewed the calculation of indicators and ratios to ensure consistency between the revenues and expenses taken into account:

• Gross margin is still defined as the difference between

net sales and cost of sales, and the gross margin ratio is still measured as a percentage of net sales.

• The ratios for operating income and net income (including and excluding minority interests) are now calculated as a percentage of the new “Total operating revenues” line.

17

The impact of the “Operating revenues” reclassification on the 2004 IFRS statement of income is shown in the table below (1) :

( million) Tooling Prototypes Other Total

Net sales 19 (33) 1 (13)

Other operating revenues - 42 7 49

Total operating revenues 19 9 8 36

Cost of sales (2) (19) 28 (1) 8

Research and development expenditure (2) - (37) (6) (43)

Administrative expenses - - (1) (1)

Operating income - - - -

(1) The impact of reclassifying customer contributions to development expenditure to “Other operating revenues” is dealt within the note on the

restatement of development expenditure (see note 3.4.2). (2) “Cost of sales” and “Research and development expenditure” are also affected by the following changes:

• prototype costs, usually recorded in “Cost of sales” previously, must now be reclassified to “Research and development expenditure”;

• some sales of prototypes, and the associated costs, were previously recorded in “Research and development expenditure”.

3.5.3 – Pensions and other employee benefits

In addition to the restatement arising from the recognition in full of its obligations in respect of pensions and other employee benefits (described in note 3.4.1), Valeo has reclassified part of

the expense related to these obligations.

This arises because the pension expense includes a financial component, comprising:

• an expense item, representing the annual unwinding of the discount on the provision for pension obligations;

• an income item, corresponding to the expected return on

plan assets held by third-party funds.

This net interest expense, amounting to 41 million, has been reclassified under “Other financial income and expense”. In the French GAAP financial statements, 25 million of this total was recorded at operating level on function-based expense lines (mainly cost of sales), and 16 million was recorded in “Other income/expense – net”.

3.5.4 – Other income and expenses

In the Group’s consolidated financial statements prepared

under French GAAP, “other income/expense – net” was shown separately from operating income. This item mainly included social and reorganization costs, impairment, as well as costs relating to significant lawsuits and other exceptional items.

Under IAS 1, such items are included in operating income, or financial income, where appropriate. Furthermore, separate disclosures are required for items deemed to be material.

Consequently, an amount of 148 million – previously recorded

under “Other income/expense – net” in the French GAAP financial statements – has been reclassified as follows:

• the interest expense of 16 million relating to discounted provisions for pension obligations under early retirement plans has been reclassified to “Other financial income and expense” (see note 3.5.3).

• items that are material to the Group, which under IAS 1 must be disclosed separately, are shown on a specific line, “Other income and expenses”, in operating income. The amount of 78 million reclassified to this line mainly comprises:

- social and restructuring costs on site closures or

major personnel downsizing programs;

- costs associated with significant litigation or risks.

• the remaining 54 million recorded in “Other

income/expense – net” in the French GAAP financial statements has been allocated to the relevant function–based expense lines (primarily cost of sales).

3.5.5 – General presentation of the balance sheet

First-time adoption of IFRS does not give rise to any major

divergences in balance sheet presentation compared with Valeo’s previous practice.

Minority interests were already included as a component of

stockholders’ equity, as required by IAS 1 and IAS 27.

In addition, the distinction between current and non-current items required under IAS 1 is broadly consistent with the split of assets (fixed/current) and liabilities (long-term/current) used in the French GAAP financial statements.

18

3.5.6 – Income taxes

In the French GAAP financial statements, income taxes payable and recoverable were classified in “Other liabilities” or “Other current assets”, depending on the position of each tax entity. The long-term and short-term portions of deferred tax assets and liabilities were shown separately.

Under IFRS, income taxes payable and recoverable must be shown on separate lines, in current liabilities and current assets respectively. This has resulted in reclassifications of 86 million (liabilities) and 59 million (assets) in the balance sheet at December 31, 2004. In addition, deferred taxes (whether long-term or short-term) must be shown on a separate line in non-current assets and liabilities, in compliance with IAS 12.

3.5.7 – Financial assets

The “Investments in companies carried at cost” and “Loans and other assets” lines have been reclassified to a new line, “Non-current financial assets”.

The “Current financial assets” and “Current financial liabilities” lines include the fair value of derivative instruments used by Valeo (see note 5). No value is recorded in the balance sheet at December 31, 2004 for such instruments, because IAS 39 (on financial instruments) is being applied by Valeo from January 1, 2005.

3.5.8 – Business combinations Valeo has elected for the option offered by IFRS 1 (first-time adoption) not to retrospectively restate business combinations carried out prior to the date of first-time adoption.

Consequently, the net carrying amount of goodwill derived from

the French GAAP financial statements has been frozen as at January 1, 2004, and reclassified as follows:

• under IAS 28, goodwill relating to companies accounted

for by the equity method is now shown in “Investments in companies at equity” ( 33 million at December 31, 2004).

• goodwill netted against share premium in the case of

acquisitions partially financed by a share issue has been reclassified to “Retained earnings”. The amount involved is 853 million.

3.6 – Main impacts of IFRS restatements on the statement of cash flows

Most of the restatements arising from first-time adoption of IFRS have no impact on the change in net cash and cash equivalents. Only two restatements were identified as having a material effect on net cash and cash equivalents:

• the change in consolidation method in accordance with IAS 27 (see note 3.4.4), which reduced net cash and cash equivalents by 28 million at December 31, 2004;

• the offset of treasury stock (recorded in “Marketable

securities” under French GAAP) against stockholders’ equity in accordance with IAS 32, which reduced net cash and cash equivalents by 32 million at January 1, 2005.

In presentational terms, the statement of cash flows required under IAS 7 is fairly close to that already used by Valeo under

French GAAP. Consequently, there is unlikely to be any major change in the presentation of the consolidated statement of cash flows, other than the line-by-line impact of the change in consolidation method described above.

19

4 – RECONCILIATION OF QUARTERLY FIGURES AT MARCH 31, 2004 ( mill ion) March 2004

French GAAP IFRS

restatements IFRS

reclassifications Total IFRS

impact March 2004

IFRS

NET SALES 2,415 (49) (4) (53) 2,362

Other operating revenues (1) - 4 13 17 17

TOTAL OPERATING REVENUES 2,415 (45) 9 (36) 2,379

Cost of sales (1,986) 36 (4) 32 (1,954)

GROSS MARGIN (2) 429 (13) (8) (21) 408

% of net sales 17.8% 17.3%

Research & development expenditure (154) 14 (12) 2 (152)

Selling expenses (49) - - - (49)

Administrative expenses (115) (1) - (1) (116)

Other income and expenses (1) - 2 (22) (20) (20)

OPERATING INCOME 111 6 (29) (23) 88

% of total operating revenues 4.6% 3.7%

Net financial expense (3) 4 - (4) (4) -

Cost of net debt (1) - - (9) (9) (9)

Other financial income and expenses (1) - (3) (6) (9) (9)

Other income/expenses – net (3) (39) - 39 39 -

INCOME BEFORE INCOME TAXES 76 3 (9) (6) 70

Income taxes 27 - 9 9 36

NET INCOME FROM CONSOLIDATED COMPANIES 103 3 - 3 106

Equity in net earnings of associated companies 2 (1) - (1) 1

Amortization of goodwill (3) (22) 22 - 22 -

NET INCOME BEFORE MINORITY INTERESTS 83 24 - 24 107

% of total operating revenues 3.4% 4.5%

Minority interests (9) 7 - 7 (2)

NET INCOME 74 31 - 31 105

% of total operating revenues 3.1% 4.4%

(1) New line in the IFRS statement of income

(2) Gross Margin is the difference between Net Sales and Cost of sales, and does not include Other operating revenues (3) Line no longer included in the IFRS statement of income

20

Details of restatements to the quarterly figures

( mill ion) Impairment of assets

Development expenditure

Consolidation methods

Share-based payment

Specific tooling

Deferred taxes

Other restatements

Total IFRS Restatements

NET SALES - - (50) - 1 - - (49)

Other operating revenues (1) - 3 - - - - 1 4

TOTAL OPERATING REVENUES - 3 (50) - 1 - 1 (45)

Cost of sales - - 39 - - - (3) 36

GROSS MARGIN (2) - - (11) - 1 - (3) (13)

Research & development expenditure - 12 2 - 1 - (1) 14

Selling expenses - - - - - - - -

Administrative expenses - - 2 (1) - - (2) (1)

Other income and expenses (1) - - - - - - 2 2

OPERATING INCOME 15 (7) (1) 2 (3) 6

Net financial expense (3) - - - - - - - -

Cost of net debt (1) - - - - - - - -

Other financial income and expense (1) - - - - - - (3) (3)

Other income/expenses – net (3) - - - - - - - -

INCOME BEFORE INCOME TAXES - 15 (7) (1) 2 (6) 3

Income taxes - - - - - - - -

NET INCOME FROM CONSOLIDATED

COMPANIES - 15 (7) (1) 2 - (6) 3

Equity in net earnings of associated companies

- - (1) - - - - (1)

Amortization of goodwill (3) 22 - - - - - - 22

NET INCOME BEFORE MINORITY INTERESTS

22 15 (8) (1) 2 - (6) 24

Minority interests - - 8 - - (1) - 7

NET INCOME 22 15 - (1) 2 (1) (6) 31

(1) New line in the IFRS statement of income

(2) Gross Margin is the difference between Net Sales and Cost of sales, and does not include Other operating revenues (3) Line no longer included in the IFRS statement of income

21

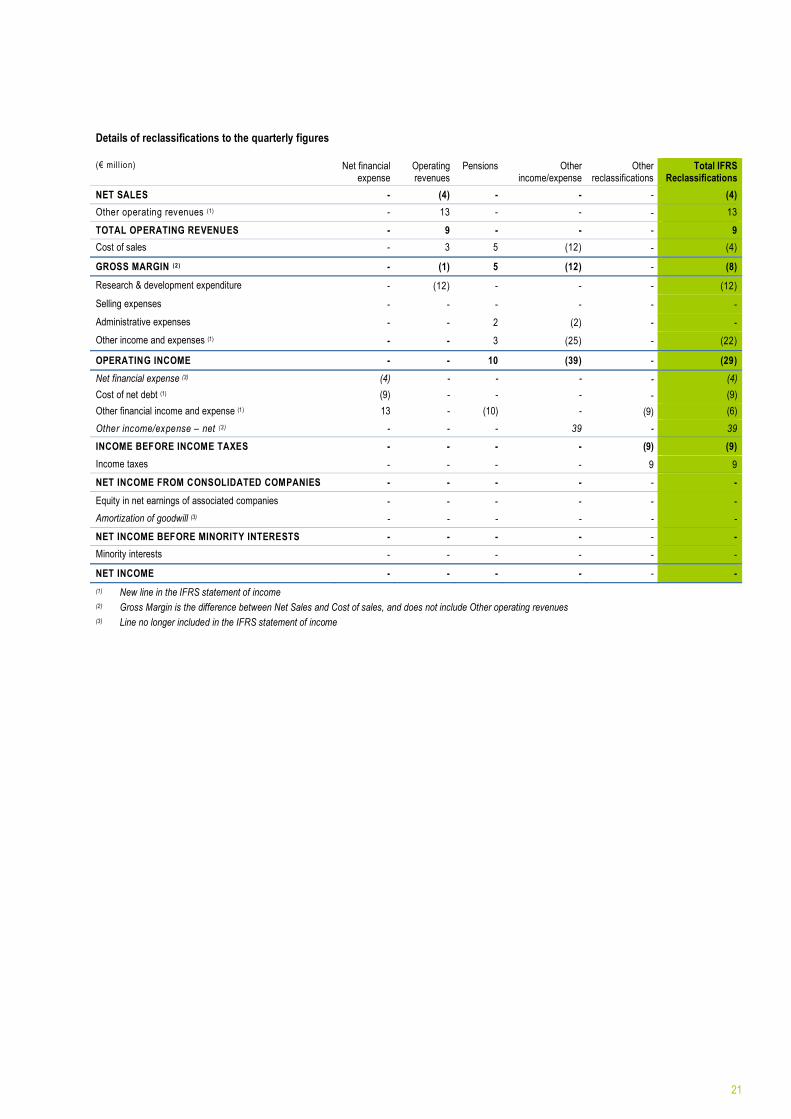

Details of reclassifications to the quarterly figures ( mill ion) Net financial

expense Operating revenues

Pensions Other income/expense

Other reclassifications

Total IFRS Reclassifications

NET SALES - (4) - - - (4)

Other operating revenues (1) - 13 - - - 13

TOTAL OPERATING REVENUES - 9 - - - 9

Cost of sales - 3 5 (12) - (4)

GROSS MARGIN (2) - (1) 5 (12) - (8)

Research & development expenditure - (12) - - - (12)

Selling expenses - - - - - -

Administrative expenses - - 2 (2) - -

Other income and expenses (1) - - 3 (25) - (22)

OPERATING INCOME - - 10 (39) - (29)

Net financial expense (3) (4) - - - - (4)

Cost of net debt (1) (9) - - - - (9)

Other financial income and expense (1) 13 - (10) - (9) (6)

Other income/expense – net (3) - - - 39 - 39

INCOME BEFORE INCOME TAXES - - - - (9) (9)

Income taxes - - - - 9 9

NET INCOME FROM CONSOLIDATED COMPANIES - - - - - -

Equity in net earnings of associated companies - - - - - -

Amortization of goodwill (3) - - - - - -

NET INCOME BEFORE MINORITY INTERESTS - - - - - -

Minority interests - - - - - -

NET INCOME - - - - - -

(1) New line in the IFRS statement of income

(2) Gross Margin is the difference between Net Sales and Cost of sales, and does not include Other operating revenues

(3) Line no longer included in the IFRS statement of income

22

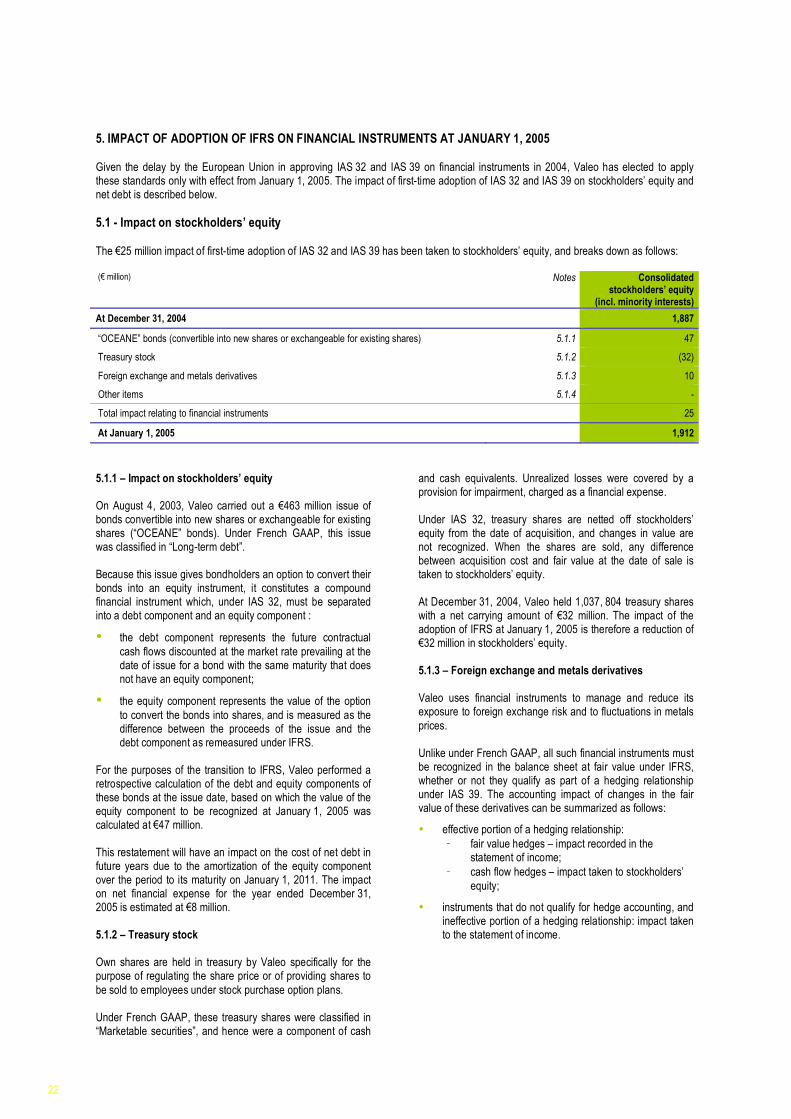

5. IMPACT OF ADOPTION OF IFRS ON FINANCIAL INSTRUMENTS AT JANUARY 1, 2005 Given the delay by the European Union in approving IAS 32 and IAS 39 on financial instruments in 2004, Valeo has elected to apply these standards only with effect from January 1, 2005. The impact of first-time adoption of IAS 32 and IAS 39 on stockholders’ equity and net debt is described below.

5.1 - Impact on stockholders’ equity The 25 million impact of first-time adoption of IAS 32 and IAS 39 has been taken to stockholders’ equity, and breaks down as follows: ( million) Notes Consolidated

stockholders’ equity (incl. minority interests)

At December 31, 2004 1,887

“OCEANE” bonds (convertible into new shares or exchangeable for existing shares) 5.1.1 47

Treasury stock 5.1.2 (32)

Foreign exchange and metals derivatives 5.1.3 10

Other items 5.1.4 -

Total impact relating to financial instruments 25

At January 1, 2005 1,912

5.1.1 – Impact on stockholders’ equity On August 4, 2003, Valeo carried out a 463 million issue of bonds convertible into new shares or exchangeable for existing shares (“OCEANE” bonds). Under French GAAP, this issue was classified in “Long-term debt”. Because this issue gives bondholders an option to convert their bonds into an equity instrument, it constitutes a compound financial instrument which, under IAS 32, must be separated into a debt component and an equity component :

• the debt component represents the future contractual

cash flows discounted at the market rate prevailing at the date of issue for a bond with the same maturity that does not have an equity component;

• the equity component represents the value of the option

to convert the bonds into shares, and is measured as the difference between the proceeds of the issue and the debt component as remeasured under IFRS.

For the purposes of the transition to IFRS, Valeo performed a retrospective calculation of the debt and equity components of these bonds at the issue date, based on which the value of the equity component to be recognized at January 1, 2005 was calculated at 47 million. This restatement will have an impact on the cost of net debt in future years due to the amortization of the equity component over the period to its maturity on January 1, 2011. The impact on net financial expense for the year ended December 31, 2005 is estimated at 8 million. 5.1.2 – Treasury stock Own shares are held in treasury by Valeo specifically for the purpose of regulating the share price or of providing shares to

be sold to employees under stock purchase option plans. Under French GAAP, these treasury shares were classified in “Marketable securities”, and hence were a component of cash

and cash equivalents. Unrealized losses were covered by a provision for impairment, charged as a financial expense. Under IAS 32, treasury shares are netted off stockholders’ equity from the date of acquisition, and changes in value are not recognized. When the shares are sold, any difference between acquisition cost and fair value at the date of sale is taken to stockholders’ equity. At December 31, 2004, Valeo held 1,037, 804 treasury shares with a net carrying amount of 32 million. The impact of the adoption of IFRS at January 1, 2005 is therefore a reduction of

32 million in stockholders’ equity. 5.1.3 – Foreign exchange and metals derivatives Valeo uses financial instruments to manage and reduce its exposure to foreign exchange risk and to fluctuations in metals

prices. Unlike under French GAAP, all such financial instruments must be recognized in the balance sheet at fair value under IFRS, whether or not they qualify as part of a hedging relationship under IAS 39. The accounting impact of changes in the fair value of these derivatives can be summarized as follows:

• effective portion of a hedging relationship:

- fair value hedges – impact recorded in the statement of income;

- cash flow hedges – impact taken to stockholders’

equity;

• instruments that do not qualify for hedge accounting, and ineffective portion of a hedging relationship: impact taken to the statement of income.

23

Foreign exchange At January 1, 2005, all Valeo’s foreign exchange instruments are measured at market value and recognized in the balance sheet date. From that date, changes in the value of these derivatives is usually recognized in net financial income and expense, and is offset by any changes in the value of the underlying liabilities or receivables. In the case of material cash flow hedges, Valeo applies hedge accounting. This involves taking changes in the value of the effective portion of the derivative to stockholders’ equity, and then recognizing these changes in value in operating income when the hedged item impacts operating income. Metals Valeo hedges its future purchases of basic metals (aluminium, secondary smelted aluminium, copper, zinc, tin). In the balance sheet at January 1, 2005, all metal derivatives are recognized at fair value. Changes in the fair value of these derivatives are

initially taken to stockholders’ equity, with only the ineffective portion taken to the statement of income. The effective portion of the hedge is then reclassified to operating income when the hedged position impacts net income.

5.1.4 - Other items Long-term debt includes a 500 million bond issue, which in 2004 was hedged in full by floating-rate swaps. The swaps are recognized in the opening balance sheet at January 1, 2005. Valeo applies fair value accounting: the bond issue hedged by these swaps is remeasured at the fair value attributable solely to interest rate movements. These changes in fair value are recognized in financial income/expense for the period, and are canceled out by matching movements in the effective portion of the interest rate swaps. Up to and including December 31, 2004, assets and liabilities expressed in foreign currencies could be translated at the hedged rate allocated to them. In the opening balance sheet, all foreign-currency assets and liabilities are translated using the closing rate at December 31, 2004. The corresponding impact is a reduction of 2 million in opening stockholders' equity. Lastly, the derivative instrument used to hedge cash outlays

relating to SARs (see note 3.4.8) was recognized in stockholders’ equity for an amount of 2 million.

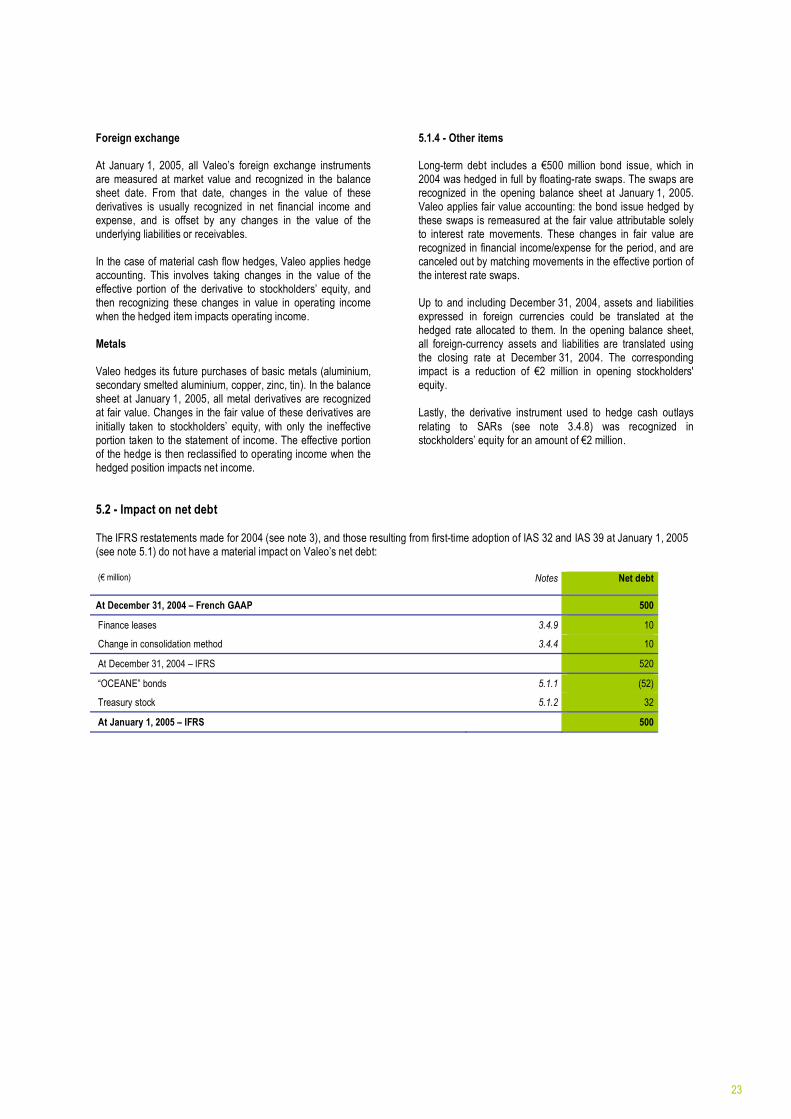

5.2 - Impact on net debt

The IFRS restatements made for 2004 (see note 3), and those resulting from first-time adoption of IAS 32 and IAS 39 at January 1, 2005 (see note 5.1) do not have a material impact on Valeo’s net debt: ( million) Notes Net debt

At December 31, 2004 – French GAAP 500

Finance leases 3.4.9 10

Change in consolidation method 3.4.4 10

At December 31, 2004 – IFRS 520

“OCEANE” bonds 5.1.1 (52)

Treasury stock 5.1.2 32

At January 1, 2005 – IFRS 500

24

6 - STATUTORY AUDITORS’ SPECIAL REPORT ON THE 2004 CONSOLIDATED FINANCIAL STATEMENTS RESTATED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS)

This is a free translation into English of the Statutory Auditors’ special report issued in the French language and is provided solely for the convenience of

English speaking readers. This report should be read in conjunction with, and construed in accordance with, French law and professional auditing standards applicable in France.

To the Board of Directors,

Further to the request made to us as Statutory Auditors, we have conducted an audit of the consolidated balance sheet and statement of income of Valeo and certain explanatory notes thereto, restated in accordance with International Financial Reporting Standards (IFRS) as adopted within the European Union, for the year ended December 31, 2004 (the “restated consolidated financial statements”), as presented in sections 2 and 3 of the note entitled “Transition to IFRS”.

The restated consolidated financial statements are the responsibility of the Board of Directors and have been prepared as part of the conversion to International Financial Reporting Standards as adopted within the European Union for the preparation of 2005 consolidated financial statements, based on the balance sheet and statement of income included in the consolidated financial statements for the year ended December 31, 2004 prepared in accordance with the accounting rules and principles generally accepted in France (the “consolidated financial statements”). We have audited the consolidated financial statements in accordance with the professional standards applied in France and expressed an unqualified opinion thereon. Our responsibility is to express an opinion on the restated consolidated financial statements based on our audit.

We conducted our audit in accordance with the professional standards applied in France. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the restated consolidated financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the restated consolidated financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the restated consolidated financial statements have been prepared, in all material respects, in accordance with the basis set out in the notes, which specify how IFRS 1 and the other international accounting standards adopted within the European Union have been applied and indicate which standards, interpretations, rules and accountings methods should in the opinion of management apply to the preparation of consolidated financial statements for 2005 in accordance with IFRS as adopted within the European Union.

Without qualifying our opinion set out above, we draw your attention to the fact that note 2 describes why the comparative information presented in the final IFRS consolidated financial statements for 2005 may differ from the information presented in the accompanying restated consolidated financial statements to reflect possible changes to IFRS and the approval of such changes by the European Union.

Moreover, as part of the conversion to International Financial Reporting Standards adopted within the European Union for the preparation of consolidated financial statements for 2005, we draw your attention to the fact that the restated consolidated financial statements do not include comparative information for 2003, a cash flow statement or all of the disclosures required by IFRS as adopted within the European Union, which would be necessary there-under to give a true and fair view of the assets and liabilities, financial position and results of operations of the consolidated group of companies.

Paris, April 25, 2005

The Statutory Auditors

PricewaterhouseCoopers Audit Salustro Reydel

Serve Villepelet Jean-Christophe Georghiou Jean-Pierre Crouzet Emmanuel Paret